doc 9161-manual on air navigation services economics english

DESCRIPTION

Doc 9161-Manual on Air Navigation Services Economics EnglishTRANSCRIPT

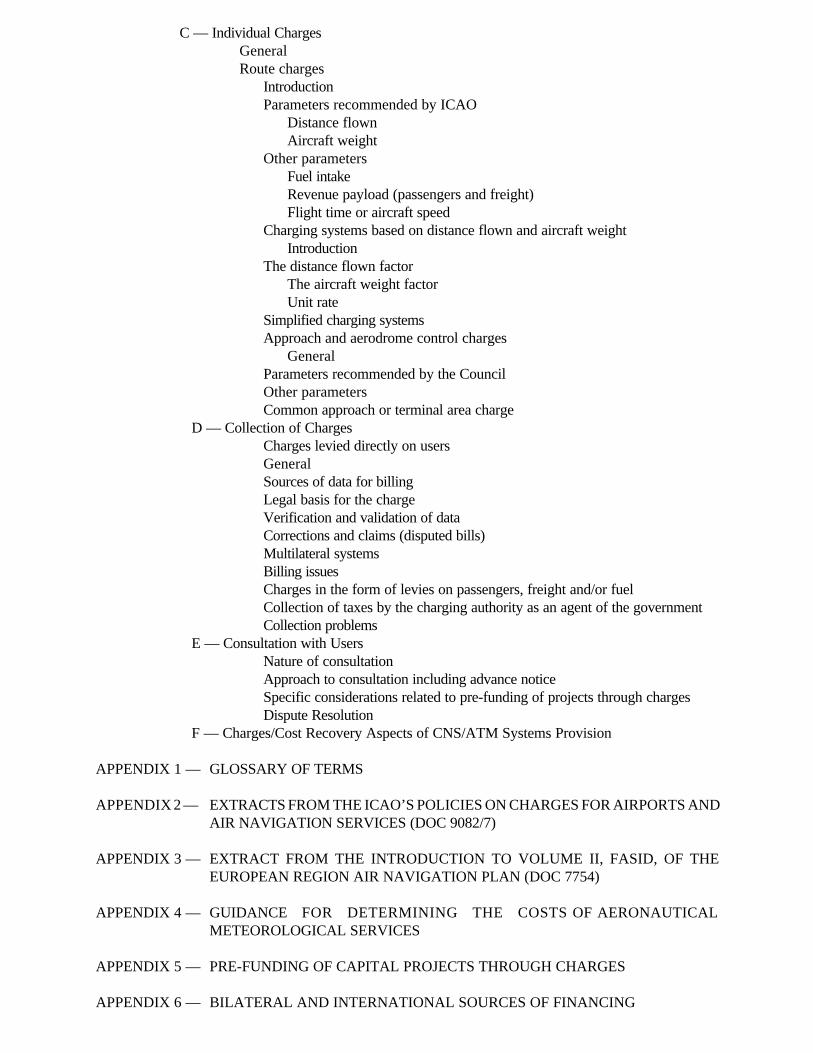

TABLE OF CONTENTS

CHAPTER 1 — ICAO POLICY ON AIR NAVIGATION SERVICES CHARGES

A — Article 15 of the Convention on International Civil AviationB — ICAO’s Policies on Charges for Air Navigation ServicesC — Assembly ResolutionsD — ICAO’s Policy on Environmental Charges

CHAPTER 2 — ORGANIZATIONAL STRUCTURES AT THE NATIONAL LEVEL

A — General CommentsB — Basic Organizational Characteristics of Air Navigation Services ProvisionC — Organizational Forms

General commentsOrganizational formsA government departmentThe autonomous public sector organizationThe private sector organizationTransitional arrangementsOver-all comments

D — Economic Oversight of Air Navigation Services ProvisionContracting States’ responsibilitiesThe need for economic oversightPossible forms of economic oversightPublic statement of desired outcomesThird party advisory commissionContracts between providers and usersArbitration/Dispute resolutionEconomic regulation/Regulatory agencyInstitutional arrangements - checks and balances

Mandatory consultation/Information disclosureStakeholder membership of the Board of DirectorsJoint ownership

Selecting appropriate forms of oversightImplementation - dispute resolution

CHAPTER 3 — INTERNATIONAL COOPERATION

A — IntroductionB — International Operating Agencies

Scope and functionsAgence pour la Sécurité de la Navigation Aérienne en Afrique et à Madagascar(ASECNA)

Methods of financingAdvantagesEstablishing the agency

Corporación Centroamericana De Servicios De Navegación Aérea (COCESNA)Methods of financing

Organizational arrangementsEuropean Organization for the Safety of Air Navigation (EUROCONTROL)

Methods of financingCollection of air navigation charges

C — Joint Charges Collection AgenciesScope and functionsFinancing aspectsImportance of States controlling collection of their chargesOptions for StatesCurrency aspects

D — Multinational Facilities and ServicesBackground developmentsDefinition and examplesEquity aspectsImplications for States and ICAO technical planning bodiesGuidance material developedAgreementBasic provisionsStatus of guidelines

E — Joint Financing ArrangementsGeneralThe Danish and Icelandic Joint Financing Agreements

Basic aspectsEstimates of the costs of providing the servicesUser chargesAssessments on contracting governmentsPayments to the provider StatesSupervision of the services

Other applications of the joint financing conceptPossible application of the joint financing concept to CNS/ATM systemimplementation

F — Political CooperationGeneralReorganization of the airspaceCommon European certification of air navigation services providersInteroperability of the ATM networkCommon charging schemeCommon air traffic controller license

G — Specific Organizational Aspects Pertaining to CNS/ATM SystemsBackgroundCommunication satellite services — implementation and option selectionGNSSAir traffic management

CHAPTER 4 — FINANCIAL MANAGEMENT

A — Basic AspectsGeneralApplication of principles of best commercial practicesPurposes of accounting and financial controlScope of accounting and financial controlThe business plan and budget

GeneralThe business planThe budgetFinancing and cash managementInternal and external auditing

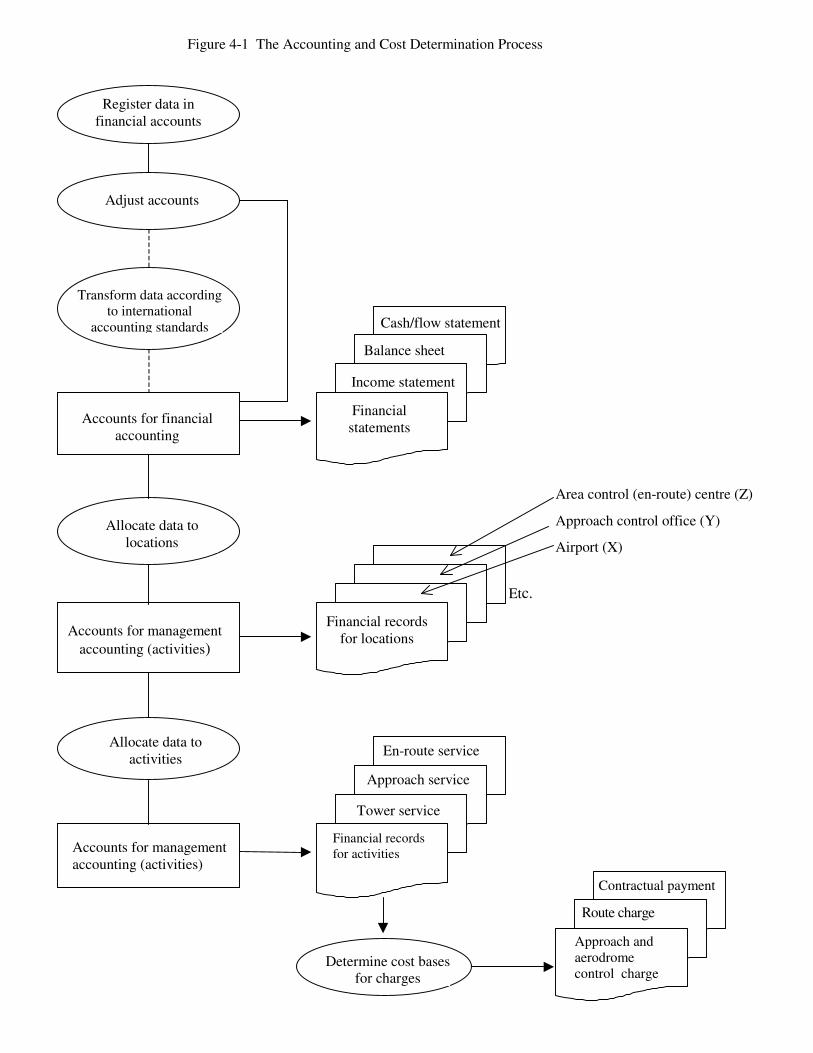

B — AccountingGeneralFinancial statementsRevenues

Air traffic operationsPortion collected for other providers of air navigation servicesRevenues from ancillary activitiesBank and cash management revenuesGrants and subsidies

