deindustrialisation and the relocation of...

TRANSCRIPT

Deindustrialisation Deindustrialisation and the relocation of industriesand the relocation of industries

HervéHervé BoulholBoulhol * * # # -- Lionel Fontagné Lionel Fontagné ** ** ##

* IXIS* IXIS--CIB CIB -- ** CEPII ** CEPII -- ## UniversitéUniversité de Paris 1de Paris 1

IntroductionIntroduction

Growing concern in EuropeUnfair competition (social - environmental - tax dumping)Inter-industry trade and adjustment costsDecline of manuf share in employment reinforced by globalisationOffshore outsourcing filling the newspapersWill Member states such as Germany or France still have factories in a decade ?

Introduction

The civil societyThe civil society

The answer is NO70% of the French consider outsourcing as a « serious issue »30% fear losing their jobGermany and France are the 2 countries where citizens do consider that globalisation has gone too far (Eurobarometer)

Introduction

Economists are less alarmingEconomists are less alarming

Costs, but also other determinants of locationSpecialisation and trade = gainsDifference between local and macro impactsUnemployment firstly due to domestic policies (UK/Germ.)Deindustrialisation mainly a domestic issueOutsourcing accounts for a negligible share of the turnover (Marin, 2004)

Introduction

Economists facing the civil societyEconomists facing the civil society

Should we care ? Politicians do care !Conjunction of– economic slowdown amplified in industry – structural lack of job creation in continental Europe– dismissals translating into long term unemployment

Recurrent concern: early 90s’ Giant sucking sound in the US, Arthuis report in FranceEconomist become ‘nervous’ : – Unconvincing argument: Mankiw (2004)– Samuelson versus Bhagwati et al. (2004)

Introduction

The right analytical frameworkThe right analytical framework

Deindustrialisation is a “natural” outcomeImprecise boundariesCombination of supply and demand determinantsBut reinforced by international competitiona.w.a. the dramatic changes of the international economyRelative price changes, productivity gains: not exogenousPrice competition, defensive innovation (Thoenig & Verdier 2002)Our question: What’s the responsibility of the South in the observed deindustrialisation? (Rowthorn & Ramaswami, 1998)Broad view in line with the concerns of the public society We will stick on industry: but services are concerned by relocationtoo (Amiti&Wei, 2004; van Welsum, 2004; GAO, 2004)

Introduction

Deindustrialisation and outsourcing in the public debateTaking stock of the recent evolutionsModel and dataEconometric results Policy implications

Profound changes of the ILOProfound changes of the ILONew competitors benefiting from a wide spectrum of comparative advantages – industry : China– services : India

Specialisation: comparative advantage is moving from industry to services (Nike syndrome)Breakdown of the VA chainGlobal factory era (Cayenne effect)Depressing impact on pricesSelection of firms - products - technologiesDevelopment of positions associated with development, innovation and organisation ...… at the expense of blue collars and bottom white collars

The public debate

A key issue for policy makersA key issue for policy makers

Rapid reduction of transaction costsAccession of large economies offering low-cost locations to the world market Labour force potentially mobilised with technologies of the North 1990 (2000): Japanese industry– 15 millions employees in Japan (- 2 millions)– 1.2 millions abroad (+ 1.6 millions)

Firms adopting such scheme are more efficient and exhibit a larger probability of survivalBut transition costs associated with inter-industry trade are largeSouth = main contribution to world trade change since 2000

The public debate

Intra-EU trade

25

27

29

31

33

35

37

39

41

43

45

1993 1994 1995 1996 1997 1998 1999 2000 2001 2002

OWT

TWTH

TWTV

IntraIntra--industry trade: intraindustry trade: intra--EUEU

Source: BACI-CEPII The public debate

IntraIntra--industry trade: EU // Chinaindustry trade: EU // China

The public debate

China

0

10

20

30

40

50

60

70

80

90

100

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

OWT

TWTH

TWTV

Deindustrialisation and outsourcing in the public debateTaking stock of the recent evolutionsModel and dataEconometric results Policy implications

DefinitionsDefinitionsDeindustrialisation: declining share of industry in employmentOutsourcing– Narrow: closing down + relocation + import– Matrix-based:

Problem: need to rely on firm level data in order to trace directimports of intermediate/final products (Cayenne, screw, gearbox,…). Alternatively I-O tables.Imports from countries hosting outsourced activities: our approach

Country

In Out

In Make OffshoreFirm

Out Buy Outsource

Descript. Stat.

