director’s & officer’s liability policy a presentation by : jk risk managers and insurance...

TRANSCRIPT

DIRECTOR’S & OFFICER’S LIABILITY POLICY

A Presentation by:

JK Risk Managers and Insurance Brokers Ltd(A JK Group Company)

The JK Group

A trusted Business House for over 124 Years

JKRMIBL

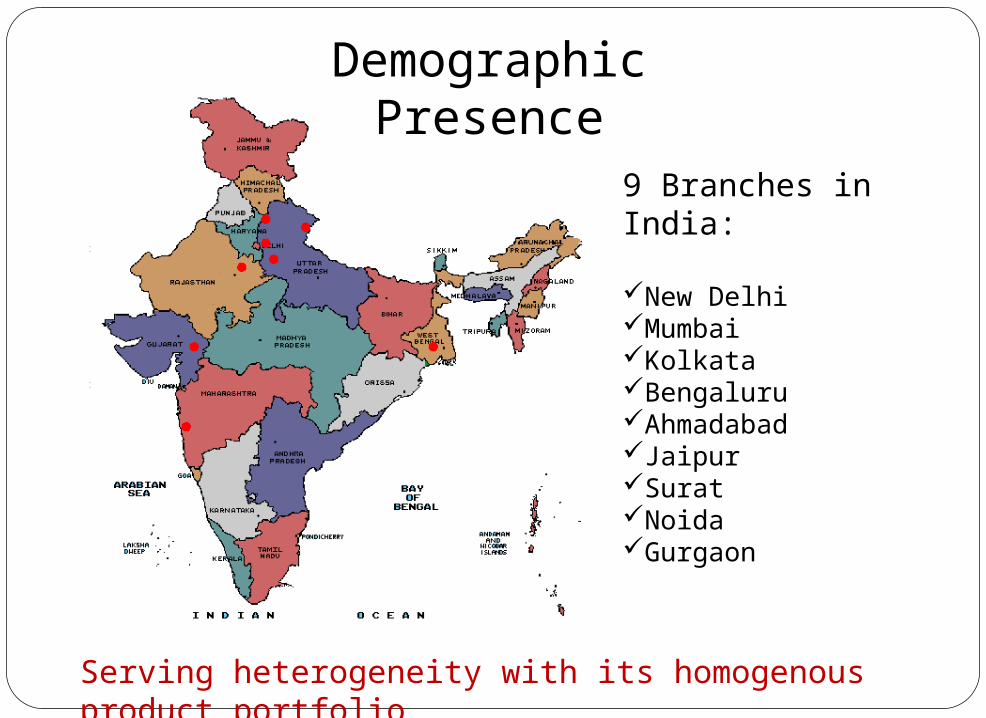

9 Branches in India:

New DelhiMumbaiKolkataBengaluruAhmadabadJaipurSuratNoidaGurgaon

Demographic Presence

Serving heterogeneity with its homogenous product portfolio

Repeated business orders ensures greater business volumes

Customer retention and customer expectation management makes JKRMIBL an emerging player in the market

Service Delivery

To Insurers

Providing relevant and concise data in form of Broking slips

Act as marketing channel without bias

Coordination with TPAs

Claim expedition

To Clients

Web based applications

Value added services

Knowledge management

Expertise covering all sectors

Introduction to D&0 liabilityAlthough a company has a separate legal entity it is obviously incapable of acting on its own and can only operate through its Directors and Officers. In addition to the statutory duties a Director & Officer must act in good faith in his dealings with and on behalf of the company and exercise the powers and fulfill the duties of his office honestly. Thus the responsibilities of a Director become increasingly onerous and complex.

It is important for company’s executives to be sensitized to the fact that virtually everything that they do creates the potential for second guessing and perhaps claims by persons adversely affected by their actions and decisions.

Executive Liability is a perennial threat for corporations, large and small.

A Company Director or Officer is thus exposed by law to a formidable array of liabilities and penalties both under the Companies act as well various other laws aimed to protect the interests of the Company as well its employees.

450 laws out of the innumerable Indian Laws, directly hold a Director or Officer in charge liable under various sections.

Cont…The Securities and Exchange Board of India (SEBI) has made several recommendations regarding the minimum number of independent directors on the Boards of listed companies, and the role that they should play. According to the code now mandated through listing agreements-at least a third of the board must consist of independent directors if the Chairman is a non-executive director, and half otherwise.

