deloitte debt & capital advisory - enterprise ireland · © 2014 deloitte & touche. all...

TRANSCRIPT

Deloitte Debt & Capital

Advisory

Presentation to Enterprise

Ireland

November 2014

© 2014 Deloitte & Touche. All rights reserved

Debt Advisory

Independent financing advice

2

Agenda Page

Introductions 3

What We Do For Our Clients 5

Case Study of Recent Transaction, Signs of a cash crises and Types of

Insolvencies 8

Overview of Bank and Capital Markets 14

Q&A 24

David Martin

Director

Office: +353 1 417 2522

Mobile: +353 86 839 2658

Email: [email protected]

Breandán O Callarán

Senior Manager

Office: +353 1 417 5721

Mobile: +353 87 124 7724

Email: [email protected]

Gordon Naughton

Manager

Office: +353 1 417 8588

Mobile: +353 87 7485060

Email: [email protected]

Introduction

© 2014 Deloitte & Touche. All rights reserved

Gordon Naughton

Manager

Debt & Capital Advisory

T: +353 1 4178588

M: +353 87 748 5060

Deloitte Debt & Capital Advisory A team with significant Corporate Finance and Banking experience

Breandán O Callarán

Senior Manager

Debt & Capital Advisory

T: + 353 1 4175721

M: +353 87 124 7724

Breandán Ó Callarán is a Senior Manager in

Corporate Finance Debt Advisory in Deloitte,

having joined in July 2012. Prior to joining

Deloitte, Breandán spent six years in Bank

of Ireland Corporate Banking, managing

banking relationships for a large number of

mid-market and SME companies across a

broad range of industries and sectors,

including; construction, retail, food &

beverage, hospitality & leisure and

healthcare.

Breandán is a member of the Institute of

Chartered Accountants in Ireland (ACA), the

Association of Chartered Certified

Accountants in Ireland (ACCA) and of the

Institute of Bankers in Ireland.

Gordon joined Deloitte in 2013 and is a

Manager in Debt and Capital Advisory

team. Gordon is a member of the Institute of

Chartered Accountants in Ireland (ACA) and

of the Institute of Bankers in Ireland.

Prior to joining Deloitte, Gordon spent six

years with AIB in both business and

corporate banking specialising in the SME

market. He previously worked for PwC for

four years.

David Martin

Director

Debt & Capital Advisory

T: +353 1 4172522

M: +353 86 839 2658

David Martin is a Director in the Corporate

Finance Advisory Services Division of

Deloitte , having joined the firm in March

2014. Prior to joining Deloitte, David was

with Bank of Ireland for 8 years working in

Business and Corporate Banking s. David is

a Fellow of the Institute of Chartered

Accountants in Ireland.

David originated, structured and managed

numerous debt facilities on a bilateral, club

and syndicated basis across a wide range of

trading sectors including hospitality &

leisure, real estate, healthcare, medical

devices, beverage and software sectors.

Since joining Deloitte David has worked on a

number Central Bank of Ireland assignments

and is currently advising a number of

companies across a broad range of sectors

including hospitality, manufacturing as well

as working as a coach for the Deloitte Best

Managed Companies Awards.

4

What We Do For Our Clients

© 2014 Deloitte & Touche. All rights reserved

• Negotiate with the loan acquirer on the Borrowers’ behalf in determining an exit price, and

managing the exit process from incumbent bank to new lenders.

Potential new to bank customer:

Existing loans acquired by a

loan acquirer

• Separating the property debt from the business to provide a viable lending proposition for

the existing or new Bank.

Strong underlying cash-flows:

Unsustainable property debt

overhang

• Work with the client in understanding their cash-flow requirements, improve cash-flow

management, and recommend appropriate funding structure.

Strong EBITDA generation:

Poor cash-flow management

Strong business:

Poor MI provided to bank

• Work with client to provide appropriate MI, that in turn will support a viable lending

proposition.

• Work with client to develop a viable lending proposition that has the flexibility to introduce

junior debt and/or equity to part fund the expansion funding e.g. (NPRF / HNW).

Strong growth prospects:

Insufficient equity input/ over

reliance on bank funding

How we can assist you Providing solutions

Typical Issues How Deloitte can help

• Together with our in-house experts (M&A, tax, etc.), work with the client in determining an

efficient exit mechanism that makes sense for owners and other key stakeholders.

Good Business:

Little or no visibility on

succession/exit Plan

Existing Client:

Covenant Breach

• Work with client in determining why covenant breach occurred and create options report to

include potential actions to include additional equity, security, margin, deleveraging, re-

financing etc.

