df 09/21/06

DESCRIPTION

TRANSCRIPT

Dean Foods Company

Prudential Equity Group’s15th Annual

Back-To-SchoolConsumer Conference

September 7, 2006

Forward Looking Statements

The following statements made in this presentation are “forward looking” and are made pursuant to the safe harbor provision of the Securities Litigation Reform Act of 1995: statements relating to (1) projected sales (including for individual segments, for specific product lines and for the company as a whole), profit margins, net income and earnings per share, (2) our growth strategy, (3) our branding initiatives (4) our integration plans, and (5) our cost-savings initiatives. These statements involve risks and uncertainties that may cause results to differ materially from those set forth in this presentation. Financial projections are based on a number of assumptions. Actual results could be materially different than projected if those assumptions are erroneous. Sales, profit margins, net income and earnings per share can vary based on a variety of economic, governmental and competitive factors, all of which are identified in our filings with the Securities and Exchange Commission, including our Annual Report on Form 10K (which can be accessed on our website at www.deanfoods.com or the website of the Securities and Exchange Commission at www.sec.gov). The success of our branding initiatives will depend on a number of factors, including customer and consumer acceptance of both the products themselves and the prices that we intend to charge for those products. We have many competitors with greater resources than ours, and significant additional spending or innovations by our competitors could render our products less successful than we currently expect. All forward looking statements in this presentation speak only as of the date of this presentation. We expressly disclaim any obligation or undertaking to release publicly any updates or revisions to any such statements to reflect any change in our expectations with regard thereto or any changes in the events, conditions or circumstances on which any such statement is based.

Agenda

Unique Beverage Platform

Dean Dairy Group

WhiteWave Foods

Well Positioned for Sustained Growth

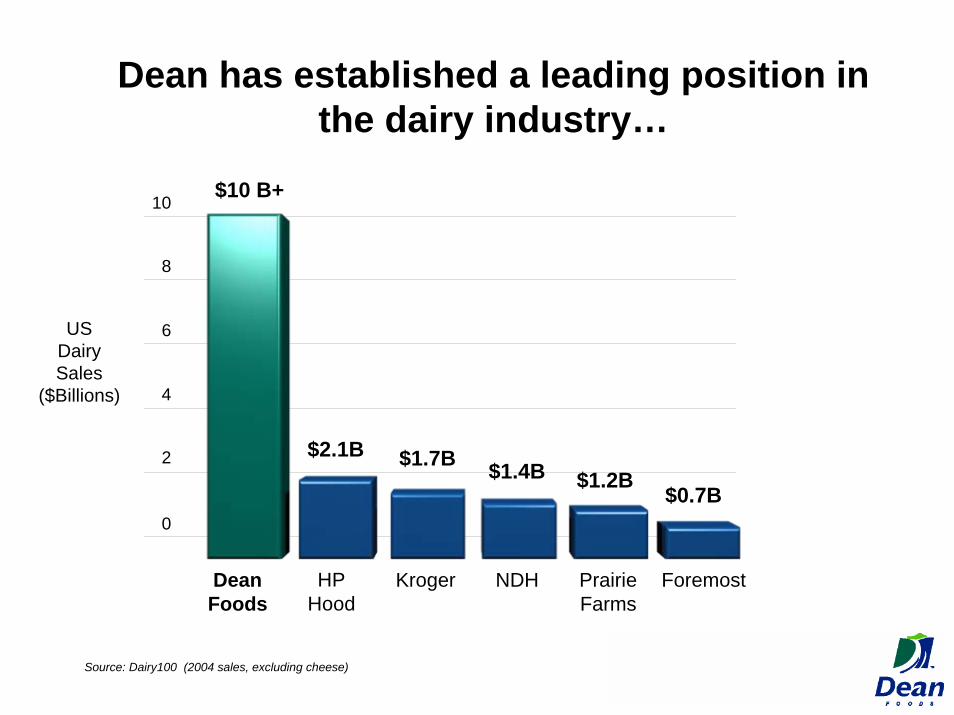

Dean has established a leading position in the dairy industry…

10

8

6

4

2

0

DeanFoods

HPHood

Kroger NDH PrairieFarms

Foremost

$10 B+

$2.1B $1.7B $1.4B $1.2B$0.7B

USDairySales

($Billions)

Source: Dairy100 (2004 sales, excluding cheese)

…and is the only national dairybeverage company

Leading portfolio of national and regional dairy brands in health and wellness beverage categories

National manufacturing system with fullest set of capabilities and with market proximity as a strategic advantage

Unparalleled refrigerated distribution network

Deep customer relationships at local, regional and national levels across all channels

Potential to innovate across the entire dairy category

Experienced management team with deep company, dairy and beverage industry expertise

