do insurance companies pose systemic risk? j. david cummins, temple university naic winter 2009...

TRANSCRIPT

Do Insurance Companies Pose Systemic Risk?

J. David Cummins, Temple University

NAIC Winter 2009 National Meeting

Perspectives on Systemic RiskDecember 3, 2009

Copyright J. David Cummins, 2009, all rights reserved. Not to be reproduced without author’s permission.

Outline of Presentation

What is Systemic Risk? Too Big To Fail – Not just for financial institutions Insurers: How Big Are They?

Relative to banks Fraction of GDP

Insurers: How Solvent Are They? Insolvency rates Guaranty fund assessments Stock performance

Do flat guaranty fund premia create moral hazard? AIG: What Went Wrong? Does insurance pose a systemic risk?

If so, what are the systemic threats to the industry?

What is Systemic Risk?

What Is Systemic Risk?

The risk that an event will trigger a loss of economic value or confidence in a substantial segment of the financial system serious enough to have significant adverse effects on the real economy. Group of 10 (2001).

Systemic financial risk involves A system-wide financial crisis . . . accompanied by a sharp decline

in asset values and economic activity The spread of instability throughout the financial system (contagion) Sufficient to affect the real economy

World Economic Forum (2008).

Systemic risk is exposure to extreme correlations

Financial Crisis and Systemic Risk

Financial Crisis Prices of risky assets drop sharply Prices of safe assets increase (flight to quality) Asset price volatility increases Liquidity dries up (rising bid-ask spread & price impact) Financial institutions become financially distressed Credit markets dry up, economic activity depressed

Financial systemic risk: Financial crisis in which many institutions become financially distressed, with a potential impact on real economic activity

Financial distress does not mean systemic risk!

All Systemic Financial Crises Involve “Runs”

In crisis, investors seek cash at all costs As prices no longer adjust supply, access to credit

becomes central Maturity mismatch compounds shock and spreads runs

Rapid withdrawals lead to “fire sales,” prices crash Losses induce margin calls, more fire sales

Runs are both cause and consequence of extreme correlation

Crises that do not spread to general credit market do not qualify (e.g., “dot-com” bubble)

“Too Big to Fail” & “Too Interconnected to Fail”

Institutions that pose significant systemic risk are viewed as “Too Big to Fail” -- e.g., failure would cause ripple effects throughout the economy due to the sheer size of the enterprises

“Too Interconnected to Fail” -- Firms with multiple counterparty relationships could trigger a cascading chain of failures – “domino effect”

Too-Big-To-Fail Has Been With Us For a Long Time and Isn’t Confined to Financial Institutions

Industry/Company Year Type of Assistance

Penn Central Railroad 1970 $676.3 million in loan guarantees – Gov’t spent $19.7 billion and got back about $4 billion

Lockheed 1971 Gov’t loan which was paid off

New York City 1975 Loans and loan guarantees

Chrysler 1980 Loan guarantees and warrants – Gov’t earned a profit of about $660 million

Continental Illinois 1984 Government took 80% ownership and phrase TBTF was coined

Airline Industry 2001 Gov’t bought stock below mkt and provided loan guarantees

Automobile industry2008-2009

Govt takes equity stake in GM & Chrysler = $80 billion

Insurers:How Big And How Risky?

Total Assets: US Banks and Insurers

02,0004,0006,0008,000

10,00012,00014,00016,00018,00020,000

Ass

ets

($B

illio

ns)

Banks Life Insurers PC Insurers

Assets: Banks $14 trillion, insurers $5.8 trillion.

Source: Federal Reserve Flow of Funds accounts.

Total US Life and P-C Premiums: % of GDP

7.0%

7.2%

7.4%

7.6%

7.8%

8.0%

8.2%

8.4%

8.6%

8.8%

9.0%

Pre

miu

ms/

GD

P (

%)

Source: A.M. Best Company, American Council of Life Insurance, St. Louis Federal Reserve Bank.