6

© 2014 Deloitte & Touche. All rights reserved

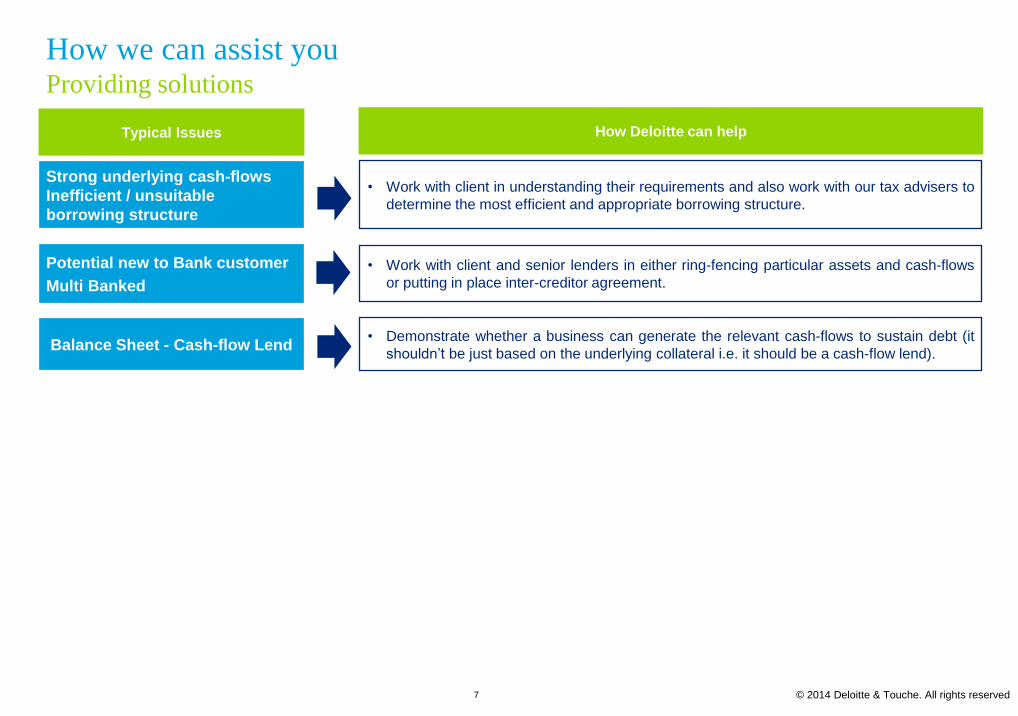

• Work with client in understanding their requirements and also work with our tax advisers to

determine the most efficient and appropriate borrowing structure.

Strong underlying cash-flows

Inefficient / unsuitable

borrowing structure

• Demonstrate whether a business can generate the relevant cash-flows to sustain debt (it

shouldn’t be just based on the underlying collateral i.e. it should be a cash-flow lend). Balance Sheet - Cash-flow Lend

• Work with client and senior lenders in either ring-fencing particular assets and cash-flows

or putting in place inter-creditor agreement.

Potential new to Bank customer

Multi Banked

How we can assist you Providing solutions

Typical Issues How Deloitte can help

7

Case Studies of Recent Transactions, Signs of a cash crises and Types of Insolvencies

© 2014 Deloitte & Touche. All rights reserved

Deloitte Debt Advisory Case Studies

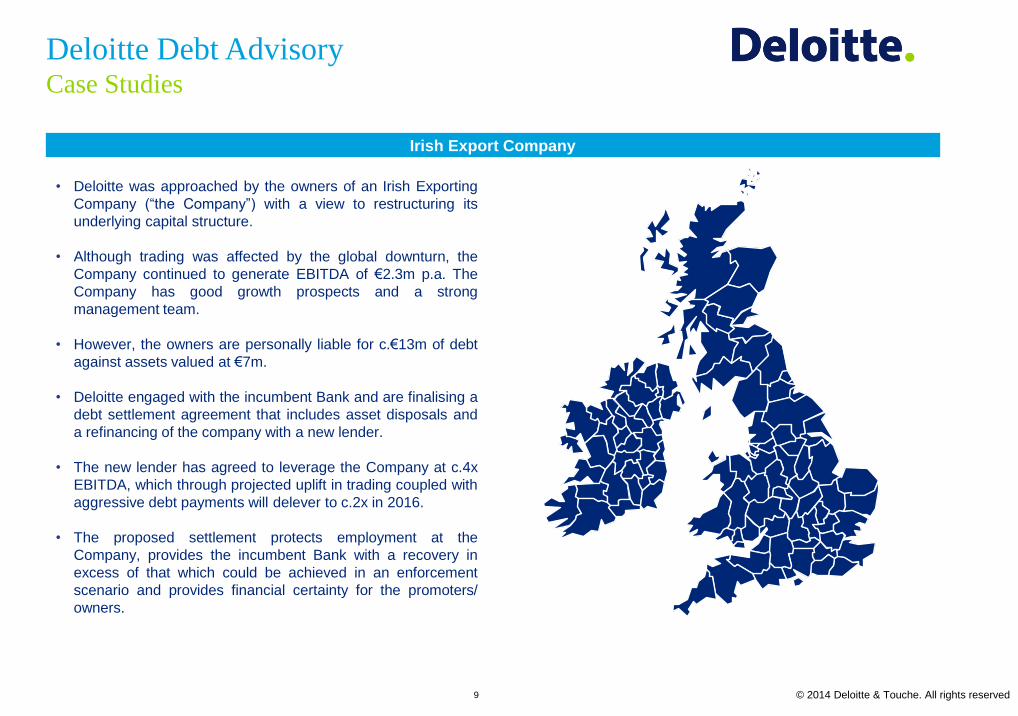

Irish Export Company

• Deloitte was approached by the owners of an Irish Exporting

Company (“the Company”) with a view to restructuring its

underlying capital structure.

• Although trading was affected by the global downturn, the

Company continued to generate EBITDA of €2.3m p.a. The

Company has good growth prospects and a strong

management team.

• However, the owners are personally liable for c.€13m of debt

against assets valued at €7m.

• Deloitte engaged with the incumbent Bank and are finalising a

debt settlement agreement that includes asset disposals and

a refinancing of the company with a new lender.

• The new lender has agreed to leverage the Company at c.4x

EBITDA, which through projected uplift in trading coupled with

aggressive debt payments will delever to c.2x in 2016.

• The proposed settlement protects employment at the

Company, provides the incumbent Bank with a recovery in

excess of that which could be achieved in an enforcement

scenario and provides financial certainty for the promoters/

owners.