Strong RegionalBrands

Strong branded position,complemented by private label…

National BrandsPrivateLabel

37% BrandedSales

63%

Dean Foods 2005Sales Mix

… supported by the country’s only national manufacturing system…

… with flexible production capabilities…

Short Shelf Life16-18 days

Extended Shelf Life45-60 days

Aseptic6-9 months

Any consumer,any occasion

Ice Creamand Novelties

…in more than just milk…

Cottage Cheese

Yogurts

…in more than just milk…

Sour Creams

Juices Teas

Waters

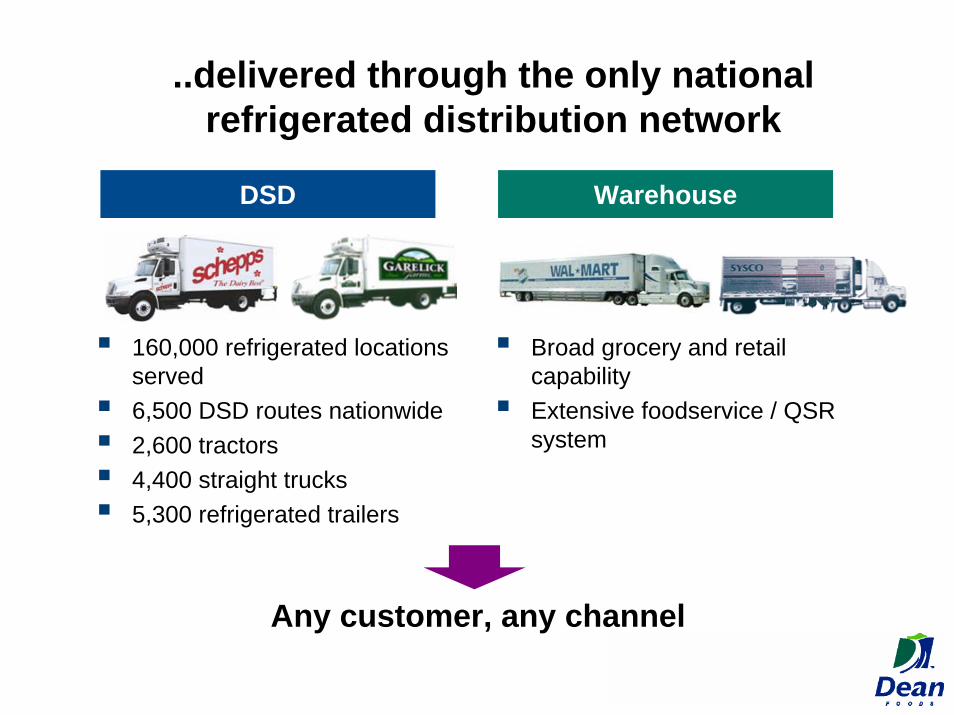

..delivered through the only national refrigerated distribution network

160,000 refrigerated locations served6,500 DSD routes nationwide2,600 tractors4,400 straight trucks5,300 refrigerated trailers

Broad grocery and retail capabilityExtensive foodservice / QSR system

Any customer, any channel

WarehouseDSD

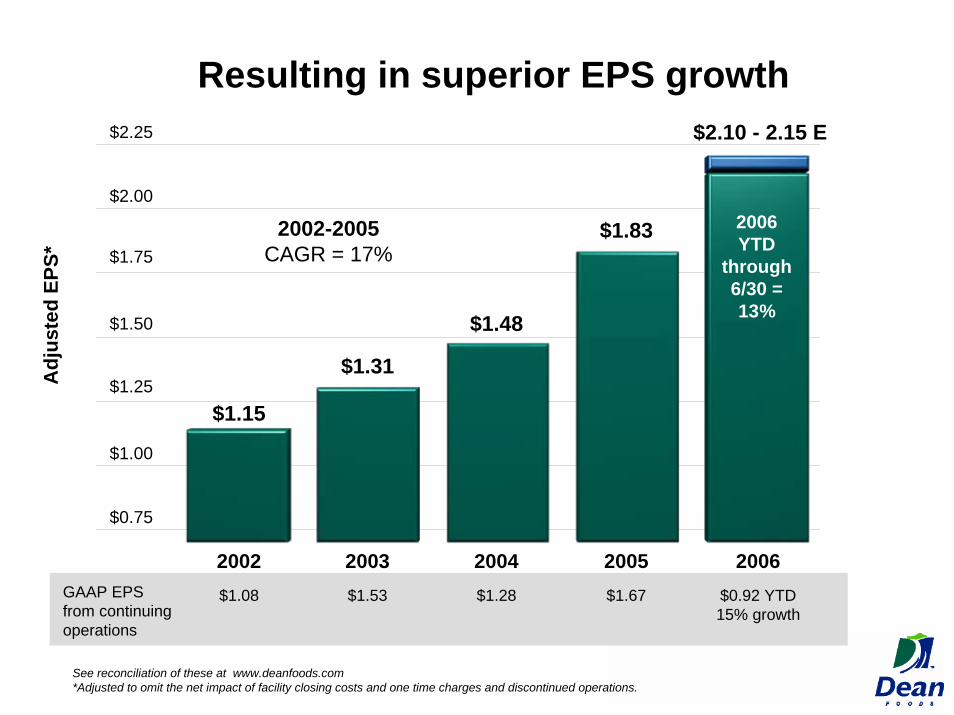

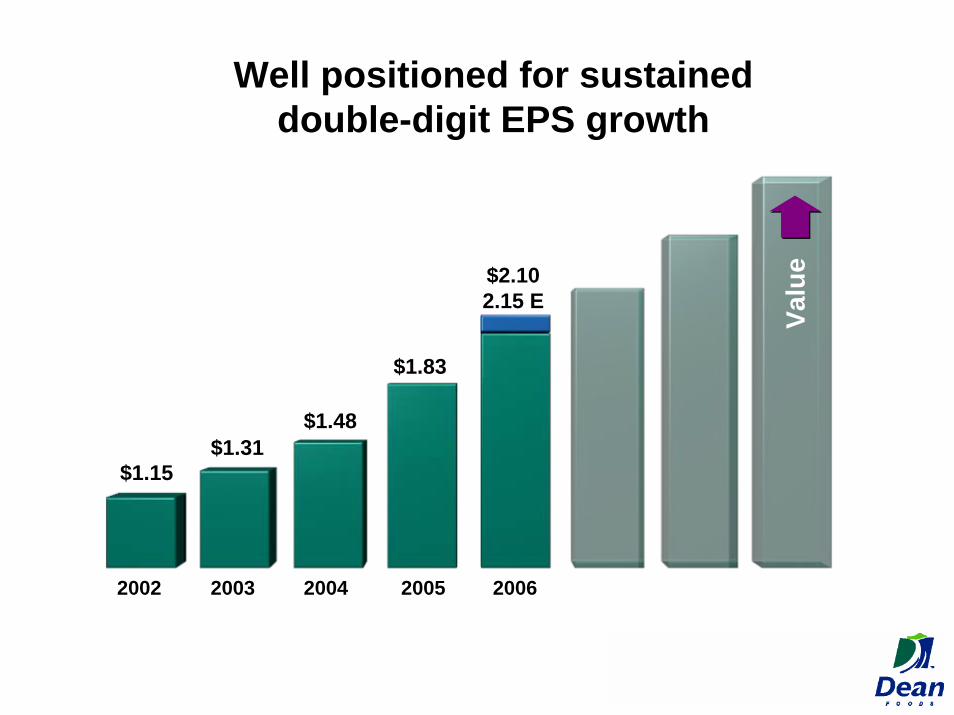

Resulting in superior EPS growth

2002-2005CAGR = 17%

$1.15

$1.31

$1.48

$1.83

$2.10 - 2.15 E

$0.75

$1.00

$1.25

$1.50

$1.75

$2.00

$2.25

2002 2003 2004 2005 2006GAAP EPSfrom continuing operations

$1.08 $1.53 $1.28 $1.67 $0.92 YTD15% growth

2006 YTD

through 6/30 = 13%

Adj

uste

d EP

S*

See reconciliation of these at www.deanfoods.com*Adjusted to omit the net impact of facility closing costs and one time charges and discontinued operations.

