dimitri vayanos and pierre-olivier weill: a search-based theory of

TRANSCRIPT

Dimitri Vayanos and Pierre-Olivier Weill:A Search-Based Theory of the On-the-Run

Phenomenon

Presented by: Andras Kiss

Economics DepartmentCEU

Vayanos-Weill A Search-Based Theory of the On-the-Run Phenomenon

The on-the-run phenomenon

Bonds with almost identical cash-flows trade at different prices(yields)

Just issued (”on-the-run”) bond portfolios have 0.55% lower averagereturn than previously issued (”off-the-run”) bonds with matchedduration (Warga, 1992)

Two potential explanations:1 On-the-run bonds are more liquid2 Repo market loans collateralized by on-the-run bonds offer lower

interest rates (”specialness”)

But why are on-the-run bonds more liquid and more special?

Are liquidity and specialness two independent phenomena?

Vayanos-Weill A Search-Based Theory of the On-the-Run Phenomenon

Walrasian vs. OTC markets: liquidity and bargaining

One asset, more buyers than sellers

Reservation prices depend on market type: pWb > pW

s , pOb > pO

s

Centralized market (Walrasian auctioneer)

Bertrand-competition, buyers bid up the price: pW = pWb

Sellers take all the surplusNo liquidity issue: ”everyone” can trade instantly

OTC market (no Walrasian auctioneer)

Buyers and sellers meet bilaterally, with frictionsSellers value transactions the same way: pO

s = pWs

Buyers expect positive search cost at future selling date ⇒pO

b < pWb ⇒ pO < pW (”liquidity discount”)

Trade occurs at some price pO ∈[pO

s , pOb

]⇒ pO ≤ pO

b < pW

(”bargaining discount”)Assets are easier to sell if they have more potential buyers, easier tobuy if they have more potential sellers

Vayanos-Weill A Search-Based Theory of the On-the-Run Phenomenon

Self-fulfilling asymmetric liquidity does not obviously arise

Take two assets with identical cash-flows

OTC market: you can only sell if someone wants to buy, and v.v.

Valuations are such that realized transactions create positive surplus

Asymmetric liquidity would arise along the following lines:

Buyers expect that asset 2 will be harder (costlier) to sell in thefutureThey are unwilling to buy asset 2 if p2 = p1

Sellers of asset 2 are hurt by the difficulty to sell and are willing toreduce the price by ∆p2

Buyers of asset 2 would be hurt the same way in the future (whenthey become sellers)Buyers accept to buy asset 2 if p2 is reduced by at leastPV (∆p2) < ∆p2

⇒ Asset 2 is still traded and equally liquid as asset 1⇒ Expectations of asymmetric liquidity are out of equilibrium⇒ p2 = p1

We need a reason why assets cannot be perfect substitutes for someagents

Vayanos-Weill A Search-Based Theory of the On-the-Run Phenomenon

Main ideas in the paper

1 Some investors are short-sellers

They initially borrow assets in the repo market from owners and sellthem in the spot marketLater, they buy assets in the spot market and return them to theowner they borrowed the asset fromShort-sellers must return the same asset they borrowed at the end ofthe repo contract

2 Spot markets are over-the-counter

Liquidity is an issueLack of asset substitutability for short-sellers at repurchase time cancreate endogenous liquidity (and price) differences

3 Repo markets are also over-the-counter

Lack of Bertrand-competition among lenders ⇒ positive lending fee⇒ specialness premiumAsymmetric liquidity ⇒ asymmetric specialness premiaRepo market frictions help make the size of price differences(originally caused by spot market frictions) empirically plausible

Vayanos-Weill A Search-Based Theory of the On-the-Run Phenomenon

Explaining the on-the-run phenomenon

Vayanos-Weill A Search-Based Theory of the On-the-Run Phenomenon

Investor types

Vayanos-Weill A Search-Based Theory of the On-the-Run Phenomenon

Centralized (Walrasian) spot market, no shorting

Two assets, issue size S for both

Too many buyers (high valuation agents): Fκ > 2S

Long position’s flow utility: δ + x − y

Long position’s flow cost: rpi

Bertrand-competition: zero surplus for buyers

No short-sales, Walrasian spot market (Proposition 1)

Both assets trade at the same price:

p1 = p2 =δ + x − y

r

Vayanos-Weill A Search-Based Theory of the On-the-Run Phenomenon

Explaining the on-the-run phenomenon

Vayanos-Weill A Search-Based Theory of the On-the-Run Phenomenon

OTC spot market, no shorting

Similar to the ”island-coconut” model of Diamond (1982)

Seller-buyer meetings established at fixed intensity Poisson arrivaltimes

Poisson intensity: λ (search friction)