ExpensesGeneralAccounting by category of expense

Staff expensesOther operating expensesDepreciationInterestExtraordinary/abnormal expenses

Expenses by activity and locationCost allocation by functional locationOther aspects of expense accountingMonitoring financial performance

CapitalEquityWorking capitalCapital employedCash Flow

Accounting of pre-funding of projects through charges

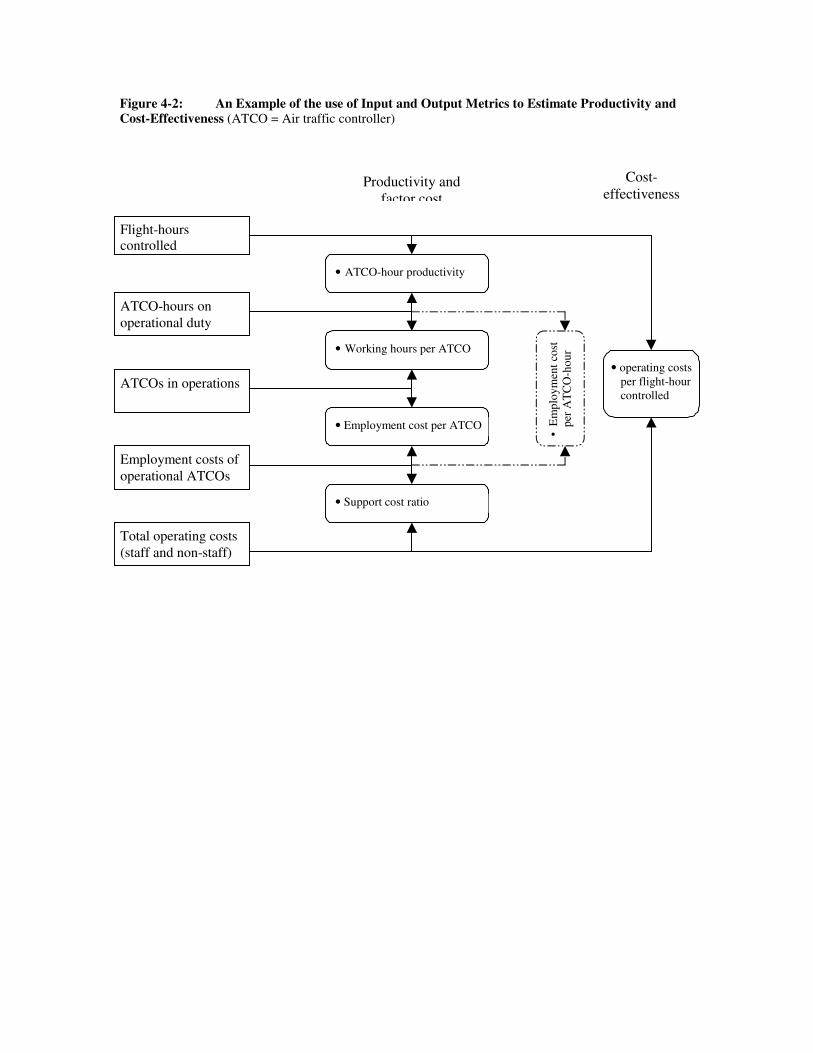

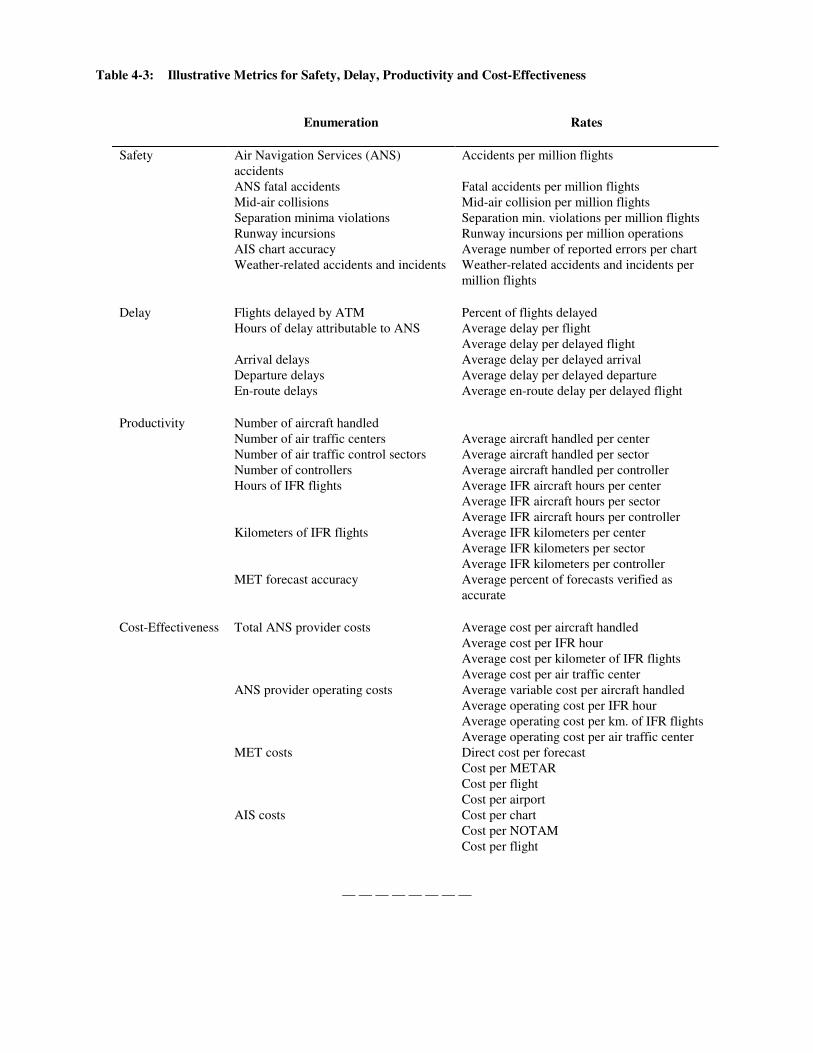

C — Means of Measuring Performance and ProductivityIntroductionPerformance managementConsultation and selecting goalsMeasurement methodSetting targetsPlanning to achieve the goalsAssessing performance metricsAreas of measurement/data sources/methodsInputOutputOutcomesSafetyDelayProductivity and cost-effectiveness Flight efficiencyAvailabilityApplying ResultsInternal assessment toolBenchmarkingIdentification of best practices and performance driversForecastingInvestment analysisConsultation with usersPrepare performance reports for management and public informationRecommended practices

CHAPTER 5 — FINANCING AIR NAVIGATION SERVICES INFRASTRUCTURE

A — Traffic ForecastsB — Use of ExpertsC — Economic and Financial Analyses

Financial evaluationCost/benefit analysisBusiness case Economic impact analysis

D — The Financing PlanPurpose and contents of a financing planCurrency requirementsCosts typically payable in domestic currencyCosts typically payable (wholly or partially) in foreign currencyRepayment of loans

E — Sources of FinancingDomestic sourcesForeign sourcesBilateral institutionsDevelopment banks and fundsUnited Nations Development ProgrammeCommercial sourcesDebt financingCredit Rating Pre-funding of projects through air navigation services chargesOther Sources

F — Special Financing Aspects of CNS/ATM Systems Implementation

CHAPTER 6 — COST BASIS FOR CHARGES

A — Inventorying the Facilities and ServicesAir traffic management (ATM)Communications, navigation and surveillance (CNS)Meteorological services for air navigation (MET)Search and rescue (SAR)Aeronautical information services (AIS)

B — Determining CostsIntroductionDifference between costs recorded in the accounts of an entity providing airnavigation services and costs applied for determining the cost basis for chargesOther operating expensesDepreciation and/or amortization and cost of capitalDepreciation and/or amortizationCost of capitalImplications of organizational structureCosts of individual facilities and services

C — Allocation of CostsIntroductionService descriptions for cost allocation purposesNon-aeronautical utilizationAllocation where facilities serve both airport and en-route requirementsAllocation of total costs to service locationsAllocation of en-route costs between flight information regionsAllocation of en-route costs among categories of users

IntroductionCategories of services and usersParameters for cost allocation to user categories

Number of flightsDistance flownTime in the systemAircraft weight

Allocation of approach and aerodrome control costs among categories of usersD — Cost Basis for Individual Charges

Basic aspectsCost basis for route chargesCost basis for approach and aerodrome control charges or basis for contractualpayments for approach and aerodrome control — by airportSecurity measures for air navigation services

E — Special Costing Considerations Pertaining to CNS/ATM SystemsDetermining CNS/ATM systems costsCost recovery during development and implementationAllocation of CNS/ATM systems costs

