disease state primer: ovarian cancer - lumleian...

TRANSCRIPT

Q1 2012 Update

Disease State Primer: Ovarian Cancer

http://www.mayoclinic.com/images/image_popup/c7_ovarian_cancer.jpg

2

Table of Contents

Slide Number

I. Introduction • Who is Lumleian and what is a disease state primer?

• What is our perspective on ovarian cancer?

• 3 – 6

• 7 – 9

II. Disease Overview and Care Paradigm • What is ovarian cancer?

• Epidemiology by geography and risk factors

• Presentation, diagnosis, classification

• Current care paradigm and clinical evidence

• Emerging care paradigm

11 • 12

• 13

• 14

• 15 - 20

• 21

III. Clinical Development Pipeline • Clinical development pipeline mapping

• Traditional chemotherapies

• Anti-Angiogenesis agents

• Kinase Inhibitors

• Folate Receptor Targeting Agents

• Ovarian Cancer Vaccines

23 • 24 – 29

• 30 - 31

• 32 – 36

• 37 – 38

• 39 – 41

• 42 – 43

IV. Commercial Landscape • Estimated use in ovarian cancer of branded therapies

• Global, US, EU, Japan market size and growth by brand

• Wall Street consensus forecasts for pipeline assets

• US growth decomposition: Rx volume, pricing, product mix

• US promotional spending, marketing mix and brand messaging

45 • 46

• 47 - 50

• 51

• 52

• 53 – 56

V. Appendix • Table of Acronyms

• More about Lumleian

• 58

• 59 – 61

3

Lumleian offers the requisite scale and depth of life science expertise required for our client’s

most critical investment decisions; We offer universal information and real time knowledge.

• Data Mining

- Regulatory filings

- Scientific literature

- Patent filings

- Company filings

and press releases

• Secondary Data

- Industry pipelines

- Wall Street analysis

- US TRx, pricing,

promotional spend

• Primary Research

- Key opinion leaders

- Practicing physicians

- Reimbursement

Expertise Based

Teams

• Experience

- Academic faculty

- Bio-pharmaceutical

- Equity research

- Strategy consulting

• Expertise

- 30+ clinicians

and Ph.D. scientists

• Analytics

- 5 Ph.D. economists

and statisticians

Universal

Information

Real-Time

Knowledge

• Disease State Primers

- Disease overview

and care paradigm

- Clinical development pipeline

- Commercial landscape

• Functional Drill Downs

- In licensing assessments

- Early and late stage

- Preliminary due dilligence

- Real-time clinical data

• Proprietary Analytics

- Asset valuation

- Epidemiologic forecasts

- Industry benchmarks

• Drug Development

and commercial

- Patient segment valuations

- Promotional response models

• Healthcare professional

and direct to consumer

• Academic and

Research Institutions

- Portfolio optimization

• Early stage

- Out licensing strategy

• Asset valuation

• Transaction support

• Royalty monetization

• Bio-pharmaceutical Companies

- Asset valuation

- Clinical strategy

- In licensing strategy

• Early and late stage

- Portfolio optimization

• Early and late stage

- Preliminary due dilligence

• Life Science Investors

- Asset valuation

- Clinical strategy

- In licensing strategy

Life Science

Client Base

Decision

Support

4

Notes: 1These are a representative sub-set of the publicly available data sources

To ensure real-time knowledge, across disease states, our team of 30+ clinicians and Ph.D.

scientists maintain a comprehensive knowledge management platform, leveraging novel data

mining technology and proprietary analytics.

Data Mining

and Analytics

• Company presentations

• Earnings announcements

• Equity research coverage

• Investor relations transcripts

• Clinical trials

• Conference presentations

• Gene ontology

• Industry pipeline databases

• NIH grants

• Scientific literature & citations

• Business development transactions

• Venture capital investments

• Disease profiles

• Industry publications

• Sales and Rx data

• Treatment algorithms

• Advisory committee transcripts

• FDA and EMA filings

Scientific

& Clinical:

Financial:

Academic

Tech Transfer:

Competitive

Landscape:

• Early stage technologies

• Intellectual property filings

Business

Development:

Regulatory:

• Leverage data mining

technology to access

novel data sources

• Standardize, collate,

and link data sources

• Execute Lumleian’s

proprietary analytical

models

Universe of Public

Information1

• 30+ clinicians and

Ph.D. scientists

- Focused by area

of expertise

• 5 Ph.D. economists

and statisticians

Expert Validation

and Decision Support

5

Our efficient platform and our expertise based teams enable us to both deliver the highest

quality product and tailor our offer, to specific client needs: Either custom decision support or

more standardized research and analytics, e.g. disease state primers.

Decision

Support

• Clinical strategy

• Portfolio optimization

- Pre-Clinical

- Clinical

• Transaction support

- In licensing

- Out licensing Disease

State Primers

Proprietary

Analytics

• Asset valuation

• Epidemiologic forecasts

• Industry benchmarks

- Commercial

- Clinical Development

• Patient segment

valuations

• Promotional

response models

- Healthcare professional

- Direct to consumer

• Royalty monetization

Functional

Drill Downs

• Real-time clinical

data

- Trial strategies

- Results

• In licensing

assessments

- Pre-clinical

- Clinical

• Preliminary

due dilligence

- Scientific

- Clinical

- Commercial

• Disease overview

and care paradigm

• Clinical development

pipeline

• Commercial

landscape Customized

Standardized

6

What information is included in a disease state primer?

• Lumleian’s objective and fact based perspective on the relative attractiveness of investing in a given disease state

• Disease overview and care paradigm - Etiology, Diagnosis and patient segmentation, Global epidemiology, Treatment algorithm, Clinical evidence, Emerging care paradigm

• Clinical Development Pipeline - Validated industry pipeline for all assets in clinical development, Select mechanism of action profiles, trial designs and evidence

• Commercial landscape - Global, US, EU, Japan market and brand revenue, Pipeline forecasts, US growth decomposition, Promotional spend and messaging

What disease states are planned for 2012? • Autoimmune: Inflammatory Bowel Disease, Lupus, Multiple Sclerosis, Psoriasis, Rheumatoid Arthritis

• Cardiovascular: Hyperlipidemia

• Central Nervous System: Alzheimer’s Disease, Depression, Pain, Schizophrenia

• Endocrine: Type II Diabetes, Obesity

• Infectious Disease: Gram Negative Bacteria, Hepatitis C Virus

• Oncology: Breast, Colorectal, Leukemia(s), Lung, Lymphoma(s), Melanoma, Ovarian, Pancreatic, Prostate

• Pulmonary: Chronic Obstructive Pulmonary Disease, Idiopathic Pulmonary Fibrosis

Can we create custom disease state primers for customers? • Yes, based on the expertise of our team of 30+ clinicians and Ph.D. scientists, 5 Ph.D. economists and statisticians we can create a

sustome primer in appoximately 3 to 4 weeks

• We can supplement the primers with deeper analysis to help customers reach a deeper understanding of critical issues e.g. KOL

interviews, Financial Models, Survey Conduction and Analysis, Pre-Clinical Asset Assessment

• We are also developing deep drills by function, e.g. Discovery, Clinical development, Business development, Commercial

Why did we create our disease state primers? • We were frustrated by having to repeatedly validate, standardize, and collate pipeline and commercial data

• Portfolio optimization requires a standard framework to compare “apples to apples” investment decisions across disease states

• Our primers began as a training tool; We require every decision scientist create one from scratch before supporting clients

What is a Lumleian’s disease state primer?

7

Disease

Overview and

Care Paradigm

• Ovarian cancer is an aggressive gynecologic cancer with a high mortality rate, and an overall 5-year survival rate of

45%; ~15K patients die annually in the US from ovarian cancer

• Due to the lack of early-stage symptoms and a corresponding delay in diagnosis, ovarian cancer is the fifth most

common cause of cancer death in women

• All ovarian cancer patients undergo the same surgical procedure, which involves the removal of the uterus, ovaries,

and fallopian tubes

• Ovarian cancer is a highly chemo-sensitive cancer, and is typically treated aggressively in all stages, usually starting

with an IV regimen of paclitaxel and carboplatin/cisplatin

Clinical

Development

Pipeline

• As of Q1 2012, Lumleian validated 81 assets in development for ovarian cancer

• The vast majority of the ovarian cancer pipeline is comprised of next-generation chemotherapeutic agents - DNA binders, microtubule destabilizers, and topoisomerase inhibitors are all validated classes of agents that dominate the

ovarian cancer pipeline, owing to the chemo-sensitive nature of this tumor

• A number of novel, targeted drug classes are being pursued, including anti-angiogenesis agents, kinase inhibitors,

tumor vaccines and immunotherapies - Numerous vascular-targeting agents are in development, including Roche’s Trebananib, Sanofi’s Aflibercept,Takeda’s

Ramucirumab, ImClone’s Vargatef, and Exelixis’ XL999

- Despite early positive data supporting Roche’s Avastin, disappointing Phase III survival data paired with significant side effects

have drawn into question whether anti-VEGF approaches will be a viable approach for ovarian cancer

- Several clinical-stage programs are directed at intracellular kinases involved in cell signaling, proliferation, and cell cycle

transcription factors, including Roche’s Tarceva and AstraZeneca’s Iressa; clinical trials are underway and it remains to be seen

if these will provide a significant advantage over existing chemotherapy regimens

Commercial

Landscape

• Systemic chemotherapy dominates the treatment paradigm for both early- and late-stage ovarian cancer

• Lilly’s Gemzar and Sanofi’s Taxotere are the key branded drugs for the treatment of both early- and late-stage

disease; additionally, BMS’ Taxol (paclitaxel) is still used despite the availability of generics

• Generic formulations of carboplatin, cisplatin, and doxorubicin are widely used in chemo regimens

Source: www.clinicaltrials.gov, Evaluate Pharma, BioPharm Insight, American Cancer Society: Cancer Facts and Figures 2011. Atlanta, Ga,

American Cancer Society, 2011, S.A. Cannistra, R.C. Bast Jr., J.S. Berek et al. Progress in the management of gynecologic cancer: consensus

summary statement. J Clin Oncol, 21 (Suppl. 10) (2003), pp. 129–132

Executive Summary: Ovarian cancer refers to a malignant growth that arises in the ovaries, most

often in the epithelial layer; this malignancy commonly goes undiagnosed until later stages,

resulting in aggressive chemotherapeutic treatment and a high mortality rate.

