determinants of wool -...

TRANSCRIPT

DETERMINANTS OF

WOOL IMPORTS BY THE

COMMONWEALTH OF INDEPENDENT STATES

ABARE RESEARCH REPORT 92.9

Adam Malarz

Greg P. Connolly

David Barrett

and

Q. T. Tran

m

e ABARE

O Commonwealth of Australia 1992

This work is copyright. The Copyright Act 1968 permits fair dealing for study, research, news reporting, criticism or review. Selected passages, tables or diagrams may be reproduced for such purposes provided acknowledgment of the source is included. Major extracts or the entire document may not be reproduced by any process without the written permission of the Executive Director, ABARE.

ISSN 1037-8286 ISBN 0 642 18045 8

Australian Bureau of Agricultural and Resource Economics GPO Box 1563 Canberra 2601

Telephone (06) 272 2000 Facsimile (06) 272 2001

ABARE is a professionally independent research organisation attached to the Department of Primary Industries and Energy.

ABARE project 7238.101

Foreword

Until the late 1980s the Soviet Union was the third largest importer of Australian wool, after the European Community and Japan. Since March 1990, however, the region that was the Soviet Union has bought very little Australian wool. This turnaround in wool purchases was one of the factors contributing to the demise of Australia's Reserve Price Scheme for wool. A resumption of purchasing of wool by members of the Commonwealth of Independent States could contribute materially to a reduction in Australia's stockpile of wool.

An understanding of the determinants of wool demand by the former Soviet Union and by the independent states that have emerged from the political restructuring process in the region is important for policy makers in the Australian wool industry. This project provides information on the determinants of CIS demand for wool.

BRIAN FISHER Executive Director. ABARE

June 1992

iii

Acknowledgments

The authors wish to acknowledge the comments on the paper provided by Franz Mizera of the International Wool Secretariat and ABARE colleagues Paul Morris and Terry Sheales.

Adam Malarz now works with the Organisation for Economic Co- operation and Development, and Greg Connolly works with the Industry Commission.

Research on this project was supported by a grant from the Wool Research and Development Corporation. Travel assistance under the Australia-Soviet Union Agricultural Co-operation Agreement enabled Adam Malarz to visit the Soviet Union in 1990 to collect information which was used for this and other papers. This assistance is gratefully acknowledged.

Contents

Summary 1

1 Introduction 8

2 Background Production of wool in the region Wool textile industry Consumption of wool Trade in wool and wool products Shares of the Soviet wool import market

3 Restructuring the former republics of the Soviet Union 25

Nature of current changes 25 Debt problem 27 Independence of the republics 30 Conclusions 32

4 Wool demand and supply 33 Impacts of reforms on Soviet wool production 33 Price effects of implementing a market oriented system in the region 35 Fibre substitution in processing and demand 36 Effects of the disintegration of central planning on the structure of the market 38 Likely situation in major wool producing and consuming republics 42 Conclusions 44

5 Concluding remarks 45

Appendixes A Trade effects of implementing a market system in

the Soviet Union B A model of Soviet wool imports

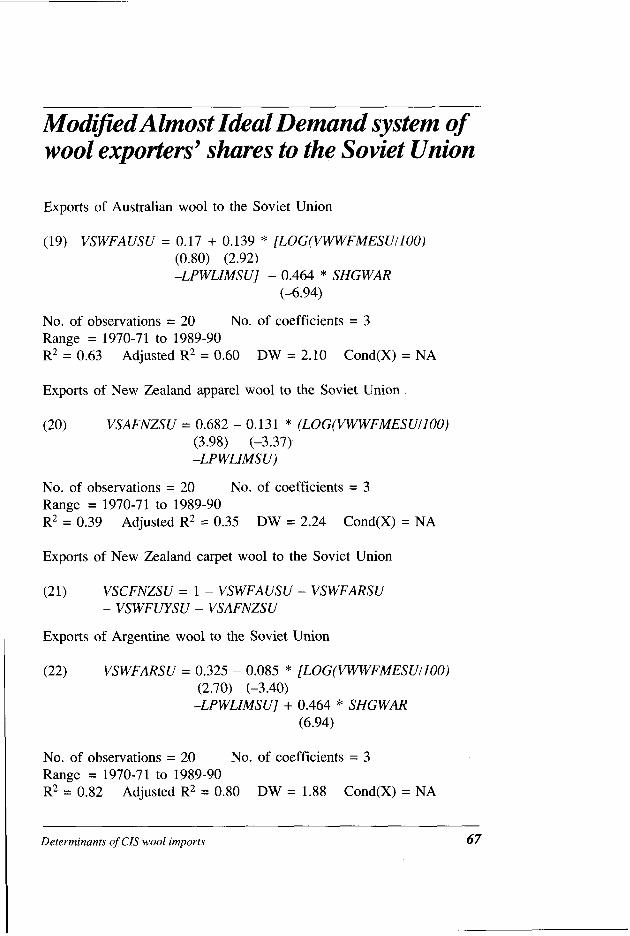

Total wool imports Wool exporters' shares Model results Concluding remarks Wool import prices in US dollars Total volume of wool exports from the main exporters to the Soviet Union Modified Almost Ideal Demand system of wool exporters' shares to the Soviet Union Data specifications

References 73

Figures A Map of the region 11 B Distribution of Soviet wool production and the sheep

flock in 1988, by republic 12 C The Soviet wool industry 18 D Wool and grain imports and the value of energy exports by

the Soviet Union 19 E Soviet wool imports, by source 23 F Average annual growth in Soviet real net material product 25 G Shares of fibres consumed in the Soviet Union 37 I

H Shares of fibres consumed in the United States

J Schematic representation of change from a planned economy

37 I I Total capital investment per person in the republics in 1988 39

to a market oriented economy 49 K Flows of foreign exchange available to Soviet importers

for imports of wool and other merchandise 52

Tables 1 Sheep numbers, wool production and cut per head in the

Soviet Union 10 2 Distribution of sheep, by republic 10 3 Wool textile activity in the Soviet Union 14 4 Estimated Soviet mill consumption of textile fibres 15 5 Per person consumption of apparel fibres in selected

countries 16 6 Prices of wool garments in the Soviet Union and their

share of family income 17 7 Conditional own-price and cross-price elasticities for Soviet

wool imports from main exporters 61

vii

The Soviet Union - Commonwealth of Independent States

For the purpose of this report, the Soviet Union refers to the area encompassing the fifteen republics that, until August 1991, constituted the Union of Soviet Socialist Republics. In December 1991 the Soviet Union ceased to exist as a state. A Commonwealth of Independent States has been established by eleven former Soviet republics. As at May 1992 the constitution of this new grouping of states had not yet been agreed. The individual republics have proclaimed their independence and there is a move to establish sovereignty of the autonomous regions. The Russian Republic declared that it represents the interests of the republics and assures some form of legal continuity following the dissolution of the Soviet Union. Georgia and the Baltic republics have not been participating in the continuing negotiations on the preservation of some political and economic links among the former Soviet republics.

viii

Summary

During the 1980s the Soviet Union emerged as an important export market for Australian wool. In 1988-89 the Soviet Union purchased around 14 per cent of Australian wool exports. These imports represented around 80 per cent of all Soviet imports of raw wool. In the years following 1989, with the deterioration in the Soviet economy, foreign exchange difficulties and the earlier effects of high wool prices, Soviet purchases of Australian wool have fallen sharply.

The move for independence by the Soviet republics under the program of perestroika (restructuring) resulted in the emergence of new sovereign states, which have proclaimed their independence. However, the legacy of the centrally planned system will be difficult to eliminate. Lack of business infrastructure and little understanding of the market system make the current period of transition very difficult and uncertain. In the process of political change the new sovereign states may form diverse trade and economic unions or act independently. With this instability and with the large number of changes taking place in the region and in other Eastern European countries, the nature of the future political and economic environment remains unclear.

