development of cost estimation tools for total

TRANSCRIPT

215Tomohisa NAGATA, et al.: Cost Estimation Tools for Occupational Safety and Health Activities

information on OSH activities and occupational health services. Conclusions: The standardized information obtained from our OSH and occupational health cost estimation tools can be used to manage OSH costs, make comparisons of OSH costs between companies and organizations and help occupational health physi-cians and employers to determine the best course of action.(J Occup Health 2014; 56: 215–224)

Key words: Costs and cost analysis, Economics, Occupational safety and health

Occupational safety and health (OSH) activities are conducted as part of business administration and entail corporate costs. Companies have to adhere to legal, financial and moral requirements of OSH1), and employers have to consider the welfare of their employees and provide adequate OSH to ensure that activities are efficient and productive. Employers have a need for relevant and comparable information so that they can prioritize their budget and thus attain the greatest OSH gains for their workforce2−4). OSH staff implement OSH activities according to a company’s individual policies while at the same time maintaining communication with employers and employees and attempting to provide the highest quality OSH at an appropriate cost5).

OSH costs are not wasted expenses but an invest-ment in prevention. Especially in occupational health (OH) services as forms of health management and health promotion, OH costs are a human resource investment for improvement of health and wellness

Abstract: Development of Cost Estimation Tools for Total Occupational Safety and Health Activities and Occupational Health Services: Cost Estimation from a Corporate Perspective: Tomohisa NAGATA, et al. Department of Occupational Health Practice and Management, Institute of Industrial Ecological Sciences, University of Occupational and Environ-mental Health, Japan—Objectives: The aim of the present study was to develop standardized cost estima-tion tools that provide information to employers about occupational safety and health (OSH) activities for effec-tive and efficient decision making in Japanese compa-nies. Methods: We interviewed OSH staff members including full-time professional occupational physicians to list all OSH activities. Using activity-based costing, cost data were obtained from retrospective analyses of occupational safety and health costs over a 1-year period in three manufacturing workplaces and were obtained from retrospective analyses of occupational health services costs in four manufacturing workplaces. We verified the tools additionally in four workplaces including service businesses. Results: We created the OSH and occupational health standardized cost estimation tools. OSH costs consisted of personnel costs, expenses, outsourcing costs and investments for 15 OSH activities. The tools provided accurate, relevant

Development of Cost Estimation Tools for Total Occupational Safety and Health Activities and Occupational Health Services: Cost Estimation from a Corporate Perspective

Tomohisa Nagata1, Koji Mori1,2, Yutaka Aratake3, Hiroshi Ide4, Hiromi Ishida5, Junichiro Nobori5, Reiko Kojima6, Kiminori Odagami7, Anna Kato2, Akizumi Tsutsumi8 and Shinya Matsuda9

1Department of Occupational Health Practice and Management, Institute of Industrial Ecological Sciences, University of Occupational and Environmental Health, Japan, 2Occupational Health Training Center, University of Occupational and Environmental Health, Japan, 3Aratake Industrial Health Consultant Office, Japan, 4Mitsui Chemicals, Inc. , Japan, 5Panasonic Healthcare Co., Ltd., Matsuyama Area, Japan, 6MARUI GROUP Co., Ltd., Japan, 7HOYA Corporation, Japan, 8Department of Public Health, Kitasato University School of Medicine, Japan and 9Department of Public Health, School of Medicine, University of Occupational and Environmental Health, Japan

Field Study

J Occup Health 2014; 56: 215–224 Journal ofOccupational Health

Received Dec 3, 2012; Accepted Feb 24, 2014Published online in J-STAGE Apr 17, 2014Correspondence to: T. Nagata, Department of Occupational Health Practice and Management, Institute of Industrial Ecological Sciences, University of Occupational and Environmental Health, 1-1 Iseigaoka, Yahatanishi-ku, Kitakyushu, Fukuoka 807-8555, Japan (e-mail: [email protected])

216 J Occup Health, Vol. 56, 2014

and enhancement of productivity. When employers make a decision about OSH, they need two kinds of information. One type is a detailed breakdown of OSH costs. A chart of accounts and clearly defined account titles are needed. The other type is the ratio of OSH costs in terms of total corporate costs. To obtain such information, OSH costs have to be comparable to costs in business accounting. However, there are no previous studies that have conducted cost estimation according to standard business accounting practices to our knowledge.

Cost analysis is a part of economic evaluation. Economic evaluation studies can be conducted from the perspective of an employee or an employer or from a societal and national perspective6). The defi-nition of the costs varies according to the different viewpoints; therefore, in economic evaluations, we need to define which perspective is being taken7, 8). However, many studies have not described the analy-sis perspective, and we can only use their data to a limited extent6). Traditionally, a societal perspective is recommended, and in principle, all costs and conse-quences regardless of who pays or gains are includ-ed8). However, results from this broad approach may be difficult to apply to decision making in the work-place from an employer’s perspective9−11). Moreover, company-level economic evaluations of possible inter-ventions can provide guidance for sound business decision making12), but such studies use a diversity of methodological approaches13). Among the previous studies, costs have not been calculated using uniform account titles, and the calculation method has not been standardized.

The aim of this study was to develop standard-ized cost estimation tools for total OSH activities in Japanese companies. Often, different departments have implemented occupational safety activities and OH services in Japan, and we therefore also devel-oped cost estimation tools for total OH services.

