delivering value - goldroad.com.au

TRANSCRIPT

PAGE | 1

NameTitle

DELIVERING VALUE

BELL POTTER UNEARTHEDFEBRUARY 2021

PAGE | 2

DISCLAIMER IMPORTANT NOTICES

Nature of this document: The purpose of this presentation is to provide general information about Gold Road Resources Limited (the ‘Company’). Unless otherwise stated herein, the information in this presentation is based on the Company’s own information and estimates. In attending this presentation or viewing this document you agree to be bound by the following terms and conditions. This document has been prepared by the Company. Information in this document should be read in conjunction with other announcements made by the Company to the Australian Securities Exchange and available at www.goldroad.com.au or www.asx.com.

Not an offer: This presentation is for information purposes only and does not constitute or form any part of any offer or invitation to sell or issue, or any solicitation of any offer topurchase or subscribe for, any securities in the Company in any jurisdiction. This presentation and its contents must not be distributed, transmitted or viewed by any person in anyjurisdiction where the distribution, transmission or viewing of this document would be unlawful under the securities or other laws of that or any other jurisdiction.

Not financial product advice: This presentation does not take into account the individual investment objectives, financial situation and particular needs of each of the Company’sShareholders. You may wish to seek independent financial and taxation advice before making any decision in respect of this presentation. Neither the Company nor any of its relatedbodies corporate is licensed to provide financial product advice in respect of the Company’s securities or any other financial products.

Forward-looking statements: Certain statements in the presentation are or may be “forward-looking statements” and represent the Company’s intentions, projections, expectations orbeliefs concerning, among other things, future operating and exploration results or the Company’s future performance. These forward looking statements speak, and the presentationgenerally speaks, only at the date hereof. The projections, estimates and beliefs contained in such forward looking statements necessarily involve known and unknown risks anduncertainties, and are necessarily based on assumptions, which may cause the Company’s actual performance, results and achievements in future periods to differ materially from anyexpress or implied estimates or projections. Accordingly, readers are cautioned not to place undue reliance on forward looking statements. Relevant factors which may affect theCompany’s actual performance, results and achievements include changes in commodity price, foreign exchange fluctuations and general economic conditions, increased costs anddemand for production inputs, the speculative nature of exploration and project development, diminishing quantities or grades of reserves, political and social risks, changes to laws andregulations, environmental conditions, and recruitment and retention of personnel.

Disclaimer: No representation or warranty, express or implied, is made by the Company that the material contained in this presentation will be achieved or prove to be correct. Except forstatutory liability which cannot be excluded, each of the Company, its directors, officers, employees, advisers and agents expressly disclaims any responsibility for the accuracy, fairness,sufficiency or completeness of the material contained in this presentation, or any opinions or beliefs contained in this document, and excludes all liability whatsoever (including innegligence) for any loss or damage which may be suffered by any person as a consequence of any information in this presentation or any error or omission there from. The Company isunder no obligation to update or keep current the information contained in this presentation or to correct any inaccuracy or omission which may become apparent, or to furnish anyperson with any further information. Any opinions expressed in the presentation are subject to change without notice.

Unverified information: This presentation may contain information (including information derived from publicly available sources) that has not been independently verified by the Company.

PAGE | 3

DELIVERING VALUE FOR SHAREHOLDERSGold Road a Low Risk Cash Generator with Upside

Low risk: Long life, high margin & consistent cash flow generation

Low risk: Debt free with a strong and growing balance sheet

Growth and returns opportunity through exploration upside and strong cash flow

Gruyere A Tier One Gold Producer

Long life, low cost production at Tier 1 gold mine1

>10 year mine life averaging ~300 kozpa*1

3.7 Moz Reserve, 6.6 Moz Resource*2

2020 production of 258,173 oz*, AISC of A$1,273/oz (US$990/oz)3

50:50 JV partner Gold Fields a proven global miner

Successful Explorer in Undercover and Underexplored Belts

Extensive (~4,500 km2) and prospective Yamarna exploration tenements (100%)

Yandina Project4 (~87%) an underexplored Greenstone belt in SW Yilgarn

* 100% basis, FX: 1AUD = US$0.781 Refer to ASX announcement dated 6 December 2019. Tier 1: Greater than 10 year mine life; greater than 300,000 ounces per annum; greater than 3.5 million ounce Ore Reserve and costs at the lower end of the cost curve2 Refer to ASX announcement dated 12 February 2020 – Gruyere JV only – excludes 0.3Moz of 100% Gold Road Resources.3 Refer to ASX announcement dated 22 January 2021. Production on 100% basis from 1 January 2020, AISC attributable to Gold Road4 Joint Venture with Cygnus Gold whereby Gold Road owns 90% interest in Yandina JV and 87% interest in Lake Grace JV. Refer ASX announcement 22 January 2021