In the short to medium term, the outlook for an improvement in wool trade with the republics of the former Soviet Union is pessimistic, even if the republics quickly develop market oriented economies. Over this timeframe the governments of the republics are likely to attempt to maintain imports of basic supplies. Wool may be one of the items on these lists of staples since the ongoing dislocation

Soviet Union a big market for

Australian wool in the 1980s

Future political and economic

environment of the region is unclear

Wool imports are likely to be a lower priority than other vital imports in the

short term

Determinants of CIS wool imports

Sheep numbers are unlikely to increase much in the longer term

. . . so there is scope for increased wool imports in the future

In 1990 the Soviet Union was the world's second largest wool producer

in these countries will adversely affect their output of wool. But in the short term, wool is likely to be a lesser priority than other vital imports such as food, pharmaceuticals and machinery.

In the longer term, if the republics become more market oriented and prices are used to provide incentives for resources to move to their most efficient uses, some republics may increase their production of grains and manufacturing goods. But because the climate is harsh in most parts of the region and there is competition for land between wool production and food production in the milder climatic areas of southern Ukraine, Georgia and Moldova, sheep numbers are unlikely to increase significantly.

Because demand for wool clothing per person is likely to continue to be strong, there may be scope for increased exports of wool to the region. To meet this export demand, Australian wool exporters will have to develop innovative ways of managing the increasingly complex wool markets in .the republics and of overcoming some of the foreign currency restrictions. Considerable risk and uncertainty are likely to be involved.

Soviet wool industry The Soviet Union was the second largest wool producing country in the world in 1990, producing around 471 000 tonnes (greasy) from a sheep population of 138.7 million. While wool production expanded at a steady rate during the 1960s and 1970s, production levelled off during the 1980s and since 1989 it is estimated to have declined.

Productivity in the region's wool industry is relatively low and costs of production are high and vary considerably between wool producing areas.

2 ABARE research report 92.9

By international standards wool consumption per person in the region is quite low. According to the International Wool Secretariat, consumption per person in the Soviet Union was 1.6 kg in 1987 compared with 2.5 kg in Norway and 2.1 kg in West Germany but only 0.5-0.8 kg in its Eastern European neighbours and 0.7 kg in the United States.

Wool consumption is low by world

standards

Although cotton is the main natural fibre used in the region, accounting for around 45 per cent of the mill consumption of textile fibres, the manufacture of synthetic fibres increased fourfold since 1970. Synthetic fibres now account for almost a quarter of the region's total textile fibre use, while wool's share has fluctuated between 7 and 8 per cent in recent years. Artificial fibres (such as rayon) and flax account for the remaining fibre use in the Commonwealth of Independent States.

Determinants of wool imports Historically, the main determinant of Soviet wool imports was the amount of convertible currency available for spending on wool and other imports after the more essential commitments such as debt service payments and imports of grains, feedstuff and machinery had been given priority. The availability of foreign exchange, in turn, was determined mainly by convertible currency loans and earnings from exports of oil, gas, coal, armaments, gold and other commodities.

The responsiveness of demand to changes in the average price of wool was low because the overriding determinants of the volume of Soviet wool imports were the availability of convertible currency and central planning decisions. Despite this relative lack of responsiveness at the aggregate level, the import shares of Australia, New Zealand, Argentina and

Cotton is the main natural fibre

consumed

. . . but consumption of

synthetics is now high

Soviet wool imports depended on

availability of foreign exchange

Responsiveness of wool imports to price

changes was low

Determinants of CIS wool imports

Uruguay changed to some degree depending on the relative prices of wool from these countries.

Soviet imports were Virtually all Soviet wool purchases from Australia, mainly greasy wool Argentina and Uruguay were of greasy wool,

although scoured coarse wool was purchased from New Zealand. The preference for greasy wool reflected previous investment in scouring mills (there are eighteen large scouring mills in the former Soviet Union) and the perception among Soviet importers that the cost of scouring wool in foreign countries was high. Hence, Australia, as the main world producer of greasy wool, became more dependent on the Soviet Union as a destination for its wool exports over the 1980s.

Pattern of wool With the collapse of the Soviet Union, the pattern imports is now of wool exports to the region has changed. Shortages changing of foreign exchange and disruptions to trading and

commercial establishments have been constraining imports. And access to credit has become an important determinant of imports. As market reforms are implemented in the region, demand for wool imports is expected to become more price responsive than in the past.

Foreign exchange The introduction of market determined exchange earnings will remain rates will reduce the importance of foreign exchange important earnings as a determinant of wool imports; however,

they will not be irrelevant. A reduction in foreign exchange earnings will still tend to lead to lower wool imports, because these lower earnings will tend to reduce the value of the currency, making imported wool more expensive and inducing a drop in imports.

Main conclusions of the analysis Current reforms will Reform of the political and economic structures of affect wool imports the former Soviet republics will have implications

for the volume of wool imported by the new states

4 ABARE research report 92.9

that formerly constituted the Soviet Union. Russia, being the largest republic in the former Soviet Union, has assumed the leading and coordinating role in the collective process of restructuring.

Although the process of transforming the economy of the former Soviet Union from centralised planning to a market oriented system has commenced, the final outcome of this process is very uncertain. In the current transition period, foreign exchange difficulties combined with low or negative rates of economic growth are likely to constrain the region's ability to import. In the short term, despite the provision of credit arrangements, the various states of the region are unlikely to resume purchases of significant volumes of wool. However, Australian wool exporters may be able to overcome some of the foreign exchange difficulties by using barter trading arrangements.

There are some reasons to believe that in the near future consumption of wool clothing could decline in the region and there could be a considerable contraction in the size of the wool industry in the republics. A smaller wool industry implies that the region is likely to remain a net importer of wool. And any reduction in agricultural support could lead to a shift in industry location and increased economic efficiency. Many less efficient wool producers would find their products too expensive for the market, especially those using imported and subsidised grain and feed concentrates.

In the short term, wool exports to the independent republics may have to be negotiated more directly with producers rather than with the foreign trade enterprises. There may also be a need to explore more innovative approaches to managing this increasingly complex market in the future. For example, clearing houses could be established to bring together exportable goods from the republics

Effects of reforms on wool imports remain unclear

. . . barter arrangements

may be required

The region's wool industry may be cut

back in future

Trading arrangements

with the region are changing

Determinants of CIS wool imports

Textiles industry is also likely to change

Market based economies are likely to import more wool in the longer term

Russia and the Ukraine are likely to remain big importers of wool

Other republics may be importers or exporters

for the purpose of assisting the local traders in arranging barter deals.

In the short to medium term, the textiles industry will be faced with the need to increase efficiency and respond to market forces rather than to planned targets. This process may be accompanied by closures of inefficient factories and competition from imported textiles and fibres. A demonopolisation of foreign trading organisations may lead to trading establishments in various republics being rather small, diversified, economically weak and dispersed.

In the longer term, reform of the economies of the countries emerging from the former Soviet Union is likely to lead to the eventual operation of a market economy. However, this process will proceed in an uneven way, with its scope and momentum uncertain. The resulting efficiency gains are likely to be reflected in higher economic growth within the region, and a consequent increase in world trade. These gains are also expected to result in an increase in the volume of wool imports.

The Russian Federation and the Ukraine will probably remain significant importers of wool from the other republics and/or from other countries. The Asian republics are likely to be net exporters of both cotton and wool. But the situation may vary between the Asian republics. Kazakhstan is likely to remain a net exporter of wheat and wool, while Tajikistan, Turkmenia, Uzbekistan and Kirghizia may become net importers of natural fibres.

