derivative products- 241007

TRANSCRIPT

8/7/2019 Derivative Products- 241007

http://slidepdf.com/reader/full/derivative-products-241007 1/72

DERIVATIVE PRODUCTS

8/7/2019 Derivative Products- 241007

http://slidepdf.com/reader/full/derivative-products-241007 2/72

FLOW O

FPRESENTATION

� INTRODUCTION

G L OBAL F OREX MARKETS

� DERIVATIVE PRODUCTS

� REGU L ATORY INSTRUCTIONS

8/7/2019 Derivative Products- 241007

http://slidepdf.com/reader/full/derivative-products-241007 3/72

INTRODUCTION� MARKETS:

� Extreme Volatility� Expanding F ast� Basket of Products Available� Interconnectivity of Global Markets

� CUSTOMER� Higher Expectations� Ample Information Availability� Marketing by Rival Banks� Education, Advice & Access

8/7/2019 Derivative Products- 241007

http://slidepdf.com/reader/full/derivative-products-241007 4/72

INTRODUCTION� OUR BANK

Out of Sync With Customer Needs

L ack of Coordination Between the Various Armsof the Bank

L ack of Proactive Coordinated Marketing Effort� Need for sanction of F orward/Derivative L imits

on a Proactive basisL ack of Product Information & Knowledge of product usage

8/7/2019 Derivative Products- 241007

http://slidepdf.com/reader/full/derivative-products-241007 5/72

GL OBAL AVERAGE DAI L YF OREX TURNOVER

Instrument 2001 2004 2007

Spot 386 621 1005

F x. Swaps 656 944 1714

Others 158 315 491

Total 1200 1880 3210

$ in Bn

Geographical distribution (2007)

UK ± 34.1%(1359), US ± 16.6% (664), India ± 1.1% (34)

Source : BIS

8/7/2019 Derivative Products- 241007

http://slidepdf.com/reader/full/derivative-products-241007 6/72

GL OBAL AVERAGE DAI L Y

DERIVATIVE TURNOVER

Instrument 2001 2004 2007

F orex 67 140 291

Interest rate 489 1025 1686

Gaps 19 55 113

Total 575 1220 2090

$ in Bn

Geographical distribution (2007)

UK ± 42.5%(1081), US ± 23.8% (607), India ± 0.3% (8)

Source : BIS

8/7/2019 Derivative Products- 241007

http://slidepdf.com/reader/full/derivative-products-241007 7/72

FOREX TURNOVER

Trading Hours� 24 hour market� Sunday 5pm EST through F riday 4pm EST.� Trading begins in New Zealand, followed by Australia, Asia, the Middle

East, Europe, and AmericaSize

L argest financial market in the world� $3.2 trillion average daily turnover, equivalent to:

� More than 10 times the average daily turnover of global equity markets

� More than 35 times the average daily turnover of the NYSE� Nearly $500 a day for every man, woman, and child on earth� An annual turnover more than 10 times world GDP

8/7/2019 Derivative Products- 241007

http://slidepdf.com/reader/full/derivative-products-241007 8/72

F OREX TURNOVER

Structure� Decentralised, over-the-counter market, also known as the

'interbank' market� Main participants: Central Banks, commercial and investment banks,

hedge funds, corporations & private speculators� The free-floating currency system began in the early 1970's and wasofficially ratified in 1978

� Online trading began in the mid to late 1990'sMajor Markets� The US & UK markets account for just over 50% of turnover � Major markets: L ondon, New York, Tokyo� Trading activity is heaviest when major markets overlap5� Nearly two-thirds of NY activity occurs in the morning hours while

European markets are open

8/7/2019 Derivative Products- 241007

http://slidepdf.com/reader/full/derivative-products-241007 9/72

F OREX TURNOVER

Currencies

� The US dollar is involved in over 80% of all foreign exchangetransactions, equivalent to over US$2.7 trillion per day

Currency Pairs� Majors: EUR/USD, USD/JPY, GBP/USD, USD/CH F � Dollar bloc: USD/CAD, AUD/USD, NZD/USD� Major crosses: EUR/JPY, EUR/GBP, EUR/CH F

Average Turnover by Currency Pair � EUR / USD 27%, USD/JPY 13%, GBP/USD 12%, AUD/USD 6%

8/7/2019 Derivative Products- 241007

http://slidepdf.com/reader/full/derivative-products-241007 10/72

ATTRACTIONS

� The main enticements of currency dealing to private investors and attractions for short-term F orex trading are:

� 24-hour trading, 5 days a week with nonstop access to global F orex dealers.� An enormous liquid market making it easy to trade most currencies.� Volatile markets offering profit opportunities.� Standard instruments for controlling risk exposure.� The ability to profit in rising or falling markets.

