derivatives notice - comments matrix · pdf filederivatives notice - comments matrix ......

TRANSCRIPT

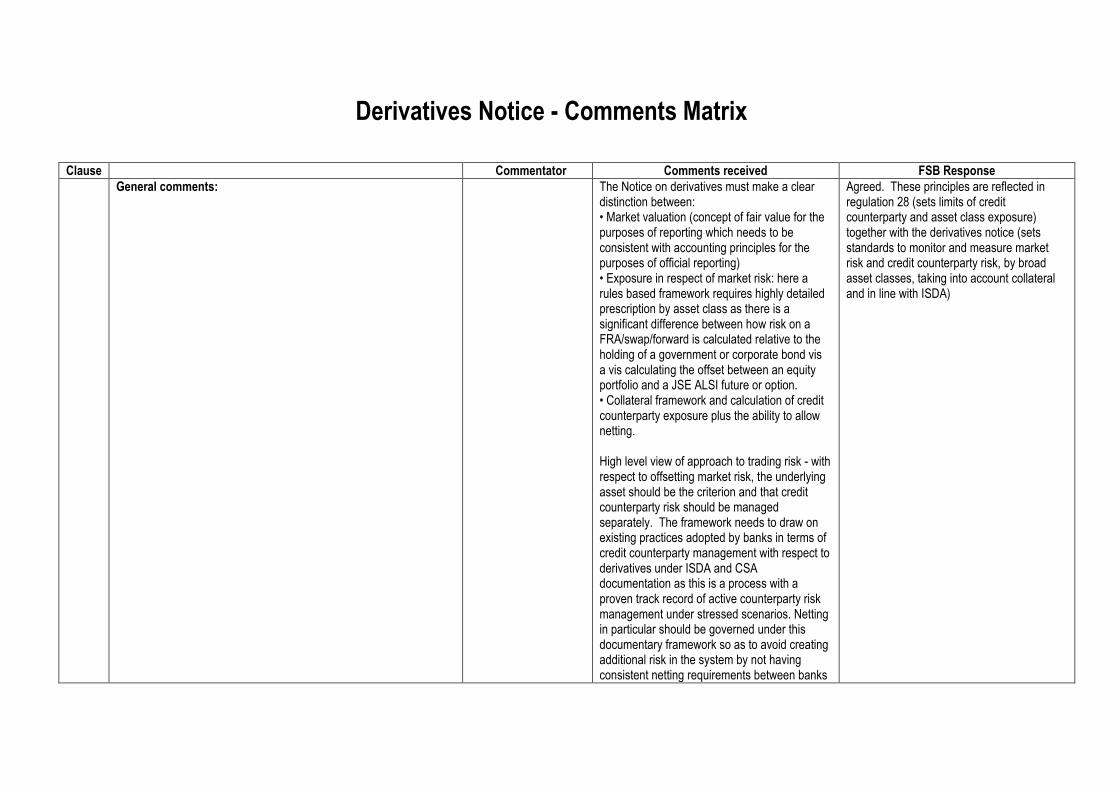

Derivatives Notice - Comments Matrix

Clause Commentator Comments received FSB Response

General comments:

The Notice on derivatives must make a clear distinction between: • Market valuation (concept of fair value for the purposes of reporting which needs to be consistent with accounting principles for the purposes of official reporting) • Exposure in respect of market risk: here a rules based framework requires highly detailed prescription by asset class as there is a significant difference between how risk on a FRA/swap/forward is calculated relative to the holding of a government or corporate bond vis a vis calculating the offset between an equity portfolio and a JSE ALSI future or option. • Collateral framework and calculation of credit counterparty exposure plus the ability to allow netting. High level view of approach to trading risk - with respect to offsetting market risk, the underlying asset should be the criterion and that credit counterparty risk should be managed separately. The framework needs to draw on existing practices adopted by banks in terms of credit counterparty management with respect to derivatives under ISDA and CSA documentation as this is a process with a proven track record of active counterparty risk management under stressed scenarios. Netting in particular should be governed under this documentary framework so as to avoid creating additional risk in the system by not having consistent netting requirements between banks

Agreed. These principles are reflected in regulation 28 (sets limits of credit counterparty and asset class exposure) together with the derivatives notice (sets standards to monitor and measure market risk and credit counterparty risk, by broad asset classes, taking into account collateral and in line with ISDA)

and non-banks. Furthermore, non-banks through hedge fund activities are already drawn into this process through Prime Broking Platforms where the method of calculating exposure as well as the acceptable securities and their haircuts are both well-defined and also have a proven track record through financial markets in turmoil Is this Notice intended to be retrospectively effective?

General Comments: Pension funds must comply with at least three sets of regulation and must apply a different valuation to a derivative instrument in terms of each, as below::

a. Reg 28 – effective economic exposure;

b. Accounting rules – fair value; and

c. Exchange Control – inward listing rules – full notional amount.

Surely, consideration should be given to harmonisation?

Long-term insurers issuing certificates in terms of non-linked policies: when will the final guidance be issued? In the interim, how should pension funds classify and report on non-linked policies, i.e. should they 1) show it as a separate asset indicating that the certificate still needs to be issued by the insurer or with a certificate issued from the asset manager or 2) should they show it under ―other assets‖ with a note describing the investment?

In view of the number of comments on this draft of the Notice and the amount of clarity needed we request that a further draft of the

It is not intended that the board notice be implemented retrospectively The comment is noted, but these rules are each designed for different purposes and the valuation methods reflect that. We are however in discussion with the Reserve Bank to see if harmonisation may be possible over time.

Notice on guaranteed policies was issued by the Long-term Insurance department

Due to the extent of comments received the draft notice was reissued for comment

Notice be circulated for comment.

In its comment on the previous Draft Notice, ASISA members made several proposals to ensure that the Conditions appropriately take the use of interest rate derivatives into account. This Draft Notice appears as having been structured mainly with equity derivative instruments in mind. It is proposed in these comments that the definition of reference assets be appropriately amended to provide for interest rate derivatives. References to Table 1 should be avoided as interest rates which are referenced by derivative instruments cannot be classified as ―assets‖ as defined in Table 1. ASISA members are of the view that the application of definitions from the Collective Investment Schemes Control Act is not appropriate in a pension fund context. Pension funds make extensive use of structured products, i.e. unlisted derivative instruments structured specifically for the hedging needs of a pension fund. To preclude pension funds from using these kinds of instruments, will severely hamper the fund‘s ability to protect the returns of the fund‘s investment portfolio and will ultimately have a negative effect on the value of the members‘ pensions.

Interest rate derivatives: Noted and accommodated, definition of reference asset amended Proposed redrafting addresses distinction between debt instruments held as assets and the risks associated with those assets in particular interest rate and the hedging of that risk Noted, see revised wording in section 2(1)(b)

Effective date of the Notice This Notice takes effect on 1 January 2012 six months from the date of publication of the Notice. The reference to 1 January 2012 creates the impression that the Conditions for the Use of Derivative Instruments shall apply

