demographic change and expenditure pressures in ireland

TRANSCRIPT

Demographic Change and Projections for the Public Finances over the Medium Term

Thomas Conefrey NERI Economics Seminar, 13 January 2016

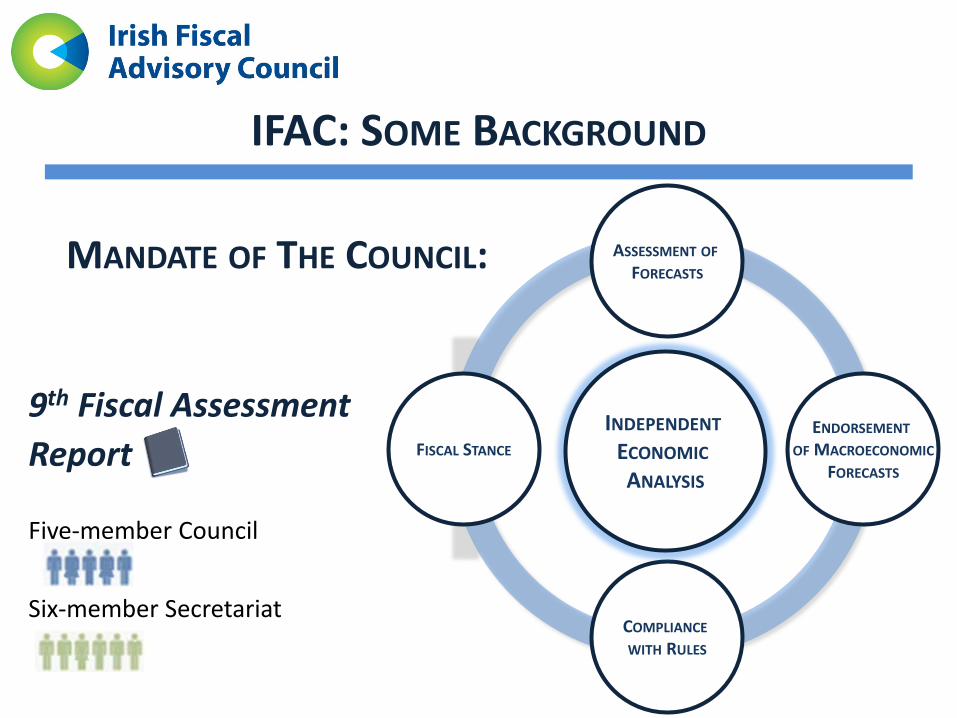

IFAC: SOME BACKGROUND

MANDATE OF THE COUNCIL:

9th Fiscal Assessment Report

Five-member Council

Six-member Secretariat

ASSESSMENT OF FORECASTS

COMPLIANCE WITH RULES

FISCAL STANCE ENDORSEMENT

OF MACROECONOMIC FORECASTS

INDEPENDENT ECONOMIC ANALYSIS

Outline • Review of recent macroeconomic and fiscal

performance (IFAC Fiscal Assessment Report, November 2015).

• Rationale for medium-term fiscal forecasts. • Estimating medium-term demographic change

and implications for public spending. • Assessment of medium-term budgetary

forecasts.