…and strong cash flow generation

$385M $414M

$542M

$265M

Cash Flow from Continuing Operations

2003 2004 2005 2006

$260M$301M $287M

$114M

Capital Expenditures for Continuing Operations

2003 2004 2005 2006

~$250M

YTD6/30

YTD6/30

$0

$5

$10

$15

$20

$25

$30

$35

$40

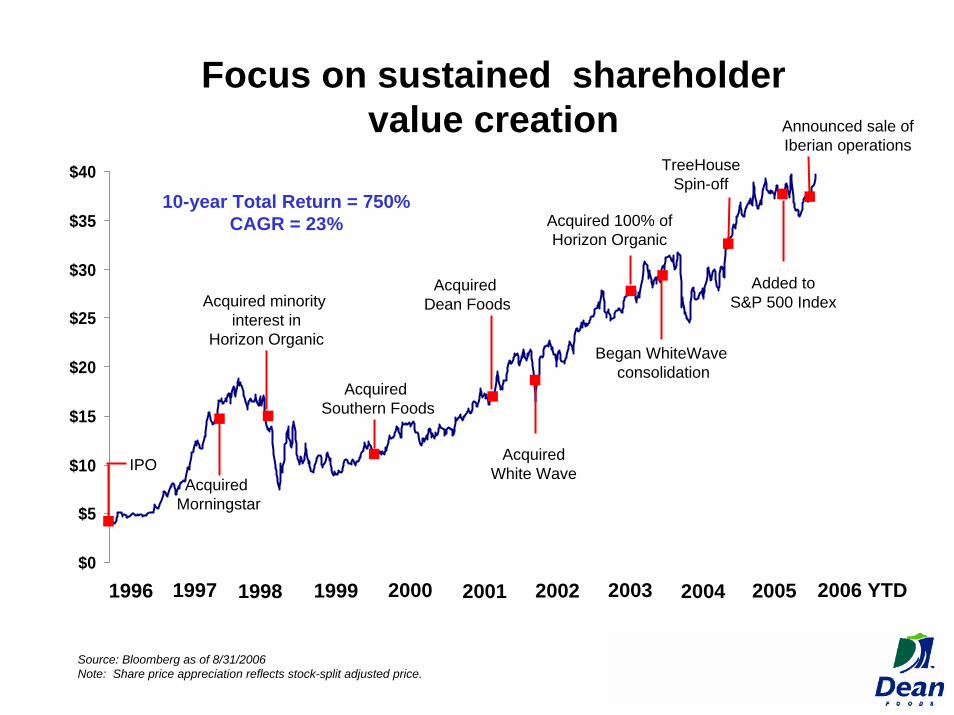

Focus on sustained shareholdervalue creation

Acquired Morningstar

Acquired Dean Foods

AcquiredWhite Wave

Acquired 100% ofHorizon Organic

Began WhiteWaveconsolidation

TreeHouseSpin-off

Source: Bloomberg as of 8/31/2006Note: Share price appreciation reflects stock-split adjusted price.

Added toS&P 500 Index

Acquired Southern Foods

IPO

Acquired minority interest in

Horizon Organic

10-year Total Return = 750%CAGR = 23%

Announced sale of Iberian operations

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 YTD

2006 first half highlightsDairy Group

– Dairy Group milk volume growth of 2.8%– Initiating a multiple-year productivity and capability-building program

WhiteWave Foods– Continued strong growth of the core brands – Strengthening the foundation with investments in G&A

infrastructure, and SAP

Dean Foods Company– Adjusted EPS growth of 13%– Announced the sale of Iberian operations, sharpening focus on

largest opportunities– Strong cash flow, supporting share repurchase of $136 million

through June 30,and debt paydown

On Track for Another Strong Year

Agenda

Unique Beverage Platform

Dean Dairy Group

WhiteWave Foods

Well Positioned for Sustained Growth

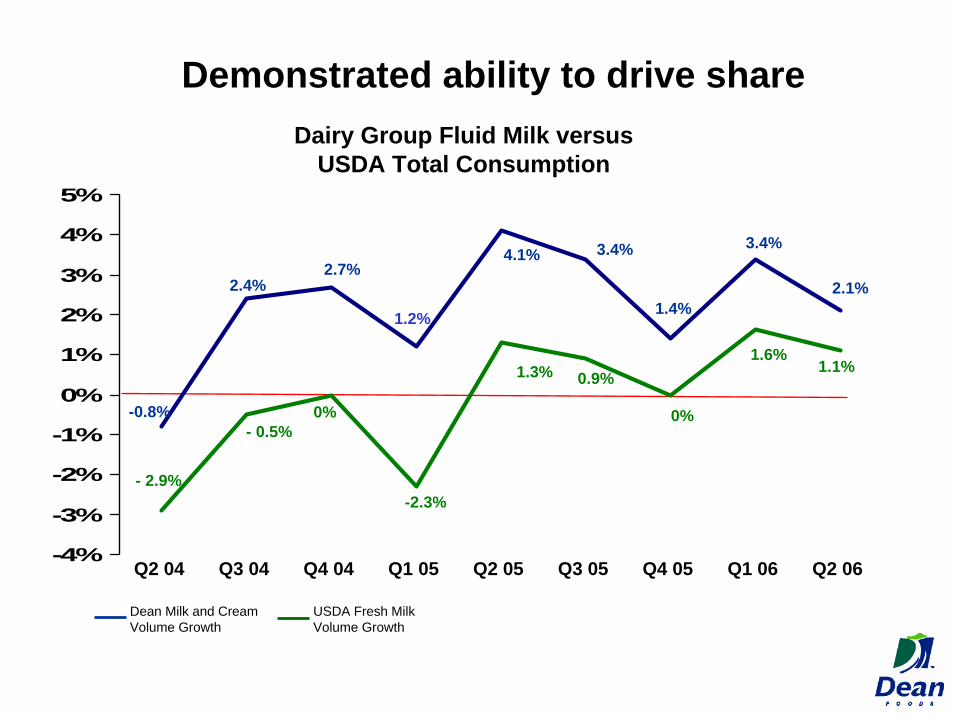

-4%

-3%

-2%

-1%

0%

1%

2%

3%

4%

5%

Dairy Group Fluid Milk versusUSDA Total Consumption

USDA Fresh MilkVolume Growth

Dean Milk and CreamVolume Growth

-0.8%

- 2.9%

- 0.5%

-2.3%

0%

1.3% 0.9%

2.4%2.7%

1.2%

4.1% 3.4%

Q2 04 Q3 04 Q4 04 Q1 05 Q2 05 Q3 05 Q4 05

0%

1.4%

3.4%

1.6%

Q1 06

1.1%

2.1%

Q2 06

Demonstrated ability to drive share

Dairy Group Overview

$6B+ in annual freshmilk sales plus:($ Millions)