9

© 2014 Deloitte & Touche. All rights reserved

2014

Debt refinancing and debt advisory

services to Russell Court Hotel

€8m

Ireland

Deloitte Debt Advisory A selection of our credentials

2014 Ireland

€0.250m

Ireland

High Net Worth Individual

2014

Financial advisor for the raising of new

debt finance to acquire commercial

properties

€9m

2014 Ireland

€18m

Debt refinancing and debt advisory

services to the LED Group

Debt refinancing and debt advisory

services to Oliver Plunkett GAA

Club

Commercial and Tax Advice on the

development of a Fibre Optic Cable

Business

€5 m

2010 Ireland

Business Modelling and Financial

Advisory Services for funding of

Biomass Gasification Facility

€10m

Ireland 2014 2014

€6m

Discounted debt purchase from

Ulster Bank and acquisition of

majority stake to the City Bin

company

Ireland

Settlement of debt facilities with

existing lender, incorporating a

refinance with new lender

€1.1m

Ireland 2013

10

© 2014 Deloitte & Touche. All rights reserved

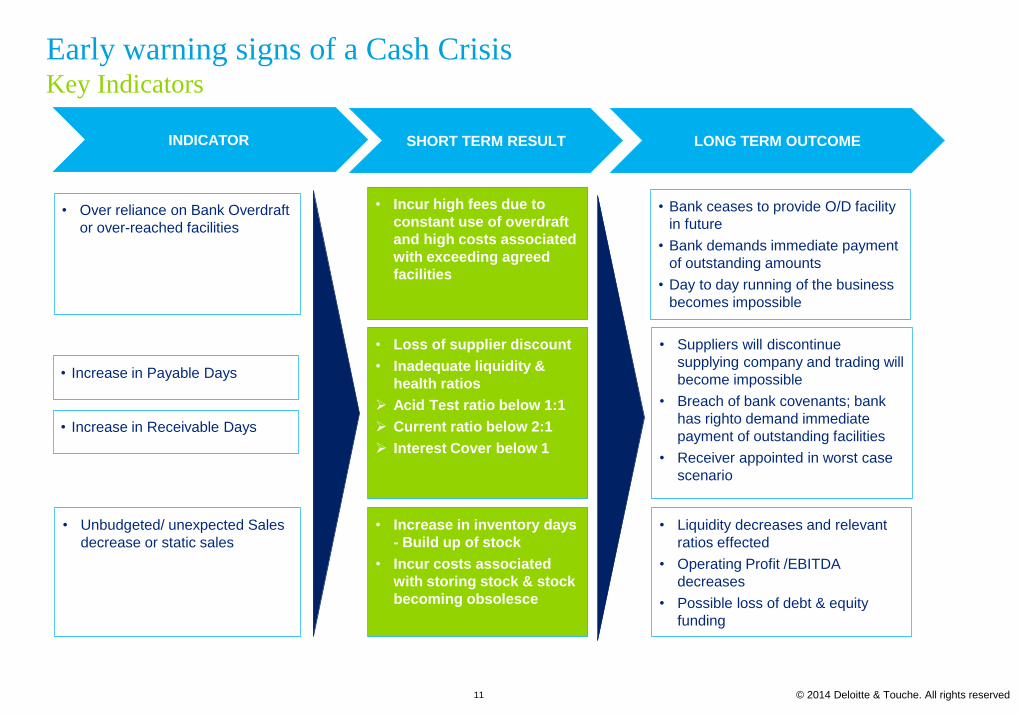

INDICATOR LONG TERM OUTCOME SHORT TERM RESULT

• Over reliance on Bank Overdraft

or over-reached facilities

• Unbudgeted/ unexpected Sales

decrease or static sales

• Loss of supplier discount

• Inadequate liquidity &

health ratios

Acid Test ratio below 1:1

Current ratio below 2:1

Interest Cover below 1

• Increase in inventory days

- Build up of stock

• Incur costs associated

with storing stock & stock

becoming obsolesce

• Bank ceases to provide O/D facility

in future

• Bank demands immediate payment

of outstanding amounts

• Day to day running of the business

becomes impossible

• Suppliers will discontinue

supplying company and trading will

become impossible

• Breach of bank covenants; bank

has righto demand immediate

payment of outstanding facilities

• Receiver appointed in worst case

scenario

• Liquidity decreases and relevant

ratios effected

• Operating Profit /EBITDA

decreases

• Possible loss of debt & equity

funding

• Incur high fees due to

constant use of overdraft

and high costs associated

with exceeding agreed

facilities

• Increase in Payable Days

• Increase in Receivable Days

11

Early warning signs of a Cash Crisis Key Indicators

© 2014 Deloitte & Touche. All rights reserved

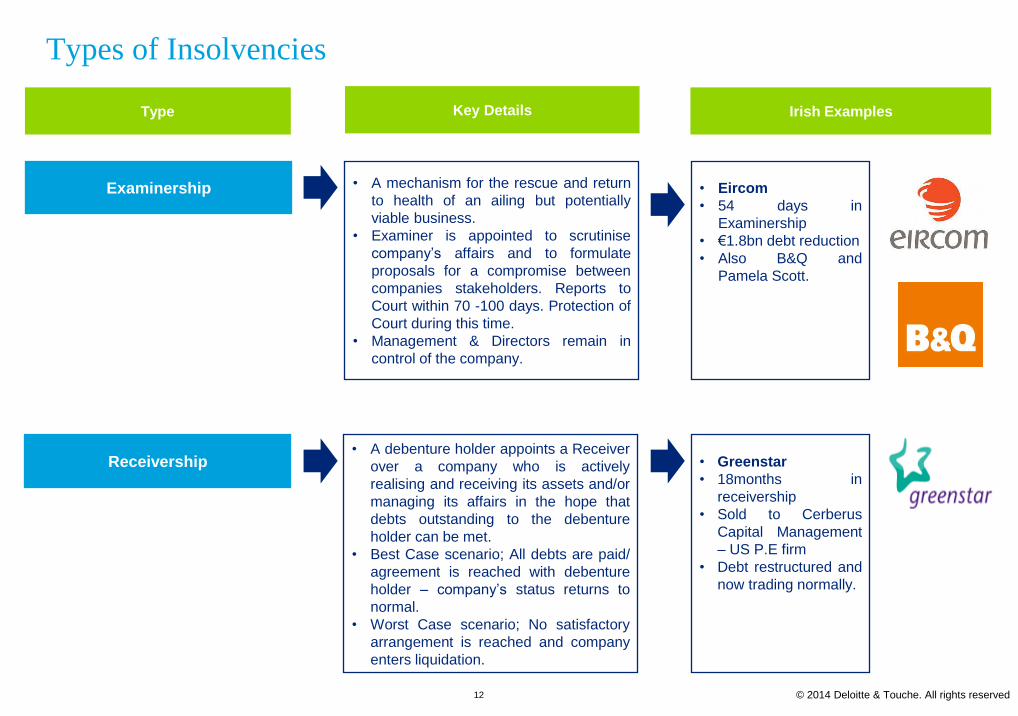

Type Key Details

• A debenture holder appoints a Receiver

over a company who is actively

realising and receiving its assets and/or

managing its affairs in the hope that

debts outstanding to the debenture

holder can be met.

• Best Case scenario; All debts are paid/

agreement is reached with debenture

holder – company’s status returns to

normal.

• Worst Case scenario; No satisfactory

arrangement is reached and company

enters liquidation.

Receivership

Irish Examples

• Greenstar

• 18months in

receivership

• Sold to Cerberus

Capital Management

– US P.E firm

• Debt restructured and

now trading normally.

• A mechanism for the rescue and return

to health of an ailing but potentially

viable business.

• Examiner is appointed to scrutinise

company’s affairs and to formulate

proposals for a compromise between

companies stakeholders. Reports to

Court within 70 -100 days. Protection of

Court during this time.

• Management & Directors remain in

control of the company.

Examinership

• Eircom

• 54 days in

Examinership

• €1.8bn debt reduction

• Also B&Q and

Pamela Scott.

12

Types of Insolvencies

© 2014 Deloitte & Touche. All rights reserved

Type Key Details

• Liquidator is appointed by the High

Court on foot of a petition to wind up

company made by a director, creditor,

shareholder or the company itself.

• Creditors can voluntarily decide to wind

up company if insolvent; Creditors

Voluntary Liquidation.

Liquidation

Irish Examples

• Setanta Insurance

Ireland

• Creditors Voluntary

Liquidation

• Ongoing.

• Same concept as full Receiverships

however prior to formal appointment of

the Receiver, a purchaser is identified

and terms of sale are agreed for assets

in question. Remaining assets in

business are left to unsecured creditors.

• Less costly and no diminution in asset

value as Goodwill remains intact.

Pre-pack Receivership

• Cleary’s SuperQuinn

• Company bought by

Musgrave Group plc

in 2011

• Remaining stores

became SuperValu in

2014.