Snapshot of the Japanese occupational safety and health system

The Industrial Safety and Health Law enacted in 1972 has contributed much to the progress of OSH activities in Japan14). The main OSH activities writ-ten in the law are health checkups to be conducted at least once a year, measurements of specified chemi-cals and other measurements in the working environ-ment to be conducted twice a year as a general rule and risk assessments and establishment of safety and health committees and workplace patrols. Workplaces regularly employing 50 workers or more are required to appoint an industrial physician. The industrial physician shall be a person who meets the require-ments provided for by the ordinance concerning

knowledge of occupational medicine by completing a 50-hour occupational health training course. In Japan, there were approximately 83,000 certified industrial physicians among approximately 275,000 medical doctors in 2012.

Subjects and Methods

We use activity-based costing methods that have previously been used to calculate healthcare treatment costs15, 16).

Definition of costsOSH costs have often been divided into costs for

prevention and costs of loss. Costs for prevention are the costs required to implement OSH activities, e.g., personnel costs, expenses and investments. Costs of loss are the equivalent of an employee’s health-related loss, e.g., absence from work due to accidents, inju-ries, and diseases and health-related productivity loss, sometimes referred to as “presenteeism”17). In the context of economic evaluation, the costs for preven-tion are often counted in the costs, and the costs of loss are often counted in the consequences. However, the total sum of costs for prevention and costs of loss can sometimes be considered as net costs. To provide informative data, we need the real costs of implement-ing OSH activities with clear definitions and detailed breakdowns of the costs. In this study, we defined the costs as just the costs for prevention and did not include the costs of loss.

Workflow of occupational safety and health activitiesWe used the workflow of health checkups as one

example of OSH activities. We divided the health checkup workflow into three phases: a preparatory phase, implementation phase and follow-up phase. Table 1 shows a breakdown of the heath checkup workflow.

The preparatory phase comprises the activities for preparing health checkups. A target company uses an outsourcing institute. OSH staff communicate with line managers to prepare health checkups. In the implementation phase, we have to calculate the oppor-tunity costs of examinees. In the follow-up phase, occupational health professionals analyze the results of health checkups.

Listing the cost items of occupational safety and health activities

Five professional occupational physicians discussed and listed all OSH activities and identified the work flow for each activity and the management of resourc-es (production, human and financial) required. Two safety specialists evaluated the list from a safety view-point. All OSH activities are listed along with the

217Tomohisa NAGATA, et al.: Cost Estimation Tools for Occupational Safety and Health Activities

composition elements of costs in Table 2.

Interviews about occupational safety and health activi-ties and costs

We visited three workplaces (Z, A and B) in three different companies and interviewed full-time profes-sional occupational physicians, department manag-ers and OSH staff to discuss practical methods of calculating OSH costs. All workplaces were involved in manufacturing and administered OSH activities according to a management system. In this study, we required detailed information about cost estima-tion. For the example of OSH education, we needed to know the contents, dates, locations and hours of education and the numbers of educated employees and teaching staff. We obtained such information from the companies that had occupational safety and health management systems in place. Consequently, we developed a beta version of the cost estimation tool for OSH activities using Microsoft Excel 2010.

Costs of occupational safety and health activitiesWe explained how to use the beta version of the

cost estimation tool to one professional occupational physician at each of workplaces Z, A and B. The physicians calculated the OSH costs through commu-nication with department managers and staff working in OSH, human resources and finance.

After calculating the total costs of OSH, we checked with each physician to ensure that all items of costs were mutually exclusive and collectively exhaustive and completed development of cost estima-tion tools for OSH.

Costs of occupational health servicesWe removed the occupational safety activities from

the cost estimation tools for OSH, and thus created cost estimation tools for OH services. We calculated the total OH costs in the workplaces of four different manufacturing companies (A, B, C and D). C and D had less than 1,000 employees.

We visited the four workplaces and confirmed the presence or absence of any possible leaked

Table 1. Workflow and costs of a health checkup operation

Activity Workflow

Overhead costs Direct costs

Capitalcost,

Expenses

OSH staff

LM EmployeeExpenses

Outsoucing cost

Investment

Personnel costs

Preparatory phase (A)1 (B)2 (C)3

Meeting with outsourcing institute

Identify examinees

Adjustment of schedule

Provide direction for health checkup

Implementation phase

Laboratory test

Medical examination by doctor

Laboratory re-test

Follow-up phase

Analyze the results of a health checkup

All phases in common (D)4

Capital cost (land)

Capital cost (buildings and equipment)

Light, fuel and water

Materials and supplies

Telephone

1 This section was calculated in A. Personnel costs for occupational safety and health staff. 2 This section was calculated in 4. Health checkup in B. Cost of each activity. 3 This section was calculated in 4. Health checkup in B. Cost of each activity. 4 This section was calculated in 7. Operation of the occupational safety and health department in B. Cost of each activity. OSH, occupational safety and health; LM, line managers.