CHAPTER 7 — AIR NAVIGATION SERVICES CHARGES AND THEIR COLLECTION

A — Basic FactorsB — Application of Economic Pricing Principles

The scope of use of economic pricingEvaluation of the application of economic pricing in a cost recovery systemTransparency and consultationIssues related to monopoly power and cost recovery

C — Individual ChargesGeneralRoute charges

IntroductionParameters recommended by ICAO

Distance flownAircraft weight

Other parametersFuel intakeRevenue payload (passengers and freight)Flight time or aircraft speed

Charging systems based on distance flown and aircraft weightIntroduction

The distance flown factorThe aircraft weight factorUnit rate

Simplified charging systemsApproach and aerodrome control charges

GeneralParameters recommended by the CouncilOther parametersCommon approach or terminal area charge

D — Collection of ChargesCharges levied directly on usersGeneralSources of data for billingLegal basis for the chargeVerification and validation of dataCorrections and claims (disputed bills)Multilateral systemsBilling issuesCharges in the form of levies on passengers, freight and/or fuelCollection of taxes by the charging authority as an agent of the governmentCollection problems

E — Consultation with UsersNature of consultationApproach to consultation including advance noticeSpecific considerations related to pre-funding of projects through chargesDispute Resolution

F — Charges/Cost Recovery Aspects of CNS/ATM Systems Provision

APPENDIX 1 — GLOSSARY OF TERMS

APPENDIX 2 — EXTRACTS FROM THE ICAO’S POLICIES ON CHARGES FOR AIRPORTS ANDAIR NAVIGATION SERVICES (DOC 9082/7)

APPENDIX 3 — EXTRACT FROM THE INTRODUCTION TO VOLUME II, FASID, OF THEEUROPEAN REGION AIR NAVIGATION PLAN (DOC 7754)

APPENDIX 4 — GUIDANCE FOR DETERMINING THE COSTS OF AERONAUTICALMETEOROLOGICAL SERVICES

APPENDIX 5 — PRE-FUNDING OF CAPITAL PROJECTS THROUGH CHARGES

APPENDIX 6 — BILATERAL AND INTERNATIONAL SOURCES OF FINANCING

CHAPTER 1 ICAO POLICY ON AIR NAVIGATION SERVICES CHARGES

Divided in four parts, this Chapter focuses on ICAO’s policy on air navigation services charges and provides the framework for the guidance material contained in this Manual. Part A addresses the basic policy principles expressed in Article 15 of the Convention on International Civil Aviation (Doc 7300). Part B focuses on the additional policy guidance provided in ICAO’s Policies on Charges for Airports and Air Navigation Services (Doc 9082); it explains how the policy was developed and highlights some principles of particular interest. Part C presents the third element in the policy-making process related to air navigation services charges, Assembly Resolutions. Finally, Part D shows the current ICAO policy with regard to the use of charges for environmental protection.

A — ARTICLE 15 OF THE CONVENTION ON INTERNATIONAL CIVIL AVIATION 1.1 The basic policy established by ICAO in the area of airport and air navigation services charges is expressed in Article 15 of the Convention on International Civil Aviation, usually referred to as the Chicago Convention, as follows:

Airport and similar charges Every airport in a contracting State which is open to public use by its national aircraft shall likewise, subject to the provisions of Article 68, be open under uniform conditions to the aircraft of all the other contracting States. The like uniform conditions shall apply to the use, by aircraft of every contracting State, of all air navigation facilities, including radio and meteorological services, which may be provided for public use for the safety and expedition of air navigation. Any charges that may be imposed or permitted to be imposed by a contracting State for the use of such airports and air navigation facilities by the aircraft of any other contracting State shall not be higher,

(a) As to aircraft not engaged in scheduled international air services, than those that would be paid by its national aircraft of the same class engaged in similar operations, and

(b) As to aircraft engaged in scheduled international air services, than those that would be paid by

its national aircraft engaged in similar international air services. All such charges shall be published and communicated to the International Civil Aviation Organization: provided that, upon representation by an interested contracting State, the charges imposed for the use of airports and other facilities shall be subject to review by the Council, which shall report and make recommendations thereon for the consideration of the State or States concerned. No fees, dues or other charges shall be imposed by any contracting State in respect solely of the right of transit over or entry into or exit from its territory of any aircraft of a contracting State or persons or property thereon.

1.2 In summary, Article 15 sets out the following three basic principles:

a) uniform conditions shall apply to the use of airports and air navigation services in a Contracting State by aircraft of all other Contracting States;

b) the charges imposed by a Contracting State for the use of such airports or air navigation services shall not be higher for aircraft of other Contracting States than those paid by its national aircraft engaged in similar international operations; and

c) no charge shall be imposed by any Contracting State solely for the right of transit over or entry into or exit

from its territory of any aircraft of a Contracting State or persons or property thereon. While the first two of these principles do not appear to have given rise to misunderstandings, the third has in some instances been interpreted to mean that no charges are to be levied when an aircraft flies into, out of or over a State. That, however, is not the intent of this principle since all States are fully within their rights to recover the costs of the services they provide to aircraft operators through charges. The substance of this principle is in fact that a State should not charge solely for granting an authorization for a flight into, out of or over its territory. 1.3 Two other aspects are also addressed in Article 15. The first is that States are obliged to publish all their airport and air navigation services charges, and also communicate them to ICAO. This information is collected and published by ICAO in the Tariffs for Airports and Air Navigation Services (Doc 7100). 1.4 Article 15 also provides for ICAO, upon representation by an interested Contracting State, to review charges imposed and make recommendations thereon to the State or States concerned. It should be observed that the Article specifically refers to representation by an interested Contracting State, not by an aircraft operator. 1.5 As to the status of the principles in Article 15 and, for that matter, all the articles of the Chicago Convention, an ICAO Contracting State cannot exempt itself from applying any of the principles expressed therein since by signing the Chicago Convention the signatory State binds itself to adhere to all its Articles without exception. B — ICAO’S POLICIES ON CHARGES FOR AIR NAVIGATION SERVICES 1.6 Additional and more detailed policy guidance is provided in ICAO’s Policies on Charges for Airports and Air Navigation Services (Doc 9082), hereafter referred to as ICAO’s Policies on Charges. These are revised periodically by the Council following major international conferences on airport and air navigation services economics, although most of the basic philosophy and principles have remained unchanged over the years. An introduction section of Doc 9082 addresses some issues which are common to airports and air navigation services: scope and proliferation of charges, organizational and managerial issues and other factors affecting the economic situation of airports and air navigation services. The section concerning air navigation services charges is together with the introduction the focus for the description in this Part.1 1.7 The ICAO’s Policies on Charges differ in status from the Chicago Convention in that an ICAO Contracting State is not legally bound to adhere thereto, unlike the Articles of the Chicago Convention. However, since the principles in ICAO’s policies, including those on charges, are based on recommendations by major international conferences, States are morally committed to follow them and to ensure that their cost recovery practices conform thereto. 1.8 In the Introduction section of ICAO’s Policies on Charges concern is expressed over the proliferation of charges on air traffic and it is recommended that States (i) permit the imposition of charges only for services and functions which are provided for, directly related to, or ultimately beneficial for civil aviation operations, and (ii) refrain from imposing charges which discriminate against international civil aviation in relation to other modes of international transport (paragraphs 8 and 9 of Doc 9082/7).

�The highlighting of certain principles in ICAO’s Policies on Charges should not be interpreted as if these principles

would be more important than the other principles in Doc 9082��

1.9 It is also recommended that, where this is in the best interests of providers and users, States consider establishing autonomous entities to operate their airports and air navigation services since the experience worldwide indicates that where airports and air navigation services have been operated by autonomous entities their overall financial situation and managerial efficiency have generally tended to improve (paragraphs 10 and 11). However, it is noted that with the rapidly growing autonomy in the provision and operation of airports and air navigation services, many States may wish to establish an independent mechanism for the economic regulation of airports and air navigation services to oversee their economic, commercial and financial practices (paragraph 15). Furthermore, it is recommended