0

200

400

600

800

2005 Sales Mix

IceCream

Yogurt &Cultured

ESL &Creamers

Juice,Water

and Tea

Ice Cream Mix

Other

Entering the next phase ofDairy Group evolution

Shifting volume to more efficient facilities, elimination of excess capacity to reduce costs

Demonstrated ability to drive market share

Significant management focus on portfolio rationalization and WhiteWave consolidation

Early steps towards developing the future Dairy Group operating model

75 fold US dairy revenue growth from 1994 to 2002

– $100 million to$7.6 billion

Expanded from 2 facilities to over 100

Developed only nationwide footprint in the industry

Four times larger than nearest competitor

Primary focus on rollup, limited change to local dairy operating model

Consolidation

1994 - 2001

Transition

2002 - 2006

Evolve the Dairy Group operating model to maximize the benefits of its scale advantage

Strengthen functional expertise to reduce costs and sustain year on year productivity

Enhance selling capability

Ensure pace of change does not inhibit business performance

Opportunity to sustain strong operating profit growth

Transformation

2007 - 2010

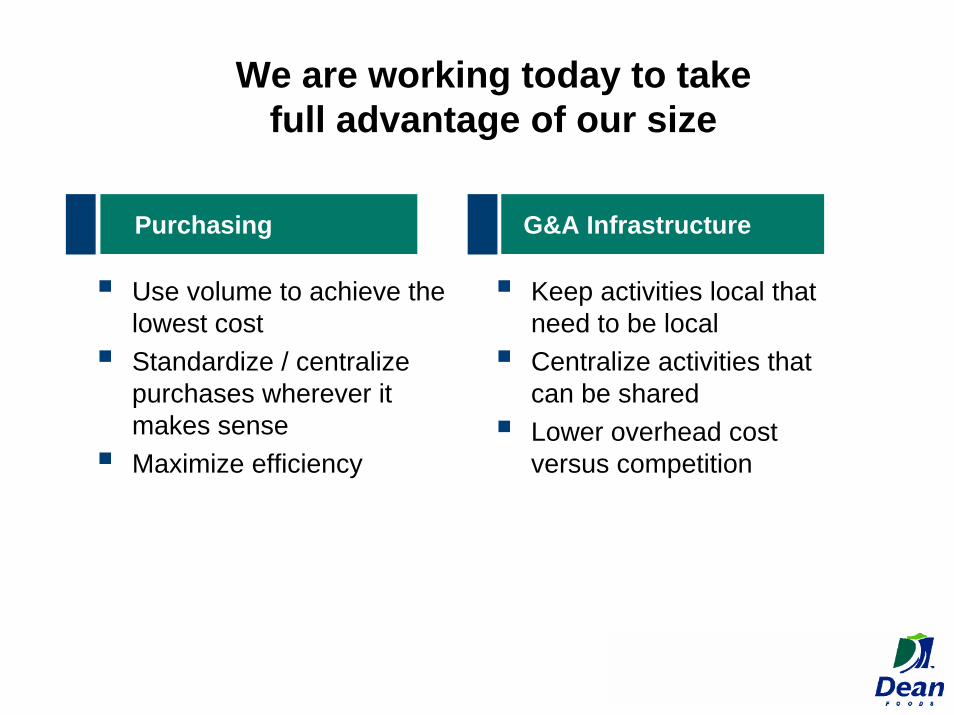

Purchasing G&A Infrastructure

We are working today to takefull advantage of our size

Use volume to achieve the lowest costStandardize / centralize purchases wherever it makes senseMaximize efficiency

Keep activities local that need to be localCentralize activities that can be sharedLower overhead cost versus competition

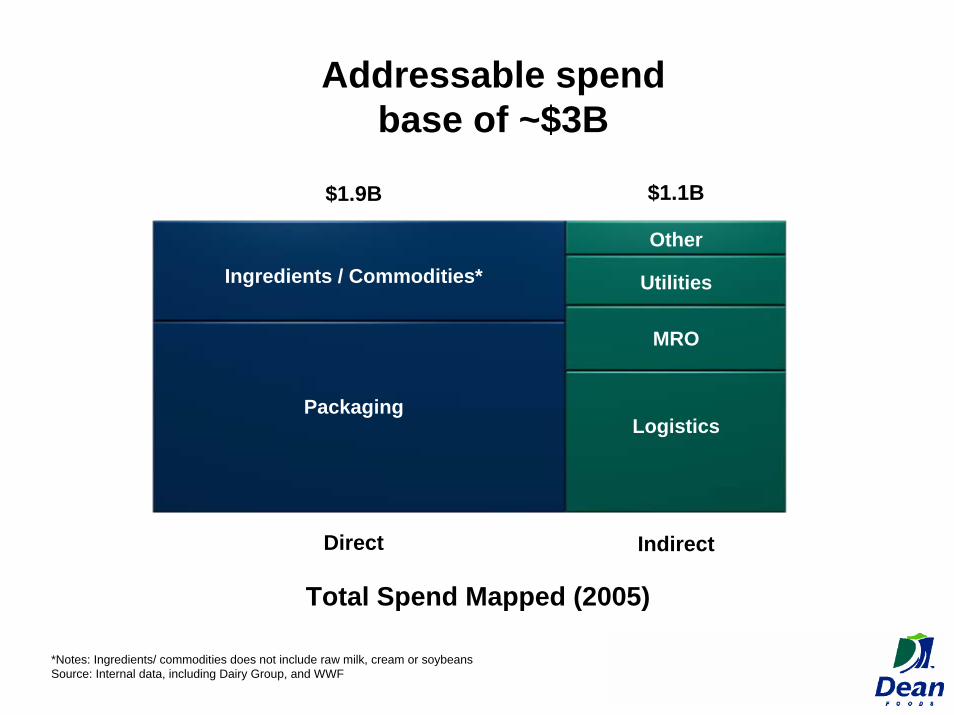

Addressable spendbase of ~$3B

Ingredients / Commodities*

Packaging

Other

Utilities

MRO

Logistics

Direct Indirect

$1.1B$1.9B

Total Spend Mapped (2005)

