digital video trend & ecosystem development: challenges ... · the world largest telecom...

TRANSCRIPT

www.ovum.com

© Copyright Ovum 2016. All rights reserved.

Digital Video Trend & Ecosystem Development:

Challenges & opportunities of AR/VR & new

technologies

Dr. CW Cheung 張智華

Research Fellow, Consulting Director, APAC

Ovum Limited

Email: [email protected]

Date: 1 August 2016

2 © Copyright Ovum 2016. All rights reserved.

Agenda and Introduction

The Consumer’s World in 2025

Digital video & ecosystem

development trend, and market

overview

Digital video & related enabling

technologies (4K/8K UHD, VR/AR,

etc.)

Key takeaways Dr. CW Cheung 張智華

Research Fellow, Consulting Director, APAC

Ovum Limited

Tel: +852 9156 8683

>35 years in ICT & Telecom industries:

tenures in operators, government,

academics and consultancies

Specialized in Fixed & Mobile

Broadband, Cable TV, Telco/OTT

Strategy and National ICT policies &

regulations

3 © Copyright Ovum 2016. All rights reserved.

About Ovum: the world largest telecom research & consulting firm

Advising on the

commercial impact of

technology and

market changes in

telecoms, digital media,

software and IT services”

Ovum – the global brand in ICT research and consulting for more than 30 years

Part of $2B Informa Group

Over 300 ICT analysts & consultants worldwide

Blue-chip client base: top tiers SP, vendors, government, etc.

We have 23 offices across the globe and more through our associates. Our 300 experts worked in

more than 50 countries in EMEA (Europe, Middle East and Africa), the Americas, and Asia Pacific.

4 © Copyright Ovum 2016. All rights reserved.

The Consumer’s World in 2025

5 © Copyright Ovum 2016. All rights reserved.

Most influential (Relatively) unknown Non-existent

The consumer’s world in 2005

6 © Copyright Ovum 2016. All rights reserved.

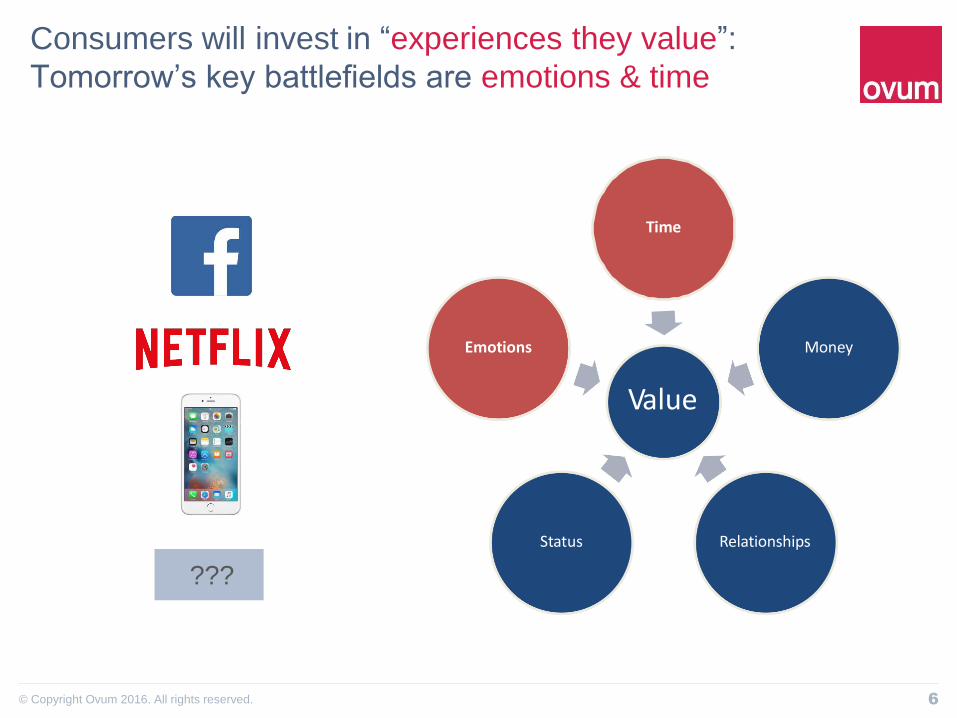

Consumers will invest in “experiences they value”:

Tomorrow’s key battlefields are emotions & time

Value

Time

Money

Relationships Status

Emotions

???

7 © Copyright Ovum 2016. All rights reserved.

