deglobalization? - europa

TRANSCRIPT

Deglobalization?Comments on paper by Pol Antràs

November 11, 2020

Susan Lund, McKinsey Global Institute

ECB Forum on Central Banking 2020

McKinsey & Company 2

Antràs paper makes many valuable contributions

Historical context for the slowdown in trade / GDP growth in

last 10 years: a natural sequel to a period of unsustainable

“hypergloblization” from 1986-2008

Convincingly shows that factors that gave rise to

“hyperglobalization” have now run out of steam:

(technological change, reduced trade costs, entry of many

new countries into global trading system)

Provides a nice theoretical model that can explain the rapid

acceleration of value chain globalization, based on scale

economies, fixed (and sunk) investment costs, and

sequential production models

Conclusion:

• Little evidence of

systemic de-

globalization so far

• Political and

institutional factors are

the main risks to trade

in the future

• Value chain stickiness

may prevent large-

scale shifts in their

geographical footprint

McKinsey & Company 3

My comments will focus on two areas

01 Micro-empirical look at past slowdown in

global trade

02 Firm-level view on how global value chain risk

could lead to a rebalancing of trade

McKinsey & Company 4

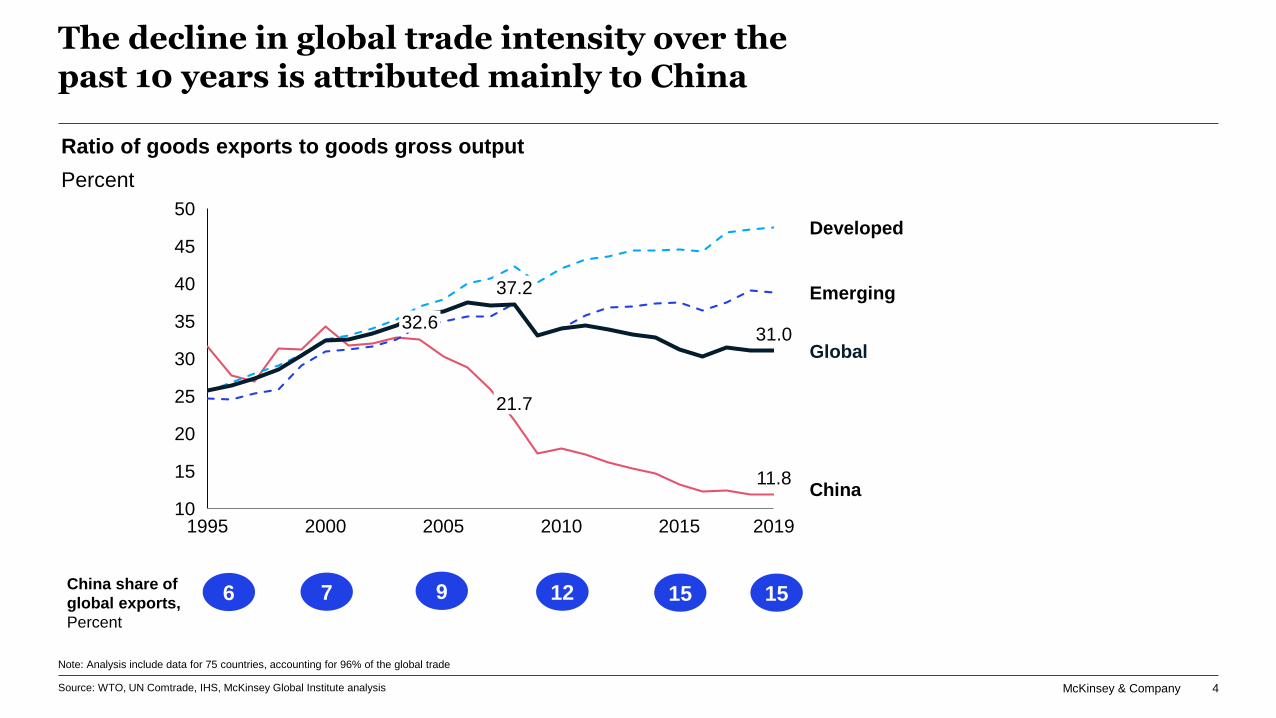

The decline in global trade intensity over the past 10 years is attributed mainly to China