13

Types of Insolvencies continued

Overview of Bank and Capital Markets in Ireland

© 2014 Deloitte & Touche. All rights reserved

Competing Banks

Divesting Banks

Portfolio Acquirers

Lending Funds and

Private Equity

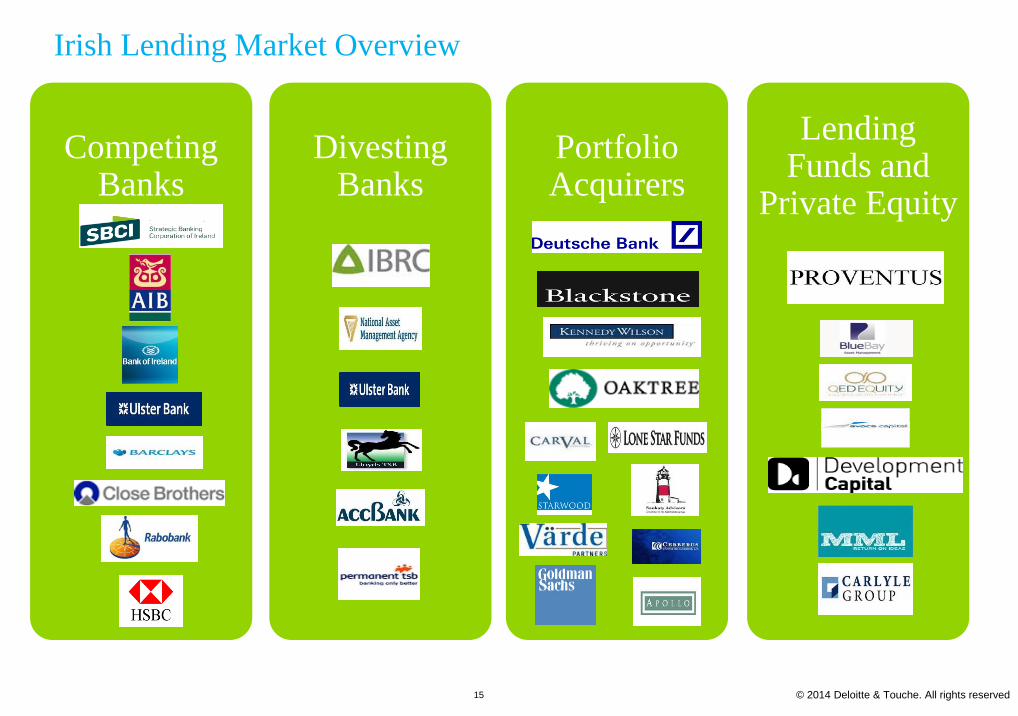

Irish Lending Market Overview

15

© 2014 Deloitte & Touche. All rights reserved

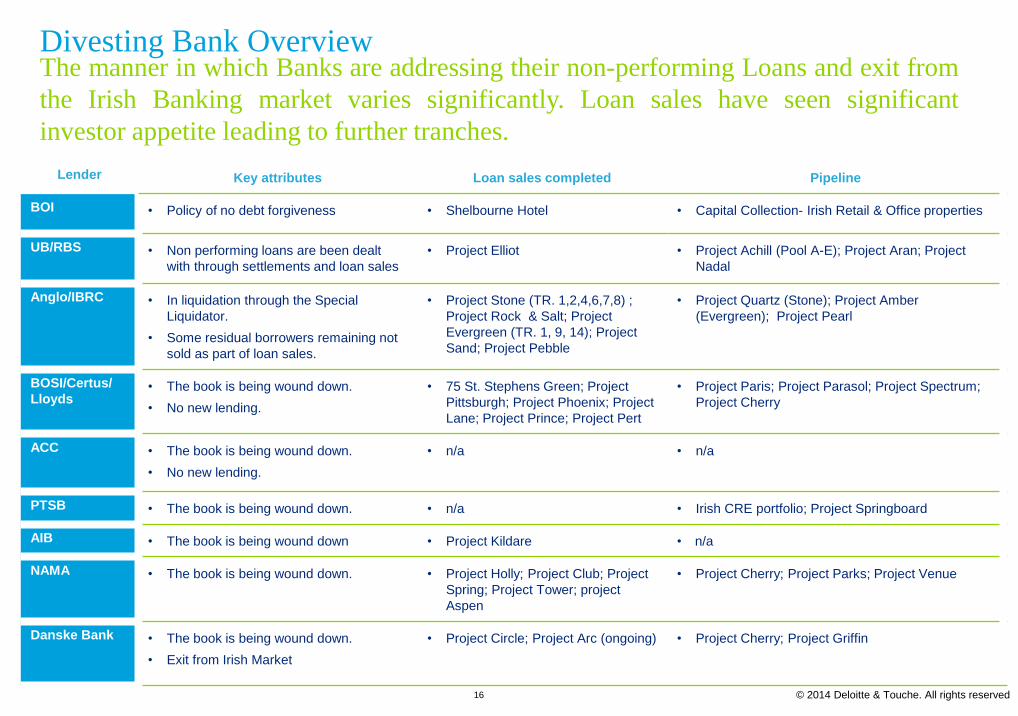

Lender Key attributes Loan sales completed Pipeline

BOI • Policy of no debt forgiveness • Shelbourne Hotel • Capital Collection- Irish Retail & Office properties

UB/RBS • Non performing loans are been dealt

with through settlements and loan sales

• Project Elliot • Project Achill (Pool A-E); Project Aran; Project

Nadal

Anglo/IBRC • In liquidation through the Special

Liquidator.

• Some residual borrowers remaining not

sold as part of loan sales.

• Project Stone (TR. 1,2,4,6,7,8) ;

Project Rock & Salt; Project

Evergreen (TR. 1, 9, 14); Project

Sand; Project Pebble

• Project Quartz (Stone); Project Amber

(Evergreen); Project Pearl

BOSI/Certus/

Lloyds • The book is being wound down.

• No new lending.

• 75 St. Stephens Green; Project