The group of 'other republics' is quite diverse. These areas in aggregate would probably be net importers of wool and cotton. This group can be split into a northern area, consisting of the Baltic republics and Belorus, and the southern republics

ABARE research report 92.9

- Georgia, Moldova, Armenia and Azerbaijan. The Baltic republics may remain net importers of wool and cotton, and exporters of the clothing and textiles that incorporate those fibres. The southern republics may be approximately self-sufficient in natural fibres if their industries are structured to use their own raw fibre production.

This implies that the Australian wool exports to the Region is likely to region are likely to compete, in future, with exports be a large net from other republics. At the same time the region importer of wool as a whole is likely to be a large net importer of wool from the rest of the world. Capturing a share of this changed market will require a move away from traditional marketing methods with the region, which was previously coordinated by the single Soviet importing agency. Given the size of the market, the type of wool demanded and Australia's experience in a variety of different markets, Australia Australia likely to is likely to be in a good position to continue to be remain the main the main supplier of wool to this market. supplier

- -

Determinants of CIS wool imports

Introduction

The collapse of the Soviet Union and the formation of independent states have important impacts on the region's markets and the future character of economic relations among the former constituent members of the Soviet Union. The emergence of new independent states in place of the former Soviet republics is expected to be followed by a process of disintegration of the economic ties among the highly specialised integrated industries of the former Soviet Union.

Russia will continue to dominate the region's economy because of the size of its population (150 million of a total of 290 million) and its resource base. Nevertheless, the Ukraine will be an important economy, with its population of over 50 million people, large agricultural and energy resources, and large industrial sector. Most of the republics have already declared that they wish to institute democratic systems of government and market economies. However, it will take many years for efficient market systems to develop from the industrial structures that have been inherited because of the need to develop appropriate infrastructure.

Before the current restructuring the Soviet Union was a large and important market for Australian agricultural exports, of which wool was the largest component. In 1988-89 the Soviet Union was Australia's third largest market for greasy wool (after the European Community and Japan), importing 113 000 tonnes of wool valued at about $869 million. This represented over 14 per cent of Australian wool exports and 80 per cent of Soviet raw wool imports. After 1989 there was a sharp reduction in Soviet purchases of Australian wool. In part this can be attributed to the relatively high wool prices in the late 1980s, but the primary causes of the fall in Soviet imports were the shortages of hard currency and the adverse effects of the process of restructuring on production and consumption.

In this report the main focus is the determinants of demand for wool in the republics that previously formed the Soviet Union and the implications of this for imports of Australian wool. A difficulty in undertaking such a review is the extensive changes that have occurred as a result of the introduction of perestroika (restructuring) during the 1980s and the rapid pace of recent developments in the region.

8 ABARE research report 92.9

Background

Production of wool in the region In 1990 the Soviet Union was the second largest raw wool producing country after Australia, producing around 471 000 tonnes (greasy) from a sheep population of around 138.7 million (table 1). Significant production gains were achieved in the 1950s and 1960s as a result of Soviet policies to increase agricultural output. Sheep numbers nearly doubled from 74.8 million in 1950 to 145.4 million in 1975. During the 1980s sheep numbers fluctuated between 140 million and 145 million.

Despite a fall in sheep numbers in the late 1980s, wool production increased, reflecting an improvement in average fleece weights. In 1990, increased sheep slaughtering, in response to severe food shortages, reduced the size of the sheep flock. As a consequence, wool production is estimated to have been at least 5 per cent lower in 1991 than in 1990 (Commonwealth Secretariat 1991).

In the Soviet Union sheep were bred for both mutton and wool production. In recent years, resources in the agricultural sector were directed to higher priority activities such as grain and meat production. Food production was considered more important than wool production, and grain production received a higher priority for the better quality land. In the livestock industry, full housing of livestock is necessary for at least six months of the year because of the severe winter conditions in the region. During that time producers are largely dependent on locally grown fodder and grain. Livestock are heavy users of both domestically produced and imported grain, with around 50 per cent of the grain harvest being used as animal feed. Consequently, priority for resources was given to the more efficient feed converters such as poultry and pigs.

Sheep farming is carried out in all fifteen republics of the former Soviet Union but, for reasons of climate and tradition, it tends to be concentrated in certain areas. In particular, in 1989 two thirds of the sheep flock were located in two republics, the Russian Federation (43 per cent) and Kazakhstan (25 per cent) (table 2 and figures A and B).

Determinants of CIS wool imports 9

Sheep numbers, wool production and wool cut per head in the Soviet 1 union

Sheep numbers Wool production Wool cut per head million kt greasy kg

1980 143.5 1981 141.6 1982 142.4 1983 142.2 1984 145.3 1985 142.9 1986 140.8 1987 142.2 1988 140.8 1989 140.7 1990 138.7

Source: Commonwealth Secretariat (1991).

2 Distribution of sheep population, by republic

Russian Federation Belorus

million million

Ukraine Trans- and Baltic caucasian

Moldova republics republics Kazakhstan

million million million million

Other central

republics Total

million million

Source: International Wool Secretariat (1990). - - --

ABARE research report 92.9

Determinants of CIS wool imports 11

Distribution of Soviet wool production and the sheep flock in 1988, by republic

Wool production 478 000 tonnes

Sheep distribution ~ A B A R E 141 million

zbekistan 6%

Kazakhstan 23% Kazakhstan 25%

1 Source: Commonwealth Secretariat (1991); Newsletter for RSEEA (1990). 1

Farms in the republics were of two main types - state farms (sovhozy) and collective farms (kolhozy). However, private plots held by state and collective farm workers accounted for an increasing share of agricultural production in the 1980s. In 1989, state and collective farms held 112 million sheep, around 79 per cent of the total sheep population. State and collective farms were operated like industrial factories, with farm inputs and outputs being determined largely by a system of plan directives.

The intensive use of labour and the extensive practice of grain and fodder feeding, combined with low yields and low wool production per head, means that wool growing is a relatively costly activity. Sheep grazing is extensive and shepherds are deployed to tend flocks of around 600-800 sheep. Despite the introduction of shearing machines, hand shearing is still carried out where flocks are small. These management practices mean there is a relatively high demand for labour on most sheep farms.

The sheep flock has been gradually converted to merino types which now account for around 65 per cent of the total compared with 38 per cent in 1959. The four main merino breeds used are the Caucasian fine fleece merino, the Stavropol merino (producing wool of 19-21 micron), the Groozney merino (which was bred from the Australian merino) and the Soviet merino.

Despite breeding programs to improve the quality of sheep, wool production per head is quite low. In 1990, for example, wool cut per head was 3.5 kg compared with an average cut per head in Australia of 4.7 kg. These

12 ABARE research report 92.9

differences can be attributed to breed types and inadequate nutrition, as well as different management practices in the two countries.

Soviet sheep management practices, involving a combination of extensive grazing and housing, also tend to result in greater contamination by vegetable matter, dust, stains and dung. Consequently, compared with corresponding wool types in the major wool producing countries, Soviet fleece wools generally had lower yields when converted from greasy to clean form. For example, while average Soviet clean yields are believed to have remained at around 45 per cent for many years, Australian clean yields have risen, from 59 per cent in 1969-70 to 66 per cent in 1989-90.

Wool textile industry During the 1950s and 1960s there was a rapid expansion in investment in the Soviet textile processing industry. Old mills were reconstructed and modernised, with emphasis on high productivity spindles and looms. Mills were established near the source of the raw material, resulting in a shift in location away from areas close to market outlets, such as Moscow. For example, new cotton mills were established in the cotton growing areas of the Central Asian region and Kazakhstan. The latter republic, a major wool growing area, also developed an important wool textile processing industry. When choosing mill location, consideration was also given to employment creation, especially in the large industrialised regions where unemployment among women was a source of social tension.

