depreciation, cost recovery, amortization, and depletionatrc/mybooks/cwu/swaneys/winter 2017/4095...

TRANSCRIPT

Depreciation, Cost Recovery,Amortization, and Depletion

L E A R N I N G O B J E C T I V E S : After completing Chapter 8, you should be able to:

LO.1State the rationale for the cost consumption conceptand identify the relevant time periods fordepreciation, ACRS, and MACRS.

LO.2Determine the amount of cost recovery underMACRS.

LO.3Recognize when and how to make the § 179expensing election, calculate the amount of thededuction, and apply the effect of the election inmaking the MACRS calculation.

LO.4Identify listed property and apply the deductionlimitations on listed property and on luxuryautomobiles.

LO.5Determine when and how to use the alternativedepreciation system (ADS).

LO.6Report cost recovery deductions appropriately.

LO.7Identify intangible assets that are eligible foramortization and calculate the amount of thededuction.

LO.8Determine the amount of depletion expense, includ-ing being able to apply the alternative tax treatmentsfor intangible drilling and development costs.

LO.9Identify tax planning opportunities for cost recovery,amortization, and depletion.

C H A P T E R O U T L I N E

8-1 Depreciation and Cost Recovery, 8-38-1a Nature of Property, 8-38-1b Placed in Service Requirement, 8-38-1c Cost Recovery Allowed or Allowable, 8-38-1d Cost Recovery Basis for Personal Use Assets Converted

to Business or Income-Producing Use, 8-4

8-2 Modified Accelerated Cost Recovery System (MACRS):General Rules, 8-48-2a Personalty: Recovery Periods and Methods, 8-58-2b Realty: Recovery Periods and Methods, 8-88-2c Straight-Line Election, 8-9

8-3 Modified Accelerated Cost Recovery System (MACRS):Special Rules, 8-108-3a Additional First-Year Depreciation, 8-108-3b Election to Expense Assets (§ 179), 8-11

8-3c Business and Personal Use of Automobilesand Other Listed Property, 8-12

8-3d Alternative Depreciation System (ADS), 8-17

8-4 Reporting Procedures, 8-18

8-5 Amortization, 8-19

8-6 Depletion, 8-228-6a Intangible Drilling and Development Costs (IDCs), 8-238-6b Depletion Methods, 8-23

8-7 Tax Planning, 8-258-7a Cost Recovery, 8-258-7b Amortization, 8-278-7c Depletion, 8-278-7d Cost Recovery Tables, 8-28

C H A P T E R

8

THE BIG PICTURE

CALCULATING COST RECOVERY DEDUCTIONS

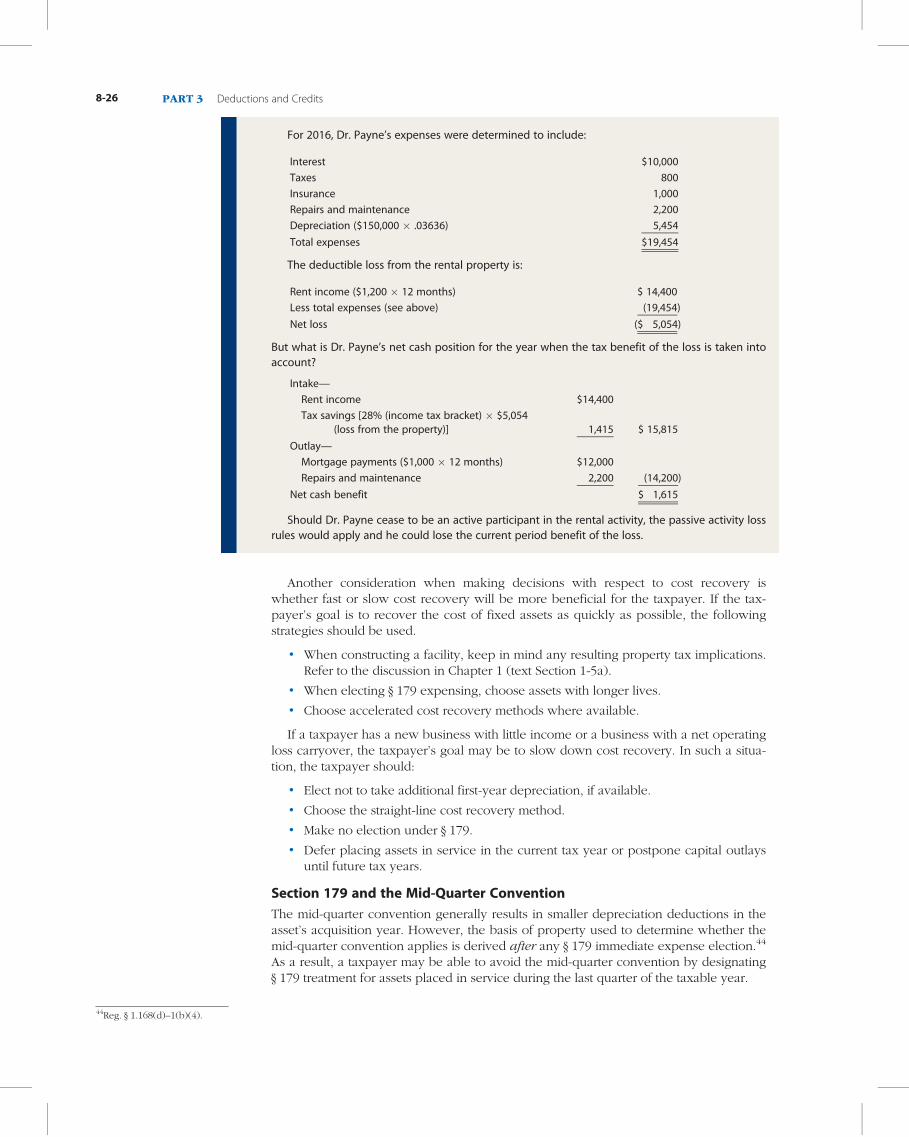

Dr. Cliff Payne purchased and placed in service $612,085 of new fixed assets in his dental practice during

the current year.

Office furniture and fixtures $ 70,000

Computers and peripheral equipment 67,085

Dental equipment 475,000

Using his financial reporting system, he concludes that the depreciation expense on Schedule C of Form

1040 is $91,298.

Office furniture and fixtures ($70,000 � 14.29%) $10,003

Computers and peripheral equipment ($67,085 � 20%) 13,417

Dental equipment ($475,000 � 14.29%) 67,878

$91,298

In addition, this year Dr. Payne purchased another personal residence for $300,000 and converted his

original residence to rental property. He also purchased a condo in the prior year for $170,000 near his

office that he is going to rent to a third party.

Has Dr. Payne correctly calculated the depreciation expense for his dental practice? Will he be able to

deduct any depreciation expense for his rental properties?

Read the chapter and formulate your response.

ª ERSLER DMITRY/SHUTTERSTOCK.COM

8-1

FRAMEWORK 1040 Tax Formula for Individuals

This chapter coversthe boldfaced portionsof the Tax Formulafor Individuals thatwas introduced inConcept Summary 3.1on p. 3-3. Belowthose portions arethe sections of Form1040 where the resultsare reported.

Income (broadly defined) .......................................................................................................... $xx,xxx

Less: Exclusions ..................................................................................................................... (x,xxx)

Gross income.......................................................................................................................... $xx,xxx

Less: Deductions for adjusted gross income......................................................................... (x,xxx)

FORM 1040 (p. 1)

12 Business income or (loss). Attach Schedule C or C-EZ . . . . . . . . . .

Adjusted gross income............................................................................................................ $xx,xxx

Less: The greater of total itemized deductions or the standard deduction................................ (x,xxx)

Personal and dependency exemptions ........................................................................... (x,xxx)

Taxable income ...................................................................................................................... $xx,xxx

Tax on taxable income (see Tax Tables or Tax Rate Schedules) ................................................. $ x,xxx

Less: Tax credits (including income taxes withheld and prepaid) ................................................ (xxx)

Tax due (or refund) ................................................................................................................. $ xxx

T he Internal Revenue Code allows a depreciation, cost recovery, amortization,or depletion deduction based on an asset’s cost. These deductions are applica-tions of the recovery of capital doctrine (discussed in Chapter 4). Cost recovery

deductions are based on the premise that the asset acquired (or improvementmade) benefits more than one accounting period. Otherwise, the expenditure isdeducted in the year incurred.1

Congress completely overhauled the depreciation rules in 1981 by creating theaccelerated cost recovery system (ACRS) , which shortened depreciable lives andallowed accelerated depreciation methods. In 1986, Congress made substantial modifi-cations to ACRS, which resulted in the modified accelerated cost recovery system(MACRS) . Tax professionals use the terms depreciation and cost recovery inter-changeably. Concept Summary 8.1 provides an overview of the various depreciationsystems and the time frames involved.

Concept Summary 8.1Depreciation and Cost Recovery: Relevant Time Periods

System Date Property Is Placed in Service

Pre-1981 depreciation Before January 1, 1981, and certain property placed in service afterDecember 31, 1980.

Accelerated cost recovery system (ACRS) After December 31, 1980, and before January 1, 1987.

Modified accelerated cost recovery system (MACRS) After December 31, 1986.

1See Chapter 6 and the discussion of capitalization versus expense.

8-2 PART 3 Deductions and Credits

The statutory changes that have taken place since 1980 have widened the gap thatexists between the accounting and tax versions of depreciation. The tax rules that existedprior to 1981 were much more compatible with generally accepted accounting principles.

This chapter focuses on the MACRS rules because they cover more recent propertyacquisitions (i.e., after 1986).2 The chapter concludes with a discussion of the amortizationof intangible property and startup expenditures and the depletion of natural resources.

Taxpayers may “write off” (deduct) the cost of certain assets that are used in a tradeor business or held for the production of income. A write-off may take the form ofdepreciation (or cost recovery), depletion, or amortization. Tangible assets, other thannatural resources, are depreciated. Natural resources, such as oil, gas, coal, and timber,are depleted. Intangible assets, such as copyrights and patents, are amortized. Gener-ally, no write-off is allowed for an asset that does not have a determinable useful life.

8-1 DEPRECIATION AND COST RECOVERY

8-1a Nature of PropertyProperty includes both realty (real property) and personalty (personal property). Realtygenerally includes land and buildings permanently affixed to the land. Personalty isdefined as any asset that is not realty.3 Do not confuse personalty (or personal property)with personal use property. Personal use property is any property (realty or personalty)that is held for personal use rather than for use in a trade or business or an income-producing activity. Cost recovery deductions are not allowed for personal use assets.

In summary, both realty and personalty can be either business use/income-producing property or personal use property. Examples include:

• A residence (realty that is personal use),

• An office building (realty that is business use),

• A dump truck (personalty that is business use), and

• Common wearing apparel (personalty that is personal use).

It is imperative that this distinction between the classification of an asset (realty orpersonalty) and the use to which the asset is put (business or personal) be understood.

Assets used in a trade or business or for the production of income are eligible for costrecovery if they are subject to wear and tear, decay or decline from natural causes, orobsolescence (e.g., an automobile that the taxpayer rents to third parties). Assets that donot decline in value on a predictable basis or that do not have a determinable useful life(e.g., land, stock, and antiques) are not eligible for cost recovery.

