deutsche bahn fixed income roadshow asia 2012 · september 2012. deutsche bahn ag / db mobility...

TRANSCRIPT

“Our future: Sustainably successful!“

Deutsche Bahn Fixed Income Roadshow Asia 2012

September 2012

Deutsche Bahn

AG / DB Mobility Logistics AG

CFO

Robert Strehl

DB2020 -

Our future: Sustainably successful!

3

Intro

Our future

Deutsche Bahn AG Road Show Asia 2012

4

Solid financial position, sustainable profit growth

Key investment highlights

DB Group combines stability with a good position for future growth

Key investment highlights

Strong track record in all key financial figures

Leading market position in all relevant markets

Core competence in managing transport networks

Balanced business mix of growth and value

Megatrends support our future growth potential

Unique geographic position in the heart of Europe

Profitable growth path continued since 2009

Very good ratings from Moody’s (Aa1), S&P (AA) and Fitch (AA)

Deutsche Bahn AG Road Show Asia 2012

5

Integrated Group structure with two holding companies (DB AG and DB ML AG) and 9 business units

DB AG is 100% owned by the Federal Republic of Germany

Privatization threshold: constitutionally mandated Federal majority shareholding in DB AG (“ownership clause”)

Infrastructure business units are directly managed by DB AG

DB ML AG operates as a holding company for DB Group’s mobility and logistics activities

Financing subsidiary DB Finance is 100% owned by DB AG

DB Bahn Long-

Distance

Deutsche Bahn AG

DB Netze Track

DB Netze Stations

DB Netze Energy

DB Bahn Regional DB Arriva

DB Schenker

Rail

DB Schenker Logistics

DB Services

DB Mobility Logistics AG

DB ML Group

DB Group

Structure

Organizational structure

Deutsche Bahn Finance B.V.

(DB Finance)

100%

100%

100%

Federal Republic of Germany

Deutsche Bahn Group Comments

Deutsche Bahn AG Road Show Asia 2012

6

Where do we come from

Turnaround of German railway business was key to success

171 174191

171184 191

388

327

299

261

239221

206194

184 177 173161160155153159159

149145144139140

127135

151154

164

149 154 154 156 157

720

893

1,106

1,247

1,1671,133

1,042

603533

468413

656

328

1,1841,220

820863 860

975

'93 '94 '95 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11

Ptkm (bn) Employees - rail (thd, year average) Productivity

2.3

1.91.7

2.52.4

0.5

1.0

1.4

2.1

-0.4-0.7-0.8

-1.5-1.7

-2.1-2.2

-2.7-3.0

6.1%

5.4%

5.7%7.4%

7.6%

-20.3%

-17.5%

-14.6%-13.3%

-11.1%

-9.8%

-5.0% -4.6%

-2.2%

7.1%

5.4%4.0%

1.6%

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

EBIT adjusted Adj. EBIT margin

1993-2011:

+272%CAGR:

+7.6%1994-2011:

€

+5.3 bnPer year:

€

+294 mn

Figures until 2004 FY according to German GAAP

Productivity –

rail (thousand ptkm/employee)

EBIT adjusted and adjusted EBIT margin (€

bn or %)

Deutsche Bahn AG Road Show Asia 2012

7

16.616.9

15.015.916.5

19.619.7

2005 2006 2007 2008 2009 2010 2011

15.114.3

13.112.2

11.0

9.2

7.7

2005 2006 2007 2008 2009 2010 2011

Where do we come from

Equity ratio significantly improved, financial debt noticeably decreased

Equity (€

bn) Net financial debt (€

bn)Equity ratio (%)

29.227.527.6

25.2

22.6

19.0

16.3

2005 2006 2007 2008 2009 2010 2011

-15.7%/-€

3.1 bn +96.1%/+€

7.4 bn +12.9 %-points

Deutsche Bahn AG Road Show Asia 2012

8

Where do we come from

Key value management figures significantly improved

ROCE

(%)

7.3

6.05.9

8.98.7

7.5

5.0

'05 '06 '07 '08 '09 '10 '11

20.5

18.119.4

22.521.1

18.6

14.7

'05 '06 '07 '08 '09 '10 '11

256

213

151

131115 118

110

'05 '06 '07 '08 '09 '10 '11

3.2

3.63.4

3.13.2

3.9

4.8

'05 '06 '07 '08 '09 '10 '11

Redemption coverage (%) Gearing

(%) Net debt/EBITDA (multiple)

Target: 10%Target: 30%

Target: 100%

Target: 2.5

Deutsche Bahn AG Road Show Asia 2012

9

InfrastructureNo.1

Rail infrastructure

No.1Operation of railway stations

Passenger Transport

No.1Local rail transport

No.2Long-distance rail transport

No.2Bus transport

Transport & Logistics

No.1Rail freight transport

No.1Land transport No.

Ocean freight

6Contract logistics

No.2Air freight

3No.

Where we are today

We hold leading market positions in Europe and the world

Deutsche Bahn AG Road Show Asia 2012

10

Where we are today

We are operating today in more than 130 countries with more than

2,000 sites

DB world wide

(examples)

Own sites Partners

Transfesa (DB SR)

DB Schenker Spain-Tir (DB SL)

DB Arriva Spain

DB Schenker

Brasil (DB SL)

DB International

DB Schenker China (DB SL)

DB International

Railion Russija Services (DB SR)

DB Schenker Russia (DB SL)

DB International

DB Schenker Australia (DB SL)

ECR (DB SR)

DB Schenker-Joyau

(DB SL)

DB Schenker Rail UK

DB Schenker UK

DB Arriva UK

DB Vertrieb UK

Deutsche Bahn AG Road Show Asia 2012

11

Entrepreneurial approach to business

Integrated

GroupCross-modal solutions

Internationally positioned

Where we are today

Our success is based on four factors

Deutsche Bahn AG Road Show Asia 2012

12

Challenges and opportunities of the future

The megatrends of the future

Deutsche Bahn AG Road Show Asia 2012

13Source: In-house figures as well as Progtrans, BMVBS figures

Ocean freight

Air freight

Land transport

Rail freight transport

Rail passenger transport

Public road/passenger transport

Contract logistics >+100

+80

+60

+35

+35

+10

+5

Market growth 2010 –

2020 % based on volumes (rounded figures)