PAGE | 4

OUR STRATEGY Deliver world class operating performance

Grow margins and mine life

DELIVER SHAREHOLDER

VALUE

GRUYERE

ESG

DISCOVERY CORPORATEDEVELOPMENT

ORGANISATIONAL CAPABILITY

Discover gold resources that transform the company

Build and maintain a project pipeline for growth

People and business systems to support the strategy

Capital management, strong liquid balance sheet, cash flow for growth and returns

Operate safely and care for our people, stakeholders & environment

Position Gold Road as an ESG market leader

Value accretive transformational M&A

Grow & Diversify production base

Quality, low risk assets

PAGE | 5

GRUYERE

ISO 45001 Safety Certification - Strong safety record – LTIFR of 2.8 Cyanide Code Compliant - obtained ISO 14001 Environmental Certification Low risk downstream tailings storage facility - water supply from saline aquifers Low emissions gas power generation – Renewable energy solar/ battery

initiatives on track to increase throughput up to 10 Mtpa Native Title Agreement - positive community impacts, creating employment and

business opportunities

YAMARNA

Yamarna Solar plant commissioned Dec 2020 Strong safety and environmental focus

FIRST SUSTAINABILITY REPORT FOR CY2020

Aligned to ASX corporate governance principles & utilising GRI standards Full calendar year of operational baseline data Incorporating operation and exploration performance

BUILDING AN ESG LEADER

PAGE | 6

GRUYERE GOLD MINEA TIER ONE GOLD PRODUCER

COARSE ORE STOCKPILE

ROM

GRINDING – 15MW SAG & BALL MILL

SETTLING POND

LEACH & CIL TANKSPOWERHOUSE

PAGE | 7

SAG &BALL MILLS

1100% basis unless otherwise stated.*Rehabilitation includes accretion and amortisation. #Gold Road operates to a calendar financial year. ** Gold produced is after GIC adjustment ***Cost per ounce reported against gold ounces produced during the quarter and either sold or held as dore/bullion during the quarter2Refer to ASX announcement 22 January. 2021 CAIC = Corporate all in costs 3 Attributable to Gold Road

GRUYERE – DECEMBER QUARTER SUMMARY

70,794 ounces produced1 at attributable AISC of

A$1,265/oz3

Above nameplate production, despite lower plant utilisation

Grade lifted to 1.12 g/t

Gold recovery of 91.8% - a slight increase Q on Q

Costs per ounce lower due to increased production

Gold Road sold 34,554 ounces at A$2,412/oz

~82% at spot

~18% hedged at average contract price of A$1,801/oz

2,653 ounces of bullion and dore held at 31 December3

Quarterly free cash flow of A$28.2M3

Quarterly CAIC of A$1,576/oz3

Operation (100% basis) Unit Dec 2020 Qtr Sep 2020 Qtr Jun 2020 Qtr Mar 2020 Qtr 2020#

Ore Mined kt 2,268 1,859 2,125 1,837 8,088Waste Mined kt 6,063 5,688 3,825 2,783 18,359Strip Ratio w:o 2.7 3.06 1.80 1.51 2.3Mined Grade g/t 1.18 1.03 1.06 1.06 1.09Ore milled kt 2,106 1,889 2,187 1,926 8,108Head Grade g/t 1.12 1.03 1.06 1.05 1.06Recovery % 91.8 91.5 93.1 94.1 92.6Gold Produced** oz 70,794 55,919 71,865 59,595 258,173Cost Summary (GOR)***Mining A$/oz 123 150 158 179 152Processing A$/oz 479 579 461 520 506G&A A$/oz 101 118 109 92 104Ore Stock & GICMovements

A$/oz 24 (33) 3 33 8

By-product Credits A$/oz (3) (4) (2) (2) (3)Cash Cost A$/oz 724 811 728 822 768Royalties, Refining, Other A$/oz 81 86 86 77 82Rehabilitation* A$/oz 20 19 16 19 18Sustaining Leases A$/oz 95 114 93 100 100Sustaining Capital & Exploration

A$/oz 346 458 309 117 304

All-in Sustaining Costs A$/oz 1,265 1,488 1,233 1,135 1,273

Sales (50% share) Unit Dec 2020 Qtr Sep 2020 Qtr Jun 2020 Qtr Mar 2020 Qtr 2020#

Gold Sold oz 34,554 31,480 28,700 31,700 126,434Average Sales Price A$/oz 2,412 2,420 2,498 2,001 2,330