Although cotton remains the most widely used fibre in the region's textile industry, the most significant development has been the growth in production of synthetic fibres, particularly polyester fibre. Since the early 1970s the production of synthetic fibres has increased nearly fourfold. The use of synthetic fibres also increased as a proportion of total mill consumption, from 15 per cent in 1980 to 23 per cent in 1989. It appears that the increase in the use of synthetics occurred partly at the expense of flax and artificial fibres (cellulosics). Mill consumption of wool declined from 8 per cent in 1983 to 7.2 per cent in 1988. However, in 1989, wool's share of mill consumption increased to 8.2 per cent as a result of a sharp decline in the use of cotton.

Soviet production of wool and wool-type yarns totalled 435 000 tonnes in 1989, 5 per cent below the 1980 peak, while production of wool fabrics totalled 712 million square metres, around 7 per cent below the 1988 peak

Determinants of CIS wool imports 13

(table 3). Production of both yarns and fabrics was the lowest in 1985, at 421 000 tonnes and 666 million square metre respectively.

By international standards the former Soviet Union had a large textile processing industry, ranking third in the world in textile fibre production. Soviet textile mills' total fibre use was a little over 4 million tonnes in 1989 (table 4), somewhat below the peak of nearly 4.5 million tonnes in the previous year but close to the level in 1980.

Although the Soviet Union was a large textile producer, the quality of finished textile products was poor compared with that of countries with market economies. This poor quality resulted from outdated textile technology, a lack of incentives for the textile industry to improve the quality of its products and limited competition from high quality imported textile products because of the operations of the foreign trading system. Supply constraints in the textile industry limited the quantity of products available to consumers. And, as a result of the production constraints and price setting for consumer goods, there was chronic excess demand for consumer goods.

In January 1992 most prices were partially freed in Russia, the Ukraine and Belorus and some other republics. Hence, producers were able to sell almost all their goods to consumers at a market price, even if the goods

3 Wool textile activity in the Soviet Union

Wool and wool-type yarn production

Wool and wool-type fabric production

million m2

Source: International Wool Secretariat (1990a)

14 ABARE research report 92.9

4 Estimated Soviet mill consumption of textile fibres

Wool Cotton Artificial

Flax fibres Synthetic

fibres Total

-

Source: International Wool Secretariat (1990a).

were of low quality. With the partial liberalisation of pricing, the prices of goods are expected to reflect more closely the prevailing costs of production and market conditions. But, so far, this price liberalisation has not been accompanied by other necessary reform measures, such as the removal of monopolies over the supply of goods, allowing greater competition from imports and so on. More detailed analysis of the reform process and its impact on wool demand is provided in chapters 3 and 4.

Consumption of wool In 1987 consumption of wool in the Soviet Union was around 1.6 kg per person (table 5). As in other countries, income and relative prices are likely to be important factors influencing the consumption of textiles. The difference in consumption between countries is likely to reflect price and income differences as well as the availability of a greater range and higher quality of wool textile fabrics in developed market economies. It may also reflect life style differences and traditional patterns of fibre use. Wool consumption per person in the Soviet Union was lower than in West Germany and Norway which experience a similar winter climate to the European part of the Soviet Union, but was higher than that of most central European countries (table 5).

Clothing and other items produced from synthetic fibres are likely to be the main competitors for wool products. However, the extent to which

Determinants of CIS wool imports 15

5 Per person consumption of apparel fibres in selected countries

United States Finland Sweden Norway Germany, FR Soviet Union Poland Czechoslovakia Germany, DR Hungary

Wool Synthetics Artificial Cotton

1974 1987 kg kg

Total

1974 1987 kg kg

Source: Food and Agriculture Organization of the United Nations (1989).

synthetic fibres can be substituted for wool is not clear since, because the climate is severe, wool is regarded as an essential fibre for Soviet clothing. The better quality synthetic fibres including newly developed microfibres are expensive to produce and require technology and chemical inputs which are not yet available to the republics' textile industry. This is reflected in the Soviet Union's relatively low consumption of synthetic fibres, compared with levels in the major developed economies. In 1987, Soviet consumption of synthetics was only 3.6 kg per person, less than half that of other European countries, including Central Europe (table 5). Since the early 1970s, the production of synthetic fibres in the Soviet Union has increased nearly fourfold, resulting in per person consumption more than doubling between 1974 and 1987. In the late 1980s, the Soviet Union continued to increase its plant capacity to produce synthetic fibres.

A final point worth making about Soviet consumption of fibres is that the price of wool garments was quite high relative to average wages. According to Soviet data (Foreign Broadcast Information Service 1990), the cost of most wool garments was equivalent to at least one month's wages for the average worker (table 6). For example, in 1988, winter overcoats cost 166 roubles, representing 116 per cent of the average monthly per person income for all families. This relatively high cost of winter clothing is probably related to the extreme shortages of these items in Soviet stores, as referred to earlier, as well as high taxes imposed on textiles and garments.

16 ABARE research report 92.9

6 Prices of wool garments in the Soviet Union and their share of family income

Overcoats and short coats Winter coats Spring or autumn coats

Womens coats Winter coats Spring or autumn coats

Mens suits Mens trousers Knitted wool garments

roubles roubles

Share of monthly per person family

income (1988) a

a Total monthly income per family member of blue collar and white collar workers (the average number of workers per family is 1.7). Source: Foreign Broadcast Information Service (1990).

Trade in wool and wool products Although the Soviet Union was a large producer of wool, its production was insufficient to meet domestic requirements and so it was a significant net importer of wool. In 1989 the Soviet Union imported 124 000 tonnes (clean wool equivalent) of raw wool, around a third of its wool textile mill requirements (figure C). Soviet imports represented approximately 10 per cent of world wool trade in that year. In the same year, the Soviet Union exported around 14 600 tonnes of wool, consisting mainly of the coarser types. Over time the main destinations of Soviet exports were Western European countries but the volumes fluctuated significantly.

While there was a 50 per cent increase in the volume of Soviet wool imports during the 1970s, imports levelled off during the 1980s, even declining in some years. For example, in 1984, there was a sharp fall, followed by a subsequent recovery in import demand. In 1990 the Soviet Union again substantially reduced imports of raw wool.

Constraints on the availability of wool products have been an important factor limiting consumption, even though income and price are important determinants of demand for wool products. Apart from domestic production of wool and wool products being planned, under the centrally planned

Determinants of CIS wool imports 17

1 C The Soviet wool industry

2 kt

clean , , , , , ,

1!9i0 ' 1&5 1980 1985 19$0 Source: International Wool Secretariat (1990a).

system the quantity of imports purchased was also planned and the necessary foreign exchange made available accordingly. This is not to say that price had no influence on Soviet buying patterns, since the main aim of the Soviet importing establishment was to buy wool at the most opportune moment and at the lowest possible price. However, the effect of price on Soviet demand was limited by the operation of the plan.

Most Soviet imports of wool were written in convertible currencies (mainly US dollars) and transacted in cash rather than credit. The rouble could not be freely converted into foreign currencies, so the availability of convertible currency was an important determinant of wool imports. The availability of convertible currency for wool purchases generally depended both on the total level of currency available and on the amount of convertible currency that was spent on debt repayment and imports that took priority over wool, such as machinery and grains.