Agreed

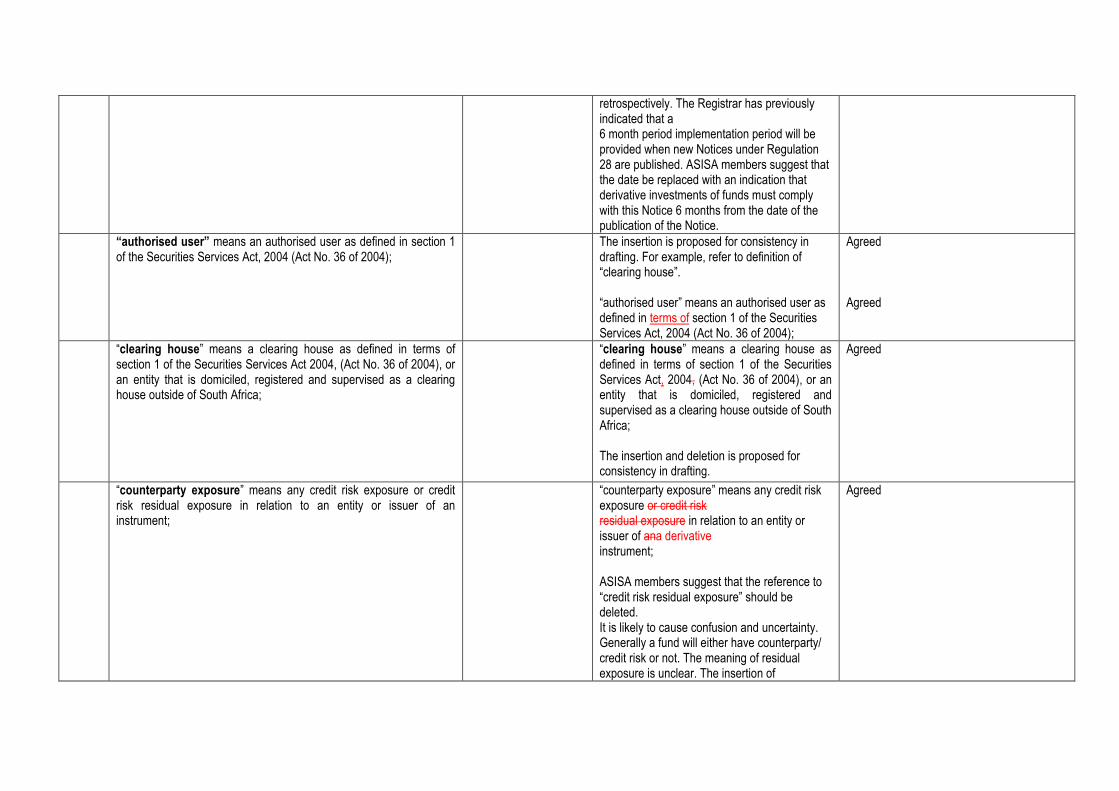

retrospectively. The Registrar has previously indicated that a 6 month period implementation period will be provided when new Notices under Regulation 28 are published. ASISA members suggest that the date be replaced with an indication that derivative investments of funds must comply with this Notice 6 months from the date of the publication of the Notice.

“authorised user” means an authorised user as defined in section 1 of the Securities Services Act, 2004 (Act No. 36 of 2004);

The insertion is proposed for consistency in drafting. For example, refer to definition of ―clearing house‖. ―authorised user‖ means an authorised user as defined in terms of section 1 of the Securities Services Act, 2004 (Act No. 36 of 2004);

Agreed Agreed

―clearing house‖ means a clearing house as defined in terms of section 1 of the Securities Services Act 2004, (Act No. 36 of 2004), or an entity that is domiciled, registered and supervised as a clearing house outside of South Africa;

―clearing house‖ means a clearing house as defined in terms of section 1 of the Securities Services Act, 2004, (Act No. 36 of 2004), or an entity that is domiciled, registered and supervised as a clearing house outside of South Africa; The insertion and deletion is proposed for consistency in drafting.

Agreed

―counterparty exposure‖ means any credit risk exposure or credit risk residual exposure in relation to an entity or issuer of an instrument;

―counterparty exposure‖ means any credit risk exposure or credit risk residual exposure in relation to an entity or issuer of ana derivative instrument; ASISA members suggest that the reference to ―credit risk residual exposure‖ should be deleted. It is likely to cause confusion and uncertainty. Generally a fund will either have counterparty/ credit risk or not. The meaning of residual exposure is unclear. The insertion of

Agreed

―derivative‖ before ―instrument‖ is proposed for consistency in drafting.

―delta‖ means the ratio measuring the change in the price of the derivative instrument relative to the corresponding change in the price of the reference asset;

delta‖ means the ratio measuring the change in the price of the derivative instrument relative to the corresponding change in the price or value of the reference asset; The insertion is suggested to align with the wording used in the definition of ―derivative instruments‖ in the Securities Services Act.

Agreed

“derivative instrument” means any—

(a) listed financial instrument; or

(b) unlisted financial instrument,

that creates rights and obligations and that derives its value from the price or value, or the value of which may vary depending on a change in the price or value, of some other particular product or thing;

ABSA Capital

This definition, together with the definitions of ―listed‖ and ―unlisted‖ financial instruments represent a deviation from the definition of a ―derivative instrument‖ as defined in Regulation 28 (―Reg 28‖) and section 1 of the Securities Services Act (the ―SSA‖). However, the reason for deviating from this definition is not clear in the Notice as currently drafted, neither is the reasoning behind splitting listed financial instruments and unlisted financial instruments clear.

If the instruments named under ―unlisted financial instruments‖ are intended to be an exhaustive list, the following questions need to be cleared-up:

(i) does this mean that any derivative instrument as defined in Reg 28 and/or the SSA that is NOT a ―listed financial instrument‖ and is NOT named as an ―unlisted financial instrument‖ in terms of this Notice, is not a ―derivative instrument under this Notice, and is therefore not subject to this Notice?

(ii) If (i) above is the case, how would unlisted derivative instruments as defined in Reg 28 and/or the SSA, but not defined in this Notice be dealt with by a fund?

Agreed, delete as it is already defined in Regulation 28

(iii) If, however, the wording as currently drafted is intended to mean that any derivative instrument as defined in Reg 28 and/or the SSA that is NOT a ―listed financial instrument‖ or an ―unlisted financial instrument‖ in terms of this Notice is NOT allowed to be entered into by a fund. The anomalous result would be that many OTC/unlisted derivative instruments as defined in Reg 28 and/or the SSA, but not listed in this Notice that are currently legitimately used by funds, would no longer be permitted. Examples of such OTC/unlisted financial instruments that are currently legitimately utilised by retirement funds would include:

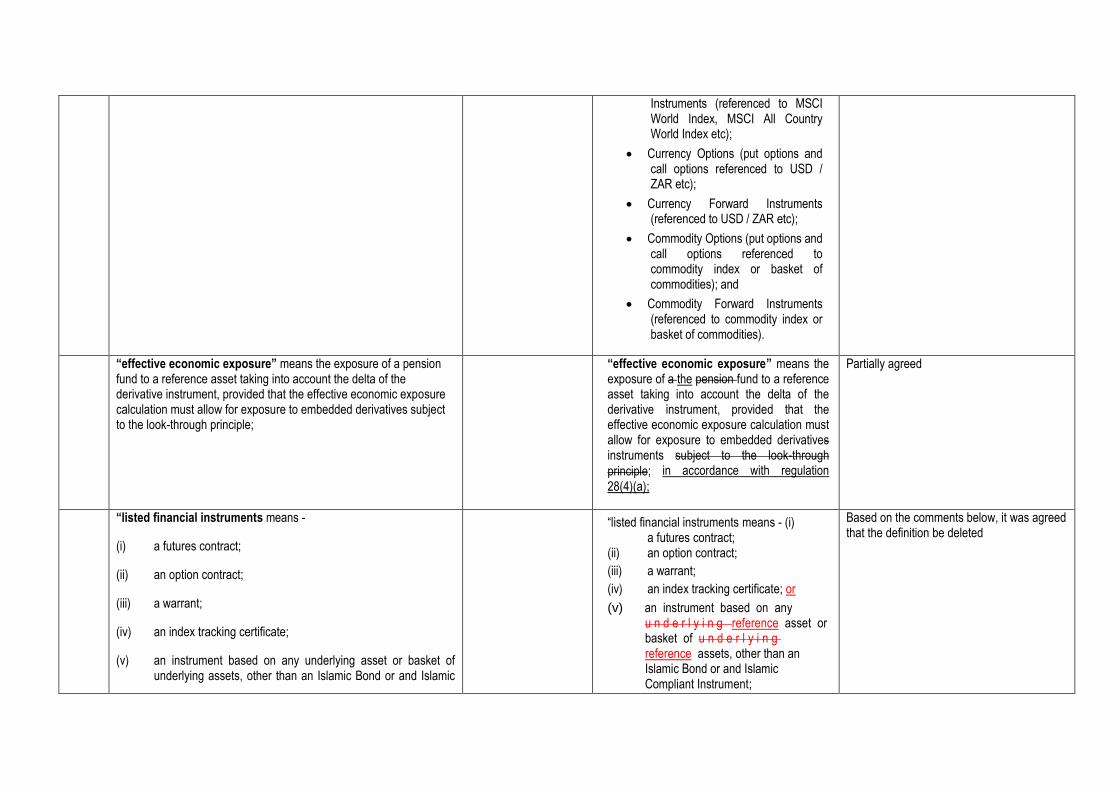

Local Equity Options (put options and call options referenced to FTSE / JSE Top 40 Index, FTSE / JSE SWIX 40 Index etc);

Offshore Equity Options (put options and call options referenced to MSCI World Index, MSCI All Country World Index etc);

Local Bond Options (put options and call options referenced to specific SA Government Bonds, e.g. R 203);

Local Bond Forward Instruments (referenced to specific SA Government Bonds and Inflation Linked Bonds, e.g. R 202);

Local Equity Forward instruments (referenced to FTSE / JSE Top 40 Index, FTSE / JSE SWIX 40 Index etc);

Offshore Equity Forward

Instruments (referenced to MSCI World Index, MSCI All Country World Index etc);

Currency Options (put options and call options referenced to USD / ZAR etc);

Currency Forward Instruments (referenced to USD / ZAR etc);

Commodity Options (put options and call options referenced to commodity index or basket of commodities); and

Commodity Forward Instruments (referenced to commodity index or basket of commodities).