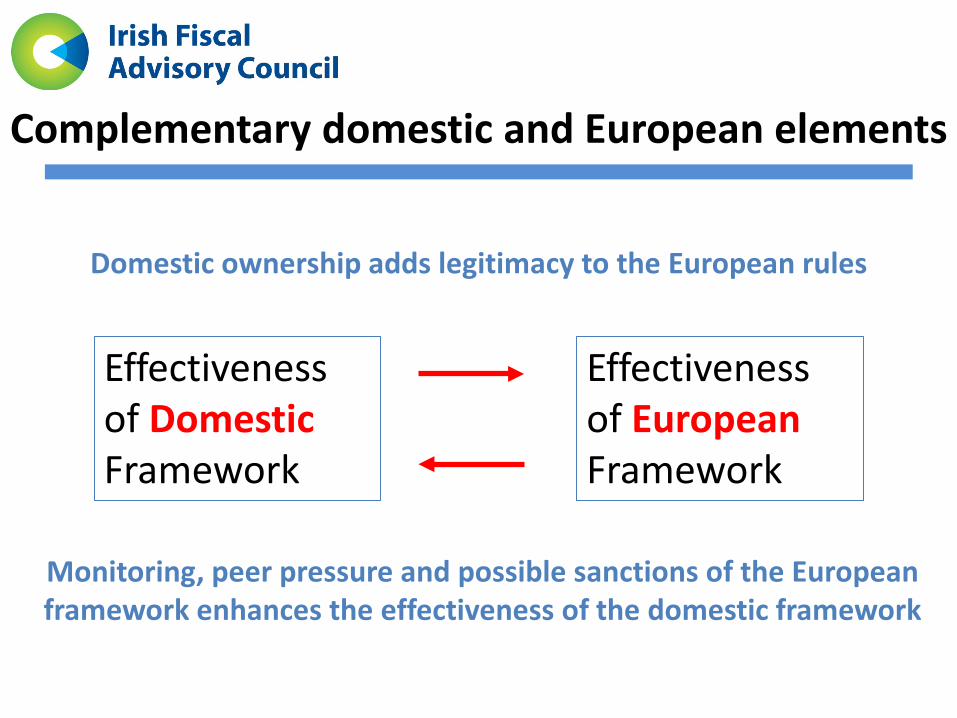

European/Domestic fiscal rules

Domestic

European

Corrective Arm of SGP

Preventive Arm of SGP

3% Deficit Rule

1/20th Debt Rule

MTO / Adjustment path to MTO

Expenditure benchmark

Domestic Budgetary

Rule

Domestic Expenditure

Ceilings

Domestic Budgetary Rule Consistent with Preventive

Arm of SGP

Domestic Expenditure Ceilings Consistent with Expenditure Benchmark

Complementary domestic and European elements

Effectiveness of Domestic Framework

Effectiveness of European Framework

Monitoring, peer pressure and possible sanctions of the European framework enhances the effectiveness of the domestic framework

Domestic ownership adds legitimacy to the European rules

REAL GDP, REAL GNP AND EMPLOYMENT GROWTH (% CHANGE Y-Y)

STRONG RECOVERY AND CENTRAL GROWTH FORECASTS

-10

-8

-6

-4

-2

0

2

4

6

8

10

12

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

% C

hang

e Y-

Y

Real GDP

Real GNP

Employment

Sources: Department of Finance (Budget 2016); CSO.

Increasing contribution of domestic demand to recovery

Source: CSO.

9.4

8.8

18.2

-10

-5

0

5

10

15

20

2010 2011 2012 2013 2014 2015

% G

row

th S

ince

Tro

ugh

in Q

2 20

09

CUMULATIVE CONTRIBUTION TO REAL GDP GROWTH SINCE TROUGH

Residual Domestic Demand

Net Exports Real GDP

Evidence of rebalancing

0%

5%

10%

15%

20%

25%

30%

35%

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

% OF NOMINAL GDP

Investment

Net Exports

Source: CSO.

Current account near balance excluding re-domiciled PLCs

-0.4 -0.6 -1.0

0.5 -0.1

-3.3

-4.9

-6.1 -5.8

-4.1

-0.8 -1.2

-1.5

3.1 3.6

-5.1

-3.9 -4.5

-5.7

-0.2

-8

-6

-4

-2

0

2

4

6

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

% G

DP

Current Account Balance

Adjusted for Re-domiciled PLCs

National Income and Consumption per Head

10

15

20

25

30

35

40

45

50

55

€ ,0

00

Macro indicators per head, real

Consumption GDP GNP

Sources: CSO and Department of finance forecasts.

Sharper downturn + recovery than trading partners

60

65

70

75

80

85

90

95

100

105

110

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Inde

x: 2

007

= 10

0

REAL GDP PER CAPITA

IE UK

US EA

Sources: CSO; IMF and internal calculations.

Employment Rate

40

45

50

55

60

65

70

75

80

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

(lat

est)

%of

15-

64 p

opul

atio

n

Employment rate, % of 15-64 population

Ireland United Kingdom

Source: CSO and Eurostat.