Challenges and opportunities of the future

Transport markets will expand further in the future

Deutsche Bahn AG Road Show Asia 2012

14

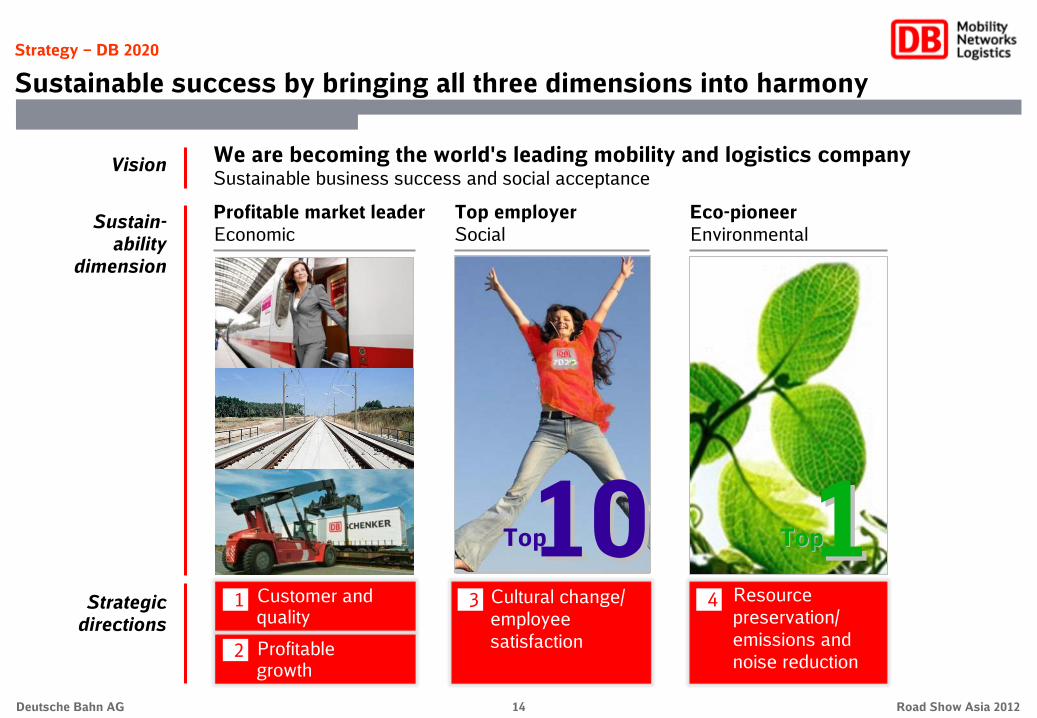

Customer and quality

Profitable growth

Strategic directions

Vision We are becoming the world's leading mobility and logistics company

Sustainable business success and social acceptance

1

2

3 4Cultural change/ employee satisfaction

Resource preservation/ emissions and noise reduction

Sustain-

ability

dimension

Profitable market leaderEconomic

Top employerSocial

Eco-pioneerEnvironmental

TopTop TopTopTopTop 11101011

Strategy ‒

DB 2020

Sustainable success by bringing all three dimensions into harmony

Deutsche Bahn AG Road Show Asia 2012

15

Strategy ‒

DB 2020

For people, for markets, for tomorrow

Deutsche Bahn AG Road Show Asia 2012

September 2012

Deutsche Bahn AG / DB Mobility Logistics AG

Group Treasurer, Head of M&A

Wolfgang Reuter

2011 Financial Year, H1 2012, Capital Market Activities and Outlook

17Deutsche Bahn AG Road Show Asia 2012

1.9

2.3

2010

2011 5.1

4.72010

2011 16.6

16.92010

2011 7.3

6.02010

2011

Favorable effects from performance development

Noticeable increase in revenues and adjusted EBIT

First-time full-year inclusion of Arriva

Further decline in net financial debt

Value management figures improved

Highlights

Revenues (€

bn) EBIT adjusted

(€

bn) Net financial debt (as of Dec 31, €

bn)ROCE

(%)

2010

2011

EBITDA adjusted

(€

bn)

2011 financial year –

At a glance

Update on financial results 2011

34.4

37.9

+10.1% +23.7% +10.5% -2.0%

18

Germany again with the strongest economic development in EuropeEconomic momentum slows down noticeablyUncertainties due to sovereign debt crisis are still existingHigh burdens from increasing energy and personnel expenses

H1 2012 –

At a glance

Highlights H1 2012

Positive development in rail passenger transport in Germany In Europe development varying from country to country

Performance decrease in rail freight transportMixed picture in the area of transport and logistics: strong increase in ocean freight, slight increase in European land transport, decrease in

air freight

Train-path demand slightly lowerDemand from non-Group railways increased again, share of total at 21.7%

Business

environment

Passenger

Transport

Transport and

Logistics

Infrastructure

Deutsche Bahn AG Road Show Asia 2012

19

Key figures (€

mn)

EBIT adjusted

Net profit

Net financial debt as of Jun 30, 2012/ Dec 31, 2011

1,321

794

16,954

19,492

19,220

H1 2012 –

At a glance

Favorable development in H1 2012

H1 2012

Revenues

Revenues comparable

+16.6

+22.5

+2.2

+3.3

+1.8

€ %Change

+188

+146

+362

+616

+344

+13.0+349Gross capital expenditures 3,038

+34.2+359Net capital expenditures 1,408

ROCE (%) 8.1 ––

H1 2011

1,133

648

16,592

18,876

18,876

2,689

1,049

7.2

Deutsche Bahn AG Road Show Asia 2012

20

Revenues (€

mn)