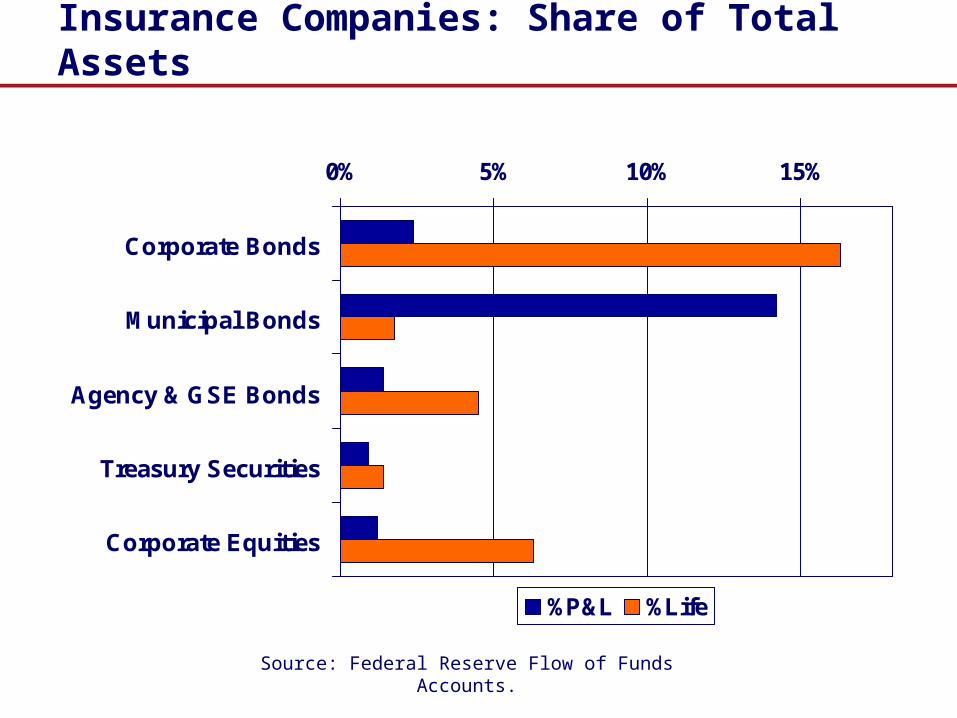

Insurance Companies: Share of Total Assets

0% 5% 10% 15%

Corporate Bonds

Municipal Bonds

Agency & GSE Bonds

Treasury Securities

Corporate Equities

%P&L %Life

Source: Federal Reserve Flow of Funds Accounts.

Equity Capital-to-Assets Ratios

0

0.05

0.1

0.15

0.2

0.25

0.3

0.35

0.4

Banks Life Insurers PC Insurers

Source: Federal Reserve Flow of Funds accounts, American Council of Life Insurance.

Premiums-to-Surplus Ratios: US Insurers

0.5

1

1.5

2

2.5

3

PC Insurers LH Insurers

P/C Insurer Impairments: 1969-2008

815

127

119

349

13 1219

916

14 1336

4931

3450

4855

6058

4129

1612

3118 19

49 5047

3518

14 15

75

0

10

20

30

40

50

60

7069 70 71 72 73 74 75 76 77 78 79 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08

Nu

mb

er o

f Im

pai

rmen

ts

Source: A.M. Best; Insurance Information Institute

Historically low impairments in 2007-2008.