45

30

10

40

15

20

25

35

50

20151995 2000

11.8

32.6

2005

21.7

37.237.2

2010

31.0

2019

China

Developed

Emerging

Global

Ratio of goods exports to goods gross output

Percent

Source: WTO, UN Comtrade, IHS, McKinsey Global Institute analysis

Note: Analysis include data for 75 countries, accounting for 96% of the global trade

China share of

global exports,

Percent

6 7 9 12 15 15

McKinsey & Company 5

China is consuming more of what it produces and

exporting less......and China’s domestic supply chains are also

growing

22

64

Computer &

electronics

Textile &

Apparel

Machinery &

equipment

61

Automotive

97

27

914

4

2007 2018

China’s exports as a share of gross output,

2007 vs. 2018Share of imported intermediate inputs to total inputs,

2007 vs. 2017

Source: UN Comtrade, IHS, WIOD, McKinsey Global Institute analysis

10

47

Textile &

Apparel

3

19

Computer &

electronics

Machinery &

equipment

Automotive

57

52

2007 2017

China

exports

CAGR

(2007-18)

0.6% 2.5% 1.9% 2.4%

China’s decline in trade intensity reflects two factors

McKinsey & Company 6

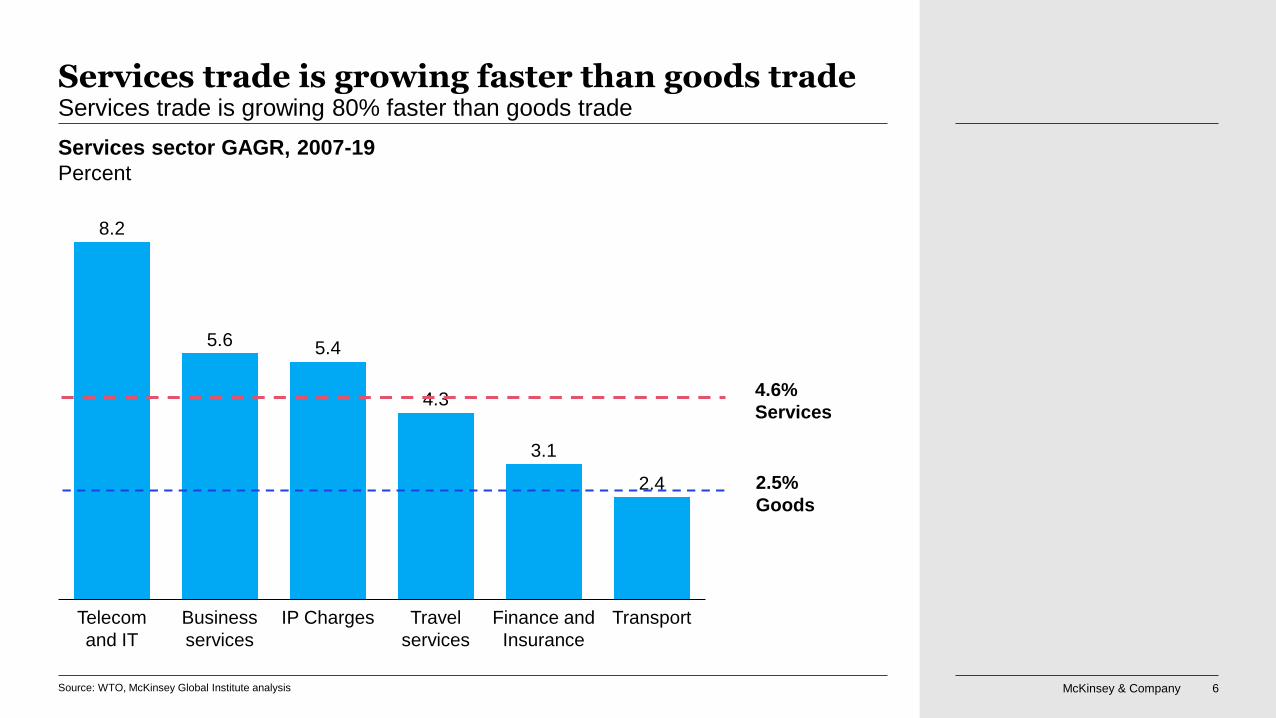

Services trade is growing faster than goods tradeServices trade is growing 80% faster than goods trade