*Notes: Ingredients/ commodities does not include raw milk, cream or soybeans Source: Internal data, including Dairy Group, and WWF

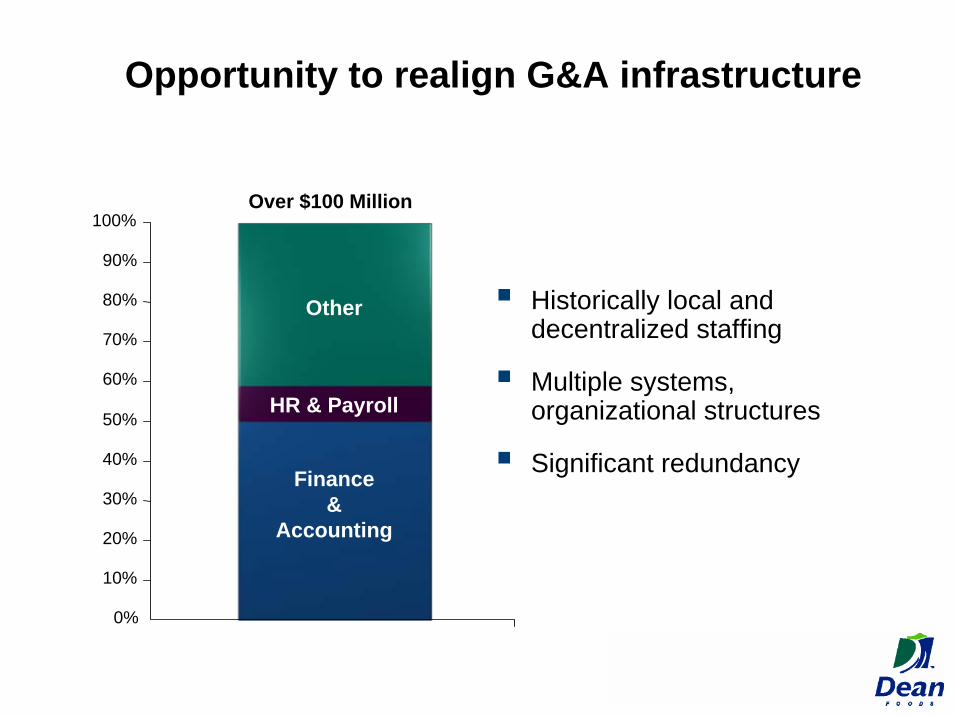

Opportunity to realign G&A infrastructure

Historically local and decentralized staffing

Multiple systems, organizational structures

Significant redundancyFinance &

Accounting

HR & Payroll

Other

Over $100 Million

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Need to build functional expertisein manufacturing and selling

Lowest cost facilitiesProducing the right products in the right facilitiesWith the right capital investmentsEnable continuous improvement mindset

Upgrade systemsMaximize truck utilizationOptimize route designLeverage network scaleBuild selling and merchandising capability

ManufacturingInfrastructure

Direct to StoreDistribution

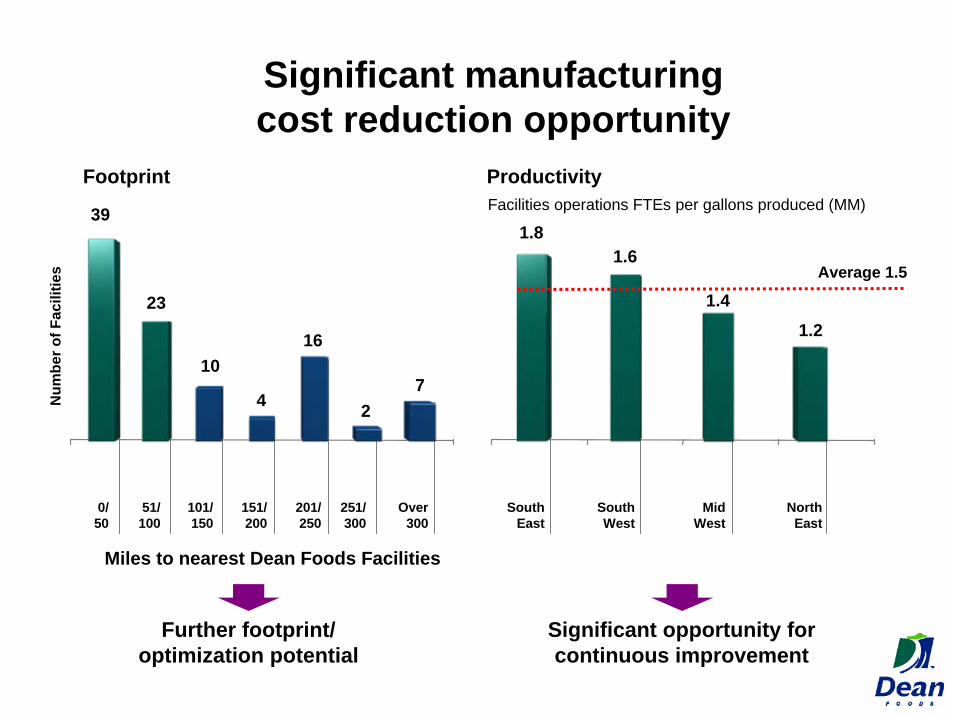

Significant manufacturingcost reduction opportunity

39

23

10

4

16

27

0/50

51/100

101/150

151/200

201/250

251/300

Over300

1.81.6

1.41.2

SouthEast

SouthWest

MidWest

NorthEast

Average 1.5

Facilities operations FTEs per gallons produced (MM)

Miles to nearest Dean Foods Facilities

Num

ber o

f Fac

ilitie

s

Further footprint/ optimization potential

Footprint Productivity

Significant opportunity for continuous improvement

Better leverage the only nationalrefrigerated DSD system

Build additional selling capability– Increase sales per route/stop– Offer customers complete dairy

solution– Innovate with branded/single

serve offerings to improve drop size and margin

Maximize route efficiency through technology-based toolsEliminate redundant or overlapping routes