Industry share in total employmentIndustry share in total employmentbel

0,15

0,2

0,25

0,3

0,35

0,4

0,45

0,5

65 68 71 74 77 80 83 86 89 92 95 98 010,15

0,20

0,25

0,30

0,35

0,40

0,45

0,50

empmanufsh empindussh empwithconstsh

Source :

gbr

0,15

0,2

0,25

0,3

0,35

0,4

0,45

65 68 71 74 77 80 83 86 89 92 95 98 01

empmanufsh empindussh empwithconstsh

Source :

Descript. Stat.

Industry share in total employmentIndustry share in total employmentusa

0,1

0,15

0,2

0,25

0,3

0,35

65 68 71 74 77 80 83 86 89 92 95 98 010,10

0,15

0,20

0,25

0,30

0,35

empmanufsh empindussh empwithconstsh

Source :

kor

0,1

0,15

0,2

0,25

0,3

0,35

0,4

70 72 74 76 78 80 82 84 86 88 90 92 94 96 98 00 02

empmanufsh empindussh empwithconstsh

Source :

Descript. Stat.

ManufManuf share in total employment, VA & share in total employment, VA & volume of the VAvolume of the VA

Descript. Stat.

United States

12%

14%

16%

18%

20%

22%

24%

26%

70 72 74 76 78 80 82 84 86 88 90 92 94 96 98 00 0212%

14%

16%

18%

20%

22%

24%

26%

Spain

16%

18%

20%

22%

24%

26%

28%

30%

32%

70 72 74 76 78 80 82 84 86 88 90 92 94 96 98 00 021

1

2

2

2

2

2

3

3

Relative employment, production, prices & Relative employment, production, prices & imports from emerging economies imports from emerging economies (France)(France)

Relative price

Relative employt

Relative production

1987 20021970-0.400

-0.300

-0.200

-0.100

0.000

0.100

0.200

0.300

0.400

1970 20021987

Relative employmt

Importsfrom

emerging

Relative price

-0.400

-0.300

-0.200

-0.100

0.000

0.100

0.200

0.300

0.400

0.000

0.005

0.010

0.015

0.020

0.025

0.030

Descript. Stat.

Deindustrialisation and outsourcing in the public debateTaking stock of the recent evolutionsModel and dataEconometric results Policy implications

A simple model with 2 sectorsA simple model with 2 sectors

Industry and services, TFP growing at gI>gS

Take into account capital, extend prod° f° to the case of constant elasticity of substitution. Define a constant positive if the industrial sector is relatively intensive in capital. CES demand.

jjj LAY .=tgg

SISSIISIeAAALYLYRELPROD ).(

0 ./)//()/( −==≡

SI ppRELPRICE /≡

)/()./11.()()( rwLogaRELPRODLogcteRELPRICELog σ−+−=

tggcteLLLog SISI ).).(1()/( −−−= η

Model & data

A simple model with 2 sectors A simple model with 2 sectors (cont.)(cont.)

Introduce Engel’s law, extended to manuf. goods: at constant relative price, the relative demand of industrial goods follow ahump shape based on the level of development.YCAP to be introduced (non linearly).

At constant prices, the relative value-added of industry in volume terms increases until a certain level of per capita income (the “turning point”), before diminishing subsequently. Expected combined effects of decreasing relative price and economic development for value-added in volume and value terms.

Model & data

)(.)(.)/().1()/( 2 YCAPLogbYCAPLogappLogcteXpXpLog SISSII ++−+= η

Figure 5: Price and wealth effectson relative output (volume)

Time

Price effect Wealth effect

Figure 6: Price and wealth effectson relative value output and

employment

Time

Wealth effect Price effect

Model & data

Volume terms: (1) share of industry increases via combination of price effect (substitution) and income effect. (2) both effects oppose one another, outcome indeterminate.

Value terms, employment: (1) demand effect counteracts loss of industrial employment linked to productivity gains. (2) the two effects operate in same direction and deindustrialisation accelerates.