Services sector GAGR, 2007-19

Percent

Telecom

and IT

4.3

8.2

TransportFinance and

Insurance

Travel

services

IP ChargesBusiness

services

2.4

3.1

5.45.6

4.6%

Services

2.5%

Goods

Source: WTO, McKinsey Global Institute analysis

McKinsey & Company 7

Implications of the “China story” of trade slowdown

Decline in trade / GDP is a sign of success, not failure, of

globalization – it reflects China’s economic development

We might expect the slower growth of trade / GDP will

continue as India and other low-income countries develop

domestic consumers and supplier industries

Conclusion: no evidence of systemic de-globalization, just a

different type of globalization

Services trade is growing faster than goods trade

McKinsey & Company 8

My comments will focus on two areas

01 Micro-empirical look at past slowdown in global

trade

02 Firm-level view on how global value chain

risk could lead to a rebalancing of trade

McKinsey & Company 9

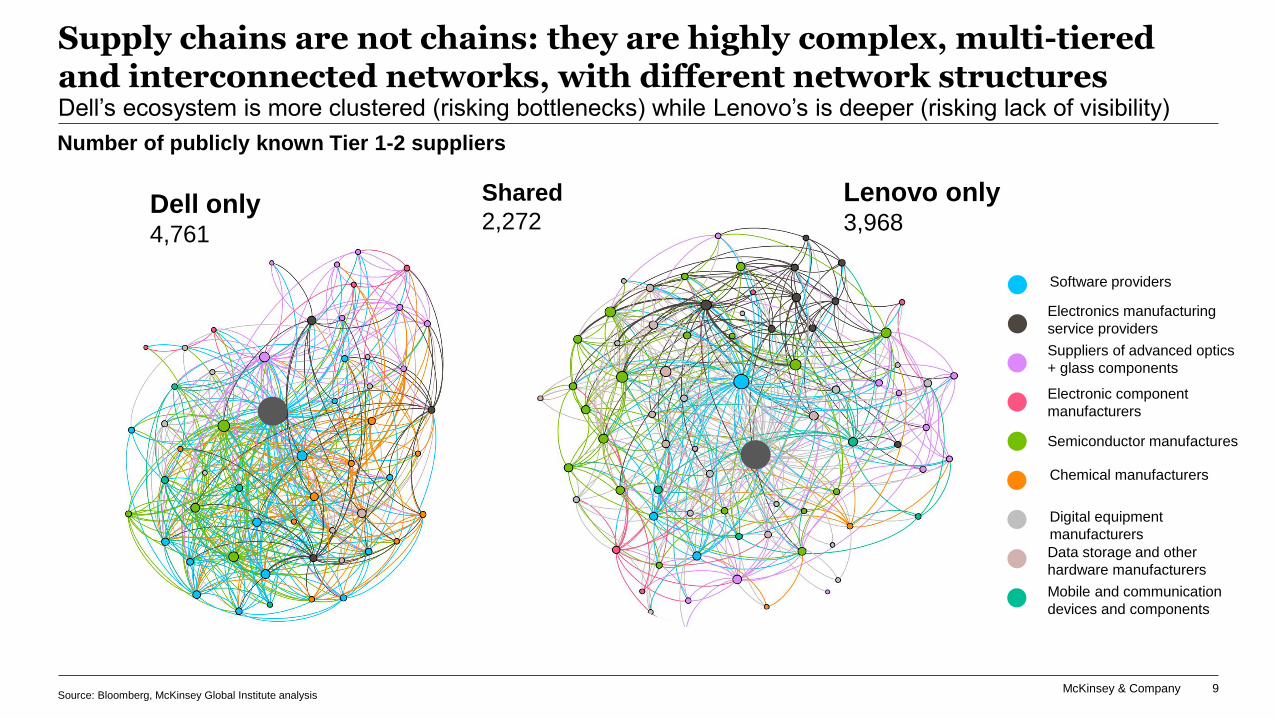

Supply chains are not chains: they are highly complex, multi-tiered and interconnected networks, with different network structures Dell’s ecosystem is more clustered (risking bottlenecks) while Lenovo’s is deeper (risking lack of visibility)

