demystifying private sector credit slowdown: a case study

TRANSCRIPT

Demystifying Private Sector Credit Slowdown: A Case

Study of Kenya and Uganda

Presented by: Britam Asset Managers

20th September 2017

| Unit Trust Funds | Wealth Management | Pensions | Property

| Discretionary Management | Offshore Investments | Alternative

Investments

2

Presentation Outline

Part One: Who We Are

I. Overview of Britam Group

II. Introduction to Britam Asset Managers

Part Two: Private Sector Credit Growth

I. Monetary Policy Effects

II. Fiscal Policy Effects

III. Asset Quality Effects

IV. Summary & Outlook

I. Who We Are

I. Overview of Britam Group

II. Introduction to Britam Asset Managers

I. Britam Holdings PLC Overview

Britam is a leading diversified financial services group and is listed on the Nairobi

Securities Exchange. The group has presence in seven Africa countries in Kenya, Uganda,

Tanzania, Rwanda, South Sudan, Mozambique and Malawi.

Britam offers a wide range of financial products and services which include: Asset

Management, Life Assurance, Retirement Planning, General Insurance, Health Insurance,

Banking and Property. These financial solutions enable our customers to create and protect

their wealth and lives every step of the way.

For more information please visit http://www.britam.com

| Unit Trust Funds | Wealth Management | Pensions | Property

| Discretionary Management | Offshore Investments | Alternative

Investments

5

Our Footprint

1965 2017

| Unit Trust Funds | Wealth Management | Pensions | Property

| Discretionary Management | Offshore Investments | Alternative

Investments

6

Corporate & Business Leadership

Benson I. Wairegi EBS

Group Managing Director

“ experienced, dynamic and cohesive leadership team and staff”

Kenneth Kaniu

CEO, Britam Asset Managers

Gladys Karuri

Principal Executive Director, Finance & Strategy

Muthoga Ngera

Director, Marketing & Corporate Affairs

Nancy K. Kiruki,

Director, Legal& Company Secretary

Stephen O. Wandera

Principal Executive Director, Insurance

| Unit Trust Funds | Wealth Management | Pensions | Property

| Discretionary Management | Offshore Investments | Alternative

Investments

7

0.6

1.0%

1.0%

Britam Holdings

Insurance

Business

Asset

Management

Banking

Business

• Life Insurance

• General

Insurance

• Health Insurance

• Pension Business

• Unit Trust Funds

• Discretionary

Portfolio

Management

• Property

• Pensions

• Wealth

Management

• Diaspora

Services

• Equity Bank

Stake – 8.2%

• Housing

Finance Stake –

48.82%

• Britam Properties-

100%

Property

Business

II. Introduction to Britam Asset Managers

| Unit Trust Funds | Wealth Management | Pensions | Property

| Discretionary Management | Offshore Investments | Alternative

Investments

9

James Mose, CFA

Ag Chief Investment

Officer

Asset Management Executive Team

Kenneth Kaniu

Chief Executive

Officer

Janet Waweru ACCA

Chief Accountant

John Etyang

Head, Business

Development

Charles Chirchir

Chief Operating

Officer

Miriam Kahiro

Legal Manager

Dennis Katei

Compliance Manager

Eva Mbora

Human Resources

Manager

| Unit Trust Funds | Wealth Management | Pensions | Property

| Discretionary Management | Offshore Investments | Alternative

Investments

10

Our Business Is Categorized as follows:

• Development Funds

• Income Funds

Asset Management Businesses

Retail Products Institutional Solutions Real Estate

Investments

• Unit Trust Funds

• Wealth Management

• Diaspora Services

• Discretionary Portfolio

Management

• Pension Schemes

| Unit Trust Funds | Wealth Management | Pensions | Property

| Discretionary Management | Offshore Investments | Alternative

Investments

11

Our Approach Is To Understand Client Needs And Apply Our

Resources To Meeting Those Needs, through:

Experienced & World Class Capabilities

Strong Brand & Group Backing

Customized Investment Approach

Diverse Product Set

| Unit Trust Funds | Wealth Management | Pensions | Property

| Discretionary Management | Offshore Investments | Alternative

Investments

12

Our Accolades

Britam Asset Managers Clinched the Fund Manager of the

Year Award in 2011, 2012 and 2013 and the Unit Trust of the

Year Award in 2012, 2013, 2015 and 2016

Think Business Awards 2011-2016

• Unit Trust of the Year, Winner - 2012, 2013, 2015, 2016

• Best Performing Money Market Fund, Winner - 2014, 2016

• Best Performing Equity Fund, 2nd Runner up 2014, Winner,

2015, 2016

• Fund Manager of the Year: Alternative Investments and

Private Equity, Winner - 2014, 2015, 2016

• Fund Manager of the Year: Overall Winner – 2011, 2012,

2013, 2nd Runner up 2014, and 1st Runner up 2015, 2016

• Fund Manager of the Year: Pensions - 1st Runner-up, 2014,

2016

• Fund Manager of the Year: Equity- 1st Runner Up, 2014,

2016, Winner – 2015

• Fund Manager of the Year: Money Market - 1st Runner-up,

2014, 2016

“Our history of success provides

financial security for our clients”

I. Introduction

I. Introduction

II. Factors Affecting Private Sector Credit Growth

Monetary Policy Effects

Fiscal Policy Effects

Asset Quality Effects

III. Summary & Outlook

| Unit Trust Funds | Wealth Management | Pensions | Property

| Discretionary Management | Offshore Investments | Alternative

Investments

14

Economic Growth GDP growth has remained stronger than regional peers

Source:: IMF

Kenya

GDP – USD 68.9bn

Population – 45.5mn

Economies of Kenya and Uganda have outpaced that of peers and the growth has mainly been infrastructure

led

The private sector has however not similarly benefited from the headline growth due to constraints in accessing

funding

1.4%

2.6%

3.5%

5.9%

5.3% 5.8%

4.7% 5.0%

5.8%

0%

1%

2%

3%

4%

5%

6%

7%

2016 2017P 2018F

SSA Kenya Uganda

GDP Growth

| Unit Trust Funds | Wealth Management | Pensions | Property

| Discretionary Management | Offshore Investments | Alternative

Investments

15

Credit Comparison

Kenya and Uganda lags peers in terms of Credit to GDP, implying more room for credit

growth

Source: World Bank ,BAM Research

Kenya

GDP – USD 68.9bn

Population – 45.5mn

Despite the improvement in headline economic growth, credit/GDP still lags behind regional peers, suggesting

greater access to credit can further spur economic growth in the medium term

26%

9%

61%

14%

27%

13%

55%

20%

33%

14%

30% 28%

0%

10%

20%

30%

40%

50%

60%

70%

Kenya Uganda SSA Least DevelopedCountries

Credit to GDP vs Peers

2005 2010 2016

| Unit Trust Funds | Wealth Management | Pensions | Property

| Discretionary Management | Offshore Investments | Alternative

Investments

16

Kenya Private Sector Credit Growth

Private Sector Credit Growth has been slowing down since 2015

Source: CBK, BAM Research

Kenya

GDP – USD 68.9bn

Population – 45.5mn

Private sector credit has been sluggish in the last two years, with growth coming in at 5.1% in 2016 and

contracting by 1.5% in the first 7 months of 2017 – the first incidence of contraction in the last 7 years

1,167 1,293

1,552

1,898

2,224 2,337 2,302

30.4%

10.8%

20.0% 22.3% 17.1%

5.1%

-1.5%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

0

500

1,000

1,500

2,000

2,500

2011 2012 2013 2014 2015 2016 2017 YTD

Private Sector Credit, KES Bns Credit Growth

Kenya Private Sector Credit Growth

YTD 2017 figures as at July 2017

| Unit Trust Funds | Wealth Management | Pensions | Property

| Discretionary Management | Offshore Investments | Alternative

Investments

17

Uganda Private Sector Credit Growth

Credit Growth has been slowing since 2015

Source: BOU, BAM Research

Kenya

GDP – USD 68.9bn

Population – 45.5mn

The same was observed in Uganda where credit growth slowed down similarly over the last two years