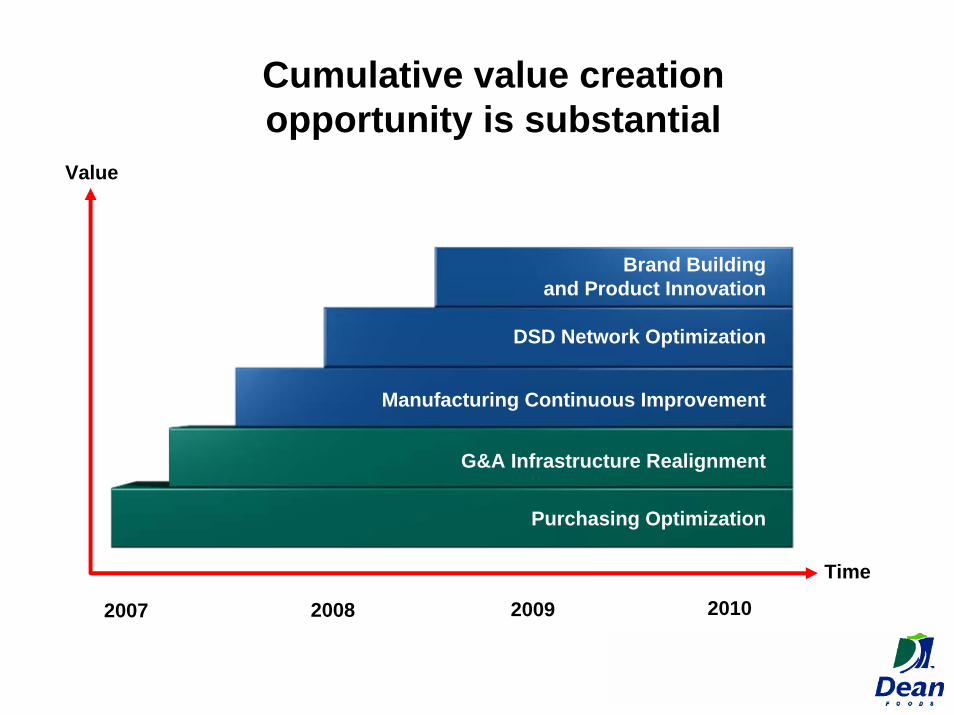

Cumulative value creationopportunity is substantial

Purchasing Optimization

Manufacturing Continuous Improvement

G&A Infrastructure Realignment

DSD Network Optimization

Brand Buildingand Product Innovation

Time

2007 20102008 2009

Value

Dairy industry evolution

Consolidated industrySingle national player – Dean FoodsGrowing profitability; resources to investInvestment in innovation and marketingEmergence of national brandsPortfolio of strong regional brandsGreater consumer focus on nutrition

Fragmented industry

Local companies/little scale

Locally managed, lack of functional expertise

Limited profitability and financial resources

Infrequent innovation

Limited marketing

High private label penetration

TraditionalDairy

NewDairy

Agenda

Unique Beverage Platform

Dean Dairy Group

WhiteWave Foods

Well Positioned for Sustained Growth

WhiteWave Foods: Strong brandswith a history of robust growth

2000 2001 2002 2003 2004 2005

5-Yr CAGR ofKey Brands = 28%

Note: Assuming full ownership in all comparable periods.

% of 2005 WhiteWave

Sales

6%

28%

23%

20%

15%

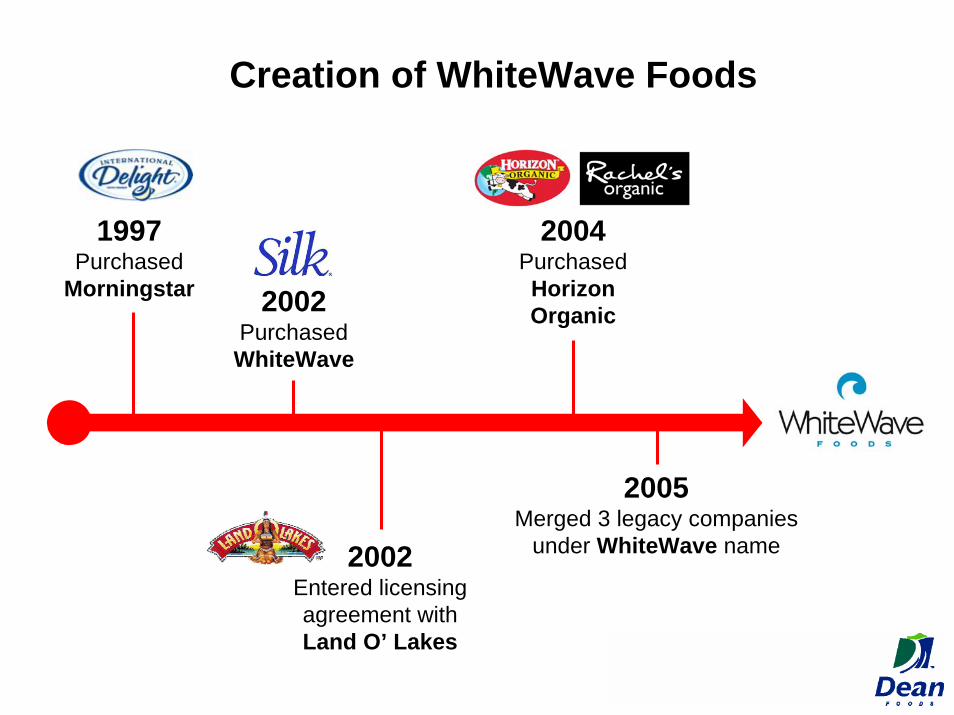

Creation of WhiteWave Foods

1997Purchased

Morningstar

2002Entered licensing agreement with Land O’ Lakes

2004Purchased HorizonOrganic

2005Merged 3 legacy companies

under WhiteWave name

2002Purchased WhiteWave

Integration of 3 legacy companies

Time2004 2005-2006 2007-2008

Sustainable growthand superior returns

3 separate,legacy companies

– 3 faces to the customer

– 3 separate,under-leveragedsupply chains

– Internal redundancy– Limited process

and systems infrastructure

One company

– 1 organization– 1 leadership team– 1 “sales” face to

the customer– Supply chain

integration in progress

– Process and systems build-out in progress

One, unified company;

