deposits. the basics of bank banks are business firms that buy (borrow) and sell (lend) money to...

TRANSCRIPT

DEPOSITS

THE BASICS OF BANK

• Banks are business firms that buy (borrow) and sell (lend) money to make a profit.

• Money is the raw material for banks –repackagers of money.

• Financial claims on both sides of balance sheet– Liabilities—Sources of funds– Assets—Uses of funds

MAIN DUTIES OF A BANK

• Handle customers business in a safe and in professional manner.

• Honour customers’ cheques.• Comply with any express (written) instruction from

the customer.• Maintain secrecy about customers’ affairs.• Give reasonable notice to close an account.

MAIN DUTIES OF A BANK

• Provide balance of account on request.• Receive customers money and cheques and credit to

the correct account.• Repay money on demand in banking hours.• Advise customers immediately of any improper event

affecting the account.• Exercise proper care and skill when performing all its

duties..

DEFINITION OF DEPOSITS

• TheFreeDictionary.com – To give over or entrust for safekeeping.– To put (money) in a bank or financial account.

• Investopedia– The money an investor transfers into a bank's savings or

checking accounts.

INTRODUCTION

• Deposits of a bank are classified under the liability management of a bank.

• A deposit is the major source of funds to a bank.• The depositors /customers of a bank are the

creditors and the bank will become the debtor.

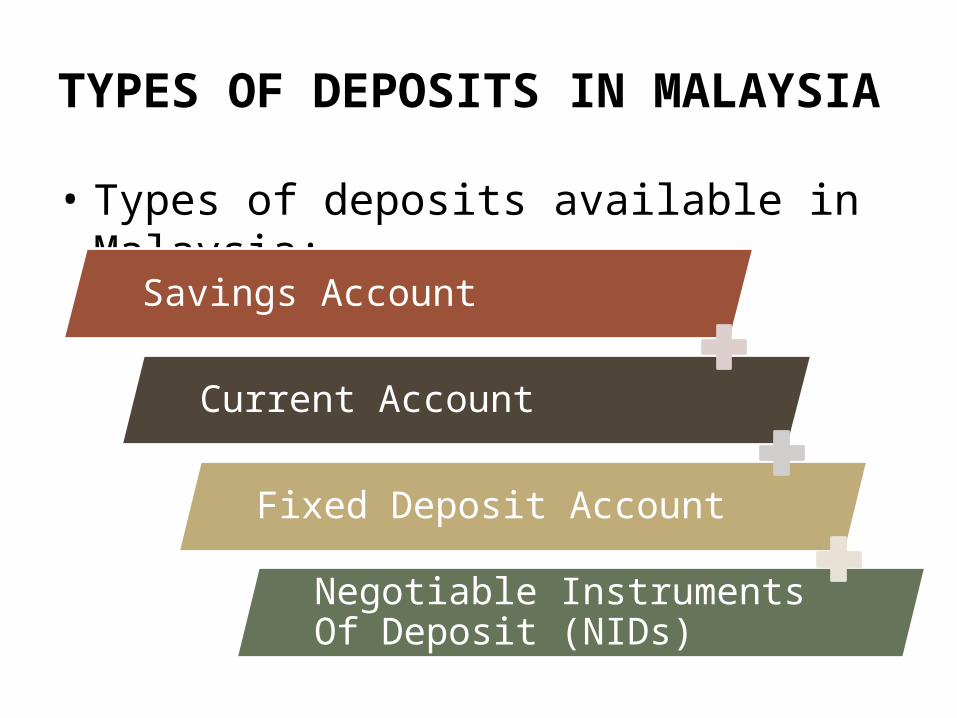

TYPES OF DEPOSITS IN MALAYSIA

• Types of deposits available in Malaysia:

Savings Account

Current Account

Fixed Deposit Account

Negotiable Instruments Of Deposit (NIDs)

SAVINGS ACCOUNT

INTRODUCTION

• Form of deposit account - an interest bearing deposits account.