218 J Occup Health, Vol. 56, 2014

Table 2. Cost items of occupational safety and health activitiesItems stipulated

in laws and regulations in

Japan

Safety items

Health items

A. Personnel costs for occupational safety and health staffOccupational physicianOccupational nurseHealth supervisorSafety supervisorWorking environment measurement expertHealth and safety promoterSafety promoterHealth promoterDietitianClerkManagerRank-and-file employeeBoard member (e.g., health and safety officer) Others

B. Cost of each activityB1. Emergency response and support

Emergency escape drillEmergency life guard drillEquipment (fire extinguisher) Equipment (AED) Equipment (emergency box) Others

B2. Equipment and fixtures(1) Local exhaust ventilation

Equipment (new) Equipment (existing) Regular inspectionEducation and training

(2) Smoking roomEquipment (new) Equipment (existing) Regular inspectionEducation and training

(3) Other equipment (e.g., heavy goods vehicle) Equipment (new) Equipment (existing) Regular inspectionEducation and training

(4) Personal protective equipmentPersonal protective equipmentMaintenanceEducation and training

B3. Working environment measurement, exposure measurement(1) Working environment measurement

Measurement (outsourcing) Measurement (insourcing) MeetingEquipment (measurement instruments) Calibration (measurement instruments)

(2) Exposure measurementMeasurement (outsourcing) Measurement (insourcing) MeetingEquipment (measurement instruments) Calibration (measurement instruments)

B4. Health checkup(1) Health checkup

General health checkupSpecific health checkupHealth checkup based on administrative guidanceReexaminationSecondary examinationOthers

(2) Investigation for health impairmentHealth checkup

B5. Health management(1) Face-to-face guidance with employees

Face-to face guidance by physicianFace-to face guidance by nurseFace-to face guidance by other professionals

(2) Face-to-face guidance with superior / human resourcesFace-to-face guidance with superiorFace-to-face guidance with human resources

(3) Overwork countermeasuresAssessment of physical and mental conditionFace-to-face guidance for workers with long working hours

(4) Health educationHealth education

B6. Mental health countermeasuresEducation (care by manager) Education (self-care) Education (others) Stress surveyEmployee assistant program

Items stipulated in laws and

regulations in Japan

safety field

health field

B7. Operation of occupational safety and health department(1) Operation of occupational safety department

Education and training for staffParticipation in conferenceExpendablesFixed assetsEquipment (repair, operation and maintenance) Company cars for emergencyOthers

(2) Operation of occupational health departmentEducation and training for staffParticipation in conferenceClinical laboratory equipment (new) Clinical laboratory equipment (maintenance) Medical equipmentExpendablesFixed assetsEquipment (repair, operation and maintenance) Company cars for emergencyOthers

(3) Institutions for health maintenance and promotionTraining roomGymnasium

(4) Information technologyHomepageHealth care systemOther system

B8. Health promotion and welfare(1) Health promotion(2) Welfare

Medical treatmentVaccinationOthers

B9. Management of occupational safety and health activities(1) Management based on OSHMS

DocumentationInternal auditExternal auditExternal certificationRisk assessmentEducation and trainingOthers

(2) Management not based on OSHMSPlan, goal settingCheckImprovementOthers

B10. Licensing, skill training courses, etc.(1) License1

Class 1 health supervisor, etc.(2) Practical training2

Practical training for operation of ship lifting appliance, etc.(3) Skill training course3

Operations chief of woodworking machines, etc.(4) Other licenses

Class 1 working environment measurement expert, etc.B11. Safety and health education

Education when hiringSpecial educationForeman's educationOthers

B12. MeetingSafety and health committeeTool box meetingOthers

B13. PatrolWorkplace patrol by physicianWorkplace patrol by health supervisorWorkplace patrol (others)

B14. Occupational accidents and injuries(1) Insurance premium for workers' compensation

Insurance premium for workers' compensation(2) Countermeasures after occupational accidents and injuries

Investigation of the causeRecurrence prevention measurementConsolation money and compensation

B15. Others(1) Outside agencies

Administrative (Labor Standards Inspection Office) External consultants

(2) Occupational safety and health projectProject (e.g., measurement of novel influenza)

(3) Awareness-promotion activitiesNational Occupational Safety weekNational Occupational Health weekOthers

(4) Others1 Articles 62-72 of the Labor Safety and Health Regulations. 2 Articles 73-77 of the Labor Safety and Health Regulations. 3 Articles 78-83 of the Labor Safety and Health Regulations. AED, auto-mated external defibrillator; OSHMS, occupational safety and health management system.

219Tomohisa NAGATA, et al.: Cost Estimation Tools for Occupational Safety and Health Activities

information about the OH cost estimation tools. Consequently, we developed beta version of the cost estimation tools for OH services using Microsoft Excel 2010. We explained how to use the tool, each physician calculated the OH costs, and we checked the results in the same way as mentioned above.

To obtain information regarding the personnel costs of non-occupational health staff, we interviewed four employees (two line managers and two rank-and-file employees) in workplace A, who did not work in the OSH department. We asked them how many hours in a month or a year they were required to conduct each OSH activity.

Validation of the toolsWe conducted cost estimation with the OSH cost

estimation tools in the other three workplaces (cate-gory of business / number of employees: services / 130, manufacturing / 115, manufacturing / 141) and with the OH cost estimation tools in one workplace (financing services / 624). We confirmed the pres-ence or absence of any possible leaked information about the tools with the occupational physician, health supervisor and safety supervisor in each workplace.

This research was approved by the Ethics Committee of Medicine and Medical Care, University of Occupational and Environmental Health, Japan.

Results

Cost items of occupational safety and health activitiesFive occupational physicians listed 13 items for

OSH staff and 15 items for activities (Table 2). Ten of the 15 activities are stipulated in Japanese laws and regulations. Safety specialists recommended adding only exposure measurement. Occupational physicians recommended adding management that was not based on the occupational safety and health management system (Table 3).

Classifications of costsWe implemented all OSH activities making use of

management resources such as production and human resources.