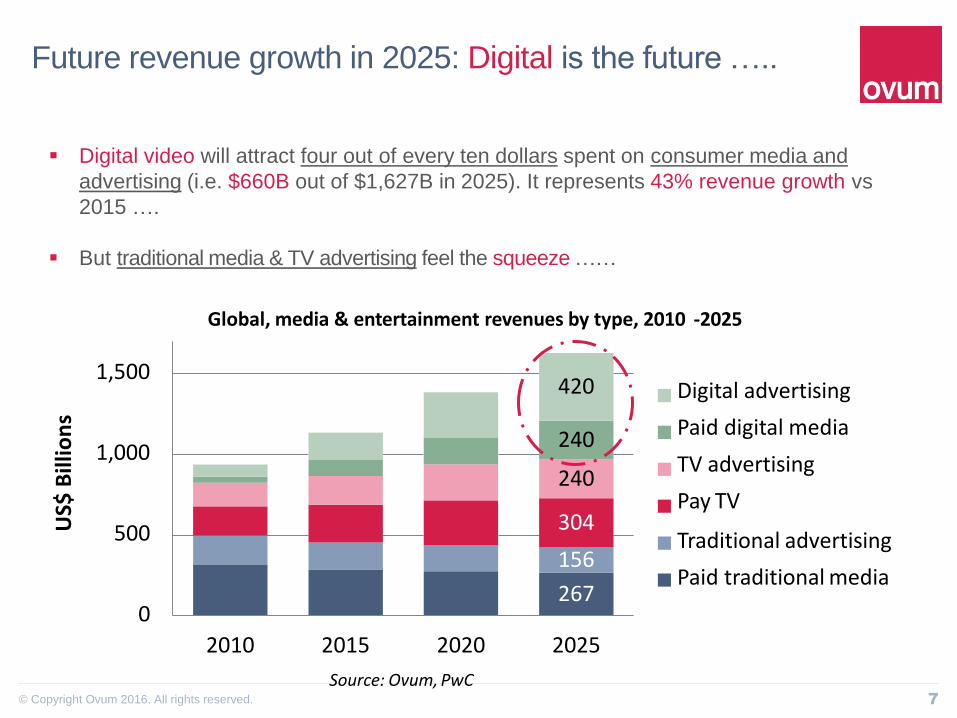

Future revenue growth in 2025: Digital is the future …..

Digital video will attract four out of every ten dollars spent on consumer media and

advertising (i.e. $660B out of $1,627B in 2025). It represents 43% revenue growth vs

2015 ….

But traditional media & TV advertising feel the squeeze ……

267

156

304

240

240

420

0

500

1,000

1,500

2010 2015 2020 2025

US$

Bill

ion

s

Global, media & entertainment revenues by type, 2010 -2025

Digital advertising

Paid digital media

TV advertising

Pay TV

Traditional advertising

Paid traditional media

Source: Ovum, PwC

8 © Copyright Ovum 2016. All rights reserved.

Over half of all revenues from consumer media

& entertainment will be from advertising

0%

50%

2010 2015 2020 2025

Global, share of media & entertainment revenues by type, 2010-2025

100%

Payments

Advertising

Source: Ovum, PwC

9 © Copyright Ovum 2016. All rights reserved.

Success with digital will require an almost

opposite approach to traditional media…

37%

63%

Traditional

Advertising Payments

44%

56% 64%

36%

TV Digital

Advertising Payments Advertising Payments

Global, share of media & entertainment revenues by sector and type, 2025

Source: Ovum, PwC

Payment or

subscription model

Advertising

model

10 © Copyright Ovum 2016. All rights reserved.

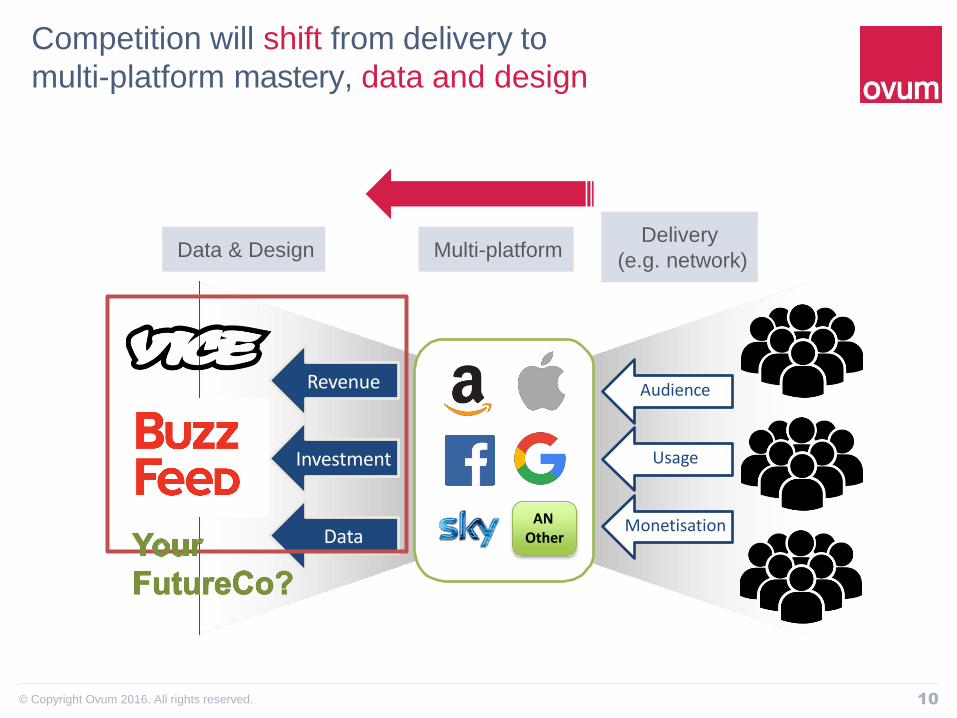

Competition will shift from delivery to

multi-platform mastery, data and design

Revenue

Investment

Data AN

Other

Audience

Usage

Monetisation

Data & Design Multi-platform Delivery

(e.g. network)

11 © Copyright Ovum 2016. All rights reserved.

Digital video & ecosystem development,

and market overview

12 © Copyright Ovum 2016. All rights reserved.

Video will shape the customer behaviors, services &

applications, business models and networks

Global video traffic will grow at CARG 25.3% in 2015-2020, with a dominated share of

>77.3% by 2020

Video will become “basic services” before 2020.