L everaged trading with low margin requirements.� Many options for zero commission trading.

8/7/2019 Derivative Products- 241007

http://slidepdf.com/reader/full/derivative-products-241007 11/72

DERIVATIVE EXPOSURE

BANKS CURRENCYDERIVATIVES

INTEREST RATEDERIVATIVES

2006 2007 2006 2007

STANDARDCHARTERED BANK

47,021 114,504 215,374 457,204

CITI BANK 46,314 286,697 149,640 359,320

HSBC 126,691 212,219 179,024 349,636

ABN AMRO 10,636 16,576 142,451 249,303

DEUSTCHE BANK 16,163 46,473 207,187 387,320

SBI 9,672 49,939 97,968 186,611

ICICI BANK 42,858 73,237 221,576 293,981

SOURCE : BSRB

Rs In Crores

total to 07-08.xls

8/7/2019 Derivative Products- 241007

http://slidepdf.com/reader/full/derivative-products-241007 12/72

INDIAN RUPEE

8/7/2019 Derivative Products- 241007

http://slidepdf.com/reader/full/derivative-products-241007 13/72

EURO

8/7/2019 Derivative Products- 241007

http://slidepdf.com/reader/full/derivative-products-241007 14/72

YEN

8/7/2019 Derivative Products- 241007

http://slidepdf.com/reader/full/derivative-products-241007 15/72

CH F

8/7/2019 Derivative Products- 241007

http://slidepdf.com/reader/full/derivative-products-241007 16/72

G BP

8/7/2019 Derivative Products- 241007

http://slidepdf.com/reader/full/derivative-products-241007 17/72

USD 6 MTH LIBOR

8/7/2019 Derivative Products- 241007

http://slidepdf.com/reader/full/derivative-products-241007 18/72

MOVEMENT OF

EXCHANGE RATES� ECONOMIC F UNDAMENTALS Calendar.xls

� TECHNICA L ANAL YSIS

The method of predicting future currency price movements basedon observation of historical currency price movements.

