distribution dialogue spring 2015 - mackay williams€¦ · distribution dialogue – spring 2015...

TRANSCRIPT

Distribution Dialogue Spring 2015 London, 26th March 2015

DISTRIBUTION DIALOGUE – SPRING 2015

1. Introduction

2. The lay of the land

3. Brand buzz – role of brand in fund distribution

4. Recipes for sales success

5. Looking into the crystal ball

6. Q&A

A snapshot of current themes in the European fund industry Mark McFee

The lay of the land

AGENDA

1. The sales context

2. Diversification rules

3. Passive contenders

4. Disruptive forces

The sales context How has the industry been doing?

2014: off with a bang, out with a fizz

Net sales of active long-term funds (€m)

Source: Lipper FundFile / Fund Radar analysis (Data excludes money market funds, funds of funds and ETFs)

Diversif ication rules Investors spread their bets

Thirst for returns drives fund influx

! Current environment continues to favour fund investment.

! But investors are still moving beyond traditional choices, with mixed assets an important solution.

! Income and absolute return remain popular.

! Fund of funds sales are trending upwards.

Fund of funds sales back on form

Net sales of third-party funds of funds (€m)

Source: Lipper FundFile / Fund Radar analysis

Passive contenders Providers of ETFs and index trackers throw fees into stark relief

Fee pressure is driving passive allocations

Source: MackayWilliams analysis based on 450 Fund Buyer Focus interviews conducted between April and September 2014.

Average fund selector allocation to passive funds (%)

Which way is the wind blowing?

The pressure from ETFs for others to continue reducing costs will impact positively on the fund industry.

Switzerland, Insurance The move over to passive investment is a knee- jerk reaction and I think things will stabilise. UK, IFA

The industry is going in two directions – either very active or passive. You’ll see more outflows in semi-active funds into passive funds. Nobody wants to pay a 2% fee for 1% growth. Switzerland, Advisory Manager

Source: Fund Buyer Focus

I only use ETFs when there is no active fund management available. Luxembourg, Fund of Funds

We plan to reduce sales volumes with the bigger bank-affiliated fund groups, due to media coverage and the perception that they are managing passively but are charging for active management.

Sweden, Fund Supermarket

Tracking developments

! Passive providers eat further into active managers’ lunch with the advent of active ETFs and smart beta.

! Active share is gaining traction as an anti-index-hugging metric – but it arguably misses the point.

! The key attraction of passive brands lies in pricing but active providers can compete on many other aspects.

Disruptive forces Who is shaking the trees of fund distribution?

Sources of upheaval

! Digital behemoths?

! Stock exchange fund platforms?

! Industry personalities?

Brand buzz – role of brand in fund distribution Trends and asset managers that are shaping the rules of engagement Fiona Maciver

THE NEXT 20 MINUTES…

1. B2B brands

2. Brand in fund selection

3. Blurring the boundaries - the

end-client

4. Successful asset management

brands

Sir Richard Branson, CEO Virgin

Branding demands commitment; commitment to

continual re-invention; striking chords with people to stir their emotions; and commitment to imagination. It is easy to be cynical about such things,

much harder to be successful.

B2B Brand characteristics

• Complex buying process • Multiple-decision makers

• Evidence based and rationale decision making process?

• B2B companies investing more in brand – more companies appearing in global ranking studies.

Brand often the only differentiator

BRAND IN FUND SELECTION Why is brand becoming more important?