“effective economic exposure” means the exposure of a pension fund to a reference asset taking into account the delta of the derivative instrument, provided that the effective economic exposure calculation must allow for exposure to embedded derivatives subject to the look-through principle;

“effective economic exposure” means the exposure of a the pension fund to a reference asset taking into account the delta of the derivative instrument, provided that the effective economic exposure calculation must allow for exposure to embedded derivatives instruments subject to the look-through

principle; in accordance with regulation

28(4)(a);

Partially agreed

“listed financial instruments means -

(i) a futures contract;

(ii) an option contract;

(iii) a warrant;

(iv) an index tracking certificate;

(v) an instrument based on any underlying asset or basket of underlying assets, other than an Islamic Bond or and Islamic

―listed financial instruments means - (i) a futures contract; (ii) an option contract;

(iii) a warrant;

(iv) an index tracking certificate; or

(v) an instrument based on any u n d e r l y i n g reference asset or basket of u n d e r l y i n g reference assets, other than an Islamic Bond or and Islamic Compliant Instrument;

Based on the comments below, it was agreed that the definition be deleted

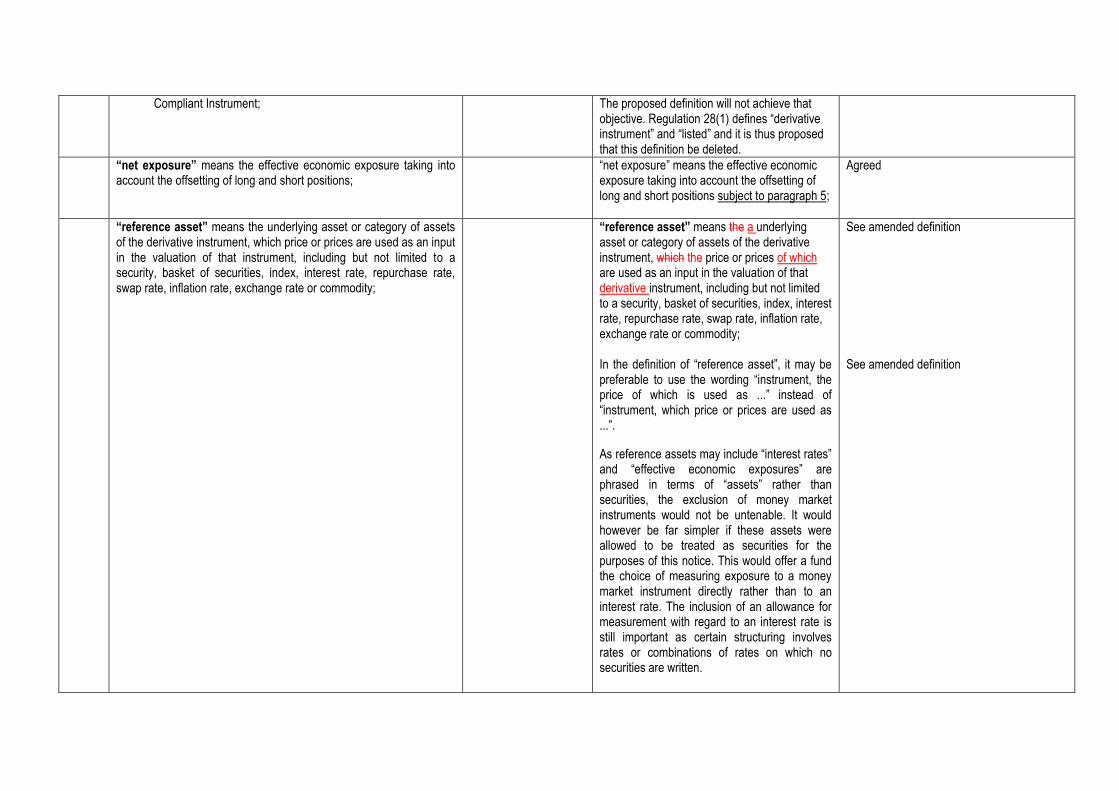

Compliant Instrument; The proposed definition will not achieve that objective. Regulation 28(1) defines ―derivative instrument‖ and ―listed‖ and it is thus proposed that this definition be deleted.

“net exposure” means the effective economic exposure taking into account the offsetting of long and short positions;

―net exposure‖ means the effective economic exposure taking into account the offsetting of long and short positions subject to paragraph 5;

Agreed

“reference asset” means the underlying asset or category of assets of the derivative instrument, which price or prices are used as an input in the valuation of that instrument, including but not limited to a security, basket of securities, index, interest rate, repurchase rate, swap rate, inflation rate, exchange rate or commodity;

“reference asset” means the a underlying asset or category of assets of the derivative instrument, which the price or prices of which are used as an input in the valuation of that derivative instrument, including but not limited to a security, basket of securities, index, interest rate, repurchase rate, swap rate, inflation rate, exchange rate or commodity; In the definition of ―reference asset‖, it may be preferable to use the wording ―instrument, the price of which is used as ...‖ instead of ―instrument, which price or prices are used as ...‖.

As reference assets may include ―interest rates‖ and ―effective economic exposures‖ are phrased in terms of ―assets‖ rather than securities, the exclusion of money market instruments would not be untenable. It would however be far simpler if these assets were allowed to be treated as securities for the purposes of this notice. This would offer a fund the choice of measuring exposure to a money market instrument directly rather than to an interest rate. The inclusion of an allowance for measurement with regard to an interest rate is still important as certain structuring involves rates or combinations of rates on which no securities are written.

See amended definition See amended definition

―reference asset‖ means the underlying asset or category of assets or variable from of the derivative instrument, which the price or value prices are used as an input in the valuation of that instrument, including but not limited to a security, basket of securities, index, interest rate, repurchase rate, swap rate, inflation rate, exchange rate or commodity of the derivative instrument is derived; It is suggested that the definition be amended as proposed for simplification and for the sake of clarity. The proposed definition will make it clear that the reference asset can be an asset (e.g. single share) or category of assets (e.g. equity) or variable (e.g. an interest rate in the case of interest rate derivatives) and the price or value of the derivative instrument is derived from those assets or calculated with reference to those assets.

Agreed.

“securities” means securities as defined in the Securities Services Act, 2004, (Act No. 36 of 2004);

―securities‖ are defined as in the Securities Services Act. This definition excludes all money market instruments, which may be unintentional. (Conditional exclusion in Securities Services Act, 2004 Chapter 1, 1 ―securities‖ 1. (b) (ii))

The definition of ―securities‖ in the Securities Services Act includes ―derivative instruments‖ and the use thereof may thus be confusing in the context of these Draft Conditions. The term is used in the definitions of ―reference assets‖ and ―underlying assets‖ and paragraphs 5.1 and 5.1.1. Please refer to the comments on these definitions and paragraphs. If these are accepted, it is not necessary to define ―securities‖.

Due to the comment below, it was agreed that the definition be deleted

Agreed, deleted the definition

“underlying asset” in relation to a listed or unlisted financial The definition of ―reference asset‖ makes this definition redundant

As this could create confusion, it is agreed to delete the definition

instrument means –

(i) any security;

(ii) an index as determined by an exchange;

(iii) a group of securities which is the subject matter of the financial instrument, whether such group of securities is represented by an index or not;

(iv) a currency rate; or

(v) an interest rate;

“unlisted financial instruments” means -

(i) forward currency swap;

(ii) interest rate swap;

(iii) exchange rate swap; and

(iv) index swap.

As above, the reason for the distinction between listed and unlisted financial instruments seems arbitrary and is not made any clearer in the body of the Notice. The definition of ―derivative instrument‖ as currently defined in the SSA/Reg 28 is more appropriate The regulator‘s potential concern in respect of unlisted derivative instruments is appropriately and adequately covered by the principles contained in Regulation 28(2)(c)(v) and (viii), the principles contained in paragraph 2 of these Draft Conditions for the Use of Derivatives, the counterparty limits in Table 1 to Regulation 28 and reporting obligations.