Pittsburgh; Project Phoenix; Project

Lane; Project Prince; Project Pert

• Project Paris; Project Parasol; Project Spectrum;

Project Cherry

ACC • The book is being wound down.

• No new lending.

• n/a • n/a

PTSB • The book is being wound down. • n/a • Irish CRE portfolio; Project Springboard

AIB • The book is being wound down • Project Kildare • n/a

NAMA • The book is being wound down.

• Project Holly; Project Club; Project

Spring; Project Tower; project

Aspen

• Project Cherry; Project Parks; Project Venue

Danske Bank • The book is being wound down.

• Exit from Irish Market

• Project Circle; Project Arc (ongoing) • Project Cherry; Project Griffin

The manner in which Banks are addressing their non-performing Loans and exit from

the Irish Banking market varies significantly. Loan sales have seen significant

investor appetite leading to further tranches.

Divesting Bank Overview

16

© 2014 Deloitte & Touche. All rights reserved

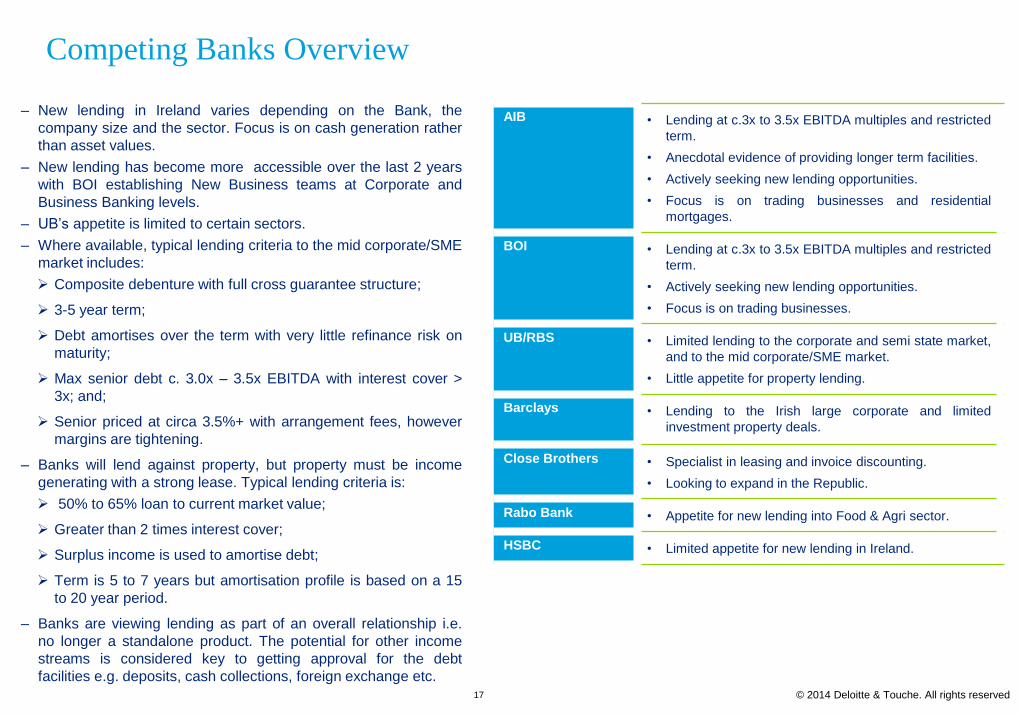

‒ New lending in Ireland varies depending on the Bank, the

company size and the sector. Focus is on cash generation rather

than asset values.