SEBI board on 14th May 2001 paved the way for the creation of a code of conduct to prevent insiders trading as also a code for corporate disclosure practices for listed companies. Thus for the first time placing responsibility on India Inc to tackle the menace of insider trading.

Even the Report on Investor Protection, calls for a clear shift in SEBI’s role as a regulator. They have proposed SEBI to be an on-and-off-the-field regulator on the lines of the Securities and Exchange Commission (SEC) of the US, which incidentally as a condition requires all the companies listing on the US Stock Exchanges to maintain a D&O Liability Insurance.

Corporate Governance often requires the executives to delicately balance the competing interest of various company constituents like Shareholders, employees, customers, lenders, regulators etc.

Cont…

A Director or Officer cannot be defended by the Company when legal activities are initiated against him for any reason although he may have discharged his duties honestly or may have been ultimately acquitted by the Court from the charges. As such, it becomes very difficult for a Director to ensure that any negligent act by his subordinates, to whom the ultimate responsibility for implementation of the decision is entrusted, perform their duties honestly and in good faith.

The recent amendment to Clause 49 of the listing Agreement by SEBI ( on lines of the Sarbanes Oxley Act of USA) places the Directors and Officers under more strenuous and stringent scanner .

Thus we have seen that the responsibilities of a Director / Officer become increasingly onerous and complex.

It is in light of this enhanced exposure faced by the companies and its Directors, that all companies should have a contingency plan in place in case the nightmare scenario occurs. This begs the questions – What can a Company/ Director/ Officer do?

The answer is purchasing a Directors and Officers Liability Insurance Policy (D&O).

1933/34 Securities Acts D&O Liability for misrepresentations, omissions in public

offerings, statements

1995 PSLRA Intended to prevent abuses of securities class action lawsuits. Heightened Pleading Standard

2002 Sarbanes-Oxley Act Blackout trading barred CEO and CFO certifications Faster insider trading disclosure Increased Audit Committee duties and SEC review More criminal penalties and fines

Historical Legislation Impacting D&O Suits in USA

Liabilities - How It Arises

Various Laws & Acts – Special focus on Companies (Amendment ) Act 2000, Environment Laws and Negotiable Instruments Act 1881, Tax Laws

Duty of skill and Care Fiduciary Duty Statutory Duty Increasing Recourse to global resources of financing and consequent

compliance requirements. Stricter implementation of the capital market regulations by SEBI. Consumer movements, class action and juridical activism. Duty to Shareholders

The Main Exposures

Publicly Quoted Companies Subsidiaries with Outside Shareholders Joint Ventures Raising Additional Capital Mergers & Acquisitions Major Restructuring International Markets Private & Public Offerings Independent Directors on Board Opening branches/subsidiaries overseas, particularly in the USA

Who Can Bring an Action?

Government or Regulatory Bodies Shareholders Employees Directors The Official Receiver / Liquidator Customers Competitors The Public The Company Creditors

The Potential Plaintiffs are:-

Can the Company Protect its Directors?

Whilst a company may indemnify its Directors for actions brought against them, the scope of protection is limited and may well be removed if:-

i) the company becomes insolvent ii) the company has insufficient funds iii) the company is the claimant iv) the protection is withdrawn v) they are no longer Directors of the company.

Most importantly indemnification by the Company is only permissible when a claim is successfully defended.

Who is protected by the policy?

A Policy is normally arranged in the name of the Parent/Holdingcompany and provides protection to the Directors and Officers of thatCompany and also to:-

1) The Directors and Officers of all subsidiary companies.

2) The directors and Officers of all Subsidiary companies acquired or created during the period of the policy.

This policy may also be extended to provide what is termed as “Outside Board” protection.

What Protection is Provided?

The policy protects the Directors and Officers against:-

1. It covers the directors and officers who commit a Wrongful Act in their capacity as directors and officers of the company.

2. Legal costs in defending allegations or suits brought

against them alleging wrongful act.

3. Any awards granted to the claimants against the Directors &

Officers, including out of court settlements.

What is a “Wrongful Act”?