Source: Bloomberg, McKinsey Global Institute analysis

Number of publicly known Tier 1-2 suppliers

Dell only4,761

Shared

2,272

Lenovo only3,968

Software providers

Electronics manufacturing

service providers

Suppliers of advanced optics

+ glass components

Electronic component

manufacturers

Semiconductor manufactures

Chemical manufacturers

Digital equipment

manufacturers

Data storage and other

hardware manufacturers

Mobile and communication

devices and components

McKinsey & Company 10

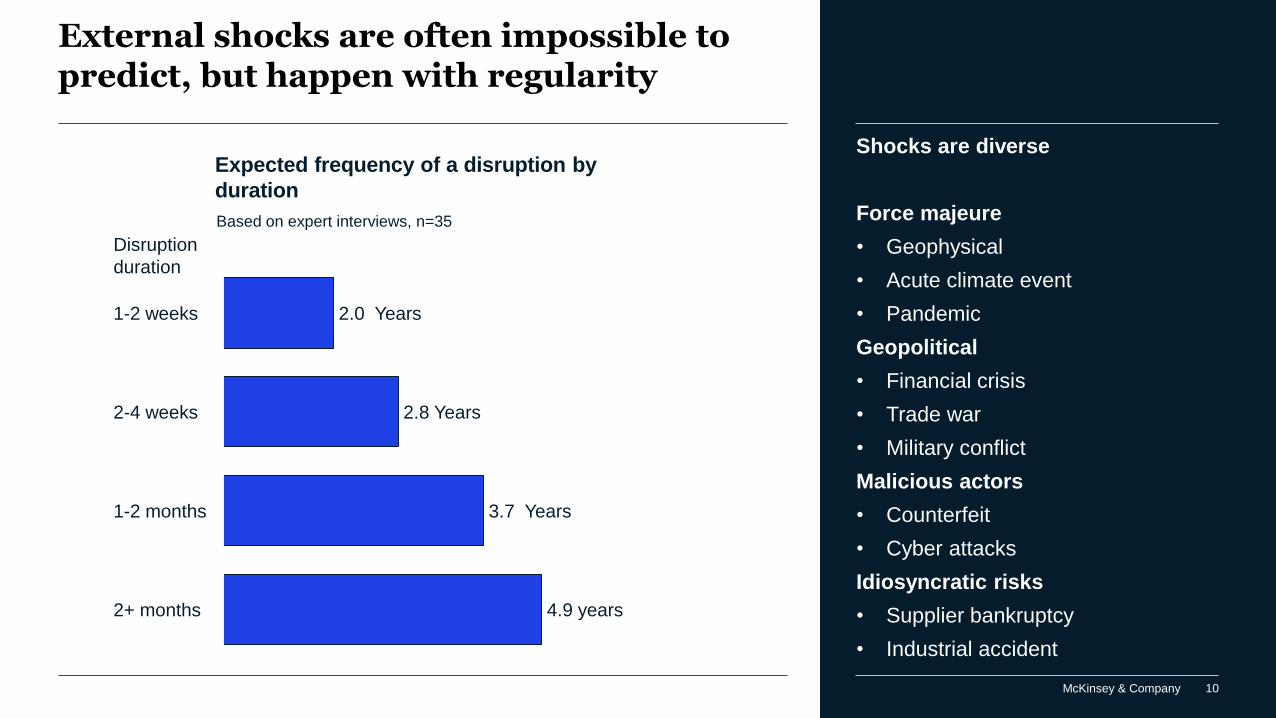

External shocks are often impossible to predict, but happen with regularity

Expected frequency of a disruption by

duration

1-2 months

2-4 weeks

1-2 weeks

2+ months

2.0 Years

2.8 Years

3.7 Years

4.9 years

Based on expert interviews, n=35

Disruption

duration

Shocks are diverse

Force majeure

• Geophysical

• Acute climate event

• Pandemic

Geopolitical

• Financial crisis

• Trade war

• Military conflict

Malicious actors

• Counterfeit

• Cyber attacks

Idiosyncratic risks

• Supplier bankruptcy