• Once customers open a saving account, the depositors–banker relationship established.

• Customer places his savings in the custody of the bank with the understanding that monies deposited may accumulate interest and be withdrawn on demand.

INTRODUCTION (CONT’D)

• An account holder for savings account will be given a passbook (optional) and bankcard.

• Purpose of bankcard:-– For easier and convenient withdrawal of funds.

ATM SERVICES

• ATM not only limited for cash withdrawals, but account holder also can enjoys other services such as:-– Bills Payment– Funds Transfer– Fixed Deposit Placement– Prepaid and Touch 'N Go Reload – MEPS Cash– Cheque Book Request– Mini Statement Request– Phone Banking Registration

TYPES OF SAVINGS ACCOUNT

Individual Savings Account

Joint Savings AccountSavings Account for Associations, Societies & ClubsTrustees Account

Minors Account

INDIVIDUAL SAVINGS ACCOUNT

• An individual needs to have an identification card and to come in person.

• He or she has to fill up a form and to sign specimen signature cards.

• He or she is also required to sign in the passbook and the signature will be covered by a spectroline sticker.

• The signature later will be used to verify withdrawals using passbook by viewing the signature using an ultra-violet light.

SPECTROLINE STICKER

JOINT SAVINGS ACCOUNT

• The applicants (two or more) needs to have an identification card and fill up a Joint Account Mandate Form.

• In addition, they are required to furnish the bank with the method of operating the joint account.– The account holder can authorize persons to operate the

account on his behalf by providing a power of attorney, which will be accepted at the sole discretion of the Bank.

SAVINGS ACCOUNT FOR ASSOCIATIONS, SOCIETIES AND CLUBS• To open a savings account for societies, associations

and clubs:-– A certified true copy of license or certificate issued by the

Registrar of Societies, a certified copy of an extract of resolution passed by the committee and identification cards of office bearers are required.

TRUSTEE SAVINGS ACCOUNT

• A Trust Deed is required for the opening of a Savings Trust Account.

• There may be one or more trustees.• The trustee may open and operate the account in

his/their names.• When there is more than one trustee, then all the

trustees must jointly operate the account.