Agreed to delete the definition

Uses of derivative instruments

A pension fund may use a derivative instrument to obtain effective economic exposure to reference assets per Table 1 of regulation 28 for purposes of reducing risk, reducing cost, generating capital or income for the fund and effective portfolio management.

It is proposed that the phrase ―to obtain effective economic exposure to reference assets per Table 1 of regulation 28‖ be deleted, firstly because it is covered by the purposes listed in the definition and secondly because read together with the definitions of ―effective economic exposure‖ and ―reference asset‖ it may exclude certain interest rate derivatives. The reference ―asset‖ for a swap is a variable interest rate which cannot be classified as an

In recognising interpretation challenges, this section has been simplified to reflect the difference between using a derivative instrument for hedging versus another purpose, and applies different governing principles and requirements to reflect the different inherent characteristics and risks of that usage.

―asset‖ per Table 1 of regulation 28. Derivative instruments are investments and it is therefore suggested that a purpose of investment be included as it was in the previous Draft Conditions. It is also suggested that the phrase ―effective portfolio management‖ be replaced with ―efficient portfolio management‖ as that is the commonly known term in the context of derivatives. Furthermore, the ―and‖ should be replaced with ―or‖ as pension funds may from time to time use derivatives for one of the listed purposes and not all of the listed purposes at the same time.

2. Principles A board of a pension fund must as all times adhere to the following principles when derivative instruments are included in its investment portfolio:

A board of a pension fund must as at all times adhere to the following principles when derivative instruments are included in its investment portfolio:

To clarify the intention of this paragraph, the wording was amended

2.1.1 not be used to circumvent any principle, regulation or limit as set out in regulation 28 on an effective economic exposure basis;

not be used to circumvent any principle, regulation or limit as set out in regulation 28 on an effective economic a net exposure basis; The limits apply on a net exposure basis, i.e. the effect of the derivative (positive/long or negative/short) should be taken into account when monitoring compliance with the limits. It is thus suggested that ―effective economic exposure‖ be replaced with ―net exposure‖.

The reference to ―an effective economic exposure basis‖ appears to be unnecessary and has been deleted.

2.1.3 the sum of the effective exposures to derivative instruments, together with the market value of all the physical underlying assets of the investments of the fund, may not exceed the relevant asset limits as set out in Table 1 to Regulation 28;

A further principle that FRB believes should be adopted is that of look-through with respect to derivative exposure so that exposure to the various drivers of market risk can be attributed to the correct asset – so an interest rate swap is viewed as a position in a floating rate instrument with the same maturity as a position with the opposite sign in a fixed rate security. This will furthermore allow for correct allocation in the case of total rate of return swaps and credit derivative swaps.

This clause has been deleted based on the comments below

This clause causes significant concern, as it effectively negates and contradicts all netting provisions as specified in the rest of the Schedule. This is because it refers to ―the sum of the effective exposures‖ instead of the ―net exposure‖. Also, this clause is not needed, as gearing and shorting is not allowed overall ito clause 2.1.5., and the limits per Table 1 need to be adhered to on a net basis per clause 4.1. Delete clause or change wording to ―the net exposure of the investments of the fund may not exceed the relevant asset limits as set out in Table 1 to Regulation 28;‖

2.1.4 be covered by sufficient liquid assets to meet the fund‘s forthcoming obligations, taking into consideration the fund‘s liability position;

Liquid assets are not defined and it is proposed that ―sufficient‖ be replaced by ―appropriate‖. The meaning of ―covered” in 2.1.4 is not clear. The term has no generally accepted meaning in the derivatives market. We see a number of possible interpretations with different implications:

a. A fund should hold a sufficient quantity of cash and/or liquid assets to settle obligations arising as a result of the derivative transaction in cash at the time(s) the derivative matures.

b. A fund is required to either meet a. or to hold a physical asset(s), such as a share(s) which could be used to settle the obligations (in kind) arising from the derivative trade at maturity, even if this

Agreed that this wording is unclear, have therefore changed ―sufficient liquid‖ [assets] to ―appropriate‖ [assets] The intention of this principle to be that a fund must hold appropriate assets as cover for the derivative instrument to ensure that the derivative position should not be naked or unfunded. As an example, a long position must be covered by cash and a short position must be covered by the asset or assets in the portfolio.

asset is illiquid.

c. A fund is required to hold cash or other assets which will be sufficient to meet margining requirements for a derivative requiring margining, but need not hold sufficient assets for maturity obligations as the derivative can be closed out or sold according to 2.1.8.

d. Covered is also used to describe a derivative holding which is not naked or unfunded. I.e. covered derivative trades are trades where losses are ‗covered‘ by a portion of the fund‘s assets, equal to the notional of the derivative in question. Under this definition, an example of a covered trade would be a fund holding R100 to back R100 of futures exposure, even if this quantity of liquidity is not required to meet margining requirements. Such a fund would not achieve any net gearing or net short positions on these two assets. An example of an uncovered fund would be a fund that chooses instead to hold no cash or sufficient cash to meet margining requirements. Whilst the effect here is similar to b. explained above, the purpose for holding the cash is different. This becomes important in more complex examples, such as where automated close outs apply. For example, a bank may require that a future is automatically closed out after a 20% loss to protect it against credit exposure from the fund. Under b., the fund would only require 20% in cash. Under the interpretation in d. the fund would require a full 100% of notional in

cash.

e. The meaning of ―taking into consideration the fund‘s liability position‖ is hence also unclear in this context. It is unclear whether this relates to member liabilities, liabilities to creditors, trading counterparties or a combination of these. It is also unclear whether this implies that liabilities can be treated as a negative economic exposure as was the case in previous drafts of this notice. (Note we do not believe it is necessary to retain the allowance for the treatment of liabilities as a negative economic exposure.)

2.1.5 not involve the use of leverage, gearing or result in net short positions at a fund level, other than those allowed for the purposes of interest rate hedging and the netting rules set out in paragraph 4 below;

The reference to leverage and gearing must be deleted. It is likely to cause confusion as it is not defined. By nature derivative instruments involve the use of leverage but what is important is that their use should not result in a net short position at a fund level. Leverage and gearing is not possible if the derivative is covered by appropriate assets.

In light of 3. (d) of the main Regulation, which prohibits investment in instruments that can lead to losses greater than the capital invested or original commitment made, we believe limited gearing should be allowed even at fund level. This is currently prohibited by 2.1.5. There are many examples where this prohibition would be problematic. A simple example is a collateralized, capital protected equity linked note. Let‘s assume the note is purchased for R100 and has a delta of 30% and is always collateralized by government bonds (or cash). This note would immediately expose the fund to R100 of government bond (or cash) exposure

The gearing restriction has been amended. Paragraph 2.1.5 has been deleted, and the revised paragraphs 1(2) and 1(3) align the notice to 3(d) of the main Regulation, and take into account the characteristics and risks of hedging versus other strategies.

using the look through principle. Additionally the Fund would have a R30 equity exposure, resulting in 130% total exposure. The fund would however face no risk of losing more than its investment as the delta of the instrument would approach 0 as the markets fall to levels significantly below the pre-agreed strike level(s), and because the note is collateralised. The fund would not even be exposed to geared equity losses. A large portion of derivatives generate an effective exposure to an asset class and a counterparty exposure. It is important to recognize both of these exposures and to limit these in line with the main regulation‘s limits to each. We do however believe that capping these at aggregate to 100% will seriously infringe on funds‘ ability to meaningfully use derivatives. We would recommend a limit of 200%, with a limit of 100% (or less) to exposure excluding cash and government issued bonds. An alternative means to address this would be to separate the concepts of asset class exposure and credit exposures and cap these separately.

In addition to above, a geared participation structure can make sense if the fund or its asset manager takes the view that potential upside to the market over the coming years is limited. A geared participation structure is one where for example, if the market moves up by x%, the fund earns a return of say 1.3x%, with the maximum return capped at some level, accompanied by a capital protection feature. Such a strategy would allow the fund to improve returns (relative to another fund that does not adopt a geared participation strategy), as long as the market does not rise above the capped

level mentioned earlier.