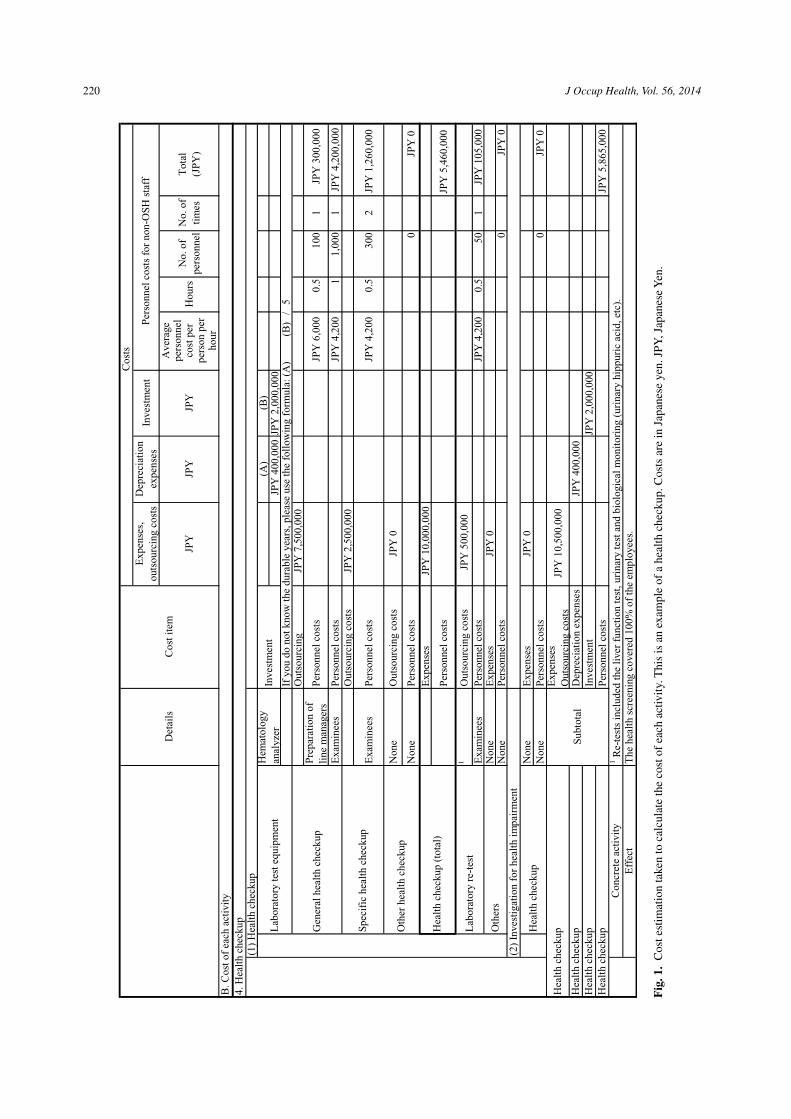

In the case of production resources, from the work-flow of a health checkup operation, we divided the costs into direct costs and overhead costs (Table 1). The information for direct costs can be obtained from the account ledgers of the OSH department, e.g., expenses, outsourcing costs and investment in C in Table 1. The costs were calculated for the health checkup listed in B4 in Table 2, and the cost estima-tion tool is shown in Fig. 1.

Capital (land, buildings and equipment), lighting, fuel and water, materials and supplies and telephone costs were allocated to the OSH department from all departments in the workplace in D in Table 1. These

Table 3. Information obtained through interviews

Comment concerning an item added to the activities from the occupational physician at workplace A“We evaluated the risk management of occupational health services. This activity was different from an internal audit of OSHMS. We patrolled all departments and investigated to what degree the activities required by laws and regulations and scheduled education were conducted. We fed back the results to all departments.”

Comments concerning difficulties with cost estimation of occupational safety and health activitiesDepreciation expenses for investments in equipment

“To calculate all expenses for local exhaust ventilation, we have to check a 15-year buying history in the account ledgers. This requires a great deal of time and effort, so we cannot calculate them all.”

Cost of fail-safe devices“Fail-safe devices are already built into the equipment, so we cannot divide costs of fail-safe devices from costs of the equipment.”

Personnel costs involved with managers coaching their subordinates on occupational safety and health“In a daily conversation between superiors and subordinates, superiors give guidance about safety behavior or health man-agement of subordinates. But it is difficult to determine the conversation time, so it is difficult to calculate the labor costs for them.”

Time per year for conducting occupational health tasks (hours)

OSHMS Risk assessment Health meeting in each department

Line manager 7 0 24

Line manager 56 7 30

Rank-and-file employee 5 0 4

Rank-and-file employee 10 1 20

OSHMS, occupational safety and health management system.

220 J Occup Health, Vol. 56, 2014

Fig

. 1.

Cos

t est

imat

ion

take

n to

cal

cula

te th

e co

st o

f ea

ch a

ctiv

ity. T

his

is a

n ex

ampl

e of

a h

ealth

che

ckup

. Cos

ts a

re in

Jap

anes

e ye

n. J

PY, J

apan

ese

Yen

.

Exp

ense

s,ou

tsou

rcin

g co

sts

Dep

reci

atio

nex

pens

esIn

vest

me n

t

JPY

JPY

JPY

Ave

rage

pers

onne

lco

st p

e rpe

rson

pe r

hour

Hou

rsN

o. o

fpe

rson

nel

No.

of

tim

esT

otal

(JPY

)

(A)

(B)

JPY

400

,000

JPY

2,0

00,0

00

Out

sour

cing

JPY

7,5

00,0

00Pr

epar

atio

n of

line

man

ager

sPe

rson

nel c

osts

JPY

6,0

000.