• Industrial accident

McKinsey & Company 11

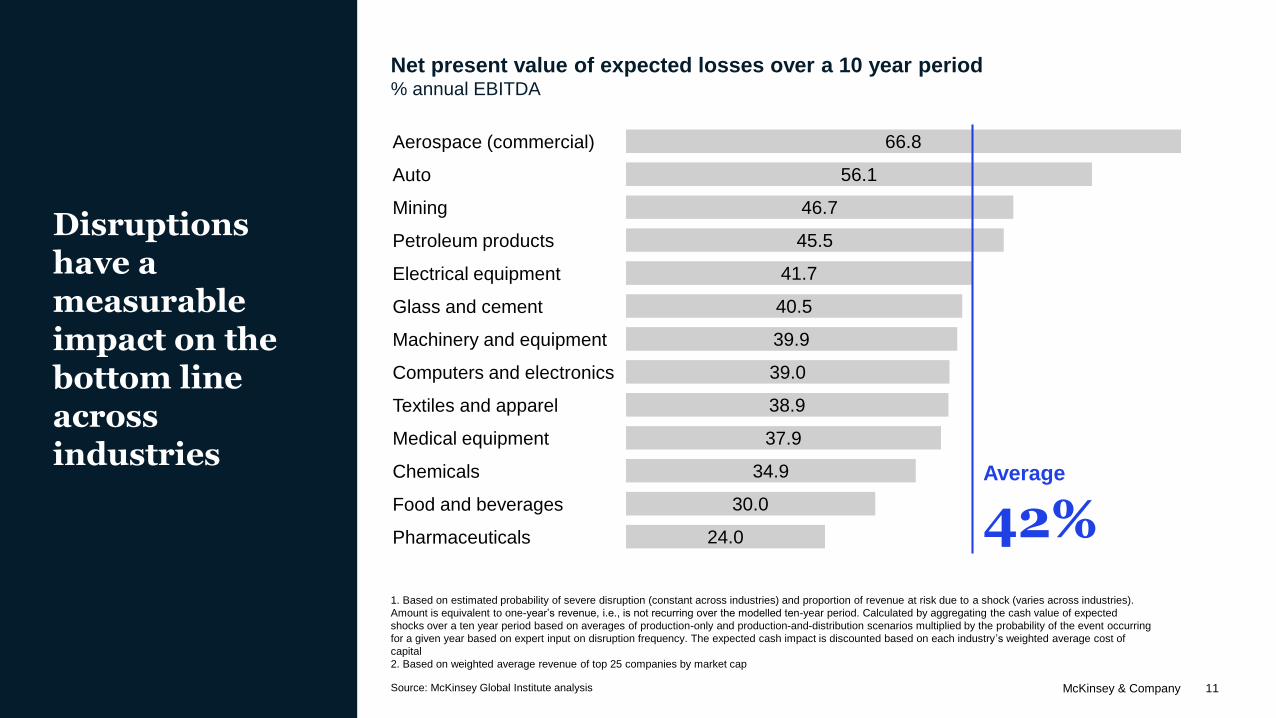

Net present value of expected losses over a 10 year period% annual EBITDA

1. Based on estimated probability of severe disruption (constant across industries) and proportion of revenue at risk due to a shock (varies across industries).

Amount is equivalent to one-year’s revenue, i.e., is not recurring over the modelled ten-year period. Calculated by aggregating the cash value of expected

shocks over a ten year period based on averages of production-only and production-and-distribution scenarios multiplied by the probability of the event occurring

for a given year based on expert input on disruption frequency. The expected cash impact is discounted based on each industry’s weighted average cost of

capital

2. Based on weighted average revenue of top 25 companies by market cap

66.8

56.1

46.7

45.5

41.7

40.5

39.9

39.0

38.9

37.9

34.9

30.0

24.0

Computers and electronics

Machinery and equipment

Glass and cement

Pharmaceuticals

Mining

Aerospace (commercial)