2.1.7 be subject to reliable, independent and verifiable valuation on a regular basis; and

What constitutes ―reliable, independent‖ valuation by whom? be subject to reliable, independent and verifiable independently verifiable valuation on a regular basis; and The principle may be read to mean that all valuations must be done by a third party. It was submitted that valuations by third parties will be onerous and costly. Listed derivative instruments are subject to valuation by the exchange. Unlisted derivative instruments are generally subject to valuation by the counterparty as set out in the master agreement. In some cases, the valuation is performed by a structure set up by an investment manager (e.g. a valuations committee consisting of representatives that are independent from the business unit that concluded the transaction). In the latter case, there is generally a documented valuations procedure approved by the board of directors and the process of valuation in accordance with the documented procedure is audited by external auditors on an annual basis. International Financial Reporting Standards (IFRS) also require a valuation policy. It is thus suggested that the paragraph be rephrased to take the mentioned circumstances into account.

The principle is captured in this paragraph and the intention is clarified in paragraph 2(6), providing flexibility regarding the valuing of listed/unlisted derivative instruments and takes into consideration how decisions relating to these instruments are made. It therefore accommodates listed instruments for which a price is readily available. Unlisted instruments may be valued by either a separate division within the investment manager or an independent party.

2.1.8 at the fund‘s initiative, be able to be sold, liquidated or closed out by an offsetting transaction at any time;

It is unclear what is meant by ―at any time‖ Proposed wording: ―at the fund‘s initiative, be able to be sold, liquidated or closed out by an offsetting transaction‖ where held directly by the fund, at the fund‘s initiative, be able to be sold, liquidated or closed

Agreed, see revised wording.

out by an offsetting transaction at any time within a reasonable time; Full liquidity should not be required for retirement funds due to the long-term nature of its liabilities. It is unduly onerous given that the same level of liquidity is not required for any other instrument e.g. small cap equity, private equity funds or property. Derivative instruments will be covered by assets, net shorting is prohibited. It is suggest that the reference to ―at any time‖ be replaced with ―within a reasonable time‖. With the look-through principle in mind, in the case of a retirement fund investing solely in collective investments schemes or a linked policy which may contain derivatives, the retirement fund will not be able to instruct the collective investment scheme or insurer to sell, liquidate or close out a derivative instrument at any time. It is thus suggested that this principle only be applicable where the fund directly holds the derivative instrument.

2.2 The board of a fund must ensure that it is aware of all the risks inherent in derivative instruments and that such risks are disclosed to it in an understandable manner, taking into consideration that more exposure in respect of an asset or asset class could be obtained through the use of a derivative instrument than would be obtained by investing directly in the asset or asset class i.e. the cash value of the derivative is often more sensitive to a change in the price of the asset than if the investment had been made directly in the asset.

The board of a fund must ensure that it is aware of all the risks inherent in derivative instruments and that such risks are disclosed to it in an understandable manner, taking into consideration that more exposure in respect of an a reference asset or asset class could be obtained through the use of a derivative instrument than would be obtained by investing directly in the reference asset or asset class i.e. the cash value of the derivative instrument is often more sensitive to a change in the price of the reference asset than if the investment had been made directly in the reference asset. The board of a fund must ensure that it is aware of all the risks inherent in derivative instruments

Agree, see revised paragraph 2(2)

and that such risks are disclosed to it in an understandable manner, taking into consideration that more exposure in respect of an asset or asset class category could be obtained through the use of a derivative instrument than would be obtained by investing directly in the asset or asset[ class] category i.e. the cash value of the derivative is often more sensitive to a change in the price of the asset than if the investment had been made directly in the asset It is not appropriate to include an explanatory note in the Draft Conditions and suggest that the last part of the paragraph be deleted. It is also suggested that the references to ―class‖ be replaced with references to ―category‖ for consistency in drafting.

2.3 In addressing the risks relating to a specific instrument or counterparties in derivative transactions, or both, the fund must perform the appropriate due diligence investigation taking into account all risks relating to a derivative instrument. Such risks include but are not limited to market-, credit-, valuation- and liquidity risks, as well as operational risk in respect of instruments not listed on an exchange. In performing the due diligence investigation a fund may take credit ratings of the derivatives counterparty into account, but such credit ratings should not be relied on in isolation for risk assessment or analysis of an asset.

In addressing the risks relating to a specific derivative instrument or counterparties counterparty in derivative transactions, or both, the fund must perform the appropriate due diligence investigation taking into account all risks relating to a derivative instrument. Such risks include but are not limited to market-, credit-, valuation- and liquidity risks, as well as operational risk in respect of instruments not listed on an exchange. In performing the due diligence investigation a fund may take credit ratings of the derivatives instrument counterparty into account, but such credit ratings should not be relied on in isolation for risk assessment or analysis of an asset derivative instrument. Some of these risks are also applicable to exchange traded instruments This principle is contained in Regulation

Due to the comment below, it was agreed to delete paragraph as it is already contained in Regulation 28(2)(c)

28(2)(c)(v) and (vii). Paragraph 2.2 of these Draft Conditions also covers the elements of risk. The duplication of principles already contained in Regulation 28 with wording slightly different to those used in the regulation may cause confusion or speculation as to whether it was intended to have a different meaning in the context of derivative instruments. It is thus suggested that this paragraph be deleted.

2.4 A board of a pension fund must ensure that risk management processes and procedures are implemented to identify, manage and measure, at any time, the exposure to and risks of all derivative instruments and the contribution of these to the overall risk profile of an investment portfolio of the fund.

A The board of a pension fund must ensure that risk management processes and procedures are implemented to identify, manage and measure, at any time, the exposure to and risks of all derivative instruments and the contribution of these to the overall risk profile of an investment portfolio of the fund.

Revised paragraph 2(3) refers to ―a fund‖

2.5 A fund must have an appropriate risk management policy or framework in place to determine amongst others with the processes and procedures in selecting a counterparty, managing counterparty exposure, monitoring counterparties, managing counterparty risks and close out in the event of a counterparty default.

A The board of a fund must ensure that have an appropriate risk management policy or framework is in place to determine amongst other things with the processes and procedures in selecting a counterparty, managing counterparty exposure, monitoring counterparties, managing counterparty risks and close out in the event of a counterparty default. It is proposed that the word ―with‖ be deleted to improve the reading of the paragraph.

Due to the comments below, paragraph 2(4) has been revised

2.6 The de minimus exception as referred to in regulation 28(4)(b) must not be used in the case of the fund‘s direct use of derivative instruments.

Why not? What about for example an option on the TOP 40 Index - does the fund have to work out the effective economic exposure of the entire structure and then weight it between the conditions of 3.1 (a) (i) and 3.1 (a) (ii) of Regulation 28 to be able to determine the underlying exposure to the various shares (issuers of the shares)? If so, this could result in unduly burdensome administrative duty being placed upon the fund

Agree to remove this clause as it may compromise the principle given effect through the de minimus rule

Regulation 28(4)(b) provides that where an asset comprises less than 5% of the portfolio, then the fund need only disclose the categories of assets specified in Table 1, and not each underlying asset. Is the intention to require look-through to each underlying individual asset of for example an equity index future even if the effect that the equity future will have on an asset or asset category is less than 5%? What potential mischief does the regulator wish to prevent? If the regulator is concerned that a derivative instrument may cause excessive exposure on an individual instrument look-through basis, it is submitted that the protection mechanisms contained in the regulation (principles, limits and cover requirements) are adequate. It is thus suggested that this principle be deleted.

I have only one suggestion regarding costs, for inclusion either under Paragraph 2 or under Paragraph 7, namely that the board must ensure that it is fully aware of all the fees and costs associated with the use of derivative products, and that the costs are reported to the board in a transparent and understandable manner. Investment managers should not be opaque on fees due to the complexity of the products offered.

Agreed

3. Counterparties

A fund may only invest in derivative instruments where the counterparties are:

3.1 the South African Government; 3.2 South African banks; 3.3 long-term insurers; 3.4 short-term insurers; 3.5 foreign banks;

A fund may only invest in derivative instruments where the relevant counterparties are: In section 3, the Notice should clarify when/where ―South African‖ or ―foreign‖ is intended upfront, particularly with reference to the long-term and short-term insurers.

Not agreed as not considered necessary in this context. Already defined in the main regulation 28 wording

3.6 authorised users; or 3.7 clearing houses.

A fund may only invest in derivative instruments where the counterparties are: 3.1 the South African Government; 3.2 South African banks; 3.3 long-term insurers; 3.4 short-term insurers; 3.5 foreign banks; 3.6 authorised users; or 3.7 clearing houses; 3.8 state owned entities; or 3.9 entities approved by the Registrar. It is suggested that 100% state owned entities (e.g. Transnet) should be included in the list of acceptable counterparties. The paragraph should also provide for counterparties to be approved by the Registrar to provide for future developments.