that States apply best commercial practices for airports and air navigation services in order to promote transparency, efficiency and cost-effectiveness in the provision of an appropriate quality of services and facilities (paragraph 17). 1.10 An important consideration of the ICAO’s Policies on Charges is that there should be a balance between the respective interests of airports and providers of air navigation services on one hand and of air carriers on the other, in view of the importance of the air transport system to States and its influence in fostering economic, cultural and social interchanges between States. This applies particularly during periods of economic difficulty. It is therefore recommended that States encourage increased cooperation between airports and providers of air navigation services and air carriers to ensure that economic difficulties facing them all are shared in a reasonable manner (paragraph 20). 1.11 The principles contained in Section III - ICAO’s Policies on Charges for Air Navigation Services - of Doc 9082/7 address such subjects as the cost basis for air navigation services charges, allocation of costs among aeronautical users, charging systems, pre-funding of projects, currency issues, approach and aerodrome control charges, route charges, charges for services used by aircraft when not over the provider State and consultation with users . 1.12 Among the basic principles included in the ICAO’s Policies on Charges concerning the cost basis for air navigation services charges are the following: that where air navigation services are provided for international use, the providers may require the users to pay their share of the related costs, but international civil aviation should not be asked to meet costs which are not properly allocable to it (paragraph 36); and that the cost to be shared is the full cost of providing the air navigation services, including appropriate amounts for cost of capital and depreciation of assets as well as the costs of maintenance, operation, management and administration (paragraph 38 (i)). 1.13 Other principles and recommendations of particular relevance in the context of the cost basis for air navigation services charges, charging systems and the collection of charges are:

a) that States are encouraged to maintain accounts for the air navigation services they provide in a manner which ensures that air navigation services charges levied on international civil aviation are properly cost-based (paragraph 36); also, that for the purpose of consultation users should be provided with transparent and adequate financial, operational and other information (paragraph 49 (ii));

b) that air navigation services may produce sufficient revenues to exceed all direct and indirect operating

costs and so provide for a reasonable return on assets (before tax and cost of capital) to contribute towards necessary capital improvements (paragraph 38 (iv));

c) that the allocation of air navigation services costs among aeronautical users should be carried out in a

manner equitable to all users, and the proportions of cost attributable to international civil aviation and other utilization of the facilities and services (including domestic civil aviation, State or other exempted aircraft, and non-aeronautical users) should be determined in such a way as to ensure that no users are burdened with costs not properly allocable to them according to sound accounting principles (paragraph 40);

d) that any charging systems should, so far as possible, be simple, equitable and, with regard to route air

navigation services charges, suitable for general application at least on a regional basis, and the administrative cost of collecting charges should not exceed a reasonable proportion of the charges collected (paragraph 41 (i));

e) that the charges should not be imposed in such a way as to discourage the use of facilities and services

necessary for safety or the introduction of new aids and techniques (paragraph 41 (ii));

f) that charges should be determined on the basis of sound accounting principles and may reflect, as required, other economic principles, provided that these are in conformity with Article 15 of the Convention on International Civil Aviation and other principles in the present Policies (paragraph 41 (iii)); and

g) that the providers of air navigation services for international use may require all users to pay their share

of the costs of providing them regardless of whether or not the utilization takes place over the territory of the provider State (paragraph 47).

1.14 Also of interest is that pre-funding of projects through air navigation services charges may be accepted in specific circumstances where this is the most appropriate means of financing long-term, large-scale investment, provided that strict safeguards are in place (paragraph 42). 1.15 The ICAO’s Policies on Charges accentuates the importance of consultation with users of air navigation services before changes in charging systems or levels of charges are introduced. The purpose of consultation is to ensure that the provider gives sufficient information to users relating to the proposed change and gives proper consideration to the views of users and the effect the charges will have on them. Users or their representative organizations should also be consulted before the finalization of plans for new or expanded air navigation services. Equally, users, particularly air carriers, should provide advance planning data to the extent possible on a 5- to 10-year forecast basis. In this context, and with regard to charges in particular, the need for a neutral party at the local level to preempt and resolve disputes before they enter the international arena (a “first resort” mechanism) is recognized (paragraphs 49 to 51). 1.16 A noteworthy aspect of the ICAO’s Policies on Charges with reference to search and rescue service is the limitation to any permanent civil establishment of equipment and personnel when determining the total costs of air navigation services (Appendix 2). 1.17 No specific reference is made in the ICAO’s Policies on Charges to particular cost recovery principles for CNS/ATM systems as all basic ICAO charging principles for air navigation services apply to the implementation of CNS/ATM systems. However, special considerations are required with respect to organizational, managerial and co-operative aspects, as well as financing, costing and cost recovery mechanisms. C — ASSEMBLY RESOLUTIONS 1.18 ICAO’s policies in the air transport field are expressed in consolidated Assembly Resolutions which are updated at each ordinary session of the Assembly. These Resolutions address policy matters in all sectors of the Air Transport Programme, through dedicated appendices. The latest Assembly Resolution in force is A35-18 — Consolidated statement of continuing ICAO policies in the air transport field, where Appendix F relates to airports and air navigation services. This Appendix urges Contracting States to ensure that Article 15 of the Chicago Convention is fully respected and reminds the States that they alone remain responsible for the commitments they have assumed under Article 28 of the Convention, regardless of the organizational structure under which airports and air navigation services are operated. 1.19 ICAO’s policy related to environmental levies is expressed in Assembly Resolution A35-5 — Consolidated statement of continuing ICAO policies and practices related to environmental protection, where Appendix I relates to the use of Market-based measures regarding aircraft engine emissions.

D — ICAO’S POLICY ON ENVIRONMENTAL CHARGES 1.20 A policy on the use of market-based measures regarding aircraft engine emissions for the purpose of environmental protection is contained in Assembly Resolution A35-5, Appendices H and I (also referred to in paragraph 1.19 above). This policy is of an interim nature while ICAO, through its Committee on Aviation Environmental Protection (CAEP), completes developing appropriate guidance on the use of market-based measures2 to limit or reduce aircraft engine emissions.”

— — — — — — —

2Market-based measures that are studied by CAEP are voluntary measures, a mechanism under which industry and governments agree to a target and/or a set of actions to reduce emissions, emission-related levies, and emissions trading, a system whereby the total amount of emissions �ould be capped and allowances in the form of permits to�emit

could be bought and sold to meet emission reduction objectives��

CHAPTER 2 ORGANIZATIONAL STRUCTURES AT THE NATIONAL LEVEL

This Chapter addresses various aspects of organizational structures of air navigation services at the national level. Part A provides some general comments essential for the understanding of the guidance in this Chapter. Part B describes basic organizational characteristics of air navigation services provision. Part C addresses three basic organizational forms for service provision. Part D deals with economic oversight and regulation.

A. GENERAL COMMENTS 2.1 Considering the diverse circumstances involved it is not the intent in this Manual to recommend one organizational form over another, but rather to provide guidance to States by describing relevant aspects of each form. The decisions made by individual States as to the organizational form under which their air navigation services should operate will depend on the situation in the State concerned and will often be strongly influenced by government policy. Regardless of the organizational form under which air navigation services are provided, according to Article 28 of the Chicago Convention, it is the State that is ultimately responsible for the provision and operation of air navigation facilities and services. In the ICAO’s Policies on Charges in Doc 9082 it is emphasized with regard to private involvement that States, when considering the commercialization or privatization of airports and providers of air navigation services, bear in mind that the State is ultimately responsible for safety, security, and, in view of the generally monopolistic nature of airports and air navigation services, economic oversight of their operations (paragraph 13 of Doc 9082/7). In addition, States making decisions regarding adoption of autonomous or private organization forms for air navigation services are cautioned to consider the potential impact of reductions in revenue that could occur due to decreases in aviation activity caused by business cycles, and to secure the continuity of their operations through contingency planning. In this Chapter reference is frequently made to a “State” as being the entity providing the air navigation services or participating in various related international or multinational activities. In many instances, though, these services are not provided by the State itself but by a separate autonomous entity to which the State has delegated that function. B. BASIC ORGANIZATIONAL CHARACTERISTICS OF AIR NAVIGATION SERVICES PROVISION 2.2 Air navigation services and airports are two of the three major components (the third being aircraft operations), which form the air transport system. The basic characteristics of air navigation services operations differ fundamentally from those of airport operations in several respects. Firstly, unlike airports, air navigation facilities and services provided by a State extend over the whole territory of the State concerned or even beyond, and are frequently also dependent on facilities and services provided in other States. Secondly, air navigation services have national defense and external relations implications with respect to the sovereignty of States’ airspace. Furthermore, in most States all or most of the air navigation services are not provided by a single entity. Instead, several entities may be involved although only a few are major service providers. Another major difference is the limited potential for revenues from non-aeronautical activities to contribute to the financial situation of air navigation services. While revenues from non-aeronautical activities for airports around the world on the average is one third of total revenues, or even