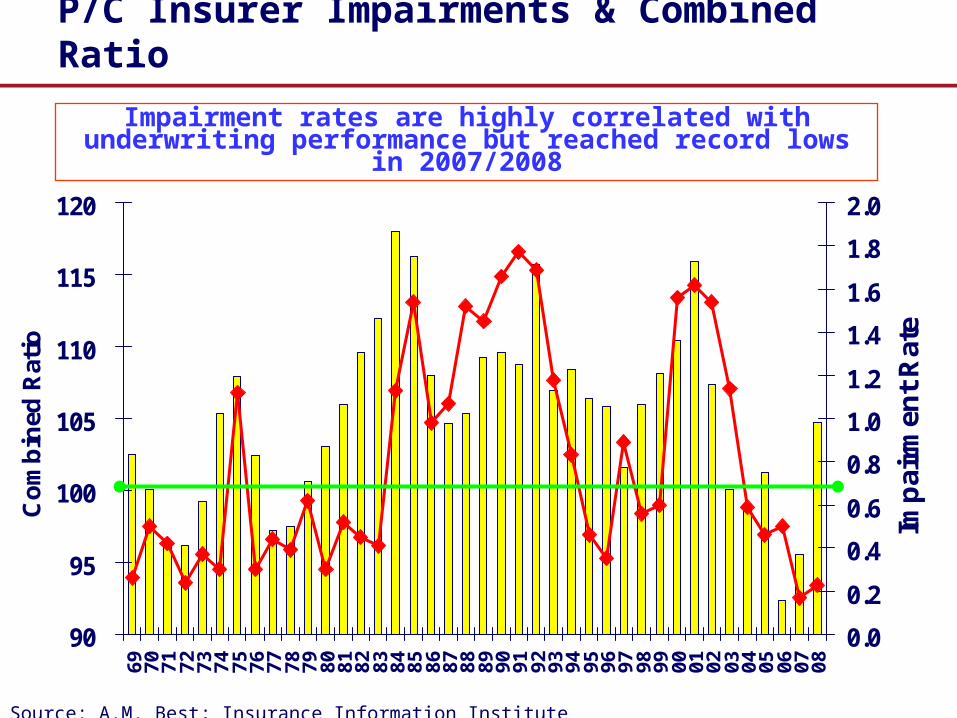

P/C Insurer Impairments & Combined Ratio

90

95

100

105

110

115

120

69 70 71 72 73 74 75 76 77 78 79 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08

Co

mb

ined

Rat

io

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

Imp

airm

ent

Rat

e

Impairment rates are highly correlated with underwriting performance but reached record lows in 2007/2008

Source: A.M. Best; Insurance Information Institute

P/C Impairment: Triggering Events

Source: A.M. Best: 1969-2008 Impairment Review, Special Report, Apr. 6, 2009.

Deficient loss reserves,

inadequate pricing, and rapid growth

are the leading triggers. Investment

& catastrophe losses play a much

smaller role.