INCREASED PRODUCTION & LOWER COSTS2

PAGE | 8

GRUYERE MINE2020 PRODUCTION1

2020 calendar year production of 258,173 ounces2

Meets 2020 Guidance 250,000-270,000 ounces (100% basis)

2020 attributable AISC A$1,273/oz*, CAIC A$1,592

Lower end of 2020 Guidance A$1,250-A$1,350/oz

Significant increase in ounces in December Quarter

Increased throughput and head grades, and processing recoveries

Plant throughput on fresh rock improved with SAG configuration changes

Mine to mill optimisation initiated. Pebble crusher improvements

Renewable energy to enable plant throughput up to 10 Mtpa

2021 Guidance expected March 2021 quarter*Gold Road attributable AISC . CAIC = Corporate all in costs1 Refer to ASX announcement dated 22 January 2021 2 100% basis

PAGE | 8

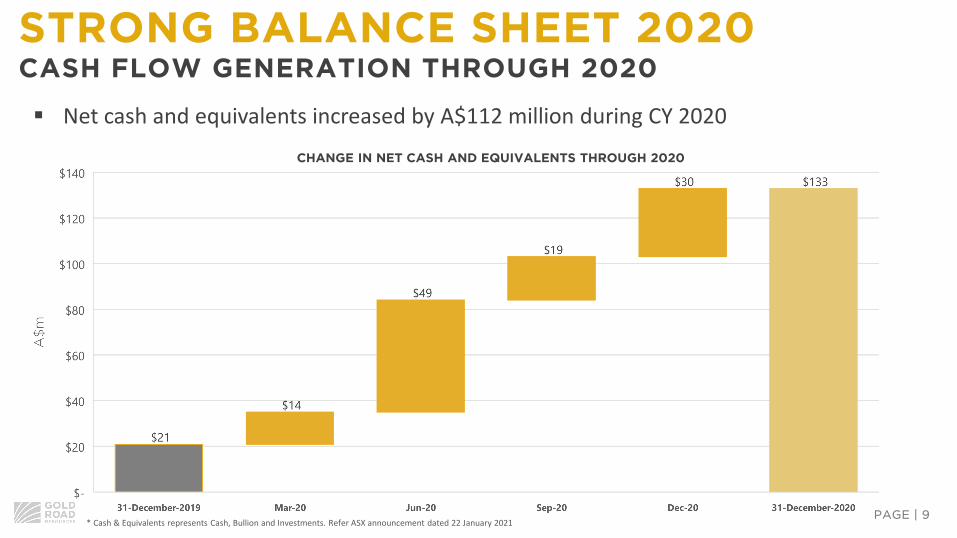

PAGE | 9

CHANGE IN NET CASH AND EQUIVALENTS THROUGH 2020

Net cash and equivalents increased by A$112 million during CY 2020

STRONG BALANCE SHEET 2020CASH FLOW GENERATION THROUGH 2020

* Cash & Equivalents represents Cash, Bullion and Investments. Refer ASX announcement dated 22 January 2021

PAGE | 10

CAPITAL MANAGEMENT

*Gold Road determines free cash flow as cash flow before debt and dividends. The Dividend Policy maintains the absolute discretion of the Board of Directors in relation to the declaration of any dividend. Refer to ASX announcement dated 16 September 2020 for further details1 As at 31 December 20192 Subject to the Board’s discretion. For clarity, the inaugural dividend will be calculated by reference to the free cash flow for that six month period

CAPITAL MANAGEMENT FOR GROWTH & RETURNS

Maintain a strong liquid balance sheet

Ensure capacity to fund new mine development

Or Invest in value accretive opportunities

DIVIDEND POLICY IN PLACE

Target an annual aggregate dividend payout of 15%-30% of free cash flow for each calendar year in two half yearly payments*

Subject to a minimum net cash balance of A$100M (after payment of any dividend)

A$65.7M in Franking Credits1

Anticipate inaugural dividend declared for 6 month period ended 31 December 20202

Dividend reinvestment plan to be established

PAGE | 11PAGE | 11

GRUYERE JVUNLOCKING GROWTH

1 100% Basis. Refer to ASX announcement dated 12 February 2020

Resource & Reserve Category (100% basis)

Tonnes (Mt)

Grade (g/t Au)