Measure of sellers: µs

Probability of finding a seller in each instant: λ · µs

Efficient bargaining over the price: transaction occurs if surplus ispositive

Possibly nonzero share of surplus going to buyers: φ ∈ [0, 1]

Vayanos-Weill A Search-Based Theory of the On-the-Run Phenomenon

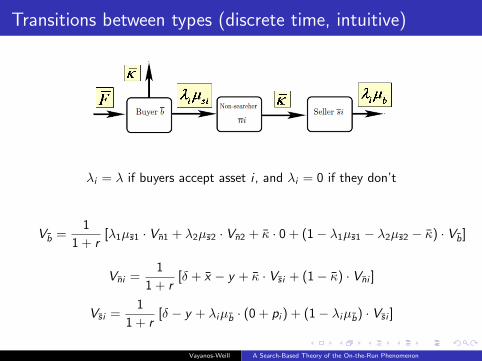

Transitions between types (discrete time, intuitive)

λi = λ if buyers accept asset i , and λi = 0 if they don’t

Vb =1

1 + r[λ1µs1 · Vn1 + λ2µs2 · Vn2 + κ · 0 + (1− λ1µs1 − λ2µs2 − κ) · Vb]

Vni =1

1 + r[δ + x − y + κ · Vs i + (1− κ) · Vni ]

Vs i =1

1 + r[δ − y + λiµb · (0 + pi ) + (1− λiµb) · Vs i ]

Vayanos-Weill A Search-Based Theory of the On-the-Run Phenomenon

Transitions between types (continuous time, exact)

rVb = −κVb +2∑

i=1

λiµs i (Vni − pi − Vb)︸ ︷︷ ︸buyer surplus

rVni = δ + x − y + κ (Vs i − Vni )

rVs i = δ − y + λiµb(pi − Vs i )︸ ︷︷ ︸seller surplus

Total surplus in selling asset i :

Σi ≡ Vni − Vb − Vs i

Surplus division:Vni − pi − Vb = φΣi

Vayanos-Weill A Search-Based Theory of the On-the-Run Phenomenon

Spot market frictions alone do not displace prices

It turns out:

Σi =x − φ

∑2j=1 λjµs j Σj

(r + κ) + (1− φ)λiµb

Remember:

λi = λ⇔ Σi ≥ 0

In equilibrium, λ1 = λ2 = λ and(Vni ,Vs i , pi , Σi

)are independent of i .

No short sales, search spot market (Proposition 2)

Suppose that short sales are not allowed. In equilibrium, all buyer-sellermeetings result in a trade, and both assets trade at the same price.

Vayanos-Weill A Search-Based Theory of the On-the-Run Phenomenon

Explaining the on-the-run phenomenon

Vayanos-Weill A Search-Based Theory of the On-the-Run Phenomenon

Short-selling and repurchase (repo) agreements

Long position: pay the asset price now, receive asset cash-flowduring ownership, receive the asset price at future sale

Short position: receive the asset price now, pay out asset cash-flowduring shorting, pay the asset price at future purchase

Need to borrow the asset for the shorting periodSell it, keep paying the cash-flow to the lender, then buy the assetand return it to the lender

Repo contract (asset-collateralized cash loan):

Lender turns his asset to borrower in exchange for cashDuring the contract, borrower does what he wants with the asset(e.g. shorts it)At maturity, same asset is returned and money is repaid with interest(repo rate)Asset specialness is the discount on its repo rate relative to highestquoted rateAsset specialness ⇔ (flow) lending fee (wi ) paid by borrower

Vayanos-Weill A Search-Based Theory of the On-the-Run Phenomenon

Walrasian spot and repo markets, short-selling

Frictionless selling, buying, borrowing

Positive lending fee ⇒ all owners want to lend the asset and nobodywants to hold it ⇒ no equilibrium ⇒ lending fee must be zero

Long position’s flow utility: δ + x − y

Long position’s flow cost: rpi

More buyers than sellers ⇒ zero seller surplus

No liquidity issue when short-sellers need to buy the asset back

Short sales allowed, Walrasian spot and repo markets (Proposition 3)

Both assets trade at the same price:

p1 = p2 =δ + x − y

r

Vayanos-Weill A Search-Based Theory of the On-the-Run Phenomenon

Explaining the on-the-run phenomenon

Vayanos-Weill A Search-Based Theory of the On-the-Run Phenomenon

Walrasian spot and OTC repo markets, short-selling

ν: repo market search friction (νi = ν if borrowers accept asset iand νi = 0 if they don’t)