� DEMAND AND SUPP L Y

� NEWS

8/7/2019 Derivative Products- 241007

http://slidepdf.com/reader/full/derivative-products-241007 19/72

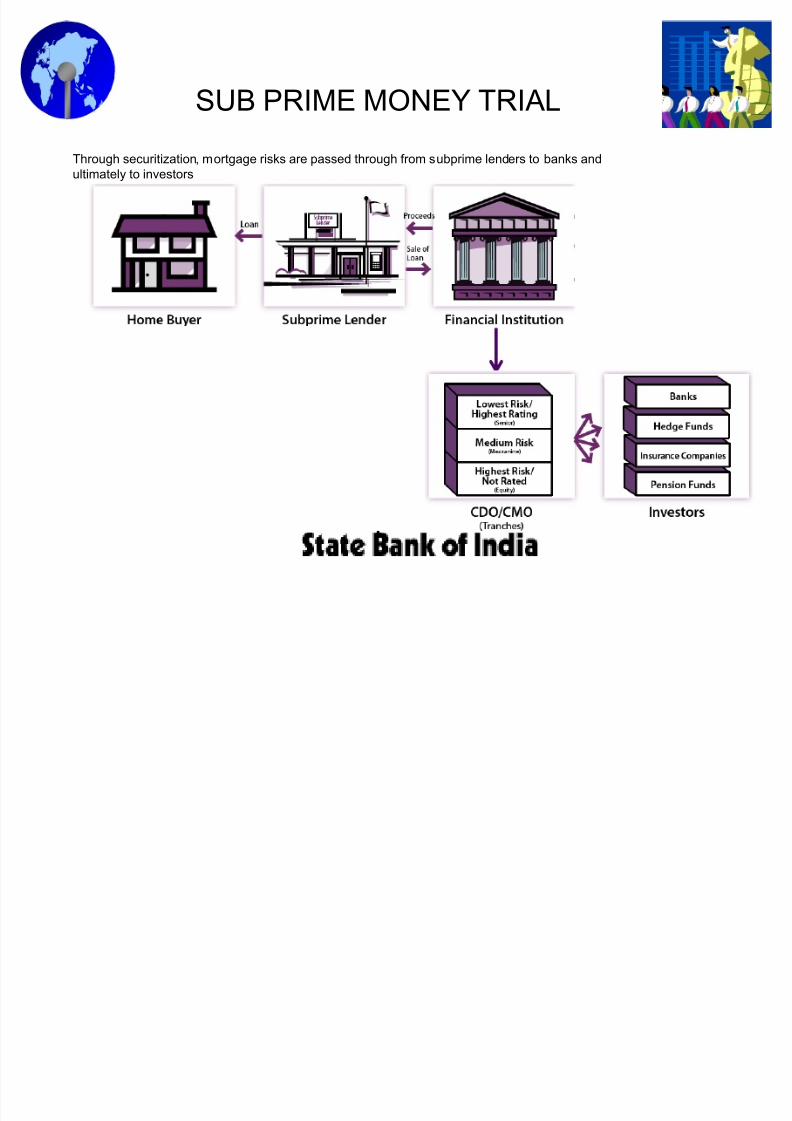

SUB PRIME LENDIN G

Subprime lending , also called "B-Paper", "near-prime" or "second chance" lending,is a general term that refers to the practice of making loans to borrowers who do notqualify for market interest rates because of problems with their credit history.

� Generally, subprime mortgages are for borrowers with credit scores of under 620.Subprime loans have higher rates than equivalent prime loans. How much higher depends on factors such as credit score, size of down payment, delinquencies historyof the borrower in the recent past etc. A subprime loan is also more likely to have aprepayment penalty.

� Subprime lending encompasses a variety of credit instruments, including subprimemortgages, subprime car loans, and subprime credit cards, among others.

8/7/2019 Derivative Products- 241007

http://slidepdf.com/reader/full/derivative-products-241007 20/72

Through securitization, mortgage risks are passed through from subprime lenders to banks andultimately to investors

SUB PRIME MONEY TRIA L

8/7/2019 Derivative Products- 241007

http://slidepdf.com/reader/full/derivative-products-241007 21/72

TREASURY PRODUCTSEXCHAN G E RATE

F ORWARD CONTRACTS� USD / INR F orward Contracts� Cross Currency F orward Contracts� Third Currency F orward Contracts

� OPTIONSPlain Vanilla Ratio SpreadRange F orwards Bull spreadSea Gull Bear SpreadStraddle Strangle

� SWAPSPrincipal only SwapCurrency and Interest rate Swap

8/7/2019 Derivative Products- 241007

http://slidepdf.com/reader/full/derivative-products-241007 22/72

TREASURY PRODUCTS

INTEREST RATE

F ORWARD RATE AGREEMENT

� SWAPS� Interest Rate Swaps ( F C)

� Interest Rate Swaps (INR ) ± Overnight Indexed Swaps

± INBMK Swaps

8/7/2019 Derivative Products- 241007

http://slidepdf.com/reader/full/derivative-products-241007 23/72

What are Derivatives?

F inancial instruments whose value is derivedfrom some other asset. Typically rates are basedon movement in the value of that asset.

Examples of DerivativesF utures & F orwards

� Swaps� Options

� Underlying Assets� Equity Shares� Interest rates

F oreign Exchange� Commodities

8/7/2019 Derivative Products- 241007

http://slidepdf.com/reader/full/derivative-products-241007 24/72

8/7/2019 Derivative Products- 241007

http://slidepdf.com/reader/full/derivative-products-241007 25/72

NO VIEW TAKEN

� A simple sell or buy of currency on the date of maturity of theexposure .

� Advantage ± simple , transparent and liquid.

� Disadvantage

If not view based, then open to risks due tovolatility

8/7/2019 Derivative Products- 241007

http://slidepdf.com/reader/full/derivative-products-241007 26/72

F ORWARD CONTRACT

F orward Contract is a contract to buy or sell a specified amountof currency at a specified price for a specific future date.

� Advantage ± Simple , liquid , less transparent and requiresno outlay of funds upfront.

� Disadvantage

� No participation in market volatility

� Profit and loss only crystallised on due date� Opportunity profit / opportunity loss unlimited

8/7/2019 Derivative Products- 241007

http://slidepdf.com/reader/full/derivative-products-241007 27/72

Option Basics

8/7/2019 Derivative Products- 241007

http://slidepdf.com/reader/full/derivative-products-241007 28/72

Options

An option is a financial contract in which the

buyer of the option has the right, but not the

obligation, to buy or sell an asset, at a pre-

specified price, on or upto a specified date.