higher, according to ICAO studies the average is around three per cent for providers of air navigation services. 2.3 Air navigation services have traditionally been classified into the following five major categories: air traffic services (ATS); telecommunications service (COM), which in turn is basically classified into aeronautical fixed service (AFS), aeronautical mobile service (AMS), and aeronautical radio navigation service; meteorological services for air navigation (MET); search and rescue services (SAR) and aeronautical information services (AIS). With the implementation of CNS/ATM systems the ATS and COM categories will be replaced by components that are broader in scope i.e. air traffic management (ATM) and communications, navigation and surveillance (CNS). All five major categories will be defined and described in greater detail in Chapter 6 — Cost basis for charges, Part A — Inventorying the facilities and services. 2.4 As to the provision of services within the individual categories ATS (and ATM eventually) is often provided by the civil aviation administration, although in a growing number of States autonomous entities, also referred to as operating agencies, have been assigned this function. In such instances the same entity may also be responsible for providing certain communications, navigation and surveillance services, for example, AFS, AMS and radio navigation service. 2.5 MET is usually provided by a separate meteorological entity which in many States reports to another branch of government than do the civil aviation administration or the telecommunication services branch. While aeronautical SAR activities are often co-ordinated by the civil aviation administration, in most States the aircraft, vehicles, vessels and personnel utilized in the actual SAR operations are provided by the military, civil defense or other similar forces. AIS on the other hand tends to be provided by the civil aviation administration. 2.6 The implications of these organizational aspects with regard to cost recovery are addressed in subsequent chapters. From an organizational viewpoint, however, it is important that where air navigation services costs are to be recovered, the State concerned should assign to one entity the duty for ensuring that the costs attributable to the provision of air navigation services by the different entities in the State all be included in the cost basis for any cost recovery programme or mechanism. The absence of such an approach has had the effect of, for example, MET costs not having been taken into account at all in some instances, thereby resulting in the States concerned not even partially recovering these costs. Also of importance is that the costs attributable to the provision of air navigation services must have been accurately and properly determined, and that transparency be maintained in financial presentations. 2.7 As to the selection of the entity that would collate the costs of the different air navigation services providers, the entity providing ATS does, apart from providing a major air navigation service, also possess the information required to identify the flights to be charged. It would therefore in most circumstances be best for that entity or branch of government to be assigned the collating function. With that would go the responsibility of ensuring that the revenue from charges be shared among the different entities providing air navigation services. Such sharing of revenue among the different entities concerned would normally be in proportion to the costs incurred by each in providing air navigation services. In the large majority of States this co-ordinating function would in light of the above best be assigned to the civil aviation administration. C. ORGANIZATIONAL FORMS General comments 2.8 The principal objective for all providers of air navigation services is to plan and operate safe and efficient services in the airspace for which the State is responsible. These services should be provided in the most effective and efficient manner possible and be focused on the needs of the users. While a State is ultimately responsible for their provision, it is recognized that they can be delegated to a specific body to

provide them on behalf of the State concerned. These bodies can cover a wide range of forms at the national level from a government department, autonomous public sector agency, through corporatization to full privatization. Alternatively, the provision of these services could be delegated to a multinational entity, as described in Chapter 3. 2.9 The decisions made by individual States as to the organizational form at the national level under which their air navigation services should operate will depend on the situation in the State concerned, the organization of airspace and whether provision is delegated to other States. These decisions will often be strongly influenced by government policy but each State may need to have regard to the following factors:

a) the over-all framework of government and system of administration followed by the State;

b) the legal and administrative arrangements to ensure that the State's responsibilities to uphold the relevant articles of the Chicago Convention are maintained;

c) forecast industry activity and the sources and cost of funds required to meet related

infrastructure investment needs. The options for financing capital investment will include:

1) government finance;

2) equity finance;

3) debt finance; and

4) leasing. The choice of financing option may have a bearing on the organizational form. For example, should public sector bodies not have access to private finance markets because of public sector borrowing restrictions, access may only become possible with a change of organizational form;

d) the requirement of the aviation industry, both international and domestic, to promote increased efficiency of their operations by the safe and efficient provision of air navigation services; and

e) the importance of civil aviation to the State's economic and social objectives and the extent to

which civil aviation has been developed to meet those needs. Organizational forms 2.10 There are three basic or core forms of organization for providing air navigation services at the national level. These are as follows:

a) a government department that is subject to government accounting and treasury rules, its staff are employed under civil service pay and conditions;

b) the autonomous public sector organization that is separate from an executive arm of

government but the government has total ownership of the organization; and

c) the private sector organization that is owned by private interests either totally or with the government holding a minority share.

A government department 2.11 Key features of this organization are:

a) the head of the organization reports directly to the executive level of government;

b) as an organization within government it is funded by the government, sometimes from general taxation. User charges levied for air navigation services could be retained either by the government for general purposes or by the organization; and

c) the organization may not be subject to taxes as paid by private business.

2.12 Other factors that may be relevant are:

a) the organization provides all types of air navigation services and may also provide related services such as search and rescue co-ordination. It would normally be responsible for the safety regulation of the aviation industry;

b) if the government accounting system is inadequate to provide the necessary accounting

information, as specified in Chapter 4, separate accounts following commercial accounting standards and practices will be necessary;

c) capital expenditure is subject to the government’s approval process and treasury rules, and

might compete with other claims for government funds; and

d) the organization would normally not have a formal agreement regarding the provision of services to military aircraft.

The autonomous public sector organization 2.13 This type of organization would normally have the following key features set out below:

a) the government, as owner of the organization, is responsible for setting the organization's objectives and monitoring its performance;

b) a Board of Directors oversees the activities of the organization. It is appointed by the

government to whom the board reports;

c) the organization is self-financing and may be required to achieve a financial return on capital employed;

d) the organization charges for its services and uses revenue from these charges to fund operating

expenses and to finance capital expenditure. Some prescribed operations (e.g. military or services to remote localities) may be exempted from charges and the cost may be borne by government;

e) the organization applies commercial accounting standards and practices; and

f) the organization may be subject to normal business taxes.

2.14 This model encompasses a range of organizations depending on the extent to which the organization is meant to behave like a private sector company. The following additional factors may be relevant:

a) public sector bodies operating closely along private sector lines could still be subject to government directions or pressure to take account of wider public issues;

b) the organization may be responsible for the safety regulation of its services and in some cases for

aviation safety in general;

c) the staff of the organization are not likely to be civil servants and may therefore not have public sector pay and conditions of service;

d) the government would normally provide finance capital for the organization by direct loan, loan

guarantee or leasing arrangements. The organization may also have access to the private capital market, although because of its public sector status, government may limit access; and

e) the organization may be subject to the government's approval process for major capital

investment. The private sector organization 2.15 Setting up a private sector organization will require consideration of a number of factors. Air navigation services are generally provided by a monopoly and consequently a number of safeguards would need to be implemented to protect users against overcharging and to ensure that obligations are met such as freedom of access, non-discrimination between categories of users and conformity with international agreements and obligations. It is noted that establishing a private air navigation services entity should not in any way diminish the State’s requirement to fulfill its international obligations, notably those contained in the Chicago Convention and its Annexes, and the State’s moral obligation to respect ICAO’s Policies on Charges in Doc 9082. In setting up a regulatory framework to oversee the private entity, these safeguards should be protected, as appropriate. 2.16 Key features of a wholly private sector organization are likely to include the following:

a) the organization is subject to the obligations of States under the Chicago Convention;

b) there is a Board of Directors for the organization appointed according to its charter;

c) the organization is self-financing, charges for its services, obtains funds from the capital market and needs to achieve a financial return;

d) the organization applies commercial accounting standards and practices; and

e) the organization is subject to normal business taxes.

2.17 Other factors that may be relevant are:

a) the organization’s financial structure must be sufficiently robust to enable it to meet its financial obligations;

b) the organization is required to comply with aviation safety regulation standards set by the

responsible government body;

c) where there is no competition in the provision of air navigation services, charges for these services would need to be subject to independent economic regulation;

d) the organization charges for its services and uses revenue from these charges to fund operating expenses and to finance capital expenditure. Some prescribed operations (e.g. military or services to remote localities) may be exempted from charges and the costs for these prescribed services may be borne by government;

e) arrangements for the co-ordination of civil/military traffic, including common use of facilities

and services, and associated financial issues, would need to be formalized and agreed with the ministers concerned; and

f) the government represents the State at the international level. Any involvement by the private

sector organization in that representation would need to be decided by the parties concerned. Transitional arrangements 2.18 The general direction of change is likely to be from a government department towards autonomous organizational forms. Before an autonomous organization can become operational its charter, or a document of a similar nature, needs to be formulated. The charter should describe the scope of the services that the organization will be responsible for providing and operating. A change of organizational form should be made in consultation with all the parties concerned. 2.19 The process of transition will depend on the circumstances and practice of each State but, in general, the transitional issues that may arise when moving from a government department are:

a) establishment of formal relationships between the Government and the autonomous organization, including financial reporting requirements;

b) establishment of formal relationships between the autonomous organization and the aviation

safety regulation and accident investigation organizations;

c) establishment of economic regulatory framework;

d) identification, valuation and transfer of assets;

e) initial financial structure;

f) conditions of employment including pension arrangements;

g) staffing including maintaining good labour relations during the transition period; and

h) consultation with users and other interested parties. Over-all comments 2.20 The above forms of organization are not mutually exclusive and a State may draw on features from one or more of them. Whichever form is chosen, an organization providing air navigation services should adhere to the ICAO’s Policies on Charges in Doc 9082 and the guidance provided in the following chapters of this Manual and should provide information on their properly calculated costs for consultation with users.