510

01

JPY

300

,000

Exa

min

ees

Pers

onne

l cos

tsJP

Y 4

,200

11,

000

1JP

Y 4

,200

,000

Out

sour

cing

cos

tsJP

Y 2

,500

,000

Exa

min

ees

Pers

onne

l cos

tsJP

Y 4

,200

0.5

300

2JP

Y 1

,260

,000

Non

eO

utso

urci

ng c

osts

JPY

0

Non

ePe

rson

nel c

osts

0JP

Y 0

Exp

ense

sJP

Y 1

0,00

0,00

0

Pers

onne

l cos

tsJP

Y 5

,460

,000

1O

utso

urci

ng c

osts

JPY

500

,000

Exa

min

ees

Pers

onne

l cos

tsJP

Y 4

,200

0.5

501

JPY

105

,000

Non

eE

xpen

ses

JPY

0N

one

Pers

onne

l cos

t s0

JPY

0

Non

eE

xpen

ses

JPY

0N

one

Pers

onne

l cos

ts0

JPY

0E

xpen

ses

Out

sour

cing

cos

tsJP

Y 1

0,50

0,00

0

Dep

reci

atio

n ex

pens

esJP

Y 4

00,0

00In

vest

men

tJP

Y 2

,000

,000

Pers

onne

l cos

tsJP

Y 5

,865

,000

B. C

ost o

f ea

ch a

ctiv

ity

Det

ails

Cos

t ite

m

Cos

t s

Pers

onne

l cos

ts f

or n

on-O

SH s

taff

4. H

ealth

che

ckup

(1)

Hea

lth c

heck

up

Lab

orat

ory

test

equ

ipm

ent

Hem

atol

ogy

anal

yzer

Inve

stm

ent

If y

ou d

o no

t kno

w th

e du

rabl

e ye

ars,

ple

ase

use

the

follo

win

g fo

rmul

a: (

A)

=

(B)

/ 5

Gen

eral

hea

lth c

heck

up

Spec

ific

hea

lth c

heck

up

The

hea

lth s

cree

ning

cov

ered

100

% o

f th

e em

ploy

ees.

Oth

er h

ealth

che

ckup

Hea

lth c

heck

up (

tota

l)

Lab

orat

ory

re-t

est

Oth

ers

(2)

Inve

stig

atio

n fo

r he

alth

impa

irm

e nt

Hea

lth c

heck

up

Hea

lth c

heck

up

Subt

otal

Hea

lth c

heck

upH

ealth

che

ckup

Hea

lth c

heck

upC

oncr

ete

activ

ity1 R

e-te

sts

incl

uded

the

liver

fun

ctio

n te

st, u

rina

ry te

st a

nd b

iolo

gica

l mon

itori

ng (

urin

ary

hipp

uric

aci

d, e

tc).

Eff

ect

221Tomohisa NAGATA, et al.: Cost Estimation Tools for Occupational Safety and Health Activities

costs were not only used for health checkups but were also used for all OSH activities and were called over-head costs. The costs of operation of an occupational safety and health department listed in B7 in Table 2 were calculated.