‒ New lending has become more accessible over the last 2 years

with BOI establishing New Business teams at Corporate and

Business Banking levels.

‒ UB’s appetite is limited to certain sectors.

‒ Where available, typical lending criteria to the mid corporate/SME

market includes:

Composite debenture with full cross guarantee structure;

3-5 year term;

Debt amortises over the term with very little refinance risk on

maturity;

Max senior debt c. 3.0x – 3.5x EBITDA with interest cover >

3x; and;

Senior priced at circa 3.5%+ with arrangement fees, however

margins are tightening.

‒ Banks will lend against property, but property must be income

generating with a strong lease. Typical lending criteria is:

50% to 65% loan to current market value;

Greater than 2 times interest cover;

Surplus income is used to amortise debt;

Term is 5 to 7 years but amortisation profile is based on a 15

to 20 year period.

‒ Banks are viewing lending as part of an overall relationship i.e.

no longer a standalone product. The potential for other income

streams is considered key to getting approval for the debt

facilities e.g. deposits, cash collections, foreign exchange etc.

AIB • Lending at c.3x to 3.5x EBITDA multiples and restricted

term.

• Anecdotal evidence of providing longer term facilities.

• Actively seeking new lending opportunities.

• Focus is on trading businesses and residential

mortgages.

BOI • Lending at c.3x to 3.5x EBITDA multiples and restricted

term.

• Actively seeking new lending opportunities.

• Focus is on trading businesses.

UB/RBS • Limited lending to the corporate and semi state market,

and to the mid corporate/SME market.

• Little appetite for property lending.

Barclays

• Lending to the Irish large corporate and limited

investment property deals.

Close Brothers • Specialist in leasing and invoice discounting.

• Looking to expand in the Republic.

Rabo Bank • Appetite for new lending into Food & Agri sector.

HSBC • Limited appetite for new lending in Ireland.

17

Competing Banks Overview

© 2014 Deloitte & Touche. All rights reserved

Borrower

• Stability and certainty

• Access to funding / credit lines

• Quick decision making process and

access to decision makers

• Funding package that reflects the

profile of the business

• Leaves management get on with

running the business i.e. no onerous

conditions

• Will work with management if the

business underperforms

No surprises! Provide relevant financial information Provide solutions

Lender

Key Considerations

• Stability and certainty

• Good quality information

• Full banking relationship to maximise

overall “share of wallet”

• Clear repayment strategy

• If the company is stressed – clear exit

strategy that demonstrates why

existing management are best placed

to maximise the Banks recovery

• Minimise losses and timeframe to exit

18

Relationship Banking Borrower and Lender have their own set of objectives however a strong working

relationship is based on finding the common ground

© 2014 Deloitte & Touche. All rights reserved Footer

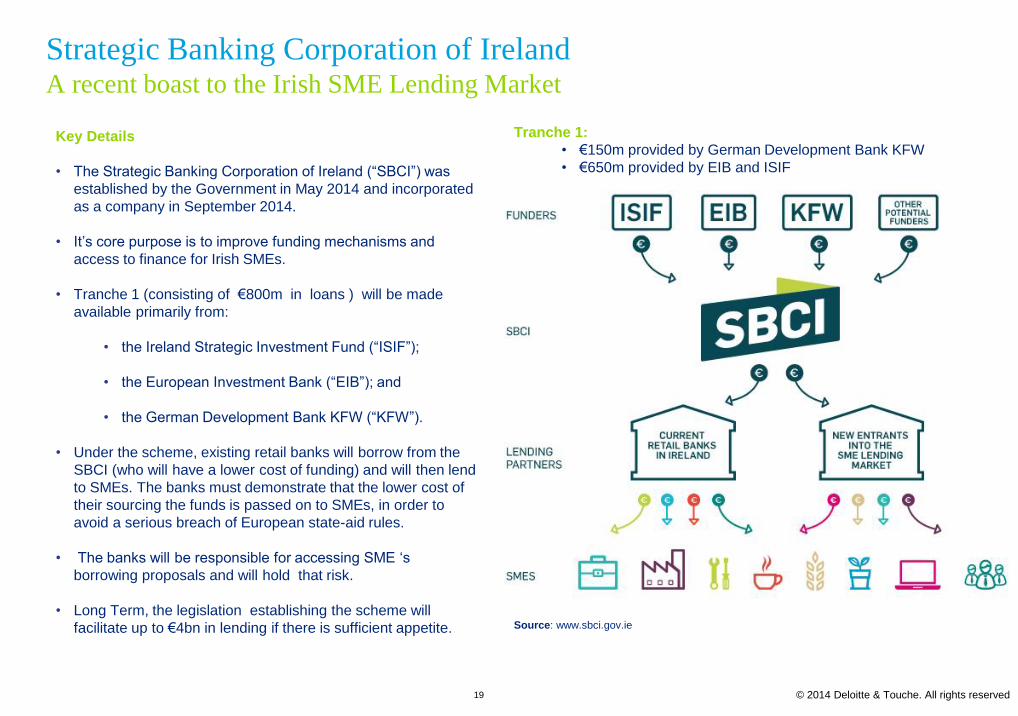

Key Details

• The Strategic Banking Corporation of Ireland (“SBCI”) was

established by the Government in May 2014 and incorporated

as a company in September 2014.