At its lowest point, March 2016, credit growth in Uganda had contracted by 1.2% but this has since recovered to

a 0.2% growth in the first six months of 2017

7,269 8,128

8,614

9,826

11,328 12,058 12,085

28.3%

11.8%

6.0%

14.1% 15.3%

6.4%

0.2%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

2011 2012 2013 2014 2015 2016 2017 YTD

Private Sector Credit, UGX Bns Credit Growth

YTD 2017 figures as at June 2017

| Unit Trust Funds | Wealth Management | Pensions | Property

| Discretionary Management | Offshore Investments | Alternative

Investments

18

Kenya Private Sector Credit Breakdown

Access to credit in the real economic sectors remains disproportionately skewed

Source: CBK, BAM Research

Kenya

GDP – USD 68.9bn

Population – 45.5mn

Most sectors of the real economy have disproportionate access to credit, with real estate and trade’s share of

total credit coming in at almost double their relative contribution to the real economy

55% of Kenya’s loans are concentrated in manufacturing, trade, real estate and transport. Agriculture, the biggest

contributor to GDP, remains relatively starved of credit

22%

10%

8% 8% 7%

6% 5%

2% 1% 1%

4%

12%

20%

14%

9%

4% 5% 5%

3% 1%

0%

5%

10%

15%

20%

25%

Agriculture Manufacturing Trade Real Estate Transport FinancialServices

Construction Energy Tourism Mining

% GDP % Credit

Loan Access by sector 2016

| Unit Trust Funds | Wealth Management | Pensions | Property

| Discretionary Management | Offshore Investments | Alternative

Investments

19

Uganda Private Sector Credit Breakdown

Similar to Kenya some sectors remain relatively starved of credit

Source: BOU BAM Research

Kenya

GDP – USD 68.9bn

Population – 45.5mn

Real estate and trade’s share of total credit coming in at almost double their relative contribution to the real

economy

Agriculture and services which have a combined contribution of 44% to GDP remain underserved

23%

13%

9%

12%

5%

21%

10%

19%

14%

23%

8% 8%

0%

5%

10%

15%

20%

25%

Agriculture Trade Manufacturing Building Construction andReal Estate

Transport andCommunication

Services

Proportion of GDP Proportion of Loans

Loan Access by sector 2016

II. Factors Affecting Private Sector Credit Growth

I. Introduction

II. Factors Affecting Private Sector Credit Growth

Policy Effects

• Monetary Policy Effects

• Fiscal Policy Effects

Asset Quality Effects

III. Summary & Outlook

| Unit Trust Funds | Wealth Management | Pensions | Property

| Discretionary Management | Offshore Investments | Alternative

Investments

21

Kenya: Monetary Policy Effects

Credit Growth has been negatively impacted by increased short term rates

Source: Bloomberg, BAM Research

Kenya

GDP – USD 68.9bn

Population – 45.5mn

Increased short term rates have led to depressed credit growth as banks allocate more to government

securities leading to crowding out of the private sector as the government gets preferential credit

The relationship between short term rates and private sector credit growth has however been weak, with

growth remaining at 10% in 2012 despite the spike in short term rates

20.2%

-1.5%

8.6%

10%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

2010 2011 2012 2013 2014 2015 2016 2017

Private Sector Credit Growth 91 Day Tbill Rates CBR

Rates vs. Credit Growth

| Unit Trust Funds | Wealth Management | Pensions | Property

| Discretionary Management | Offshore Investments | Alternative

Investments

22

Kenya: Monetary Policy Effects- Interest Rate Caps

Interest rate capping has been detrimental to credit growth

Source: CBK, BAM Research

Kenya

GDP – USD 68.9bn

Population – 45.5mn

Banks have become more averse to lending since the enactment of the interest rate caps. The effect has been

more severe in 2017 where credit has contracted 1.5% from the levels seen in December 2016.

The direct link between the Central Bank Rate and lending rates has impeded setting of monetary policy due to

the ramifications of any change in CBR to loan pricing

-1.5%

-1.0%

-0.5%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

Jan

Ma

r

Ma

y

Ju

l

Sep

No

v

Jan

Ma

r

Ma

y

Ju

l

Sep

No

v

Jan

Ma

r

Ma

y

Ju

l

Sep

No

v

Jan

Ma

r

Ma

y

Ju

l

Sep

No

v

Jan

Ma

r

Ma

y

Ju

l

Sep

No

v

Jan

Ma

r

Ma

y

Ju

l

2012 2013 2014 2015 2016 2017

Month-on-month Private Sector Credit Growth

5 Year Historical Average = 1.0%

| Unit Trust Funds | Wealth Management | Pensions | Property

| Discretionary Management | Offshore Investments | Alternative

Investments

23

Uganda: Monetary Policy Effects

Similar to Kenya, short term rates have had negative correlation to credit growth