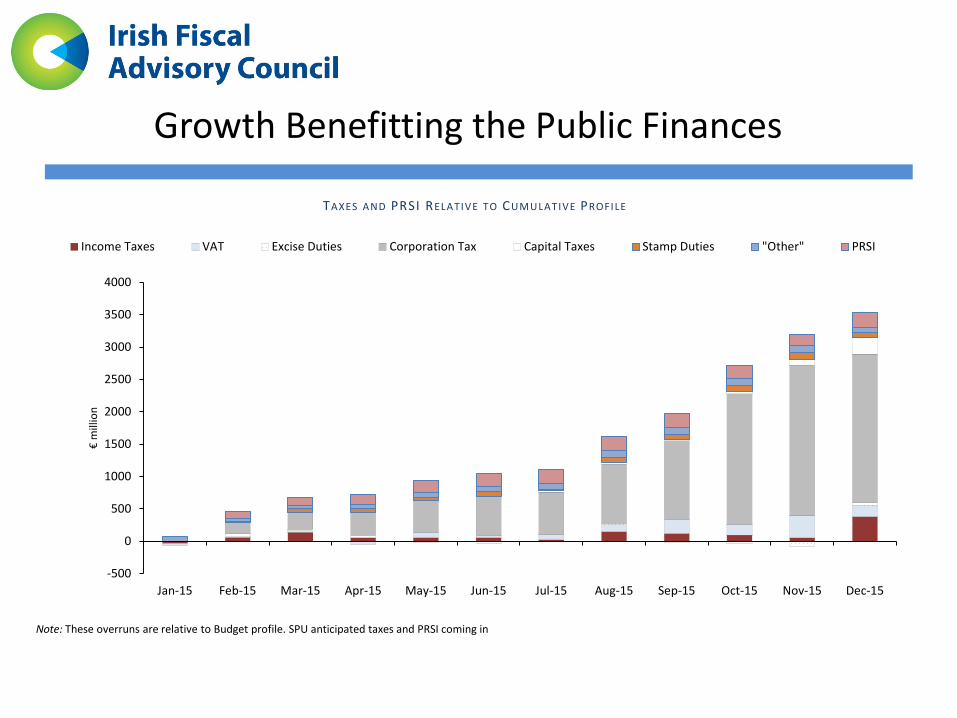

Growth Benefitting the Public Finances

-500

0

500

1000

1500

2000

2500

3000

3500

4000

Jan-15 Feb-15 Mar-15 Apr-15 May-15 Jun-15 Jul-15 Aug-15 Sep-15 Oct-15 Nov-15 Dec-15

€ m

illio

n

TAXES AND PRSI RELATIVE TO CUMULATIVE PROFILE

Income Taxes VAT Excise Duties Corporation Tax Capital Taxes Stamp Duties "Other" PRSI

Note: These overruns are relative to Budget profile. SPU anticipated taxes and PRSI coming in

Exchequer Tax Revenue

- 5

10 15 20 25 30 35 40 45 50

Jan-

95N

ov-9

5Se

p-96

Jul-9

7M

ay-9

8M

ar-9

9Ja

n-00

Nov

-00

Sep-

01Ju

l-02

May

-03

Mar

-04

Jan-

05N

ov-0

5Se

p-06

Jul-0

7M

ay-0

8M

ar-0

9Ja

n-10

Nov

-10

Sep-

11Ju

l-12

May

-13

Mar

-14

Jan-

15N

ov-1

5

€ bi

llion

ANNUALISED EXCHEQUER TAX RECEIPTS 1995-2015

Source: Department of Finance.

EXCESSIVE DEFICIT CLOSED IN 2015

0.3

-7.0

-11.5 -11.0

-8.4 -7.9

-5.7

-3.9

-2.1 -1.2

-14

-12

-10

-8

-6

-4

-2

0

2

4

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

% o

f GDP

Primary Balance

Interest

General Government Balance

EDP Ceiling

Source: CSO; Budget 2016.