8

Source: www.clinicaltrials.gov, http://www.cancer.gov/cancertopics/types/ovarian, Company press releases, Cannistra SA, et al. Progress in the

management of gynecologic cancer: consensus summary statement. J Clin Oncol, 21:10 (2003), Lutz AM, et al. Early diagnosis of ovarian

carcinoma: is a solution in sight? Radiology 259:2(2011),

Key Questions

• Will agents currently in development provide distinct clinical benefits over the generic drugs that have become

entrenched as first-line therapies? - Novel formulations of established therapies, such as conjugation of chemotherapies to molecules which specifically target

tumor cells, may demonstrate greater efficacy while reducing overall toxicity; promising examples include EC-145 and

Abraxane

• Will mechanistic understanding of an agent’s effects in other tumor types be transferable to ovarian cancer?

• Can molecular diagnostic screening tools facilitate the selection and treatment of patients with specific

biochemical profiles? - To date, the kinase inhibitors which have revolutionized the treatment of other cancer indications have not affected

ovarian cancer treatment; this may change as the molecular basis of ovarian cancer becomes better understood, and the

selection of targeted agents becomes more disease-specific

- Established links between specific mutations and the therapeutic efficacy of targeted agents will lead to increased

sequencing of tumors as part of the treatment selection process

Lumleian’s

Perspective

• Ovarian cancer will remain an enduring unmet need, predominantly due to the lack of routine diagnostics with

the ability to detect the disease at an early stage - Although levels of tumor antigens such as CA-125 and OVA can be reliable indicators of therapy effectiveness and tumor

progression, these antigens are poor diagnostic tools for the detection of early-stage ovarian cancer

- Development of a reliable test for early-stage ovarian cancer could significantly change the treatment paradigm by shifting

the market in ovarian cancer treatment to different agents, and by increasing our understanding of ovarian cancer

development

• Due to the depth of the current development pipeline, the treatment paradigm is likely to evolve over the next

five to ten years, based on next-generation chemotherapeutics, as well as the probable launch of novel

approaches to treat the disease - Current approaches to treating ovarian cancer have severe side effects, adversely impacting the quality of life; novel

formulations of chemotherapies may increase efficacy while decreasing the toxicity of systemic treatments

- Insights from other cancer indications, such as the link between specific mutations and treatment efficacy, may inform

future ovarian cancer trials and treatments

• As evidenced by Roche’s Avastin, targeted therapies may encounter difficulty demonstrating a clinically

meaningful benefit in this patient population - Due to the late diagnosis of most ovarian cancers, these tumors are difficult to treat

- Significant advances in ovarian cancer treatment are most likely to come from development of diagnostics and better

understanding of ovarian tumor pathology

What are the key questions for 2012?

9

0

1

2

3

4

5

Level of Unmet Need Likelihood of Technical Success Regulatory Impetus Commerical Attractiveness Required Investment

Sources: Bharwani et al. Ovarian Cancer Management: the role of imaging and diagnostic challenges. Eur J Radiol (2011), www.seer.cancer.gov,

Schorge et al. SGO White Paper on ovarian cancer: etiology, screening and surveillance. Gynecologic Cncology 119:1 (2010)

Greenfield investment in clinical development for ovarian cancer is a high risk vs. moderate

rewards proposition; probability of technical success is low, and the market is small (though

growing), but there is high unmet need, potential Orphan Drug status and strong patient advocacy.

Average

Ovarian Cancer: Relative Attractiveness of Greenfield Investment in Late Stage Clinical Development

High

Low

Required

Investment

Phase III Investment

- Phase III trials require

at least a 1000 patient

trial

- Expensive monitoring

costs during trial

Commercial Spend

- Modest commercial

spend; highly data

driven

- Focused audience of

gyn-oncs and medical

oncologists

Phase IV Investment

- Limited requirements

(monitoring adverse

events)

- Ability to obtain

institutional

sponsorship of

additional trials

Level of

Unmet Need

Clinical Unmet Need

- High, few drugs are

approved

- Due to late diagnosis,

disease progresses rapidly,

leading to high mortality

Global Epidemiology

- 190,000 new diagnoses

and 125,000 deaths each

year worldwide

Disease Burden

- 21,550 new diagnoses/yr.

(US)

- 14,600 deaths/yr. (US)

- 177,578 women alive with

history of OC (US)

- Lifetime risk: 1.4 %

- Median age of diagnosis:

63 (US)

A Cause of Mortality

- Highly lethal

Commercial

Attractiveness

Market Size

- OC market is under $1B;

potential for dramatic growth

in aging populations

Global Epidemiology

- 190,000 new diagnoses &

125,000 deaths each year

worldwide

Market Expansion

- Limited opportunity due to

widespread use of low cost

generics

Generic Penetration

- Highly generic market

dominated by legacy chemo

agents (>95%)

Competitive Launches

- No significant launches

anticipated near-term

- Robust, competitive pipeline

(80+ agents)

Likelihood of

Technical Success

Poorly Understood Etiology

- Cell of origin is unclear

- Multiple etiology hypotheses:

incessant ovulation,

gonadotropin stimulation,

hormonal stimulation,

inflammation

Historic Ph. III /IIIB Failures

- Avastin (RHHBY)

- Phenoxodiol (Marshall

Edwards)

- Pemtumomab (Antisoma/

RHHBY)

- Pautipilone (NVS)

Statistical Challenges

- Late-stage diagnosis results in

more advanced and intractable

disease

Target Patient Populations

- Postmenopausal women

- Women with BRCA mutations

- Women with Lynch syndrome

Regulatory

Environment

Clinical Unmet Need

- High, few drugs are

approved

- Due to late diagnosis,

disease progresses rapidly,

leading to high mortality

Historical Precedents

- Ovarian Cancer National

Alliance

Advocacy

- Ovarian Cancer National

Alliance

- National Ovarian Cancer

Coalition

- Ovarian Cancer Research

Fund

10

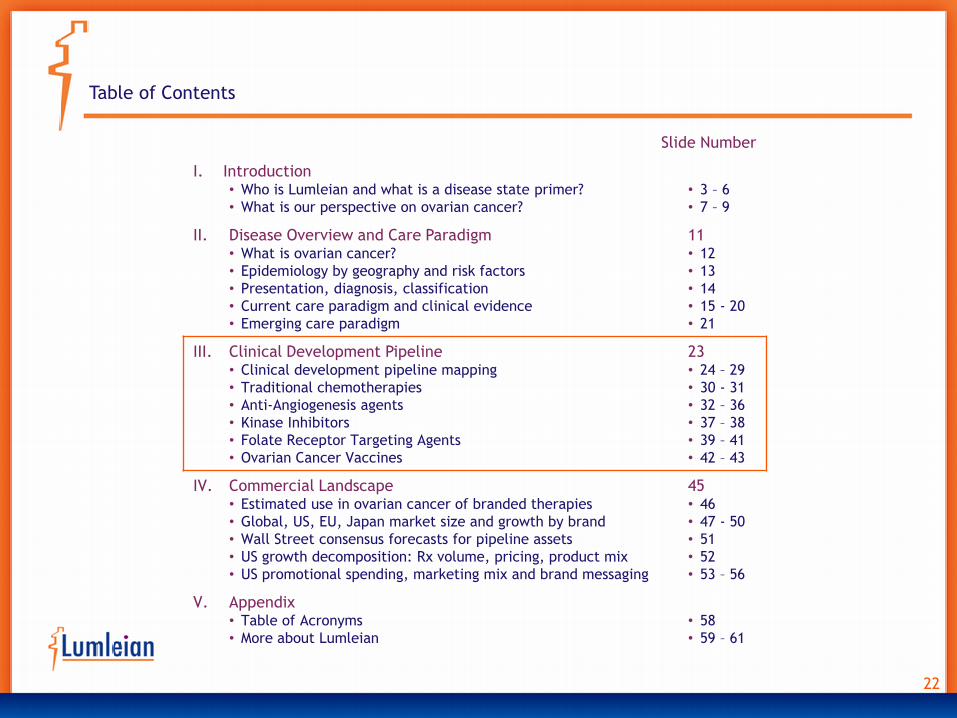

Table of Contents

Slide Number

I. Introduction • Who is Lumleian and what is a disease state primer?

• What is our perspective on ovarian cancer?