Wrongful Act is defined as : Any error Misstatement Misleading statement Providing relevant and concise data in form of Broking slips Act, omission, neglect Breach of duty, breach of trust or breach of warranty of authority Employment related Disputes - means any claim to a past present or

prospective employee of the company and arising out of any actual or alleged unfair or wrongful dismissal, discharge or termination, either actual or constructive, employment-related misrepresentation, wrongful failure to employ or promote, wrongful deprivation of career opportunities, wrongful discipline; failure to grant tenure or negligent employee evaluation; or sexual or workplace or racial or disability harassment of any kind or unlawful discrimination, whether direct, indirect, intentional or unintentional, or failure to provide adequate employee policies and procedures, violation of any state law concerning discrimination

Type of Allegations Shareholders

- Inadequate or inaccurate disclosures- Financial Performance and Bankruptcy- Financial Reporting- Gross Mismanagement- Conflict of Interest- Dishonesty or Fraud- Investment or Loan Decision

Employees- Breach of Employment Contract- Employment Practices Liability - discrimination, sexual

harassment, unfair dismissal, invasion of privacy, failure to provide a proper or safe working environment

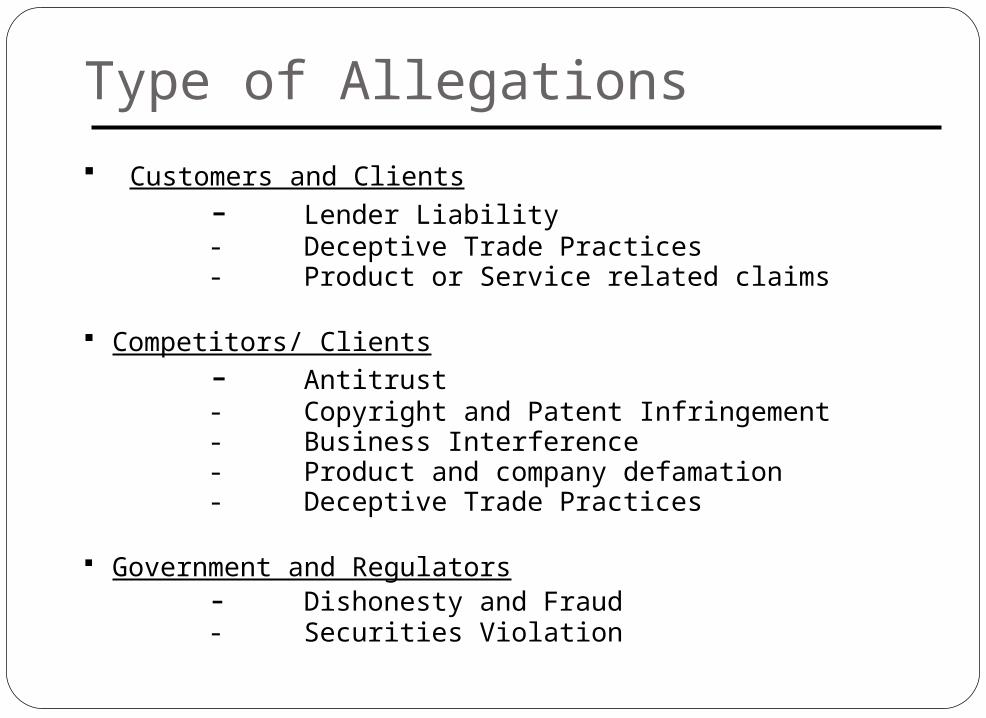

Type of Allegations

Customers and Clients

- Lender Liability- Deceptive Trade Practices- Product or Service related claims

Competitors/ Clients- Antitrust- Copyright and Patent Infringement- Business Interference- Product and company defamation- Deceptive Trade Practices

Government and Regulators- Dishonesty and Fraud- Securities Violation

Principal Policy Features Scope of Cover

Cover 1 - Directors and Officers

To pay on behalf of the DIRECTORS AND OFFICERS all LOSS arising out of a CLAIM for a WRONGFUL ACT for which coverage applies and for which the DIRECTORS AND OFFICERS are not entitled to indemnification pursuant to 2 below.

Cover 2 - Company Reimbursement

To pay on behalf of the COMPANY all LOSS arising out of a CLAIM for a WRONGFUL ACT for which coverage applies and for which the COMPANY is permitted or required by law common or statutory to grant indemnification to the DIRECTORS AND OFFICERS.