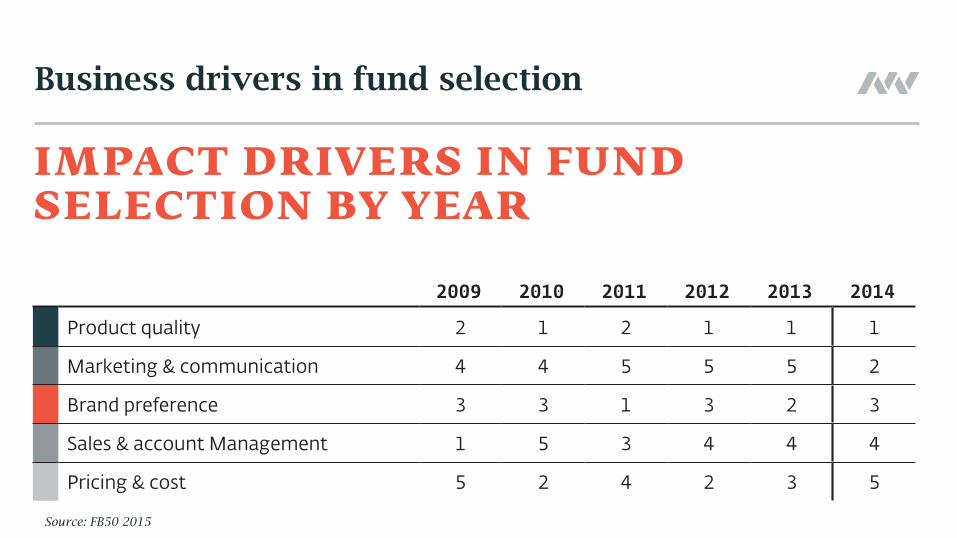

Business drivers in fund selection

Impact drivers in fund selection by year

2009 2010 2011 2012 2013 2014

Product quality 2 1 2 1 1 1

Marketing & communication 4 4 5 5 5 2

Brand preference 3 3 1 3 2 3

Sales & account Management 1 5 3 4 4 4

Pricing & cost 5 2 4 2 3 5

Source: FB50 2015

Trends driving brand and marketing activity

! Crowded marketplace – differentiation

! More retail investors returning to the market

! Intermediaries requiring more support ! Regulation and transparency

! Disruptors – new entrants and DIGITAL

! End-investors

Digital disruption…

• New entrants • Increased user expectations

• Transparency of information

• More content being consumed online via different channels and devices!

Cross-border companies leading the challenge Rank Public website Social/New Media

1 JPMorgan JPMorgan

2 BlackRock BlackRock

3 M&G M&G

4 Franklin Templeton Fidelity

5 DeAWM Franklin Templeton

Data source: Fund Buyer Focus, Retail Sector, Yearly Comparison Dec 2014, No of interviews 431

There should be a wider use of social media to improve the presence in this field on the whole. The point is, to find the perfect mix of informing end-customers and also generating interest in all manner of different ways. Austria, Retail Banking

Influence of the end-client

! Trust

! Comfort of familiar names ! Curiosity

! Access and quality of content

! Future regulation - Mifid2

The brand awareness is important to us when selecting providers because our clients only buy well-know brands. Furthermore we take the risk management and low volatility into account. Germany, Discretionary Portfolio Management Brand recognition is a key consideration, whether a provider is a big global firm or a smaller niche player. In itself, the size of the firm is not important as far as we are concerned, as long as clients are familiar with the brand name [...] Recognition of the brand among our sales staff is also important. Sweden, Fund Supermarket

SUCCESSFUL ASSET MANAGEMENT BRANDS Fund Brand 50 2015

How does FBF measure brand?

BRAND PREFERENCE

+

10 WEIGHTED BRAND ATTRIBUTES

=

TOTAL BRAND SCORE

Active AM Brand Profile

Source: FB50 2015

Brand preference Appealing investment strategy

Keeping best informed

Stability of investment management team

Client-oriented thinking Expert in what they do

Solidity Quick adaptation to market evolution Innovative power Key international player Local knowledge

Different ways to stand out in FB50 rankings

Manager Type Typical Brand Visibility

Differentiation Example

Multi-disciplinary Push Extensive market coverage combined with high levels of sales and a marketing support.

JP Morgan Schroders

Multi-disciplinary plus flagship fund

Pull Product and marketing M&G

Active specialist Pull Product Ethenea

Passive specialist Pull Price Vanguard

Brand rankings 2014

Source: FB50 2015

Building brand success - Schroders

Business Drivers

Brand Attributes

I like the fact that you can easily meet the fund managers there and quickly run the rule over the products. Furthermore, this provider is good at keeping costs down. In addition, it generally provides good product and market commentaries in very timely fashion each month and its website is good.