Video will drive digital transformation of industry stakeholders especially of network

operators and CSPs “voice-/data-centric” network migration to “video-centric” network

13 © Copyright Ovum 2016. All rights reserved.

Key trends of development …..

OTT SVOD to set new opportunity for content owners, and new wave of competition for

incumbent TV and video distributors.

SVOD has already become a mass-market leisure activity in developed markets

Evolution of bundling in multi-play: TV, OTT, and mobile entertainment are being bundled in

existing telecoms bundles in innovative ways.

Mobile video: live video streaming as mobile-first services will hit the social media mainstream

(e.g. Facebook)

Go east: The biggest visual entertainment growth opportunities are in Asia.

Linear OTT TV is upcoming, until then OTT video will be dominated by TV series viewed as part

of subscriptions

OTT (Digital) video revenue will grow fast to challenge pay TV …. the pace will be much

accelerated with possibility to come close to pay TV’s within a decade!

Consumption of digital video is not about collecting, it is all about fast access to exclusive new

content, and delighted video experience

“Convergence Video” = entertainment + communications + vertical video applications

14 © Copyright Ovum 2016. All rights reserved.

OTT from online to mainline:

SVOD take lead in global OTT Video trend ….

OTT Video will grow from $13.5B in 2015 to more than double $22.9B in 2019

Business models comprise of subscription, transaction and digital retail (or electronic

sell-through, EST)

15 © Copyright Ovum 2016. All rights reserved.

Video traffic over cellular

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

-

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

200,000

2015 2016 2017 2018 2019 2020

Pe

tab

yte

s p

er

year

Total 4G Traffic of which video

Mobile Video will be the second high growth video area after OTT Video.

Mobile video traffic (excluding WiFi) will increase tenfold during the next five years to

188,129 PB/year in 2020 – open up huge opportunity & challenges to 4G network

operators

Network operators need to address it at both a business and technology level

ranging from network cost savings (efficiency) to monetization (e.g. service convergence)

16 © Copyright Ovum 2016. All rights reserved.

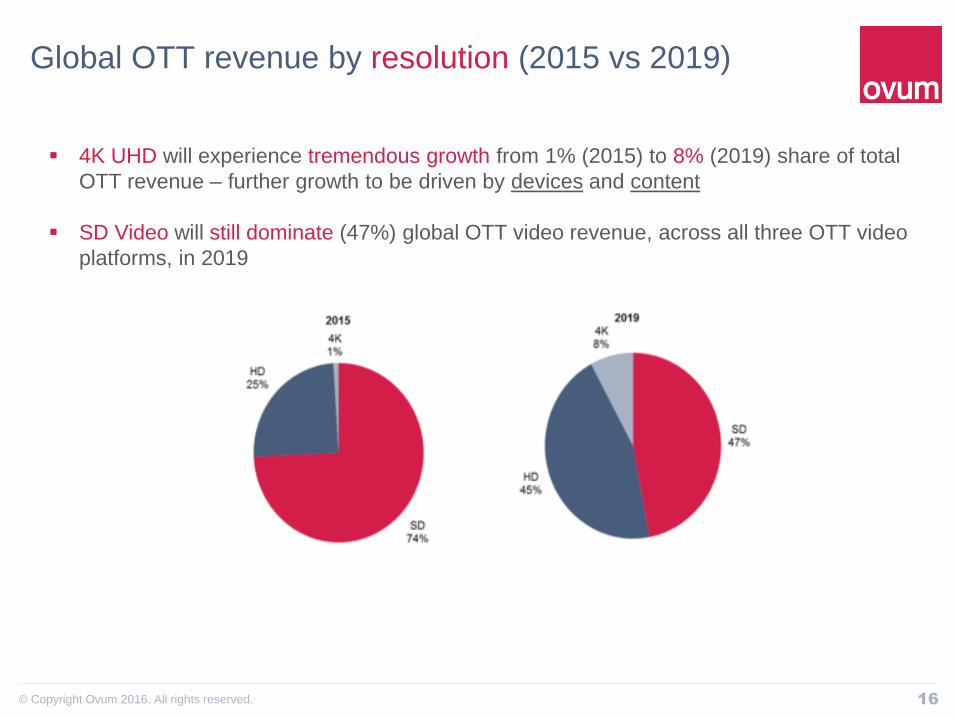

Global OTT revenue by resolution (2015 vs 2019)

4K UHD will experience tremendous growth from 1% (2015) to 8% (2019) share of total

OTT revenue – further growth to be driven by devices and content

SD Video will still dominate (47%) global OTT video revenue, across all three OTT video

platforms, in 2019

17 © Copyright Ovum 2016. All rights reserved.