Principal Policy Features

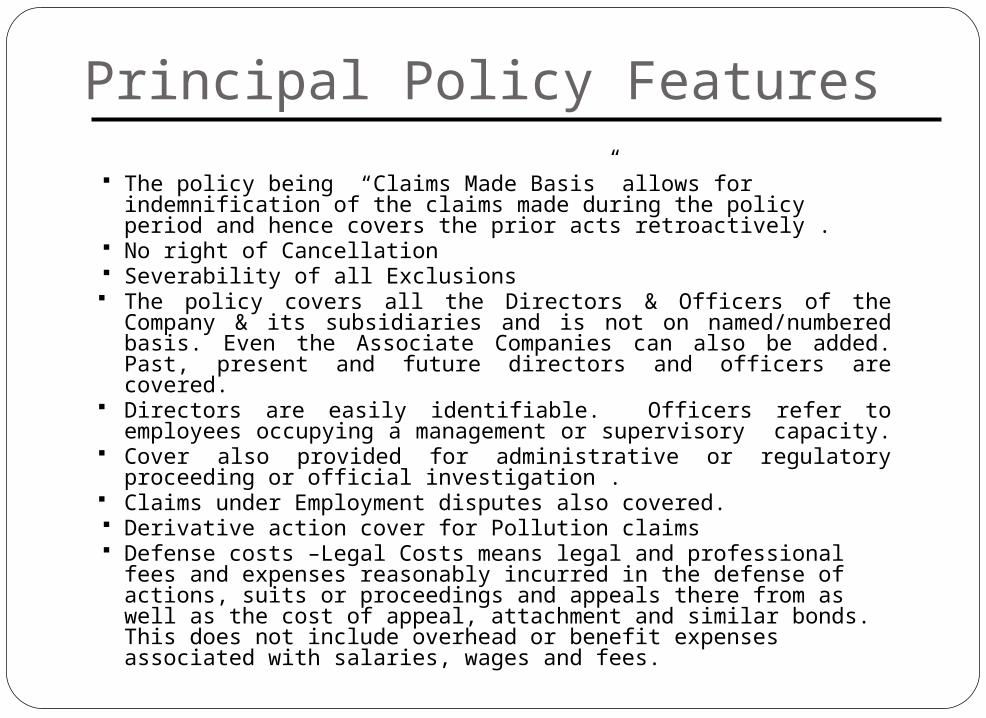

The policy being “Claims Made Basis” allows for indemnification of the claims made during the policy period and hence covers the prior acts retroactively .

No right of Cancellation Severability of all Exclusions The policy covers all the Directors & Officers of the Company & its

subsidiaries and is not on named/numbered basis. Even the Associate Companies can also be added. Past, present and future directors and officers are covered.

Directors are easily identifiable. Officers refer to employees occupying a management or supervisory capacity.

Cover also provided for administrative or regulatory proceeding or official investigation .

Claims under Employment disputes also covered. Derivative action cover for Pollution claims Defense costs –Legal Costs means legal and professional fees and expenses

reasonably incurred in the defense of actions, suits or proceedings and appeals there from as well as the cost of appeal, attachment and similar bonds. This does not include overhead or benefit expenses associated with salaries, wages and fees.

Principal Policy Features

Scope of Cover (Contd.)

Aimed at protecting directors and officers of the company. It is therefore a cover to protect individual corporate managers

The policy does not cover the company for its liability (though there are extensions available that will protect the company in certain areas).

The directors are protected against claims made by court appointed or externally appointed liquidators and /or receivers

Defence costs cover if a director/officer is legally compelled to appear at an official investigation

Severability as to all policy exclusions and the application form No restriction on prior acts/retroactive date. Broad definition of Claim Includes Criminal proceedings, formal

administrative and regulatory proceedings Any fresh IPOs or buy backs occurring during the policy period could also

be covered at NIL or an Additional Premium subject to advising the insurer

Principal Policy Features

Few Extensions

Outside Directorship Crisis Communication Insured Vs Insured Pecuniary Penalties Court Attendance Costs EPL Entity Cover Securities Entity Cover Predetermined Allocation of Legal Costs Retrodate – unlimited Discovery Period