Reinsurance Failure3.7%

Rapid Growth14.3%

Misc.9.1%

Affiliate Impairment

7.9%

Sig. Change in Business

4.2%

Deficient Loss

Reserves/In-adequate Pricing38.1%

Investment Problems

7.0%

Alleged Fraud8.1%

Catastrophe Losses7.6%

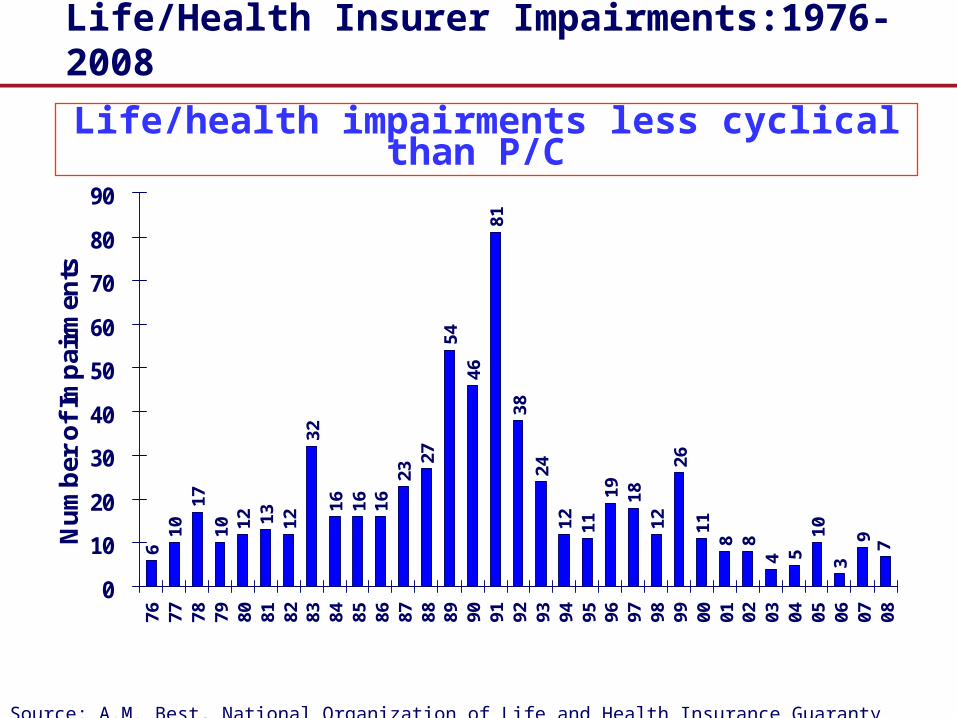

Life/Health Insurer Impairments:1976-2008

610

1710 12 13 12

3216 16 16

2327

5446

8138

2412 11

19 1812

2611

8 84 5

103

9 7

0

10

20

30

40

50

60

70

80

90

76 77 78 79 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08

Nu

mb

er o

f Im

pai

rmen

ts

Life/health impairments less cyclical than P/C

Source: A.M. Best, National Organization of Life and Health Insurance Guaranty Associations.

L-H Impairment Frequency & Profits

0

0.5

1

1.5

2

2.5

3

3.5

Fai

lure

Fre

qu

ency

-1

0

1

2

3

4

5

Aft

er-t

ax P

rofi

t M

arg

in (

%)

Source: A.M. Best.

L-H: Less obvious relationship with profits than P-L

L-H Impairments: Triggering Events

Source: A.M. Best: 2009 U.S. Life/Health – 1976-2008 Impairment Review, Special Report, May 25, 2009.

Inadequate pricing, affiliate problems, rapid

growth, and investments are

primary causes of L/H insolvencies.

Affiliate Problems

19.3%

Sig. Change in Business

4.6%

Misc8.6%

Reins Failure2.0%

Inadequate Pricing27.7%Alleged Fraud

8.6%

Rapid Growth14.7%

Investment Problems

14.5%

Life insurers more susceptible to affiliate problems.

Property-Casualty InsurerGuaranty Fund Assessments: 1978-2007

0

200

400

600

800

1000

1200

1400

Ass

essm

ents

($M

illio

ns)

0.00%

0.05%

0.10%

0.15%

0.20%

0.25%

0.30%

0.35%

0.40%

0.45%

0.50%

Ass

essm

ents

: % o

f Pre

miu

ms

GF Assessments % of NPW

Source: A.M. Best Company, National Conference of Insurance Guaranty Funds.

Life-Health Insurer Guaranty Fund Assessments: 1988-2007

0

100

200

300

400

500

600

700

800

900

1000

As

se

ss

me

nts

($

Mill

ion

s)

0.00%

0.05%

0.10%

0.15%

0.20%

0.25%

0.30%

0.35%

0.40%

As

se

ss

me

nts

: %

of

Pre

miu

ms

Assessments % of Premiums

Source: A.M. Best, National Organization of Life and Health Insurance Guaranty Associations.

US Life Insurers: 12 Month Change in Premiums (as of June 30, 2009)

Met

Pru

AIG

Har

tford

Man

ulife

TIAA

NY Life

Aeg

on U

SA

ING

USA

NW

Mut

ual

Linc

oln

Fin

Axa

US

-60

-50

-40

-30

-20

-10

0

10

20

30

40

% C

hang

e

Source: A.M. Best Company.

US Insurance Stock Indices vs. S&P 500

200

400

600

800

1000

1200

1400

1600

1800

Ind

ex 1

2/31

/04

= 1

000

P-C Life S&P 500

PC insurers beat the S&P, life insurers do not.

Source: A.M. Best Company.