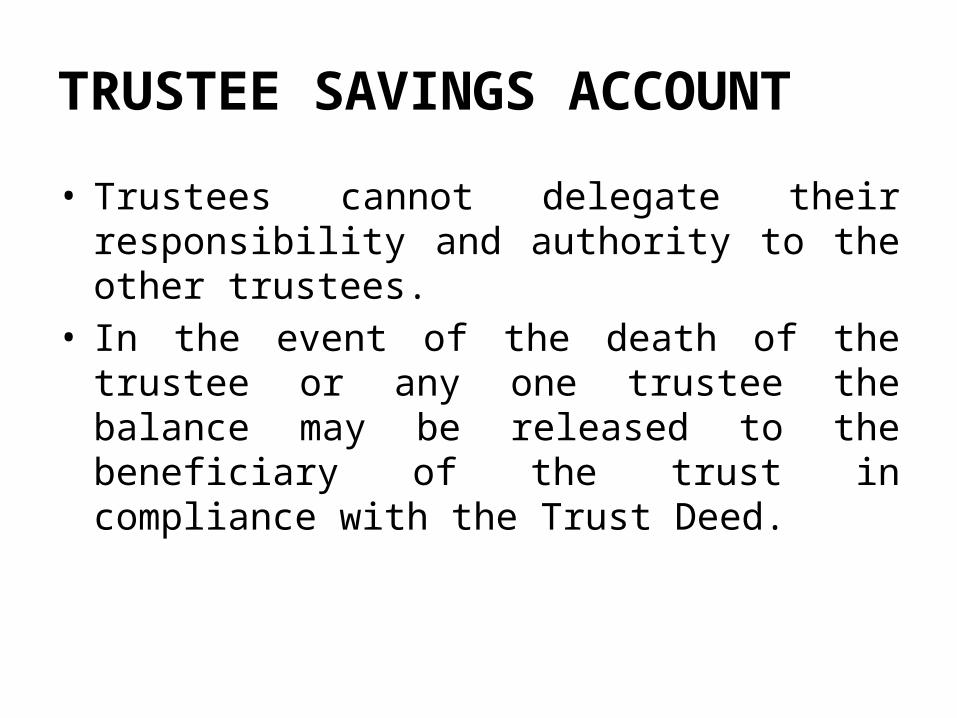

TRUSTEE SAVINGS ACCOUNT

• Trustees cannot delegate their responsibility and authority to the other trustees.

• In the event of the death of the trustee or any one trustee the balance may be released to the beneficiary of the trust in compliance with the Trust Deed.

MINOR SAVINGS ACCOUNT

• Minor is an individual who is lack contractual capacity.

• Minors over the age of twelve (>12) are normally allowed to open and operate a savings account using their identity card.

• Minors below the age of twelve (<12) need their parents or guardians to open the account for them.

• The account will be opened and operated by their parents /guardians on behalf of the minors.

CURRENT ACCOUNT

INTRODUCTION

• A current account is a deposit account available at all banking institutions in Malaysia and can be used for either personal or business purposes.

• Current account holders are allowed to use cheques as a way to make payments.

• Different banking institutions have different requirements for opening a current account.

• The product features also vary amongst the banking institutions i.e. some banking institutions offer interest bearing current accounts while some do not.

FEATURES

• Operated through the use of cheques.• Cheques are used for deposit /withdrawal of funds.• Interest is not paid on non-interest bearing account.• Provides an overdraft facility.• To open a current account normally need an

introducer(reference).• A minimum initial deposit is required(depends on the

banks).