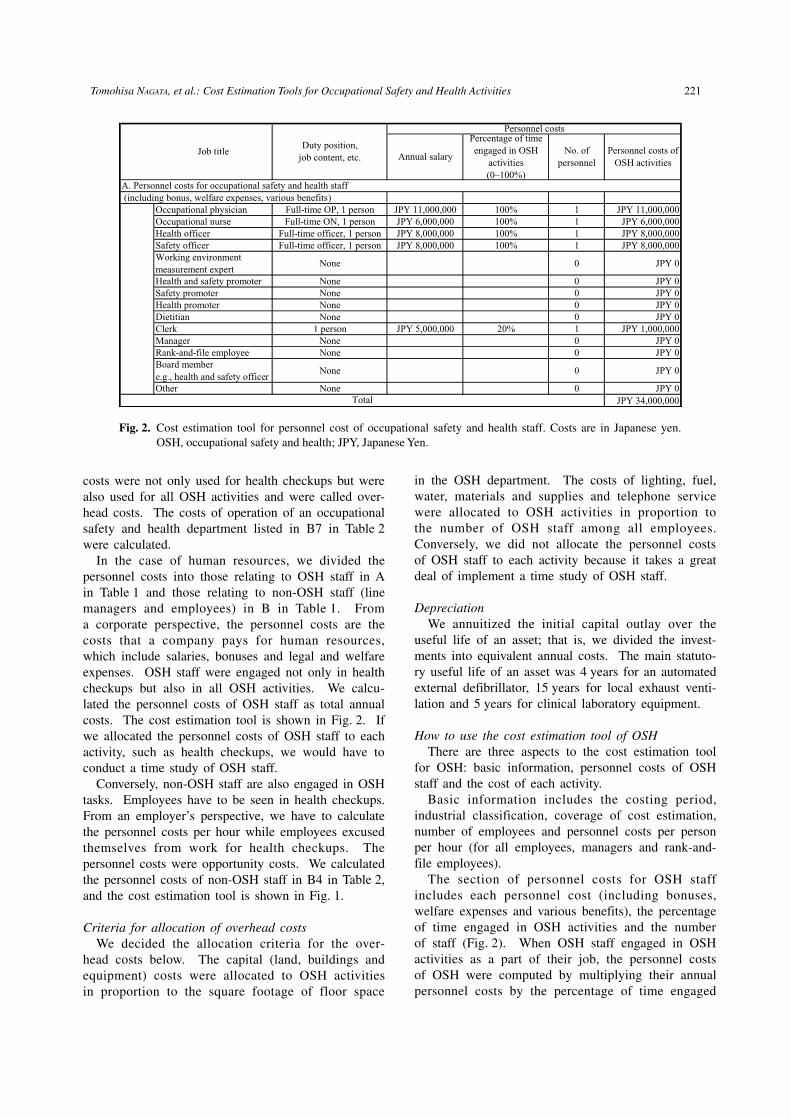

In the case of human resources, we divided the personnel costs into those relating to OSH staff in A in Table 1 and those relating to non-OSH staff (line managers and employees) in B in Table 1. From a corporate perspective, the personnel costs are the costs that a company pays for human resources, which include salaries, bonuses and legal and welfare expenses. OSH staff were engaged not only in health checkups but also in all OSH activities. We calcu-lated the personnel costs of OSH staff as total annual costs. The cost estimation tool is shown in Fig. 2. If we allocated the personnel costs of OSH staff to each activity, such as health checkups, we would have to conduct a time study of OSH staff.

Conversely, non-OSH staff are also engaged in OSH tasks. Employees have to be seen in health checkups. From an employer’s perspective, we have to calculate the personnel costs per hour while employees excused themselves from work for health checkups. The personnel costs were opportunity costs. We calculated the personnel costs of non-OSH staff in B4 in Table 2, and the cost estimation tool is shown in Fig. 1.

Criteria for allocation of overhead costs We decided the allocation criteria for the over-

head costs below. The capital (land, buildings and equipment) costs were allocated to OSH activities in proportion to the square footage of floor space

in the OSH department. The costs of lighting, fuel, water, materials and supplies and telephone service were allocated to OSH activities in proportion to the number of OSH staff among all employees. Conversely, we did not allocate the personnel costs of OSH staff to each activity because it takes a great deal of implement a time study of OSH staff.

DepreciationWe annuitized the initial capital outlay over the

useful life of an asset; that is, we divided the invest-ments into equivalent annual costs. The main statuto-ry useful life of an asset was 4 years for an automated external defibrillator, 15 years for local exhaust venti-lation and 5 years for clinical laboratory equipment.

How to use the cost estimation tool of OSHThere are three aspects to the cost estimation tool

for OSH: basic information, personnel costs of OSH staff and the cost of each activity.

Basic information includes the costing period, industrial classification, coverage of cost estimation, number of employees and personnel costs per person per hour (for all employees, managers and rank-and-file employees).

The section of personnel costs for OSH staff includes each personnel cost (including bonuses, welfare expenses and various benefits), the percentage of time engaged in OSH activities and the number of staff (Fig. 2). When OSH staff engaged in OSH activities as a part of their job, the personnel costs of OSH were computed by multiplying their annual personnel costs by the percentage of time engaged

(including bonus, welfare expenses, various benefits)Occupational physician Full-time OP, 1 person JPY 11,000,000 100% 1 JPY 11,000,000Occupational nurse Full-time ON, 1 person JPY 6,000,000 100% 1 JPY 6,000,000Health officer Full-time officer, 1 person JPY 8,000,000 100% 1 JPY 8,000,000Safety officer Full-time officer, 1 person JPY 8,000,000 100% 1 JPY 8,000,000Working environmentmeasurement expert

None 0 JPY 0

Health and safety promoter None 0 JPY 0Safety promoter None 0 JPY 0Health promoter None 0 JPY 0Dietitian None 0 JPY 0Clerk 1 person JPY 5,000,000 20% 1 JPY 1,000,000Manager None 0 JPY 0Rank-and-file employee None 0 JPY 0Board membere.g., health and safety officer

None 0 JPY 0

Other None 0 JPY 0JPY 34,000,000

A. Personnel costs for occupational safety and health staff

Total

Job titleDuty position,

job content, etc.

Personnel costs

Annual salary

Percentage of timeengaged in OSH

activities(0–100%)

No. ofpersonnel

Personnel costs ofOSH activities

Fig. 2. Cost estimation tool for personnel cost of occupational safety and health staff. Costs are in Japanese yen. OSH, occupational safety and health; JPY, Japanese Yen.

222 J Occup Health, Vol. 56, 2014

in OSH activities. For a clerk whose annual person-nel costs were 5 million Japanese Yen (JPY) and whose rate of engagement in OSH activities was 20%, the personnel costs were 1 million JPY (multiply 5 million JPY by 0.20), as shown in Fig. 2.

The section for the cost of each activity contains expenses, outsourcing costs, investments, depreciation and personnel costs for non-OSH staff (Fig. 1). To calculate the personnel costs for non-OSH staff, we required information on the average personnel costs per person per hour, activity time (hours), number of people involved and number of times each activity was performed in a year. In the case of the general health checkup, given that the average personnel costs per employee per hour was 4,200 JPY, the mean examination time was 1 hour, there were 1,000 exam-inees, and the activity was performed once a year, the personnel costs of the activity were 4.2 million JPY (4,200 JPY × 1 hour × 1,000 people × 1 time), as shown in Fig. 1.

The activity time (hour) needs to be identified to calculate the personnel costs. In the case of the health checkup above, the mean examination time was 1 hour per person, and the time was approximately the same among examinees. However, the time required for some activities differed for different employ-ees. We conducted an interview in workplace A and determined times required for two managers and two rank-and-file employees to conduct OSH activities (OSH management work, risk assessment and a health meeting) (Table 3). The times required were differ-ent from person to person. In such cases, we recom-mend holding interviews with some employees about the time required for each activity and calculating the average time.