Insurer Solvency: Conclusions

Insurers have about $6 trillion in assets but are not especially large relative to overall economy (8% of total U.S. financial assets)

US regulated insurance companies highly solvent Insolvency rates are low Guaranty fund costs are low

Life insurers give cause for concern May be over-leveraged Recent adverse performance is danger signal More interconnected than PC insurers (susceptibility to affiliates)

Inter-connectedness does not pose serious solvency threat for PC insurers based on past experience

Monolines are a different story – but not traditional insurance

Do Guaranty Funds Create Moral Hazard?

In theory, mis-priced guaranty fund coverage provides incentives for excessive risk-taking

In practice, guaranty funds do not seem to be a problem So-far, at least, there is no solvency crisis for US

regulated insurance companies Guaranty fund assessments have been very low

Possible rationale: Risk-based capital (introduced in 1994) blunts insurer

incentives for excessive risk-taking GF protection is incomplete (low maximums, etc.)

AIG: What Went Wrong?

AIG: What Went Wrong?

AIG’s traditional insurance operations did not cause its meltdown

AIG’s problems came from: Credit default swaps out of AIG Financial Products

● (Supposedly) regulated by Office of Thrift Supervision● US regulators had no jurisdiction

Securities lending program of life insurance subsidiaries

● Indicates need for more regulatory scrutiny in the future● US regulators do have jurisdiction if lending is out of regulated

life insurance subsidiaries

AIG Revenues Before the Crash

Foreign Life & Retirement

28%

Asset Management

5%

Foreign P&C11%

US P&C32%

Financial Services (AIGFP)

9%

US Life&Retirem

ent15%

12 months ending 12/31/2006.

AIG’s Credit Default Swaps

AIG sold CDS contracts, mostly to European banks

Banks were using the swaps to reduce regulatory capital, relying on AIGs overall credit rating (regulatory arbitrage)

AIG Financial Products had about $500 billion in CDS outstanding but virtually no capital AIG’s models supposedly showed that losses on the

CDS portfolio were virtually impossible Watch out for model risk and managerial moral hazard

AIG’s Securities Lending Operation

AIG loans securities to broker dealer or bank (e.g., to cover short selling or for diversification)

Borrower posts collateral in form of cash or high quality securities

AIG reinvests the collateral and earns spread between yield on invested assets and yield on underlying securities

AIG had $82 billion in liabilities for securities lending as of year-end 2007, $69 billion in August 2008

AIG Securities Lending: What Went Wrong

Declines in value of mortgages and other assets in 2007-2008 reduced value of reinvested collateral in securities lending programs

Many of the counterparties in the securities lending operation were the same institutions holding AIG credit default swaps

As asset values declined, borrowers terminated the securities lending arrangement to Improve liquidity Reduce exposure to AIG’s credit risk

At the same time, AIG had to post additional collateral for the CDS transactions as underlying “insured” asset values declined