best-in-class brands, talent and

infrastructure

– Focused portfolio of premium brands

– 1 face to the customer

– Fully integrated supply chain

– Top-talent organization

– Best-in-class processes and systems

Platform for further premiumbranded beverage growth

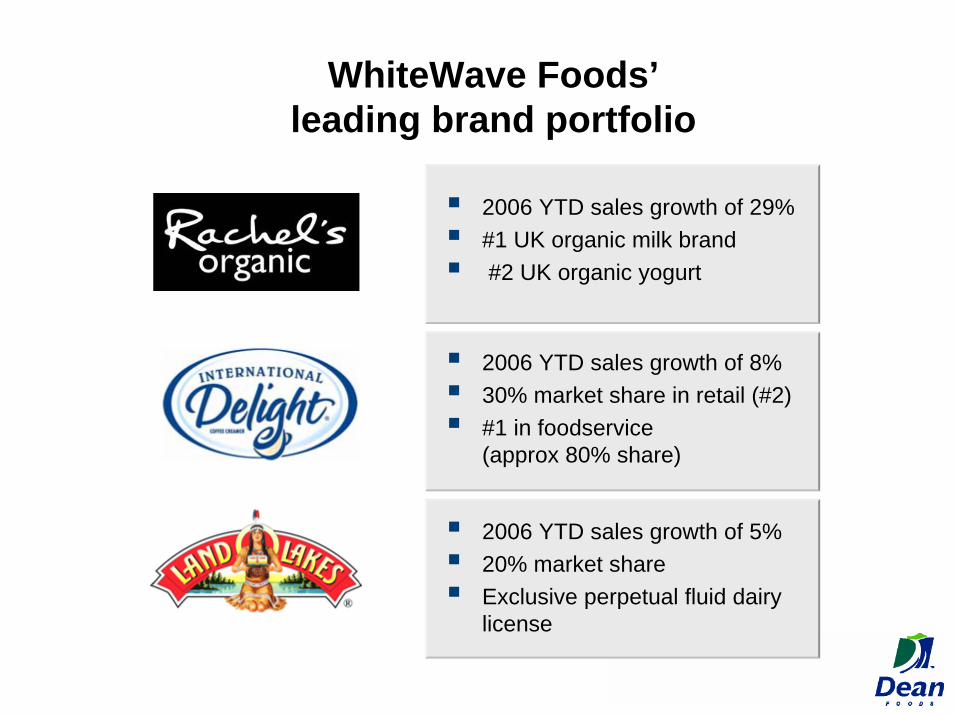

WhiteWave Foods’leading brand portfolio

2005 Sales: $337 million

2005 growth of 20%

2006 YTD* growth of 14%

74% market share**

Strategic Summary

No. 1 soy beverage

Compelling health benefits

Significant growth opportunity

– Education– Innovation

Focus on driving trial and adoption in US

Multiple opportunities for growth

– Product adjacencies– International

*Through June 30, 2006 for continuing products**Source: IRI, Spins, IRI Walmart panel data

Market studies indicate a$1B+ soymilk category by 2008

$1.1B$1.2B

$1.4B

Soyatech Cambridge Mintel

2008 Soymilk Sales Estimates ($Billions)

Rapid growth of the soymilkcategory should continue

Penetration should increase– Virtually all sales are to 11%

of households– These buyers represent 80%

of category volume– Another 30% of US households

are interested in soymilkFrequency should increase– Core soymilk households still

consume 3X as much conventional milk as soymilk

Represents significant opportunity to grow the category

WhiteWave Foods’leading brand portfolio

2005 Sales: $273 Million

2005 milk sales increaseof 44%

2006 YTD* growth of 28%

46% market share**

Strategic Summary

Invest to increase supply

localize the supply chainand drive margin

Realign pricing as supply increases for profitability and sustainable category growth

Drive growth on core fluid milk by targeting interested organically inclined consumers

*Through June 30, 2006 for continuing products**Source: IRI, Spins, IRI Walmart panel data

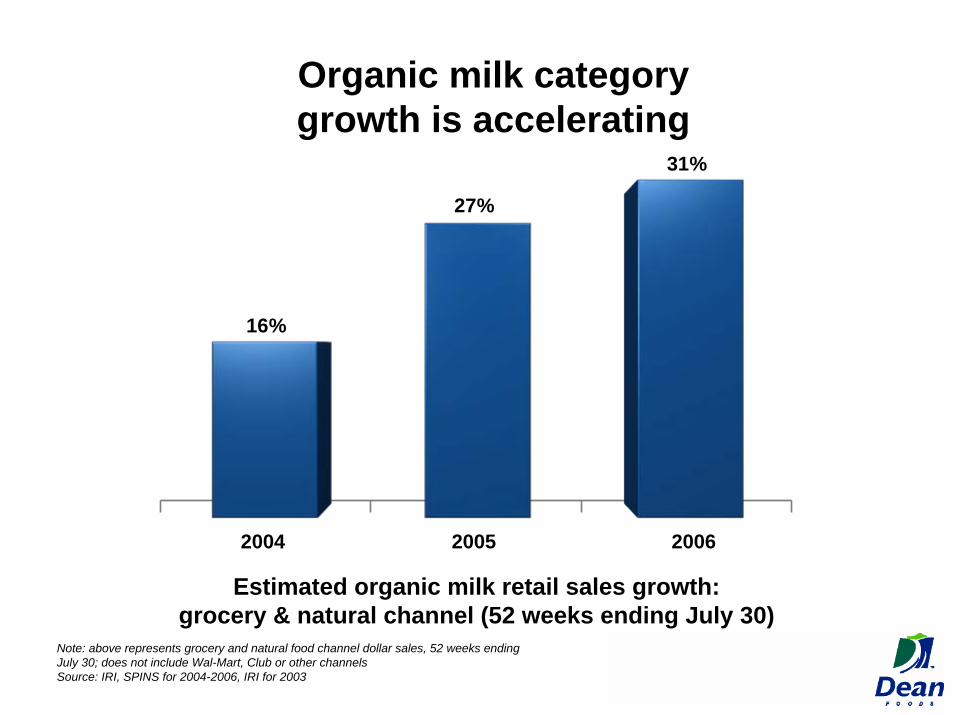

Organic milk categorygrowth is accelerating

Estimated organic milk retail sales growth:grocery & natural channel (52 weeks ending July 30)

Note: above represents grocery and natural food channel dollar sales, 52 weeks endingJuly 30; does not include Wal-Mart, Club or other channelsSource: IRI, SPINS for 2004-2006, IRI for 2003

16%

27%

31%

2004 2005 2006

Rapid growth of the organicmilk category should continue

Penetration should increase– Virtually all sales are to 3.3% of

households, up 1.2 pts (150 index) versus 20031.