Econometric specification

RELOUTPUT = h (YCAP, YCAP2, RELPRICE, TRADE, FIXCAP)

EMPSHARE = f (YCAP, YCAP², TRADE, FIXCAP, TOUTSOURC)

Percentage change in the share of manuf. in employment

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

aut

bel

can

dnk

esp fin fra gbr

ita jpn

kor

nld

nor

prt

swe

usa

aver

age

Model & data

RemarksRemarks

1-Variable of total outsourcingCountry

In Out

In Make OffshoreFirm

Out Buy OutsourceTOTOUTSOURC

2-Autocorrelation TRADE

Model & data

Residual analysis reveals strong first-order autocorrelation, estimates based on an AR(1) process, allowing for country-heterogeneity in the auto-correlation coefficient (ARH1).

Deindustrialisation and outsourcing in the public debateTaking stock of the recent evolutionsModel and dataEconometric resultsPolicy implications

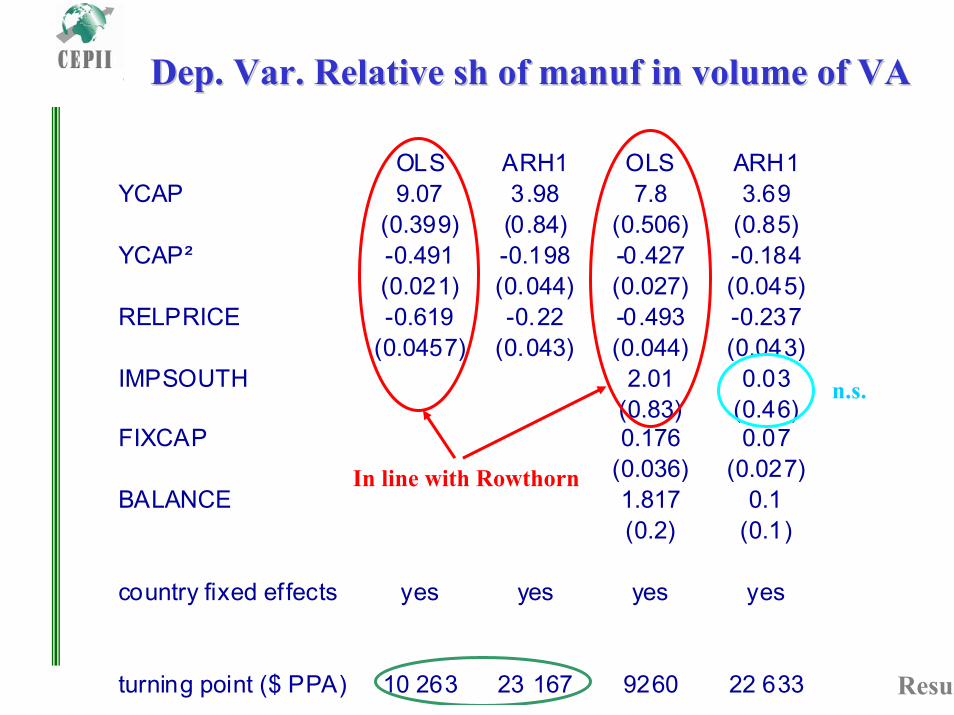

Dep. Var. Relative Dep. Var. Relative shsh of of manufmanuf in volume of VAin volume of VA

OLS ARH1 OLS ARH1YCAP 9.07 3.98 7.8 3.69

(0.399) (0.84) (0.506) (0.85)YCAP² -0.491 -0.198 -0.427 -0.184

(0.021) (0.044) (0.027) (0.045)RELPRICE -0.619 -0.22 -0.493 -0.237

(0.0457) (0.043) (0.044) (0.043)IMPSOUTH 2.01 0.03

(0.83) (0.46)FIXCAP 0.176 0.07

(0.036) (0.027)BALANCE 1.817 0.1

(0.2) (0.1)

country fixed effects yes yes yes yes

turning point ($ PPA) 10 263 23 167 9260 22 633

In line with Rowthorn

n.s.