• 3 – 6

• 7 – 9

II. Disease Overview and Care Paradigm • What is ovarian cancer?

• Epidemiology by geography and risk factors

• Presentation, diagnosis, classification

• Current care paradigm and clinical evidence

• Emerging care paradigm

11 • 12

• 13

• 14

• 15 - 20

• 21

III. Clinical Development Pipeline • Clinical development pipeline mapping

• Traditional chemotherapies

• Anti-Angiogenesis agents

• Kinase Inhibitors

• Folate Receptor Targeting Agents

• Ovarian Cancer Vaccines

23 • 24 – 29

• 30 - 31

• 32 – 36

• 37 – 38

• 39 – 41

• 42 – 43

IV. Commercial Landscape • Estimated use in ovarian cancer of branded therapies

• Global, US, EU, Japan market size and growth by brand

• Wall Street consensus forecasts for pipeline assets

• US growth decomposition: Rx volume, pricing, product mix

• US promotional spending, marketing mix and brand messaging

45 • 46

• 47 - 50

• 51

• 52

• 53 – 56

V. Appendix • Table of Acronyms

• More about Lumleian

• 58

• 59 – 61

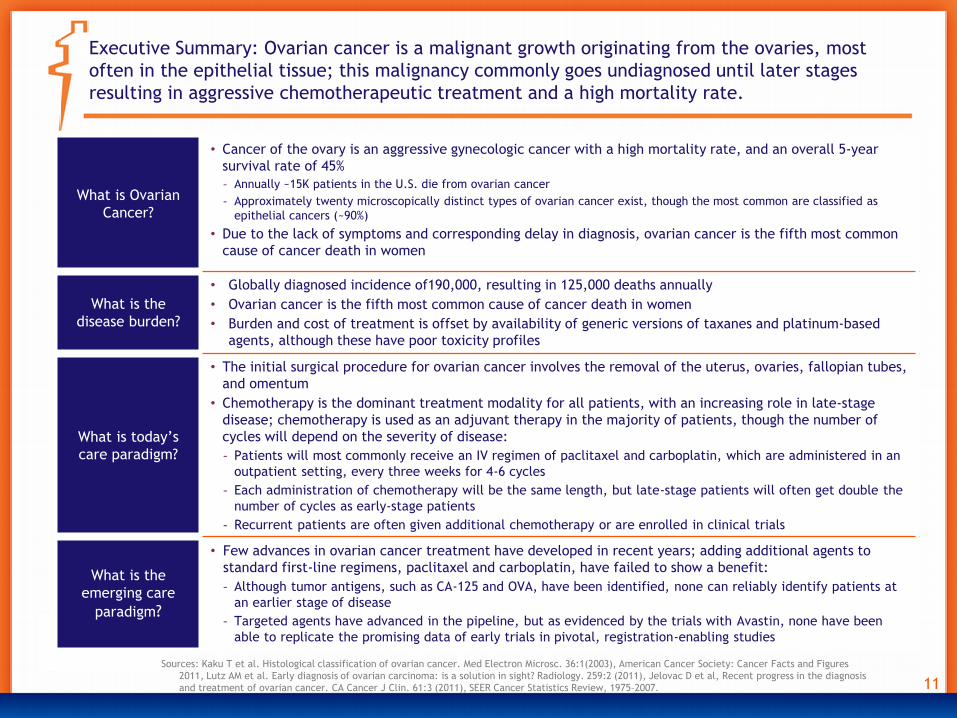

11

What is Ovarian

Cancer?

• Cancer of the ovary is an aggressive gynecologic cancer with a high mortality rate, and an overall 5-year

survival rate of 45%

- Annually ~15K patients in the U.S. die from ovarian cancer

- Approximately twenty microscopically distinct types of ovarian cancer exist, though the most common are classified as

epithelial cancers (~90%)

• Due to the lack of symptoms and corresponding delay in diagnosis, ovarian cancer is the fifth most common

cause of cancer death in women

What is the

disease burden?

• Globally diagnosed incidence of190,000, resulting in 125,000 deaths annually

• Ovarian cancer is the fifth most common cause of cancer death in women

• Burden and cost of treatment is offset by availability of generic versions of taxanes and platinum-based

agents, although these have poor toxicity profiles

What is today’s

care paradigm?

• The initial surgical procedure for ovarian cancer involves the removal of the uterus, ovaries, fallopian tubes,

and omentum

• Chemotherapy is the dominant treatment modality for all patients, with an increasing role in late-stage

disease; chemotherapy is used as an adjuvant therapy in the majority of patients, though the number of

cycles will depend on the severity of disease:

- Patients will most commonly receive an IV regimen of paclitaxel and carboplatin, which are administered in an

outpatient setting, every three weeks for 4-6 cycles

- Each administration of chemotherapy will be the same length, but late-stage patients will often get double the

number of cycles as early-stage patients

- Recurrent patients are often given additional chemotherapy or are enrolled in clinical trials

What is the

emerging care

paradigm?

• Few advances in ovarian cancer treatment have developed in recent years; adding additional agents to

standard first-line regimens, paclitaxel and carboplatin, have failed to show a benefit:

- Although tumor antigens, such as CA-125 and OVA, have been identified, none can reliably identify patients at

an earlier stage of disease

- Targeted agents have advanced in the pipeline, but as evidenced by the trials with Avastin, none have been

able to replicate the promising data of early trials in pivotal, registration-enabling studies

Sources: Kaku T et al. Histological classification of ovarian cancer. Med Electron Microsc. 36:1(2003), American Cancer Society: Cancer Facts and Figures

2011, Lutz AM et al. Early diagnosis of ovarian carcinoma: is a solution in sight? Radiology. 259:2 (2011), Jelovac D et al, Recent progress in the diagnosis

and treatment of ovarian cancer. CA Cancer J Clin. 61:3 (2011), SEER Cancer Statistics Review, 1975–2007.

Executive Summary: Ovarian cancer is a malignant growth originating from the ovaries, most

often in the epithelial tissue; this malignancy commonly goes undiagnosed until later stages

resulting in aggressive chemotherapeutic treatment and a high mortality rate.

12

Description

• Ovarian cancer is a malignant growth that arises in the ovaries, most often

from epithelial tissue

• Most ovarian cancer patients are post-menopausal women

• Ovarian cancer is subdivided into epithelial cancers, germ cell tumors, and

tumors of low malignant potential; the epithelial subtype is the most

dominant (90% of cases)

Etiology & Risk

Factors

• Women who have BRCA1/2 mutations or with hereditary non-polyposis

colorectal cancer have the highest risk, but account for only 10% of patients

• Risk is inversely proportional to number of lifetime ovulations; pregnancies,

lactation, oral contraceptives, tubal ligation and hysterectomy decrease risk

• Nulliparity, early menarche/ late menopause, hormone replacement therapy

and endometriosis increase risk

Diagnosis &

Symptom

Progression

• Screening tests, such as those which exist for the CA-125 and OVA-1 antigens,

do not improve outcome

• Early symptoms are non-specific, resulting in late-stage diagnosis; tumors

spread to the pelvis and upper abdomen, cause pelvic/abdominal pain,

swelling; weight loss, pain, bowel or ureteral obstruction are symptoms of

advanced disease

• Diagnosis: palpation of adnexal mass during pelvic examination, ultrasound, CA

125 & OVA-1 assessment, laparoscopy/laparotomy

Disease

Burden

• Estimated new cases: 21,990 (US, 2011)

• Estimated deaths: 15,460 (US, 2011)

• Lifetime incidence: 1 in 72 (1.39%); lifetime risk: 1 in 96 (1.04%) (US)

• Median age at diagnosis: 63 years. Age-adjusted incidence rate 12.9/100,000

Sources: Kaku T et al. Histological classification of ovarian cancer. Med Electron Microsc. 36:1(2003), American Cancer Society: Cancer Facts and Figures

2011, Lutz AM et al. Early diagnosis of ovarian carcinoma: is a solution in sight? Radiology. 259:2 (2011), Jelovac D et al, Recent progress in the diagnosis

and treatment of ovarian cancer. CA Cancer J Clin. 61:3 (2011), SEER Cancer Statistics Review, 1975–2007.

What is ovarian cancer?

Yes: Women No

2. Is ovarian cancer a primary cause of mortality?

7. Where is ovarian cancer treated?

Yes No

Out

Patient

Inpatient

Hospital

Long Term

Care

Symptom

Relief

Disease

Treatment

Disease

Cure

3. Is ovarian cancer an acute or chronic disease?

Acute Chronic

6. Which specialties treat ovarian cancer?

5. What is ovarian cancer’s treatment goal?

8. Who pays for ovarian cancer (Rx)?

3rd party Cash CMS

Gynecologist Gyn-

Oncologist

Medical

Oncologist

4. Is ovarian cancer a communicable disease?

Yes No

Yes No

9. Does ovarian cancer impact a special

population?

1. Is ovarian cancer etiology well understood?

13

Sources: www.seer.cancer.gov, GloboCan 2008: World Cancer Report 2008, IARC 2010, PDQ Cancer Information Summary, NCI. Genetics of Breast

and Ovarian Cancer

Global ovarian cancer incidence was 190K in 2010, with an estimated 22K new cases in the US;

the incident patient population will grow at a rate consistent with the aging population.

• BRCA1 or BRCA2 mutations (increases lifetime risk from 1.4%

in general population to 15-40% with a harmful mutation of

BRCA 1/2)

• Hereditary non-polyposis colorectal cancer (increases lifetime

risk from 1.4% to 10%)

High-Risk Factors Risk Factors

• Post-menopausal women are more likely to develop OC

• Risk is inversely proportional to number of lifetime

ovulations: pregnancies, lactation, oral contraceptives, tubal

ligation and hysterectomy decrease risk; nulliparity, early

menarche/late menopause and hormone replacement therapy

increase risk

• Endometriosis (increased inflammation) increases the risk

• 190,000 new diagnoses each year

• 125,000 deaths each year

Global Incidence

• Because 50% of ovarian cancer cases occur in women over the

age of 65, the incident patient population will grow at a rate

consistent with the aging population

US Incidence

• 21,990 new diagnoses each year

• 15,460 deaths each year

• Lifetime risk 1.4 %

• Median age of diagnosis: 63

• Age-adjusted incidence rate: 12.9 per 100,000 women

• 177, 578 women alive with a history of OC

14

Clinicians segment patients based initially on clinical stage, though tumor grade is also

considered to inform treatment; more than half of cases are diagnosed in Stage III or IV, which

contributes to the relatively high mortality rate.

Stage I Stage II Stage III Stage IV

% of presentations • 15% • 17% • 69%

Dia

gnosi

s Criteria

• Disease confined to

ovaries

• Dissemination confined

to pelvis

• Dissemination to

peritoneum

• Dissemination to liver

parenchyma, lung,

pleura, other sites

Presenting

Symptoms

• Non-specific

symptoms

• Pelvic pain • Abdominal pain;

Swelling

• Weight loss; Pain;

Bowel or ureteral

obstruction

Treatm

ent

1st line

• Debulking surgery, including, for well-differentiated Stage I & II tumors, total abdominal hysterectomy and

bilateral salpingo-oophorectomy with omentectomy for Stage III & IV disease

• The primary chemotherapy regimen is IV paclitaxel/carboplatin that is administered as adjuvant on an

outpatient basis once every three weeks, for a total of 4-6 cycles

Outcome of 1rst line

therapy

determines 2nd and

3rd line therapy

• Platinum-resistant—progressive disease during platinum therapy or within 6 months of last platinum

treatment; these patients can only expect a13% to 19% chance of response to further chemotherapy

- Platinum-resistant patients are treated with paclitaxel, pegylated liposomal doxirubicin, gemcitabine,

topotegan, cyclophosphamide or other non-platinum agents in 2nd and 3rd line therapy

• Platinum partially sensitive—progressive disease 6–12 months from last platinum therapy; patients can

expect to have a 27% chance of response to further chemotherapy

- Platinum-sensitive patients are treated with a combination of carboplatin and a non-platinum agent, such as

paclitaxel, gemcitabine and pegylated liposomal doxirubicin

• Patients with advanced disease that recur often cycle through various chemotherapy regimens and may be

enrolled in clinical trials

5 year survival rate • 93.8% • 72.8% • 28.2%

Sources: http://www.cancer.gov/cancertopics/types/ovarian, Kaku T et al. Histological classification of ovarian cancer. Med Electron Microsc.