– Another 29% of US households are interested in organic milk2.

Frequency should increase– 22% of consumers view organic as

“extremely” or “very important” to healthy lifestyle3.

1. IRI Household Panel.2. Cambridge Group – Demand Landscape March 2006.3. Natural Marketing Institute: Health and Wellness Trends Report 2006.

Represents significant opportunity to grow the category

Supply regionality for Horizon Organic

We have a locally aligned supply chainDesigned to provide shortest time from farmto tableThis will increasingly become a strategic advantage

9%

22%10%

11%

18%

13% 17%

We are investing to grow supply

Adding new family farms to producer network is our first priority – 342 currently, 240 in

transition– Horizon Organic Producer

Education Program –Assists farmers in transition to organic

– Transition takes time 12 months for cows, 36 months for land

Pursuing strategic partnerships with innovative producersSelectively leveraging supply at company-owned farms – 20% of current supply

Expecting supply growthin excess of 20% for 2007

WhiteWave Foods’leading brand portfolio

2006 YTD sales growth of 29%#1 UK organic milk brand#2 UK organic yogurt

2006 YTD sales growth of 8%30% market share in retail (#2)#1 in foodservice(approx 80% share)

2006 YTD sales growth of 5%20% market shareExclusive perpetual fluid dairy license

Agenda

Unique Beverage Platform

Dean Dairy Group

WhiteWave Foods

Well Positioned for Sustained Growth

Well positioned for long term growth

Dairy Group entering next phase of long-term strategy– Consistently growing market share

– Multi-year productivity and capability-building program to extend advantage and improve margins

WhiteWave Foods executing for growth– Driving strong growth of well-positioned brands in attractive

categories

– Pushing efficiency through integration of businesses

– Focus on building an innovation center of excellence

Intense focus on cash flow generation andsustained shareholder value creation

WhiteWave Foods

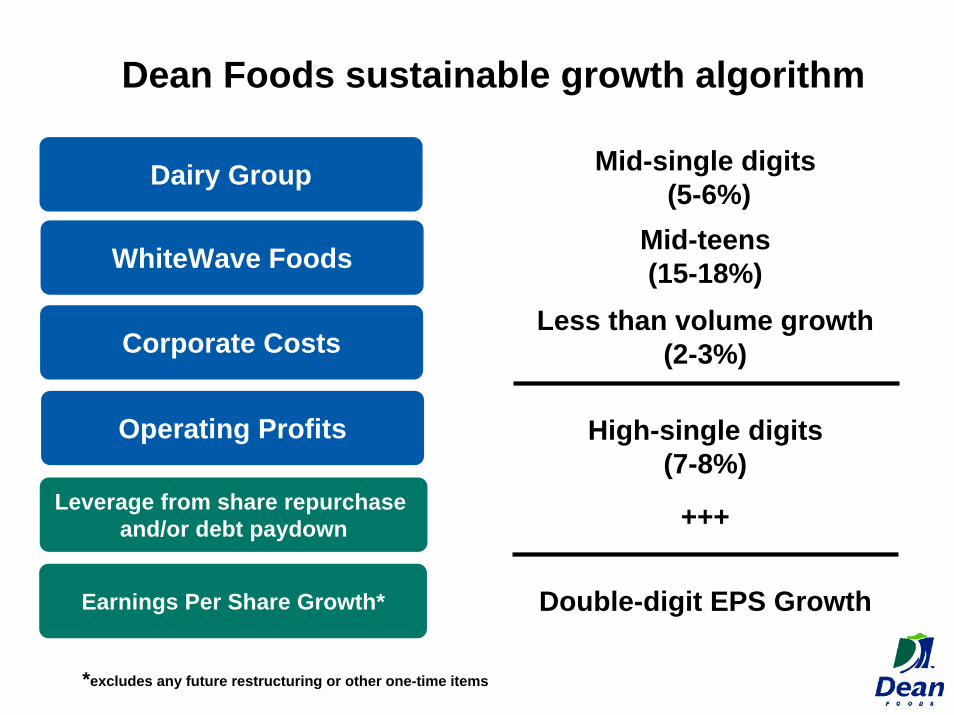

Dean Foods sustainable growth algorithm

Dairy Group

Leverage from share repurchase and/or debt paydown

Corporate Costs

Operating Profits

Earnings Per Share Growth*

Mid-single digits(5-6%)

Mid-teens (15-18%)

Less than volume growth (2-3%)

High-single digits(7-8%)

+++

Double-digit EPS Growth

*excludes any future restructuring or other one-time items

Well positioned for sustaineddouble-digit EPS growth

$1.15$1.31

$1.48

$1.83

$2.102.15 E

2002 2003 2004 2005 2006

Valu

e

Dean Foods Company

Prudential Equity Group’s15th Annual

Back-To-SchoolConsumer Conference

September 7, 2006

Reconciliation of Diluted to Adjusted EPS

March 31, June 30, Sept. 30, Dec. 31, March 31, June 30,2002 2003 2004 2005 2005 2005 2005 2005 2006 2006

Diluted EPS from continuing operations (GAAP): 1.08$ 1.53$ 1.28$ 1.67$ 0.32$ 0.47$ 0.40$ 0.48$ 0.38$ 0.53$

Facility closing and reorganization costs 0.07 0.04 0.09 0.15 0.03 0.01 0.07 0.04 0.02 0.02

Settlement of tax matter (0.04) - - - - - - - - -

Losses on investment in affiliate 0.04 - - - - - - - - -

Gain on sale of frozen pre-whip topping business - (0.25) - - - - - - - -

Gain on litigation settlement - - (0.02) - - - - - - -

Write-off of deferred financing costs - - 0.13 - - - - - - -

Other non-recurring charges - (0.01) - 0.01 0.01 - - - - -

Diluted EPS from continuing operations (Adjusted) 1.15$ 1.31$ 1.48$ 1.83$ 0.36$ 0.48$ 0.47$ 0.52$ 0.40$ 0.55$

Three Months EndedFiscal Year Ended December 31,