Results

Dep. Var. Relative Dep. Var. Relative shsh of of manufmanuf in in employmentemploymentOLS OLS ARH1 AR H1 AR H1

(1) (2) (3) (4) (5)

YCAP 7.015 4.52 6.23 3.98 3.59(0.387) (0.42) (0.56) (0.49) (0.61)

YCAP² -0.387 -0.229 -0.33 -0.188 -0.196(0.021) (0.024) (0.03) (0.026) (0.032)

IMPSOUTH -3.67 -1.846 -0.78 -0.113 0.4(0.64) (0.60) (0.33) (0.27) (0.58)

EXPSOUTH 1.56 0.316 0.22(0.29) (0.17) (0.22)

NORTH BALANC E 0.42 0.06 0.02(0.17) (0.07) (0.07)

TOTAL BALANCE 0.983 0.176(0.129) (0.055)

FIXCAP 0.142 0.059 0.159 0.073 0.141(0.026) (0.024) (0.018) (0.016) (0.018)

TOT OUTSOURCING -0.664 -0.28 -0.993(0.284) (0.24) (0.283)

IMPSOUTH*time87 -1.35(0.60)

EXPSOUTH*time87 0.294(0.2)

Time trend -0.022(0.001)

time fixed effects no yes no no no

country fixed ef fects yes yes yes yes yes

turning point 8 633 19 322 12 574 39 542 9 492

Contributions

1 point GDP increase in net imports from South => - 2.8 % relative employtinstead of 1%

Large exogenous trend: - 2.2 % p.a. relative employt

Results

Contributions Contributions (taken from column 2)(taken from column 2)

Results

Country Relativeemployment

change

Investment Income percap

Manufbalance

Importsfrom

emerging

Exports toemerging

trend residuals Contrib°trade

emergingFinland -3.5 -0.7 1.5 1.8 -1.7 0.7 -9.7 4.6 28.6

Italy -3.8 -0.3 1.5 0.2 -1.5 0.5 -11.6 7.4 26.3Austria -5.9 0.1 1.0 0.1 -2.0 0.5 -8.7 3.0 25.9Netherl. -13.8 -0.3 0.6 0.4 -3.3 0.2 -9.6 -2.2 23.1Japan -7.2 -0.2 1.3 0.3 -2.0 0.5 -10.5 3.3 21.1

Canada -7.7 0.3 -0.1 0.4 -1.5 0.0 -8.1 1.2 19.7Portugal -4.2 0.0 4.2 0.0 -0.8 0.0 -10.1 2.4 19.5

USA -12.3 0.3 -1.1 -0.2 -1.9 0.1 -8.4 -1.6 15.3Belgium -16.5 0.0 0.9 1.2 -3.2 0.9 -11.1 -5.8 14.5Spain -7.8 0.0 3.1 -0.2 -1.3 0.2 -9.7 0.0 14.3

Denmark -9.8 0.1 0.2 1.1 -1.6 0.3 -9.4 -0.7 13.5Norway -10.9 -0.5 0.7 -0.7 -1.1 0.0 -8.7 -0.9 10.4France -10.5 0.0 0.4 0.0 -1.2 0.2 -9.3 -0.8 9.7

United-K -19.2 0.3 0.8 -0.6 -1.5 0.0 -10.3 -9.0 8.3Sweden -9.9 -0.1 0.0 0.8 -0.9 0.3 -9.9 -0.2 6.1Korea 6.2 0.5 13.8 0.5 -1.5 0.8 -7.4 -0.4 -11.5

average -8.6 0.0 1.8 0.3 -1.7 0.3 -9.5 0.0 15.3

Deindustrialisation and outsourcing in the public debateTaking stock of the recent evolutionsModel and dataEconometric results Policy implications

What points to optimism: – Depending on the econometric methodology, the contribution of net

trade with “countries of offshoring” to deindustrialisation is varying. – However, upper bound remains limited (15% on average), despite

acceleration of the phenomenon. Accordingly, 15% is an upper bound on average and 25% for individual countries.

– Not all trade flows with countries hosting offshored activities are associated with offshoring: some “autonomous” trade flows take place just because emerging economies are specialising and trading with us.

– Auto-correlation of series conducing to (upward) biased estimates. After correction, impact culminating at 6% of deindustrialisation (for the Netherlands).

– All in all, deindustrialisation hardly driven by outsourcing.

Policy implications

What points to pessimism:– The pb is not jobs outsourced but jobs not created– The pb with Euroland: low growth, limited opportunities.– Factories are following the clients … in the CEECS, or in China– But now, the most promising markets are also low-cost locations

Hence new challenges to be faced by the European industry– Cost differentials do matter: structural reforms to be completed– But: no hope to be placed in competing on wages or taxes– Better keep the traditional (low elasticity) market positioning:

techno, quality, innovation– knowledge eco

Policy implications