The Bailout: Payments to AIG Counterparties

Counterparty CDS Trans. Asset Lending Total

Goldman Sachs 8.10 4.80 12.90

Societe Gen. 11.00 0.90 11.90

Deutsche Bank 5.40 6.40 11.80

Barclays 1.50 7.00 8.50

Merrill Lynch 4.90 1.90 6.80

Bank of Amer 0.70 4.50 5.20

UBS 3.30 1.70 5.00

BNP Paribus 0 4.90 4.90

Others 14.70 11.60 26.30

Total 49.60 43.70 93.30

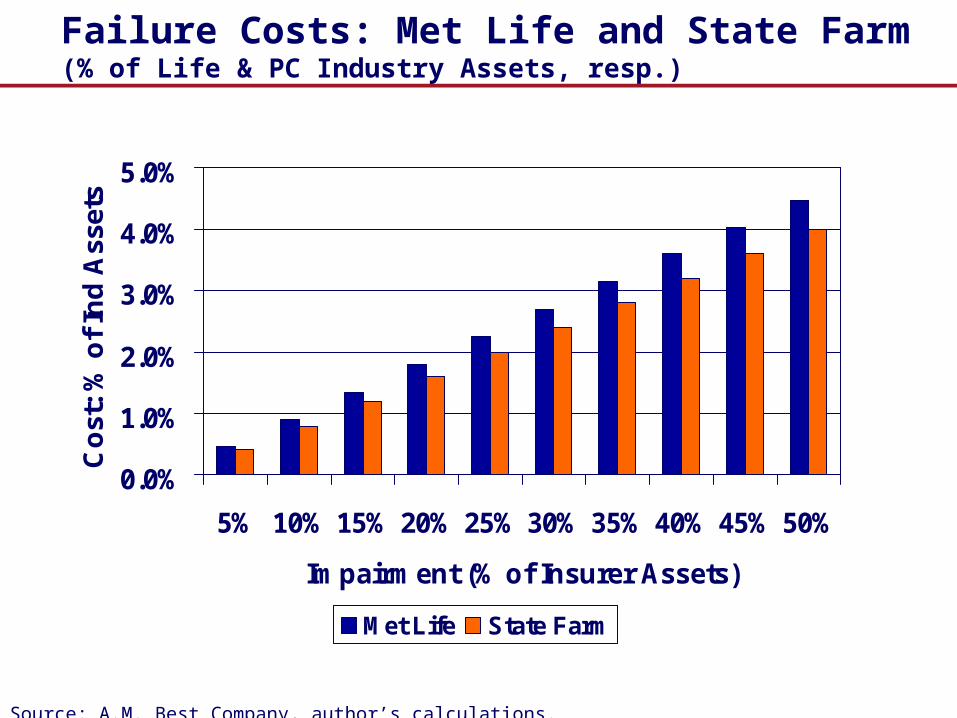

US Insurer Assessments vs. AIG

Total US life and P-C assessments: 1988-2007 $18 billion

Federal assistance to AIG (as of June 30, 2009): $136 billion Not necessarily a net loss But . . . .

Total assets of largest insurers: 2008 Met Life: $422.6 billion State Farm: $116.5 billion

Source: A.M. Best Company, Harrington (2009).

Failure Costs: Met Life and State Farm(% of Life & PC Industry Assets, resp.)

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

5% 10% 15% 20% 25% 30% 35% 40% 45% 50%

Impairment (% of Insurer Assets)

Co

st:

% o

f In

d A

sset

s

Met Life State Farm

Source: A.M. Best Company, author’s calculations.

Does Insurance Pose Systemic Risk?

What Is Systemic Risk Policy Trying to Prevent?

Runs on banks – traditional concern Contagion – information asymmetries

Banking system collapse – Continental bank

● Correspondent bank collapse – counterparties● Jobs would be lost

Threat to settlement system and network effects Fear that Infrastructure of short term money market and OTC derivatives would

not handle failure of significant counterparty and might cast doubts on the soundness of other counter parties (Bernanke on Bear Stearns)

Panic due to loss of confidence Risks to system due to failure of “highly interconnected” firm “Unpredictable consequences of a failure for broader financial system” Reaction of counterparties of other firms that might come under future

government control AIG was large, complex and interconnected whose failure would impose losses on

counterparties and also endanger the entire world’s financial sector (Bernanke-Morehouse University)

Property-Casualty Insurance Does Not Create Systemic Risk

“Runs” are not possible To obtain funds, it is necessary to have a claim Unlike bank deposits, which are instanteously “putable”

Inter-sector exposure among insurers and between insurers and reinsurers not sufficiently large to cause cascading failures (e.g., reinsurance failures and affiliate problems account for about 11% of P-C failures but 20% in L-H insurance)

Insurance not involved in liquidity creation, payments system or business/consumer lending