TYPES

• Individual Accounts

• Joint Accounts

• Sole Proprietorship Accounts

• Partnership Accounts

• Professional Accounts

• Company Accounts

• Trustee Accounts

• Religious Bodies Accounts

FIXED DEPOSIT

INTRODUCTION

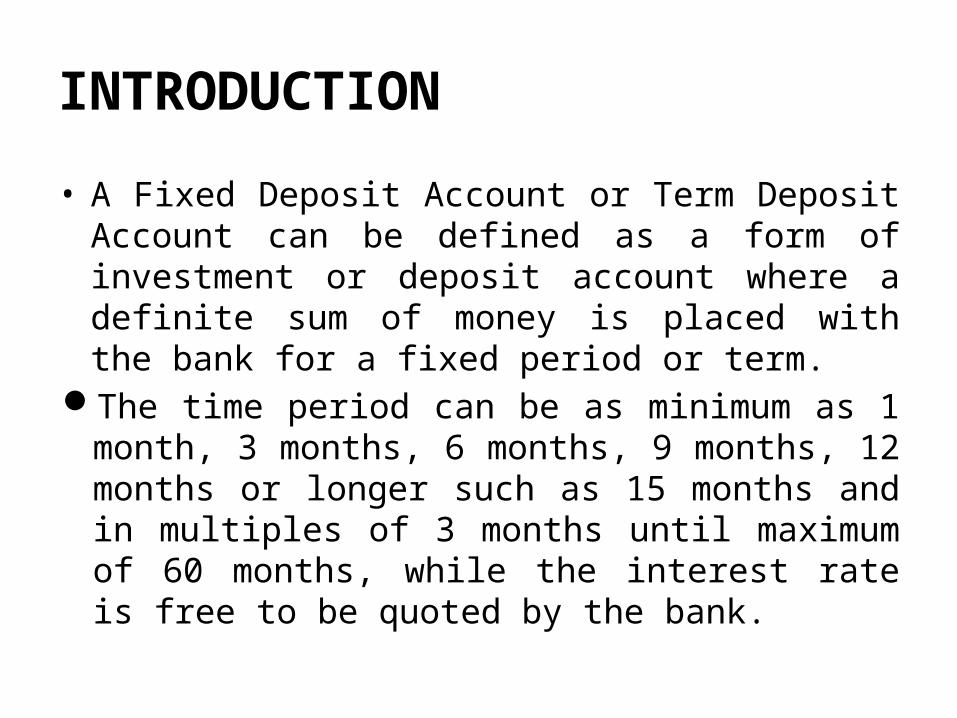

• A Fixed Deposit Account or Term Deposit Account can be defined as a form of investment or deposit account where a definite sum of money is placed with the bank for a fixed period or term.

The time period can be as minimum as 1 month, 3 months, 6 months, 9 months, 12 months or longer such as 15 months and in multiples of 3 months until maximum of 60 months, while the interest rate is free to be quoted by the bank.

INTRODUCTION (CONT’D)

• The rates for fixed deposits for periods exceeding 12 months are negotiable.

• The bank may quote appropriate interest rate and the interest rates are displayed in a special display board within the bank premises.

• Banks are not required to display publish announce the interest rates on deposits for than 12 months.

FEATURES

• No chequebook is given for this type of account.• Deposit certificates will be issued to depositors.– If the depositor wants to renew or terminate the FD

account, the depositor can notify the bank before the existing FD matures.

– If he /she does not notify the bank, the bank will automatically renew the FD.

• Can be apply through ATM.

EARLY WITHDRAWN

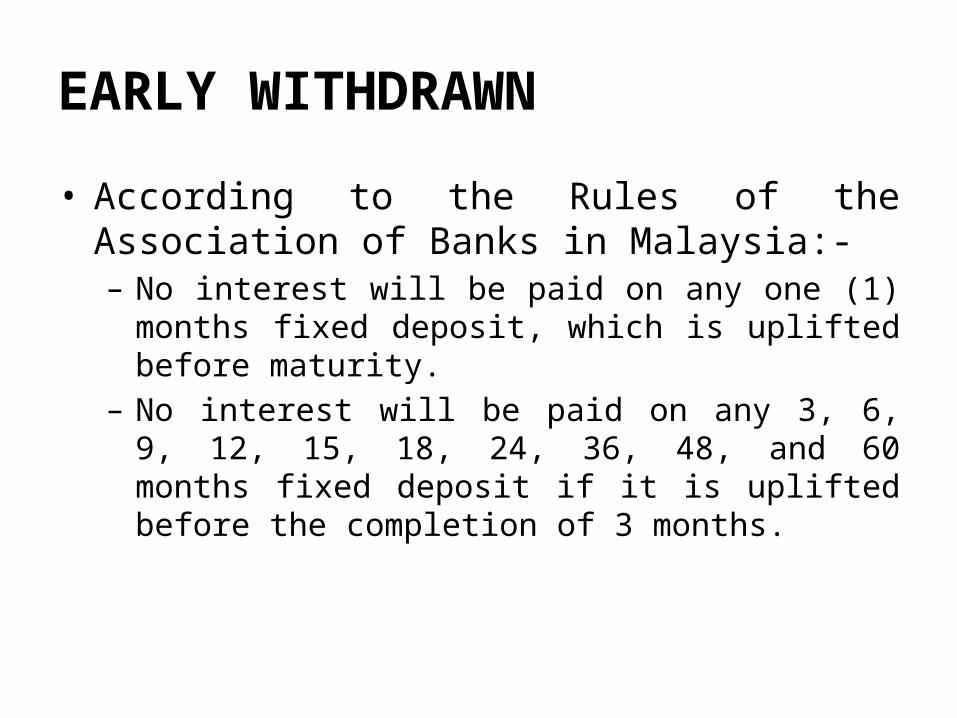

• According to the Rules of the Association of Banks in Malaysia:-– No interest will be paid on any one (1) months fixed

deposit, which is uplifted before maturity.– No interest will be paid on any 3, 6, 9, 12, 15, 18, 24, 36,

48, and 60 months fixed deposit if it is uplifted before the completion of 3 months.