36:1(2003), American Cancer Society: Cancer Facts and Figures 2011

15

Carboplatin

(Paraplat, Paraplatin, Paraplatin-AQ)

Cisplatin

(Platinol, Platinol-AQ)

MoA • DNA binder/crosslinking agent – Platinum • DNA binder/crosslinking agent – Platinum

Sponsor • Widely available as generic

• Paraplatin is sold by BMS

• Widely available as generic

• Platinol is sold by BMS

Formulation

(Generic)

• Aqueous solution • Aqueous solution

Dosing • 300-360 mg/m2 IV every 4 weeks or target AUC 5-7.5

every 3 weeks (4-10 cycles)

• May be administered IP in ovarian cancer; a typical

regimen for intra-peritoneal infusion is 200-650

mg/m2

• IV; 75 mg/m2

• May be administered IP in ovarian cancer

Indications • OC that has recurred after cisplatin, or is advanced

and has never been treated; also used for palliative

treatment of OC that has recurred after earlier

chemotherapy

• OC that is advanced, or has metastasized in patients

whose disease has not gotten better with other types

of treatment or chemotherapy

Adverse Events

(Discontinuation)

• Severe side-effects include infusion reactions,

gastrointestinal toxicity (nausea/vomiting),

nephrotoxicity, myelo-suppression, peripheral

sensory neuropathy

• Severe side-effects include infusion reactions,

gastrointestinal toxicity (nausea/vomiting),

nephrotoxicity, myelo-suppression, peripheral

sensory neuropathy

Lumleian

Commentary

• Carboplatin is the preferred platinum agent to cisplatin for platinum-sensitive ovarian cancer, owing to the

belief that carboplatin is significantly less toxic, although does not confer an efficacy advantage; this

demonstrates that an improved side effect profile can govern uptake as standard of care

Sources: www.carboplatin.org, www.cisplatin.org, Sakaeda et al., Adverse event profiles of platinum agents: data mining of the public version of

the FDA adverse event reporting system, AERS, and reproducibility of clinical observations. Int J Med Sci 8:6 (2011)

The first-line, post-surgical chemotherapy regimen for ovarian cancer consists of a platinum-

based agent, generic carboplatin or cisplatin, usually in combination with generic paclitaxel; in

most markets, this combination is considered the SoC therapy.

16

Paclitaxel

(Taxol)

MoA • Microtubule inhibitor/tubulin binder

Sponsor • Paclitaxel is sold by BMS

Formulation

(Generic)

• Solution for injection

Dosing • For previously untreated patients one of the following recommended regimens may be given every 3 weeks: 1)

over 3 hours at a dose of 175 mg/m2 followed by cisplatin at a dose of 75 mg/m2 or 2) over 24 hours at a dose of

135 mg/m2 followed by cisplatin at a dose of 75 mg/m2

• In patients previously treated with chemotherapy, paclitaxel injection has been used at several doses and

schedules; although, the optimal regimen is not yet clear, the current recommended regimen is injection 135

mg/m2 or 175 mg/m2 administered intravenously over 3 hours every 3 weeks

Indications • Frequently used in combination with platinum therapy in platinum-sensitive recurrences

• Single-agent use in platinum-refractory or platinum-resistant ovarian cancer

Adverse Events

(Discontinuations)

• Severe side-effects include myelosuppression, hypersensitivity, neurotoxicity, nausea/vomiting,

myalgia/arthralgia, diarrhea, asthenia, peripheral neuropathy

Lumleian

Commentary

• Widespread availability of low cost generic versions of Taxol have supported adoption into first-line regimens in

the majority of markets, despite conflicting data supporting use first-line

• Novel, solvent-free formulations of paclitaxel are in Phase III clinical trial in ovarian cancer: Paclical (Oasmia

Pharmaceutical) is nano particle-bound paclitaxel, Abraxane (Abraxis/Celgene) is albumin-bound paclitaxel,

and Opaxio (paclitaxel poliglumex; Cell Therapeutics) is amino acid-bound paclitaxel

Sources: www.cancer.gov, Taxol drug label, www.clinicaltrials.gov

The microtubule inhibitor, Taxol, continues to be used as standard-of-care; however, data from

the ICON3 trial has showed that the addition of Taxol to platinum-based monotherapy does not

confer a survival benefit.

17

Doxorubicin Hydrochloride

(Adriamycin, Evacet/DOXIL/Dox-SL/LipoDox liposomes)

MoA • Microtubule inhibitor/tubulin binder – Anthracycline

Sponsor • Liposomal formulation (DOXIL) sold by Johnson and Johnson (Centocor)

Formulation

(Generic)

• Powder must be dissolved for IV administration (Adriamycin)

• Liposomal formulation approved by FDA in 1995, solution (DOXIL)

Dosing • Liposomal formulation (DOXIL): 50 mg/m2 IV every 4 weeks for 4 courses minimum

Indications • Liposomal formulation (DOXIL): single-agent use in platinum-refractory or platinum-resistant OC

• Frequently used in combination with platinum therapy in platinum-sensitive recurrences

Adverse Events

(Discontinuations)

• Severe side-effects include infusion reactions, myelo-suppression, cardio-toxicity, Hand-Foot syndrome

Lumleian

Commentary

• Liposomal doxorubicin alleviates the cardio-toxicity and neurotoxicity associated with doxorubicin and

provides a longer half-life of the molecule, although the Doxil provides only a modest benefit (12%

response rates; 11-month median overall survival) in recurrent disease setting

• Data from the ICON 5 trial demonstrated that adding a third cytotoxic agent in the first-line setting did not

improve progression-free survival, limiting the agent’s ability to penetrate earlier treatment lines

Sources: DOXIL drug label, Journal of Clinical Oncology, 2006 ASCO Annual Meeting Proceedings Part I. Vol 24, No. 18S, 2006

The anthracycline, liposomal doxorubicin, is a component of regimens targeting patients with

platinum-resistant disease, although clinicians will often re-treat with the initial combination

after a first relapse before moving on to second-line agents.

18

Cyclophosphamide

(Clafen/Cytoxan/Neosar)

MoA • DNA binder/alkylating agent

Sponsor • Powder for injection sold by Baxter Healthcare

• Tablets for oral use sold by Roxane

Formulation

(Generic)

• Powder for injection

• Tablets for oral use

Dosing • When used as the only oncolytic drug therapy, the initial course of cytoxan for patients with no hematologic

deficiency usually consists of 40 to 50 mg/kg given intravenously in divided doses over a period of 2 to 5 days;

other intravenous regimens include 10 to 15 mg/kg given every 7 to 10 days or 3 to 5 mg/kg twice weekly

• Oral cytoxan dosing is usually in the range of 1 to 5 mg/kg/day for both initial and maintenance dosing

Indications • Recurrent OC

• Frequently used in combination with platinum therapy in platinum-sensitive recurrences

Adverse Events

(Discontinuations)

• Severe side-effects include myelosuppression, gastrointestinal toxicity, pulmonary toxicity, cardiotoxicity,

hypersensitivity and secondary neoplasias

Lumleian

Commentary

• Cyclophosphamide is commonly used in relapse patients although other agents, such as liposomal doxorubicin,

are preferable due to toxicity issues, leading to a decline in use over the past years

Sources: www.fda.gov, www.drugs.com, Cytoxan prescribing information

Cyclophosphamide once was a core component of first-line regimen CAP, but has now been

supplanted by the more effective taxanes.

19

Topotecan hydrochloride

(Hycamtin)

MoA • Topoisomerase inhibitor

Sponsor • GSK

Formulation

(Generic)

• Solution for injection

Dosing • 1.5 mg/m2 by intravenous infusion over 30 minutes daily for 5 consecutive days, starting on day 1 of a 21 day

course. In the absence of tumor progression, a minimum of 4 courses is recommended because tumor response

may be delayed

Indications • Single-agent use in platinum-refractory or platinum-resistant OC

Adverse Events

(Discontinuations)

• Severe side-effects include myelosuppression, nausea, vomiting, alopecia and asthenia

Lumleian

Commentary

• Hycamtin’s utility is further constrained in the second-line setting, due to the fact that recurrent patients

who have Hycamtin-resistant or Paclitaxel-resistant disease have little chance of responding to the other

drug

• Similarly, the negative results of the ICON 5 trial, paired with a poor toxicity profile, has relegated

Hycamtin to a third-line option for most patients

Sources: www.cancer.gov, www.fda.gov, Hycamtin prescribing information

Severe hematological toxicities are observed with Hycamtin when it is used as triple therapy in

combination with paclitaxel and carboplatin, limiting the agent’s ability to penetrate the first-

line setting.

20

Gemcitabine Hydrochloride

(Gemzar)

MoA • Antimetabolite/pyrimidine analog

Sponsor • Generic formulations widely available since Q4 2010

• Eli Lilly

Formulation

(Generic)

• Solution for injection

Dosing • Intravenously at a dose of 1000 mg/m2 over 30 minutes on Days 1 and 8 of each 21-day cycle

Indications • Single-agent use in platinum-refractory or platinum-resistant OC

• Frequently used in combination with platinum therapy in platinum-sensitive recurrences

• Responses have been observed in paclitaxel-refractory OC

Adverse Events

(Discontinuations)

• Severe side-effects include myelosuppression, cardiotoxicity, vascular toxicity, hepatotoxicity, pulmonary

toxicity, renal toxicity

Lumleian

Commentary

• As with other agents, Gemzar failed to demonstrate an efficacy benefit as first-line triple therapy in the

ICON 5 trial

• However, Gemzar is well tolerated and produces relatively mild side effects, such as minor

myelosuppression, so the agent is used frequently as mono-therapy in the second-line setting

Sources: www.drugs.com, Gemzar drug label

Lilly’s Gemzar has been approved for ovarian cancer for patients that have had a relapse of at

least six months after failure of a platinum-based regimen; however, the agent is now subject to

generic competition after loss of patent exclusivity at the end of 2010.