The Main Exclusions Bodily Injury, Sickness, Disease, Death, or Damage / Destruction of Property. Seepage & Pollution or Contamination. Liability of a Director or Officer to restore or account for Remuneration paid to him for

which he is not legally entitled. War and Civil War Exclusion ; Radioactive Contamination Exclusion Terrorism Exclusion USA / Canada Specific Exclusions Prior and Pending Litigation Exclusion at Inception Major Shareholder Suits Exclusion at 15-20% Absolute BI / PD and Professional Indemnity Future Securities Offering Exclusion Criminal Fines and Penalties. Insured Vs Insured Claims punitive or exemplary damages Claims on Directors / Officers acting in a capacity as trustee or fiduciary under law

(statutory or non-statutory including common) or administrator of any pension, profit sharing or employee benefits programme

Exclusion due to underwriting considerations - Insurers may in addition to the standard exclusions, endorse the Policy with additional exclusion because of the nature of the case. For example, the company may be facing litigation; therefore the Policy will exclude any claim or development arising from the claim. Family Holding / Parent Co. ex Is an example of this

Suggested Limits

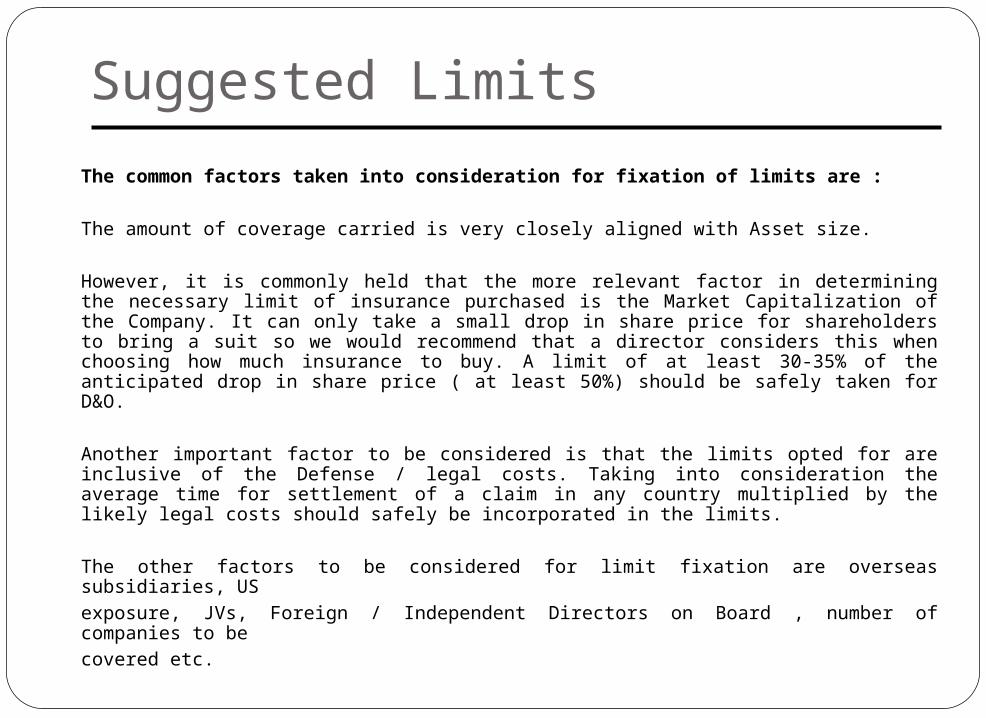

The common factors taken into consideration for fixation of limits are :

The amount of coverage carried is very closely aligned with Asset size.

However, it is commonly held that the more relevant factor in determining the necessary limit of insurance purchased is the Market Capitalization of the Company. It can only take a small drop in share price for shareholders to bring a suit so we would recommend that a director considers this when choosing how much insurance to buy. A limit of at least 30-35% of the anticipated drop in share price ( at least 50%) should be safely taken for D&O.

Another important factor to be considered is that the limits opted for are inclusive of the Defense / legal costs. Taking into consideration the average time for settlement of a claim in any country multiplied by the likely legal costs should safely be incorporated in the limits.

The other factors to be considered for limit fixation are overseas subsidiaries, USexposure, JVs, Foreign / Independent Directors on Board , number of companies to becovered etc.

Suggested LimitsAnother consideration for the Assessment of Risk and loss arising out of a legal suit isBalancing Costs against Risk.