UK, Advisory Portfolio Management

Business driver

Product Quality

Sales & Acc Mgt

Mkting & Comm Pricing

Brand Pref

Rank 6 5 7 7 6

Brand attribute

Appealing Inv strategy

Keeping best informed

Stability of Inv Mangement team

Client-oriented thinking

Rank 7 4 9 4

Source: FB50 2015 / Fund Buyer Focus

And finally…

Zig Ziglar

If people like you they will listen to

you, but if they trust you, they’ll do

business with you.

Recipes for sales success Or how client service is a crucial component of a winning business Chris Chancellor

AGENDA

1. Why does sales and account

management matter?

2. What is important in sales and

account management?

3. How frequently should you see

clients?

What is sales and account management?

We think:

! A partner to clients, helping and

supporting them in their businesses.

! The key point of personal client

contact, the living embodiment of

your brand

! A critical route for information and

marketing messages to be delivered

“A person whose job involves selling

or promoting commercial products,

either in a shop or visiting locations

to get orders.”

Oxford Dictionary definition

The perfect mix

Sales & account management Marketing

Brand Product,

performance & pricing

Positive net sales

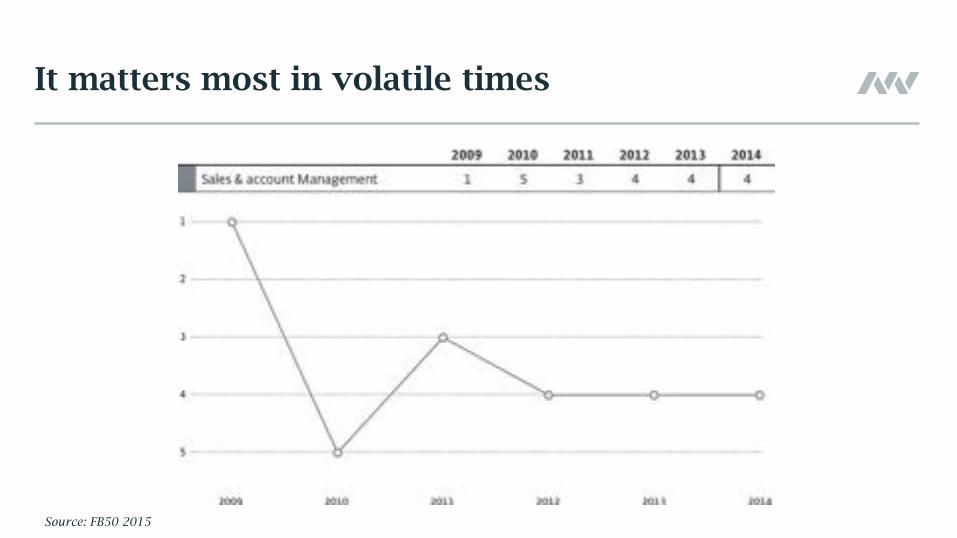

It matters most in volatile times

Source: FB50 2015

The simple things matter… [They are] very responsive, as soon we ask a question the answer returns. If you ask them questions, you can really go into detail and the information you receive is accurate and precise.

France, F-o-F Mgt.