8/7/2019 Derivative Products- 241007

http://slidepdf.com/reader/full/derivative-products-241007 29/72

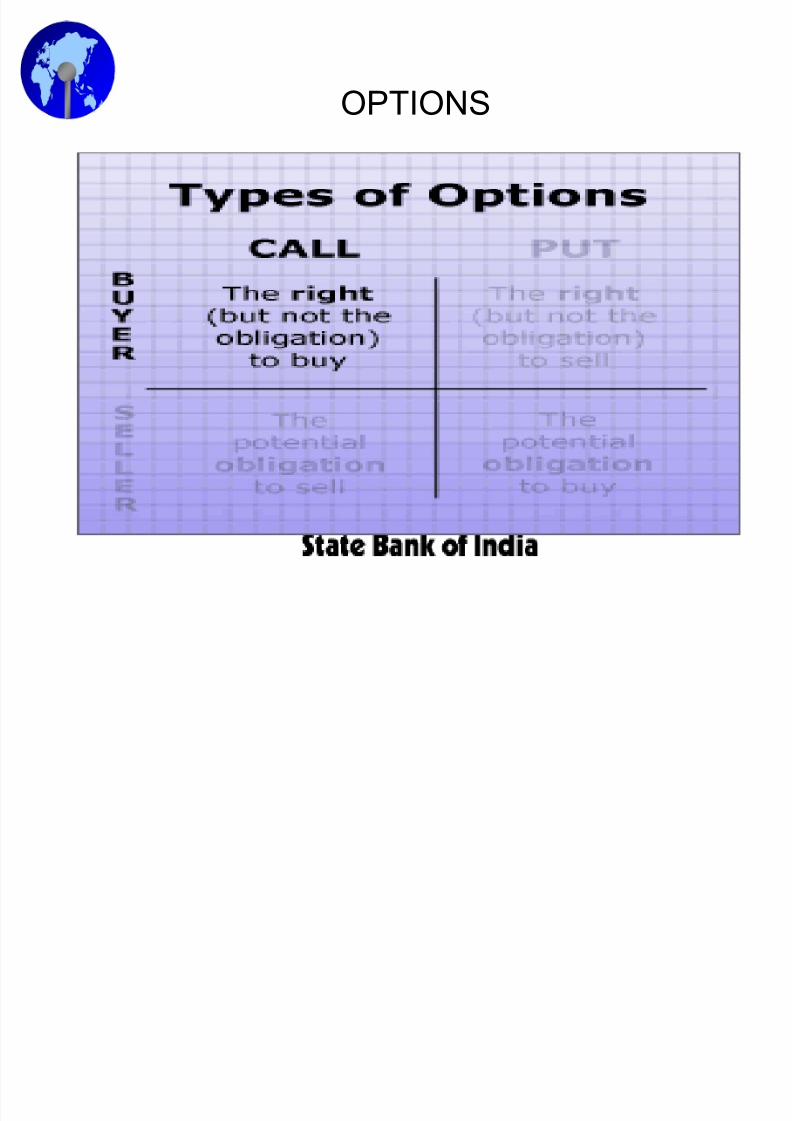

OPTIONS

C O N F I D E N C E

H I G H L O W

U S D

F I R M I N G

F O R W A R D

R A T E T O B E

L O C K E D I N

B U Y A N U S D

C A L L

O P T I O N

V

I

E

W

U S D F A L L I N G K E E P T H E

E X P O S U R E

O P E N

B U Y A N U S D

C A L L

O P T I O N

8/7/2019 Derivative Products- 241007

http://slidepdf.com/reader/full/derivative-products-241007 30/72

OPTIONS

8/7/2019 Derivative Products- 241007

http://slidepdf.com/reader/full/derivative-products-241007 31/72

Call Option

� An option but not an obligation to buy theunderlying at a pre-specified rate on / beforea pre-specified future date

� Buyer of the option pays a premium for thesame

� Seller / writer of the option receives thepremium from the buyer of the option

8/7/2019 Derivative Products- 241007

http://slidepdf.com/reader/full/derivative-products-241007 32/72

Put Option

� An option but not an obligation to sell theunderlying at a pre-specified rate on / beforea pre-specified future date

� Buyer of the option pays a premium for thesame

� Seller / writer of the option receives thepremium from the buyer of the option

8/7/2019 Derivative Products- 241007

http://slidepdf.com/reader/full/derivative-products-241007 33/72

European Option

� European Type ± which expire only on a particular pre-specified date

� E.g. An importer wants to hedge rising USD risk atthe current exchange rate of Rs 41.20 / USD. Hebuys a USD call option, where he has the right butnot the obligation to buy USD at Rs 41.20 / USD onlyat the end of 6 months

8/7/2019 Derivative Products- 241007

http://slidepdf.com/reader/full/derivative-products-241007 34/72

8/7/2019 Derivative Products- 241007

http://slidepdf.com/reader/full/derivative-products-241007 35/72

Strike Price

� Strike price is the price at which the optionhas been struck, I.e. the price at which theoption buyer has the option to buy / sell theunderlying for the call / put option it hasbought