H1 2012 –

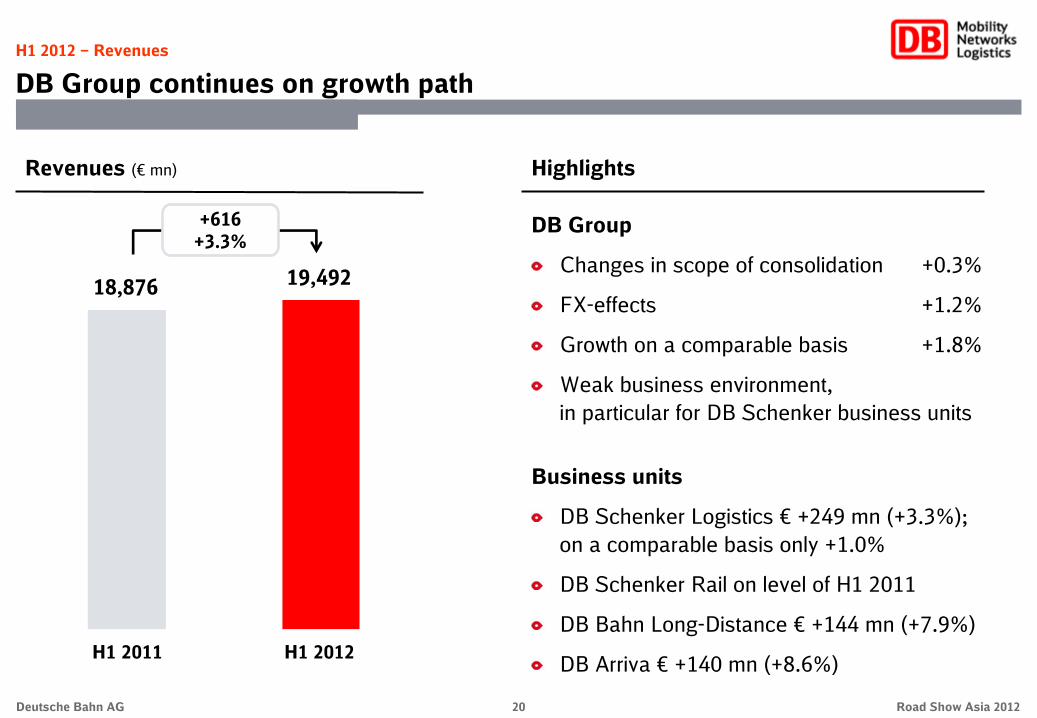

Revenues

DB Group continues on growth path

H1 2011 H1 2012

18,876 19,492

+616

+3.3%

Highlights

DB Group

Changes in scope of consolidation

+0.3%

FX-effects

+1.2%

Growth on a comparable basis

+1.8%

Weak business environment, in particular for DB Schenker business units

Business units

DB Schenker Logistics €

+249 mn (+3.3%); on a comparable basis only +1.0%

DB Schenker Rail on level of H1 2011

DB Bahn Long-Distance €

+144 mn (+7.9%)

DB Arriva €

+140 mn (+8.6%)H1 2011 H1 2012

Deutsche Bahn AG Road Show Asia 2012

21

H1 2012 –

Revenues

No significant changes in revenue structure

4%7%

1%

58%30%

41%

1% 7%

51%

52% 48%

Revenues by division H1 2012

Germany

Europe (excl. Germany)

North America

Asia/Pacific

Other

Passenger Transport

Transport and Logistics

Infrastructure

(H1 2011)

(52%)

(41%)

(6%)(1%)

Other

(59%)(29%)

(1%)

(5%)(6%)

Revenues by regions H1 2012

(H1 2011)

Revenues by activities H1 2012

Rail Non-rail

(H1 2011)

(48%)(52%)

Deutsche Bahn AG Road Show Asia 2012

22

H1 2012 –

Profits

EBIT development significantly positive

EBIT and EBIT adjusted (€

mn)

EBIT Special items EBIT adjusted

H1 2011 H1 2012

+23.8%

+16.6% +188

EBIT Special itemsEBIT adjusted Reclassifications

1,076 +57 1,133

1,321 -40 +51 1,332

Deutsche Bahn AG Road Show Asia 2012

23

9.8

10.1

1.0

2.6

2.91)

17.1

25.0

3.8

-

6.8

5.3

Margin (%)

H1 2012–

Profits

Mixed EBIT development on business units level

EBIT adjusted (€

mn)

DB Bahn Long-Distance

DB Bahn Regional

DB Schenker Rail

DB Schenker Logistics

DB Services

DB Netze Track

DB Netze Stations

DB Netze Energy

Other/Consolidation

DB Group

DB Arriva

46

477

58

170

80

262

124

24

-179

1,133

71

H1 2011

192

447

24

201

48

398

140

55

-278

1,321

94

H12012

+146 -

-30 -6.3

-34 -58.6

+31 +18.2

-32 -40.0

+136 +51.9

+16 +12.9

+31 +129

-99 +55.3

+188 +16.6

+23 +32.4

€ %Change

2.5

10.9

2.3

2.3

5.11)

11.5

23.1

1.7

-

6.0

4.4

Margin (%)

1)

Based on segment revenuesDeutsche Bahn AG Road Show Asia 2012

24

Dec 31, 2011 Jun 30, 2012

Deutsche Bahn AG Road Show Asia 2012

Balance sheet structure (as of Jun 30, 2012/Dec 31, 2011)

H1 2012 –

Balance sheet

Strong increase of capital expenditures

Equity and liabilitiesAssets

Non-current assets82.5% (85.1%)

Current assets 17.5% (14.9%)

Equity28.7% (29.2%)

Pension prov.3.8% (3.8%)

€ 53.5 bn(€

51.8 bn)Total€

53.5 bn(€

51.8 bn)Total

Financial debt36.7% (35.4%)

Other provisions10.2% (10.8%)

Other20.6% (20.8%)

Capital expenditures (€

mn)

H1 2011 H1 2012

2,689

3,038

Gross:

+349

+13.0%

1,049

1,408

Net: +359

+34.2%

Financial debt (€

mn; as of Dec 31, 2011 / Jun 30, 2012)

18,351

19,639

Net:

16,592Net:

16,954

+362+2.2%

+1,288+7.0%

25Deutsche Bahn AG Road Show Asia 2012

Debt and financing

Expected funding requirements in 2012

Bond issues 2011/12

Redemptions (2012) -2.0

Net liquidity

(as of Jan 1, 2012) +1.7

Net capex / other -4.2

Net liquidity

(as of Dec 31, 2012) +1.7

Anticipated funding requirements 2012 (€

bn)

Operating cash flow +4.8

Dividend for 2011 financial year -0.5

Bond issues (as of June 30, 2012) +1.4

Planned additional bond issues in 2012 +0.5

MaturityCurrency

4.6YNOK 1.72 17

5.5YCHF 2.20 40

12YCHF 3.32 72

13.9YEUR 3.47 85

12YEUR 3.12 71

€ all-in-

costs (%)

Swap spread (BP)Million

750

150

100

98

500

10YGBP 2.82* 71400

2012: 6 transactions / €

1.4 bn

2011: 11 transactions / €

2.1 bn

Including 5 transactions with Asian investors

in HKD, EUR and USD (€

377 mn)

*Not swapped, cost in GBP.

26

Ratings

Very good ratings:

Moody’s:

Aa1/negative S&P: AA/stable

Fitch:

AA/stable

Key rating driver:

Improvements in performance, revenues and profits

Bond issues (€

bn)

Debt and financing

Rating and financing activities

Stable financial profile, sound financing structure and conservative funding strategy

DB guarantees overall mobility in Germany and is Europe‘s largest company providing integrated mobility, transport and logistics services

Federal obligations resulting from Art. 87e German Constitution-

“Infrastructure obligations”: High share in funding of infrastructure capex in Germany,

-

“Public interest obligations”: Funds for ordering local passenger transport services in Germany, amounting to around €

6.9 bn p.a.