Insurers hold only small proportion of total invested assets in the economy

Insurance claim payments not a major financial asset for any economic sector

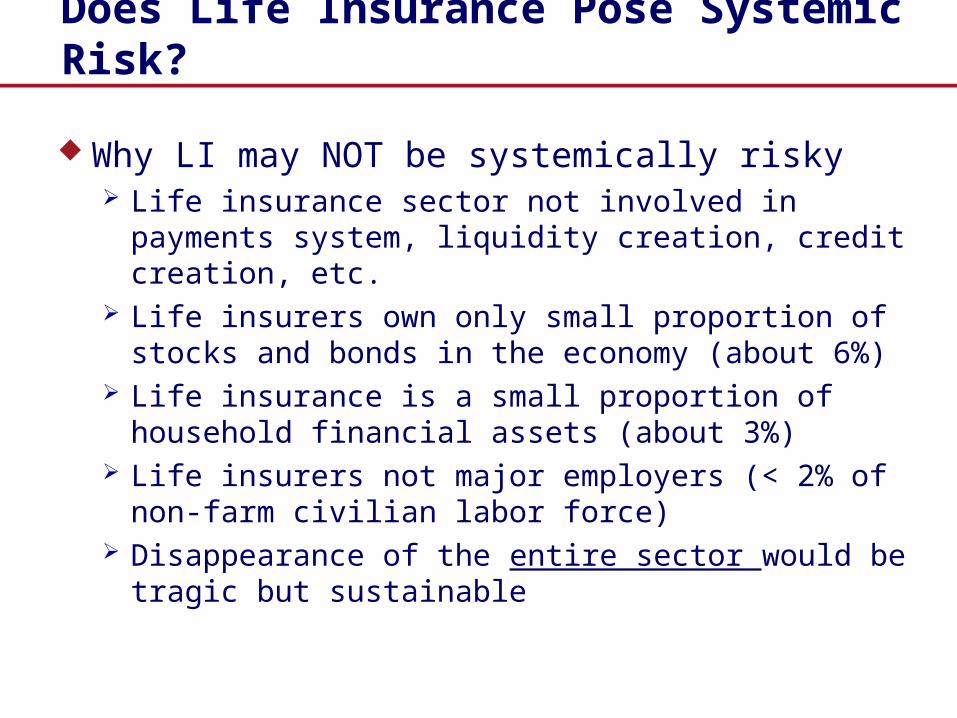

Does Life Insurance Pose Systemic Risk?

Why LI may be systemically risky Life insurance investment products are susceptible to

“runs” (withdrawals and/or suspension of premium payments/annuity considerations)

Life insurers are thinly capitalized Insurance guaranty fund system probably not adequate

for a major run or liquidity crisis Life insurers owned by banks (and vice versa) could

add to fragility of banking system

Does Life Insurance Pose Systemic Risk?

Why LI may NOT be systemically risky Life insurance sector not involved in payments system,

liquidity creation, credit creation, etc. Life insurers own only small proportion of stocks and

bonds in the economy (about 6%) Life insurance is a small proportion of household

financial assets (about 3%) Life insurers not major employers (< 2% of non-farm

civilian labor force) Disappearance of the entire sector would be tragic but

sustainable

Systemic Risk In Insurance: Banking Activities

As AIG debacle shows, the main systemic risk posed by the insurance industry comes from insurer participation in “banking” activities, e.g., credit default swaps (CDS) and other derivatives

Swiss Re data shows that insurers and reinsurers accounted for 33% of CDS market in early 2000s

As with AIG, most insurers are not adequately capitalized to sustain large CDS meltdown

Insurance groups should not be permitted to conduct CDS operations

Systemic Risk and OTC Derivatives

“Too big to fail” partly based on counterparty risk Reduce counterparty risk by moving popular products to

centralized clearing – e.g., credit default swaps Reduce remaining counterparty risk by trade

transparency Liquidity also improved by enhanced transparency

Require CDS writers to hold adequate capital Derivatives trading poses significant “model risk,” i.e.,

impossible to foresee all possible eventualities that could cause major losses.