8/7/2019 Derivative Products- 241007

http://slidepdf.com/reader/full/derivative-products-241007 36/72

Strike Price

� The premium of the option depends upon thestrike price

� Higher the strike price lower the premium inthe case of a call option and higher thepremium in case of a put option

� The strike price decides the ³moneyness´ of the option

8/7/2019 Derivative Products- 241007

http://slidepdf.com/reader/full/derivative-products-241007 37/72

At The Money Strike

� The strike price of the option is at the sameprice at the spot price

� In the case of currency options it is the sameas spot + forward premia for the maturity

8/7/2019 Derivative Products- 241007

http://slidepdf.com/reader/full/derivative-products-241007 38/72

In The Money Strike� In the money options - the strike price of the

option is below the the spot price, i.e. theoption is already in a profitable position

� In the case of currency options it is more thanas spot + forward premia for the maturity

8/7/2019 Derivative Products- 241007

http://slidepdf.com/reader/full/derivative-products-241007 39/72

Out Of The Money Strike� Out of the money options - the strike price of

the option is above the spot price, I.e. theoption is not profitable now, but if the pricemoves up, it would become in the money

� In the case of currency options it is more thanas spot + forward premia for the maturity

8/7/2019 Derivative Products- 241007

http://slidepdf.com/reader/full/derivative-products-241007 40/72

Volatility

� The volatility is a measure of uncertainty.

� The higher the uncertainty the higher theprice of the option

� Simply speaking, it is ³how many sleeplessnights will the traders spend, having taken aposition´

8/7/2019 Derivative Products- 241007

http://slidepdf.com/reader/full/derivative-products-241007 41/72

OPTIONS

F ACTORS A FF ECTING PREMIUM

� Type of Option (Call, Put)� Market Price

� Strike Price

� Time to expiry

� Volatility

� Interest rates in two currencies

8/7/2019 Derivative Products- 241007

http://slidepdf.com/reader/full/derivative-products-241007 42/72

Option Pricing ± BS Model

T

T f r r X S

d

T

T f r r X S

d

d N T

f r

S d N rT X p

d N rT X d N T

f r

S c

W

W

W

W

)2/2

()/ln(

2

)2/2

()/ln(

1 where

)1(e)2(e

)2

(e)1

(e

!

!

!

!