D. ECONOMIC OVERSIGHT OF AIR NAVIGATION SERVICES PROVISION Contracting States’ responsibilities 2.21 As discussed earlier, Contracting States are responsible under the Chicago Convention for securing the provision of air navigation services on a non-discriminatory basis within their national airspace. Key to this is the provision of safe air navigation services in accordance with the Standards and Recommended Practices (SARPs) contained in the Annexes to the Convention. While Contracting States may delegate the provision of air navigation services to public or private entities, for example through the grant of a licence with appropriate conditions, they may not delegate their basic responsibility to secure the provision of safe air navigation services. The need for economic oversight 2.22 In addition to proper and effective safety regulation, there may be a need for appropriate economic oversight of an air navigation services provider’s operations in order to compensate for the lack of competition and to avoid monopoly abuse. However, the nature, scope and extent to which such oversight may be required will depend on the specific circumstances in a State, or group of States if air navigation services are provided on a supra-national basis. Competition in the provision of air navigation services is beginning to evolve (see paragraph 2.23). The degree to which effective competition is feasible as well as the ownership structure of an air navigation services entity may influence the extent to which economic oversight is needed. Effective competition, or the realistic prospect of it, provides the best guarantee of users’ needs being properly met, for example in terms of price and quality of service and through the increased pressures for efficiency and effective investment which help underpin these. Similarly, an entity’s ownership and governance structure may be an important factor. For example, if in the extreme an entity was owned and controlled collectively by its users, this could substantially mitigate any concerns with respect to the potential for abuse of monopoly power. 2.23 While the scope for competition in the provision of air navigation services is currently limited, and direct competition between different air navigation services providers within the same airspace is not a practical possibility, there are nevertheless aspects of operations of providers where more limited competition “for” the market is an option which could be considered. For example, there are already many instances where the provision of aerodrome control services is subject to periodic competitive tendering. Moreover, regional cooperation in the provision of air navigation services may lead to the establishment of a certification/designation mechanism where all air navigation services providers will have to be certified against common requirements. Where these certificates are mutually recognized through an entire region, States will be free to designate any entity with a valid certificate to provide air navigation services in a specific part of their airspace. 2.24 However, where competition remains absent and air navigation services continue to be provided by a statutory or natural monopoly not subject to direct or even realistic indirect competition, there is likely to be a need for appropriate economic oversight. Paragraph 15 of the ICAO’s Policies on Charges (Doc 9082/7) sets out a number of possible objectives reflecting areas of potential need for appropriate economic oversight. These areas of potential need, which apply only where competition is absent or insufficiently strong to provide users with adequate protection, may be summarised as follows:

a) the need to protect users against overcharging or other potentially anti-competitive practices where they constitute abuse of a dominant position;

b) the need for transparency with respect to an air navigation services provider’s financial and other

data required to enable users properly to assess the basis for charging proposals;

c) the need to protect users against undue discrimination in the application of charges;

d) the need to address efficiency in the provision of air navigation services;

e) the need to address the adequacy and consistency of service standards and quality;

f) the need to encourage appropriate and efficient investment;

g) the need for effective consultation with users so as to ensure that their views are taken properly into account; and

h) the need for a dispute resolution mechanism.

Possible forms of economic oversight

2.25 The framework for economic oversight that governments might put in place in order to protect users from potential monopoly abuse, while ensuring that the costs of such oversight are kept to the necessary minimum, could take different forms depending, for example, on whether it would be applied to public or private entities and the degree of market power of those entities.

Public statement of desired outcomes 2.26 The State in establishing the public or private autonomous air navigation services provider could, as a part of the establishment arrangement, indicate that direct regulation would be initiated (Fallback Regulation) if the provider does not ensure that its behaviour stays within “acceptable” bounds. The objective is to achieve the benefits of regulation, in terms of mitigating the worst characteristics of monopoly, without incurring the costs and distortions caused by such regulation. Normally, this would be accompanied by the application of standard competition law. For this approach to work the provider must have an understanding of what constitutes unacceptable behaviour. A difficulty might be that by defining the commercial boundaries in detail there might be a risk of creating precisely the regulatory distortions that it seeks to avoid.

Third party advisory commission

2.27 This more traditional approach to guard against monopoly abuse is often considered more appropriate when stakeholders do not form cohesive groups and thus have little or no means by which to organise for class action. A third party advisory commission could be composed of airlines, general aviation users, the military and other stakeholders to engage in meaningful dialogue with the management of the air navigation services provider on an ongoing basis and to review specific pricing, investment and service proposals. Contracts between providers and users 2.28 Rather than directly regulate an air navigation services provider the State could require the provider to negotiate a service contract with users. The objective of the responsible State would be to assure that users would be able to influence the nature, quality and cost of service. If a contract is successfully negotiated, it could eliminate or reduce the need for direct State oversight. Arbitration/Dispute resolution 2.29 If either the State defines acceptable standard of behaviour, such as suggested in paragraph 2.26, or if there is a contract between an air navigation services provider and users, arbitration or a dispute resolution mechanism could come into play where the provider and the users were unable to agree about their

application in practice. It might be necessary to specify some form of “triggers” for initiating arbitration and probably also criteria for settling disputes. The main advantage of such arbitration is that it would focus the pressure on the parties to reach and adhere to commercial agreements and in doing so would help to reinforce any underlying countervailing market power which the airlines may possess. However, its success is likely to depend, inter alia, on the degree of an air navigation services provider’s monopoly power, particularly if it was the only “regulatory” mechanism available. Economic regulation/Regulatory agency 2.30 The most common forms of economic regulation are cost of service, or rate of return regulation, and the use of predetermined caps on prices over longer periods. 2.31 Rate of return regulation is designed principally to address the issue of excessive profits under monopoly. The air navigation services provider may be required to obtain approval for investments and service charges rates. The objective would be to limit the rate of return of the provider on necessary investments. In its simple form at least, it allows cost pass through for both operating and capital expenditure. Its impact on assuring either greater cost efficiency or appropriate and efficient investment in new capacity or improved quality is uncertain. Rate of return is often characterised as risking over-investment through “gold plating”. In order to compensate for this, it risks intrusion without providing clear incentives to improve performance or efficiency. 2.32 Longer term price caps may create incentives for cost efficiency. If a longer term price cap is set, for example over five years, a commercial entity has a strong incentive to reduce its costs and keep the resulting higher profits for the remainder of the period. The revealed cost efficiencies then feed through into lower prices for users at the next review. 2.33 However, the price cap approach can be uncertain in its effects on capital investment. It suffers from the problem that fixed price caps may be set for several years on the basis of projected capital expenditure as well as on existing assets. This can create an incentive to overstate capital expenditure prior to the price cap being set, and subsequently not to undertake the full programme since the price cap can give the provider a short term return on the assets without actually having to invest in them. The fundamental problem here results from a failure to establish a clear and comprehensive definition of outputs and their pricing, which allows the regulated entity to argue that the lower than planned expenditure was the result of (desirable) efficiency gains. 2.34 Output based price caps may mitigate this problem. Prices set instead in relation to output performance may provide better incentives to invest efficiently. The price can be varied up or down based on meeting performance specifications. If price caps can be linked closely to outputs over time, the air navigation services provider will have fewer incentives to delay or not undertake productive investments.

Institutional arrangements - checks and balances

Mandatory consultation/Information disclosure

2.35 Airlines, the principal users of the services provided, are often substantial international companies. Thus, timely access to appropriate information on, for example, an air navigation services provider's operating and capital costs, their proposed investment programmes, and the traffic forecasts and proposed quality/service standards which underpin these, can provide an important aspect of the institutional checks and balances helping to bring about fair, reasonable and efficient prices and levels of service. Where air navigation services are provided by private or mixed private/public entities, consultation and information disclosure could be mandated and enforced through conditions in a licence granted to the air navigation services provider.

Stakeholder membership of the Board of Directors 2.36 This can help to promote transparency and accountability between an air navigation services providers and the users.