ISLAMIC FIXED DEPOSIT

• The Islamic Fixed Deposit is using al-Mudharabah concept.– Investment partnership.

• Features:-– No interest and it has the same tenor and amount like

the conventional Fixed Deposit.– Bank will act as an entrepreneur (the Mudarib) and

depositor as the financier (the Rab ul Mal).– While profits are shared on a pre-agreed ratio (70:30) ,

loss of investment is born by the investor only.

TYPES

Individual age 18 years and above

Joint Account

Societies

Association and Clubs

Companies

NEGOTIABLE INSTRUMENTS OF DEPOSITS (NIDs)

INTRODUCTION

• Introduced in Malaysia in 1979. • It was designed as a new instrument for the

commercial banks to mobilize domestic savings from the public and to promotes the development of domestic Money market.

• Issued by an authorized commercial banks or financial institutions in Malaysia.

NEGOTIABLE INSTRUMENTS OF DEPOSITS (NIDs)• NID is deposit document issued by the Bank to a

customer certifying that a certain amount has been deposited with the Bank at a specific rate and for a specific tenor /maturity date.

• Unlike Fixed Deposits (FDs), NIDs is negotiable. – NIDs can be sold before its maturity date. – If the customer needs to realise cash before the NIDs

maturity, he /she has to sell the NIDs. – However, the NIDs cannot be withdrawn prematurely like

in FDs.

FEATURES

• A minimum deposit of RM100,000 per deposit and in multiple of RM50,000 subject to .

• Minimum denomination per certificate is RM100,000 and maximum denomination is RM10 million per certificate.

• Tenor available is between 1 month - 10 years. • NIDs rate is generally influenced by interbank rates

and may be higher or lower than the bank's FD rates.

FEATURES (CONT’D)

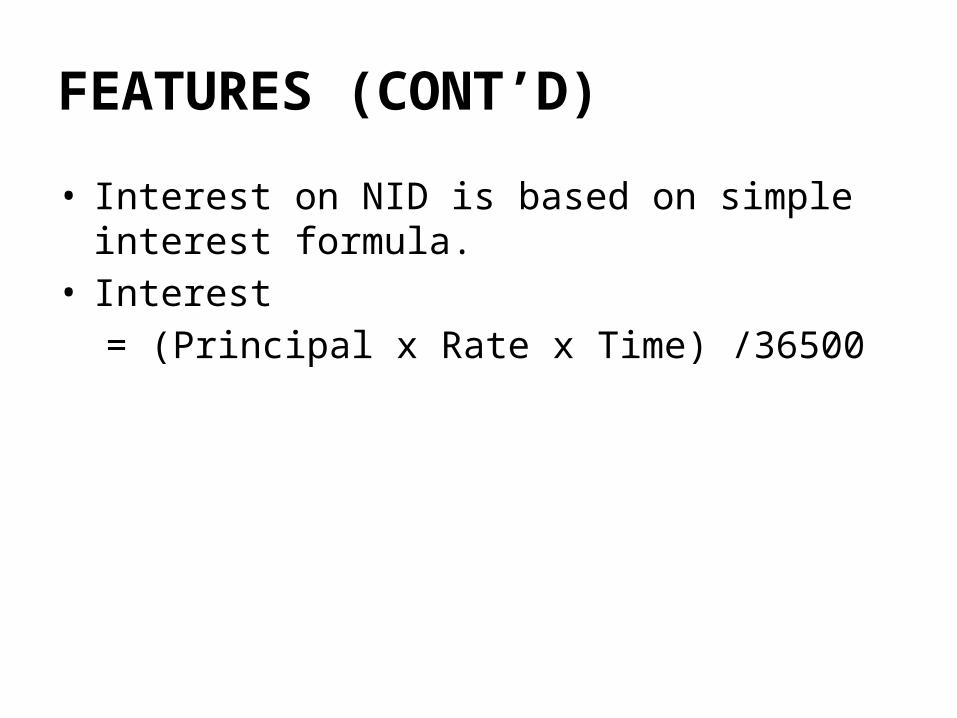

• Interest on NID is based on simple interest formula.• Interest

= (Principal x Rate x Time) /36500

TYPES

• Short-term Negotiable Certificate of Deposits

(SNCDs) with maturity between 90 to 364 days.