21

• Ovarian cancer has a poor treatment response profile and high mortality, primarily due to lack of specific

symptoms and the resulting late-stage diagnosis

• Numerous blood markers and protein profiles are being evaluated, though success is not expected in the

near-term

- Markers, such as CA125 and OVA, though performing well as indicators of treatment success and disease

progression, do not achieve the level of sensitivity that would be required for a molecular diagnostic tool in

the clinic

- Antigens which are being tested for early-stage diagnosis of ovarian cancer include SPAG9, OY-TES-1, Piwil2,

LAGE-1, NY-ESO-1, Sp17, SSX, AKAP-3, SCP-1

• Treatment selection in late stage ovarian cancer would be significantly improved by the discovery and

development of biomarkers predictive of tumor resistance to platinum-based regimens

Sources: www.clinicaltrials.gov, EvaluatePharma, Lutz AM, et al. Early diagnosis of ovarian carcinoma: is a solution in sight? Radiology

259:2(2011), Mirandola L et al., Cancer test antigens: novel biomarkers and targetable proteins for ovarian cancer. Int Rev Immunol. 30:2-3

(2011)

None of the late-stage assets are likely to transform the treatment paradigm; the most likely

changes will be in platinum-resistant patients, with only incremental improvements in efficacy.

Future

Diagnosis

Future

Treatment

• Novel formulations of established chemotherapies, such as conjugation of chemotherapies to molecules

which specifically target tumor cells, may demonstrate greater efficacy while reducing overall toxicity;

promising examples include EC-145 and Abraxane

• In addition to new generation cytotoxic agents, novel targeted therapies are undergoing clinical testing;

late-phase (III-IV) emerging therapies include new-generation topoisomerase inhibitors, DNA binders and

microtubule inhibitors as well as immunotherapy, epigenetic therapy, vascular-targeting therapy and

kinase inhibitors

- Insights from other cancer indications, such as the link between specific mutations and treatment efficacy,

may inform future ovarian cancer trials and treatments

- Established links between specific mutations and the therapeutic efficacy of targeted agents will lead to

increased sequencing of tumors as part of the treatment selection process

• Combination therapy, personalized medicine, prediction and monitoring of treatment responses by

biomarkers are foreseen as part of the future standard of care

22

Table of Contents

Slide Number

I. Introduction • Who is Lumleian and what is a disease state primer?

• What is our perspective on ovarian cancer?

• 3 – 6

• 7 – 9

II. Disease Overview and Care Paradigm • What is ovarian cancer?

• Epidemiology by geography and risk factors

• Presentation, diagnosis, classification

• Current care paradigm and clinical evidence

• Emerging care paradigm

11 • 12

• 13

• 14

• 15 - 20

• 21

III. Clinical Development Pipeline • Clinical development pipeline mapping

• Traditional chemotherapies

• Anti-Angiogenesis agents

• Kinase Inhibitors

• Folate Receptor Targeting Agents

• Ovarian Cancer Vaccines

23 • 24 – 29

• 30 - 31

• 32 – 36

• 37 – 38

• 39 – 41

• 42 – 43

IV. Commercial Landscape • Estimated use in ovarian cancer of branded therapies

• Global, US, EU, Japan market size and growth by brand

• Wall Street consensus forecasts for pipeline assets

• US growth decomposition: Rx volume, pricing, product mix

• US promotional spending, marketing mix and brand messaging

45 • 46

• 47 - 50

• 51

• 52

• 53 – 56

V. Appendix • Table of Acronyms

• More about Lumleian

• 58

• 59 – 61

23

Source: Lumleian perspective

Executive Summary: Clinical Development Pipeline

What is in the

industry’s

clinical

development

pipeline?

• As of Q1 2012, Lumleian validated 81 assets in development for ovarian cancer

• The vast majority of the ovarian cancer pipeline is comprised of next-generation as well as novel

chemotherapeutic agents

- DNA binders, microtubule destabilizers, and topoisomerase inhibitors are all validated classes of agents that

dominate the ovarian cancer pipeline, owing to the chemo-sensitive nature of this tumor

• A number of novel, targeted drug classes are being pursued, including monoclonal antibodies, anti-

vascular approaches, agents targeting kinases, and immunotherapy

- Numerous anti-angiogenesis agents are in development, including Roche’s Trebananib, Sanofi’s

Aflibercept,Takeda’s Ramucirumab, ImClone’s Vargatef, and Exelixis’ XL999

- Despite early positive data supporting Roche’s Avastin, disappointing Phase III survival data paired with

significant side effects have drawn into question whether anti-VEGF approaches will be a viable approach for

ovarian cancer

- Several clinical-stage programs are directed at intracellular kinases involved in cell signaling, proliferation,

and cell cycle transcription factors

What is the

evidence for late

stage assets?

• Although the overall pipeline contains numerous assets in development, the vast majority are at a pre-

proof of concept stage in ovarian cancer and lack data showing tumor-specific efficacy

• Roche’s Avastin has been moderately successful in targeting the VEGF pathway in other oncology

indications; Phase III data has demonstrated minimal benefit over existing therapy, with significant

adverse effects

- Assets with any proof-of-concept data are likely to become used following paclitaxel/carboplatin, as few

agents provide any benefit in this high unmet need setting

24

Sources: : Lumleian perspective

Drug sponsors have numerous entry points in advanced ovarian cancer (Stage IIb-IV), when

developing a clinical development strategic plan; although each market segment presents

unique opportunities, each segment also poses unique development issues.

Neoadjuvant

Adjuvant

(First-Line)

Active Comparator Opportunity Key Issues

• Paclitaxel + Carboplatin

• Standard of care provides limited

tumor reduction; opportunity to

increase magnitude of response

• Ability to obtain institutional

sponsorship for such a study

• Neoadjuvant protocols are only

applicable to a subset of patients

with Stage III-IV disease

• Chemo generally administered for

only 3 cycles; limited duration of

treatment

• Paclitaxel + Carboplatin

• Given the limited survival benefit,

new agents may be tested first-line

by showing a benefit in addition to

SOC chemotherapy

• Efficacy benefit would result in

rapid uptake by clinicians

• Avastin was unable to improve PFS

in large, pivotal trial, despite

promising data

• ICON 5 trial showed that adding a

third chemo to SOC did not improve

SOC

Relapse

(Second-Line) • Gemzar, Doxorubicin,

Cyclophosphamide

• Relapse and treatment refractory

rates remain very high in this tumor

• Limited efficacy of available

second-line agents

• Ability to gain approval based on

PFS endpoint

• Difficult population to treat;

median progression-free survival of

3-5 months

• Challenging to differentiate

resistant and refractory patients

Patient Segment

Novel agents have an opportunity to penetrate the first-line treatment setting initially;

however, no agents have been able to demonstrate a significant improvement in overall

survival in pivotal trials to date

25

OC Pipeline: Current (N= 81) Phase III

(N = 16)

Phase II

(N = 42)

Phase I

(N = 23)

DNA binders (6)

Alkylating agent (4) 1 2 1

DNA intercalation agent (1) - 1 -

Hypomethylation agent (1) - 1 -

Apoptosis Induction (10)

Antibody-mediated (1) - - 1

Antimetabolite (1) - 1 -

Gene therapy (1) - 1 -

Lytic Peptide (1) - 1 -

PARP Inhibitor (3) - 3 -

Other (3) 1 2 -

Mitosis Disruptors (14)

G2 disrupter (2) - 1 1

HDAC inhibitor (1) - - 1

Microtubule Disruptor (5) 2 1 2

Topoisomerase Inhibitor (6) 2 2 2

Anti-Angiogenesis agents (11)

Angiopoetin antagonist (1) 1 - -

Anti-PIGF (1) - - 1

VEGFR inhibitor (5) 4 1 -

Other (4) 1 2 1

Kinase Inhibitors (11) Akt, Aurora A Kinase, BRAF, c-MET, EGFR,

Her2, IGF1R, BDGFR, Ras 1 9 2

Immunomodulation (7) T-cell, B-cell, NK cell activation - 5 2

Vaccines (12) 1 8 3

Folate-Targeting Agents (3) 2 - 1

Other (6) HSP inhibitors, viral therapy, etc. - 1 5

Sources: www.clinicaltrials.gov, EvaluatePharma

The ovarian cancer pipeline is comprised of next-generation cytotoxic agents with potential for

incremental improvement, as well as novel, targeted agents with transformational potential,

but which require validation, as little is known about signaling mechanisms in ovarian cancer.

26

Sources: Lumleian estimates based on publicly available data from bio-pharmaceutical companies (financial statements, investor presentations,

pipeline presentations, analyst day transcripts); 3rd party equity research reports; Bio-Pharma Insight; Clinical Trials.gov; CenterWatch

As of Q1 Lumleian validated 81 assets in ‘active’ clinical development for OC: 23 in Phase III, 42

in Phase II, and 16 in Phase I; leading oncology companies hold multiple assets, while the

pipeline is dominated by smaller biotech companies with an interest in cancer.

OC Assets in ‘Active’ Clinical Development

Phase III (N = 23) Phase II (N =42) Phase I (N = 16)

1 1 1 1 1 1 1

3

1

5 2

1 1

1 1 1

1

1

5

1

1

1

1

2

1 1

1 2

0

5

10

27

Traditional chemotherapeutics, such as mitosis disruptors, apoptosis induction agents and DNA

binders are under investigation due to the chemo-sensitive nature of ovarian cancer; however,

pipeline agents are likely to provide only incremental improvement over current SoC.