Joint ownership

2.37 An ownership structure that includes aircraft operators and the resulting extension of board membership could be used as a means of securing information flow, consultation and consensus in the establishment of rates and charges. Selecting appropriate forms of oversight 2.38 When deciding whether economic oversight going beyond normal competition law is necessary and, if so, what form would be most appropriate, States should first consider the scope for competition and thus the extent of any potential for abuse of monopoly power and, second, the potential cost of alternative oversight mechanisms. Where competition or the prospect of it is sufficiently strong, economic oversight beyond competition law may be unnecessary. 2.39 Another important factor in assessing the most appropriate approach is the ownership and governance structure of the air navigation services provider and the more general institutional and legal framework within which economic oversight, the provider and users operate. Generally speaking, the greater the extent to which an air navigation services entity is owned and controlled by its users, the less obvious is the need for specific external economic oversight arrangements to protect those users. However, ownership by a subset of users can, depending on the specific circumstances, raise concerns in terms of increased potential for discriminatory behaviour against other users. 2.40 The institutional framework within which economic oversight takes place can be key to its success in addressing monopoly power and in providing air navigation services entities with incentives to operate efficiently and to invest in a manner that best secures the outputs, in terms of capacity and service quality, required by users. It is important to consider carefully the roles, rights and responsibilities of the different parties involved - government, air navigation services provider, users and, where they exist, regulatory agencies. 2.41 If, taking account of local circumstances, a State wished to establish an economic regulatory agency rather than simply relying on general competition law, it would be important that an appropriate balance be established between independence and accountability for the regulatory agency as well as for the air navigation services provider which it would regulate. In order to hold the regulatory agency accountable, government would need to give it clear objectives, preferably through statute, coupled with sufficient operating autonomy. 2.42 Whatever model is adopted, it is desirable to ensure that the arrangements for economic oversight are designed so as to minimise unnecessary restrictions on the air navigation services provider and the users. Improved consultation based on effective information disclosure should be a basic requirement of most of the approaches identified above in order to maximise the prospects for responsiveness of the provider to user preferences, not only in the short term but also in the medium and long term.

Implementation - dispute resolution 2.43 The involvement of autonomous entities in the provision of air navigation services has brought about business practices and new market forces that can potentially result in new and different kinds of disputes

that need to be resolved before they enter the international arena. Economic oversight should provide for equitable, transparent, expeditious and effective dispute settlement mechanisms that build confidence between the provider of air navigation services and its users. Its purpose is to instil trust between parties where market forces do not provide for resolution of disputes. 2.44 No single mechanism could meet all needs and circumstances. In general, the procedures for settling a dispute between parties to an agreement may be carried out in two stages: a) consultations between the parties; and/or b) the dispute is submitted for a decision to an arbitration tribunal at the request of either party. Decisions reached under this latter stage of the mechanism are usually binding and both parties have the obligation to enforce the decision. 2.45 In addition to administrative and judicial proceedings, a State may consider a “first resort” mechanism. Such a “first resort” mechanism concept could provide for an intermediate level between the two stages of consultation and arbitration. This intermediate level calls for either an independent mediator or an independent dispute settlement panel to be used for the fact finding investigation, including the determination of the substance of the dispute, or for providing a recommendation to remedy the dispute. It is based on clear time frames, implementation arrangements, interim measures and provision for third party involvement. 2.46 An independent tribunal could be established where users could appeal if they had reason to believe they were being subject to abuse of monopoly powers or other unfair practices. This body could also handle appeals lodged with respect to complaints about non-compliance with the required principles for establishing fees. The mechanism should not affect the right of the parties to have access to other dispute resolution mechanisms, including those under general competition laws. Nor does it preclude the implementation of the formal arbitration process in an agreement. 2.47 Third-party protection could also be ensured through the use of a less costly mechanism, such as, for example, an ombudsman office. Note should be taken, however, that while the role of an ombudsman is to provide a neutral forum, he ultimately has no enforcement power. 2.48 In addition, with respect to complaints relating to decisions taken by the economic oversight authority, the right of appeal to a higher tribunal should be available. A compliance and enforcement regime providing for the creation of an administrative monetary penalty system, with appeals to an independent appeal tribunal, could be envisaged. It has to be recognized, however, that while an effective enforcement mechanism is a point of critical importance, it could be very demanding in terms of resources for many States. — — — — — — — —

CHAPTER 3 INTERNATIONAL COOPERATION

This Chapter addresses the various forms of international cooperation existing in the air navigation services field. Part A identifies the different forms of international cooperation. Part B focuses on various aspects related to international operating agencies. Part C deals with the scope, functions and financial aspects of joint charges collection agencies. Part D discusses multinational facilities and services, including provisions to be addressed in an agreement covering their establishment. Part E describes joint financing arrangements administered by ICAO. Part F addresses a political cooperation, the Single European Sky initiative, being developed in Europe. Part G considers organizational aspects in the context of major CNS/ATM components.

A. INTRODUCTION 3.1 International cooperative ventures in the provision of air navigation services have normally proven to be highly cost-effective for the provider States as well as the users, and in some instances have constituted the only means for implementing costly facilities and services which offer capacity that exceeds the requirements of individual States. By cooperating in such facility or service provision the States concerned have been able to provide more efficient services and at lower cost than if they had to finance the facilities concerned themselves. The ICAO’s Policies on Charges (Doc 9082/7) encourages international cooperation in the provision and operation of air navigation services where this is beneficial for the providers and users concerned (paragraph 12), and States or their delegated service providers are particularly recommended to consider participating in joint charges collection agencies (paragraph 18). 3.2 According to Assembly Resolution A35-14, Appendix X, States are expected to give consideration to cooperative efforts for introducing more efficient airspace management, in particular the upper airspace, taking into account the need for cost-effective introduction and operation of CNS/ATM systems. In this context Contracting States should consider, as necessary, establishing jointly a single air traffic services authority to be responsible for the provision of air traffic services within ATS airspace extending over the territories of two or more States or over the high seas. Also, operating agencies are referred to in ICAO Assembly Resolutions A22-19 “Assistance and advice in the implementation of Regional Plans” and A16-10 “Economic, financial and joint support aspects of implementation”. 3.3 The international cooperation may take different forms. In its simplest form there is a coordination and harmonization process initiated as a sub-regional activity between a limited number of States. There are significant synergies to be created and savings to be made by coordinating the planning, implementation and operation of air navigation facilities and services across borders with neighbouring States. Examples of such sub-regional activities are Roberts FIR Organization in Africa and Piarco FIR in Eastern Caribbean. An example of a regional activity is the initiative to cooperation in search and rescue (SAR) services in Africa (see text box below). A more formal machinery for cooperation may be established as an International

Operating Agency, a Joint Charges Collection Agency, a Multinational Facility/Service or an ICAO Joint Financing Arrangement. These forms of cooperation are described in parts B through E below. With reference to Assembly Resolution A35-14 above, a political cooperation, known as the Single European Sky, has emerged within the framework of the European Union Treaty. The Single European Sky initiative is described in Part F.

REGIONAL COOPERATION IN SEARCH AND RESCUE

The concept of regionalized, cooperative service provision can, to a certain extent,

compensate for the shortage of funds allocated to SAR systems in some States. Where there is a shortage of funds the allocation of suitable, local search units to life-saving tasks may not be possible. In such situations an infrastructure of trained personnel, appropriate

accommodation, shared communication facilities and multi-lateral memoranda of agreement in place could facilitate that search units volunteered from other places be

effectively and efficiently allocated by regional SAR coordinators. Such a base of human and material resources can be more easily established on a regional basis.

B. INTERNATIONAL OPERATING AGENCIES Scope and functions 3.4 An international operating agency in this context is a separate entity assigned the task of providing air navigation services, principally route facilities and services, within a defined area on behalf of two or more sovereign States. The services they provide are usually in the categories of ATS (ATM), COM (CNS), SAR (essentially rescue co-ordinating centres) and AIS, but can extend to MET as well. These agencies are also responsible for the operation of charges collection systems for services provided. 3.5 Examples of international operating agencies are the Agence pour la Sécurité de la Navigation Aérienne en Afrique et à Madagascar (ASECNA) in Africa (which however, operates airports as well as air navigation services), Corporación Centroamericana de Servicios de Navegación Aérea (COCESNA) in Central America and the European Organization for the Safety of Air Navigation (EUROCONTROL). A brief description of these three agencies is provided below.

AGENCE POUR LA SÉCURITÉ DE LA NAVIGATION AÉRIENNE EN AFRIQUE ET À MADAGASCAR (ASECNA) ASECNA, a public entity with financial autonomy, founded in 1959, is operated by 16

States in Africa and France, which is also a member. Its mission, on their behalf, includes the provision and operation of air traffic control, meteorological services and

communication facilities for the en-route and approach in member States as well as, aerodrome control and landing on the main airports listed in the Convention. The Agency may enter, under a separate individual contract, into agreement with each of these States

for the management of its airports or the maintenance of any facility serving an aeronautical purpose. The Agency may also be authorized to establish special equipment programmes for any State, especially with regard to the operation of terminal navaids or

any other tasks that could be entrusted to it.

The Agency is governed by a Ministerial Committee, composed of the ministers responsible for civil aviation in the signatory States, which defines general policy. It is administered by an Administrative Council, composed of one representative from each signatory State, assisted by a Director General. The Agency employs its own staff but it

can also have staff from signatory States seconded to it. ASECNA headquarters are located in Dakar (Senegal).