Source: BOU BAM Research

Kenya

GDP – USD 68.9bn

Population – 45.5mn

Rising short term rates have negatively impacted credit growth as banks allocate more to government

securities which are perceived to be risk free unlike loans which have a higher probability of default

From its lowest point, private sector credit has recovered by more than 8% due to the Central Bank’s aggressive

monetary easing

28.3%

0.2%

18.2%

11.2%

14.6% 11.8%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

0%

5%

10%

15%

20%

25%

30%

2011 2012 2013 2014 2015 2016 *June 17

Rates vs. Credit Growth

Private Sector Credit Growth CBR Average 91 day tbill

| Unit Trust Funds | Wealth Management | Pensions | Property

| Discretionary Management | Offshore Investments | Alternative

Investments

24

Kenya: Fiscal Policy Effects

Source: National Treasury, BAM Research

Kenya

GDP – USD 68.9bn

Population – 45.5mn

38%

14%

22%

4%

-2%

38%

14%

20%

31%

10%

20% 22%

17%

5%

-10%

0%

10%

20%

30%

40%

2010 2011 2012 2013 2014 2015 2016

Public Sector Credit Growth Private Sector Credit Growth

Public vs Private Sector Credit Growth

The government has recently been increasing its fiscal deficits, largely due to infrastructure led spending

The Governments increased use of domestic financing has resulted in crowding out of the private sector

Increased fiscal deficits have led to increased domestic borrowing

| Unit Trust Funds | Wealth Management | Pensions | Property

| Discretionary Management | Offshore Investments | Alternative

Investments

25

Source: BOU,BAM Research

Kenya

GDP – USD 68.9bn

Population – 45.5mn

Uganda: Fiscal Policy Effects

The Ugandan government has had a similar pattern to Kenya’s, increasing budget deficit from 3.4% of GDP in

2013 to 6.4% in 2016 thus increasing government borrowing to fund infrastructure spending

However, this has been more pronounced than Kenya which has sourced more external borrowing

36%

-20%

43%

21% 21%

-10%

27%

42%

28%

12% 6%

14% 15%

6%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

2010 2011 2012 2013 2014 2015 2016

Public Sector Credit Growth Private Sector Credit Growth

Public vs Private Sector Credit Growth

Increased fiscal deficits have led to increased government borrowing

II. Factors Affecting Private Sector Credit Growth

I. Introduction

II. Factors Affecting Private Sector Credit Growth

Policy Effects

• Monetary Policy Effects

• Fiscal Policy Effects

Asset Quality Effects

III. Summary & Outlook

| Unit Trust Funds | Wealth Management | Pensions | Property

| Discretionary Management | Offshore Investments | Alternative

Investments

27

Kenya : Asset Quality Effects

Slowing loan growth has coincided with a worsening non performing loans position

Source: CBK; BAM Research

Kenya

GDP – USD 68.9bn

Population – 45.5mn

An overall slowdown in the growth of loans in 2015 and 2016 was followed by a corresponding increase in

non-performing loans necessitating an investigation into developments per sector

21.4%

31.5%

12.5%

18.2%

22.8%

11.2%

4.4% 6.6%

4.6% 4.8% 5.3% 5.8% 7.0%

9.8%

0%

5%

10%

15%

20%

25%

30%

35%

2010 2011 2012 2013 2014 2015 2016

Loan Growth Gross NPL Ratios

Loan Growth vs NPLs

| Unit Trust Funds | Wealth Management | Pensions | Property

| Discretionary Management | Offshore Investments | Alternative

Investments

28

Kenya: Non Performing Loan ratios per sector

Construction, Trade & Agriculture all have above banking sector average NPL ratios

Source: CBK, BAM Research

Kenya

GDP – USD 68.9bn

Population – 45.5mn

Agriculture’s weak asset quality may have been affected by recent drought experience, with trade suffering as a

result of weak consumer demand while construction was influenced by delayed government payments