GENERAL GOVERNMENT BALANCE (% GDP)

REAL GDP FAN CHART BASED ON BUDGET 2016 PROJECTIONS (TO 2016)

BUT SIGNIFICANT RISKS AROUND CENTRAL FORECASTS

-6

-4

-2

0

2

4

6

8

2008 2009 2010 2011 2012 2013 2014 2015 2016

% C

hang

e Y-

Y

80% likelihood range60% likelihood range40% likelihood range20% likelihood rangeOfficial Outturns / Central Forecasts

Sources: CSO; Department of Finance; internal IFAC calculations. Note: Distributions or 'fans' around historical growth estimates are based on previous revisions to real GDP data. Both forecast errors and revisions are based on 1999-05 sample.

CRISIS LEGACY OF HIGH DEBT AND ASSOCIATED RISKS

76.0

84.2

62.5

69.3

0

20

40

60

80

100

120

140

160

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Gross Debt (% GDP)Gross Debt (% Hybrid)Net Debt (% GDP)Net Debt (% Hybrid)

Sources: Department of Finance; internal IFAC calculations. Note: Changes in EDP debt instrument assets for forecast years are assumed to be in line with Budget 2016 projected changes in cash balances.

GENERAL GOVERNMENT DEBT

Outlook

Short Term • Policy vigilance and economic growth have helped to improve

the public finances – But significant risks surround the forecasts.

– Importance of prudence to ensure sustainable growth.

Medium Term • Key weakness remains the absence of realistic medium-term

projections for the public finances. • Projections for expenditure, tax revenue, deficit and debt based

largely on technical assumptions. • With period of crisis management and repair coming to an end,

opportunity to re-focus on medium term.

Why are Medium-Term Budgetary Plans Important?

• Budgetary process has focussed attention excessively on one-year ahead.

• This has contributed to pattern of procyclicality in Irish fiscal policy.

• Medium-term fiscal plans are required in order to: – Provide a medium-term anchor for the public finances and

avoid the risk that incoming cyclical revenues are spent. – Increase the predictability of the budgetary planning

process. – Provide a link between resource allocation and

Government policy and priorities. • Key theme of recent Fiscal Assessment Reports

Deviations from Expenditure Plans

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2009* 2010 2011 2012 2013 2014 2015

% d

evia

tion

GROSS CURRENT EXPENDITURE, % DEVIATION FROM FORECAST

Yr1 % Deviation Yr2 % Deviation

Yr3 %Deviation Real GDP growth

Budget Year

Source: Department of Finance Note: * denotes the Supplementary budget in 2009. Bars show the forecast error for 1 year ahead, 2 years ahead and 3 years ahead. Latest figures for 2016 to 2018 (used in calculation the latest deviation from Budget 2015 years 2 and 3) are adjusted by €1 billion to reflect the change in the treatment of the HSE from 2015. This adjustment is made for comparison purposes.