In accordance with the provisions of Article 15 of the Chicago Convention, the Agency may not extend to any user, directly or indirectly, or in any form whatsoever, benefits not

offered to other users availing themselves, under the same conditions, of the facilities under its management.

Methods of financing

At present, the Agency is totally financed from its own operating income. It is authorized

to levy charges to offset the financial obligations it assumes in the performance of the tasks entrusted to it and in return for services rendered to users. The Agency is also

authorized to collect all income that the property under its management generates in the course of serving aeronautical purposes.

Advantages 3.6 Experience indicates that international operating agencies have contributed, often significantly, to improved efficiency in the provision of facilities and services at lower cost to both providers and users. Among the advantages offered are more efficient use of personnel, facilities and equipment, as well as savings in research and development, given the avoidance of duplication at the national level, and through achievement of economies of scale. This has special relevance for States with less advanced economies where trained personnel and financial resources are scarce and where aviation must compete with other sectors of the economy. Operating agencies levying route facility charges may usually be more successful in the collection of amounts due for overflights owing to the larger geographical areas usually covered by their activities. Moreover, since such agencies represent a number of States, they tend to be in a stronger negotiating position in their financial and commercial dealings and may therefore be able to secure more advantageous terms. Establishing the agency

3.7 The size and composition of an agency's membership, and hence its geographical scope of operation, will primarily depend on political, economic, demographic and geographic considerations. The scope of its activities will also be influenced by these factors and the extent to which new and improved facilities may be required in some States to serve present and future traffic.

CORPORACIÓN CENTROAMERICANA DE SERVICIOS DE NAVEGACIÓN AÉREA (COCESNA)

COCESNA, founded in February 1960, has six member States, namely Belize, Costa Rica, El Salvador, Guatemala, Honduras and Nicaragua. The Corporation is an

integrated, international, Central American autonomous organization.

According to its Charter, the Corporation has exclusive rights to provide air traffic services, aeronautical telecommunications and radio navigation aids for international

civil aviation in the territories of the contracting parties. In practice, however, it provides services in the upper airspace (above flight level 200) and co-operates only partially with contracting governments in the provision of air traffic services in the lower airspace. It

may also provide to other States, through agreements, the above-mentioned services and aids specified in the ICAO Regional Air Navigation Plan. Furthermore, it may also

provide services and radio aids of the type mentioned above that are not specified in the ICAO Regional Plan within the territories of the contracting parties, by means of

contracts with public or private entities.

Methods of financing

In addition to working capital, the contracting parties also agreed to acquire, when necessary, and concede the use and possession of, at no cost to the Corporation, certain equipment listed in the Charter, as well as to provide the land on which the equipment

was situated, as well as all other property or furnishings directly related to the discharge of its functions. In order to maintain financial equilibrium and provide for the

development and expansion of its aeronautical services, the Corporation is authorized to levy charges on facility users. By this means COCESNA is at present wholly financed

from its own operating income. Organizational arrangements 3.8 The circumstances that lead to the creation of an international operating agency, as well as many other factors, will influence its structure. Since these will differ significantly from case to case, it is not practicable to prescribe any specific pattern of organizational arrangements for such agencies in general. Certain basic common features, however, have normally emerged. For example, the over-all policies governing the agency's functions, operations and financial affairs, as well as decisions on fundamental matters such as capital investments and the appointment of key staff, are likely to be the responsibility of a board of management composed of representatives of the Member States. Similarly, the chief executive will usually be responsible to the board, which is ultimately responsible for the general administration of the agency. From the outset, sound and well-defined financial and economic policies and practices need to be established relating to cost recovery and financial control, including accounting and budgeting procedures. Recruitment of agency personnel will also require careful consideration. (Reference should also be made to the text on agreement(s) between States and related contractual aspects in Part D of this Chapter.)

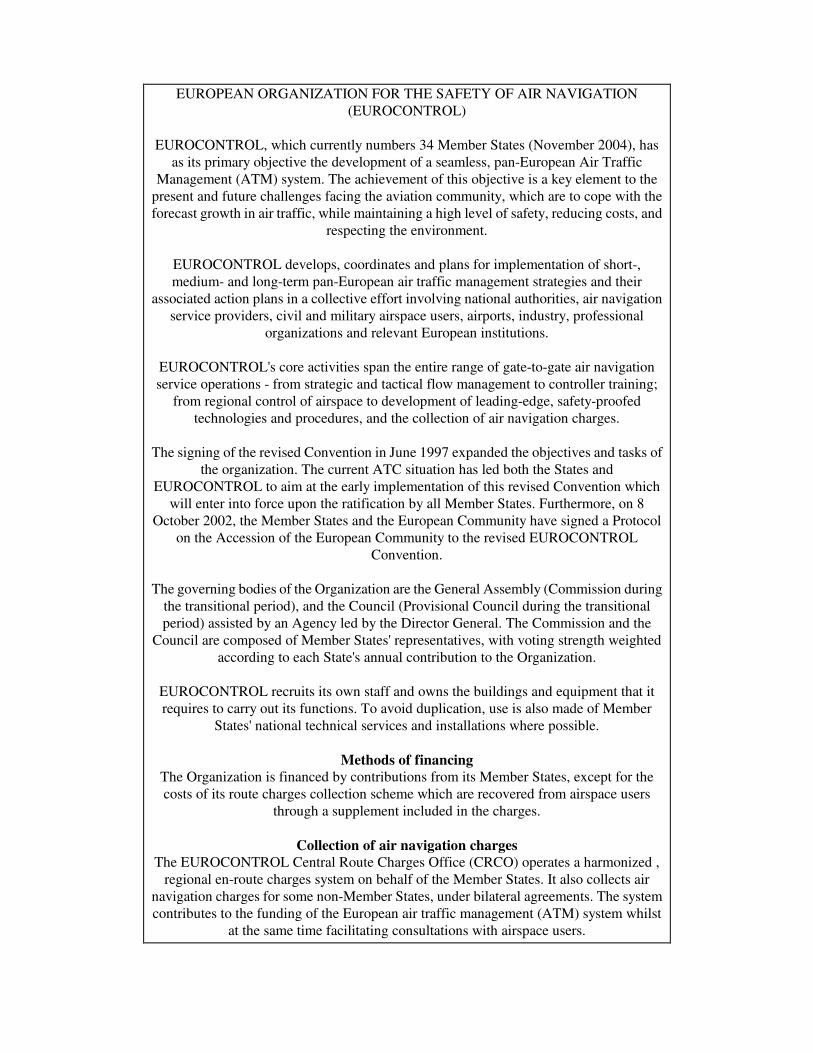

EUROPEAN ORGANIZATION FOR THE SAFETY OF AIR NAVIGATION (EUROCONTROL)

EUROCONTROL, which currently numbers 34 Member States (November 2004), has

as its primary objective the development of a seamless, pan-European Air Traffic Management (ATM) system. The achievement of this objective is a key element to the

present and future challenges facing the aviation community, which are to cope with the forecast growth in air traffic, while maintaining a high level of safety, reducing costs, and

respecting the environment.

EUROCONTROL develops, coordinates and plans for implementation of short-, medium- and long-term pan-European air traffic management strategies and their

associated action plans in a collective effort involving national authorities, air navigation service providers, civil and military airspace users, airports, industry, professional

organizations and relevant European institutions.

EUROCONTROL's core activities span the entire range of gate-to-gate air navigation service operations - from strategic and tactical flow management to controller training;

from regional control of airspace to development of leading-edge, safety-proofed technologies and procedures, and the collection of air navigation charges.

The signing of the revised Convention in June 1997 expanded the objectives and tasks of

the organization. The current ATC situation has led both the States and EUROCONTROL to aim at the early implementation of this revised Convention which

will enter into force upon the ratification by all Member States. Furthermore, on 8 October 2002, the Member States and the European Community have signed a Protocol

on the Accession of the European Community to the revised EUROCONTROL Convention.

The governing bodies of the Organization are the General Assembly (Commission during

the transitional period), and the Council (Provisional Council during the transitional period) assisted by an Agency led by the Director General. The Commission and the

Council are composed of Member States' representatives, with voting strength weighted according to each State's annual contribution to the Organization.

EUROCONTROL recruits its own staff and owns the buildings and equipment that it requires to carry out its functions. To avoid duplication, use is also made of Member

States' national technical services and installations where possible.

Methods of financing The Organization is financed by contributions from its Member States, except for the costs of its route charges collection scheme which are recovered from airspace users

through a supplement included in the charges.

Collection of air navigation charges The EUROCONTROL Central Route Charges Office (CRCO) operates a harmonized ,

regional en-route charges system on behalf of the Member States. It also collects air navigation charges for some non-Member States, under bilateral agreements. The system contributes to the funding of the European air traffic management (ATM) system whilst

at the same time facilitating consultations with airspace users.