-

Privatization threshold: constitutionally mandated Federal majority shareholding (“ownership clause”)

1.4

2.1

2.5

2.2

0.6

1.81.71.7

2.2

1.21.0

00

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Total: €

18.4 bn, Ø

p.a.: €

1.4 bn

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026

Maturity profile of financial debt (as of Jun 30, 2012; €

bn; incl. underlying swaps)

Bonds Eurofima EIBBank Federal loans Leasing

1.8

1.41.2

1.1

2.3

1.71.9 1.8

1.7 1.7

1.1

0.2

0.7

0.2

0.6

1.6

Deutsche Bahn AG Road Show Asia 2012

27

(€

mn) 2011

ROCE (%)

>7.5

Revenues adjusted ~40,000

EBIT adjusted >2,600

Outlook 2012 (as of March 2012)

7.3

37,901

2,309

2012 financial year –

Outlook

Outlook for 2012 financial year is still positive

Net financial debt (as of Dec 31)

16,592

Gross capital expenditures

7,501

>7.5

~39,000

>2,600

Outlook 2012 (as of July 2012)

Change

Dampened growth expectations at DB Schenker

Outlook confirmed

Outlook confirmed

Outlook confirmed

Outlook confirmed

Deutsche Bahn AG Road Show Asia 2012

Appendix

29

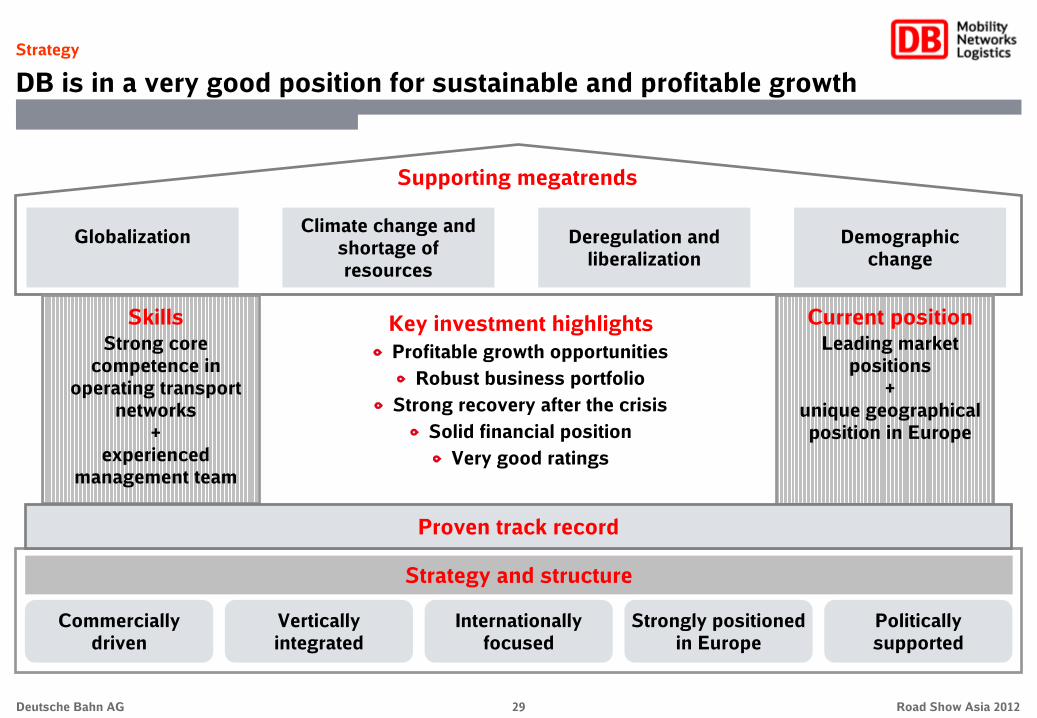

Strategy

DB is in a very good position for sustainable and profitable growth

SkillsStrong core

competence in operating transport

networks +

experienced management team

Supporting megatrends

Globalization Climate change and shortage of resources

Deregulation and liberalization

Demographic change

Key investment highlightsProfitable growth opportunities

Robust business portfolioStrong recovery after the crisis

Solid financial positionVery good ratings

Current positionLeading market

positions

+

unique geographical position in Europe

Strategy and structure

Vertically integrated

Internationally focused

Politically supported

Strongly positioned in Europe

Commercially driven

Proven track record

Deutsche Bahn AG Road Show Asia 2012

30

Leading market position

Revenues (€

bn)

Appropriate returns

ROCE (%)

Financial stability

Redemption coverage (%)

6%

≥10%

18%

≥30%

34.4

70

As

a

profitable

market leader we offer our customers

first-class

mobility and logistics solutions

11TopTop

Strategy –

DB 2020

We want to become the profitable market leader by 2020

Deutsche Bahn AG Road Show Asia 2012

31

Strategy –

DB 2020

We want to improve customer satisfaction

1)

Including €

34 billion DB funds

86Areas for action (selected examples)

Expand customer information and service

Modernization of vehicle fleet

Upgrade and expand infrastructure

Consistent process quality

Link global IT systems together

Modernize and expand passenger stations

Push product and process innovation

Customer and quality

Information and Service

Gross capital expendituresuntil 2020

billion €1)

Deutsche Bahn AG Road Show Asia 2012

32

Acquisitions and

tenders

Expand existing and

new customer business

+100%

34,4

70

Profitable growth Areas for action

(selected examples)

Retain integrated structure and entrepreneurial approachImprove capacity utilization and productivity Develop, optimize and integrate transport networksTake advantage of opportunities arising from liberalization of European passenger transport marketExpand industrial competenceFurther development of cross-modal mobility and logistical

Strategy –

DB 2020

We intend to defend and expand our leading market position

Deutsche Bahn AG Road Show Asia 2012

33

Top 10 in Germany

Top 20 in Germany

…

…

NEW

TopTop

As a top employer

we

win and build loyalty with qualified employees

who work

with enthusiasm for DB and its customers

I’m a proud DB

employee

Strategy –

DB 2020

We want to become one of the top employers

Deutsche Bahn AG Road Show Asia 2012

34

Cultural change/ employee satisfaction

employeesenthusiastically

work

for DB and its customers

Qualified Areas for action (selected examples)

Regional future-focused discussions

Employee satisfaction

Employer attractiveness

Manage demographics

Understanding leadership

Diversity in leadership

Compatibility of career and family

Internationalization

Talent Pools

Career planning

Strategy –

DB 2020

We want to significantly increase employee satisfaction

Deutsche Bahn AG Road Show Asia 2012

35

Cultural change/ employee satisfaction

Strategy –

DB 2020

Our values form the foundation of how we interact with each other

Deutsche Bahn AG Road Show Asia 2012

36

Specific CO2

-

emissions DBShare of renewable energy in the DB Bahn energy mix

-15%TopTop

+75%

Noise emissions –

rail

-50%

20%

35%

Strategy –

DB 2020

By 2020 we’ll be recognized as the pioneer of environmental measures

As an eco-pioneer our products set standards for the efficient use of resources

Deutsche Bahn AG Road Show Asia 2012

37

Resource preservation/ emissions and noise reduction We are a leader in

environmental protection

Areas for action (selected examples)