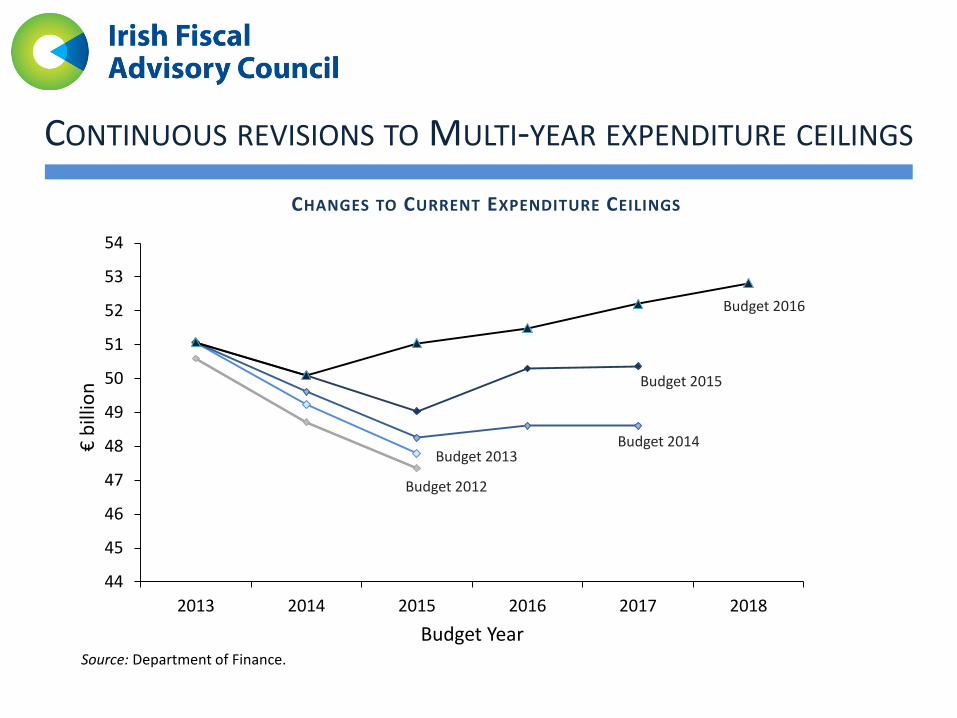

44

45

46

47

48

49

50

51

52

53

54

2013 2014 2015 2016 2017 2018

€ bi

llion

Budget Year Source: Department of Finance.

Budget 2012

CONTINUOUS REVISIONS TO MULTI-YEAR EXPENDITURE CEILINGS

CHANGES TO CURRENT EXPENDITURE CEILINGS

Budget 2013 Budget 2014

Budget 2015

Budget 2016

Medium-Term Fiscal Plan in Budget 2016

• Budget 2016 medium-term fiscal projections include: – €0.4 billion per annum for demographic pressures – Cost of Lansdowne Road Agreement until 2018

• Tax forecasts allow for indexation but assume no change in policy, despite stated commitments to reduce taxes.

• Medium-term plans imply over-compliance with fiscal rules although stated policy is for minimum compliance.

• Develop an alternative medium-term expenditure scenario for 2015-2021

• Scenario takes into account estimated demographic changes and assumptions on the cost of providing public services based on Budget 2016 macro projections.

Budget 2016 Projections imply Steep Fall in Primary Spending

20

25

30

35

40

45

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

% o

f GDP

Government Revenue and Primary Expenditure, % of GDP

Primary expenditure/GDP Revenue/GDP

Note: Chart shows Exchequer revenue and primary expenditure as a share of GDP. Source: Budget 2016 and internal IFAC calculations.

Methodology: Steps

1. Produce baseline demographic projections using Cohort Component Method.

2. Demographic scenario with projections of population by age used as input into long-term fiscal model.

3. Volume of public expenditure linked to demographics, price indexed to relevant deflators.

4. Compare resulting scenario to Budget 2016 projections and estimates of fiscal space.

Medium-Term Demographic Projections

• First step in producing alternative expenditure scenario is to develop baseline population projections.

• Cohort Component Method used to build basic demographic model.

• Most frequently used methodology for projections. • UK Office for National Statistics, AWG, CSO, Smith (2013). • Provides projections not only of total population but also of

demographic composition and individual components of growth by age and gender

• The cohort component equation describes population at time

t+1 as today’s population varied with changes in births, deaths, and net migration:

Overview of the Cohort Component Method

Launch Year Population (CSO 2015)

Survived Population

Projected Migration

Budget 2016, Dept. Finance.

Survival Rates (CSO 2015)

Child-bearing Population (Females, 15 – 54)

Survived Births

Projected Population

Survival Rates for Under 1 year old

(CSO, 2015)

Fertility Rates (EUROPOP, 2013)

Steps 1. Calculate the number of people in the base

population that survive to the next age interval. 2. Project migration flows for each year and add

them to the survived population. 3. Project the number of births occurring during

the projection interval. 4. Add the number of births to the rest of the

population to get a projection of the total population by gender and age for each projection 1 year interval.

Assumptions • Projections for the population structure involve assumptions about

mortality, migration, and fertility. For our basic projections we assume :

1. Mortality: estimated by applying the survival rates from recently released CSO Irish Life Tables (CSO, 2015).

2. Fertility: ASFR used to calculate births. Fertility assumptions in line with EC AWG (2015) and imply slight decrease in fertility rate to 1.98 by 2065. Immigrants face same age-specific fertility rate (CSO, 2013).