Mechanism of Action Phase III (N = 6) Phase II (N = 16) Phase I (N = 8)

DN

A

bin

ders

(10)

Alkylating agent (4) • Eloxatine (SNY) • Irofulven

• Prolindac (ACCP)

• Picoplatin (PARD)

DNA intercalation agent (1) • Zoptarelin Doxorubicin (AEZS)

Hypomethylation agent (1) • Dacogen (ESALY)

Apopto

sis

Inducti

on (

10)

Antibody-mediated (1) • GT-Mab 2.5 GEX (Glycotope)

Antimetabolite (1) • Alimta (LLY)

Gene therapy (1) • BC-819 (BICL)

Lytic Peptide (1) • EP-100 (Esperance

Pharmaceuticals)

PARP Inhibitor (3)

• Iniparib (SNY) • Olaparib (AZN) • Rucaparib (CLVS)

Other (3) • Canfosfamide (TELK) • Tasisulam (LLY)

• Tirapazamine

Mit

osi

s D

isru

pto

rs

(14)

G2 disrupter (2) • Ispinesib (CYTK) • CBP-501 (CanBas)

HDAC inhibitor (1) • Belinostat (TPTGF)

Microtubule Disruptor (5) • Opaxio (CTIC) • Paclical (Oasmia)

• Abraxane (CELG) • Lorvotuzumab (IMGN) • SAR-566658 (IMGN)

Topoisomerase Inhibitor (6)

• Hycamtin (GSK) • Karenitecin (BioNumerik)

• Quinamed (ChemGenex) • Vosaroxin (SNSS)

• Brakiva (TLON) • Pegylated Irinotecan (PFE)

Sources: www.clinicaltrials.gov, EvaluatePharma

28

Mechanism of Action Phase III (N = 6) Phase II (N = 3) Phase I (N = 2)

Anti

-angio

genesi

s agents

(11)

Angiopoetin

Antagonist (1)

• Trebananib (Takeda

Pharmaceuticals)

Anti-PIGF (1)

• RO5323441 (RHHBY)

VEGF inhibitors (5)

• Votrient (GSK) • Zaltrap (SNY) • Avastin (RHBY) • Vargatef (Boehringer Ingelheim)

• Ramucirumab (LLY)

Other (4)

• Thalomid (CELG) • Panzem (ENMD) • Zybrestat (OXGN)

• Vadimezan (NVS)

Anti-angiogenesis agents target several pathways involved in vascular development; VEGF

pathway inhibition dominates the anti-angiogenesis landscape.

Sources: www.clinicaltrials.gov, EvaluatePharma

29

Numerous kinase-targeting strategies are being pursued in treatment of ovarian cancer, in hopes

of replicating the dramatic success of some kinase inhibitors in different oncology indications;

however, to date kinase inhibition has not demonstrated significant improvement on SoC.

Mechanism of Action Phase III (N = 1) Phase II (N = 8) Phase I (N = 2)

Kin

ase

Inhib

itors

(11)

Akt inhibitors (1) • VQD-002

Aurora A Kinase inhibitors (1) • Alisertib (Takeda Pharmaceuticals)

BRAF inhibitors (2) • Nexavar (BAYN)

• Selumetinib (AZN)

c-MET inhibitors (1) • Cabozantinib (EXEL)

EGFR inhibitors (2) • Tarceva (RHHBY) • Erbitux (BMY/LLY/MRK)

Her2 inhibitors (1) • Omnitarg (RHHBY)

IGF-1R inhibitors (1) • Linsitinib (Astellas Pharma, Inc.)

PDGFR inhibitors (1) • Olaratumab (LLY)

Ras inhibitors (1) • TLN-4601 (TLN)

Sources: www.clinicaltrials.gov, EvaluatePharma

30 Sources: Bio-Pharma Insight; Clinical Trials.gov. http://chemweb.bham.ac.uk

Telcyta and Eloxitine are two of the most advanced traditional chemotherapeutics attempting

to provide improvements over existing standard of care, however, the currently available low-

cost and well-know therapies present a significant hurdle to commercial success.

Physiology • Unimpeded DNA synthesis and segregation is

required for cell division

Pathophysiology • Cancer cells divide at a faster rate than normal

cells and fail to respond to normal mitosis

inhibition signals

Hypothesized

Mechanism

• Interference with DNA structure leads to inhibition

of DNA and protein synthesis, stopping cell division

and even causing cell death

• DNA binding is a well-established MOA for cancer

treatment, and is the basis of many traditional

chemotherapies

• Impeding other mechanisms of mitosis, such as

disruption of microtubules or inhibition of

topoisomerase are other mechanisms of traditional

chemotherapy

Pipeline

2 doxorubicin molecules

bound to DNA

Phase III (6) • Eloxatine (SNY) • Telcyta (TELK)

• Paclical (Oasmia) • Hycamtin (GSK)

• Karenitecin (BioNumerik) • Opaxio (CTIC)

Phase II (16) • Irofulven • Prolindao (ACCP) • Zoptarelin Doxiorubicin (AEZS) • Dacogen (ESALY) • Alimta (LLY)

• EP-100 (Esperance) • Iniparib (SNY) • Olapanib (AZN) • Rucaparib (CLVS) • Tasisulam (LLY)

• BC-819 (BICL) • Tirapazmine, Ispinesib (CYTK) • Abraxane (CELG) • Quinamed (ChemGenex) • Vosaroxin (SNSS)

Phase I (8) • Picoplatin (PARD) • GT-Mab 2.5 GEX (Glycotope)

• CBP-501 (CanBas) • Belinostat (TPTGF) • Lorvotuzumab (IMGN)

• SAR-566658 (IMGN) • Brakiva (TLON), Pegylated • Irinotecan (PFE)

31

Sources:www.clinicaltrials.gov, Vergote, I et al. Randomized Phase III study of canfosfamide in combination with pegylated liposomal doxorubicin

compared with pegylated liposomal doxorubicin alone in platinum-resistant ovarian cancer. Int J Gynecol Cancer. 20:5 (2010)

Telcyta/Canfosfamide (TELK), a glutathione s-transferase-activated cytotoxic pro-drug, has

shown promise by increasing survival with the drawback of accompanied increased toxicity;

further clinical evaluation is expected.

Telcyta (Canfosfamide)

Efficacy: Phase III results of combination study of canfosfamide + pegylated liposomal doxorubicin (PLD) published in 2010:

• PFS Canfosfamide + PLD: 5.6 months (n=65)

• PFS PLD alone: 2.9 months (n=60)

Safety: • Hematologic adverse events: 66% for canfosfamide + PLD vs 44% for PLD alone

• Palmar-plantar erythrodysesthesia and stomatitis incidence: 23% and 31% for canfosfamide + PLD vs 39% and 49%

for PLD alone

Lumleian Commentary: • Clinical trials of Telcyta have demonstrated that increased PFS was obtained with increased hematological

toxicity; further clinical evaluation of Telcyta is expected in ovarian cancer

Phase III (Completed)

Patient Segment: • Platinum-resistant ovarian cancer

Stratification: • Randomized, open-label

Studies:

(Target Enrollment)

• N = 244, N = 125, N = 440

Comparator: • PLD alone

Dosing: • 1000 mg/m2 canfosfamide; 50 mg/m2; IV; day 1 and every 28 days

• Dose until progression or unacceptable toxicity

Duration: • 60 months

Primary End-Points: • Primary: PFS

• Secondary: Objective Response

• Secondary: Tolerance/Toxicity

32

Physiology • Tumors secrete angiogenic factors that promote the

formation of blood vessels;

– Vascular endothelial growth factor (VEGF), basic

fibroblast growth factor (bFGF), platelet-derived

growth factor (PDGF), placental growth factor

(PlGF) and angiopoietins play a role in blood

vessel formation

Hypothesized

Mechanism • Normal cells cannot live past the diffusion limit of

oxygen and nutrients, and therefore depend on the

proximity of blood vessels; therefore, tumors

cannot grow unless they secure their own blood

supply by promoting the growth of nearby

vasculature in a process called angiogenesis

• Two main classes of therapeutic agents target

tumor vasculature: angiogenesis inhibitors and

vascular-disrupting agents (VDA)

Phase III (6) • Avastin (RHHBY) • Trebananib (Millenium/Takeda)

• Vargatef (Boehringer Ingelheim) • Zaltrap (Regeneron)

• Votrient (GSK) • Thalomid (CELG)

Phase II (3) • Ramucirumab (LLY) • Panzem (ENMD)

• Zybrestat (OXGN)

Phase I (2) • Vadimezan (NVS) • RO5323441 (RHHBY)

Sources: Bio-Pharma Insight, www.clinicaltrials.gov, http://www2.nau.edu, Hall M, et al. Recurrent ovarian cancer: when and how to treat. Curr

Oncol Rep. 13:6 (2011)

Pipeline

Avastin and trebananib are the most advanced vascular-targeting agents, with Avastin showing a

modest efficacy benefit in pivotal trials; although FDA approval is unlikely, Avastin is likely to be

used widely in this difficult-to-treat tumor type.

33

Sources: www.clinicaltrials.gov, Perren et al. A phase 3 trial of bevacizumab in ovarian cancer. N Engl J Med 365:26 (2011), Hall M, et al. Recurrent

ovarian cancer: when and how to treat. Curr Oncol Rep. 13:6 (2011), Aghajanian C, et al. OCEANS: A Randomized, Double-Blind, Placebo-Controlled

Phase III Trial of Chemotherapy With or Without Bevacizumab in Patients with Platinum-Sensitive Recurrent Epithelial Ovarian, Primary Peritoneal or

Fallopian Tube Cancer. J Clin Oncol. (2012)

Although Avastin showed promise in Phase II studies, the pivotal trials (ICON7 and Oceans) led to

a modest efficacy benefit with increases in the development of fistulae and GI perforations that

raise the patients’ risk factors; FDA approval is unlikely.