Moz Au

M&I Mineral Resource (M,I) 144 1.32 6.12

Total Mineral Resource (M,I,I) 154 1.34 6.62

Ore Reserve (P,P) 93 1.24 3.72 PAGE | 11

GRUYERE JV100% OWNED GOLD ROAD

Measured & Indicated Resource growth of 29% to 6.1 Moz1

M&I ounces increased by 1.2 Moz

M&I grade increased to 1.32 g/t Au

2020/21 focus on growing Gruyere JV 3.7 Moz Reserve

Convert M&I Resource into Reserve

Grow Reserve through optimised economics – 2020/21

Golden Highway

Resources - 0.7 Moz maintained

Reserves - 0.3 Moz maintained

PAGE | 12PAGE | 12

GRUYERE MINE OPTIMISATION GROWING A HIGH MARGIN OPERATION

Note: Refer to ASX announcement dated 9 September 2019, 12 February 2020 and 24 July 2020

Gruyere Joint Venture is focused on optimising: Mining Plant

Extended Indicated Resource below mine design. Geotechnical and metallurgical studies for potential pit deepening in progress

Process plant (SAG mill) configured for fresh ore. Capability to be determined over next ~6 months. SAG mill confirmed as main throughput constraint

Powerhouse upgrade. Additional gas power generation augmented by solar and battery (studies underway)

PAGE | 13PAGE | 13

MEANINGFUL DISCOVERYDiscover gold resources that transform the company

Build and maintain a project pipeline for growth

PAGE | 14

Targeting 100% owned operation to add 150 kozpa

Exploring for >1 Moz discoveries on 100% ground

Strategy aligned to a discovery that ‘moves the dial’

Focus on high priority targets in Southern Project Area

Yamarna offers a unique opportunity, combining

An under-explored ‘frontier’ greenstone belt

Favourable global mining jurisdiction of Western Australia

Development optionality with Gruyere

Stage gate approach to exploration investment

Note: Refer to ASX announcement dated 12 February & 10 September 2020

EXPLORATIONSTRATEGY OF MEANINGFUL DISCOVERY

Gruyere

PAGE | 15

EXPLORATION DEC QUARTER FOCUSED ON SOUTHERN PROJECT (800km2)

Note: Refer to ASX announcement dated 22 January 2021

Gilmour South

Kingston

Beefwood

Gilmour

SavoieSmokebush

Hirono

Gilmour: More high-grade gold at Gilmour including:

4.9 metres at 5.16 g/t Au from 353 metres

3.75 metres at 3.66 g/t Au from 535 metres

Access permits granted Gilmour South Q4 2020

Smokebush: High grade results including:

15 metres at 6.37g/t Au from 144 metres

25 metres at 2.02 g/t Au from 172 metres

Kingston: Follow-up RC & diamond drilling including:

5 metres at 2.89 g/t Au from 72 metres

Beefwood: Large regolith anomalies identified

PAGE | 15

PAGE | 16

Resource of 2.6 Mt at 3.09 g/t Au for 258,400 oz (100% Gold Road)

Open pit: 129,100 oz at 2.21 g/t Au

Underground: 129,300 oz at 5.13 g/t Au

Indicated: 120,000 oz at 5.2 g/t Au (46%)

Initial metallurgical test-work

89-90% overall recovery

28-82% gravity recovery

Development Alternatives

Potentially part of future standalone operation

Alternative is to toll treat – 55 km from Gruyere

SOUTHERN PROJECT AREAGILMOUR RESOURCE – 258,000oz

Note: Refer to ASX announcement dated 4 December 2019

PAGE | 17

SOUTHERN PROJECT AREAGILMOUR RESOURCE

Note: Refer to ASX announcement dated 22 January 2021

PAGE | 18

SOUTHERN PROJECT AREASMOKEBUSH PROSPECT

Note: Refer to ASX announcement dated 22 January 2021

PAGE | 19PAGE | 19

SAVE THE DATE

Tuesday 16 Feb – 7am AWST / 10am AESTStrategy Investor Presentation Call & Webcast

PAGE | 20

DELIVERING SHAREHOLDER VALUE

INVESTOR RELATIONS ENQUIRES Duncan Hughes: Manager – Corporate Development & Investor RelationsTel: +61 8 9200 1600 | [email protected]

STRENGTHStrong business and balance sheet

MARGINConsistent low-cost production for >10 years

GROWTHGruyere Operational ExcellenceDiscoveryCorporate Development

SHAREHOLDER RETURNS*Dividend Policy in placeTSR (from Gruyere discovery): ~1,040%* Total shareholder returns from 11 October 2013 to 21 January 2021: 11c – 125c