Cost estimation of occupational safety and health activities

We calculated all OSH costs using the tool in three workplaces, Z, A and B. Through this process, we observed difficulties in cost estimation of three items: the depreciation for investments in equipment incurred before the current costing year, the costs of fail-safe devices already installed in manufacturing facilities and the personnel costs of line managers for coaching of subordinates in terms of OSH (Table 3). Except for these three items, no issues arose in calculating the costs of OSH.

Cost estimation of occupational health servicesWe constructed the cost estimation tool for OH

services by removing the safety-only items from the cost estimation tool for OSH. Items classified by safety and health are listed in Table 2. When calcu-lating the costs in workplaces A, B, C and D, we

only encountered difficulties in assessing the costs of the three items mentioned above: depreciation, costs of fail-safe devices and the personnel costs of line managers when coaching.

Validation of the toolsWe interviewed the OSH staffs about the presence

or absence of any possible leaked information about the cost estimation tools, and all of them answered that there was no leaked information in the tools.

The cost estimation tools for OSH activities and OH services can be downloaded freely from http://ohtc.med.uoeh-u.ac.jp/healthaccounting/tool/index.html.

Discussion

In this study, we developed cost estimation tools for OSH activities and OH services from a corporate perspective. With these tools, it is possible to clarify the entire OSH and OH costs in a standardized way.

The cost estimation tools are compatible with busi-ness accounting standards. We calculated the OSH costs from a corporate perspective. We listed account titles in detail and defined overhead cost allocation rules. In this study, we calculated OSH costs by referring to the accounting information in cooperation with financial department staff. This made it possible to calculate real OSH costs.

OSH costs, from a corporate perspective, should be contained in the personnel costs of non-OSH staff. This means that, from the data for OSH costs, employers can evaluate not only OSH activities conducted by OSH staff but also company-wide OSH activities conducted by all employees. Using this tool, we can manage OSH systematically in a manner consistent with corporate management. In addition to this, the tool needs to meet the following two requirements. First, OSH practitioners must conduct the cost estimation from the employers’ perspective so that employers (decision makers) can understand and accept the results within the scope of their own management field. Second, employers need to be able to compare results with other management indices and use results as management indicators.

We can analyze the OSH cost estimation data in a number of ways. We can understand the break-down of expenses, outsourcing costs and investments allocated to the respective OSH activities. We can compare the three costs and evaluate the balance for each activity. By reference to budget documents and financial statements, we can calculate the rate of each cost of OSH among total costs in the workplace. We can also calculate the breakdown of personnel costs for OSH staff and non-OSH staff. Moreover, we can calculate the proportion of total OSH costs in net personnel costs of the company. OSH costs are

223Tomohisa NAGATA, et al.: Cost Estimation Tools for Occupational Safety and Health Activities

thought of as human resource investments in terms of preventing accidents and promoting employee health, and we thus believe that OSH costs have value as an indicator of human resource investment. If we can measure productivity, it will be a challenge in the OSH field to reveal the relationship between OSH costs per employee and work productivity.

In this study, we actually calculated OSH costs for eight companies and OH costs for nine companies. Two occupational physicians interviewed in this study were responsible for the administration of the occupa-tional health department budgets of their businesses. They held a similar view: “This is the first time that we can capture the entire picture of the occupational health costs including out-of-sight costs. The out-of-sight costs are the personnel costs when employees (non-OSH staff) conduct OSH activities and receive OSH services. With this tool, we can grasp the work-ers’ behavior in the OSH activities.” An account manager interviewed said: “To create financial state-ments and manage the problem in terms of tax report-ing, we enter details in a book daily. We assess profit-and-loss accounts and cash flow. However, this is the first time that we have seen data on OSH, as usually the costs of OSH are buried in a large volume of accounting data.”

Use scenarios for the cost estimation toolsWe present three use scenarios for the tools.

One is cost management of outsourcing. We can compare insourcing costs of OSH with outsourcing costs. Employers can make decisions according to the comparison and appropriate cost management. Occupational safety activities are often conducted by in-house staff. OH services are sometimes outsourced, similar in ways to the implementation of employee-assistant programs. Therefore, comparisons of outsourcing and insourcing costs are needed. Cost analysis requires a job analysis of OSH activities, and the costs need to contain the opportunity costs of non-OSH staff. The cost estimation tools can meet these requirements in a standardized manner. In a competitive business environment, cost management is requisite, and the demand will be higher in the future.

The second scenario is accountability to multiple stakeholders such as customers, employees, stock holders, and the local community. OSH is widely recognized as being part of corporate social respon-sibility (CSR) and is written in the labor practices of ISO 26000: 2010 under health and safety at work. In addition, ISO 26000 indicates that the financial and social costs to society of work-related illness, injuries and death are high18). Many Japanese companies list-ed on the Tokyo Stock Exchange First Section publish CSR reports each year, and they describe OSH

activities in their reports19). Some companies have described OSH costs in the report contents20). Using CSR reports, employers can explain their OSH activi-ties to multiple stakeholders. Multiple stakeholders, especially stock holders, can use the information to make decisions about equity investment.

The third scenario is the provision of a standard-ized format in economic evaluation. Cost estimation is imperative for economic evaluation studies. The OSH cost estimation tool provides the real OSH costs. Above all, this tool provides a detailed breakdown of OSH costs, allowing comparison between the results of economic evaluations.

LimitationsThere are several limitations to these findings.