• It’s core purpose is to improve funding mechanisms and

access to finance for Irish SMEs.

• Tranche 1 (consisting of €800m in loans ) will be made

available primarily from:

• the Ireland Strategic Investment Fund (“ISIF”);

• the European Investment Bank (“EIB”); and

• the German Development Bank KFW (“KFW”).

• Under the scheme, existing retail banks will borrow from the

SBCI (who will have a lower cost of funding) and will then lend

to SMEs. The banks must demonstrate that the lower cost of

their sourcing the funds is passed on to SMEs, in order to

avoid a serious breach of European state-aid rules.

• The banks will be responsible for accessing SME ‘s

borrowing proposals and will hold that risk.

• Long Term, the legislation establishing the scheme will

facilitate up to €4bn in lending if there is sufficient appetite.

Tranche 1:

• €150m provided by German Development Bank KFW

• €650m provided by EIB and ISIF

Source: www.sbci.gov.ie

19

Strategic Banking Corporation of Ireland A recent boast to the Irish SME Lending Market

© 2014 Deloitte & Touche. All rights reserved Footer

Key Criteria to Qualify for an SME Loan

• SBCI loans will be available to full range of SMEs, from micro

one person enterprises to medium sized businesses. SMEs

defined using the Europeans Commission’s definition;

• Enterprises which employ fewer than 250 persons and

which have an annual turnover not exceeding €50m

and/or an annual balance sheet total not exceeding

€43m’.

• According to the new definition;

• An enterprise is ‘any entity engaged in an economic

activity, irrespective of its legal form’.

• Thus, the self-employed, family firms, partnerships and

associations regularly engaged in an economic activity

may be considered as enterprises. It is the economic

activity that is the determining factor, not the legal

form.

• No information at present on whether certain industries are

excluded. SCBI have listed the following beneficiary

industries; Hospitality, Professional services, Agriculture,

Manufacturing and recent start-ups.

Key Characteristics of the Loans:

• Offering; Long Term working capital and capital investment

finance

• “Reduced funding costs”

• Extended repayment holiday/ payment flexibility

• Longer repayment term/longer maturities

• A single SME can borrow up to €4million

Case Study Example 1 – Family owned restaurant

• Requires: Loan of €30,000 to rollout deliver service and

upgrade computer system.

• Traditional Bank: Payback must start immediately over 24

months.

• SBCI: Repayment holiday for 1 year then payback is

arranged over the following 2 years.

Case Study Example 2 – Letterkenny Legal Firm

• Requires: Loan of €15,000 to invest in new computer

system which has yearly maintenance costs.

• Traditional Bank: Full loan given now and payback must

start immediately over 18 months.

• SBCI: Loan is offered over 6 years to match life of

investment.

20

Strategic Banking Corporation of Ireland Key Criteria

© 2014 Deloitte & Touche. All rights reserved

Increasing number of domestic and foreign funds looking to fund Irish companies.

Funds will invest through equity, mezzanine debt and senior debt. Investment is

typically IRR driven however some funds are prepared to take a longer term view.

Selected Providers Offering Targets/Strategies

NPRF Funds:

Bluebay

Carlyle Cardinal Group

BDO Development Capital Fund

MML

Senior/Mezzanine/Uni-tranche.

Equity.

Equity/Bridging Underwrite.

Performing trading businesses.

Promote M&A and growth strategies.

Stressed and distressed businesses.

PE Firms:

Avoca / KKR

QED Equity

Proventus

Full capital stack.

Will look to fund performing and stressed

businesses. Preference for performing

businesses is to enter the capital stack at a

mezzanine and/or equity level. Preference

for stressed business is to acquire debt on

a loan to own basis.

Lending Funds and Private Equity

Selected Providers Offering Targets/Strategies

NPRF Funds:

Bluebay

Carlyle Cardinal Group

BDO Development Capital Fund

MML

Senior/Mezzanine/Uni-tranche.

Equity.

Equity/Bridging Underwrite.

Performing trading businesses.

Promote M&A and growth strategies.

Stressed and distressed businesses.

PE Firms:

Avoca / KKR

Broadhaven Capital Partners

Proventus

LDC

Starwood

Earlsfort Capital Partners

Full capital stack.

Will look to fund performing and stressed

businesses. Preference for performing

businesses is to enter the capital stack at a

mezzanine and/or equity level. Preference

for stressed business is to acquire debt on

a loan to own basis.

21

© 2014 Deloitte & Touche. All rights reserved

Raising Funds < €1million in Ireland Microfinance, HNWI, VC funds, Enterprise Ireland

Selected Providers Offering Targets/Strategies

Microfinance Ireland

• Offer loans between €2,000 and

€25,000 at 8.8% fixed APR

• ‘Enterprise’ – turnover below €2m and

fewer than 10 employees

• TaxAssist Accountants

• Castlemine Farm

• Lilliput Loaf Company

High Net Worth Individuals/

Angel Investors

• Angel Investors

• Funding and/or mentorship in return

for an equity stake in the business

• Currently €70m is invested by HNWIs

in Ireland

• The Business Angel Partnership have

invested €71m to date – average €180k

• Recent investments by HNWI

include;