Agreed, Registrar will prescribe those state owned entities to be permitted, consistent with the main Regulation.

4. Calculating exposure

4.1 The calculation of assets and categories of assets referred to in regulation 28 must include the net exposure of a derivative instrument subject to paragraph 4 of this Schedule;

) The draft derivative notice requires in section 4.1 that ―the calculation of assets and categories of assets referred to in regulation 28 must include the net exposure of a derivative instrument‖. Section 5.1 indicates that ―netting of long and short derivatives and securities positions is allowed in calculating the limits set out in regulation 28‖ if certain conditions are met. This would therefore require derivatives to be disclosed at exposure value (not fair value). The Regulation and the Draft derivative notice seem to be in conflict if interpreted for the purposes of Schedule IB reporting. The Regulation requires reporting of derivatives at fair value whereas the Notice requires exposure value. If the intention is that Schedule IB

Agree For clarity, have added ―effective economic‖ and removed the reference to ―net,‖ as this term is not defined

includes derivatives at exposure value, Schedule IB would not reconcile to the financial statements which include derivatives at fair value. We recommend clarifying the following in the notice:

Should the fair value or exposure value be used to compile the Schedule IB report to be included in the financial statements?

If exposure value is to be used the schedule IB would not reconcile to the fair value of the assets on the financial statements. Guidance should be given with regards to the reconciliation / adjustments needed to explain this difference.

Agree, revised wording has been proposed to provide clarity as a footnote to Schedule IA of the annual financial statements. Schedule IA will reconcile to Schedule F and Schedule IB

4.3 Notwithstanding paragraph 4.2, where a derivative instrument is traded on an exchange, such counterparty exposure will not form part of the calculation in determining the counterparty exposure, if cleared through a clearing house, on condition that:

First Rand Bank

It would appear that the draft proposal on interest rate derivative netting is trying to take into account a notion of counterparty credit risk by disallowing netting for limit purposes unless closeout netting and setoff will apply for the two positions. This problem can be addressed by rather calculating and managing the risk of the expected loss due to default of either counterparty (CVA reporting and hedging). A simplistic alternative approach might be to have a static ratings table lookup for the netting percentage, whereby if both positions are with AAA counterparties 95% netting can be achieved, but if one is with, say, a B counterparty then only 10% netting can be achieved. In none of these cases will closeout netting be possible across counterparties, but the reduced likelihood of default reduces the risk of incorrectly netting positions which ultimately cannot be set off.

Similar has been described in the proposed draft paragraph 5(1).

Notwithstanding paragraph 4.2, where a derivative instrument is traded on an exchange, such counterparty exposure will not form part of the calculation in determining the counterparty exposure, if cleared through a clearing house, on condition that, in terms of the rules of an exchange,:

Agreed, see amended wording

4.3.1 the due performance of the derivative instrument is underwritten from the time of trade to the time of settlement;

Underwritten by whom? The rules will determine the underwriting requirements

5. Netting

5.1 Netting of long and short derivative and securities positions is allowed in calculating the limits set out in regulation 28 where:

A concern has been raised that many investment managers and ―white label‖ managers are constantly speculating, juggling and netting off derivative instruments to inflate fund performance on measurement dates, which pose enormous systemic risk in the event of them being called on these bets should there be a major withdrawal from some of the markets traded in with unsecured (―over the counter‖) unlisted instruments. Many asset managers, stockbrokers and banks have specifically set up nominee and trading houses so that they do not carry the risk – leaving it unfairly but squarely on the shoulders of BoT and members who generally are completely unaware of the risks being taken. Asset managers are creaming off ―performance bonuses‖ on specific measurement dates where these instruments play quite a large role. The extent of this is ―hidden‖ by netting off – but if both put and call options go bad, in truth the ―assets‖ vaporise and there will be no netting off in real life – just a loss to members, who in many cases hold no scrip or other form of title. Let‘s imagine that a 20% option was offset by another 10% derivative instrument – and both become value less. The real loss to members

Already addressed in the reporting of continuous compliance and increase of transparency of fees and costs. This provision has been revised, now paragraph 4(2)(d) of the revised draft. In terms of calculating counterparty exposure, derivative instruments may only be netted off if a single legal obligation between the parties can be created in terms of the ISDA master agreement in the event of default. In terms of calculating effective economic exposure, two derivative positions on the same underlying security with different counterparties may be netted off without any haircut applying to allow for counterparty risk. 5 in the revised draft makes no reference to counterparty. Any net-short positions will be disclosed in Notes G1 and G2 of Schedule IA of the annual financial statements if there is a breach on any provision of the derivatives notice

could be 30%, and in many cases these are unsecured trades between ―authorised users‖ with no capital guarantee to the funds, even if ―cash‖ is supposedly the asset class in question. In calculating the limits set out in regulation 28, the asset or asset category held by the fund may be netted with the effective economic exposure of a derivative instrument where: Netting of long and short derivative and securities positions is allowed in calculating the limits set out in regulation 28 where: It is proposed that the wording to clarify that the physical assets held by the fund may be netted with the derivative exposure. The delta of the derivative can be positive or negative, depending on whether it is a long or short position. The proposed wording will have the same effect but will not require defining ―long and short derivative and securities positions‖.

Agreed, see revised wording

5.1.1 the derivative instrument is aimed at reducing or eliminating the risks associated with an asset or category of assets obtained through the use of derivative instruments or securities;

5.1.1 may read better by removing ―obtained through the use of derivative instruments or securities‖ at the end. This clause is unnecessarily limiting. i.t.o. the Schedule, gearing and shorting is not allowed, and Table 1 limits have to be adhered to for net exposure. So there is no reason for this additional requirement. Also, it is not clear what ―reducing or eliminating risks‖ would mean in the context of fund investment, e.g. does this refer to risk in the sense of capital protection, or not obtaining returns in real terms, or not meeting the fund‘s investment objectives? It is proposed that the clause be deleted or reworded to:

Based on the comments received, it was agreed that paragraph 5.1.1 be deleted

―the derivative instrument is aimed at managing the risks associated with an asset or category of assets obtained through the use of derivative instruments or securities;‖ Paragraph 1 of the Draft Conditions sets out the permissible uses of derivative instruments. It seems inconsistent to allow netting only for some of the permissible investment purposes. ASISA members therefore propose that this paragraph be deleted.

5.1.2 the reference asset(s) of the derivative instrument is identical or similar to the assets underlying the position of which the risks are being reduced or eliminated, where similar in this context means that the reference assets -

In 5.1.2 the driver of netting with respect to equity derivatives is the underlying asset and there is no additional criterion that the derivatives counterparty must be the same when it comes to netting. However in the case of debt instruments the focus is on the ―issuer‖ or credit counterparty to the derivative transaction rather than the underlying instrument except in the case of 5.1.2 (iv). the reference asset(s) of the derivative instrument is identical or similar to the assets underlying the position of which the risks are being reduced or eliminated held by the fund, where similar in this context means that the reference assets - Similar to the comments on paragraph 5.1.1 above, the reference to investment purposes which is not aligned with paragraph 1 of the Draft Notice should be deleted. It is proposed that the references to ―assets underlying the position‖ be replaced with ―assets held by the fund‖. This will have the same effect, i.e. netting will be allowed if the reference assets of the derivative instrument is

Noted. Agreed Agreed

identical or similar to the assets held in the portfolio of the fund, but will remove the reference to ―underlying‖ and the need to define it. The references to ―underlying reference assets‖ should be replaced with ―reference assets‖ to align with the defined term.

(i) are of an index form and listed on an exchange, or are highly correlated to the assets underlying the position, leaving no material residual risk;

(i) are of an index form, and listed on an exchange, or are highly correlated to the assets underlying the position held by the fund, leaving no material residual risk; In paragraph 5.1.2(i), it is proposed that a comma be inserted after ―an index form‖ to avoid potential misinterpretation as it may be read to mean that the index must be listed. ASISA members proposed in its comments on the previous Draft Conditions that the paragraph should read ―are of an index form and its constituents are listed‖.

An exchange traded index is subject to requirements that govern the make-up and calculation of the index, giving comfort to its reliability. The revised draft therefore differentiates between a listed and unlisted index, and imposes a higher standard on the unlisted index.