Coverage Limits by Asset Size: AverageUnder $100 million $ 5.8M$100-$400 million $ 14.4M $400 million-$1 billion $ 27.1M$1 - $2 billion $ 46.0M $2 - $5 billion $ 50.9MOver $5 billion $100.3M All Assets Sizes $ 27.6M Total Limits by Ownership:

AverageFewer than 500 shareholders $ 8.03M500 or more shareholders(public) $39.51M

Distinguishing Advantages

Have tailor made and Serviced this policy for a varied clientele. Have worked for PSU companies as Consultants for their Policy

Procurement Process and servicing. Competitive Premiums Wider Policy Wordings with no ambiguity on the

Interpretation The premium is not assessed on the basis of the number of

Directors / officers to be covered which is a far more costlier option.

Bankruptcy or insolvency does not cancel the policy. 90 days automatic cover for outside position /directorship

taken by a director. Claims Handling Ability in view of the in-depth experience on

this policy.

Claim Case Studies Regulatory Claims

The Securities and Exchange Board of India (SEBI) has fined Reliance Industries (RIL) a penalty of Rs. 4.75 lakh in a case related to violation of Sebi’s takeover regulations with respect to RIL’s holding in cement and engineering major L&T. Sebi sources confirmed the move and said its investigation pertaining to violation of takeover regulations by RIL is now over.

Top Officials of Stock Holding Corporation have been named in a Criminal lawsuit relating to dishonoring of cheques issued by SHCIL. The client is looking to have their Defence costs paid under their D&O policy

Shareholder’s Claims A public interest litigation has been filed by a JPIL shareholder alleging

violation of takeover code by the company. The shareholder has alleged that during 1999-2000, the promoters of JPIL, Jaiprakash Gaur ' and his associates, had acquired 1,46,40,000 equity shares, which is around 10 per cent of JPIL shares in 12 months without making a public offer. This is in violation of the Sebi takeover code which allows creeping acquisition only up to 5 per cent during any 12 months.

Claim Case Studies Miscellaneous Claims

ICICI Bank has lodged a claim under their D&O policy for Rs. 25 Crores as an outcome of an ongoing legal battle initiated by Commerce bank. The case is related to funding of the Arvind Mills by ICICI Bank . Commece ban which was also part of the consortium had objections to this funding. The claim filed under D&O policy for recovery of legal expenses.

Director Vs Director Claims The Tatas have filed a police complaint recently against six top executives

including Dilip Pendse, the former managing Director of Tata Finance Ltd. (TFL), who were sacked last month following the discovery of unauthorized transactions leading to substantial losses. The client has charged the accused, Dilip Pendse and four others, of criminal conspiracy, falsification of accounts, forgery and criminal breach of trust “causing substantial wrongful loss to the company (TFL) and its investors, specially of the 9 per cent CCP”.

Claim case studies Merger & Acquisition Claims

A shareholder class-action suit was filed against a parent company and its directors and officers alleging the defendants were attempting to acquire 100% ownership of a partially owned subsidiary for grossly inadequate consideration. The subsidiary was 61% owned by the parent company, and the remainder was publicly owned. The parent company was attempting to purchase the remaining 39% interest from the public, thereby turning the entity into a wholly owned subsidiary. The case was settled out of court with the defendants agreeing to pay $1.15 million to plaintiffs to cover their attorney's fees in the litigation. The defendants incurred defense expenses of approximately $1.2 million.

Employment Practices Claims In 1994, Directors of an American Corporation was sued by 6 African-

American employees for alleged racial discrimination in the Corporation’s hiring and promotion practices. The case settled in 1996 for $175 million. Employment Practices Claims

An ex-employee of Infosys in US filed a Sexual Harassment case against the Company and its former Director . The case was settled out of Court for US$3 MN. D&O underwriters paid for the Director’s Damages (US$1.5 MN ) and the defence costs (US$900,000). (Detailed write up in Slide no. 32)

Claim case studies Infosys case:

Mr. Narayana Murthy –Chairman and chief mentor of Infosys of Infosys Technologies Ltd (NASDAQ:INFY) said:“Infosys has learned that the sexual harassment lawsuit filed by Ms. Jennifer Griffith, a former employee against the company and Mr. Phaneesh Murthy, a former director has been settled by Mr. Phaneesh Murthy and Ms. Griffith shortly before October 29, 2004 the trial date set for the lawsuit’s trial. Infosys has now learned that the settlement agreement was recently signed by the parties to the settlement agreement- Mr. Phaneesh Murthy and Ms. Griffith.Infosys did not contribute any money to the settlement and was not a signatory to the settlement agreement. However, Infosys has learned from its insurer’s counsel that the settlement releases Infosys from all claims and liabilities alleged in the lawsuit. Infosys learnt from its insurers’ council that the insurer’s contributed US$400,000 towards the settlement and this represents 50% of the total settlement payment. The remaining 50% of the contribution was paid by Mr. Phaneesh Murthy since Infosys refused to make any contribution to the settlement.