Agent types and flow-value equations:¯i : lender (high valuation owner) of asset i , looking for a borrower

rV ¯i = δ + x − y + κ (pi − V ¯i ) + νiµbo (Vni − V ¯i )

ni : high valuation non-searcher in a repo contract (former lender,who has found a borrower)

rVni = δ + x − y + wi + κ (pi − Vni ) + κ (V ¯i − Vni )

bo : low valuation borrower, looking for a lender

rVbo = −κVbo +2∑

i=1

νiµ ¯i (Vni + pi − Vbo)

ni : low valuation non-searcher in a repo contract (former borrower,who has found a lender)

rVni = −δ + x − y − wi + κ (Vbo − pi − Vni ) + κ (−pi − Vni )

Vayanos-Weill A Search-Based Theory of the On-the-Run Phenomenon

Short-sellers without spot search do not displace prices

It turns out:

(r + κ+ κ) Σi = x + x − 2y − (1− θ)2∑

j=1

νjµ ¯jΣj

Remember:

νi = ν ⇔ Σi ≥ 0

In equilibrium, ν1 = ν2 = ν and(V ¯i ,Vni ,Vni , pi ,wi ,Σi

)are all

independent of i .

Short sales, Walrasian spot, search repo market (Proposition 4)

In equilibrium, both assets trade at the same price and carry the samepositive lending fee.

Symmetric positive lending fee (specialness) due to repo marketbargaining (θ ≥ 0).

Vayanos-Weill A Search-Based Theory of the On-the-Run Phenomenon

Explaining the on-the-run phenomenon

Vayanos-Weill A Search-Based Theory of the On-the-Run Phenomenon

Full model (OTC spot + OTC repo + shorting)

Vayanos-Weill A Search-Based Theory of the On-the-Run Phenomenon

Solving the model

Inflow-outflow equations for types (steady state):

b : F = κµb +2∑

i=1

λ(µs i + µsi

)µb

Market clearing:µ ¯i + µs i + µsi = S

µnsi + µnni + µnbi = µsi + µni + µbi

Flow-value equations:

b : rVb = −κVb +2∑

i=1

λ(µs i + µsi

)(V ¯i − pi − Vb)

In general, only numerical solutions

Closed-form solutions for ”small” search frictions (in the limit)

Vayanos-Weill A Search-Based Theory of the On-the-Run Phenomenon

Symmetric equilibrium

Vayanos-Weill A Search-Based Theory of the On-the-Run Phenomenon

Asymmetric equilibrium

Vayanos-Weill A Search-Based Theory of the On-the-Run Phenomenon

Arbitrage

Identical cash-flows, different prices: arbitrage opportunity?

Buy asset 2 and short asset 1:

Benefit: p1 − p2 > 0Cost (of shorting): w1

r

p1 exceeds p2 due to the liquidity and bargaining discounts(”liquidity premium”) and the specialness premiumSpecialness premium is only a fraction of the lending cost, sincecontinuous lending is not assured (market frictions)With a large enough lending fee, w1

r> p1 − p2 and arbitrage is

unprofitable

Opposite strategy can also be unprofitable

For certain (calibrationally plausible) parameter values, the pricedifferences are robust to the presence of arbitrageurs

Vayanos-Weill A Search-Based Theory of the On-the-Run Phenomenon

Equilibrium selection

Why do short-sellers systematically concentrate in on-the-run bonds?

”Effective issue size” is smaller for off-the-run bonds (buy-and-holdinvestors)

Theoretically, if asset supplies differ (S1 > S2), as search frictionsbecome small:

Short-selling can always be concentrated in asset 1Short-selling can only be concentrated in asset 2 if S1 − S2 is not toolargeSymmetric short-selling of both assets vanishes

Vayanos-Weill A Search-Based Theory of the On-the-Run Phenomenon

Explaining the on-the-run phenomenon

Vayanos-Weill A Search-Based Theory of the On-the-Run Phenomenon

App. 1: All inflow-outflow equations

Vayanos-Weill A Search-Based Theory of the On-the-Run Phenomenon

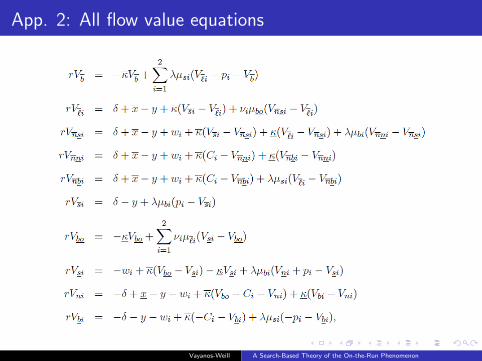

App. 2: All flow value equations

Vayanos-Weill A Search-Based Theory of the On-the-Run Phenomenon