10% 9%

14%

8% 8%

3%

26%

5%

8% 9%

6% 4%

12%

20%

14%

9%

4% 5% 5%

3% 1%

25%

0%

5%

10%

15%

20%

25%

30%

Agriculture Manufacturing Trade Real Estate Transport FinancialServices

Construction Energy Tourism Mining Household

NPL Ratio % Credit

NPLs Ratios per sector

Figures are as at 31st December 2016

| Unit Trust Funds | Wealth Management | Pensions | Property

| Discretionary Management | Offshore Investments | Alternative

Investments

29

Kenya: Historical Evolution of NPLs

Construction & Trade had significantly better asset quality historically

Source: CBK, BAM Research

Kenya

GDP – USD 68.9bn

Population – 45.5mn

Historical performance of construction & trade sectors points to their relatively large shares of credit in the

banking sector, as these have had lower NPLs than other sectors

10% 9%

14%

8% 8%

3%

26%

5%

8% 9%

6% 7%

3% 4% 4%

3% 2%

4%

1%

7%

1%

6%

0%

5%

10%

15%

20%

25%

30%

Agriculture Manufacturing Trade Real Estate Transport FinancialServices

Construction Energy Tourism Mining Household

2016 2011

NPL Ratio Evolution

| Unit Trust Funds | Wealth Management | Pensions | Property

| Discretionary Management | Offshore Investments | Alternative

Investments

30

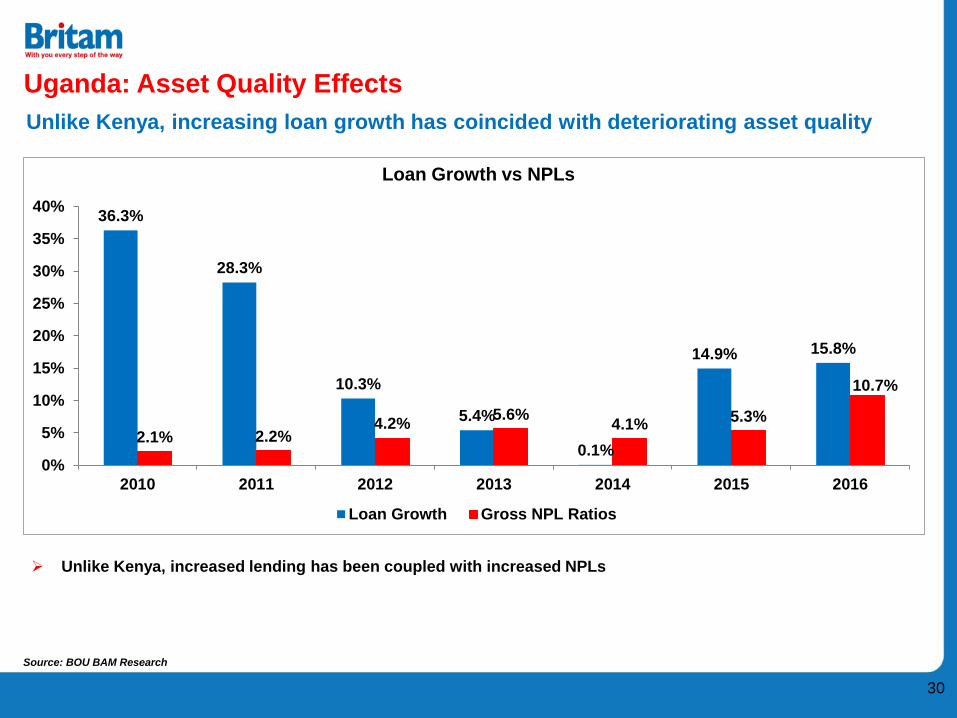

Uganda: Asset Quality Effects

Unlike Kenya, increasing loan growth has coincided with deteriorating asset quality

Source: BOU BAM Research

Kenya

GDP – USD 68.9bn

Population – 45.5mn

Unlike Kenya, increased lending has been coupled with increased NPLs

36.3%

28.3%

10.3%

5.4%

0.1%

14.9% 15.8%

2.1% 2.2% 4.2%

5.6% 4.1%

5.3%

10.7%

0%

5%

10%

15%

20%

25%

30%

35%

40%

2010 2011 2012 2013 2014 2015 2016

Loan Growth Gross NPL Ratios

Loan Growth vs NPLs

| Unit Trust Funds | Wealth Management | Pensions | Property

| Discretionary Management | Offshore Investments | Alternative

Investments

31

Uganda: Non Performing Loans per sector

Agriculture and Construction have the highest NPL ratios

Source: BOU, BAM Research

Kenya

GDP – USD 68.9bn

Population – 45.5mn

Similar to Kenya, agriculture, trade and construction’s NPL ratios remain above average