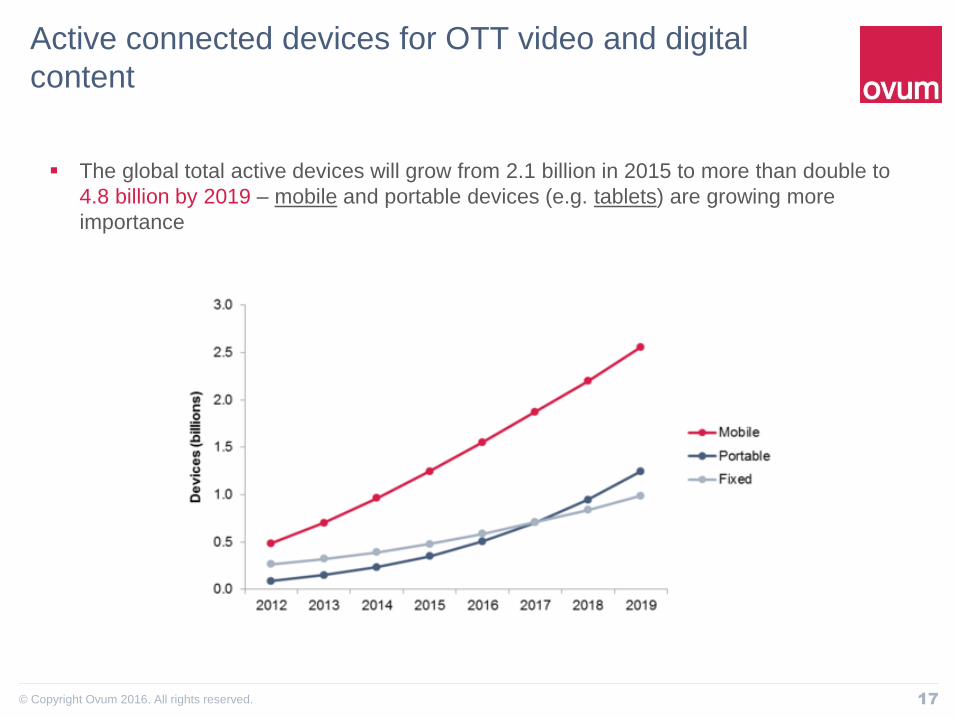

Active connected devices for OTT video and digital

content

The global total active devices will grow from 2.1 billion in 2015 to more than double to

4.8 billion by 2019 – mobile and portable devices (e.g. tablets) are growing more

importance

18 © Copyright Ovum 2016. All rights reserved.

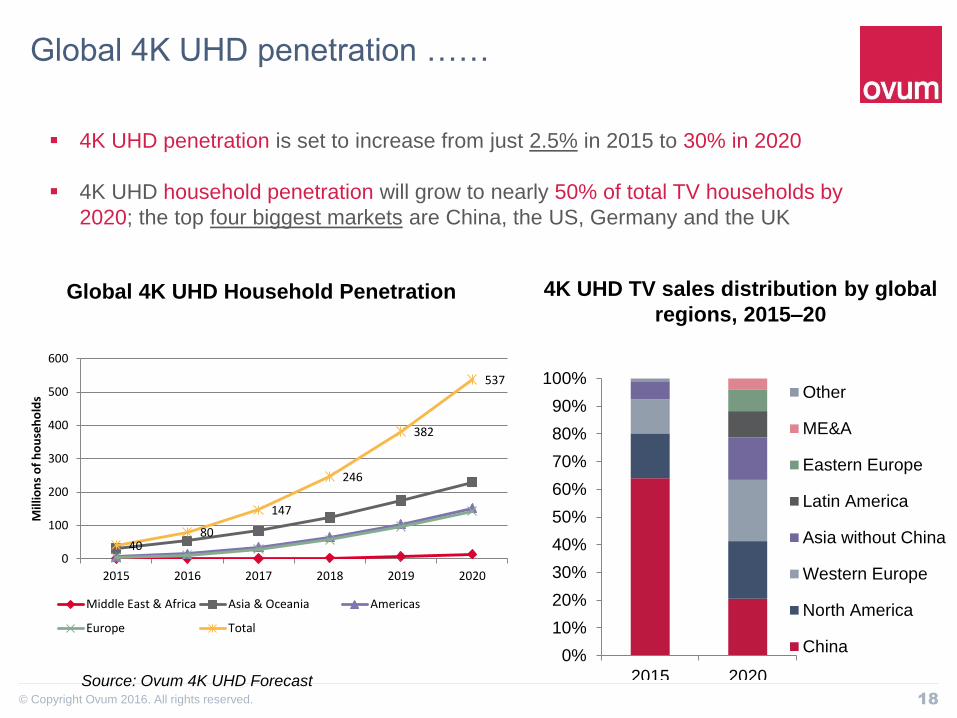

Global 4K UHD penetration ……

4K UHD penetration is set to increase from just 2.5% in 2015 to 30% in 2020

4K UHD household penetration will grow to nearly 50% of total TV households by

2020; the top four biggest markets are China, the US, Germany and the UK

Source: Ovum 4K UHD Forecast

Global 4K UHD Household Penetration

40 80

147

246

382

537

0

100

200

300

400

500

600

2015 2016 2017 2018 2019 2020

Mill

ion

s o

f h

ou

seh

old

s

Middle East & Africa Asia & Oceania Americas

Europe Total

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2015 2020

Other

ME&A

Eastern Europe

Latin America

Asia without China

Western Europe

North America

China

4K UHD TV sales distribution by global

regions, 2015–20

19 © Copyright Ovum 2016. All rights reserved.

Netflix’s aggression in global market development

Netflix launched its aggressive SVOD development in 130 markets at the start of 2016

Forecast to increase its international subscriber numbers to surpass the total in the US

home market

20 © Copyright Ovum 2016. All rights reserved.

UK’s Sky using OTT to compete in more release

windows

Sky and Netflix leverage on OTT content to compete with other pay-TV operators

Telcos increasingly bundle OTT content & services in their existing convergence service

packages

From simply usage revenue to increased monetization, reduced churn, customer loyalty

management or enhanced competition …..

21 © Copyright Ovum 2016. All rights reserved.