3. Migration: most difficult component to estimate. Number of options for migration projections:

• Use CSO (2013) judgemental projections • Model migration (ESRI) • Use Department of Finance projections

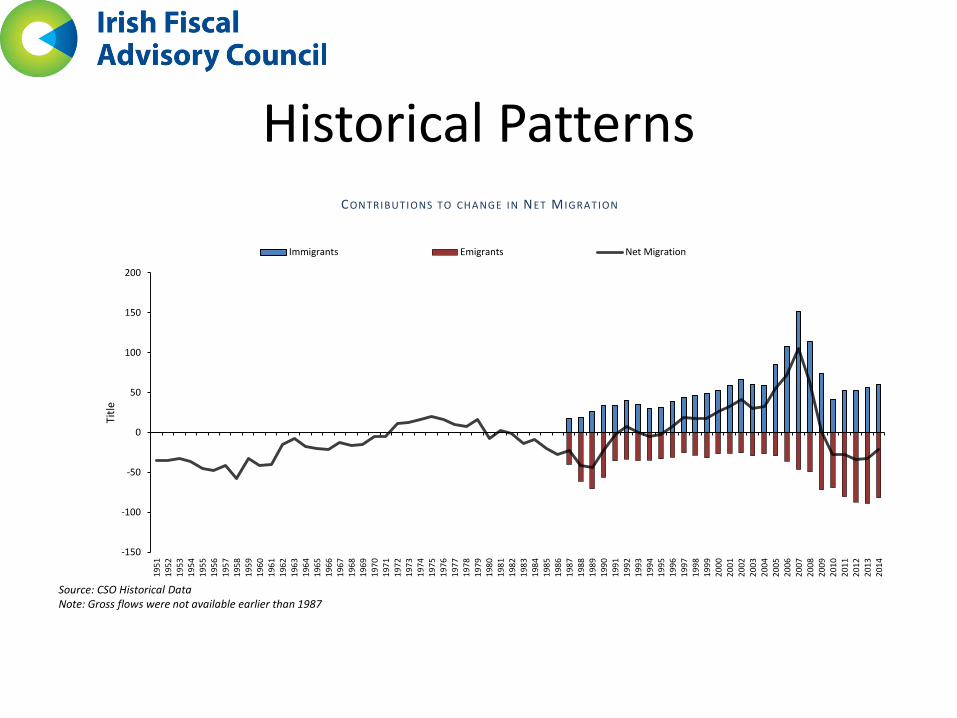

Historical Patterns

-150

-100

-50

0

50

100

150

200

1951

1952

1953

1954

1955

1956

1957

1958

1959

1960

1961

1962

1963

1964

1965

1966

1967

1968

1969

1970

1971

1972

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

Title

CONTRIBUTIONS TO CHANGE IN NET MIGRATION

Immigrants Emigrants Net Migration

Source: CSO Historical Data Note: Gross flows were not available earlier than 1987