(ii) are sufficiently diversified so that price movements of one of the assets do not unduly affect the performance of the underlying reference assets as a whole, whether such underlying reference assets are in an index form or other as allowed in sub-paragraph (i); and

are sufficiently diversified so that price movements of one of the assets do not unduly affect the performance of the underlying reference assets as a whole, whether such underlying reference assets are in an index form or other as allowed in sub-paragraph (i); and [Comment: does not make sense in the context of the meaning of ―similar‖, this clause needs to be moved] 5.1.2 (ii) requires that no single asset dominates the basket of assets underlying a short position if the fund wishes to (1) offset this short position against a long position (2) using a ―similar‖ economic exposure. (Note that the requirement for diversification is not present if the investor is using an identical short position rather than a similar short position). Arguably single stock

Due to the diversity of comments received, these comments will be reconsidered with the comments received on the second draft.

futures are not identical to physical shares due to differences such the lack of dividends. It may be useful to clarify this paragraph as follows (italics indicate words that have been added):

―the reference asset(s) of the derivative instrument is identical (including single stock futures) or similar to the assets….‖ It may also be useful to issue guidance on what assets are acceptably ―similar‖ in 5.1.2. This could be done in the Conditions for the use of Derivative Instruments or in a separate guidance note. Examples of acceptable usage would be useful. For example can a fund hedge out exposure to the All Share using a derivative written on the Top 40, a more liquid subset of the All Share, which is generally cheaper to trade. (ii) are sufficiently diversified so that price movements of one of the assets do not unduly affect the performance of the underlying reference assets as a whole, whether such underlying reference assets are in an index form or other as allowed in sub-paragraph (i); and or It is suggested that the ―and‖ at the end of paragraph 5.1.2(ii) be replaced with ―or‖. A view was expressed that this requirement is too restrictive to require that all three conditions be met.

(iii) represent an adequate benchmark or reference asset for the market or portfolio to which it refers, including regular measurement, rebalancing and liquidity appropriate to replicability;

represent an adequate benchmark or reference asset for the market or portfolio to which it refers, including regular measurement, rebalancing and liquidity appropriate to replicability replicating the reference asset;

Agreed

and further with regard to the netting of debt instruments-

(iv) the effective economic exposure to debt instruments as defined in Table 1 of regulation 28 may be hedged and netted with a derivative instrument whose underlying reference asset is a government bond, JIBAR or the repurchase rate; however, any consequential or residual spread exposure as a result of the netting must be disclosed; and

the effective economic exposure to debt instruments as defined in Table 1 of rRegulation 28 may be hedged and netted with a derivative instrument whose underlying reference asset is a government bond, JIBAR or the repurchase rate; however, any consequential or residual spread exposure as a result of the netting must be disclosed; and In 5.1.2 iv, it would be useful to clarify whether ―government bond‖ is RSA government-issued, or if can include government-guaranteed (e.g. would SANRAL bonds count?) It is proposed that paragraph 5.1.2(iv) be deleted as it is appropriately covered in paragraph 5.1.2(i) through the reference to ―highly correlated‖. If subparagraph (iv) remains as is, it will for example not be possible for an Eskom bond to be hedged with an Eskom bond derivative. The reference to debt instruments in Table 1 is also not appropriate as the reference asset of most interest rate derivatives is a variable rate and Table 1 does not define interest rates. It is not clear why the Registrar wishes to limit the types of reference assets in the case of interest rate derivatives. Risks will be covered by the principles of due diligence, cover requirements, limits and reporting requirements.

Agreed This clause only provides for government bonds and does not currently include bonds that are government guaranteed. Paragraph 5(2) should be read with paragraph 5(1) and therefore gives added flexibility in the netting of debt instruments. This clause will enable funds to use the debt instruments listed in (iv) (now par 5(2)(a)) to hedge or net even though it is not ―highly correlated‖ as per paragraph 5(1).

(v) the effective economic exposure to debt instruments may be netted off with an opposite exposure where the issuer is the same but the term may differ; however, any residual exposure as a result of the difference in term must be disclosed; and

In 5.1.2 v, can clarify ―issuer‖ to be ―issuer of the debt instruments‖. Paragraph 5.1.2(v) may cause confusion as to the meaning of ―opposite exposure‖. The reference to the residual exposure that must be disclosed will also cause confusion as it is not

Agree, see wording in revised notice. Agree, the reference to opposite exposure has been removed. The wording has been amended to provide for the residual exposure to be managed and monitored and no longer

stipulated how this exposure should be disclosed.

be disclosed

5.1.3 exposure to a counterparty may be netted off with the opposite exposure to the same counterparty only where an appropriate master agreement is in place which give legal effect to netting as contemplated in section 35B of the Insolvency Act, 1936 (Act No. 24 of 1936) to create a single legal obligation, covering the relevant transactions included in the calculation of the counterparty exposure. Such master agreement must provide that, where such counterparty fails to perform, or in cases of bankruptcy, liquidation or any similar circumstance, the fund would have a preference claim to receive or an obligation to pay only the net sum of the positive and negative mark-to-market values of the underlying transactions

exposure to a counterparty may be netted off with the opposite exposure to the same counterparty only where an appropriate master agreement is in place which give legal effect to netting as contemplated in section 35B of the Insolvency Act, 1936 (Act No. 24 of 1936) to create a single legal obligation, covering all the relevant transactions included in the calculation of the counterparty exposure. Such master agreement must provide that, where such counterparty fails to perform, or in cases of bankruptcy, liquidation or any similar circumstance, the fund would have a preference claim right to receive or an obligation to pay only the net sum of the positive and negative mark-to-market values of the underlying transactions It is unclear what the intention of the ―preference claim‖ wording is (i.e. preferential to what?) Our understanding is that the aim of industry standard ISDA documentation is to ensure that net obligations rank equal to other obligations of the counterparty, and the ―preference claim‖ wording may be unduly onerous and effectively prohibit generally acceptable and standard swap transactions in the market. Suggested wording: ―5.1.3. …Such master agreement must provide that, where such counterparty fails to perform, or in cases of bankruptcy, liquidation or any similar circumstance, the fund would have a claim to receive or an obligation to pay only the net sum of the positive and negative mark-to-market values of the underlying transactions.‖

Due to comments below, the paragraph was moved to paragraph 4(2)(d) in the revised draft notice Comment regarding preference claim/right is noted to be reconsidered in the redraft.

It is suggested that this paragraph should not follow on paragraph 5.1 as it relates to the netting of counterparty exposure whereas paragraph 5.1 relates to netting of asset exposure. It is thus proposed that this paragraph should form part of paragraph 4.2.

6. Collateral Collateral may be used to reduce counterparty exposure, subject to the following conditions:

With respect to collateral, there is no mention of standard ISDA-type terms/concepts for collateral posting - minimum transfer amount, threshold, independent amount and frequency of posting. In assessing the risk of collateralised positions FRB takes these terms into account - more risky counterparties are those who are contractually required to post less frequently, post no independent amount, post nothing below a large threshold or post only large minimum amounts. This is achieved through a collateralised CVA calculation, which effectively lessens the offset available from collateral by increasing the expected loss where the CSA includes riskier provisions The section on collateral from the Notice on Securities Lending (which is already released and in force), could be adopted for this Notice on Derivatives. This would offer greater consistency between these notices. If this approach is used, the over-collateralisation required would need to be regularly reviewed to ensure it remains appropriate. It may also be necessary to supplement the section from the Notice on Securities Lending with 6.1 and 6.2 to achieve the same effect as the original Notice on Derivatives.

The introductory paragraph of 6 allows one to use collateral to reduce counterparty exposure, but does not suggest explicitly that one would

The comment is noted, however the bi-lateral agreement is required in terms of the ISDA agreement The comment is noted. The principles contained in regulation 28 apply and are not necessarily repeated.

need to recognise the counterparty exposure of the collateral. This is implied by the requirement to use the look-through principle in the main body of regulation 28. We do however think it would be beneficial to explicitly include this in 6.

6.1 The assets that are backing the collateral must be- Who will be doing the measurement? The fund may not have the capability to do so? The assets that are backing the received as collateral must be- In reading this condition 6,it is difficult to determine the context of the condition as the concepts of collateral posted and collateral received appear to be intermingled. The wording is proposed for the sake of clarity.