The availability of convertible currency depended on earnings from exports and the scope for increasing debt or foreign reserves. Soviet export earnings from oil and gas were particularly important. During the 1970s and early 1980s, the value of exports of oil and gas rose significantly, providing foreign exchange for imports of wool and other commodities (figure D). However, Soviet energy exports fell after 1984, contributing to a worsening of the current account problem. The production of oil declined by 9 per cent in 1990 and is estimated to have fallen further in 1991, resulting in a decline in export availability and a resultant fall in export revenue.

18 ABARE research report 92.9

Selling gold was another way the Soviet Union improved its current account position and afforded increased merchandise imports or debt repayment. Sales of gold from non-market countries (principally the Soviet Union) rose from 210 tonnes in 1985 to 450 tonnes in 1990. In 1990, this represented 17 per cent of total world supply. However, production and sales of gold from the region are projected to fall in the next few years as some high cost mines are closed and stocks are now thought to be low (Cairns, Dermody and Huggan 1991).

The Soviet Union's foreign debt in convertible currencies was also an important determinant of its ability to import merchandise. An increase in the Soviet Union's foreign borrowing increased its ability to import

Energy exports (US$b)

rain imports (kt)

I 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1

1971 1974 1977 1980 1983 1986 1989

Source: Economic Commission for Europe (1990); FA0 (1990); International Wool Secretariat (l990a).

merchandise, provided that the increase reflected new loans and not increases in debt servicing charges. However, that debt escalated over the years and the republics of the former Soviet Union are currently experiencing difficulties in making repayments.

Soviet gross foreign debt in convertible currencies rose from US$31.4 billion in 1985 to US$50.6 billion in 1989 (Economic Commission for Europe 1990). It is estimated to have totalled US$65 billion in 1991, with more than US$5 billion in arrears in trade credits to Western companies (Fidler 1991). Debt in 1992 is forecast to total US$84 billion; but the composition of this debt is difficult to establish. This high level of foreign debt has resulted in debt servicing payments that are high relative to export returns in convertible currencies, constraining merchandise imports.

The ability of the newly independent states to increase merchandise imports by reducing their foreign exchange reserves is expected to be low in the foreseeable future because their total foreign exchange reserves are already low (International Monetary Fund 1990).

As mentioned earlier, the second factor affecting the availability of convertible currency for wool purchases was the amount of currency allocated for imports of other goods. Under the centrally planned system, foreign exchange for wool imports was allocated after the requirements of priority imports such as machinery, grain, meat and other foods had been met. It appears that the same set of priorities has been continued by the Russian government in 1992 and hard currency expenditure will be limited to imports of food, equipment and replacement parts for strategic export industries such as oil and gas, and debt repayments scheduled according to the G-7 (group of 7 large industrialised countries) and International Monetary Fund program (Boulton 1992).

Currently in Russia, imports of grain are considered essential to meet the basic food and animal feed requirements of the populace. Given the recent virtual collapse of the consumer market in the newly independent states, even more emphasis has probably been given to imports of grain and other food items than to wool. Imports of machinery from the West are also important as they are required to upgrade the technological capacity of industry (Economic Commission for Europe 1987, pp. 302-3).

The disbanding of the Soviet Central Planning Committee and the State Price Authority, however, has not removed the instruments and methods

20 ABARE research report 92.9

characteristic of central planning. Central controls over imports have been preserved and the banking sector has assumed these controls by selectively approving foreign exchange payments. Import approvals include indications of the countries from which the goods should be sourced, the quantity and quality of the goods, the timing of deliveries, payment arrangements and other essential elements of commercial transactions.

While the price of the product to be imported will influence some of these decisions, the main point here is that economic criteria related to price advantages were not the only and most important criteria of a decision to import. For example, in a model of Soviet wool demand developed by ABARE (see appendix B) it was estimated that the price elasticity of Soviet demand for imported wool from all sources was -0.1. This means that for the period over which the model was estimated (1970-71 to 1989- 90) a 10 per cent fall in the price of wool would have resulted in a rise of only 1 per cent in the quantity of imported wool demanded by the Soviet Union. In comparison, the elasticity of Japanese demand for imported wool has been estimated at around -0.62 (Connolly, Wittwer and Roper 1992). This is not to say that the decision about the country of orgin of imports is unresponsive to prices, but rather that the overall quantity of wool imports is relatively unresponsive to price changes. As discussed later, once the quantity of imports has been determined, prices become more important in selecting the source country for the imports.

In the early 1990s, Soviet expenditure on imports of Australian wool appears to have been driven by the level of the credit guarantee provided by the Australian government. In late 1990 the Australian government decided to help boost commodity exports to the Soviet Union by providing credit facilities ($A400 million) to purchase Australian wool and some other commodities. Soviet importers appeared to use part of this facility to substitute funds to cover outstanding payments for wool previously purchased from Australia, and also used the facility to buy more wool.

The facility is of a rollover type (revolving credit) in the sense that the credit can be paid back and then reused for further purchases. If the credit facility is being used to its limit [in fact, most but not all of the available credit was used] and no additional funds from other sources are used, the quantity of wool that can be imported is simply the value of expenditure (that is, the credit available) divided by the price. In this case, a fall in price would lead to an equal percentage rise in quantity imported. However, once the credit facility becomes exhausted and the republics

Determinants of CIS wool imports 21

stop purchasing wool, the demand from these republics becomes unresponsive to changes in the Australian wool price.

With the collapse of the Soviet Union the Australian credit guarantee facility was no longer binding on the independent republics. In January 1992 the Russian Federation, which claimed to accept some of the former Soviet Union's international legal obligations, failed to service the credit guaranteed by the Australian government, thus precluding any future wool contracting under this facility.

In the future, structural changes in the region that was the Soviet Union imply that import demand is likely to be considerably more responsive to prices than it was in the past, once a market system is working. This is analysed in chapter 4.

Shares of the Soviet wool import market Important to Australia is not only the allocation of the republics' scarce foreign exchange to total wool imports, but the allocation of wool imports between countries. Given that there was only limited scope for influencing total Soviet wool imports in the past, the factors that enabled Australia to influence its share of these imports were critical.

During the 1980s the Soviet Union emerged as Australia's second largest market. In 1988-89 it accounted for around 14 per cent of total Australian wool exports. Between 1969-70 and 1988-89 Australia's wool exports to the Soviet Union increased from 23 900 tonnes to 73 700 tonnes (clean equivalent). Over the period, Australia's share of total Soviet wool imports increased from 30 per cent to almost 60 per cent (figure E).

The share of wool imports from Uruguay and New Zealand also increased over the period. Most of the increase in share by Australia, New Zealand and Uruguay occurred during the 1970s during which time the Soviet Union reduced the proportion of its wool imports from smaller exporters, such as Mongolia, Syria and Afghanistan. In 1988-89, these smaller exporting countries accounted for only 13 per cent of total Soviet imports, well down from their 41 per cent share in 1969-70. Wool imports from Argentina, another significant exporter, declined from the mid-1980s. However, in 1990 the Soviet Union increased its purchases from Argentina when the price of Argentine wool was relatively low.

-

ABARE research report 92.9

Soviet wool imports, by source I J

1969-70 1989-90 ~ A B A A E 83 000 tonnes (actual) 59 000 tonnes (actual)

Argentina 11% 19% Source: International Wool Secretanat (1990)

Part of the reason for the growth of Australian wool exports to the Soviet Union may have been a preference for imports of the finer greasy wools suitable for the Soviet textile industry. Sufficient quantities of such wool to meet the import needs of the Soviet Union were produced only in Australia. The proportion of wool exported from Argentina in greasy form declined substantially in the 1970s and 1980s as wool processing expanded in that country. In contrast, Australia has not developed its early stage processing to nearly the same degree as the other main exporters. In the late 1980s, just under 24 per cent of Australia's shorn wool clip was scoured or further processed before export (Department of Primary Industries and Energy 1989). Similarly, Uruguay exports a higher proportion of its wool in greasy form than Argentina, although over half of Uruguay's exports are now at least early stage processed.