Avastin

Efficacy: • In the ICON7 trial, patients treated with carboplatin + paclitaxel had a mean PFS of 22.4 months, while the

carboplatin + paclitaxel + Avastin arm had a mean PFS of 24.1 months

- In patients at high risk for progression, PFS was 14.5 months with standard therapy and 18.1 months with

Avastin, while median OS was 28.8 months in the control group and 36.6 months with Avastin

• In the OCEANS trial, patients with relapsed, platinum-sensitive disease treated with carboplatin + gemcitabine had a

PFS of 8.4 months, while patients given carboplatin + gemcitabine + Avastin had a PFS of 12.4 months

- Overall survival was 35.2 months in patient receiving no Avastin and 33.3 months in Avastin-treated patients

Safety: • Avastin treatment is associated with serious toxicities , including hypertension, gastrointestinal perforations and

inracereberal hemorrhage

Lumleian

Commentary:

• Avastin has demonstrated positive data in advanced ovarian cancer (ICON7) and early-stage patients with multiple risk

factors; however, the efficacy benefit is modest and unlikely to support FDA approval given the increase in adverse

events

Phase III Program (Completed) Phase III Program (Completed)

Patient Segment: • ICON7: Advanced Ovarian Cancer (Stage IIB or greater) • OCEANS: Recurrent, platinum-sensitive ovarian cancer

Stratification: • Randomized, two arm trial (N=1528) • Randomized, double-blinded (N=484)

Comparator: • Standard of care, carboplatin and paclitaxel • Control: Carboplatin and gemcitabine + placebo

• Research: Carboplatin and gemcitabine + Avastin

Dosing: • 6 cycles, 1 Avastin for 6 cycles and then Avastin alone

for a further 12 cycles

• 6, 21-day treatment cycles; research arm followed by

Avastin as a single agent until disease progression

Duration: • Control: 18 weeks; Research: 54 weeks • Control: 18 weeks; Follow-up to 24 months

Primary End-Points: • Primary: Progression-free survival

• Secondary: Objective Response; Overall survival

• Primary: Progression-free survival

• Secondary: Objective Response; Overall survival

34

Sources: www.Clinicaltrials.gov, Karlan BY et al., Randomized, double-blind, placebo-controlled phase II study ofAMG 386 combined with weekly

paclitaxel in patients with recurrent ovarian cancer. J Clin Oncol. 30:4 (2012)

Millenium/Takeda’s vascular-targeting agent lead asset trebananib has been advanced to Phase

3 trials in Australia, Canada, and Europe for recurrent ovarian cancer patients.

Trebananib (AMG 386)

Efficacy: • Prolongation of PFS in Phase II in combination with weekly paclitaxel from 4.6 to 7.2 months; may not dramatically

extend survival in terminal patients, but shows promise in recurrent patient population not pursued by Avastin

Safety: • Side effects included edema, hypertension, thromboembolic events

Lumleian

Commentary:

• Trebananib could renew promise for vascular-targeting agents if Phase III data is positive, although the mechanistic

similarity to Avastin makes those results uncertain; the side effect profile looks distinct from other VEGF inhibitors

Phase II (Completed) TRINOVA-1, TRINOVA-3 Phase III (Ongoing)

Patient Segment: • Recurrent ovarian cancer • Recurrent ovarian cancer

Stratification: • Randomized, double-blind • Global multicenter, randomized, double-blind trial of

paclitaxel plus trebananib or placebo

Studies:

(Target Enrollment)

• N = 161 • N = 900

Comparator: • Trebananib plus paclitaxel vs. placebo • Trebananib plus paclitaxel vs. placebo

Dosing: • Paclitaxel at 80 mg/m2 IV QW (3 on/1 off) plus

Trebananib at 10 mg/kg (Arm A), 3 mg/kg (Arm B) or

placebo (Arm C) IV QW

• Experimental: Weekly Intravenous (IV) Trebananib 15

mg/kg plus IV paclitaxel 80 mg/m2 weekly (3 on / 1

off); Control: Weekly Intravenous (IV) placebo plus IV

paclitaxel 80 mg/m2 weekly (3 on / 1 off)

Duration: • Disease progression or unacceptable toxicity • Primary data: July 2013; study completion: April 2017

Primary End-Points: • Primary: Progression-free survival

• Primary: Progression-free survival

• Secondary: Overall survival, objective response rate

35

Sources: www.clinicaltrials.gov, Ledermann JA et al. Randomized phase II placebo-controlled trial of maintenance therapy using the oral triple

angiokinase inhibitor BIBF 1120 after chemotherapy for relapsed ovariancancer. J Clin Oncol. 29:28 (2011), Bousquet G et al. Phase I study

of BIBF 1120 with docetaxel and prednisone in metastatic chemo-naive hormone-refractory prostate cancer patients.. Br J Cancer. 105:11 (2011)

Boehringer Ingelheim’s Vargatef is a novel triple angiokinase inhibitor that inhibits VEGFR, FGFR

and PDGFR; Phase II data in relapse patients is promising.

Vargatef (BIBF 1120)

Efficacy: • 14.3% of patients in the active arm were progression-free at 9 months, compared to just 5% progression-free in the

placebo arm of the trial

Safety: • Generally well tolerated; no significant hypertension

Lumleian

Commentary:

• Vargatef has shown promise in relapse patients who have already undergone treatment with chemotherapy in order to

delay the time to relapse; study was not powered to show significance but trends in efficacy looked favorable, but BI

has not announced plans for a Phase III maintenance trial

• A Phase III clinical trial is in progress for first-line treatment of primary disease

Phase II (Completed) LUME-Ovar 1 Phase III (Ongoing)

Patient Segment: • Continuous Maintenance Treatment Following

Chemotherapy in Patients With Relapsed Ovarian Cancer

• First-line in Patients With Advanced Ovarian Cancer

Stratification: • Randomized Placebo-Controlled • Multicenter, Randomized, Double-blind

Studies:

(Target Enrollment)

• N = 84 • N = 1300

Comparator: • Placebo during maintenance phase • Combination with carboplatin and paclitaxel vs.

placebo, carboplatin and paclitaxel

Dosing: • Oral, BID dosing of active drug • Oral, BID dosing of active drug

Duration: • 9 months • 41 months

Primary End-Points: • Progression-free survival (PFS) • Progression-free survival (PFS)

36

Sources:www.clinicaltrials.gov, Friedlander M et al. A Phase II, open-label study evaluating pazopanib in patients with recurrent ovarian

cancer. Gynecol Oncol.119:1 (2010)

GSK has advanced its oral, vascular-targeting agent Votrient to the second stage of a Phase II

trial with promising biochemical response, but no data is available on the agent’s ability to

impact survival in a randomized, controlled study.

Votrient (Pazopanib)

Efficacy: • In Phase II clinical trials, Votrient monotherapy has demonstrated a biochemical response in 31% of recurrent

ovarian cancers; ORR was 18%

Safety: • Generally well tolerated; no significant hypertension

Lumleian Commentary: • Although Votrient has demonstrated a biochemical response in ovarian cancer patients, and is generally well-

tolerated, clinical trials have so far failed to demonstrate meaningful efficacy in treatment of ovarian cancer

• A Phase III trial is underway, but this trial has been designed to test Votrient as a maintenance therapy,

rather than a treatment for the primary disease

Phase II (Completed) Phase III (Ongoing)

Patient Segment: • First-line in Patients With Advanced Ovarian

Cancer

• Stage III/IV ovarian cancer which has not progressed after

first-line therapy

Stratification: • Multicenter, Randomized, Double-blind • Randomized, placebo-controlled, double-blind

Studies:

(Target Enrollment)

• N = 35, N = 12 • Target enrollment N = 900

Comparator: • None • Placebo

Dosing: • 800 mg daily, 800 mg daily w/carboplatin,

800 mg daily w/paclitaxel

• 800 mg daily

Duration: • Baseline to response after 3 years • Up to 8 years

Primary End-Points: • Primary: Best Biochemical Response

• Primary: Toxicity/Tolerance

• Secondary: Overall response

• Primary: PFS

• Secondary: OS

• Secondary: Toxicity/Tolerance

37

Sources: Faivre, Kroemer & Raymond. Current development of mTOR inhibitors as anticancer agents. Nature Reviews Drug Discovery. 5:8 (2006).

www. clinicaltrials.gov, EvaluatePharma

To date, non-VEGFR kinase inhibitors have failed to replicate the successes achieved in other

oncology indications; however, numerous clinical trials remain underway and results may

improve with a greater understanding of ovarian cancer etiology.

Physiology • The numerous kinase mediate cell growth,

proliferation and survival

Pathophysiology • Hyperactivation of these critical pathways can

result in inappropriate cell growth, proliferation

and survival

Hypothesized

Mechanism

• Inhibition of the kinase-mediated pathway can

abrogate the cell proliferation and survival signals

that tumors depend upon

Pipeline

Phase III • Tarceva (RHHBY)

Phase II • Alisertib (Takeda) • Nexavar (BAYN) • Selumetinib (AZN)

• Cabozantinib (EXEL) • Erbitux (BMY/LLY/MRK) • Omnitarg (RHHBY)

• Linsitinib (Astellas) • Olaratumamb (LLY)

Phase I • TLN-4601 (TLN)

38

Sources:www.clinicaltrials.gov, Gordon AN et al. Efficacy and safety of erlotinib HCl, an epidermal growth factor receptor (HER1/EGFR) tyrosine kinase

inhibitor, in patients with advanced ovarian carcinoma: results from a phase II multicenter study. Int J Gynecol Cancer. 15:5 (2005), H. Hirte et al.

phase II study of erlotinib (OSI-774) given in combination with carboplatin in patients with recurrent epithelial ovarian cancer (NCIC CTG IND.149).

Gynecologic Oncology. 118 (2010), Halla S. Nimeiri et al., Efficacy and safety of bevacizumab plus erlotinib for patients with recurrent ovarian, primary

peritoneal, and fallopian tube cancer. Gynecologic Oncology 110 (2008), Blank SV, Erlotinib added to carboplatin and paclitaxel as first-line treatment

of ovarian cancer: Gynecologic Oncology 119 (2010)

Tarceva (RHHBY/OSI) has disappointed as a second- and third-line treatment for ovarian cancer;

Tarceva is currently in Phase III clinical trials as a maintenance therapy for patients who have

demonstrated an objective response to platinum therapy.

Tarceva (erlotinib)

Efficacy: • Tarceva was found to have an ORR of 57% in platinum-sensitive and 7% in platinum-resistant tumors

• A Phase II combination trial found that Tarceva did not demonstrate clinical benefit over Avastin alone

Safety: • Tarceva was generally well-tolerated; the most frequent adverse events were rash and diarrhea

Lumleian

Commentary:

• Although Tarceva has performed disappointingly in ovarian cancer to date, it is currently in Phase III trials as a

maintenance therapy; the favorable toxicity profile may increase odds of approval if Phase III data is positive

Phase II (Completed) Phase III (Ongoing)

Patient Segment: • Refractory ovarian cancer, platinum-sensitive and

platinum-resistant

• Patients with no evidence of disease progression after

successful first-line platinum therapy

Stratification: • Open-label • Randomized, open-label

Studies:

(Target Enrollment)

• N = 34, N = 50, N = 13, N = 56 • Target enrollment N = 830

Comparator: • None, Avastin alone • Observation

Dosing: • 150 mg daily, 150 mg daily w/carboplatin or Avastin • Twice daily

Duration: • 12 months • Up to 24 months

Primary End-Points: • Primary: PFS

• Secondary: OS

• Secondary: Toxicity/Tolerance

• Primary: PFS

• Secondary: OS

• Secondary: Adverse events/Toxicity

• Secondary: Quality of life

39

Sources: EvaluatePharma, Company product information, Kalli KR et al., Folate receptor alpha as a tumor target in epithelial ovarian cancer. Gynecol Oncol. 108:3 (2008), Kelemen, LE. The role of folate receptor alpha in cancer development, progression and treatment: Cause, consequence or innocent bystander? Int. J. Cancer. 119 (2006).