Claim case studies Outside Board Directorship Claims

A Director of a Company in Hong Kong was asked by his Company to sit on the Board of another company in which it had a financial interest. The Board of this other Company was subsequently accused by the regulatory authorities of having been in breach of local regulations. Although it was able to successfully defend these allegations, the legal defense costs for all the Board Members was more than US$400,000 per Director. The breaches which were alleged to have taken place were unknown to the one Director who was assigned to the Board of that Company but this made no difference to his need to defend himself against the allegations for which he was held personally liable.

Shareholder Claim on an Indian Company related to ADR listing An Indian Portal company listed on the US stock Exchange and

its Directors and officers have been recently faced with a class action suit from its Shareholders for not disclosing material information in their prospectus, mis-statement and omissions.

Claim case studies Ex-Director’s Claims on Subhiksha Case

PremjiInvest, the $1 billion private equity fund owned by Azim Premji, the billionaire chairman of Wipro Ltd, is saying it was taken for a ride on Subhiksha, the now-shuttered retailer in which it had invested Rs 230 crore in early 2008. Investment banking sources said the private equity firm was understood to have said it was misled on the true financial position of Subhiksha, which has prompted it to send notices to the other directors on Subhiksha’s board, including those from ICICI Venture, which sold a part of its stake to Zash Investment, an investment vehicle of PremjiInvest. PremjiInvest officials confirmed the communication but declined to share the details.

Sexual Harassment caseCoca-Cola India has paid beauty queen Sushmita Sen Rs 1.45 crore to buy her silence over an alleged sexual harassment case against its marketing head Sripad Nadkarni. Sen made the allegation soon after Coca-Cola terminated its celebrity engagement contract with her on February 23. She alleged this was being done because she had rejected the sexual overtures of a senior Coke official. Sen’s lawyers also claimed sum of Rs 1.45 crore by way of compensation for sexual harassment should be paid by way of charity to an orphanage of our client’s choice. The sum has since been paid by Coke. But according to the copy of the cheque of ABN Amro Bank (No 932968, dated September 19, ’03), a payment of Rs 1.45 crore has been made to Sen, not to any charity

Claim case studies Satyam Fiasco:

This is one insurance that has failed to bring relief to Satyam as the company’s claims towards the legal costs have been rejected by Tata group’s insurance venture Tata AIG. Tata AIG has, in its preliminary view, disputed the claim sent by Satyam under its Directors & Officers Liability Policy (D&O Policy), subject to the company providing additional documentation and information. The primary policy was issued by TATA AIG, along with The New India Assurance and ICICI Lombard, forming multiple layers of cover. Satyam sent claim notifications regarding receipt of notices from several regulatory authorities and the Class Actions. It had also enclosed copies of letters from directors and officers on likelihood of potential claims. However, TATA AIG has sought additional documentation and information. Satyam expressed its disagreement with positions taken by TATA AIG, but agreed to furnish additional details. Satyam had incurred insurance cost of Rs three crore in October-December 2008 and Rs one crore each in January and February.

Top Five Largest Securities Class Action Settlements

Rankings Company Year Settlement Value ($Mn)

1 Lerach Coughlin Stoia Geller Rudman & Robbins

2006 $7,307

2 Bernstein Litowitz Berger & Grossmann

2005 $3,745

3 Cendant Corp. 2000 $3,528

4 WorldCom,Inc. 2004 $2,629

5 Lucent Technologies ,Inc. 2003 $517

According to the PwC study, between 1996 and 2004 there were 153 securities class actions that involved both SEC and DOJ investigations, of which 90 percent, involved accounting issues. CFOs were named as defendants in 83 percent of all class actions filed in 2004

Security Class Action Settlements

*Source: Stanford law school research

Federal Court Securities class Action Settlements Involving Corporate Governance Changes

_______ ______________ ______________ __________

Oct –07 American Italian pasta $25 million Company

June-07 DHB Industries $35 million

Dec-06 United Health Group $895 million

Jan-04 HCA Inc. $50 million

Dec-02 Mattel Inc. $122 million

$33 million of stock

Approximate Settlement

Date

Company Description

Settlement Amount

Corporate Governance

Reforms

American Italian Pasta Company (Pink Sheets: AITP), announced that it has entered into a Stipulation of Settlement (the "Stipulation") with lead plaintiff in the pending federal securities class action lawsuit. The Company also addressed current durum wheat market conditions and announced the additional retirement of debt under its credit facility.