8-1b Placed in Service RequirementThe key date for the commencement of depreciation is the date an asset is placed inservice. This date, and not the purchase date of an asset, is relevant. This distinction isparticularly important for an asset that is purchased near the end of the tax year, butnot placed in service until after the beginning of the following tax year.

8-1c Cost Recovery Allowed or AllowableThe basis of cost recovery property is reduced by the cost recovery allowed (and by notless than the allowable amount). The allowed cost recovery is the cost recovery actuallydeducted, whereas the allowable cost recovery is the amount that could have beentaken under the applicable cost recovery method. If the taxpayer does not claim anycost recovery on property during a particular year, the basis of the property still isreduced by the amount of cost recovery that should have been deducted (the allowablecost recovery).

2§ 168. The terms depreciation and cost recovery are used interchangeably in thetext and in § 168. The ACRS rules and the pre-1981 rules are covered in theonline appendix Depreciation and the Accelerated Cost Recovery System (ACRS).

3Refer to Chapter 1 (text Section 1-5a) for further discussion.

LO.1

State the rationale for thecost consumption conceptand identify the relevant timeperiods for depreciation,ACRS, and MACRS.

CHAPTER 8 Depreciation, Cost Recovery, Amortization, and Depletion 8-3

8-1d Cost Recovery Basis for Personal Use AssetsConverted to Business or Income-Producing UseIf personal use assets are converted to business or income-producing use, the basis forcost recovery and for loss is the lower of the adjusted basis or the fair market value atthe time the property was converted. As a result of this lower-of basis rule, losses thatoccurred while the property was personal use property are not recognized for taxpurposes through the cost recovery of the property.

8-2 MODIFIED ACCELERATED COST RECOVERYSYSTEM (MACRS): GENERAL RULES

Under the modified accelerated cost recovery system (MACRS), the cost of an asset isrecovered over a predetermined period that generally is shorter than the useful life ofthe asset or the period that the asset is used to produce income. The MACRS rules weredesigned to encourage investment, improve productivity, and simplify the pertinent lawand its administration.

MACRS provides separate cost recovery systems for realty and personalty. Based oncost recovery periods (called class lives), methods, and conventions specified in the Inter-nal Revenue Code, the IRS provides tables that identify cost recovery allowances forpersonalty and for realty. Excerpts from those tables are provided in text Section 8-7d.

Concept Summary 8.2 provides an overview of the class lives, methods, and conven-tions that apply under MACRS.

E XAMP L E

1

On March 15, year 1, Jack purchased a copier, to use in his business, for $10,000. The copieris 5-year property, and Jack elected to use the straight-line method of cost recovery. Jackmade the election because the business was a new undertaking and he reasoned that inthe first few years of the business, a large cost recovery deduction was not needed.

Because the business was doing poorly, Jack did not even claim any cost recovery deductions in years3 and 4. In years 5 and 6, Jack deducted the proper amount of cost recovery. Therefore, the allowed costrecovery (cost recovery actually deducted) and the allowable cost recovery are computed as follows.

Cost Recovery Allowed Cost Recovery Allowable

Year 1 $1,000 $1,000

Year 2 2,000 2,000

Year 3 –0– 2,000

Year 4 –0– 2,000

Year 5 2,000 2,000

Year 6 1,000 1,000

If Jack sold the copier for $800 in year 7, he would recognize an $800 gain ($800 amount realized�$0 adjusted basis); the adjusted basis of the copier is zero ($10,000 cost� $10,000 total allowablecost recovery in years 1 through 6).

E XAMP L E

The Big Picture

2

Return to the facts of The Big Picture on p. 8-1. Five years ago, Dr. Payne purchased a personal resi-dence for $250,000. In the current year, with the housing market down, Dr. Payne found a largerhome that he acquired for his personal residence. Because of the downturn in the housing market,however, he was not able to sell his original residence and recover his purchase price of $250,000.The residence was appraised at $180,000.

Instead of continuing to try to sell the original residence, Dr. Payne converted it to rental prop-erty. The basis for cost recovery of the rental property is $180,000 because the fair market value isless than the adjusted basis. The $70,000 decline in value is deemed to be personal (because itoccurred while the property was held for personal use by Dr. Payne) and therefore nondeductible.

LO.2

Determine the amount of costrecovery under MACRS.

8-4 PART 3 Deductions and Credits

8-2a Personalty: Recovery Periods and Methods

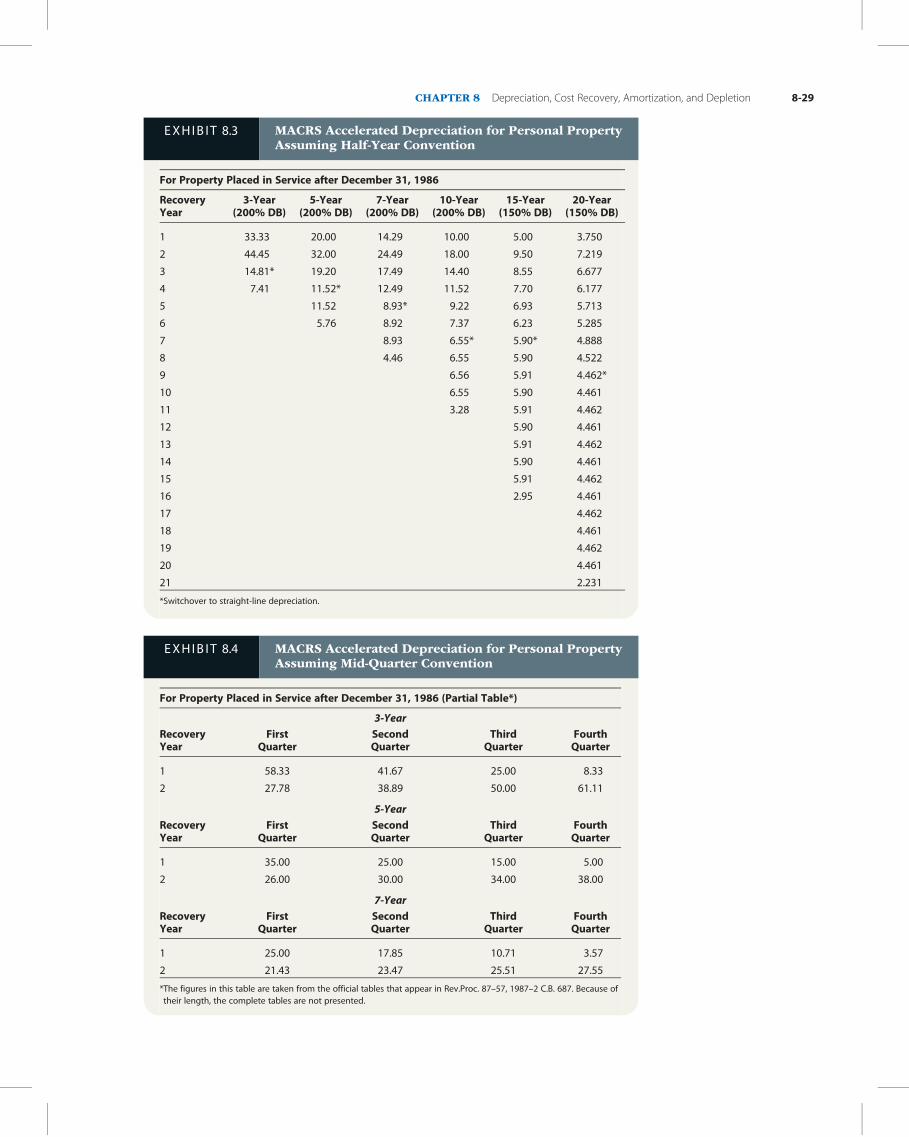

Classification of PropertyMACRS provides that the cost recovery basis of eligible personalty (and certain realty) isrecovered over 3, 5, 7, 10, 15, or 20 years. Property is classified by recovery periodunder MACRS through the use of Asset Depreciation Range (ADR) midpoint lives issuedby the IRS.4 See Exhibit 8.1 for examples of assets in each class.5

Accelerated depreciation is allowed for these six MACRS classes of property. Doubledeclining balance is used for the 3-, 5-, 7-, and 10-year classes, with a switchover tostraight-line depreciation when the latter computation yields a larger amount. Costrecovery for the 15- and 20-year classes is based on the 150-percent declining balance

E X H I B I T 8.1 Cost Recovery Periods: MACRS Personalty

PropertyClass

Generally Includes Assets with theFollowing ADR Lives Examples

3-year 4 years or less Tractor units for use over-the-road

A racehorse that is more than 2 years old, or any other horse that is more than12 years old, at the time it is placed in service

Special tools used in the manufacturing of motor vehicles, such as dies,fixtures, molds, and patterns

5-year More than 4 years and less than 10 years Automobiles and taxis

Light and heavy general-purpose trucks

Calculators and copiers

Computers and peripheral equipment

Rental appliances, furniture, carpets

7-year 10 years or more and less than 16 years Office furniture, fixtures, and equipment

Agricultural machinery and equipment

10-year 16 years or more and less than 20 years Vessels, barges, tugs, and similar water transportation equipment

Assets used for petroleum refining or for the manufacture of grain and grain millproducts, sugar and sugar products, or vegetable oils and vegetable oil products

Single-purpose agricultural or horticultural structures

15-year 20 years or more and less than 25 years Land improvements

Assets used for industrial steam and electric generation and/or distribution systems

Assets used in the manufacture of cement

20-year 25 years or more Farm buildings except single-purpose agricultural and horticultural structures

Water utilities

Concept Summary 8.2MACRS: Class Lives, Methods, and Conventions

Personalty Realty

Class lives 3 to 20 years Residential: 27.5 yearsNonresidential: 39 years

Method 200% declining balance for property with class livesless than 15 years

150% declining balance for property with15- or 20-year class lives

Straight-line

Convention Half-year or mid-quarter Mid-month

4Personalty is assigned to recovery classes based on asset depreciation range(ADR) midpoint lives (Rev.Proc. 87–56, 1987–2 C.B. 674). ADR lives gener-ally represent estimates of an asset’s useful economic life.

5§ 168(e).

CHAPTER 8 Depreciation, Cost Recovery, Amortization, and Depletion 8-5

method, with an appropriate straight-line switchover.6 The appropriate computationmethods and conventions are built into the tables, so it is not necessary to calculate theappropriate percentages.

To determine the amount of the cost recovery allowances, identify the asset by class andgo to the appropriate table for the percentage. The MACRS percentages for personaltyappear in Exhibit 8.3 (see text Section 8-7d). Concept Summary 8.3 provides an overview ofthe various conventions that apply under the MACRS statutory percentage method.

Taxpayers may elect the straight-line method to compute cost recovery allowancesfor each of these classes of property. Certain property is not eligible for accelerated costrecovery and must be depreciated under an alternative depreciation system (ADS). Boththe straight-line election and ADS are discussed later in the chapter.

MACRS views property as placed in service in the middle of the asset’s first year (thehalf-year convention ).7 Thus, for example, the statutory recovery period for propertywith a life of three years begins in the middle of the year an asset is placed in serviceand ends three years later. In practical terms, this means that taxpayers must wait anextra year to recover the full cost of depreciable assets. That is, the actual write-offs areclaimed over 4, 6, 8, 11, 16, and 21 years. MACRS also allows for a half-year of costrecovery in the year of sale or retirement.