The board of the fund is responsible for the compliance and must ensure that the expertise and resources are available to monitor compliance. If not, a fund should not make use of derivative instruments. Agree, see revised draft

6.1.1 capable of being liquidated within seven days based on 5% of the previous 30 days‘ total available liquidity in the market for the assets being liquidated;

This could be reworded to:

―realizable by the fund within seven days….‖ capable of being liquidated within seven business days based on 5% of the previous 30 days‘ total available liquidity in the market for the assets being liquidated; From the comments received from ASISA members, it is evident that the interpretation of this condition may be problematic. A liquidity test based on a historical percentage of the market is not always possible. Total available liquidity data may not be available from foreign markets as it is not common for foreign gilts to trade on market. Should total available liquidity be determined on traded positions or bids or offers? It should be sufficient to require liquidity within 7 business days.

For flexibility, the wording has been revised to provide for a principles approach

6.1.2 transparent; and transparent and identifiable; and It is understood that the condition intends to ensure that the fund can properly identify the asset it received as collateral so that it is not misled but it is not clear how the term ―transparent‖ can and should be applied to an asset. It is suggested that the condition be amended as proposed.

Agreed

6.1.3 priced daily priced valued daily It is proposed that the reference to ―priced‖ be replaced with a reference to ―valued‖. A reference to ―price‖ implies selling and will not be appropriate in this context.

Agreed.

6.2 There must be legal separation between the counterparty and the collateral received.

In particular 6.2 would appear to address wrong-way risk on collateral value in a situation where the counterparty has defaulted. FRB looks at a wider risk profile in terms of the correlation of the collateral valuation to the exposure valuation under default scenarios of the counterparty. As a concrete example, if facing a sovereign on a currency swap (with one leg in their domestic currency), collateralised with that sovereign's bonds there is a lot of wrong way risk not only because of lack of legal separation between counterparty and collateral, but also because the currency of the country will depreciate due to a sovereign default. The condition may, from a legal perspective, be impossible to interpret. The collateral is assets and the counterparty is a person so there will always be ―legal separation‖ between the assets and the recipient. Is the intention that the collateral may not increase the exposure to the counterparty? Should it be bankruptcy remote from the counterparty? Will paragraph 6.3 not appropriately provide for separation?

Agree with view expressed, see revised 6(2)(d)

6.3 The collateral received must be held by the fund or an approved nominee or an independent custodian on behalf of the fund; where held by an independent custodian such collateral must not form part of the assets of the independent custodian and such collateral in a segregated account with an independent will not be regarded as counterparty exposure.

ABSA Capital ASISA

The collateral received must be held by the fund or an approved nominee or an independent custodian on behalf of the fund; where held by an independent custodian such collateral must not form part of the assets of the independent custodian and such collateral in a segregated account with an independent custodian will not be regarded as counterparty exposure.

See revised draft

6.4 Non-cash collateral posted to a counterparty may not be sold, hypothecated, re-invested or pledged unless it is agreed to by the fund and immediately replaced with other eligible collateral.

What about posting that happens via the mechanism of an outright transfer of ownership? The counterparty should not have to ―immediately replace‖ as it is effectively protecting its exposure to the fund. Margining occurs regularly, as such there is only very short term settlement risk for the fund. Collateral delivered by way of a pledge cannot in law be sold, hypothecated, re-invested or pledged by the recipient without the consent of the provider of the collateral. If a fund delivers collateral on an out-and-out basis, it by necessary implication consents that the recipient can do with it what it chooses. In that instance the provider of the collateral takes full credit exposure to the recipient, irrespective of what the recipient does with the assets received as collateral. The requirement that the collateral must be replaced thus does not make sense in this context. This clause is not practical. Collateral is either given, ceded or pledged. Where given outright, it is reused in practice.

Agree, clause deleted

6.5 Collateral held in the form of cash must be in the form of bank deposits or bank issued money market instruments.

It is unclear from 6.5 whether the assets within a collateral arrangement need to be accessible to the fund within seven days or whether the assets within the collateral arrangement need to be capable of liquidation within seven days. For

Agree, clause deleted

example, the concept of collateral pledge (defined and established by the Security Services Act) is widely used in South Africa. In an arrangement where a counterparty pledges government bonds to a fund, the actual bonds may have sufficient liquidity to be liquidated within 7 days. It may take the fund longer than 7 days to access these bonds via the collateral pledge arrangement.

It is not clear why the collateral should be held in the form of bank deposits or bank issued money market instruments. Will it be the fund that holds the collateral? It can only be assumed that it is intended to limit collateral held by funds to liquid assets. Is this a duplication of paragraph 6.1? Why may collateral not be held in Treasury Bills, other money market instruments and commercial paper of similar liquidity? Cash is typically transferred on an out and out basis. The credit support agreement deals with and specifies the interest rate that the credit support provider will receive on the cash so posted.

6.6 Counterparties must manage the risk associated with the cash reinvestment and the credit quality of the reinvestment institution.

These Conditions cannot place an obligation on an entity not subject to these Conditions and thus propose that it be deleted. The Registrar should take comfort from the fact that counterparties are regulated entities. Furthermore a fund will not be able to monitor the risk management procedures of counterparties.

Agree, clause deleted

7. Reporting A fund‘s investment mandates with its relevant investment managers must ensure that the fund receives appropriate and timely information to enable proper management and monitoring of derivative positions and compliance with the relevant limits set out in regulation 28. Amongst others, a fund must receive the following information at least

Section 7 on Reporting – Will the certificates issued by CIS schemes mentioned in 7.4 stand in place of the requirements listed in 7.1, 7.2 and 7.3 or the certificates are over and above these requirements?

Agree, that the certificates will be in the place of these requirements Paragraph 7.4 has been deleted

quarterly:

7.4 certificates issued by collective investment schemes and long-term insurers, as contemplated in regulation 28(8), which must provide the information referred to in sub-paragraphs 1 to 3, except for policies contemplated in regulation 28(8)(b)(iii); and

Regulation 28(8) provides for the exclusion of collective investment schemes, linked policies and guaranteed policies when a fund applies the limits set out in the regulation if the fund has obtained an annual certificate of compliance with the limits set out in the regulation. Reporting on these assets on a look-through basis would defeat the purpose of obtaining a certificate. It will potentially increase costs in obtaining the information on a quarterly basis even if Regulation 28 compliance is confirmed on an annual basis with the issue of the certificate. The purpose of the exclusions is also to assist smaller funds with compliance where the funds are only invested in Regulation 28 compliant collective investment scheme portfolios and policies. It is submitted that the use of derivatives in collective investment schemes and by insurers are adequately regulated and the Registrar should take comfort from those protection mechanisms. It is therefore propose that this paragraph be deleted.

Agreed, paragraph deleted

7.5 an investment statement showing that the derivative instruments are valued and disclosed in compliance with international financial reporting standards.

ASISA an investment a statement showing confirming that the derivative instruments are valued and disclosed in compliance with international financial reporting standards. It is proposed that the paragraph be rephrased for the sake of clarity. It is also proposed that the reference to ―international financial reporting standards‖ be replaced with a reference to ―financial reporting standards‖ as that is the term defined by Regulation 28.

This provision has been deleted, valuation requirements are dealt with by the revised clauses 2(1)(d), 2(6) and 7(2)(d).

8. Investment policy statement The fund‘s investment policy statement must include the following:

Requirements contained in this section has been integrated into the revised section 2

8.3 a requirement that compliance to investment mandates must be monitored and reported at least monthly and that the board of the fund

The requirement for trustees to apply their mind (8.3) – we think this needs to be qualified,

See revised paragraph 7(1)

must apply its mind to understanding all risks related to the use of derivative instruments.

trustees have always asked what would it mean ―to apply our minds,‖ we suggest that this requirement read as follows; ―The board of trustees must apply its mind to understanding all risks related to the use of derivative instruments through acquiring the basic education on how derivatives can be used in their fund and putting in place a derivative policy to monitor their use. a requirement that compliance to investment mandates must be monitored and reported at least monthly quarterly and that the board of the fund must apply its mind to understanding all risks related to the use of derivative instruments. It is unusual to include a monitoring and reporting requirement in an investment policy statement. The reporting requirement should be aligned to quarterly as with the other reporting requirements contained in paragraph 7. The last part of paragraph 8.3 is a duplication of principles in paragraph 2 and should be deleted. The Registrar should take comfort from the fact that only investment managers regulated in terms of the Financial Advisory and Intermediary Services Act (―the FAIS Act‖) may manage the assets of a pension fund. The FAIS Act (Code of Conduct for Discretionary FSPs) requires that an investment manager enter into a written agreement with the pension fund and that such agreement must stipulate investment objectives and restrictions. Reporting in terms of FAIS is required at least on a quarterly basis.