DHB Industries said it intends to settle numerous class action lawsuits and one shareholder derivative suit for more than $35 million. The suits accuse DHB directors and officers of pumping up DHB's stock price by misrepresenting its products and then selling the shares at the inflated prices

UnitedHealth Group (NYSE: UNH) announced it has reached an agreement in principle with lead plaintiff California Public Employees' Retirement System (CalPERS) and plaintiff class representative Alaska Plumbing and Pipefitting Industry Pension Trust, on behalf of themselves and members of the class, to settle the federal securities class action lawsuit arising from the consolidated amended complaint filed on December 8, 2006, in the U.S. District Court in Minnesota against the Company and certain current and former officers and directors relating to its historical stock options practices. Under the terms of the proposed settlement, UnitedHealth Group will pay $895 million into a settlement fund for the benefit of class members

Brief about the cases involving Federal Court Securities class Action Settlements Involving Corporate Governance Changes

HCA Inc. (HCA) has tentatively agreed to settle several shareholder class action lawsuits for $49.5 million, the company said Thursday in its third-quarter report. In the filing with the Securities and Exchange Commission, the managed care services provider also said it reached a preliminary understanding with insurers that are expected to pay the majority of the settlement. HCA would establish a settlement fund to pay class members based on individual claims under the tentative agreeement reached in the third quarter.

Mattel Inc. on Thursday closed the books on what has been called one of the worst acquisitions in corporate history, announcing a $122-million settlement with shareholders over its ill-fated purchase of Learning Co. The El Segundo-based toy maker said it would take a $25.5-million pretax charge in the fourth quarter to cover legal fees and an uninsured portion of the settlement, with the balance to be paid by insurers. Mattel's settlement ranks No. 12 on the list of largest monetary agreements between a company and its shareholders, according to Cornerstone Research, a litigation consulting company.

Cont…

Facts And FiguresClaim Susceptibility and Frequency by Asset Size

Company SizeCompany Size SusceptibilitySusceptibility FrequencyFrequency

Under $100 Million 12% 17

$100 - $400 Million 24% 34

$400 Million - $1 Billion 31% 50

$1 - $2 Billion 37% 61

$2 - $5 Billion 37% 74

$5 - $10 Billion 44% 84

Over $10 Billion 63% 4.87

All Assets Sizes 31% 0.87

Facts And FiguresClaim Susceptibility and Frequency by Business Class

Susceptibility FrequencyPetroleum, Mining & Agricultural 32% 0.71High Technology 27% 0.47Durable Goods Manufacturing 26% 0.52Nondurable Goods Manufacturing 28% 0.42Transportation & Communications 34% 1.18Utilities 46% 0.76Merchandising 33% 0.61Large Banking 42% 0.69Non-Banking Financial Services 34% 0.95Construction & Real Estate 28% 0.63Personal & Business Services 24% 0.34Middle Market Banking 19% 0.30

All Business Classes 31% 0.8

Private Securities Litigation

Historical Claim Frequency by Sector

Facts And Figures

Number of Claims by Source and Allegation Worldwide% of All

ClaimsA. Past, current or prospective employees

or unions 49B. Competitors, suppliers and other contractors 8C. Customers, clients, ratepayers, students

and consumer groups 14D. Government and regulatory agencies 2E. Other third-party claimants 4F. Shareholders and other investors, including

partners and members, prior owners 23

THANK YOU

Disclaimer: To the best of our knowledge, the information supplied in this document is accurate. JK Risk Managers & Insurance Brokers Ltd nor any entity of JK Organization assumes any legal liability or responsibility for the accuracy, completeness, or usefulness of any information, product or process disclosed in this presentation. Information has been gathered from the website, journals and various other sources and wherever possible we have mentioned the source JK Insurance accepts no liability for any loss arising out of your reliance on information, which has been supplied.