• Long-term Negotiable Certificate of Deposits

(LNCDs) with maturity between 1 to 5 years.

TYPES (CONT’D)

• Zero-coupon Negotiable Certificate of Deposits

(ZNCDs) with maturity of 3 months and without

interest and sold at discount.

• Floating Rate Negotiable Certificate of Deposits

(FRNCDs) with maturity of 1 year and interest rate is

not fixed and interest is dependent on Kuala Lumpur

Inter Bank Offers (KLIBOR).

PERBADANAN INSURANS DEPOSIT MALAYSIA (PIDM)

INTRODUCTION

• Perbadanan Insurans Deposit Malaysia (PIDM) is a Government body established in 2005 under the Akta Perbadanan Insurans Deposit Malaysia (Akta PIDM).

• Main role under the Akta PIDM:- – To administer the Deposit Insurance System and the

Takaful and Insurance Benefits System to protect depositors and owners of takaful certificates and insurance policies in the event of a failure member institution.

INTRODUCTION (CONT’D)

• PIDM is also mandated to provide inentives for sound risk management in the financial system, as well as promote and contribute to the stability of the financial system.

SCOPE /COVERAGE

Deposit Insurance

System (DIS)

Takaful and Insurance Benefits

Protection System (TIPS)

DIS

• Protects depositors against the loss of their insured deposits placed with member banks, in the unlikely event of a member bank failure.

TIPS

• Protects owners of takaful certificates and insurance policies from the loss of their eligible takaful or insurance benefits, in the unlikely event of failure an insurer member.

BENEFITS TO DEPOSITORS

BENEFITS TO DEPOSITORS

• PIDM protects depositors /customers’ bank deposits and will promptly reimburse insured deposits in unlikely event of a member bank fail.

• The protection is provided by PIDM automatically - no application is required.

BENEFITS TO THE FINANCIAL SYSTEM

• PIDM promotes public confidence in Malaysia’s financial system by protecting depositors against the loss of their deposits.

• PIDM reinforces and complements the existing regulatory and supervisory framework by providing incentives for sound risk management in the financial system.

BENEFITS TO THE FINANCIAL SYSTEM (CONT’D)• PIDM minimizes costs to the financial system by

finding least cost solutions to resolve failing member institutions.

• PIDM contributes to the stability of the financial system by dealing with member institution failures expeditiously and reimbursing depositors as soon as possible.

BENEFITS TO TAKAFUL CERTIFICATE AND INSURANCE POLICY OWNERS

BENEFITS TO TAKAFUL CERTIFICATE AND INSURANCE POLICY OWNERS

• PIDM protects takaful certificate and insurance policy owners against the loss of eligible takaful or insurance benefits should an insurer member fail.

• The protection is provided by PIDM automatically - no application is required.

BENEFITS TO THE FINANCIAL SYSTEM

• PIDM promotes public confidence in Malaysia’s financial system by protecting takaful certificate and insurance policy owners against the loss of their benefits.

• PIDM reinforces and complements the existing regulatory and supervisory framework by providing incentives for sound risk management in the financial system.

BENEFITS TO THE FINANCIAL SYSTEM (CONT’D)• PIDM minimizes costs to the financial system by

finding least cost solutions to resolve non-viable insurer members.

• PIDM contributes to the stability of the financial system by dealing with non-viable insurer member expeditiously (in efficient manner).

THE ENDANY QUESTIONS?