Farletuzumab (MORAb-003) and vintafolide (EC-145) are the most advanced folate receptor

targeting agents, though it is currently unclear whether they will provide significant

improvement over SoC.

Physiology • Folate receptors bind and transport folate, a

critical component of cell metabolism and DNA

synthesis

Pathophysiology • Cancer cells require high levels of folate, due to

more rapid metabolism and frequent cell division;

loss of functioning folate receptors can seriously

inhibit tumor growth and activity

• Folate receptor is overexpressed in 72%-81% of all

ovarian cancers

Hypothesized

Mechanism

• Inhibition of folate receptors (by antibody or small

molecule) leads to impairment of cell metabolism

and DNA synthesis, halting mitotsis and leading to

cell death

• Alternatively, therapeutic agents are conjugated to

folate-like molecules and are transported

preferentially into cells with high levels of folate

receptor, such as ovarian cancer cells Pipeline

Phase III (2) • MORAb-003/farletuzumab (ESALY) • EC145 (BMY/ECYT)

Phase II (0)

Phase I (1) • IMGN-853 (IMGN)

40

Sources: www.clinicaltrials.gov, Armstrong, DK et al. Exploratory Phase II efficacy study of MORAb-003, a monoclonal antibody against folate

receptor alphha, in platinum-sensitive ovarian cancer in first relapse. 2008 ASCO Annual Meeting. (2008)

Farletuzumab (Morphotek/ESALY), a monoclonal antibody with anti-folate receptor activity, has

demonstrated a modest increase in response rate and overall survival in recurrent ovarian

cancer; data from a Phase III trial is expected in September 2012.

Farletuzumab (MORAb-003)

Efficacy: • In a Phase II clinical trial, patients treated with MorAb-003 in combination with paclitaxel and carboplatin

demonstrated a 6.8% CR, 63.6% PR and 20.5% SD, with an average PFS of 10.2 months

• MorAb-003 treatment alone resulted in a change in CA-125 levels in only 2/21 patients

Safety: • MorAb-003 was generally well-tolerated; the most common adverse events were fatigue, anemia, and nausea

Lumleian

Commentary:

• MorAb-003 has demonstrated a modest increase in response rate when compared to standard chemotherapies in

treatment of recurrent ovarian cancer; data from ongoing Phase III trials are due in September

Phase II (Completed) Phase III (Ongoing)

Patient Segment: • Recurrent ovarian cancer • Ovarian cancer, in first relapse

Stratification: • Non-randomized, open label • Randomized, double blind

Studies:

(Target Enrollment)

• Two Phase II trials (N = 111, N = 52) • Target enrollment N = 900

Comparator: • Intravenous MorAb-003 alone or MorAb-003 +

paclitaxel + carboplatin

• Carboplatin/cisplatin + taxane

Dosing: • 100 mg/m2 MorAb-003, or 100 mg/m2 MorAb-003 +

175 mg/m2 paclitaxel on

• IV dosing, two different dosages

Duration: • 60 months • 12-24 months

Primary End-Points: • Serologic Response (change in CA125 levels)

• PFS

• OS

• PFS

41

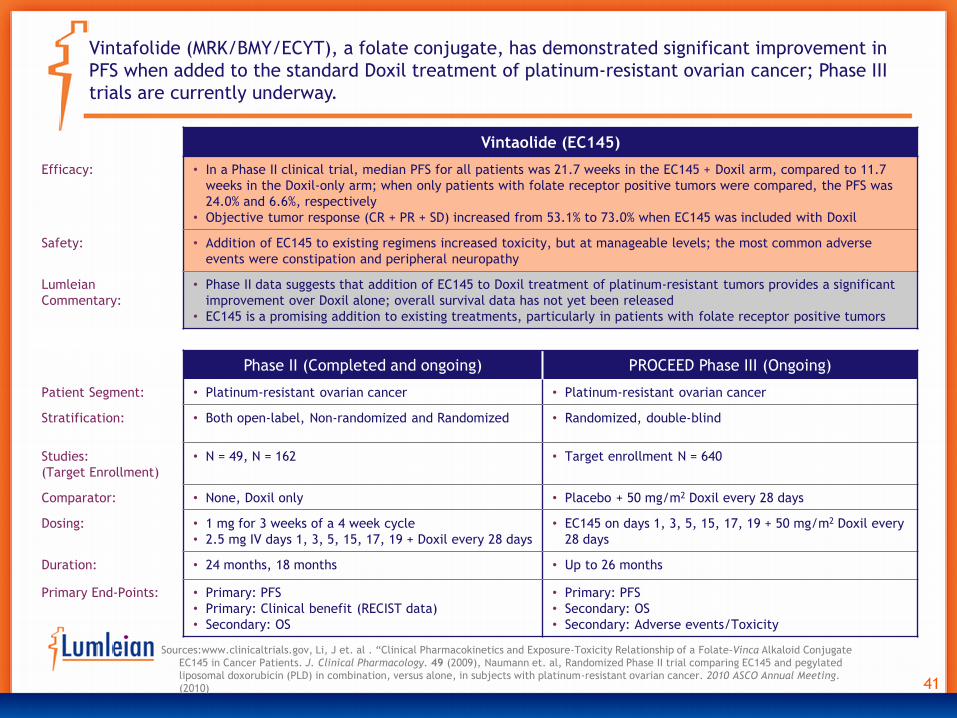

Sources:www.clinicaltrials.gov, Li, J et. al . “Clinical Pharmacokinetics and Exposure-Toxicity Relationship of a Folate-Vinca Alkaloid Conjugate

EC145 in Cancer Patients. J. Clinical Pharmacology. 49 (2009), Naumann et. al, Randomized Phase II trial comparing EC145 and pegylated

liposomal doxorubicin (PLD) in combination, versus alone, in subjects with platinum-resistant ovarian cancer. 2010 ASCO Annual Meeting.

(2010)

Vintafolide (MRK/BMY/ECYT), a folate conjugate, has demonstrated significant improvement in

PFS when added to the standard Doxil treatment of platinum-resistant ovarian cancer; Phase III

trials are currently underway.

Vintaolide (EC145)

Efficacy: • In a Phase II clinical trial, median PFS for all patients was 21.7 weeks in the EC145 + Doxil arm, compared to 11.7

weeks in the Doxil-only arm; when only patients with folate receptor positive tumors were compared, the PFS was

24.0% and 6.6%, respectively

• Objective tumor response (CR + PR + SD) increased from 53.1% to 73.0% when EC145 was included with Doxil

Safety: • Addition of EC145 to existing regimens increased toxicity, but at manageable levels; the most common adverse

events were constipation and peripheral neuropathy

Lumleian

Commentary:

• Phase II data suggests that addition of EC145 to Doxil treatment of platinum-resistant tumors provides a significant

improvement over Doxil alone; overall survival data has not yet been released

• EC145 is a promising addition to existing treatments, particularly in patients with folate receptor positive tumors

Phase II (Completed and ongoing) PROCEED Phase III (Ongoing)

Patient Segment: • Platinum-resistant ovarian cancer • Platinum-resistant ovarian cancer

Stratification: • Both open-label, Non-randomized and Randomized • Randomized, double-blind

Studies:

(Target Enrollment)

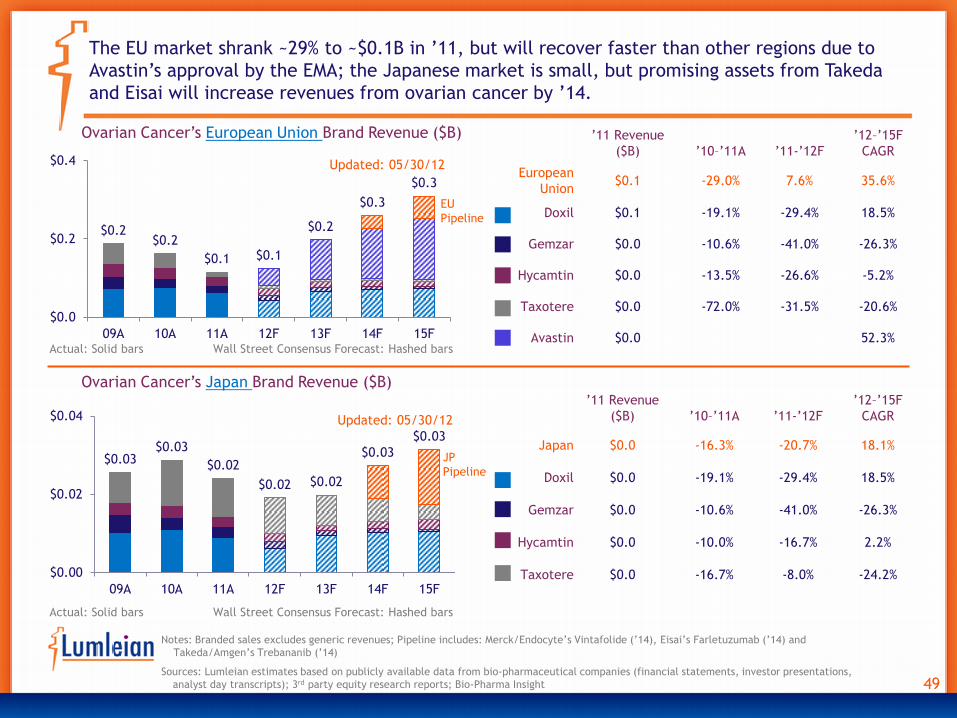

• N = 49, N = 162 • Target enrollment N = 640