First, we may not be able to completely calculate the depreciation for investments in equipment incurred before the current costing year with our cost estima-tion tools based on activity-based costing. The OSH costs will be underestimated, but the underestima-tion will have a relatively small effect because these investments are few except in manufacturing. Second, we developed the OSH cost estimation tools for large-scale enterprises. Further OSH cost estimation is needed for small- or medium-scale enterprises to confirm the availability of this tool. In this study we used the tool in three medium-scale enterprises and confirmed the availability. Third, we developed the OSH cost estimation tools in Japan, and the activ-ity items in them are compliant with actual activities, laws and regulations in Japan. If these OSH cost estimation tools are to be used in other countries, it would be better to add items for activities unique to those countries. This would hopefully enable compar-ison of OSH costs in various countries.

In conclusion, we developed cost estimation tools for OSH activities and OH services from a corporate perspective in Japanese companies. These tools can be used to standardize reporting of information on the costs associated with OSH and thus provide employ-ers and researchers alike with relevant, accurate infor-mation so that they can make informed decisions.

Acknowledgments: The authors express their sincere appreciation to the companies that participated in this study. The authors would also like to thank Mr. Haruo Hashimoto (industrial hygienist), Mr. Takuro Shoji (safety specialist) and Mr. Osamu Sonoda (certi-fied public accountant). This research was funded by Grants-in-Aid from the Ministry of Health, Labour and Welfare of Japan (H23-Roudou-Wakate-006, Tomohisa Nagata as a representative researcher). The authors declare no conflicting interests.

224 J Occup Health, Vol. 56, 2014

References

1) Verbeek J, Pulliainen M, Kankaanpaa E. A system-atic review of occupational safety and health busi-ness cases. Scand J Work Environ Health 2009; 35: 403−12.

2) Uegaki K, de Bruijne MC, van der Beek AJ, van Mechelen W, van Tulder MW. Economic evaluations of occupational health interventions from a compa-ny’s perspective: a systematic review of methods to estimate the cost of health-related productivity loss. J Occup Rehabil 2011; 21: 90−9.

3) Tompa E, Dolinschi R, de Oliveira C. Practice and potential of economic evaluation of workplace-based interventions for occupational health and safety. J Occup Rehabil 2006; 16: 367−92.

4) Mayne TJ, Howard K, Brandt-Rauf PW. Measuring and evaluating the effects of disease on workplace productivity. J Occup Environ Med 2004; 46: S1−2.

5) Anstadt GW, Lester DL, Powell BH, Mitchell JW, Tunaitis EM. The business planning process applied to an in-house corporate occupational medicine unit. Journal of Occupational Medicine: Official Publication of the Industrial Medical Association 1991; 33: 354−7.

6) Uegaki K, de Bruijne MC, Lambeek L, et al. Economic evaluations of occupational health inter-ventions from a corporate perspective: a systematic review of methodological quality. Scand J Work Environ Health 2010; 36: 273−88.

7) Evers S, Goossens M, de Vet H, van Tulder M, Ament A. Criteria list for assessment of method-ological quality of economic evaluations: consensus on health economic criteria. Int J Technol Assess Health Care 2005; 21: 240−5.

8) Drummond MF, Sculpher MJ, Torrance GW, O’Brien BJ, Stoddart GL. Methods for the economic evaluation of health care programmes. 3rd ed. Oxford (UK): Oxford University Press; 2005.

9) Berger ML, Murray JF, Xu J, Pauly M. Alternative valuations of work loss and productivity. J Occup Environ Med 2001; 43: 18−24.

10) Brouwer WB, van Exel NJ, Baltussen RM, Rutten FF. A dollar is a dollar is a dollar: or is it? Value Health 2006; 9: 341−7.

11) Young AE, Wasiak R, Roessler RT, McPherson KM, Anema JR, van Poppel MN. Return-to-work outcomes following work disability: stakeholder motivations, interests and concerns. J Occup Rehabil 2005; 15: 543−56.

12) Biddle E, Ray T, Owusu-Edusei K, Jr., Camm T. Synthesis and recommendations of the economic evaluation of OHS interventions at the company level conference. J Safety Res 2005; 36: 261−7.

13) Tompa E, Verbeek J, van Tulder M, de Boer A. Developing guidelines for good practice in the economic evaluation of occupational safety and health interventions. Scand J Work Environ Health 2010; 36: 313−8.

14) Sakurai H. Occupational safety and health in Japan: current situations and the future. Ind Health 2012; 50: 253−60.

15) Ridderstolpe L, Johansson A, Skau T, Rutberg H, Ahlfeldt H. Clinical process analysis and activity-based costing at a heart center. J Med Syst 2002; 26: 309−22.

16) Godderis L, Fabiani P, Van Peteghem J, Moens G, Masschelein R, Veulemans H. Detailed calculation of occupational health service costs through activity-based costing: the cost of risk-assessment projects. Occup Med (Lond) 2005; 55: 131−2.

17) Brady W, Bass J, Moser R, Jr., Anstadt GW, Loeppke RR, Leopold R. Defining total corporate health and safety costs: significance and impact. Review and recommendations. J Occup Environ Med 1997; 39: 224−31.

18) The International Organization for Standardization (ISO). ISO 26000:2010 Guidance on social respon-sibility. ISO; 2010.

19) Kawashita F, Taniyama Y, Hwi SY, Fujisaki T, Kameda T, Mori K. Occupational safety and health aspects of corporate social responsibility (CSR) in Japanese companies listed on the Tokyo Stock Exchange (TSE) first section. J Occup Health 2005; 47: 533−9.

20) Teijin Limited, Teijin Group CSR Report. p. 49. [Online]. 2012 [cited 2014 Apr 16] ; Available from: URL: http://www.teijin.com/csr/report/pdf/csr_12_en_all.pdf