Use of wind and hydro-

electric energy

Noise abatement

Efficient use of energy

Freight transport using Eco Solutions

CO2

-free offers for passenger transport

Electro-mobility on the road

Efficient usage of materials and resources

Strategy –

DB 2020

We will expand our leading environmental position

Deutsche Bahn AG Road Show Asia 2012

38

Sustained recovery of global economy (GDP world +2.5%)Germany as a driver of economic growth in Europe

(GDP +3.0%)Economic development weakened during the course of the yearPrevailing insecurities as a result of the Euro-/debt crisisHigh cost burdens due to increase in energy, personnel and maintenance expenses

2011 Financial Year –

Overview

Highlights 2011

Positive development of German rail passenger transportFirst-time full-year inclusion of Arriva; major success in tender procedures in Denmark and Sweden

Rail freight transport again with strong growth Varying development in freight forwarding and logistics: strong growth in European land transport, further growth in ocean freight, decline in air freight

Train-path demand reached a new all time high at 1,051 mn train-path kmNon-Group demand showed again double digit growth rates, share of total train-path demand increased to 20.9%

General conditions

Passenger transport

Transport and

logistics

Infrastructure

Deutsche Bahn AG Road Show Asia 2012

39

Key figures (€

mn)

EBIT adjusted

Net profit for the year

Net financial debt as of Dec 31

2,309

1,332

16,592

37,901

35,888

2011 Financial Year –

Overview

Strong development in 2011 financial year

2011

Revenues adjusted

Revenues comparable

+23.7

+25.9

-2.0

+10.1

+4.3

€ %Change

+443

+274

-347

+3,491

+1,481

+8.9+610Gross capital expenditures 7,501

+24.0+497Net capital expenditures 2,569

ROCE (%) 7.3 --

2010

1,866

1,058

16,939

34,410

34,407

6,891

2,072

6.0

Deutsche Bahn AG Road Show Asia 2012

40

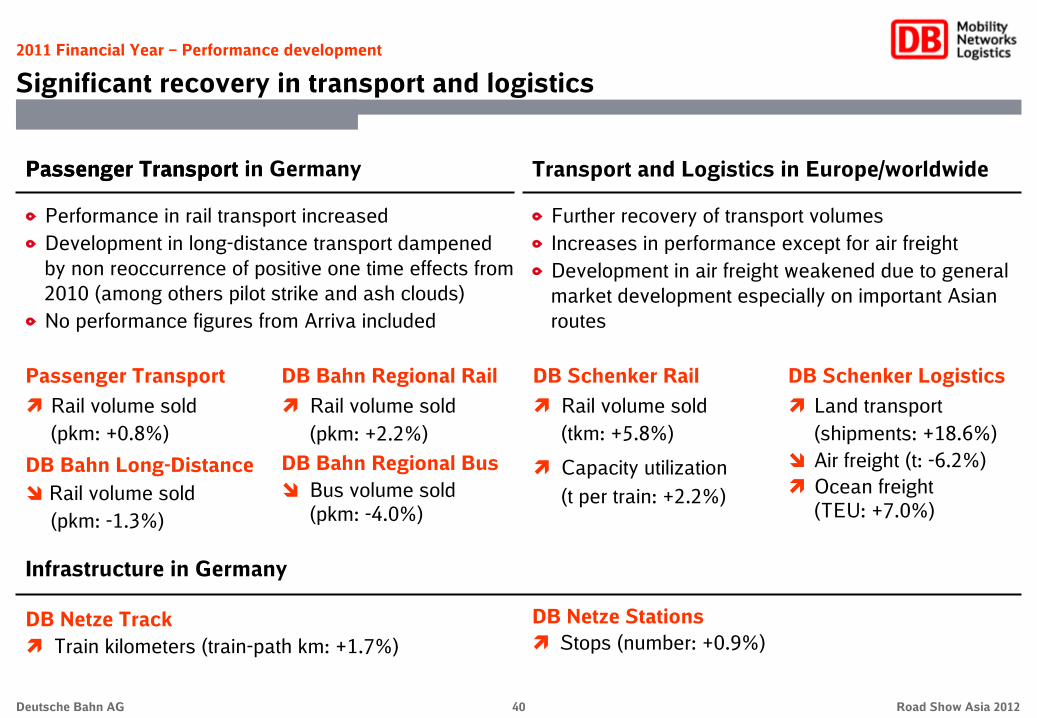

2011 Financial Year –

Performance development

Significant recovery in transport and logistics

Performance in rail transport increasedDevelopment in long-distance transport dampened by non reoccurrence of positive one time effects from 2010 (among others pilot strike and ash clouds)No performance figures from Arriva included

Passenger Transport

DB Netze Track

Train kilometers (train-path km: +1.7%)

Infrastructure in Germany

DB Netze Stations

Stops (number: +0.9%)

Passenger Transport

Rail volume sold (pkm: +0.8%)

DB Bahn Long-Distance

Rail volume sold (pkm: -1.3%)

DB Bahn Regional Rail

Rail volume sold (pkm: +2.2%)

DB Bahn Regional Bus

Bus volume sold (pkm: -4.0%)

Further recovery of transport volumesIncreases in performance except for air freightDevelopment in air freight weakened due to general market development especially on important Asian routes

Transport and Logistics in Europe/worldwide

DB Schenker Rail

Rail volume sold (tkm: +5.8%)

Capacity utilization (t per train: +2.2%)

DB Schenker Logistics

Land transport (shipments: +18.6%)

Air freight (t: -6.2%)

Ocean freight

(TEU: +7.0%)

Passenger Transport in Germany

Deutsche Bahn AG Road Show Asia 2012

41

2011 Financial Year –

Revenues

Further increase in revenues

35,88835,87634,410

37,979 37,901 2,025 1278

Revenues (€

mn)

2010 2011 2011comparable

+10.4%

Changes in scope of

consolidation

+1,478 / +4.3%

FX

effects

2011adjusted

-5.8%-P. -0.0%-P.

Special items

-0.3%-P.

Deutsche Bahn AG Road Show Asia 2012

42

2011 Financial Year –

Revenues

Revenue increases across all business units

DB Group

Total revenues (€

mn)

+1,481 +4.3-2,0222) 12

€ %

Changes

DB Schenker Logistics +542 +3.8-1 -14

DB Netze Track +62 +1.4- -

DB Netze Stations +33 +3.2- -

DB Netze Energy +352 +14.1- -

DB Bahn Long-Distance +56 +1.5-8 -1

DB Bahn Regional +115 +1.3- -

DB Arriva +145 +11.7-2,001 15

DB Services +139 +10.9- -

DB Schenker Rail +340 +7.4-12 12

Other/Consolidation -303 +4.1- -

Consol.1) FX

Changes

35,888

14,852

4,642

1,077

2,853

3,785

8,718

1,381

1,413

4,924

-7,754

34,410

2010

14,310

4,580

1,044

2,501

3,729

8,603

1,236

1,274

4,584

-7,451

37,901

2011

14,867

4,642

1,077

2,853

3,794

8,718

3,367

1,413

4,924

-7,754

2011

comp.