Danish’s Telmore Play bundling with 3rd party OTT

media services

Fixed and mobile telcos partner with OTT video services and digital content (e.g. streaming music

and e-books) to:

drive data usage

drive higher-tier subscriptions to larger data caps

offer better QoS

diversify revenue away from data which is become increasingly commoditized.

22 © Copyright Ovum 2016. All rights reserved.

Digital video and enabling technologies

23 © Copyright Ovum 2016. All rights reserved.

Digital video enabling technologies

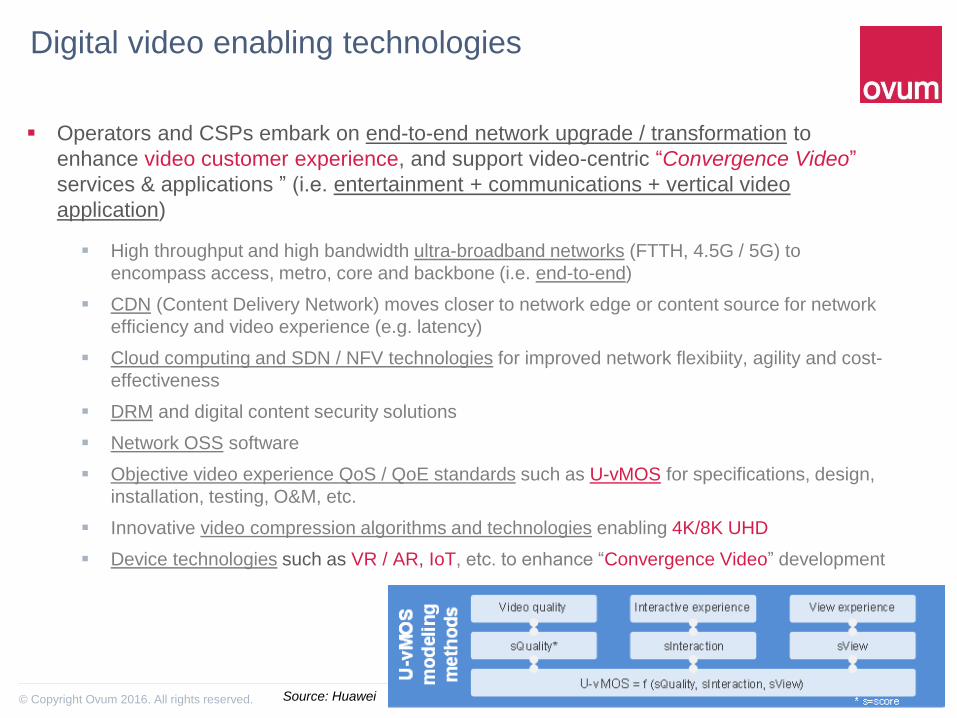

Operators and CSPs embark on end-to-end network upgrade / transformation to

enhance video customer experience, and support video-centric “Convergence Video”

services & applications ” (i.e. entertainment + communications + vertical video

application)

High throughput and high bandwidth ultra-broadband networks (FTTH, 4.5G / 5G) to

encompass access, metro, core and backbone (i.e. end-to-end)

CDN (Content Delivery Network) moves closer to network edge or content source for network

efficiency and video experience (e.g. latency)

Cloud computing and SDN / NFV technologies for improved network flexibiity, agility and cost-

effectiveness

DRM and digital content security solutions

Network OSS software

Objective video experience QoS / QoE standards such as U-vMOS for specifications, design,

installation, testing, O&M, etc.

Innovative video compression algorithms and technologies enabling 4K/8K UHD

Device technologies such as VR / AR, IoT, etc. to enhance “Convergence Video” development

Source: Huawei

24 © Copyright Ovum 2016. All rights reserved.

4K UHD: setting boundaries and definitions

ITU defines the two resolutions of ultra-

high definition (UHD) television:

4K UHD 3,840 pixels x 2,160 lines

(8.3 megapixels)

8K UHD 7,680 pixels x 4,320 lines

(33.2 megapixels)

At end 2014 , the US Consumer

Electronics Association agreed to “4K

Ultra HD” and “4K UHD” as “common

terminology to describe the new

generation of television products,

technology, and content.”

8K = 4 x 4K = 16 x FHD = 108 x SD

bandwidth challenges of 360º 3D Video

for AR/VR

2,160

4,320

1,080

480

0

8K UHD

4K UHD

FHD

Scope of the report

SD

Evolution of TV resolution*

3,840 7,680 1,920

*Horizontal axis – pixels; vertical axis - lines

640

25 © Copyright Ovum 2016. All rights reserved.