FINANCIAL DISCLOSURE INSIGHTS Tax and Book Depreciation

A common book-tax difference relates to thedepreciation amounts that are reported for GAAP andFederal income tax purposes. Typically, tax depreciationdeductions are accelerated; that is, they are claimed inearlier reporting periods than is the case for financialaccounting purposes.

Almost every tax law change since 1980 has includeddepreciation provisions that accelerate the related deductionsrelative to the expenses allowed under GAAP. Accelerated

cost recovery deductions represent a means by which thetaxing jurisdiction infuses the business with cash flow createdby the reduction in the year’s tax liabilities.

For instance, recently, about one-quarter of General Elec-tric’s deferred tax liabilities related to depreciation differences.For Toyota’s and Ford’s depreciation differences, that amountwas about one-third. And for the trucking firm Ryder Systems,depreciation differences accounted for all but 1 percent of thedeferred tax liabilities.

E XAMP L E

3

Half-Year Convention

Kareem acquires a 5-year class asset on April 10, 2016, for $30,000. Kareem’s cost recovery deduc-tion for 2016 is computed as follows.

MACRS cost recovery [$30,000 � .20 (Exhibit 8.3)] $6,000

Concept Summary 8.3Statutory Percentage Method under MACRS

Personal Property Real Property*

Convention Half-year or mid-quarter Mid-month

Cost recovery deduction in theyear of disposition**

Half-year for year of sale orhalf-quarter for quarter of sale

Half-month for month of sale

*Straight-line method must be used.**A disposition can include a sale, exchange, abandonment, or retirement. For simplicity, we will assume a sale in this

chapter.

6§ 168(b). 7§ 168(d)(4)(A).

8-6 PART 3 Deductions and Credits

Mid-Quarter ConventionThe half-year convention arises from the simplifying presumption that assets gener-ally are acquired at an even pace throughout the tax year. However, Congress wasconcerned that taxpayers might defeat that presumption by placing large amounts ofproperty in service towards the end of the taxable year (and, by doing so, receive ahalf-year’s depreciation on those large, end-of-year acquisitions).

To inhibit this behavior, Congress added the mid-quarter convention that applies ifmore than 40 percent of the value of property other than eligible real estate (discussedin a later section) is placed in service during the last quarter of the year.8 Under this con-vention, property acquisitions are grouped by the quarter they were acquired for costrecovery purposes. Acquisitions during the first quarter are allowed 10.5 months (threeand one-half quarters) of cost recovery; the second quarter, 7.5 months (two and one-half quarters); the third quarter, 4.5 months (one and one-half quarters); and the fourthquarter, 1.5 months (one-half quarter). The percentages are shown in Exhibit 8.4.

E XAMP L E

5

Silver Corporation acquires the following new 5-year class property in 2016.

Property Acquisition Dates Cost

February 15 $ 200,000

July 10 400,000

December 5 600,000

Total $1,200,000

Under the statutory percentage method, Silver’s cost recovery allowances for the first two yearsare computed below. Because more than 40% ($600,000/$1,200,000 ¼ 50%) of the acquisitionsare in the last quarter, the mid-quarter convention applies.

2016

Mid-Quarter ConventionDepreciation (Exhibit 8.4)

TotalDepreciation

February 15 $200,000 � .35 $ 70,000

July 10 $400,000 � .15 60,000

December 5 $600,000 � .05 30,000

$160,000

2017

Mid-Quarter ConventionDepreciation (Exhibit 8.4)

TotalDepreciation

February 15 $200,000 � .26 $ 52,000

July 10 $400,000 � .34 136,000

December 5 $600,000 � .38 228,000

$416,000

Without the mid-quarter convention, Silver’s 2016 MACRS deduction would have been$240,000 [$1,200,000 � .20 (Exhibit 8.3)]. The mid-quarter convention slows down the taxpayer’savailable cost recovery deductions.

E XAMP L E

4

Assume the same facts as in Example 3. Kareem sells the asset on March 5, 2018. Kareem’s costrecovery deduction for 2018 is $2,880 [$30,000� 1=2 � :192 (Exhibit 8.3)].

8§ 168(d)(3).

CHAPTER 8 Depreciation, Cost Recovery, Amortization, and Depletion 8-7

When “mid-quarter” property is sold, the property is treated as though it were sold atthe midpoint of the quarter. So in the quarter when sold, cost recovery is allowed forone-half of the quarter.

8-2b Realty: Recovery Periods and MethodsUnder MACRS, the cost recovery period for residential rental real estate is 27.5 years, and thestraight-line method is used. Residential rental real estate includes property where 80 percentor more of the gross rental revenues are from residential units (e.g., an apartment building).Hotels, motels, and similar establishments are not residential rental property. Low-incomehousing is classified as residential rental real estate. Nonresidential real estate uses a recov-ery period of 39 years; it also is depreciated using the straight-line method.9

Some items of real property are not treated as real estate for purposes of MACRS. Forexample, single-purpose agricultural structures are in the 10-year MACRS class. Landimprovements are in the 15-year MACRS class.

All eligible real estate is depreciated using the mid-month convention .10 Regardlessof when the property is placed in service, it is deemed to have been placed in service at

E XAMP L E

6

Assume the same facts as in Example 5, except that Silver Corporation sells the $400,000 asset onNovember 30, 2017. The cost recovery allowance for 2017 is computed as follows (Exhibit 8.4).

February 15 $200,000 � .26 $ 52,000

July 10 $400,000 � .34 � (3.5/4) 119,000

December 5 $600,000 � .38 228,000

Total $399,000

E XAMP L E

The Big Picture

7

Return to the facts of The Big Picture on p. 8-1. If the placed-in-service date for the office furnitureand fixtures and computers and peripheral equipment is September 29 and the placed-in-servicedate for the dental equipment is October 3, Dr. Payne’s total cost recovery is computed as follows.

Office furniture and fixtures:

MACRS cost recovery $70,000 � .1071 (Exhibit 8.4) $ 7,497

Computers and peripheral equipment:

MACRS cost recovery $67,085 � .15 (Exhibit 8.4) 10,063

Dental equipment:

MACRS cost recovery $475,000 � .0357 (Exhibit 8.4) 16,958

Total cost recovery $ 34,518

Note the implications of the mid-quarter convention. If the dental equipment had been placedin service before October 1 (the beginning of the fourth quarter), the total cost recovery deductionwould have been $91,298 (p. 8-1).

TAX IN THE NEWS Cost Segregation

Cost segregation identifies certain assets withina commercial property that can qualify for shorter depreciationschedules than the building itself. The identified assets are clas-sified as 5-, 7-, or 15-year property, rather than 39-year property,as part of the building. This allows for greater accelerated

depreciation, which reduces taxable income and hence the taxliability.

For instance, a telecommunications system might be segre-gated from the building in which it is installed. This allows thesystem to be depreciated over 5 or 7 years, instead of 39 years.

9§§ 168(b), (c), and (e). A 31.5-year life is used for such property placed inservice before May 13, 1993.

10§ 168(d)(1).

8-8 PART 3 Deductions and Credits

the middle of the month. This allows for one-half month’s cost recovery for the monththe property is placed in service. If the property is sold before the end of the recoveryperiod, one-half month’s cost recovery is permitted for the month of sale (no matterwhen the property is sold).

Cost recovery is computed by multiplying the applicable rate (Exhibit 8.8) by the costrecovery basis.

8-2c Straight-Line ElectionAlthough MACRS requires straight-line depreciation for all eligible real estate, the tax-payer may elect to use the straight-line method for depreciable personal property.11

The property is depreciated using the class life (recovery period) of the asset witha half-year convention or a mid-quarter convention, whichever applies. The electionis available on a class-by-class and year-by-year basis (see Concept Summary 8.4).The percentages for the straight-line election with a half-year convention appear inExhibit 8.5.

E XAMP L E

8

Real Estate Cost Recovery

Alec acquired a building on April 1, 1999, for $800,000. If the building is classified as residentialrental real estate, the cost recovery deduction for 2016 is $29,088 (:03636� $800,000).

If the building is sold on October 7, 2016, the cost recovery deduction for 2016 is $23,028[:03636� (9:5=12)� $800,000]. (See Exhibit 8.8 for percentage.)

E XAMP L E

10

Mark acquired a building on November 19, 2016, for $1.2 million. If the building is classified asnonresidential real estate, the cost recovery deduction for 2016 is $3,852 [:00321� $1,200,000(Exhibit 8.8)]. The cost recovery deduction for 2017 is $30,768 [:02564� $1,200,000 (Exhibit 8.8)].

If the building is sold on May 21, 2017, the cost recovery deduction for 2017 is $11,538[:02564� (4:5=12)� $1,200,000 (Exhibit 8.8)].

E XAMP L E

9

Jane acquired a building on March 2, 1993, for $1 million. If the building is classified as non-residential real estate, the cost recovery deduction for 2016 is $31,740 (:03174 � $1,000,000).

If the building is sold on January 5, 2016, the cost recovery deduction for 2016 is $1,323[:03174� (:5=12)� $1,000,000]. (See Exhibit 8.8 for percentage.)

Concept Summary 8.4Straight-Line Election under MACRS

Personal Property Real Property*

Convention Half-year or mid-quarter Mid-month

Cost recovery deduction in theyear of disposition**

Half-year for year of saleor half-quarter for quarterof sale

Half-month for month of sale

Elective or mandatory Elective Mandatory

Breadth of election Class by class

*Straight-line method must be used.**A disposition can include a sale, exchange, abandonment, or retirement. For simplicity, we will assume a sale in this

chapter.

11§ 168(b)(5).