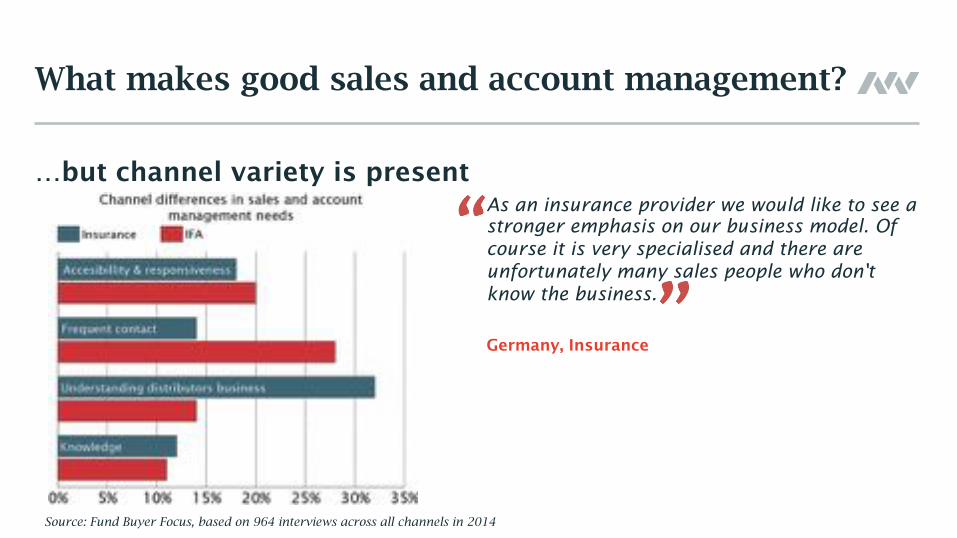

What makes good sales and account management?

Source: Fund Buyer Focus, based on 964 interviews in 2014

…but channel variety is present As an insurance provider we would like to see a stronger emphasis on our business model. Of course it is very specialised and there are unfortunately many sales people who don't know the business.

Germany, Insurance

What makes good sales and account management?

Source: Fund Buyer Focus, based on 964 interviews across all channels in 2014

Groups have different strengths and weaknesses

That makes sense if it aligns with channel needs

Source: Fund Buyer Focus, based on 964 interviews in 2014

Average number of visits wanted Two selected groups’ visits per channel

Digging deeper – how frequent is frequent?

Source: Fund Buyer Focus, based on 964 interviews from October 2014 – March 2015

Frequency of contact is critical, but so is quality

I would suggest that they take care not to overdo their contact and communication with us. We want good service but we don't want to have it pressed on us to the point where it becomes counter-productive. Netherlands, Discretionary Portfolio Management

A number of fund houses have very aggressive sales teams that try to push us into accepting more visits from them than we would like. Spain F-o-F Mgt.

They need to strike the right balance and provide us with an adequate level of service, without overdoing things to the point of pestering us. At times, they send too much information, or visit us more frequently than we want them to. Swiss, Advisory Portfolio Management

Source: Fund Buyer Focus, based on 964 interviews in 2014

Keys to success

! Know what matters for clients in the

countries and channels you care about.

! Know your strengths and weaknesses.

Get the basics right, then work on

excelling.

! Sales & account management is the key

personal client contact. They must work

as a team with Marketing, Product,

Brand and Pricing.

Looking into the crystal ball Assessing future trends in European distribution Mauro Baratta

AGENDA

1. Outlook for 2015 and beyond

2. Markets & products to watch

3. 2020 vision

LOOKING INTO THE FUTURE What to expect in 2015

Factors at play in 2015

1. Record low interest rates in Eurozone likely to remain unchanged, driving more retail money into funds. Meanwhile possible US rate rises later in the year likely to affect EM and US$ fixed income products.

2. Weak oil prices provide help to struggling economies in Eurozone but could further weaken some Asian and exporter emerging markets

3. QE introduced in March by Draghi – still too soon to assess impact across Europe but stimulus to the economy and markets likely to be negligible

4. Greece’s troubles are far from over: likely to add further uncertainty and create periodic market volatility. Market seems to assume there will be no Grexit

5. UK general elections in mid-May could potentially cause further instability if Conservatives win and referendum on EU membership is set for 2017

How successful will 2015 be for the industry?