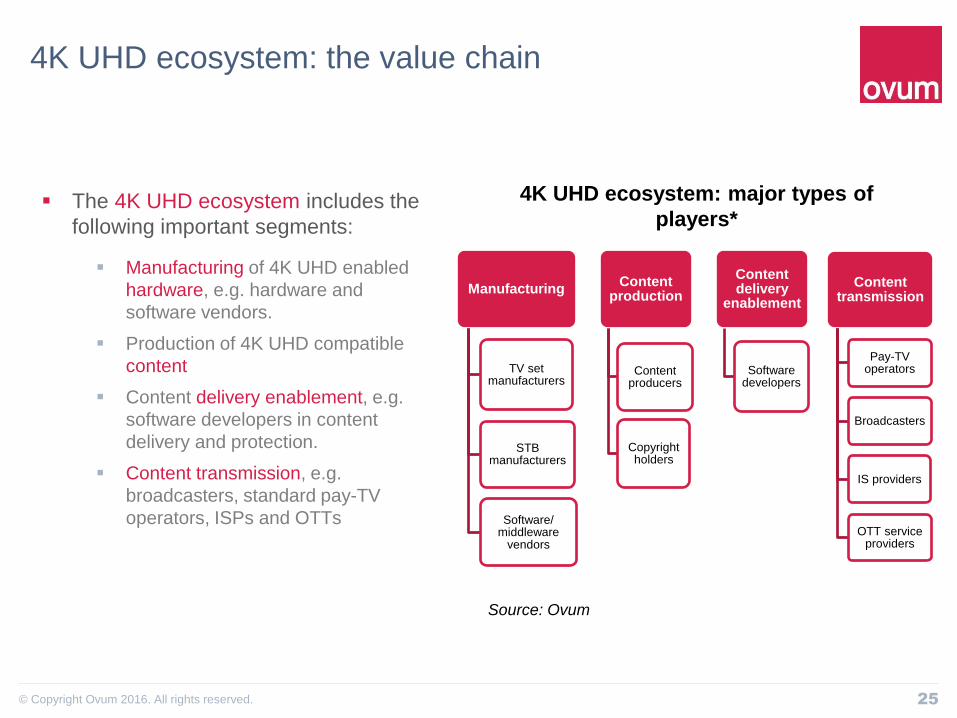

4K UHD ecosystem: the value chain

The 4K UHD ecosystem includes the

following important segments:

Manufacturing of 4K UHD enabled

hardware, e.g. hardware and

software vendors.

Production of 4K UHD compatible

content

Content delivery enablement, e.g.

software developers in content

delivery and protection.

Content transmission, e.g.

broadcasters, standard pay-TV

operators, ISPs and OTTs

Manufacturing

TV set manufacturers

STB manufacturers

Software/ middleware

vendors

Content production

Content producers

Copyright holders

Content delivery

enablement

Software developers

Content transmission

Pay-TV operators

Broadcasters

IS providers

OTT service providers

4K UHD ecosystem: major types of

players*

Source: Ovum

26 © Copyright Ovum 2016. All rights reserved.

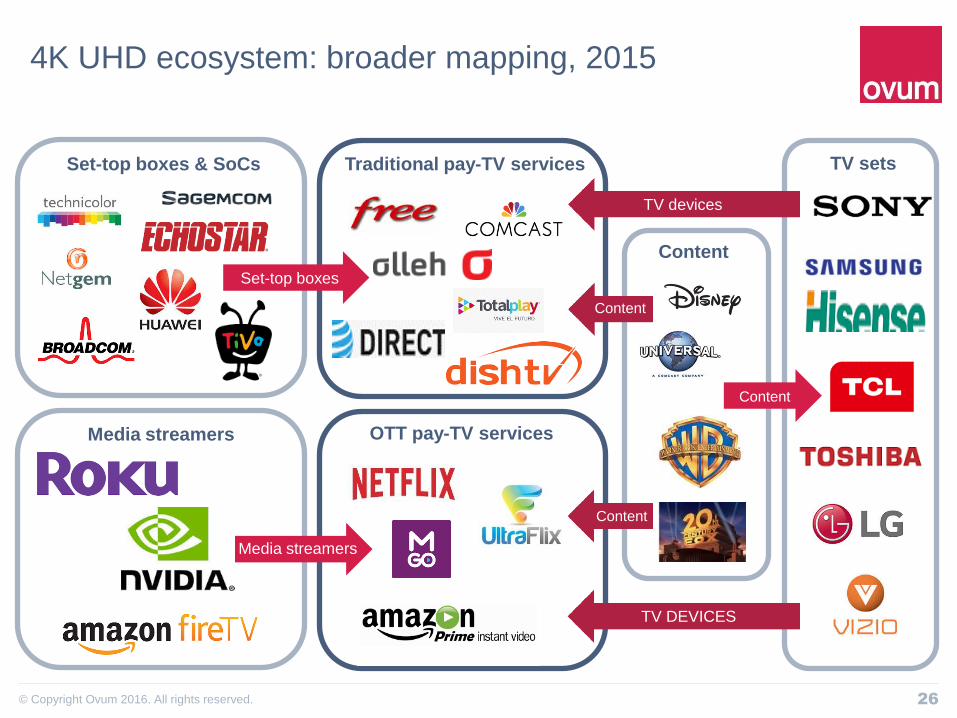

4K UHD ecosystem: broader mapping, 2015

Set-top boxes & SoCs

Media streamers

Traditional pay-TV services

OTT pay-TV services

TV sets

Content

TV devices

TV DEVICES

STBs

Media streamers

Content

Content

Content

Set-top boxes

27 © Copyright Ovum 2016. All rights reserved.