CHAPTER 8 Depreciation, Cost Recovery, Amortization, and Depletion 8-9

8-3 MODIFIED ACCELERATED COST RECOVERYSYSTEM (MACRS): SPECIAL RULES

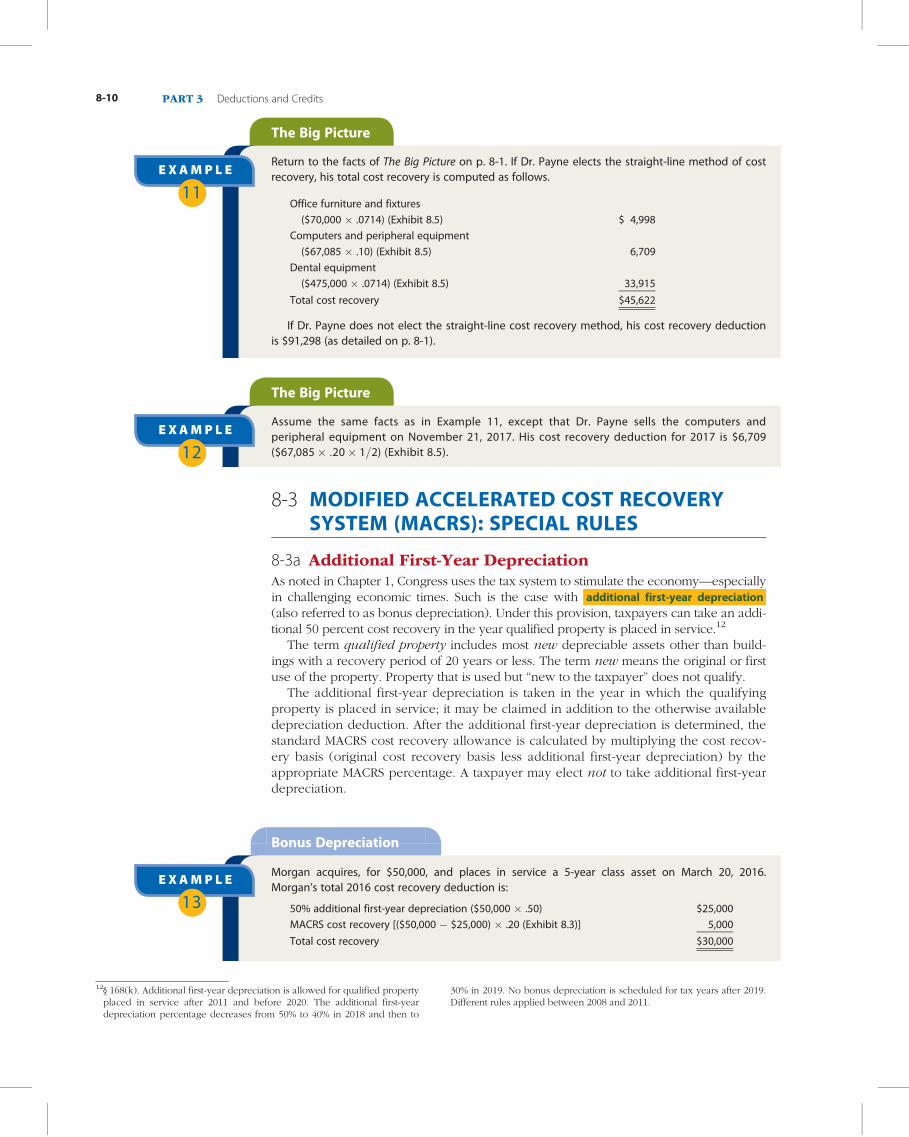

8-3a Additional First-Year DepreciationAs noted in Chapter 1, Congress uses the tax system to stimulate the economy—especiallyin challenging economic times. Such is the case with additional first-year depreciation(also referred to as bonus depreciation). Under this provision, taxpayers can take an addi-tional 50 percent cost recovery in the year qualified property is placed in service.12

The term qualified property includes most new depreciable assets other than build-ings with a recovery period of 20 years or less. The term new means the original or firstuse of the property. Property that is used but “new to the taxpayer” does not qualify.

The additional first-year depreciation is taken in the year in which the qualifyingproperty is placed in service; it may be claimed in addition to the otherwise availabledepreciation deduction. After the additional first-year depreciation is determined, thestandard MACRS cost recovery allowance is calculated by multiplying the cost recov-ery basis (original cost recovery basis less additional first-year depreciation) by theappropriate MACRS percentage. A taxpayer may elect not to take additional first-yeardepreciation.

E XAMP L E

The Big Picture

12

Assume the same facts as in Example 11, except that Dr. Payne sells the computers andperipheral equipment on November 21, 2017. His cost recovery deduction for 2017 is $6,709($67,085� :20� 1=2) (Exhibit 8.5).

E XAMP L E

The Big Picture

11

Return to the facts of The Big Picture on p. 8-1. If Dr. Payne elects the straight-line method of costrecovery, his total cost recovery is computed as follows.

Office furniture and fixtures

($70,000 � .0714) (Exhibit 8.5) $ 4,998

Computers and peripheral equipment

($67,085 � .10) (Exhibit 8.5) 6,709

Dental equipment

($475,000 � .0714) (Exhibit 8.5) 33,915

Total cost recovery $45,622

If Dr. Payne does not elect the straight-line cost recovery method, his cost recovery deductionis $91,298 (as detailed on p. 8-1).

E XAMP L E

13

Bonus Depreciation

Morgan acquires, for $50,000, and places in service a 5-year class asset on March 20, 2016.Morgan’s total 2016 cost recovery deduction is:

50% additional first-year depreciation ($50,000 � .50) $25,000

MACRS cost recovery [($50,000 � $25,000) � .20 (Exhibit 8.3)] 5,000

Total cost recovery $30,000

12§ 168(k). Additional first-year depreciation is allowed for qualified propertyplaced in service after 2011 and before 2020. The additional first-yeardepreciation percentage decreases from 50% to 40% in 2018 and then to

30% in 2019. No bonus depreciation is scheduled for tax years after 2019.Different rules applied between 2008 and 2011.

8-10 PART 3 Deductions and Credits

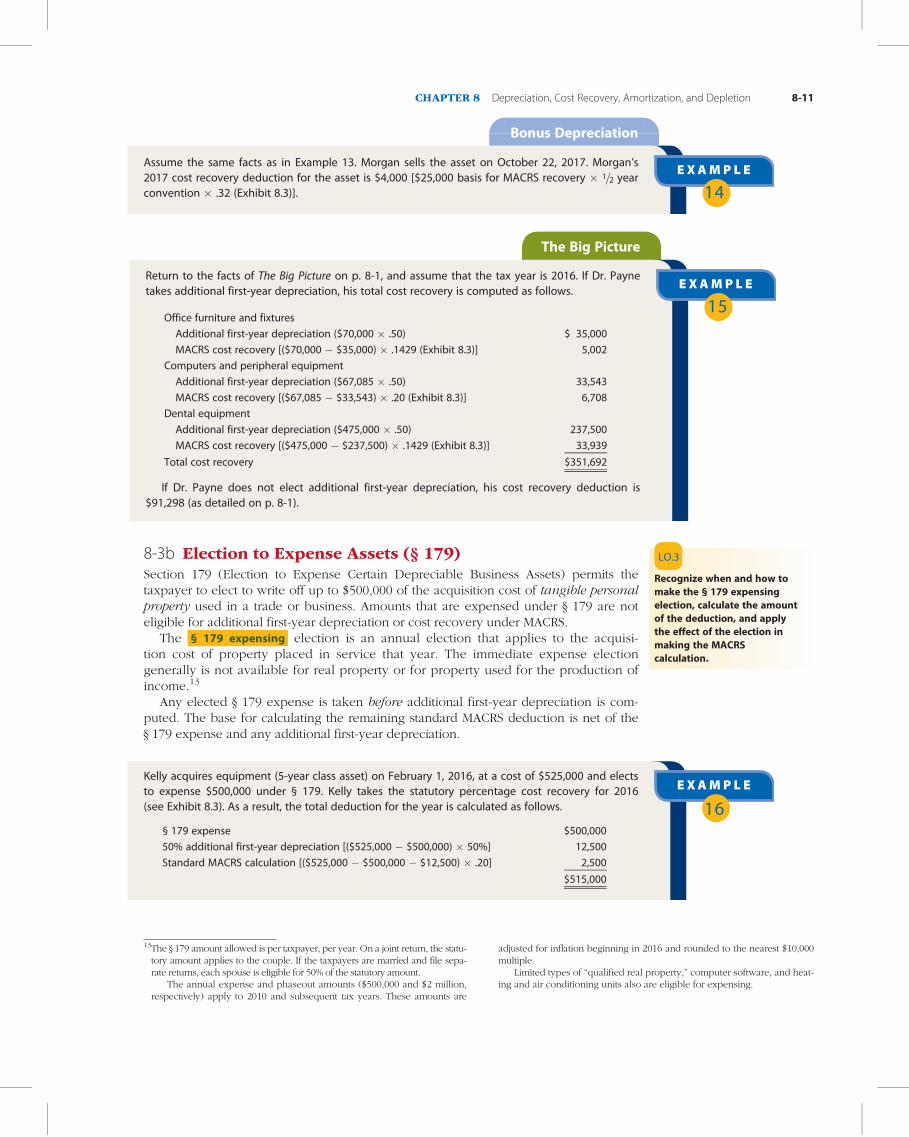

8-3b Election to Expense Assets (§ 179)Section 179 (Election to Expense Certain Depreciable Business Assets) permits thetaxpayer to elect to write off up to $500,000 of the acquisition cost of tangible personalproperty used in a trade or business. Amounts that are expensed under § 179 are noteligible for additional first-year depreciation or cost recovery under MACRS.

The § 179 expensing election is an annual election that applies to the acquisi-tion cost of property placed in service that year. The immediate expense electiongenerally is not available for real property or for property used for the production ofincome.13

Any elected § 179 expense is taken before additional first-year depreciation is com-puted. The base for calculating the remaining standard MACRS deduction is net of the§ 179 expense and any additional first-year depreciation.

E XAMP L E

The Big Picture

15

Return to the facts of The Big Picture on p. 8-1, and assume that the tax year is 2016. If Dr. Paynetakes additional first-year depreciation, his total cost recovery is computed as follows.

Office furniture and fixtures

Additional first-year depreciation ($70,000 � .50) $ 35,000

MACRS cost recovery [($70,000 � $35,000) � .1429 (Exhibit 8.3)] 5,002

Computers and peripheral equipment

Additional first-year depreciation ($67,085 � .50) 33,543

MACRS cost recovery [($67,085 � $33,543) � .20 (Exhibit 8.3)] 6,708

Dental equipment

Additional first-year depreciation ($475,000 � .50) 237,500

MACRS cost recovery [($475,000 � $237,500) � .1429 (Exhibit 8.3)] 33,939

Total cost recovery $351,692

If Dr. Payne does not elect additional first-year depreciation, his cost recovery deduction is$91,298 (as detailed on p. 8-1).

E XAMP L E

14

Bonus Depreciation

Assume the same facts as in Example 13. Morgan sells the asset on October 22, 2017. Morgan’s2017 cost recovery deduction for the asset is $4,000 [$25,000 basis for MACRS recovery � 1=2 yearconvention � .32 (Exhibit 8.3)].

E XAMP L E

16

Kelly acquires equipment (5-year class asset) on February 1, 2016, at a cost of $525,000 and electsto expense $500,000 under § 179. Kelly takes the statutory percentage cost recovery for 2016(see Exhibit 8.3). As a result, the total deduction for the year is calculated as follows.

§ 179 expense $500,000

50% additional first-year depreciation [($525,000 � $500,000) � 50%] 12,500

Standard MACRS calculation [($525,000 � $500,000 � $12,500) � .20] 2,500

$515,000

LO.3

Recognize when and how tomake the § 179 expensingelection, calculate the amountof the deduction, and applythe effect of the election inmaking the MACRScalculation.

13The § 179 amount allowed is per taxpayer, per year. On a joint return, the statu-tory amount applies to the couple. If the taxpayers are married and file sepa-rate returns, each spouse is eligible for 50% of the statutory amount.

The annual expense and phaseout amounts ($500,000 and $2 million,respectively) apply to 2010 and subsequent tax years. These amounts are

adjusted for inflation beginning in 2016 and rounded to the nearest $10,000multiple.

Limited types of “qualified real property,” computer software, and heat-ing and air conditioning units also are eligible for expensing.

CHAPTER 8 Depreciation, Cost Recovery, Amortization, and Depletion 8-11

Annual LimitationsTwo additional limitations apply to the amount deductible under § 179. First, the ceil-ing amount on the deduction ($500,000) is reduced dollar for dollar when § 179 prop-erty placed in service during the taxable year exceeds a maximum amount ($2,010,000in 2016; $2 million in 2015). Second, the § 179 deduction cannot exceed the taxpayer’strade or business taxable income, computed without regard to the § 179 amount.