Auto

Electrical equipment

Petroleum products

Textiles and apparel

Medical equipment

Chemicals

Food and beverages

Average

42%

Disruptions have a measurable impact on the bottom line across industries

Source: McKinsey Global Institute analysis

McKinsey & Company 12

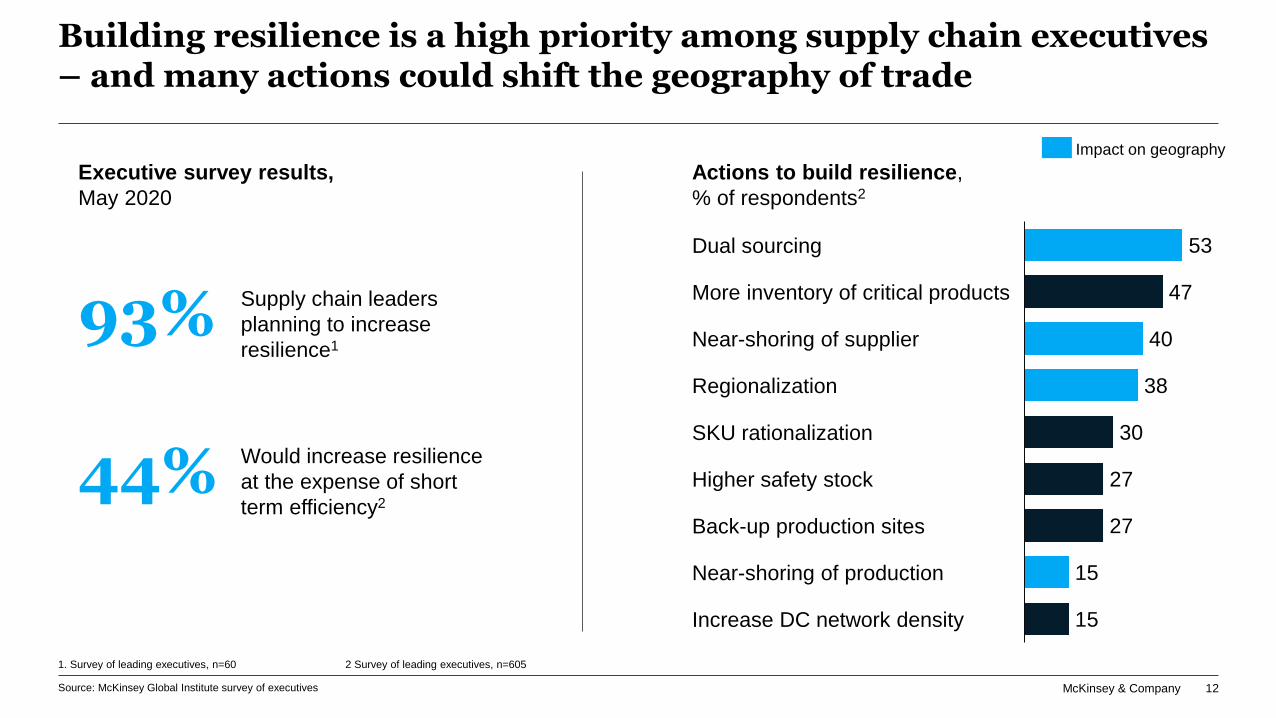

Building resilience is a high priority among supply chain executives – and many actions could shift the geography of trade