1) Scope of consolidation; 2)

Net amount, including €

3 mn from 2010Deutsche Bahn AG Road Show Asia 2012

43

572,309

1,8661,817

75

49

2,177

2011 Financial Year –

Profits

EBIT development significantly positive

EBIT and EBIT adjusted (€

mn)

EBIT Special items EBIT adjusted

2010 2011

+19.8%

+23.7% +443

EBIT Special itemsEBIT adjusted Reclassifications

Deutsche Bahn AG Road Show Asia 2012

44

2011 Financial Year –

Profit development

Differentiated EBITDA development by business units

Changes

by business units (€

mn)

DB Group

DB Schenker Rail

DB Services

DB Netze Track

DB Netze Stations

DB Bahn Long-Distance

DB Bahn Regional

DB Netze Energy

DB Schenker Logistics

DB Arriva

Other/Consolidation

+23 +4.8

+10 +0.7

+183 +129

+34 +11.3

+94 +19.7

-9 -3.1

+100 +6.6

+8 +2.3

-6 -3.6

+53 -12.6

+490 +10.5

EBITDA adjusted (€

mn)

5,141

336

278

1,624

351

504

1,361

159

572

325

-369

2011

4,651

302

287

1,524

343

481

1,351

165

478

142

-422

2010

Deutsche Bahn AG Road Show Asia 2012

€ %

Changes

45

2011 Financial Year –

Profit development

Reconciliation to the adjusted income statement

Income statement (€

mn)

Com-

pounding/

discounting IFRS

Personnel expenses -

Depreciation -

Operating profit | EBIT adjusted -

Net interest | Operating net interest 98

Revenues -

Inventory changes and internally produced and capitalized assets -

Other operating income -

Other operating expenses -

Cost of materials -

Operating profit after interest 98

Other financial result -98

PPA amortization customer contracts -

Extraordinary result -

Results from at equity investments | investment income -

Profit before taxes -

Net investment

income

-

-

-

-

-

-

-

-

-

-

-1

-

-

1

-

PPA-

amorti-

zation

-

75

75

-

-

-

-

-

-

75

-

-75

-

-

-

Personnel-

related provisions

-

-

-114

-

-

-

-114

-

-

-114

-

-

114

-

-

Restruc-

turing of US domestic business

28

13

118

-

-78

-

-22

70

107

118

-

-

-118

-

-

Decommis-

sioning of GKN I

-

-

46

-

-

-

-

-

46

46

39

-

-85

-

-

Other

-

44

7

-

-

7

-76

-

32

7

-

-

-7

-

-

2011

-13,076

-2,964

2,177

-840

37,979

2,457

3,062

-4,375

-20,906

-

3

-

-

19

1,359

2011

adjusted

-13,048

-2,832

2,309

-742

37,901

2,464

2,850

-4,305

-20,721

1,567

-57

-75

-96

20

1,359

RECLASSIFICATIONS ADJUSTMENT OF SPECIAL ITEMS

Deutsche Bahn AG Road Show Asia 2012

46

2011 Financial Year –

Profit development

Significant improvement in operating profits

Adjusted income statement (€

mn) 2010

-11,583

-2,785

1,866

-752

34,410

2.207

2,636

-3,885

-19,134

1,114

-183

-

-49

18

900

Change

-1,465

-47

+443

+10

+3,491

+257

+214

-420

-1,587

+453

+126

-75

-47

+2

+459

Thereof due to changes in scope

of consolidation

-943

-96

+78

-8

+2,022

+4

+55

-281

-683

+70

+2

-50

-

+2

+24

Thereof due to exchange rate

effects

+6

+1

-20

-2

-12

-

-11

-13

+9

-22

-14

-

-

-

-36

2011

-13,048

-2,832

2,309

-742

37,901

2,464

2,850

-4,305

-20,721

1,567

-57

-75

-96

20

1,359

Personnel expenses

Depreciation

Operating profit | EBIT adjusted

Net interest | Operating net interest

Revenues

Inventory changes and internally produced and capitalized assets

Other operating income

Other operating expenses

Cost of materials

Operating profit after interest

Other financial result

PPA amortization customer contracts

Extraordinary result

Results from at equity investments | investment income

Profit before taxes

Deutsche Bahn AG Road Show Asia 2012

47

2011 Financial Year –

Balance sheet

Development of balance sheet

(€

mn, as of Dec 31)

Equity and liabilities

Assets

+/-

Current assets +259

Cash and cash equivalents +228

Equity +810

Non-current liabilities -524

Current liabilities -498

Non-current assets -471

Total assets -212

AssetsEquity and

liabilities

Non-current assets(85%, 2010: 86%)

Current assets

(15%, 2010: 14%)

Equity (29%, 2010: 28%)

Non-current liabilities(47%, 2010: 48%)

Current liabilities

(24%, 2010: 25%)

Maturity structure (as of Dec 31, 2011)

€

51.8 bnTotal€

51.8 bnTotal

Property, plant and equipment -501

Trade receivables +217

Intangible assets +15

Deferred tax assets -10

Financial debt -27

Financial debt -175

Trade liabilities

2011

7,732

1,703

15,126

24,238

12,427

44,059

51,791

37,372

4,094

4,169

1,461

16,367

1,984

4,312 +26

2010

7,473

1,475

14,316

24,762

12,925

44,530

52,003

37,873

3,877

4,154

1,471

16,394

2,159

4,286

Deutsche Bahn AG Road Show Asia 2012

48

4,399

983

500

2,569

347

Reconciliation of decline in net financial debt (€

mn)

Operatingcash flow

2011 Financial Year –

Net financial debt

Decline in net financial debt

Net capex

Changes in

working

capital/Other

Dividend Surplus of funds

Dec 31, 2009 Dec 31, 2010 Dec 31, 2011

-347

16,592

Net financial debt (€

mn)

15,011

13,966

-1,045

DividendArriva

16,092

16,939-847

Deutsche Bahn AG Road Show Asia 2012

49

Net financial debt

+ Commercial paper

+ Bank borrowings (incl. European Investment Bank (EIB))

+ Finance Lease (present value)

+ Other finance liabilities

Financial debt excl. Federal loans

+ Federal loans (present value)