Any § 179 amount in excess of taxable income is carried forward to future taxable yearsand added to other amounts eligible for expensing. For 2016, the § 179 amount eligible forexpensing in a carryforward year is limited to the lesser of (1) the statutory dollar amount($500,000) reduced by the cost of § 179 property placed in service in excess of $2,010,000in the carryforward year or (2) business taxable income in the carryforward year.

Effect on BasisThe basis of the property for cost recovery purposes is reduced by the § 179 amountafter accounting for the current-year amount of property placed in service in excess ofthe specified maximum amount ($2,010,000 for 2016). This adjusted amount does notreflect any business income limitation.

Conversion to Personal UseConversion of the expensed property to personal use at any time results in recaptureincome (see Chapter 14). A property is converted to personal use if it is not usedpredominantly in a trade or business.14

8-3c Business and Personal Use of Automobilesand Other Listed PropertyLimits exist on MACRS deductions for automobiles and other listed property that areused for both personal and business purposes.15 If the listed property is predominantlyused for business, the taxpayer can use the MACRS tables to recover the cost. In caseswhere the property is not predominantly used for business, the cost is recovered usingthe straight-line method.

ETHICS & EQUITY Section 179 Limitation

Joe Moran worked in the construction businessthroughout most of his career. In June of the current year, hesold his interest in Ajax Enterprises LLC for a profit of $300,000.Shortly thereafter, Joe started his own business, which involvesthe redevelopment of distressed residential real estate.

In connection with his new business venture, Joepurchased a dump truck at a cost of $70,000. The newbusiness struggled and showed a net operating loss for theyear. Joe is considering expensing the $70,000 cost of thetruck under §179 on this year’s tax return. Evaluate Joe’s plan.

E XAMP L E

17

Jill owns a computer service and operates it as a sole proprietorship. In 2016, taxable income is$138,000 before considering any § 179 deduction. If Jill spends $2.3 million on new equipment,her § 179 expense deduction for the year is computed as follows.

§ 179 deduction before adjustment $ 500,000

Less: Dollar limitation reduction ($2,300,000 � $2,010,000) (290,000)

Remaining § 179 deduction $ 210,000

Business income limitation $ 138,000

§ 179 deduction allowed $ 138,000

§ 179 deduction carryforward ($210,000 � $138,000) $ 72,000

14See Reg. § 1.179–1(e) and related examples. 15§ 280F.

LO.4

Identify listed propertyand apply the deductionlimitations on listed propertyand on luxury automobiles.

8-12 PART 3 Deductions and Credits

Listed property includes:

• Any passenger automobile.

• Any other property used as a means of transportation.

• Any property of a type generally used for purposes of entertainment, recreation,or amusement.

• Any computer or peripheral equipment, with the exception of equipment usedexclusively at a regular business establishment, including a qualifying home office.

• Any other property specified in the Regulations.

Automobiles and Other Listed Property Used Predominantly in BusinessFor listed property to be considered as predominantly used in business, its businessusage must exceed 50 percent.16 The use of listed property for production of incomedoes not qualify as business use for purposes of the more-than-50% test. However,both production of income and business use percentages are used to compute the costrecovery deduction.

In determining the percentage of business usage for listed property, a mileage-basedpercentage is used for automobiles. For other listed property, one employs the mostappropriate unit of time (e.g., hours) for which the property actually is used (rather thanits availability for use).17

Limits on Cost Recovery for AutomobilesThe law places special limitations on cost recovery deductions for passenger automo-biles. These statutory dollar limits were imposed on passenger automobiles becauseof the belief that the tax system was being used to underwrite automobiles whose costand luxury far exceeded what was needed for the taxpayer’s business use.

A passenger automobile is any four-wheeled vehicle manufactured for use on pub-lic streets, roads, and highways with an unloaded gross vehicle weight (GVW) ratingof 6,000 pounds or less.18 This definition specifically excludes vehicles used directlyin the business of transporting people or property for compensation, such as taxicabs,ambulances, hearses, and trucks and vans as prescribed by the Regulations.

The following “luxury auto” depreciation limits apply.19

Date Placedin Service First Year Second Year Third Year

Fourth andLater Years

2015* $3,160 $5,100 $3,050 $1,875

2012–2014 $3,160 $5,100 $3,050 $1,875

2010–2011 $3,060 $4,900 $2,950 $1,775

2009 $2,960 $4,800 $2,850 $1,775

* Because the 2016 indexed amounts are not yet available, the 2015 amounts are used in the Examples and end-of-chapterproblem materials.

E XAMP L E

18

On September 1, 2016, Emma places in service listed 5-year recovery property. The property cost$10,000. She elects not to take any available additional first-year depreciation.

If Emma uses the property 40% for business and 25% for the production of income, the propertyis not considered as predominantly used for business. The cost is recovered using straight-line costrecovery. Emma’s cost recovery allowance for the year is $650 ($10,000� :10� 65%).

If, however, Emma uses the property 60% for business and 25% for the production of income,the property is considered as used predominantly for business. Therefore, she may use the statutorypercentage method. Emma’s cost recovery allowance for the year is $1,700 ($10,000� :20� 85%).

16§ 280F(b)(3).17Reg. § 1.280F–6T(e).

18§ 280F(d)(5).19§ 280F(a)(1); Rev.Proc. 2015–19 (2015–8 I.R.B.656).

CHAPTER 8 Depreciation, Cost Recovery, Amortization, and Depletion 8-13

For an automobile placed in service prior to 2009, the limitation for subsequent years’cost recovery is based on the limits for the year the automobile was placed in service.20

In the event a passenger automobile used predominantly for business qualifies for addi-tional first-year depreciation (i.e., new property), the first-year recovery limitation isincreased by $8,000.21 Therefore, for acquisitions made in 2015, the initial-year cost recov-ery limitation increases from $3,160 to $11,160 ($3,160 þ $8,000).

There are also separate cost recovery limitations for trucks and vans and for electric auto-mobiles. Because these limitations are applied in the same manner as those imposed onpassenger automobiles, these additional limitations are not discussed further in this chapter.

The luxury auto limits are imposed before any percentage reduction for personaluse. In addition, the limitation in the first year includes any amount the taxpayer electsto expense under § 179.22 If the passenger automobile is used partly for personal use,the personal use percentage is ignored for the purpose of determining the unrecoveredcost available for deduction in later years.

The cost recovery limitations are maximum amounts. If the regular MACRS calcula-tion produces a lesser amount of cost recovery, the lesser amount is used.

The luxury auto limitations apply only to passenger automobiles and not to otherlisted property.

E XAMP L E

19

On July 1, 2016, Dan places in service a new automobile that cost $40,000. He does not elect§ 179 expensing, and he elects not to take any available additional first-year depreciation. The caris used 80% for business and 20% for personal use in each tax year. Dan chooses the MACRS200% declining-balance method of cost recovery (the auto is a 5-year asset).

The depreciation computation for 2016 through 2021 is summarized in the table below. Thecost recovery allowed is the lesser of the MACRS amount or the recovery limitation.

Year MACRS AmountRecovery

LimitationDepreciation

Allowed

2016 $6,400 $2,528 $2,528

($40,000 � .2000 � 80%) ($3,160 � 80%)

2017 $10,240 $4,080 $4,080

($40,000 � .3200 � 80%) ($5,100 � 80%)

2018 $6,144 $2,440 $2,440

($40,000 � .1920 � 80%) ($3,050 � 80%)

2019 $3,686 $1,500 $1,500

($40,000 � .1152 � 80%) ($1,875 � 80%)

2020 $3,686 $1,500 $1,500

($40,000 � .1152 � 80%) ($1,875 � 80%)

2021 $1,843 $1,500 $1,500

($40,000 � .0576 � 80%) ($1,875 � 80%)

If Dan continues to use the car after 2021, his cost recovery is limited to the lesser of the recoverable basisor the recovery limitation (i.e., $1,875� business use percentage). For this purpose, the recoverable basisis computed as if the full recovery limitation was allowed even if it was not. Thus, the recoverable basis asof January 1, 2022, is $23,065 ($40,000� $3,160� $5,100� $3,050� $1,875� $1,875� $1,875).

If Dan takes additional first-year depreciation, the calculated amount of additional first-yeardepreciation is $16,000 ($40,000� 50%� 80%). However, the deduction would be limited to$8,928 [($8,000þ $3,160)� 80%].

E XAMP L E

20

On April 2, 2016, Gail places in service a used automobile that cost $10,000. The car is alwaysused 70% for business and 30% for personal use. The cost recovery allowance for 2016 is $1,400($10,000 � .20 MACRS table factor � 70%), and not $2,212 ($3,160 passenger auto maximum � 70%).

20Cost recovery limitations for years prior to 2009 are found in IRS Publication 463.21§ 168(k)(2)(F). The $8,000 amount will decrease to $6,400 in 2018 and $4,800 in

2019. No increase in the first-year recovery limitation will be allowed after 2019.

22§ 280F(d)(1).

8-14 PART 3 Deductions and Credits

Special LimitationA $25,000 limit applies for the § 179 deduction when the luxury auto limits do not apply.The limit is in effect for sport utility vehicles (SUVs) with an unloaded GVW rating ofmore than 6,000 pounds and not more than 14,000 pounds.23

Automobiles and Other Listed Property Not Used Predominantlyin BusinessFor automobiles and other listed property not used predominantly in business in theyear of acquisition (i.e., 50 percent or less), the straight-line method under the alterna-tive depreciation system is required (see text Section 8-3d).24 Under this system, thestraight-line recovery period for automobiles is five years. However, the cost recoveryallowance for any passenger automobile cannot exceed the luxury auto amount.

The straight-line method is used even if, at some later date, the business usage of theproperty increases to more than 50 percent. In that case, the amount of cost recoveryreflects the increase in business usage.

Change from Predominantly Business UseIf the business use percentage of listed property falls to 50 percent or less after the yearthe property is placed in service, the property is subject to cost recovery recapture. Theamount required to be recaptured and included in the taxpayer’s ordinary income is theexcess cost recovery.

Excess cost recovery is the excess of the cost recovery deduction taken in prior yearsusing the statutory percentage method over the amount that would have been allowedif the straight-line method had been used since the property was placed in service.25

E XAMP L E

21

During 2016, Jay acquires and places in service a new SUV that cost $70,000 and has a GVWof 8,000 pounds. Jay uses the vehicle 100% of the time for business use. The total deductionfor 2016 with respect to the SUV is computed as follows.

§ 179 expense $25,000

50% additional first-year depreciation [($70,000 � $25,000) � 50%] 22,500

Standard MACRS calculation [($70,000 � $25,000 � $22,500) � .20 (Exhibit 8.3)] 4,500

$52,000

E XAMP L E

22

Auto Not Predominantly Used in Business

On July 27, 2016, Fred places in service an automobile that cost $20,000. The auto is used 40% forbusiness and 60% for personal use. The cost recovery allowance for 2016 is $800 [$20,000 � .10(Exhibit 8.7) � 40%].