The Soviet preference for purchasing wool in greasy form may have reflected the necessity for hard currency 'savings'. However, in the future this preference may change with the increased recognition of the environmental problems with wool scouring effluent. Already, one of the Soviet's eighteen large wool scouring mills uses solvent scouring technology and does not produce aqueous effluent, but many of the others lack efficient sewage cleaning facilities.

Soviet wool imports were mostly of semifine (less than 25 micron) and medium (26-34 microns) types. In 1988, imports of these types accounted for 72 per cent and 22 per cent respectively of total Soviet wool imports (International Wool Secretariat 1990a). Soviet purchases from Australia

Determinants of CIS wool imports 23

were generally of medium merino or fine crossbred wool, of 22-28 microns. This wool is often substantially cheaper than the average price of Australian wool.

The Soviet Union also bought apparel wool from Argentina. And small amounts of carpet wool were purchased from Argentina between 1970-71 and 1977-78. From New Zealand, the Soviet Union purchased a mixture of greasy and scoured wool (but with the majority being greasy) and a roughly even amount of carpet and non-carpet wool. The mix of wool types purchased from New Zealand varied substantially over the 1970s and 1980s. In some years, however, the Soviet Union bought wool finer than 28 microns from New Zealand.

As indicated earlier, Soviet imports of wool historically were influenced strongly by the central planning authorities. Apart from general trade issues, central planners' considerations included relations between the Soviet Union and other countries, the availability of advantageous credits and existing clearing and/or barter arrangements. For example, imports of sugar from Cuba were made at high prices, with the aim of assisting that country's economy. Another example is that the Soviet Union had no economic relations with South Africa and did not purchase wool from that country. Nevertheless, the relative prices of Australian, New Zealand, Argentine and Uruguayan wool were important in determining each of these countries' shares of wool exports to the former Soviet Union.

Relative prices of wool produced in different countries are expected to remain important determinants of the shares of each of the main exporters, but some changes in responsiveness to price changes are likely to occur. This change in the response is likely to make policy analysis of the wool market more difficult until more information about purchasing by the new states is obtained.

24 ABARE research report 92.9

Restructuring the former republics of the Soviet Union

Major changes at the political as well as the macroeconomic and microeconomic levels are occurring to the underlying structures of the formerly centrally planned economic system of the region that was the Soviet Union. The region's production and consumption of wool and textiles are likely to be affected by a different set of factors from those of the past. The reforms cannot take place overnight and there is likely to be short to medium term disruption in the performance of the economy as a result of the adjustment of output, closures of inefficient operations and a reduction in demand. In this chapter, the nature of the changes is considered in broad terms to provide a perspective of events in the region. The impact of these changes on the wool industry is considered in more detail in the next chapter.

Nature of current changes Over a considerable period of time the standard of living in the Soviet Union was falling. After 1965 there was a long term decline in the rate of growth in real net material product (approximately equivalent to gross national product) albeit from very high levels (figure F). As well, national income per person declined gradually (Fink 1985; International Monetary Fund 1990). This was reflected in low productivity, declining domestic

F Average annual growth in Soviet real net material product

Determinants of CIS wool imports 25

demand and exports, unemployment and underemployment and dislocation of the population. The initial attempt undertaken between 1986 and 1988 at improving the economic performance initiated under perestroika (restructuring) by a 'traditional' way of increased investment and administrative measures failed. As the underlying problems required fundamental changes to the social and economic system, which were not pursued at that stage, the attempt at improving the economy only aggravated the existing problems and resulted in a substantially increased foreign debt, a crippling budget deficit and a further decline in income.

The adoption of glasnost and perestroika were aimed at eroding the traditional patterns of hierarchy and command and establishing new freedoms essential to the process of restructuring and developing a market system. However, achieving these objectives was slow, partly because implementing them was piecemeal rather than economywide. For example, farm production and textile processing remained state owned and managed. This slowed the pace of change and encouraged disquiet and a striving for independence among the republics, which eventually resulted in the dissolution of the Soviet Union.

There are now fundamental changes resulting from the disintegration of central planning - producer subsidies and the state procurement system are changing, the standard of living has been falling, a debt crisis is developing, inflation rates are high and the republics have become independent. These changes are discussed below.

Prices and quantities of both inputs and outputs in the Soviet Union were largely administratively determined. In an attempt to improve the management of production the administratively determined production targets were replaced with a system of state procurement quotas in 1986. Under this scheme a government agency entered into agreements with establishments for the delivery of a fixed quantity of a product. The aggregated quantities of the contracted products represented a new form of central plan, with the bulk of production being procured by the state under these quotas. The non-contracted production was intended to be sold freely at the market price.

Inefficient production of goods and inputs, combined with subsidisation of certain consumer goods (such as childrens clothing), resulted in market shortages. This contributed to rising inflation and a fall in the purchasing power of the rouble. The widespread use of US dollars as a hedge against

26 ABARE research report 92.9

the rouble's falling purchasing power further weakened the rouble. This process of rouble 'substitution', if allowed to continue, has the potential to undermine the rouble as a financial instrument of reform, thus making macroeconomic stability more difficult to achieve and also more expensive.

The practice of bartering between enterprises has become widespread. In an expectation of higher prices in future, producers hold back their products, creating very serious problems of supplying the large population centres with food and other necessities.

In 1991 the Soviet Union's budget deficit may have reached 20 per cent of gross domestic product (for more about market distortions see Portes and Winter 1980; Podkaminer 1982; and Davis and Charemza 1989). Overall, it appears that the incentives provided in the procurement system in the independent republics are unlikely to result in either an efficient use of resources or consumer requirements being met.

The accelerating inflation resulting from printing rouble notes to compensate for the drastic decline in Russian budget revenue further has disrupted the supply of goods. In January 1992 a corrective action in the form of price rises was instigated by the Russian Federation and was promptly followed by the other republics. This drastic price increase for food and other consumer necessities was implemented with no other policy measures in place designed to remove the fundamental economic imbalances that currently prevent supply response in the economy. If no further measures are undertaken, this price increase is likely to contribute to an aggravation of social tensions and may result in further inflation.

Debt problem Beginning in 1986 the Soviet government introduced a series of policy measures in an initial attempt to improve the efficiency of the existing system. The measures included expanding investment in manufacturing, which was based on imports purchased with credits, devolving import decisions to the republics, and decentralising foreign trade and banking. These changes were aimed at improving the system rather than reforming it. The decentralisation of decisions to import without sufficient incentives to repay credits resulted in an uncontrolled burst of imports using credit.

With other elements of the central planning system remaining intact and with shrinking economic output and mounting structural problems, the

Determinants of CIS wool imports 2 7

Soviet administration resorted to a policy of heavy foreign borrowing. Between 1985 and 1989 cumulative Soviet borrowings from major Western banks rose to US$20 billion. To meet net repayments, the Soviet Union exhausted virtually all its foreign exchange bank deposits and reserves. Although foreign banking was recentralised after some adverse experiences, there developed a widespread practice among exporters of withholding foreign exchange payments received for exports and of pursuing other means of avoiding the obligatory exchange of foreign currency earnings into roubles.

In 1990, net Soviet repayments of Western bank credits were US$6.2 billion. These net repayments were particularly high after the fourth quarter of 1990. Gross repayments were much greater but were offset, in part, by new bank credits guaranteed by Western governments. Much of this debt was short term, with about half due for repayment within one year. In 1991 the Soviet external financial position deteriorated further. The rapidly worsening internal situation and delays in meeting repayment obligations made Western commercial banks extremely reluctant to extend any further credit that was not secured by Western government guarantees.