Executive survey results,

May 2020

93% Supply chain leaders

planning to increase

resilience1

44% Would increase resilience

at the expense of short

term efficiency2

Source: McKinsey Global Institute survey of executives

1. Survey of leading executives, n=60 2 Survey of leading executives, n=605

53

47

40

38

30

27

27

15

15

SKU rationalization

Increase DC network density

Higher safety stock

Dual sourcing

More inventory of critical products

Back-up production sites

Near-shoring of supplier

Regionalization

Near-shoring of production

Actions to build resilience,

% of respondents2

Impact on geography

McKinsey & Company 13

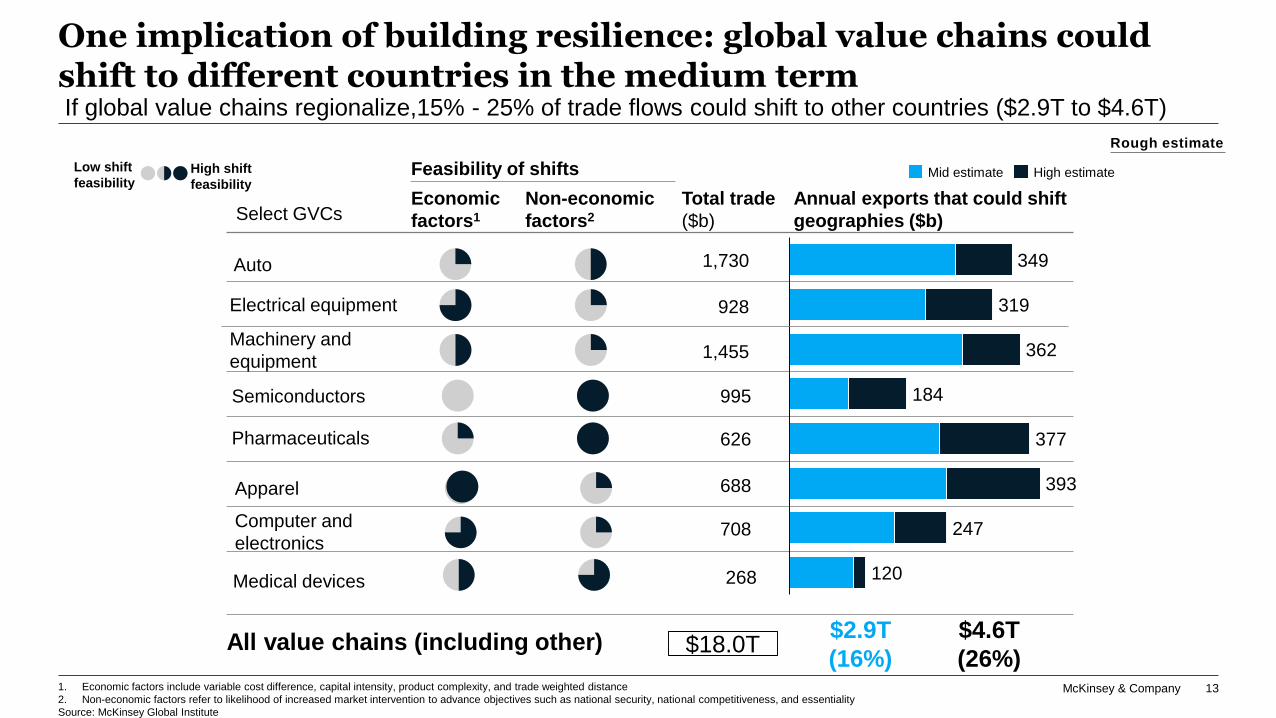

If global value chains regionalize,15% - 25% of trade flows could shift to other countries ($2.9T to $4.6T)

Annual exports that could shift

geographies ($b)

Mid estimate High estimate

Non-economic

factors2

Economic

factors1

Feasibility of shifts

Total trade

($b)

Machinery and

equipment

Computer and

electronics

Auto

Electrical equipment

Semiconductors

Pharmaceuticals

1,455

708

688

1,730

928

995

626

349

319

362

377

184

247

393

120

$4.6T

(26%)

$2.9T

(16%)$18.0T

1. Economic factors include variable cost difference, capital intensity, product complexity, and trade weighted distance

2. Non-economic factors refer to likelihood of increased market intervention to advance objectives such as national security, national competitiveness, and essentiality

Source: McKinsey Global Institute

All value chains (including other)

268Medical devices

Apparel

Low shift

feasibilityHigh shift

feasibility

Select GVCs

Rough estimate

One implication of building resilience: global value chains could shift to different countries in the medium term

CONFIDENTIAL AND PROPRIETARY

Any use of this material without specific permission of McKinsey & Company

is strictly prohibited

Thank you

Please see full MGI report at:

https://www.mckinsey.com/business-

functions/operations/our-insights/risk-resilience-and-

rebalancing-in-global-value-chains