Source: Lipper FundFile / MackayWilliams estimates

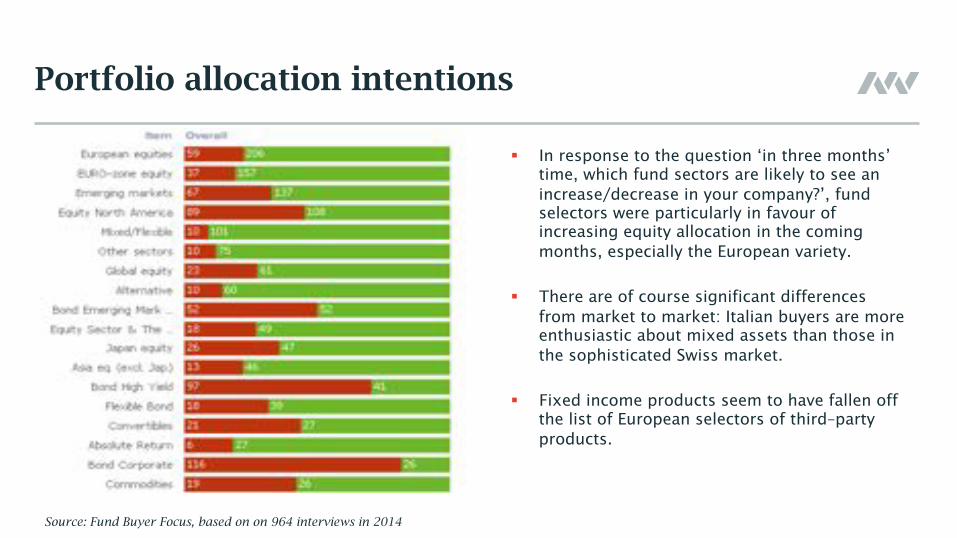

Portfolio allocation intentions

! In response to the question ‘in three months’ time, which fund sectors are likely to see an increase/decrease in your company?’, fund selectors were particularly in favour of increasing equity allocation in the coming months, especially the European variety.

! There are of course significant differences from market to market: Italian buyers are more enthusiastic about mixed assets than those in the sophisticated Swiss market.

! Fixed income products seem to have fallen off the list of European selectors of third–party products.

Source: Fund Buyer Focus, based on on 964 interviews in 2014

Drivers of change in 2015

Source: Fund Buyer Focus, based on on 964 interviews in 2014

2

Markets & products Most successful markets and products in 2015

Markets to watch in 2015

United Kingdom

Italy

Germany

Spain

-100

-50

0

50

100

150

200

250

300

2010 2011 2012 2013 2014

Captive Third-party

3rd party distribution developments

Net sales by type of channel - €bn AUM by channel type

Captive 45%

Third-party 55%

FoFs 9%

Insurance 13%

Advisory 38%

Discretionary 20%

Retail Banking/Financial Advice 20%

Source: Lipper FundFile (Data excludes money market funds, funds of funds and ETFs), Fund Radar / Fund Buyer Focus analysis

Products to watch in 2015

! Solutions, comprising absolute return, flexible, multi asset, volatility-controlled products;

! Income remains a key feature for launches as groups find for ever more colorful ways to play this theme;

! Passive funds (ETFs and index trackers) likely to grow, on the back of constant fee pressure. Smart beta will also start to tip over into the retail space.

Source: MackayWilliams analysis based on 450 Fund Buyer Focus interviews conducted between April and September 2014

Respondents may mention more than one need

2020 vision Key Dynamics to watch in 2015 and growth projections to 2020

Key dynamics to watch in 2015

1. Market volatility and interest rates in Europe and the US will continue to affect sales volumes during 2015;

2. According to fund selectors, regulation and issues relating to pricing/costs remains the likely drivers of change in the structure of European fund distribution landscape;

3. Star markets for 2015 are likely to be UK, Italy, Germany and Spain – for both local players and cross-border fund houses;

4. Increased competition for cross-border groups from local fund houses. Banks in key markets will continue to migrate their clients into captive fund products;

5. In product development, shift towards multi-asset solutions, flexible products, income generating funds set to continue in 2015;

Asset growth projections to 2019 (€bn)

Source: Lipper FundFile / MackayWilliams estimates

CAGR 10.3%

€9.4tn