Soviet debt in 1991 is estimated by the Bank for International Settlements to have exceeded US$60 billion but the exact amount is difficult to establish because of a combination of factors affecting the calculation. For example, the transition to a convertible currency in trade with former Council for Mutual Economic Assistance countries left some unspecified and unsettled claims on both sides to be paid in future, either in kind or in money, while a significant proportion of the Soviet sales on credit to developing countries may not be performing and will have to be converted to grants.

Because of increasing maintenance problems with installed oil producing equipment, oil production in what was the Soviet Union has been falling. Exports of energy, the main foreign exchange earner for the Soviet Union, fell in 1990 and were much lower in 1991 in spite of the then strong oil prices. This will further reduce Russia's ability to pay for imports.

The management of foreign exchange reserves has become critical in view of diminishing exports and demands from the republics for their share in foreign exchange export earnings. Implementation of an ad hoc order for delayed payment for imports has been a source of additional uncertainty for exporters.

28 ABARE research report 92.9

A proposed transfer of finance for the Soviet Union (known as the Marshal Plan for Eastern Europe) was not provided to the Gorbachev Soviet government by industrialised countries, as this was not seen as encouraging it to deal with its structural problems (Kristiansen 1991). There was a belief that if new credits were extended this might be spent largely on consumption and could create a disincentive for addressing the restructuring problems still unsolved. It was thought that only a serious and concerted effort to restructure their economies and bring about macroeconomic balance could restore the import capability of the republics.

Nevertheless, problems arising from the republics' push for independence and the progressive disintegration of the Soviet economic structure persuaded the Russian government to apply for large quantities of food aid and a temporary moratorium on principal repayments from the industrialised countries. Russia, the Ukraine and some other republics applied for membership of the International Monetary Fund, where appropriate policy advice to the governments of the Commonwealth of Independent States is expected to be backed up by financial assistance from the Fund as well as from other sources.

Moreover, some credits or grants have been made by governments for political reasons (for example, the reunification of Germany, disarmament) rather than being commercial credits based on an assumption of secure future repayments. Such politically motivated credits (usually in the form of a government credit guarantee to a private bank that actually provides the finance) are repaid by the taxpayers of the creditor country (budget expense) in the case of default. The bad debt is usually written off or else remains unserviced, which can create a problem in future trade relations between the countries. For example, 50 per cent of the Polish debt owed to Western governments was recently written off (70 per cent of the debt owed to the government of the United States will be written off provided that the reform of the Polish economy continues).

The recent shifts in the power structure in the former Soviet Union make it difficult to establish which organ of administration of which republic might endorse such credit obligations and on whose behalf. The apportioning of credit repayment obligations is expected to be subject to negotiations among the independent republics in the Commonwealth of Independent States.

Determinants of CIS wool imports 29

Debt relief action was recently granted to Russia, for the period until 1993, by the major Western industrialised economies, known as the G7 countries (the United States, Britain, France, Germany, Italy, Japan and Canada). It was designed to help prevent the potential collapse of law and order in the region and the possible grave consequences for economic stability in the rest of the world.

Independence of the republics With the decline of Soviet central planning and the weakening of central authority, the institutions that formerly directed production, trade and finance have been exposed to considerable change and uncertainty. The functioning of these institutions has been impaired and the risks of trading with the region have increased greatly. In particular, there is considerable uncertainty about the nature of the regimes that may develop in the future.

Hanson in August 1991, in considering the extreme uncertainty of the Soviet economic future, indicated a range of possible outcomes:

- severe fragmentation, not just into republics but also into regions and independent cities;

- benign fragmentation into republics with informal cooperation;

- re-establishment of central control with a resurgence of Marxism;

- privatisation in the hands of authoritarian leaders; and

- a confederation of democratic republics with development of market economies. (Hanson 199 1)

The likelihood of the re-establishment of central controls in the form experienced prior to 'perestroika' appears to be relatively low following the failure of the August 1991 coup. However, with a very limited experience of the democratic system and an almost complete absence of the institutional framework necessary for instituting a market oriented economy in Russia and in other republics, it is conceivable that an authoritarian form of government may emerge. Such republican governments are likely to be burdened with the task of restructuring their economies.

The newly signed Commonwealth treaty does not contain agreed solutions to many outstanding problems, leaving their solution for future negotiations.

30 ABARE research report 92.9

Such negotiations may need to determine the delegation of power to the central authorities (for example, to establish a joint military force or joint command, if this is desired) as well as to distribute assets and obligations. Among the obligations, the outstanding foreign debt repayment procedure will have to be regulated. The issues to be included in the treaty of Commonwealth of Independent States are potentially divisive and no early solution is likely. Under any of the above outcomes, the disintegration of the Soviet Union into a number of separate states implies higher costs for marketing wool and other products to a set of fragmented markets. But it may also open up a new range of opportunities for wool sales in the future.

Most of the republics have declared that they wish to institute democratic systems of government and market economies. However, it will take many years for efficient market systems to develop because of the inadequate industrial structures, the lack of understanding of market economies and poorly developed commercial infrastructure. A fundamental factor affecting the speed and path of the transformation process is efficiency of production at the microeconomic (firm) level. Under the centrally planned system, Soviet production establishments had virtually no discretion left for managerial decisions because the plan was used to determine all significant elements of production.

The nature and extent of future trade in agricultural and other products with the region will depend on a number of interrelated factors including the degree of economic independence and political autonomy of the separate states that are formed.

The new and evolving relations between the independent republics and the future Commonwealth authorities could create serious practical problems for foreign business. For example, it is not clear how economic power (such as control over banking, business regulations and payment systems) might be apportioned between the republics and the new Commonwealth. Similarly, it is not clear what the respective legal responsibilities and contractual capabilities of the republics would be and the extent of responsibility of commercial banks for the liabilities of the individual independent republics for repaying the existing foreign debt. The current situation contributes to instability and disruption in commercial contacts, payment difficulties and non-recognition of the republics' liabilities by the Soviet commercial bank.

Determinants of CIS wool imports 31

Conclusions

There is no single blueprint for reforming a formerly centrally planned economy. It is likely that, whatever measures are adopted, there will be significant adjustment costs as well as disruption to the economies of the independent republics over the medium term. The disintegration of the Soviet Union into independent republics is likely to bring about significant variations in economic performance and in the rate of transition toward more market oriented systems. A similar process of transition in the former centrally planned economies of Poland, Czechoslovakia and Hungary is expected to take many years. Some of their problems are similar to those of the former Soviet Union. However, unlike those East European countries, the former Soviet republics have little past experience of private ownership of land or small business to provide a reference point, so that the process of reform could well be even slower than in Eastern Europe.

32 ABARE research report 92.9

Wool demand and supply

The key policy reforms affecting the agricultural sector in the Soviet Union were initiated in March 1989. The focus of these reforms has been on establishing private property rights, legislation on land and leases, incentive structures and price and market reforms in all republics of the Union. Creation of the Commonwealth of Independent States and the current political and economic instability are likely to overshadow many of these reforms, but it may add a new impetus to individual republics' programs of transition to more market oriented economic systems. The impact of these changes on the wool industry and demand for wool products is analysed in this chapter.

Impacts of reforms on Soviet wool production Wool production represents only a relatively small component of the Soviet agricultural sector, accounting for around 2 per cent of the total value of agricultural output. The policy reforms initiated in March 1989 and continued since that time, although directed at the broader economy, have implications for the agricultural sector. Investment in the agro- industrial complex (agricultural production, agricultural inputs and food processing systems) was estimated to have increased by 5-10 per cent in 1990, compared with a 5 per cent decline for the economy as a whole (US Department of Agriculture 1990a). This reflected the Soviet strategy of increasing the agricultural capital base for production, processing and

I distribution. Subsidies to the agro-industrial complex were projected to increase further in 199 1. Consequently, the central government was continuing to address the problem of food shortages by attempting to increase production and processing through higher levels of investment.