Bonds

+ EUROFIMA loans

-

Cash and cash equivalents and receivables from financing

Financial debt

-347

+/-

+160

-155

+154

-8

+642

-844

+799

-

+804

+145

-202

Financial debt (€

mn; as of Dec 31)

2011 Financial Year –

Financial debt

Components of financial debt

2011

16,592

202

991

1,270

9

16,259

2,092

12,634

1,153

14,980

1,759

18,351

Dec 31, 2010 Dec 31, 2011

18,553 18,351

Net:

16,939Net:

16,592

-347

2010

16,939

42

1,146

1,424

17

15,617

2,936

11,835

1,153

14,176

1,614

18,553

-202

Deutsche Bahn AG Road Show Asia 2012

50

2010 2011

2011 Financial Year –

Capital expenditures

Significant increase of capital expenditures

By business units (€

mn) 2010Gross capital expenditures (€

mn)€ %

Change

DB Group

DB Schenker Rail

DB Services

DB Netze Track

DB Netze Stations

DB Bahn Long-Distance

DB Bahn Regional

DB Netze Energy

DB Schenker Logistics

DB Arriva

6,891

350

177

4,986

511

48

287

144

189

187

Other/consolidation 12

+610

-90

+70

+157

+36

+91

+106

+63

+57

+113

+7

+8.9

-25.7

+39.5

+3.1

+7.0

-

+36.9

+43.8

+30.2

+60.4

+58.3

6,891

7,501

2,0722,569

Net:

+610 +8.9%

+497 +24.0%

2011

7,501

260

247

5,143

547

139

393

207

246

300

19

Deutsche Bahn AG Road Show Asia 2012

51

H1 2012 –

Revenues

Revenue increase in almost all business units

DB Group

Total revenues (€

mn)

+344 +1.8–53 –219

€ %

Change

DB Schenker Logistics +70 +0.9–28 –151

DB Netze Track +59 +2.6– –

DB Netze Stations +22 +4.1– –

DB Netze Energy –8 –0.6– –

DB Bahn Long-Distance +144 +7.9– 0

DB Bahn Regional +60 +1.4– –

DB Arriva +64 +3.9–14 –62

DB Services +39 +6.0– –

DB Schenker Rail –13 –0.5–11 –6

Other/consolidation –93 +2.5– –

Consol.1) FX

Adjustments

19,220

7,536

2,328

559

1,440

1,969

4,425

1,696

687

2,468

–3,888

18,876

H1 2011

7,466

2,269

537

1,448

1,825

4,365

1,632

648

2,481

–3,795

19,492

H1 2012

7,715

2,328

559

1,440

1,969

4,425

1,772

687

2,485

–3,888

H1 2012

comp.

1) Changes in scope of consolidation.Deutsche Bahn AG Road Show Asia 2012

52

H1 2012 –

Profits

In total positive EBIT development on business unit level

EBIT adjusted (€

mn)

+146DB Bahn Long-Distance –

–30DB Bahn Regional –6.3

–34DB Schenker Rail –58.6

+31DB Schenker Logistics +18.2

–32DB Services –40.0

+136DB Netze Track +51.9

DB Netze Stations +16 +12.9

+31DB Netze Energy +129

–99Other/consolidation +55.3

+188DB Group +16.6

+23DB Arriva +32.4

46

477

58

170

80

262

124

24

–179

1,133

71

2011€ %

Change

17,830

2,875

909

32,479

Capital employed

192

447

24

201

48

398

140

55

–278

1,321

94

2012

9,924

1,237

198

16,954

Net financial debt

Deutsche Bahn AG Road Show Asia 2012

53

Capital expenditures (€

mn)

H1 2011 H1 2012

2,689

3,038

Gross:

+349

+13.0%

Highlights

DB Group

Key gross capex are unchanged:

74% Infrastructure

94% Germany

Gross and net capex increased by about €

350 mn respectively €

360 mn

Still delays in delivery of new vehicles, in particular at DB Bahn Regional

Business units

DB Bahn Regional €

+162 mn

DB Netze Track €

+129 mn

H1 2012 –

Capital expenditures

Significantly higher capital expenditures

1,049

1,408

Net: +359

+34.2%

Deutsche Bahn AG Road Show Asia 2012

54

H1 2012 –

Capital expenditures

Significant higher capital expenditures

By business units (€

mn)H1

2011Capital expenditures (€

mn)€ %

Change

DB Group

DB Schenker Rail

DB Services

DB Netze Track

DB Netze Stations

DB Bahn Long-Distance

DB Bahn Regional

DB Netze Energy

DB Schenker Logistics

DB Arriva

2,689

135

97

1,872

190

40

116

39

89

72

Other/consolidation 39

+349

–16

+28

+129

–1

+17

+162

+21

+9

+20

–20

+13.0

–11.9

+28.9

+6.9

–0.5

+42.5

+140

+53.8

+10.1

+27.8

–51.3

2,689

3,038

1,049

1,408

Net:

+359

+34.2%

H1 2012

3,038

119

125

2,001

189

57

278

60

98

92

19

Gross:

+349

+13.0%

H1 2011 H1 2012

Deutsche Bahn AG Road Show Asia 2012

55

Derivation of change in H1 2012 (€

mn)

OperatingCash

flow

H1 2012 –

Net financial debt

Increase in net financial debt as of Jun 30, 2012

Net capex

Working capital/

other

Dividend Fundingneed

+362

Net financial debt (€

mn)

Arriva

+351

-1,408

2,327

-756

-525

-362

Jun 30,

2011

Jun 30,

2012

Dec 31,

2011

Dec 31,

2010

16,939 17,290 16,592 16,954

-347/-2.0%

Deutsche Bahn AG Road Show Asia 2012

56

9.27.9 8.1

11.610.88.7

Dec 31,2010

Dec 31,2011

Jun 30,2012

Dec 31,2010

Dec 31,2011

Jun 30,2012

53.246.040.8

35.1

32.430.6

Dec 31,2010

Dec 31,2011

Jun 30,2012

H1 2012 –

Order book

Order book in regional transport increased significantly

DB order book* (€

bn)

78.471.4

43.432.3 37.3

23.3

21.421.7

Dec 31,2010

Dec 31,2011

Jun 30,2012

58.754.1

0.80.8

18.916.6

DB Group DB Bahn Regional (rail) DB Bahn Regional (bus) DB Arriva

* Secured and unsecured revenues (mostly farebox revenues).