8/7/2019 Derivative Products- 241007

http://slidepdf.com/reader/full/derivative-products-241007 43/72

Option Strategies

8/7/2019 Derivative Products- 241007

http://slidepdf.com/reader/full/derivative-products-241007 44/72

Building BlocksBuy Call Option

� Unlimited profitL oss limited to premium

� Breakeven: When spot above strike issame as premium

Call Strike

8/7/2019 Derivative Products- 241007

http://slidepdf.com/reader/full/derivative-products-241007 45/72

Building BlocksBuy Put Option

� Unlimited profitL oss limited to premium

� Breakeven: When spot below strike issame as premium

Pu t Strike

8/7/2019 Derivative Products- 241007

http://slidepdf.com/reader/full/derivative-products-241007 46/72

Bull SpreadBuy a call at A, sell a call at higher strike B

� Profit limited to difference between two strikes

L oss limited to initial premium

� Breakeven: When spot above strike A issame as premium

A

B

8/7/2019 Derivative Products- 241007

http://slidepdf.com/reader/full/derivative-products-241007 47/72

Bear Spread� Sell a put at A, buy a put at higher strike B

� Profit limited to difference between strikes

L oss limited to net premium at B

� Breakeven: When spot below strike B is sameas premium

A

B

8/7/2019 Derivative Products- 241007

http://slidepdf.com/reader/full/derivative-products-241007 48/72

Exporter Range F orward

� Buy a put at A, sell a call at higher strike B

� Profit ± Unlimited in a falling market

L oss ± Unlimited in a rising market

A

B

8/7/2019 Derivative Products- 241007

http://slidepdf.com/reader/full/derivative-products-241007 49/72

Importer Range F orward

� Sell a put at A, buy a call at higher strike B

� Profit ± Unlimited in a rising marketL oss ± Unlimited in a falling market

A

B

8/7/2019 Derivative Products- 241007

http://slidepdf.com/reader/full/derivative-products-241007 50/72

Seagull Spread

� Buy call at B, sell call at C, sell put at A

� Profit ± L imited, greatest at or above C

L oss ±Unlimited in a falling market

A

C

B

8/7/2019 Derivative Products- 241007

http://slidepdf.com/reader/full/derivative-products-241007 51/72

Straddle� Buy a put at A, buy a call at same strike

� Profit ± Unlimited in a rising/falling market

L oss ± L imited to premium, greatest at A

A

8/7/2019 Derivative Products- 241007

http://slidepdf.com/reader/full/derivative-products-241007 52/72

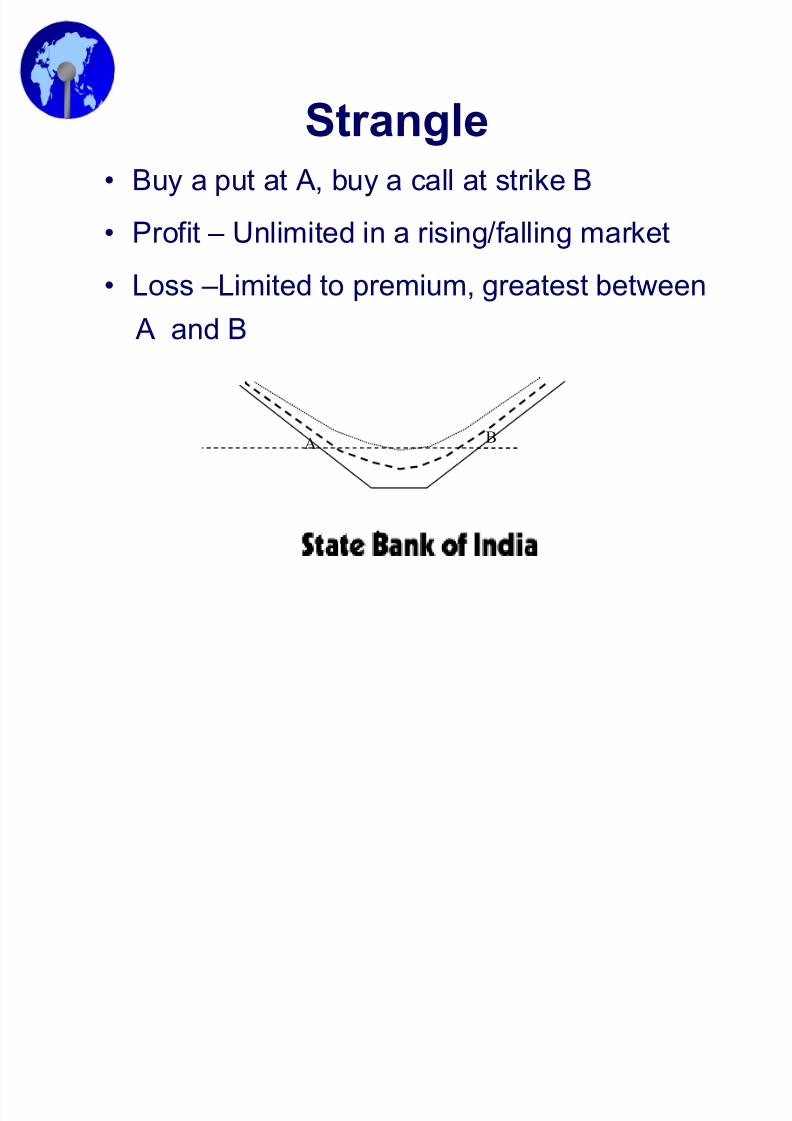

Strangle� Buy a put at A, buy a call at strike B

� Profit ± Unlimited in a rising/falling market

L oss ± L imited to premium, greatest between A and B

A B

8/7/2019 Derivative Products- 241007

http://slidepdf.com/reader/full/derivative-products-241007 53/72

Exotic Options

8/7/2019 Derivative Products- 241007

http://slidepdf.com/reader/full/derivative-products-241007 54/72

Barrier Options

� Barrier options are path-dependent options,which come in many flavors and forms, but

their key characteristic is that these types of options are either initiated (in the case of Knock-in options) or exterminated (in the

case of Knock-out options) upon reaching acertain barrier level; that is, they are either knocked in or knocked out.

8/7/2019 Derivative Products- 241007

http://slidepdf.com/reader/full/derivative-products-241007 55/72

Barrier Options

� They can be in the form of a call option or a putoption

� A ³Knock-In" barrier means that the underlying optionbecomes active once it crosses the barrier level

� A ³Knock-Out" barrier means that the underlying

option becomes inactive once it crosses the barrier level

8/7/2019 Derivative Products- 241007

http://slidepdf.com/reader/full/derivative-products-241007 56/72

Barrier Options� There are single barrier options and double barrier

options

� A single barrier option has one barrier that may beeither greater than or less than the strike price

� A double barrier option has barriers on either side of the strike (i.e. one trigger price is greater than thestrike and the other trigger price is less than thestrike)

8/7/2019 Derivative Products- 241007

http://slidepdf.com/reader/full/derivative-products-241007 57/72

Barrier Options

� Barrier options are cheaper than buying the plainvanilla option and we have a specific view about the

path that spot will take over the lifetime of thestructure.