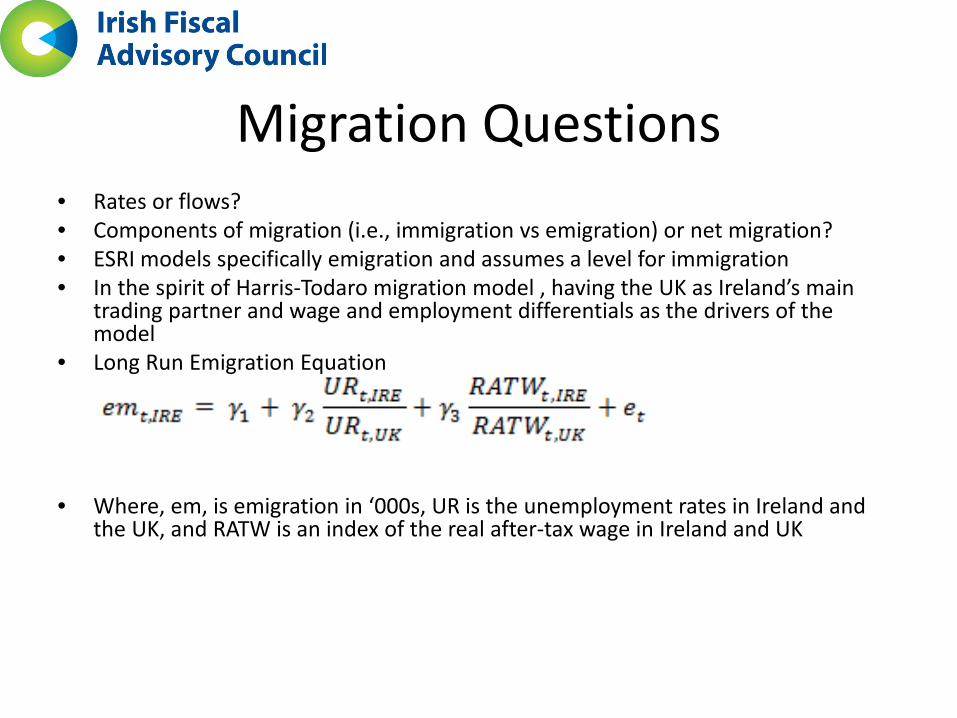

Migration Questions • Rates or flows? • Components of migration (i.e., immigration vs emigration) or net migration? • ESRI models specifically emigration and assumes a level for immigration • In the spirit of Harris-Todaro migration model , having the UK as Ireland’s main

trading partner and wage and employment differentials as the drivers of the model

• Long Run Emigration Equation

• Where, em, is emigration in ‘000s, UR is the unemployment rates in Ireland and the UK, and RATW is an index of the real after-tax wage in Ireland and UK

Baseline Demographic Scenario

-1.5%

-1.0%

-0.5%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

-60

-40

-20

0

20

40

60

80

100

120

140

160

1951

1953

1955

1957

1959

1961

1963

1965

1967

1969

1971

1973

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

2013

2015

2017

2019

2021

2023

2025

2027

2029

2031

2033

2035

2037

2039

2041

2043

2045

2047

2049

'000

Annual Population change

growth in '000 % growth (rhs)

Dependency Ratios

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

% o

f wor

king

age

pop

ulat

ion

Year

Dependency Ratios

Very Old age dependency ratio (80+)

Old age dependency ratio (65+)

Youth dependency ratio (0-14)

Total dependency ratio

Share of People 65+

Note: The dependency ratio is an age-population ratio of those typically not in the labor force (the dependent part) and those typically in the labor force (the productive part). It shows the pressure on the productive part of the population. For the estimation of the “Total Dependency Ratio” we took into account the share of the population over 65 and under 14 divided by the rest of the population. Source: CSO, EUROSTAT, Author’s own Estimations