E XAMP L E

23

Assume the same facts as in Example 22, except that the automobile cost $50,000. The cost recov-ery allowance for 2016 is $1,264 [$50,000 � .10 (Exhibit 8.7) ¼ $5,000 (limited to $3,160) � 40%].

E XAMP L E

24

Assume the same facts as in Example 22, except that in 2017, Fred uses the automobile 70% forbusiness and 30% for personal use. Fred’s cost recovery allowance for 2017 is $2,800 [$20,000 �.20 (Exhibit 8.7) � 70%], which is less than 70% of the second-year limit.

23§ 179(b)(6).24§ 280F(b)(1).

25§ 280F(b)(2).

CHAPTER 8 Depreciation, Cost Recovery, Amortization, and Depletion 8-15

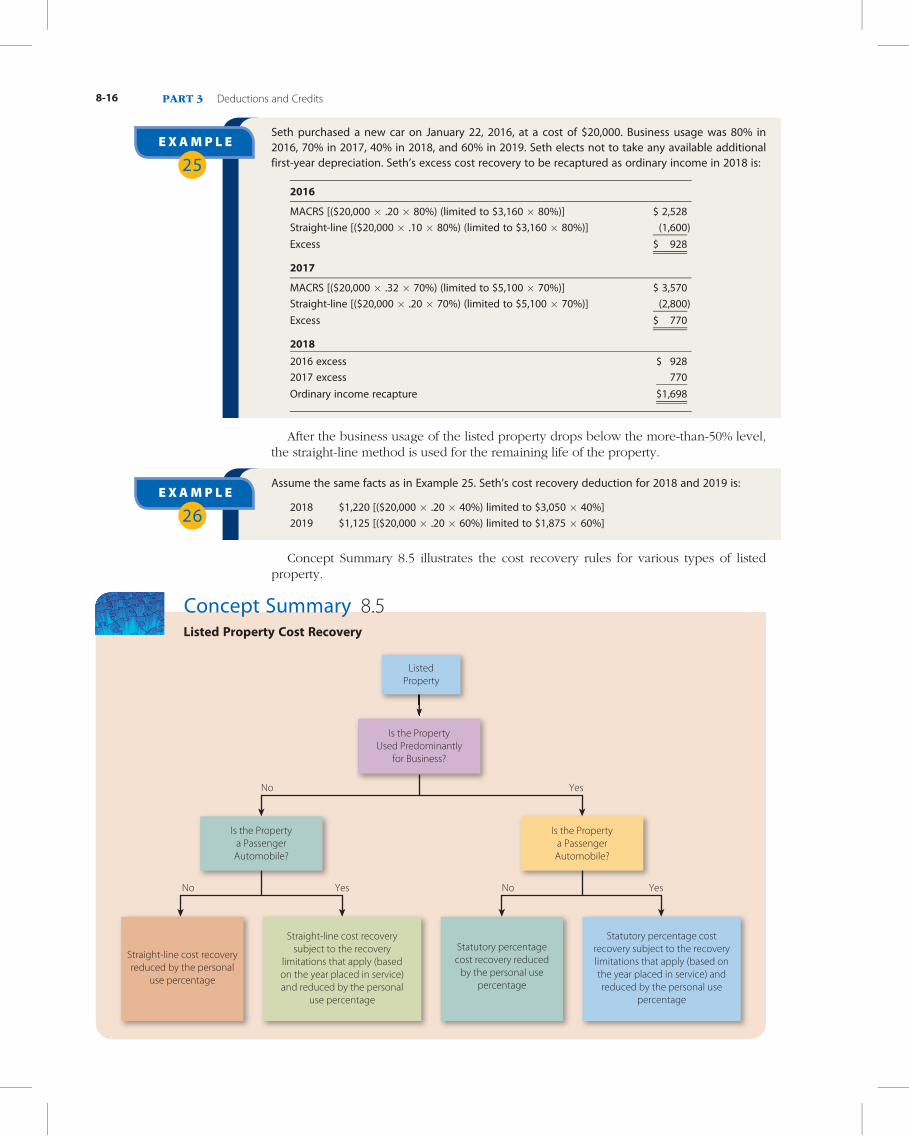

After the business usage of the listed property drops below the more-than-50% level,the straight-line method is used for the remaining life of the property.

Concept Summary 8.5 illustrates the cost recovery rules for various types of listedproperty.

E XAMP L E

25

Seth purchased a new car on January 22, 2016, at a cost of $20,000. Business usage was 80% in2016, 70% in 2017, 40% in 2018, and 60% in 2019. Seth elects not to take any available additionalfirst-year depreciation. Seth’s excess cost recovery to be recaptured as ordinary income in 2018 is:

2016

MACRS [($20,000 � .20 � 80%) (limited to $3,160 � 80%)] $ 2,528

Straight-line [($20,000 � .10 � 80%) (limited to $3,160 � 80%)] (1,600)

Excess $ 928

2017

MACRS [($20,000 � .32 � 70%) (limited to $5,100 � 70%)] $ 3,570

Straight-line [($20,000 � .20 � 70%) (limited to $5,100 � 70%)] (2,800)

Excess $ 770

2018

2016 excess $ 928

2017 excess 770

Ordinary income recapture $1,698

E XAMP L E

26

Assume the same facts as in Example 25. Seth’s cost recovery deduction for 2018 and 2019 is:

2018 $1,220 [($20,000 � .20 � 40%) limited to $3,050 � 40%]

2019 $1,125 [($20,000 � .20 � 60%) limited to $1,875 � 60%]

Concept Summary 8.5Listed Property Cost Recovery

No

No Yes

NoYes Yes

ListedProperty

Is the Propertya PassengerAutomobile?

Is the Propertya PassengerAutomobile?

Is the PropertyUsed Predominantly

for Business?

Straight-line cost recovery reduced by the personal

use percentage

Straight-line cost recovery subject to the recovery

limitations that apply (based on the year placed in service) and reduced by the personal

use percentage

Statutory percentage cost recovery reduced

by the personal use percentage

Statutory percentage cost recovery subject to the recovery limitations that apply (based on the year placed in service) and reduced by the personal use

percentage

8-16 PART 3 Deductions and Credits

Leased AutomobilesA taxpayer who leases a passenger automobile reports an inclusion amount in grossincome. The inclusion amount is computed from an IRS table for each taxable year forwhich the taxpayer leases the automobile. The purpose of this provision is to preventtaxpayers from circumventing the luxury auto and other limitations by leasing, insteadof purchasing, an automobile.

The inclusion amount is based on the fair market value of the automobile; it is pro-rated for the number of days the auto is used during the taxable year. The prorateddollar amount then is multiplied by the business and income-producing usagepercentage.26 The taxpayer deducts the lease payments, multiplied by the business andincome-producing usage percentage. In effect, the taxpayer’s annual deduction for thelease payment is reduced by the inclusion amount.

Substantiation RequirementsListed property is subject to the substantiation requirements of § 274. This means thatthe taxpayer must prove for any business usage the amount of expense or use, the timeand place of use, the business purpose for the use, and the business relationship to thetaxpayer of persons using the property.

Substantiation requires adequate records or sufficient evidence corroborating the tax-payer’s statement. However, these substantiation requirements do not apply to vehiclesthat, by reason of their nature, are not likely to be used more than a de minimis amountfor personal purposes.27

8-3d Alternative Depreciation System (ADS)The alternative depreciation system (ADS) must be used:28

• To calculate the portion of depreciation treated as an alternative minimumtax (AMT) adjustment for purposes of the corporate and individual AMT (seeChapter 15).29

• To compute depreciation allowances for property:• Used predominantly outside the United States.

• Leased or otherwise used by a tax-exempt entity.

• Financed with the proceeds of tax-exempt bonds.

• Imported from foreign countries that maintain discriminatory trade practices orotherwise engage in discriminatory acts.

• To compute depreciation allowances for earnings and profits purposes (seeChapter 19).

E XAMP L E

27

On April 1, 2016, Jim leases and places in service a passenger automobile worth $52,400. The leaseis to be for a period of five years. During the taxable years 2016 and 2017, Jim uses the automobile70% for business and 30% for personal use.

Assuming that the dollar amounts from the IRS table for 2016 and 2017 are $53 and $115,respectively, Jim includes in gross income:

2016 $53 � (275/366) � 70% ¼ $28

2017 $115 � (365/365) � 70% ¼ $81

In each year, Jim still can deduct 70% of the lease payments made, related to his business useof the auto.

26Reg. § 1.280F–7(a).27§§ 274(d) and (i).28§ 168(g).

29This AMT adjustment applies for real and personal property placed in ser-vice before 1999. However, it also applies for personal property placed inservice after 1998 if the taxpayer uses the 200% declining-balance methodfor regular income tax purposes. See Chapter 15.

LO.5

Determine when and howto use the alternativedepreciation system (ADS).

CHAPTER 8 Depreciation, Cost Recovery, Amortization, and Depletion 8-17

In general, ADS depreciation is computed using straight-line recovery. However,for purposes of the AMT, depreciation of personal property is computed using the150 percent declining-balance method with an appropriate switch to the straight-linemethod.

The taxpayer must use the half-year or the mid-quarter convention, whichever isapplicable, for all property other than eligible real estate. The mid-month convention isused for eligible real estate. The applicable ADS rates are found in Exhibits 8.6, 8.7,and 8.9. Generally, personal property is depreciated under the ADS using the appropri-ate asset class life (e.g., 5- or 7-year) and the 150 percent declining-balance method.ADS uses straight-line depreciation for all realty, over a 40-year class life.30

Taxpayers may elect to use the 150 percent declining-balance method to computethe regular income tax rather than the 200 percent declining-balance method that isavailable for personal property. If this election is made, there is no difference betweenthe cost recovery for computing the regular income tax and the AMT.31

Rather than determining depreciation under the regular MACRS method, taxpayersmay elect straight-line under ADS for property that qualifies for the regular MACRSmethod. One reason for making this election is to avoid a difference between deduct-ible depreciation and earnings and profits depreciation, thereby reducing the number ofcost recovery computations that must be made.32