� Intuitively, barrier options should be cheaper thantheir plain vanilla counterparts because they riskeither not being knocked in or being knocked out.

8/7/2019 Derivative Products- 241007

http://slidepdf.com/reader/full/derivative-products-241007 58/72

Barrier Options

� A double knockout option is cheaper than asingle knockout option because the doubleknockout has two trigger prices either of which could knock the option out of existence.How much cheaper a barrier option is

compared to the plain vanilla option dependson the location of the trigger.

8/7/2019 Derivative Products- 241007

http://slidepdf.com/reader/full/derivative-products-241007 59/72

Swaps

8/7/2019 Derivative Products- 241007

http://slidepdf.com/reader/full/derivative-products-241007 60/72

SWAPS

SWAP is a contract u al agreement to exchange specified cash

flows at f u tu re dates

Contracts that can be constr u cted with m u ltiple forwardcontracts

Some key u ses of Swaps

Cost saving or Yield enhancement on existing activity.� H edging of existing risk � M echanism to access the benefits available in the markets

which are otherwise closed to them

8/7/2019 Derivative Products- 241007

http://slidepdf.com/reader/full/derivative-products-241007 61/72

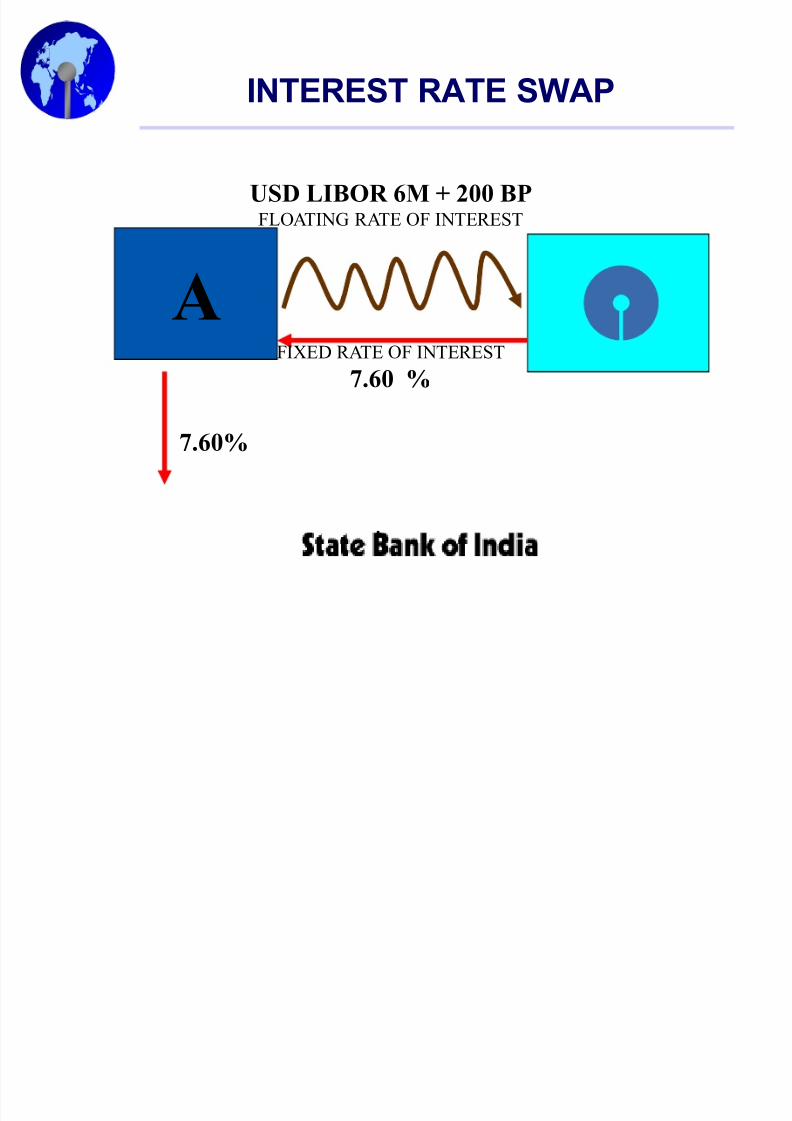

A

USD LIBOR 6M + 200 BPFLO AT ING R ATE OF INTE R EST

F IXED R ATE OF INTE R EST7.60 %

7.60%

INTEREST RATE SWAP

8/7/2019 Derivative Products- 241007

http://slidepdf.com/reader/full/derivative-products-241007 62/72

A INTE R EST R ATE D IFF ER E NTIAL

BET WEE N US D A ND INR IN INR

P RINCI PAL O NLY SWAP

USD P RINCI PAL

EQ UIV INR P RINCI PAL

EQ UIV INR P RINCI PAL

USD P RINCI PAL

USDCH F POS.xls

8/7/2019 Derivative Products- 241007

http://slidepdf.com/reader/full/derivative-products-241007 63/72

A

FLO AT ING R ATE OF INTE R EST IN US D

6M USD L IBO R

F IXED R ATE OF INTE R EST ININR 6.90%

USD P RINCI PAL 10 M io

EQ UIV INR P RINCI PAL 41.25 Crores

EQ UIV INR P RINCI PAL 41.25 Crores

USD P RINCI PAL 10 M io

CROSS CURRENCY INTEREST RATE SWAP

8/7/2019 Derivative Products- 241007

http://slidepdf.com/reader/full/derivative-products-241007 64/72

RE G ULATORY INSTRUCTIONS

� RBI allows the following Derivative instruments:

Forwards

Interest Rate Swaps

Cross Currency Interest rate Swaps

Cross Currency Options

Foreign Currency/Rupee Options

8/7/2019 Derivative Products- 241007

http://slidepdf.com/reader/full/derivative-products-241007 65/72

RE G ULATORY REQUIREMENTS

Necessary Board approval to u ndertake the transaction

The Derivative transaction sho u ld be u sed to cover expos u re on the

balance sheet

Size and tenor of the transaction sho u ld not be in excess of theu nderlying expos u re

The risks associated with the transaction sho u ld be u nderstood

There sho u ld be no net receipt of premi u m