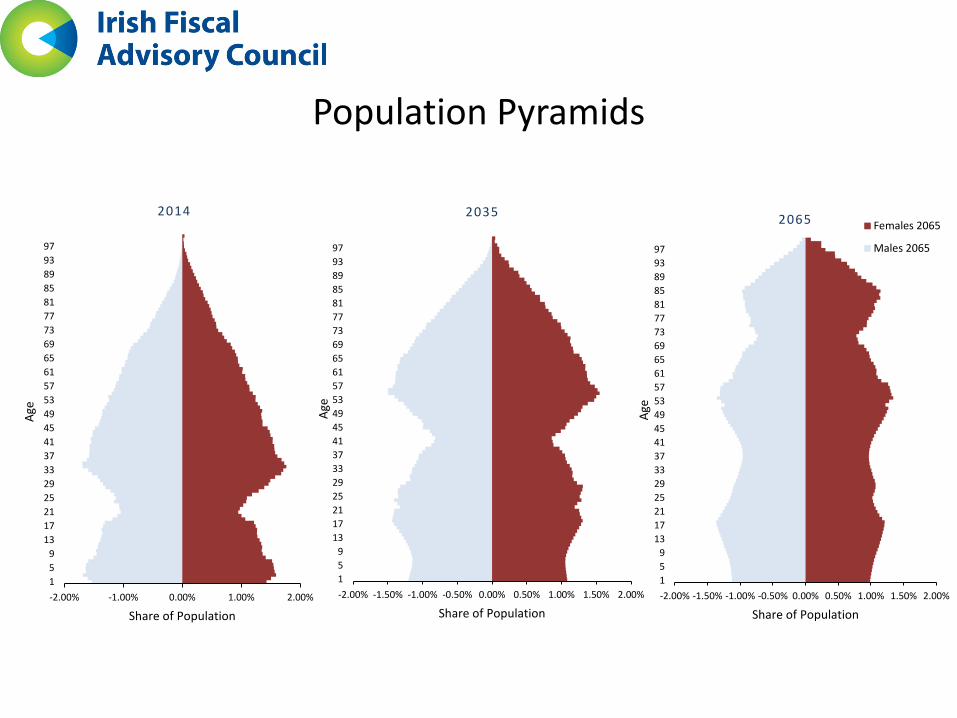

Population Pyramids

-2.00% -1.00% 0.00% 1.00% 2.00%159

13172125293337414549535761656973778185899397

Share of Population

Age

2014

-2.00% -1.50% -1.00% -0.50% 0.00% 0.50% 1.00% 1.50% 2.00%159

13172125293337414549535761656973778185899397

Share of Population

Age

2035

-2.00% -1.50% -1.00% -0.50% 0.00% 0.50% 1.00% 1.50% 2.00%159

13172125293337414549535761656973778185899397

Share of Population

Age

2065 Females 2065

Males 2065

Medium-Term Expenditure Scenario

• Baseline demographic projections used to construct expenditure scenario. • Macroeconomic assumptions from Budget 2016. • Government expenditure split into five components: Health, Education,

Social Payments, Capital Expenditure, National Debt Interest. • Pay: LRA until 2018, thereafter public sector pay grows in line with non-ag

wages and expected service demand. • Non-pay: in health, education grow in line with expected demand linked to

demographics. • Social Protection: split into four broad components: old age, child related

payments, unemployment and other. • Capital expenditure: projections based on Infrastructure and Capital

Investment Plan 2016-2021. • Debt interest: average interest rate from Budget 2016 applied to

difference between Exchequer balance projections.

Capital Expenditure

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

f20

17f

2018

f20

19f

2020

f20

21f

grow

th in

spen

ding

Departmental Capital Expenditure, % of GDP

Capital spending, % of GDP

Average 1983-2015

Source: Budget 2016, Budget and Economic Statistics (Department of Finance).

Comparison of Expenditure Scenarios

20%

22%

24%

26%

28%

30%

32%

2015 2016 2017 2018 2019 2020 2021

% o

f GDP

Primary expenditure, % of GDP - Budget 2016 Primary expenditure, % of GDP - IFAC Scenario 1

Primary expenditure, % of GDP - IFAC Scenario 2

Note: Scenario 1 allows for demographic change with no indexation. Scenario 2 allows for demographic change plus indexation. Source: Internal IFAC calculations.

COMPARISON OF PRIMARY EXPENDITURE UNDER ALTERNATIVE SCENARIOS

Budget Projections imply Steep Fall in Primary Spending

20

25

30

35

40

45

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

% o

f GDP

Government Revenue and Primary Expenditure, % of GDP

Primary expenditure/GDP

Revenue/GDP

Primary expenditure/GDP, IFAC Scenario

Note: Chart shows Exchequer revenue and primary expenditure as a share of GDP. Source: Budget 2016 and internal IFAC calculations.

Expenditure Scenario and Estimated Fiscal Space

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

2017 2018 2019 2020 2021

grow

th in

spen

ding

Estimated Expenditure Pressures Compared With Allowable Expenditure Growth

Allowable Expenditure Growth Expenditure Pressures

Source: Internal IFAC calculations. Note: Expenditure pressures are estimated under the assumptions outline in Box E. Allowable expenditure refers to expenditure growth that would be compliant with the Expenditure Benchmark. The calculation of allowable expenditure growth assumes indexation of the income tax system. If the Government decides not to fully index income tax bands, this would create additional fiscal space.

Conclusion • Significant progress made in resolving Ireland’s fiscal crisis. • Encouraging central scenario for projected growth. • But significant risks around that scenario in environment of

elevated uncertainty. • Realistic medium-term fiscal plans needed to avoid repeat of past

mistakes. • Need for comprehensive bottom-up medium-term expenditure

projections and comparison to likely fiscal space. • Ongoing work:

– Impact of demographics on long-run growth. – Link demographics and macro scenario with the fiscal model. – Incorporate results of research on pensions, health projections from

ESRI, IGEES.