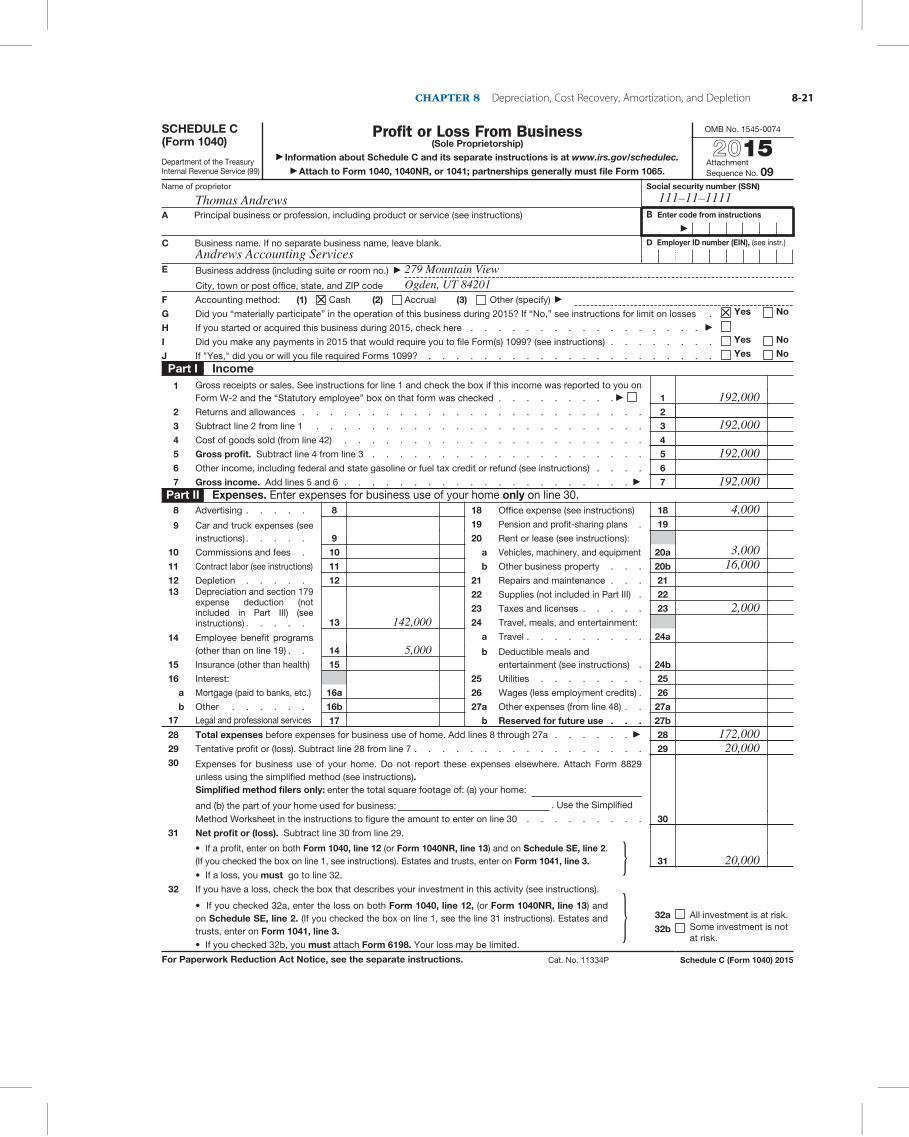

8-4 REPORTING PROCEDURESSole proprietors engaged in a business file a Schedule C, Profit or Loss from Business, toaccompany Form 1040. A 2015 Schedule C is illustrated, as the 2016 Schedule C is notyet available.

The top part of page 1 requests certain key information about the taxpayer (e.g.,name, address, Social Security number, principal business activity, and accountingmethod used). Part I provides for the reporting of items of income. If the businessrequires the use of inventories and the computation of cost of goods sold (see Chapter16 for when this is necessary), Part III must be completed and the cost of goods soldamount transferred to line 4 of Part I.

E XAMP L E

28

On March 1, 2016, Abby purchases computer-based telephone central office switching equipmentfor $80,000. Abby elects not to take any available additional first-year depreciation. If Abbyuses statutory percentage cost recovery (assuming no § 179 election), her deduction for 2016 is$16,000 [$80,000� :20 (Exhibit 8.3, 5-year class property)].

If Abby elects to use ADS 150% declining-balance cost recovery for the regular income tax(assuming no § 179 election), the cost recovery allowance for 2016 is $12,000 [$80,000� :15(Exhibit 8.6, 5-year class property)].

E XAMP L E

29

Polly acquires an apartment building on March 17, 2016, for $700,000. She takes the maximumcost recovery allowance for determining taxable income. For 2016, Polly deducts $20,153[$700,000� :02879 (Exhibit 8.8)].

However, Polly’s cost recovery for computing her earnings and profits is only $13,853[$700,000� :01979 (Exhibit 8.9)].

30The class life for certain properties described in § 168(e)(3) is speciallydetermined under § 168(g)(3)(B).

31For personal property placed in service before 1999, taxpayers making theelection use the ADS recovery periods in computing cost recovery for theregular income tax. The ADS recovery periods generally are longer thanthe regular recovery periods under MACRS.

32This straight-line election is made on a year-by-year basis. For propertyother than real estate, the election is made by MACRS class and applies toall assets in that MACRS class. So, for example, the election could be madefor 7-year MACRS property and not for 5-year MACRS property placed inservice during the same year. For real estate, the election is made on aproperty-by-property basis.

LO.6

Report cost recoverydeductions appropriately.

8-18 PART 3 Deductions and Credits

Part II allows for the reporting of deductions. Some of the deductions discussed inthis chapter and their location on the form are depletion (line 12) and depreciation (line13). Other expenses (line 27) include those items not already covered (see lines 8–26).An example is research and experimental expenditures.

If depreciation is claimed, it should be supported by completing Form 4562. A 2015Form 4562 is illustrated, as the 2016 Form 4562 is not yet available. The amount listed online 22 of Form 4562 is transferred to line 13 of Part II of Schedule C.

8-5 AMORTIZATIONTaxpayers can claim an amortization deduction on intangible assets called “amortizable§ 197 intangibles.” The amount of the deduction is determined by amortizing theadjusted basis of such intangibles ratably over a 15-year period beginning in the monthin which the intangible is acquired.33

An amortizable § 197 intangible is any § 197 intangible acquired after August 10,1993, and held in connection with the conduct of a trade or business or for the produc-tion of income. Section 197 intangibles include goodwill and going-concern value,franchises, trademarks, and trade names. Covenants not to compete, copyrights, andpatents also are included if they are acquired in connection with the acquisition of abusiness. Generally, self-created intangibles are not § 197 intangibles.

The 15-year amortization period applies regardless of the actual useful life of anamortizable § 197 intangible. No other depreciation or amortization deduction is permit-ted with respect to any amortizable § 197 intangible except those permitted under the15-year amortization rules.

Startup expenditures are partially amortizable by using a § 195 election.34 A taxpayermust make this election no later than the due date of the return for the taxable year inwhich the trade or business begins.35 If no election is made, the startup expendituresare capitalized.36

E XAMP L E

30

Thomas Andrews, Social Security number 111-11-1111, was employed as an accountant until May2015, when he opened his own practice. His address is 279 Mountain View, Ogden, UT 84201.Andrews keeps his books on the cash basis and reported the following revenue and businessexpenses in 2015.

a. Revenue from accounting practice, $192,000.b. Insurance, $5,000.c. Office supplies, $4,000.d. Office rent, $16,000.e. Copier lease payments, $3,000.f. Licenses, $2,000.g. New furniture and fixtures were acquired on May 10, for $142,000. Thomas elects § 179 expens-

ing and uses the statutory percentage cost recovery method.

Andrews reports the above information on Schedule C and Form 4562 as illustrated on the follow-ing pages.

E XAMP L E

31

On June 1, 2016, Neil purchased and began operating the Falcon Caf�e. Of the purchase price, $90,000is allocated to goodwill. The 2016 § 197 amortization deduction is $3,500 [($90,000=15)� (7=12)].

LO.7

Identify intangible assets thatare eligible for amortizationand calculate the amount ofthe deduction.

33§ 197(a).34§ 195(b).

35§ 195(d).36§ 195(a).

CHAPTER 8 Depreciation, Cost Recovery, Amortization, and Depletion 8-19

Form 4562Department of the Treasury Internal Revenue Service (99)

Depreciation and Amortization (Including Information on Listed Property)

▶ Attach to your tax return.▶ Information about Form 4562 and its separate instructions is at www.irs.gov/form4562.

OMB No. 1545-0172

2015Attachment Sequence No. 179

Name(s) shown on return Business or activity to which this form relates Identifying number

Part I Election To Expense Certain Property Under Section 179 Note: If you have any listed property, complete Part V before you complete Part I.

1 Maximum amount (see instructions) . . . . . . . . . . . . . . . . . . . . . . . 12 Total cost of section 179 property placed in service (see instructions) . . . . . . . . . . . 23 Threshold cost of section 179 property before reduction in limitation (see instructions) . . . . . . 34 Reduction in limitation. Subtract line 3 from line 2. If zero or less, enter -0- . . . . . . . . . . 45 Dollar limitation for tax year. Subtract line 4 from line 1. If zero or less, enter -0-. If married filing

separately, see instructions . . . . . . . . . . . . . . . . . . . . . . . . . 56 (a) Description of property (b) Cost (business use only) (c) Elected cost

7 Listed property. Enter the amount from line 29 . . . . . . . . . 78 Total elected cost of section 179 property. Add amounts in column (c), lines 6 and 7 . . . . . . 89 Tentative deduction. Enter the smaller of line 5 or line 8 . . . . . . . . . . . . . . . . 9

10 Carryover of disallowed deduction from line 13 of your 2014 Form 4562 . . . . . . . . . . . 1011 Business income limitation. Enter the smaller of business income (not less than zero) or line 5 (see instructions) 1112 Section 179 expense deduction. Add lines 9 and 10, but do not enter more than line 11 . . . . . 1213 Carryover of disallowed deduction to 2016. Add lines 9 and 10, less line 12 ▶ 13

Note: Do not use Part II or Part III below for listed property. Instead, use Part V.Part II Special Depreciation Allowance and Other Depreciation (Do not include listed property.) (See instructions.)14 Special depreciation allowance for qualified property (other than listed property) placed in service

during the tax year (see instructions) . . . . . . . . . . . . . . . . . . . . . . 1415 Property subject to section 168(f)(1) election . . . . . . . . . . . . . . . . . . . . 1516 Other depreciation (including ACRS) . . . . . . . . . . . . . . . . . . . . . . 16Part III MACRS Depreciation (Do not include listed property.) (See instructions.)

Section A17 MACRS deductions for assets placed in service in tax years beginning before 2015 . . . . . . . 1718 If you are electing to group any assets placed in service during the tax year into one or more general

asset accounts, check here . . . . . . . . . . . . . . . . . . . . . . ▶

Section B—Assets Placed in Service During 2015 Tax Year Using the General Depreciation System

(a) Classification of property(b) Month and year

placed inservice

(c) Basis for depreciation(business/investment useonly—see instructions)

(d) Recoveryperiod

(e) Convention (f) Method (g) Depreciation deduction

19a 3-year propertyb 5-year propertyc 7-year propertyd 10-year propertye 15-year propertyf 20-year property

g 25-year propertyh Residential rental

propertyi Nonresidential real

property

Section C—Assets Placed in Service During 2015 Tax Year Using the Alternative Depreciation System20a Class life

b 12-yearc 40-year

Part IV Summary (See instructions.)21 Listed property. Enter amount from line 28 . . . . . . . . . . . . . . . . . . . . 2122 Total. Add amounts from line 12, lines 14 through 17, lines 19 and 20 in column (g), and line 21. Enter

here and on the appropriate lines of your return. Partnerships and S corporations—see instructions . 2223 For assets shown above and placed in service during the current year, enter the

portion of the basis attributable to section 263A costs . . . . . . . 23For Paperwork Reduction Act Notice, see separate instructions. Cat. No. 12906N Form 4562 (2015)

25 yrs. S/L27.5 yrs. MM S/L27.5 yrs. MM S/L39 yrs. MM S/L

MM S/L

S/L12 yrs. S/L40 yrs. MM S/L

Thomas Andrews Andrews Accounting Services 111-11-1111

142,000

-0-

Furniture and Fixtures 142,000 142,000

142,000

142,000142,000

142,000142,000

142,000

-0-

8-20 PART 3 Deductions and Credits

SCHEDULE C (Form 1040) 2015

Profit or Loss From Business (Sole Proprietorship)

Department of the Treasury Internal Revenue Service (99)

▶ Information about Schedule C and its separate instructions is at www.irs.gov/schedulec.▶ Attach to Form 1040, 1040NR, or 1041; partnerships generally must file Form 1065.