The str u ctu re of the Derivative transaction sho u ld not enhance the risk profile

8/7/2019 Derivative Products- 241007

http://slidepdf.com/reader/full/derivative-products-241007 66/72

Business Potential

FCNRB / ECB/FCCB customers,

To manage the exchange rate risk

To manage the interest rate risk

Cost Reduction Structures

Rupee Loan Borrowers,

To manage interest rate risk

Exporters

Importers

8/7/2019 Derivative Products- 241007

http://slidepdf.com/reader/full/derivative-products-241007 67/72

TAR G ETIN G

� INTERNA L RATING - SB 3 OR BETTER

� TWO YEAR BANKING REL ATIONSHIP WITH A

SATIS F ACTORY CONDUCT O F ACCOUNT

� MINIMUM SIZE O F TRANSACTION PRE F ERRED

� SWAPS - USD 1 MIO� OPTIONS - USD 0.25 MIO

8/7/2019 Derivative Products- 241007

http://slidepdf.com/reader/full/derivative-products-241007 68/72

What are o u r expectations «

Customer Database - Preparation and sharing of information with Treasury

Margin Matrix ± Complete the exercise.Credit assessment by Branches and Presumptive Credit

Limits based on potential levels of business

ISDA Documentation for all potential customers

irrespective of whether trades are in the pipeline ornot

8/7/2019 Derivative Products- 241007

http://slidepdf.com/reader/full/derivative-products-241007 69/72

Treasury Marketing

Initiatives

F ormation of Regional Treasury Marketing Units to marketTreasury products

� Develop joint account plans with the Relationship Managers

� Mercury F x on line for customer F orex transactions

8/7/2019 Derivative Products- 241007

http://slidepdf.com/reader/full/derivative-products-241007 70/72

RO L ES - RTMU

L iaise with the Treas u ry and the Branch.

�M aintain contact with c u stomers, by way of seminars, personalmeetings, prod u ct presentations and daily c u rrency reports etc

P rovide inp u ts for specialized treas u ry prod u cts to the c u stomers.

Work towards a s u stained increase of market share/ penetration in termsof prod u cts and vol u mes.

Contin u ou sly monitor c u stomer portfolio

Gather market intelligence on client needs, prod u cts trends andcompetition .

8/7/2019 Derivative Products- 241007

http://slidepdf.com/reader/full/derivative-products-241007 71/72

Straight Through Processing ±

MercuryF

x SolutionsProvides on line rates for Customer Transactions

L imits� Margins

F acility of online chat for negotiation of ratesWould be implemented for all Treasury Products

� Would include F orex, Money, F ixed Income and Derivative ProductsData warehousing for Customer Relationship Management

� Customer wise turnover

� Profitability of account� Product bias� Customer behavior and risk tolerance� Mark to market and Potential future exposures

8/7/2019 Derivative Products- 241007

http://slidepdf.com/reader/full/derivative-products-241007 72/72

THANK YOU

C.VENKAT NAGESWAR

DGM, TMG, CORP CENTRE

TREASURY, MUMBAI