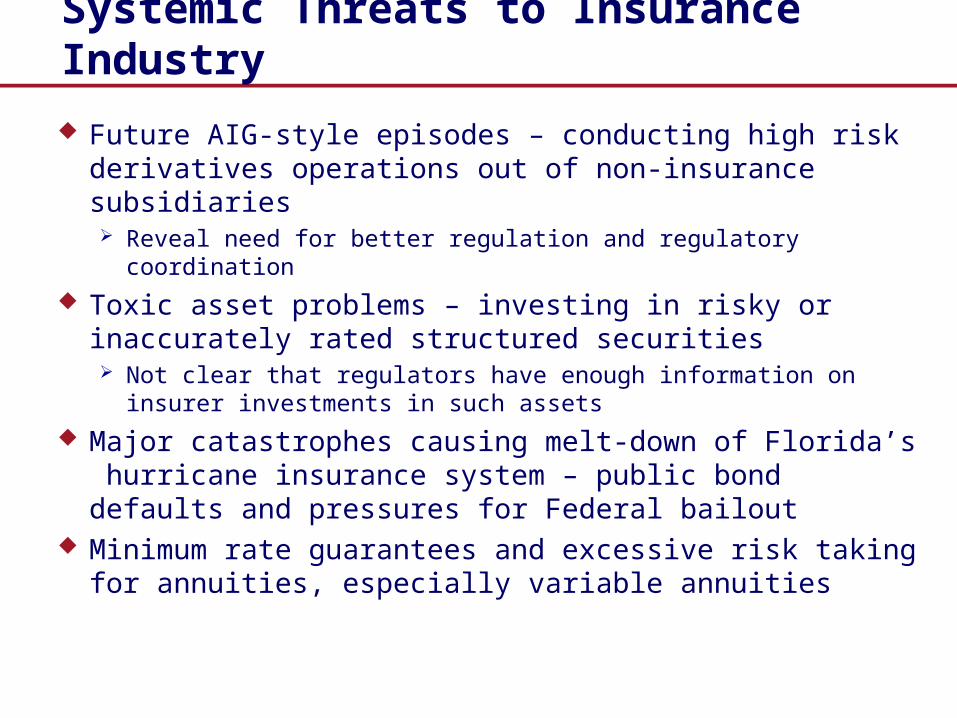

Systemic Threats to Insurance Industry

Future AIG-style episodes – conducting high risk derivatives operations out of non-insurance subsidiaries Reveal need for better regulation and regulatory coordination

Toxic asset problems – investing in risky or inaccurately rated structured securities Not clear that regulators have enough information on insurer

investments in such assets

Major catastrophes causing melt-down of Florida’s hurricane insurance system – public bond defaults and pressures for Federal bailout

Minimum rate guarantees and excessive risk taking for annuities, especially variable annuities

Systemic Risk: Lessons

At the national level, the financial crisis exposed the limits of supervision that is geared only to local entities and neglects the systemic implications of financial institutions with global reach

There can be little doubt that global governance and the institutions charged to develop the frameworks and carry out such governance should be strengthened (World Economic Forum 2009)

Further Information

American International Group, 2009, AIG: Is the Risk Systemic? Powerpoint presentation (New York).

De Bandt, Olivier and Philipp Hartmann, 2000, Systemic Risk: A Survey (Frankfurt, Germany: European Central Bank).

Group of 10, 2001, Report on Consolidation in the Financial Sector Harrington, Scott E., 2009, The Financial Crisis, Systemic Risk, and the Future of Insurance

Regulation (Indianapolis, IN: National Association of Mutual Insurance Companies). Kaufman, George G., 1996, “Bank Failures, Systemic Risk, and Bank Regulation,” The CATO

Journal 16: 17-45. Kaufman, George G., 2000, “Banking and Currency Crises and Systemic Risk: Lessons from

Recent Events,” Federal Reserve Bank of Chicago Economic Perspectives 24: 9-28. Swiss Re, 2003, Reinsurance – A Systemic Risk, Sigma No. 5/2003 (Zurich, Switzerland). World Economic Forum, 2009, Global Risks 2009 (Geneva, Switzerland).