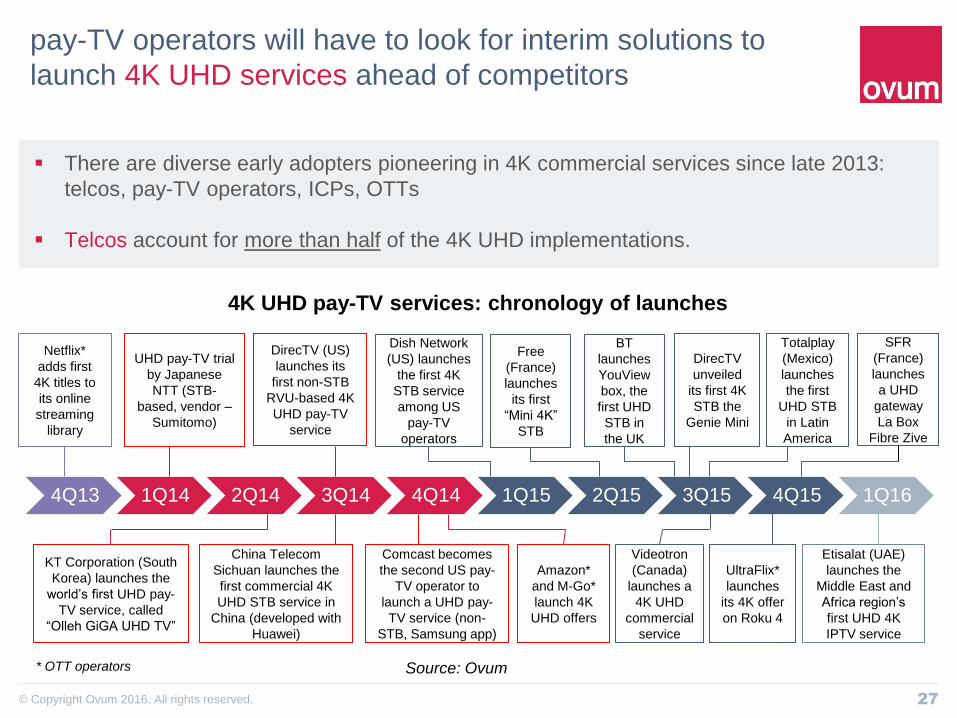

pay-TV operators will have to look for interim solutions to

launch 4K UHD services ahead of competitors

4Q13 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16

UHD pay-TV trial

by Japanese

NTT (STB-

based, vendor –

Sumitomo)

Dish Network

(US) launches

the first 4K

STB service

among US

pay-TV

operators

KT Corporation (South

Korea) launches the

world’s first UHD pay-

TV service, called

“Olleh GiGA UHD TV”

DirecTV (US)

launches its

first non-STB

RVU-based 4K

UHD pay-TV

service

Comcast becomes

the second US pay-

TV operator to

launch a UHD pay-

TV service (non-

STB, Samsung app)

Videotron

(Canada)

launches a

4K UHD

commercial

service

BT

launches

YouView

box, the

first UHD

STB in

the UK

China Telecom

Sichuan launches the

first commercial 4K

UHD STB service in

China (developed with

Huawei)

Netflix*

adds first

4K titles to

its online

streaming

library

DirecTV

unveiled

its first 4K

STB the

Genie Mini

Totalplay

(Mexico)

launches

the first

UHD STB

in Latin

America

Etisalat (UAE)

launches the

Middle East and

Africa region’s

first UHD 4K

IPTV service

There are diverse early adopters pioneering in 4K commercial services since late 2013:

telcos, pay-TV operators, ICPs, OTTs

Telcos account for more than half of the 4K UHD implementations.

4K UHD pay-TV services: chronology of launches

Source: Ovum

Amazon*

and M-Go*

launch 4K

UHD offers

UltraFlix*

launches

its 4K offer

on Roku 4

* OTT operators

SFR

(France)

launches

a UHD

gateway

La Box

Fibre Zive

Free

(France)

launches

its first

“Mini 4K”

STB

28 © Copyright Ovum 2016. All rights reserved.

VR / AR technologies & ecosystem, and

market overview

Rony Abovitz, CEO Magic Leap

29 © Copyright Ovum 2016. All rights reserved.

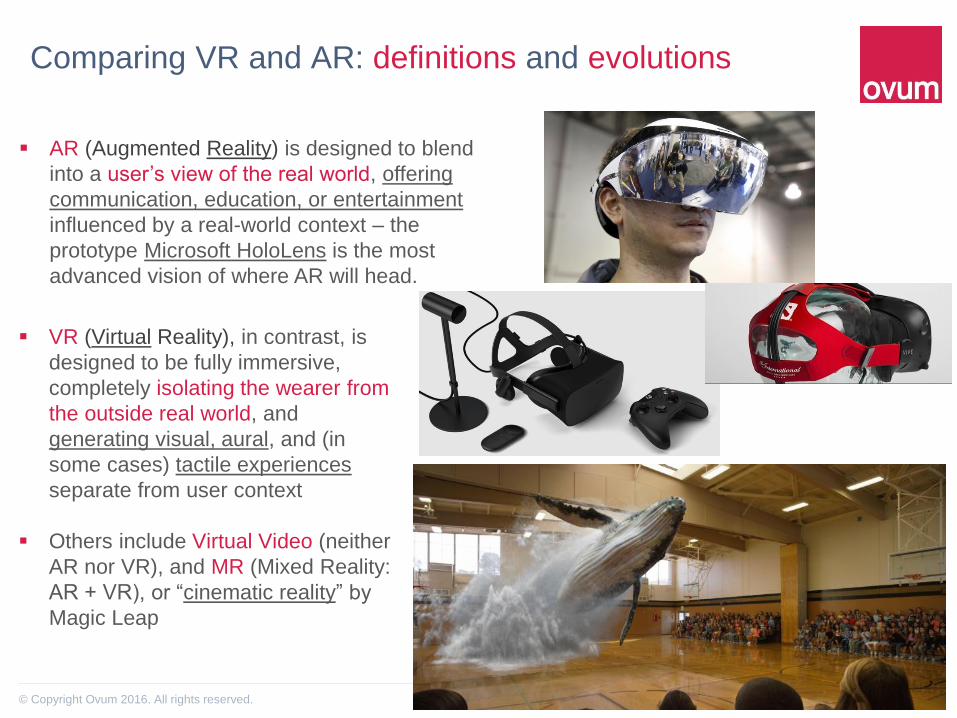

Comparing VR and AR: definitions and evolutions

AR (Augmented Reality) is designed to blend

into a user’s view of the real world, offering

communication, education, or entertainment

influenced by a real-world context – the

prototype Microsoft HoloLens is the most

advanced vision of where AR will head.