Secured

Unsecured

Deutsche Bahn AG Road Show Asia 2012

88.3

+9.9 +13%

66.7

+7.0 +9.8% +8.0

+14%+4.6

+8.5%

0.7

-0.1

-14%

-

+1.9 +10%

+2.3 +14%

20.8

57

2011 Financial Year –

Order book

€

46 bn of long-term secured revenues in regional transport

Long-term secured revenues (as of Dec 31, 2011) Remarks

5.7 5.4 4.7 4.1 3.3 2.4 2.1 1.7

10.2

5.9

4.0 3.83.8

3.22.7

1.8 1.6 1.4

6.2

3.8

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021ff

Total:

€

78 bn (€

46 bn secured + €

32 bn unsecured) As of December 31, 2011 the volume of revenues secured by long-term rail transport contracts (concession fees) in the DB Bahn Regional business unit increased by €

5.0 billion. The total of unsecured revenues decreased slightly by €

0.3 bn.

As of December 31, 2011, volume of revenues secured by long-term contracts (concession fees) in the DB Arriva business unit increased by €

0.2 billion. The total of unsecured revenues increased by €

2.1 bn.

secured unsecured

9.7 9.7 9.28.5

7.3

6.0

4.2 3.73.1

16.4

Deutsche Bahn AG Road Show Asia 2012

58

Capex and financing (€

bn)

59

125Total

16

35

2005 2006 2007 2008 2009 2010 2011

Net financial debt (as of Dec 31, €

bn)

19.7 19.6

16.5 15.915.0

16.9

-3.1 / -

15.7%

Proven track record: Capex campaign and deleveraging

Despite high capex volume significant reduction of net financial

debt

16.6

95

14

64

DB funds

133Total

Infra-structure

17

38 37Other

Investment

grants

Interest-free

loans

1994-2011

FinancingCapex

Other grants

DB funds

(71%)

(29%)

Deutsche Bahn AG Road Show Asia 2012

59

Major portfolio changes in DB Group: total M&A transactions (EqV) of €

11 bn

(€

4 bn divestitures and €

7 bn acquisitions)

2001 2002 2005 20062004 2007

Stinnes,Joyau

BAX,StarTrans

RAG Bahn

Brenntag,Interfer,Mitropa

2008

EWS

2009

Transfesa

…

Proven track record: Reshaping the entire DB Group

Expansion of transport networks partly through focused portfolio

measures

2010

PCC

2011

NordCargo

SDS

Rail freight

Logistics

Passenger transport

Divesti-

tures

DSB Gods

Deutsche Eisenbahn-

reklame

Scandlines,Aurelis,

Nuclear Cargo

Linjegods Spain-Tir

Arcor

Arriva

Romtrans

Chiltern,PanBus

RailNon Rail 9%

91%

RailNon Rail

31%

69%

2001 2003

Non Rail

48% 52%

Rail

2006

Non Rail

47% 53%

Rail

2010

Non Rail

47% 53%

Rail

2008

Revenue split

Non Rail

48% 52%

Rail

2011 / H1 2012

2012

COBRA

Jean Heck

GrandCentral

Arriva Germany

Suomen Kiitoautot

Ambuline

TFG Transfracht

Metrans,Polzug

Deutsche Bahn AG Road Show Asia 2012

60

Long-distancetransport

Land transport

Contract

logistics/SCM

Air/ocean freight

Regionaltransport

Rail infrastructure

Rail freighttransport

Skills and current positions

Successfully developed transport networks ensure top market positions

DB

worldwide

No. 2

Air freight

No. 2

Long-distance rail passenger transport

No. 1

Regional rail passenger transport

No. 2

Urban bus transport

No. 1

Rail infrastructure

No. 1

Rail freight

transport

No. 3

Ocean freight

No. 6

Contract logistics/SCM

No. 1

Land transport

Our transport networks DB

in Europe

Deutsche Bahn AG Road Show Asia 2012

61

Contacts

DB road show team

Dr. Richard LutzCFO

Wolfgang ReuterGroup Treasurer, Head of Mergers and Acquisitions

Tel.:

+49 30 297-64300

Address

Deutsche Bahn AG/

DB Mobility Logistics AG

Europaplatz 1

10557 Berlin

Germany

Internet

www.db.de/ir-e

www.db.de/ir-dbml-e

Robert Allen StrehlHead of Investor Relations

Tel.:

+49 30 297-64030

Sascha FriedrichManager Investor Relations

Tel.:

+49 30 297-64032

Hartwig SchneidereitHead of Capital Market Financing

Tel.:

+49 30 297-64010

Marcus MehlingerHead of Equity and Debt Financing

Tel.:

+49 30 297-64006

Ute HaasCapital Market Financing

Tel.:

+49 30 297-64007

Deutsche Bahn AG Road Show Asia 2012

62

Appendix

Disclaimer and photo credits

This information contains forward-looking statements or trend information that are based on current beliefs and estimates of Deutsche Bahn

AG’s/DB Mobility Logistics AG´s

management and involves known and unknown risks and uncertainties. They are not guarantees of future performance. In addition to statements which are forward-looking by reason of context, including without limitation, statements referring to risk limitations, operational profitability, financial strength,

performance targets, profitable growth opportunities, and risk adequate pricing, as well as the words "may, will, should, expects, plans, intends, anticipates, believes, estimates, predicts, or continue", "potential, future, or further", and similar expressions identify forward-looking statements. These forward-looking statements are subject to certain risks and uncertainties that could cause the Company's actual results or performance to be materially different from those expressed or implied by such statements. Many of these risks and uncertainties relate to

factors that are beyond Deutsche Bahn

AG’s/DB Mobility Logistics AG’s ability to control or estimate precisely, e.g. future market and

economic conditions and the behavior of market participants. Deutsche Bahn

AG and DB Mobility Logistics AG do not intend or assume any obligation to update these forward-looking statements. This document represents the Company‘s judgment as on the date of this presentation.

Page 4

–

Jo Kirchherr, Claus Weber

Page 11

–

ClipDealer

(#393325), Max Lautenschläger, Wolfgang Klee, Michael Neuhaus

Page 12

–

Tobias Heyer, ClipDealer

(#218972), ClipDealer

(#132843), Simon Kent, ClipDealer

(#245691)

Page 14

–

Jo Kirchherr, Claus Weber, S. Müller, ClipDealer

(#70420)

Page 30 –

Jo Kirchherr, Claus Weber

Page 31

–

Jochen Manz, Christian Bedeschinski

Page 32

–

Thomas Schwörer

Page 33

– S. Müller

Page 34

–

Heiner Müller-Elsner

Page 35

–

GettyImages

(#88752051)

Page 36

–

ClipDealer

(#70420)

Page 37

–

Bartlomiej

Banaszak

Page 60

–

Günter Jazbec, Ralf Braum, Claus Weber, Stefan Warter, Rainer Garbe, Michael Neuhaus

Page 60

–

Pablo Castagnola, Max Lautenschläger

Disclaimer

Photo credits

Deutsche Bahn AG Road Show Asia 2012