Reforms initiated in March 1989 were focused on relaxing central control over food production and reducing the practice of income levelling between farms and farm workers. It was intended that the legislation on leasing land and property would lead to a restructuring of Soviet agriculture by increasing the number of small scale, family agricultural units. State and collective farms were given the ability to lease the land they controlled. However, many managers of these farms viewed leasing as a potential constraint on their authority (US Department of Agriculture 1990a). A

Determinants of CIS wool imports 33

further problem with leasing was the lack of machinery of a suitable size and the lack of support services for small scale agriculture.

In the short term the reform process is likely to have a serious impact on wool production. Between 1989 and 1990 wool production declined by 3 per cent mainly as a result of a fall in sheep numbers following increased slaughterings. This may be explained by the need to curtail some of the costs associated with sheep farming and a requirement for meat. Wool and mutton production compete for scarce resources, such as grain, with other end users (poultry, pig and dairy farms). Further, grain and other inputs were generally allocated first to the most efficient users - in the case of the livestock industry, pigs, poultry and dairy cows are more efficient than sheep as converters of feed into protein for human consumption. The expected shortage of foreign exchange is likely to reduce grain and meat imports in the short term. This could lead, in turn, to increased sheep slaughtering as a means of reducing dependence on feedgrains and of boosting domestic meat supplies.

The low protein content of Soviet feedgrains affects feed conversion rates. In the past, this led to an overuse of feedgrains simply to achieve minimum protein requirements. In future, measures directed at increasing the use of better quality feeds (for example, lupins and soybeans) could improve the use of available feedgrains in the medium term. There is also scope for reducing the losses associated with grain handling and distribution which are currently estimated to be 30-40 million tonnes a year. In the medium term, therefore, dependence of the independent republics on imports of certain types of grain may diminish. In the long term the increased availability and improved quality of feedgrains could result in gains in wool and mutton production per sheep.

In the longer term the move to a market oriented economy could lead to further adjustments in the wool industry, particularly in its size and location. A reduction in agricultural support, such as lower subsidies and the elimination of zone pricing, could lead to a shift in industry location and increased economic efficiency. There appears to be a wide disparity in average costs of wool production between republics. For example, in 1986 average costs ranged from R6156lt in Turkmenia to R16 551lt in Lithuania. In the two main wool producing republics, the Russian Federation and Kazakhstan, average costs were R9830/t and R7541/t respectively (US Department of Agriculture 1990a). Many less efficient wool producers would find their products too expensive for the market, especially those

34 ABARE research report 92.9

using imported and subsidised grain and feed concentrates. In these cases, a shift out of wool production could prove necessary. However, the governments of the republics are under strong pressure to raise prices of agricultural products and thus reduce their budget deficits. These price adjustments, if not supported by further market oriented measures, would only perpetuate market distortions in the republics.

Similarly, a move to make the rouble convertible could lead to changes in the exchange rate which could affect future domestic wool production, by varying the cost of production inputs such as grains. Exchange rate changes would also affect the demand for imported wool. For example, a large devaluation of the rouble against other currencies would increase the cost to Soviet buyers of imported wool and other products. It could also result in exports of some lower quality wools from Russia and imports of more suitable types from other countries.

Further, given the high cost of inputs required for wool production in the republics, if there were full convertibility of the currency and a move toward free market pricing, there could be a considerable contraction in the size of the wool industry in the republics, especially those producing low quality and expensive wools. This implies that the region is likely to remain a net importer of wool. A risk with this assessment is that if an agricultural policy goal of self-sufficiency were adopted by the republics then only moderate reductions in agricultural support may occur and, in these circumstances, imports of wool may remain low.

Price effects of implementing a market oriented system in the region As reforms of the economy progress and central planning is replaced with more market oriented systems, supply is likely to become more price responsive. With managerial freedom given to enterprises and the removal of plan targets and the subsidy system, the quantity of wool produced domestically should better reflect the natural endowment of the economies of the individual republics and the alternative opportunities available to producers. It would also mean that wool producers, textile manufacturers and trade organisations would have to become oriented toward customer demand rather than to fulfilling targets. In the past wool was imported by the Soviet Union in quantities indicated in the plan. In this sense planned domestic supply of wool was not sensitive to either domestic or international market prices. Consumer price subsidies further modified the retail price.

Determinants of CIS wool imports 35

If the import price was below the fixed price, taxes were used. As a result there was unfulfilled demand at the subsidised price. After purchasing products available to them, customers turned to other items, which were similarly in short supply for reasons discussed before.

There are some reasons to believe that consumption of wool clothing could decline in the republics in the future. Under the centrally planned system, supplies of wool clothing to the community were relatively liberal. With higher domestic prices, consumption of wool in the republics can be expected to fall but the degree of the contraction is difficult to estimate. At the extreme, domestic consumption may be reduced to a point of triggering net wool exports to the rest of the world.

The currently disintegrating system of planned supply and demand and the implications of changes to the system in terms of its effects on trade in wool is illustrated in a stylised fashion in appendix A.

Fibre substitution in processing and demand With the recently declining level of income per person in the region the structure of the textile market should not be compared directly with those in developed market economies. In the case of textile supplies, the 'basic comes first' principle appears to apply. These 'basic' textile needs tend to be satisfied by a lower quality of textiles, consisting mainly of cheaper blends of manufactured fibres and natural fibres. This wool market 'niche' is likely to continue to provide opportunities for Australian wool exporters in the future. Direct contact with textile producers would facilitate the pursuit of such market strategies.

Reduced subsidies are expected to change the structure of consumer spending. For consumers, lower subsidies will result in higher prices of virtually all necessities. Expenditure on housing, transport, health care, education and other services will increase substantially as the state welfare system contracts. In view of declining economic activity and generally lower incomes and possibly declining domestic inputs, the textile factories and their associations may need to reduce imported inputs of wool and other components. One short term option could be to reduce the proportion of natural fibres used in textile production. However, bearing in mind the severe climatic conditions prevailing in much of the Soviet Union during winter, this measure may be only a temporary expedient. Currently, the textile industry does not have the technology required to produce new

36 ABARE research report 92.9

G Shares of fibres consumed in the Soviet Union EABARE

19'80 1981 19'82 19'83 19'84 19'85 1986 19'87 19'88 1989 Source:International Wool Secretariat (1990).

generation, high quality artificial fibres, which might substitute for natural fibres at competitive prices. These high quality artificial fibres and fabrics, used mainly for sportswear such as ski outfits, are expensive even in the developed economies which have the technology.

The share of artificial manufactured fibres in total fibre consumed in the Soviet Union increased slightly during the 1980s at the expense of cotton and wool (figure G). The share of wool in the total fibre use declined slightly from 9.7 per cent in 1983 to 7.7 per cent in 1988. This is in contrast to a general return by consumers in the developed countries to natural fibres after the extensive market inroads made by manufactured fibres in the 1960s and 1970s. For example, in the United States there was

Shares of fibres consumed in the United States

Lsource: US Department of Agriculture (1991); Textile Organon, January 1984 and March 1980.

Determinants of CIS wool imports 3 7

a return to cotton starting in the early 1980s (figure H). Consumption of natural fibres in the Soviet Union (and wool in particular) was significantly higher than in the United States. This reflects abundant production capacity in the republics for natural fibres, but insufficient production capacity and raw materials (for example, cellulosis) for manufactured fibres competing with wool.