VR (Virtual Reality), in contrast, is

designed to be fully immersive,

completely isolating the wearer from

the outside real world, and

generating visual, aural, and (in

some cases) tactile experiences

separate from user context

Others include Virtual Video (neither

AR nor VR), and MR (Mixed Reality:

AR + VR), or “cinematic reality” by

Magic Leap

30 © Copyright Ovum 2016. All rights reserved.

The best way to compare the VR/AR technologies and

applications

There is a spectrum of VR/AR applications ….

Need to look at their hardware components,

platforms, which firms are involved, and, most

importantly their envisaged applications.

Involving extensive ecosystem: content &

development platform (e.g. Valve), headset,

360° camera, optics, display card, chipset, etc.

31 © Copyright Ovum 2016. All rights reserved.

VR hits first, but AR will eventually be bigger (1)

VR “goes mainstream” in 2016 though with low-end headsets and lack of enabling platforms

but real progress is being made from Google, Facebook and Starbreeze

B2B for ads & sale promotion, followed by B2C for high-end headsets …..

Add in many more mobile VR users (e.g. Google) – manufacturers go for viewing headsets to

complement their high-end devices from 2017 onwards

VR content and 360º Video applications in media and non-media segments: healthcare (virtual doctor),

education (virtual classroom)

Console platforms have the best chance of content monetization, and driving content

development ecosystem for dedicated home VR (rumour on Microsoft’s VR-capable Xbox One

by 2017)

VR drives industry-specific managed services in rights & loyalties, analytics, etc. in longer term

HTC & HP: Vive PC version

32 © Copyright Ovum 2016. All rights reserved.

VR hits first, but AR will eventually be bigger (2)

Revenues will be slow to follow though – though there is a small base of high-end VR

headset owners to buy games (or upgrade existing games)

AR has a much broader development space – running on smartphones, tablets,

wearable headsets, and dashboards, with many more application areas:

AR games such as Pokémon Go unveil monetization potential in entertainment and adjunct

business models

classic navigation in retail,

augmented ads

version 2 AR using HoloLens or Magic Leaps technology.

AR overtakes VR in terms of spending within 3-5 years – device flexibility and

applications will be more integrated in both existing user behaviours and usage

Content owners to prepare its properties and portfolios for both VR and AR

Content creators to focus at VR for wide adoption from 2017 onwards

Advertisers to focus at unique marketing experience of VR

Telcos to develop network with location-based and mutli-4K video streaming capability

33 © Copyright Ovum 2016. All rights reserved.

VR development: consumer market

0

50

100

150

200

250

300

350

400

2015 2016 2017 2018 2019 2020

Mill

ion

s o

f u

nit

s

Dedicated VR (home)

Promotional VR (portable)

Mobile VR (portable)

Dedicated VR (portable)

Total VR installed base will grow from 71 million (2016) to 337 million devices (2020):

Promotional VR lead "sales" 2016-17, with disposable experimentation devices predominating

Mobile VR will gain traction in 2017 and contribute 65% of sales by 2020.

Dedicated VR device volumes will remain small with 19–21% market share between 2018-20

(e.g. high-end dedicated headsets from Oculus and Valve, Sony’s PSVR, etc.)

2. Mobile

VR

1 Promotional

VR

3. Dedicated

VR

34 © Copyright Ovum 2016. All rights reserved.

VR development: enterprise market

0% 10% 20% 30% 40%

Telemedicine

Contact centre /mass customer service

High-capacity meetings (25+ participants)

Meetings with customers or clients - support

Meeting/collaboration with partners

Employee training

Internal meetings

Meetings with Partners

Videoconferencing users

Mobile videoconferencing Desktop videoconferencing Room-based videoconferencing

Video applications have high development potential in the enterprise segment:

Video communications services such as video-conferencing

Video surveillance to be key component of managed security solutions

VR/AR maturity (e.g. 360º cameras) to accelerate diverse vertical video applications (e.g.

contact center, telemedicine, training, sales promotion / demonstration, etc.)

35 © Copyright Ovum 2016. All rights reserved.

Key takeaways

Digital (video) is the future of growth (40% out of 1,627B in 2025): the way forwards is

innovation and constant change – digital advertising is the approach to development.

Video will become the basic services before 2020. It offers tremendous opportunities &

challenges to early movers

Consumers will invest in experiences they value: emotion and time will become

increasingly precious

Competition will shift from “delivery” to “platform” and ultimately to “data & design”

OTT SVOD sets the trend of future development ... Operators leverage OTT content for

enhanced competition and customer experience delivery

There is fully array of video enabling technologies for “Convergence Video” development

(i.e. entertainment + communications + vertical video applications)

Many telcos early invest and launch 4K UHD service

VR hits first (2016 - 2017), but AR will eventually be bigger (2018 - 2020)

36 © Copyright Ovum 2016. All rights reserved.

The End

Thank you