10%

15%

18% 16%

24%

12%

6%

11%

4%

12%

0%

5%

10%

15%

20%

25%

Agriculture Manufacturing Trade Household Construction

% Credit NPLs

NPLs Ratios per sector

Figures are as at 31st December 2016

| Unit Trust Funds | Wealth Management | Pensions | Property

| Discretionary Management | Offshore Investments | Alternative

Investments

32

Uganda: Historical Evolution of NPLs

NPL ratios have increased across all sectors in Uganda

Source: CBK, BAM Research

Kenya

GDP – USD 68.9bn

Population – 45.5mn

Historical NPL ratios point to a fundamental problem in the credit environment in Uganda. We believe this could

be a direct result of being in an economic downturn, which the BOU has been trying to reverse with loose

monetary policy – we expect to see improvement across the sectors in 2017

12%

6%

11%

4%

12%

2%

0% 1% 2% 1%

0%

2%

4%

6%

8%

10%

12%

14%

Agriculture Manufacturing Trade Household Construction

2016 2011

NPLs Ratio Evolution

III. Summary & Outlook

I. Introduction

II. Factors Affecting Private Sector Credit Growth

Monetary Policy Effects

Fiscal Policy Effects

Asset Quality Effects

III. Summary & Outlook

| Unit Trust Funds | Wealth Management | Pensions | Property

| Discretionary Management | Offshore Investments | Alternative

Investments

34

Summary: Influences on Private Sector Credit Growth

Private Sector Credit Growth has mainly been influenced by asset quality & fiscal policy

Asset Quality Monetary

Policy Fiscal Policy

Mainly through

movement in short

term interest rates

Mainly through

crowding out of

private sector

Mainly through banks’

credit appetite

Affects both demand

and supply of credit Affects supply of

credit

Affects Supply

Kenya: Fiscal policy and asset quality have been the main influences on private sector credit growth

in 2016-17 with the Central Bank unable to utilize monetary policy to drive increased lending

Uganda: The same has been observed in Uganda. However, private sector credit growth has seen a

recovery from mid 2016 since the Bank of Uganda has been able to effectively employ monetary

policy to boost growth

| Unit Trust Funds | Wealth Management | Pensions | Property

| Discretionary Management | Offshore Investments | Alternative

Investments

35

Way Forward

A combination of policy & lending reforms will be required to improve credit growth

Monetary Policy

Fiscal Policy

Fiscal consolidation will significantly reduce crowding out of the private

sector which will provide greater incentive for banks to grow their loan

books

Prioritization of investment spending while including the private sector will

ensure inclusive and sustainable growth

Asset Quality

Kenya: Adoption of market-based policies such as reversal or

amendment of the interest rate caps in Kenya would allow banks to

adequately price for credit risk thus spurring private sector credit growth

Uganda: Sustained loose policies will continue to support the rebound in

growth of credit to real sectors of the economy

Enhanced risk and credit assessment as well as improved information

sharing to more easily identify good borrowers and reduce underwriting

risk

Diversifying loan book exposures could dampen the effects of weak asset

quality in specific sectors of the economy

| Unit Trust Funds | Wealth Management | Pensions | Property

| Discretionary Management | Offshore Investments | Alternative

Investments

36

Risks Going Forward

Several risks remain which could further slow down private sector credit growth

Regulatory Risk:

• Implementation of IFRS 9: Expected to come into effect from January 2018. It will increase

the threshold of provisions for impairment losses thereby requiring banks to hold a more

capital buffers to cushion the loan loss allowances following its implementation

• Interest Rate Caps: The longer the rate caps stay in place the greater the magnitude of

credit contraction which further puts the anticipated economic growth at risk

Political Risk: Outcome of elections remains uncertain which in turn affects business output in

the country

Economic underperformance: Prolonged periods of extreme weather conditions continues to

place pressure on the performance of Agriculture which remains a significant contributor to GDP

| Unit Trust Funds | Wealth Management | Pensions | Property

| Discretionary Management | Offshore Investments | Alternative

Investments

37

Recap

Repeal of interest rate caps will help in improving private sector credit growth

Weak Private Credit Growth

Interest Rate Caps

Declining Asset

Quality

Increased government borrowing

THANK YOU

With you every step of the way