• Yellow Schedule

• OnePageCRM

• CurrencyFair

• Investment by Victor Treacy

(HNWI) in Carlow Brewery Company

Venture Capital funds • Delta - €250m under management

• Kernel – €173m raised to date

• ACT - €350m invested to date

• Frontline ventures

• Enterprise Equity

• Hybird Energy

• Sport Authority

• Eventovate

• Game

• Boxfish

Enterprise Ireland • Range of funding options for SMEs

including grants to; grow your business;

engage in R&D; and develop your

Management Team

• Veronica’s snacks

• VistaMed

• Treemetrics

• ProFlame

22

© 2014 Deloitte & Touche. All rights reserved

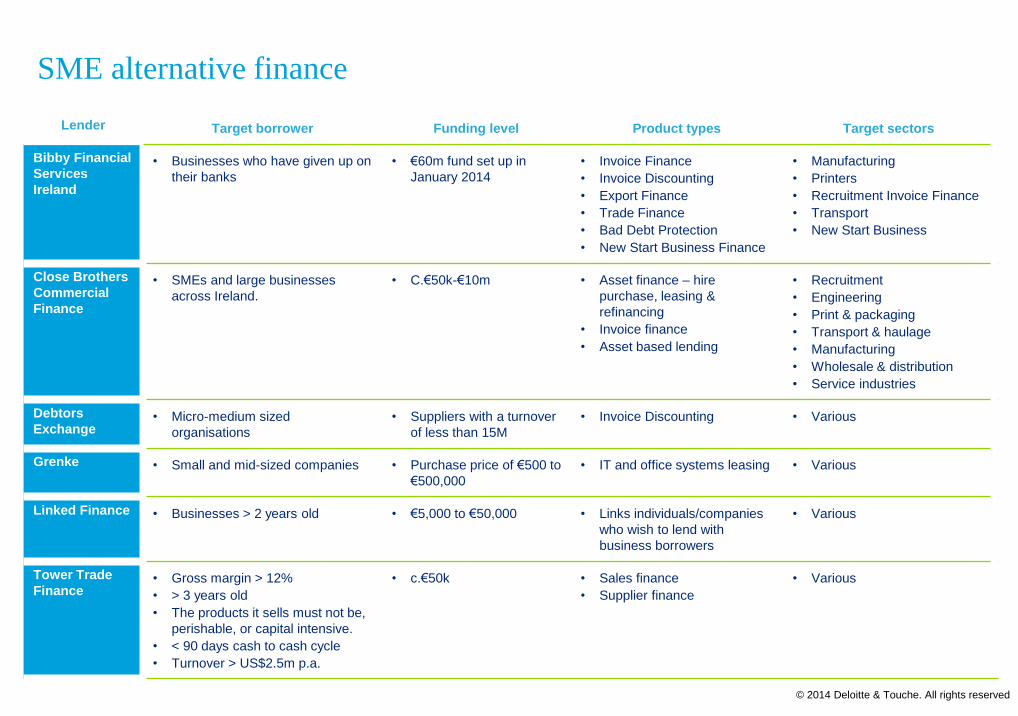

Lender Target borrower Funding level Product types Target sectors

Bibby Financial

Services

Ireland

• Businesses who have given up on

their banks

• €60m fund set up in

January 2014

• Invoice Finance

• Invoice Discounting

• Export Finance

• Trade Finance

• Bad Debt Protection

• New Start Business Finance

• Manufacturing

• Printers

• Recruitment Invoice Finance

• Transport

• New Start Business

Close Brothers

Commercial

Finance

• SMEs and large businesses

across Ireland.

• C.€50k-€10m • Asset finance – hire

purchase, leasing &

refinancing

• Invoice finance

• Asset based lending

• Recruitment

• Engineering

• Print & packaging

• Transport & haulage

• Manufacturing

• Wholesale & distribution

• Service industries

Debtors

Exchange • Micro-medium sized

organisations

• Suppliers with a turnover

of less than 15M

• Invoice Discounting • Various

Grenke • Small and mid-sized companies • Purchase price of €500 to

€500,000

• IT and office systems leasing • Various

Linked Finance • Businesses > 2 years old • €5,000 to €50,000 • Links individuals/companies

who wish to lend with

business borrowers

• Various

Tower Trade

Finance • Gross margin > 12%

• > 3 years old

• The products it sells must not be,

perishable, or capital intensive.

• < 90 days cash to cash cycle

• Turnover > US$2.5m p.a.

• c.€50k • Sales finance

• Supplier finance

• Various

SME alternative finance

Open Q&A

© 2014 Deloitte & Touche. All rights reserved

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a private company limited by guarantee, and its network of member firms, each of which is a legally separate and

independent entity. Please see www.deloitte.com/ie/about for a detailed description of the legal structure of Deloitte Touche Tohmatsu Limited and its member firms.

These materials and the information contained herein are provided by Deloitte & Touche and are intended to provide general information on a particular subject or subjects and are not

an exhaustive treatment of such subject(s). Accordingly, the information in these materials is not intended to constitute accounting, tax, legal, investment, consulting or other

professional advice or services. The information is not intended to be relied upon as the sole basis for any decision which may affect you or your business. Before making any decision

or taking any action that might affect your personal finances or business, you should consult a qualified professional adviser. These materials and the information contained therein are

provided as is, and Deloitte & Touche makes no express or implied representations or warranties regarding these materials or the information contained therein. Without limiting the

foregoing, Deloitte & Touche does not warrant that the materials or information contained therein will be error-free or will meet any particular criteria of performance or quality. Deloitte &

Touche expressly disclaims all implied warranties, including, without limitation, warranties of merchantability, title, fitness for a particular purpose, non-infringement, compatibility,

security and accuracy.

Your use of these materials and information contained therein is at your own risk, and you assume full responsibility and risk of loss resulting from the use thereof. Deloitte & Touche

will not be liable for any special, indirect, incidental, consequential or punitive damages or any other damages whatsoever, whether in an action of contract, statute, tort (including,

without limitation, negligence) or otherwise, relating to the use of these materials or the information contained therein. This document or extracts thereof should not be released to any

other party without the consent of Deloitte & Touche.

If any of the foregoing is not fully enforceable for any reason, the remainder shall nonetheless continue to apply.