OMB No. 1545-0074

Attachment Sequence No. 09

Name of proprietor Social security number (SSN)

A Principal business or profession, including product or service (see instructions) B Enter code from instructions

▶

C Business name. If no separate business name, leave blank. D Employer ID number (EIN), (see instr.)

E Business address (including suite or room no.) ▶

City, town or post office, state, and ZIP code

F Accounting method: (1) Cash (2) Accrual (3) Other (specify) ▶

G Did you “materially participate” in the operation of this business during 2015? If “No,” see instructions for limit on losses . Yes No

H If you started or acquired this business during 2015, check here . . . . . . . . . . . . . . . . . ▶

I Did you make any payments in 2015 that would require you to file Form(s) 1099? (see instructions) . . . . . . . . Yes No

J If "Yes," did you or will you file required Forms 1099? . . . . . . . . . . . . . . . . . . . . . Yes No

Part I Income 1 Gross receipts or sales. See instructions for line 1 and check the box if this income was reported to you on

Form W-2 and the “Statutory employee” box on that form was checked . . . . . . . . . ▶ 1

2 Returns and allowances . . . . . . . . . . . . . . . . . . . . . . . . . 2

3 Subtract line 2 from line 1 . . . . . . . . . . . . . . . . . . . . . . . . 3

4 Cost of goods sold (from line 42) . . . . . . . . . . . . . . . . . . . . . . 4

5 Gross profit. Subtract line 4 from line 3 . . . . . . . . . . . . . . . . . . . . 5

6 Other income, including federal and state gasoline or fuel tax credit or refund (see instructions) . . . . 6

7 Gross income. Add lines 5 and 6 . . . . . . . . . . . . . . . . . . . . . ▶ 7 Part II Expenses. Enter expenses for business use of your home only on line 30.

8 Advertising . . . . . 8

9 Car and truck expenses (see instructions) . . . . . 9

10 Commissions and fees . 10

11 Contract labor (see instructions) 11

12 Depletion . . . . . 12 13 Depreciation and section 179

expense deduction (not included in Part III) (see instructions) . . . . . 13

14 Employee benefit programs (other than on line 19) . . 14

15 Insurance (other than health) 15

16 Interest:

a Mortgage (paid to banks, etc.) 16a

b Other . . . . . . 16b17 Legal and professional services 17

18 Office expense (see instructions) 18

19 Pension and profit-sharing plans . 19

20 Rent or lease (see instructions):

a Vehicles, machinery, and equipment 20a

b Other business property . . . 20b

21 Repairs and maintenance . . . 21

22 Supplies (not included in Part III) . 22

23 Taxes and licenses . . . . . 23

24 Travel, meals, and entertainment:

a Travel . . . . . . . . . 24a

b Deductible meals and entertainment (see instructions) . 24b

25 Utilities . . . . . . . . 25

26 Wages (less employment credits) . 26

27 a Other expenses (from line 48) . . 27a

b Reserved for future use . . . 27b

28 Total expenses before expenses for business use of home. Add lines 8 through 27a . . . . . . ▶ 28

29 Tentative profit or (loss). Subtract line 28 from line 7 . . . . . . . . . . . . . . . . . 29

30 Expenses for business use of your home. Do not report these expenses elsewhere. Attach Form 8829 unless using the simplified method (see instructions). Simplified method filers only: enter the total square footage of: (a) your home:

and (b) the part of your home used for business: . Use the Simplified

Method Worksheet in the instructions to figure the amount to enter on line 30 . . . . . . . . . 30

31 Net profit or (loss). Subtract line 30 from line 29.

• If a profit, enter on both Form 1040, line 12 (or Form 1040NR, line 13) and on Schedule SE, line 2. (If you checked the box on line 1, see instructions). Estates and trusts, enter on Form 1041, line 3.

• If a loss, you must go to line 32.} 31

32 If you have a loss, check the box that describes your investment in this activity (see instructions).

• If you checked 32a, enter the loss on both Form 1040, line 12, (or Form 1040NR, line 13) and on Schedule SE, line 2. (If you checked the box on line 1, see the line 31 instructions). Estates and trusts, enter on Form 1041, line 3. • If you checked 32b, you must attach Form 6198. Your loss may be limited.

} 32a All investment is at risk.

32b Some investment is not at risk.

For Paperwork Reduction Act Notice, see the separate instructions. Cat. No. 11334P Schedule C (Form 1040) 2015

Thomas Andrews

Andrews Accounting Services

111–11–1111

×

279 Mountain ViewOgden, UT 84201

×

192,000

192,000

192,000

192,000

4,000

3,00016,000

2,000

172,00020,000

20,000

142,000

5,000

CHAPTER 8 Depreciation, Cost Recovery, Amortization, and Depletion 8-21

The amortization election for startup expenditures allows the taxpayer to deductthe lesser of (1) the amount of startup expenditures with respect to the trade or businessor (2) $5,000, reduced, but not below zero, by the amount by which the startup expen-ditures exceed $50,000. Any startup expenditures not deducted are amortized ratablyover a 180-month period, beginning in the month in which the trade or businessbegins.37

Amortizable startup expenditures generally must satisfy two requirements.38 First, theexpenditures must be paid or incurred in connection with:

• The creation of an active trade or business,

• The investigation of the creation or acquisition of an active trade or business, or

• Any activity engaged in for profit in anticipation of it becoming an active trade orbusiness.

Second, the expenses must reflect those that could be deducted in an existing tradeor business in the same field (see Investigation of a Business, Chapter 6).

The startup costs of creating a new active trade or business could include advertising;salaries and wages; travel and other expenses incurred in lining up prospective distribu-tors, suppliers, or customers; and salaries and fees for executives, consultants, and profes-sional services. Costs that relate to either created or acquired businesses could includeexpenses incurred for the analysis or survey of potential markets, products, labor supply,transportation facilities, and the like. Startup expenditures do not include allowabledeductions for interest, taxes, and research and experimental costs.39

Amortization deductions also can be claimed for organizational expenses (see Chapter 17)and research and experimental expenditures (see Chapter 7).

8-6 DEPLETIONNatural resources (e.g., oil, gas, coal, gravel, and timber) are subject to depletion , whichcan be seen as a form of depreciation applicable to natural resources. Land generallycannot be depleted.

The owner of an interest in the natural resource is entitled to deduct depletion. Anowner is one who has an economic interest in the property.40 An economic interest

E XAMP L E

33

Assume the same facts as in Example 32, except that the startup expenditures total $53,000.The 2016 deduction is computed as follows.

Deductible amount [$5,000 � ($53,000 � $50,000)] $2,000

Amortizable amount {[($53,000 � $2,000)/180] � 5 months} 1,417

Total deduction $3,417

E XAMP L E

32

Startup Expenditures

Green Corporation begins business on August 1, 2016. The corporation incurs startup expenditures of$47,000. If Green elects amortization under § 195, the total startup expenditures that Green maydeduct in 2016 is computed as follows.

Deductible amount $5,000

Amortizable amount {[($47,000 � $5,000)/180] � 5 months} 1,167

Total deduction $6,167

37§§ 195(b)(1)(A) and (B).38§§ 195(c)(1)(A) and (B).

39§ 195(c).40Reg. § 1.611–1(b).

LO.8

Determine the amount ofdepletion expense, includingbeing able to apply thealternative tax treatmentsfor intangible drilling anddevelopment costs.

8-22 PART 3 Deductions and Credits

requires the acquisition of an interest in the resource in place and the receipt of incomefrom the extraction or severance of that resource. Like depreciation, depletion is a tradeor business deduction for adjusted gross income.

Although all natural resources are subject to depletion, oil and gas wells are used as anexample in the following paragraphs to illustrate the related costs and issues.

In developing an oil or gas well, the producer typically makes four types ofexpenditures.

• Natural resource costs.

• Intangible drilling and development costs.

• Tangible asset costs.

• Operating costs.

Natural resources are physically limited, and the costs to acquire them (e.g., oil under theground) are, therefore, recovered through depletion. Costs incurred in making the prop-erty ready for drilling, such as the cost of labor in clearing the property, erecting derricks,and drilling the hole, are intangible drilling and development costs (IDCs) . These costs gen-erally have no salvage value and are a lost cost if the well is dry.

Costs for tangible assets such as tools, pipes, and engines are capitalized and recov-ered through depreciation (cost recovery). Costs incurred after the well is producing areoperating costs. These costs include expenditures for such items as labor, fuel, and sup-plies. Operating costs are deductible as trade or business expenses. Depletable costsand intangible drilling and development costs receive different treatment.

8-6a Intangible Drilling and Development Costs (IDCs)Intangible drilling and development costs can be handled in one of two ways at theoption of the taxpayer. They can be either charged off as an expense in the year inwhich they are incurred or capitalized and written off through depletion. The taxpayermakes the election in the first year such expenditures are incurred, either by taking adeduction on the return or by adding them to the depletable basis.

Once made, the election is binding on both the taxpayer and the IRS for all suchexpenditures in the future. If the taxpayer fails to elect to expense IDCs on the originaltimely filed return for the first year in which such expenditures are incurred, an irrevo-cable election to capitalize them has been made.

As a general rule, it is more advantageous to expense IDCs. The obvious benefit ofan immediate write-off (as opposed to a deferred write-off through depletion) is not theonly advantage. Because a taxpayer can use percentage depletion, which is calculatedwithout reference to basis (see Example 35), the IDCs may be completely lost as adeduction if they are capitalized.

8-6b Depletion MethodsThere are two methods of calculating depletion. Cost depletion can be used on any wast-ing asset (and is the only method allowed for timber). Percentage depletion is subject to anumber of limitations, particularly for oil and gas deposits. Depletion should be calculatedboth ways, and the method that results in the larger deduction should be used. Thechoice between cost depletion and percentage depletion is an annual decision; the tax-payer can use cost depletion in one year and percentage depletion in the following year.

Cost DepletionCost depletion is determined by using the adjusted basis of the asset.41 The basis isdivided by the estimated recoverable units of the asset (e.g., barrels and tons) to arrive atthe depletion per unit. This amount then is multiplied by the number of units sold (not theunits produced) during the year to arrive at the cost depletion allowed. Cost depletion,therefore, resembles the units-of-production method of calculating depreciation.

41§ 612.

CHAPTER 8 Depreciation, Cost Recovery, Amortization, and Depletion 8-23

If the taxpayer later discovers that the original estimate was incorrect, the depletionper unit for future calculations is redetermined, using the revised estimate.42

Percentage DepletionPercentage depletion (also referred to as statutory depletion) uses a specified percent-age provided by the Code. The percentage varies according to the type of mineralinterest involved. A sample of these percentages is shown in Exhibit 8.2. The rate isapplied to the gross income from the property, but in no event may percentage deple-tion exceed 50 percent of the taxable income from the property before the allowancefor depletion.43

Note that percentage depletion is based on a percentage of the gross income from theproperty and makes no reference to cost. All other deductions detailed in this chapter are

E XAMP L E

34