definitions in accordance with article no. (1) of the law ... · definitions in accordance with...

TRANSCRIPT

Instructions To Banks – September 2013

Fifteenth Edition September 2013 5

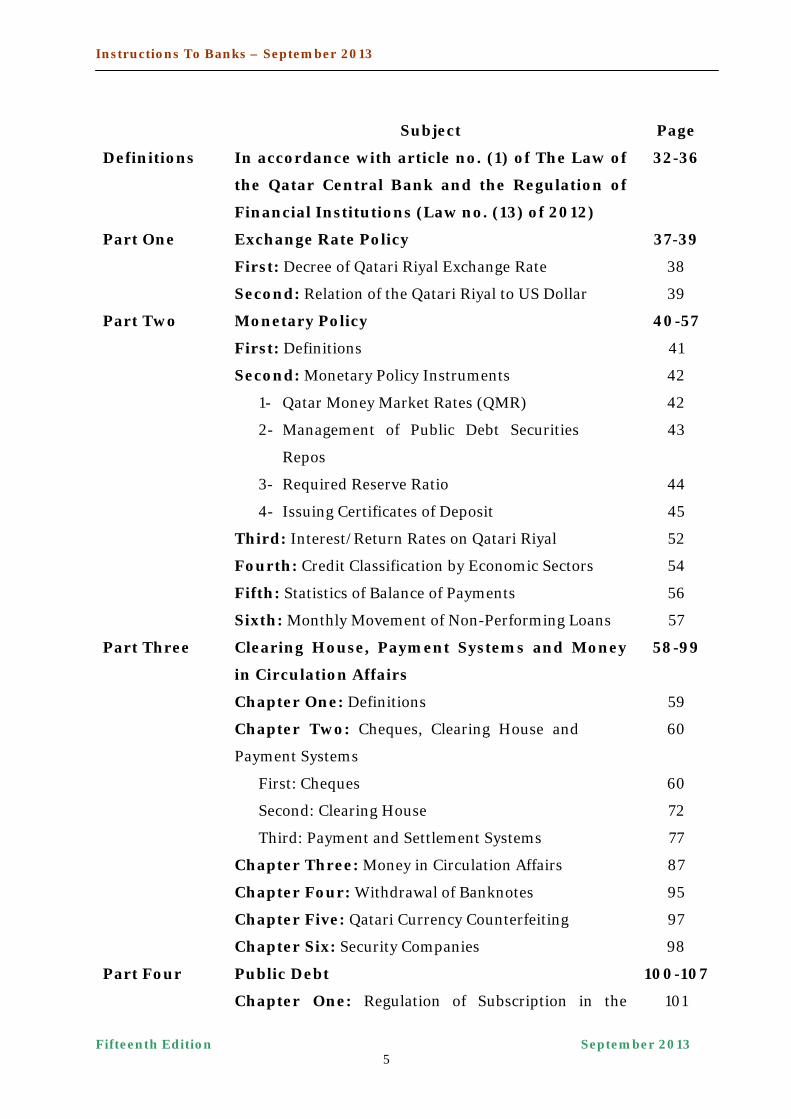

Subject Page

Definitions In accordance with article no. (1) of The Law of

the Qatar Central Bank and the Regulation of

Financial Institutions (Law no. (13) of 2012)

32-36

Part One Exchange Rate Policy 37-39

First: Decree of Qatari Riyal Exchange Rate 38

Second: Relation of the Qatari Riyal to US Dollar 39

Part Two Monetary Policy 40-57

First: Definitions 41

Second: Monetary Policy Instruments 42

1- Qatar Money Market Rates (QMR) 42

2- Management of Public Debt Securities

Repos

43

3- Required Reserve Ratio 44

4- Issuing Certificates of Deposit 45

Third: Interest/Return Rates on Qatari Riyal 52

Fourth: Credit Classification by Economic Sectors 54

Fifth: Statistics of Balance of Payments 56

Sixth: Monthly Movement of Non-Performing Loans 57

Part Three Clearing House, Payment Systems and Money

in Circulation Affairs

58-99

Chapter One: Definitions 59

Chapter Two: Cheques, Clearing House and

Payment Systems

60

First: Cheques 60

Second: Clearing House 72

Third: Payment and Settlement Systems 77

Chapter Three: Money in Circulation Affairs 87

Chapter Four: Withdrawal of Banknotes 95

Chapter Five: Qatari Currency Counterfeiting 97

Chapter Six: Security Companies 98

Part Four Public Debt 100-107

Chapter One: Regulation of Subscription in the 101

Instructions To Banks – September 2013

Fifteenth Edition September 2013 6

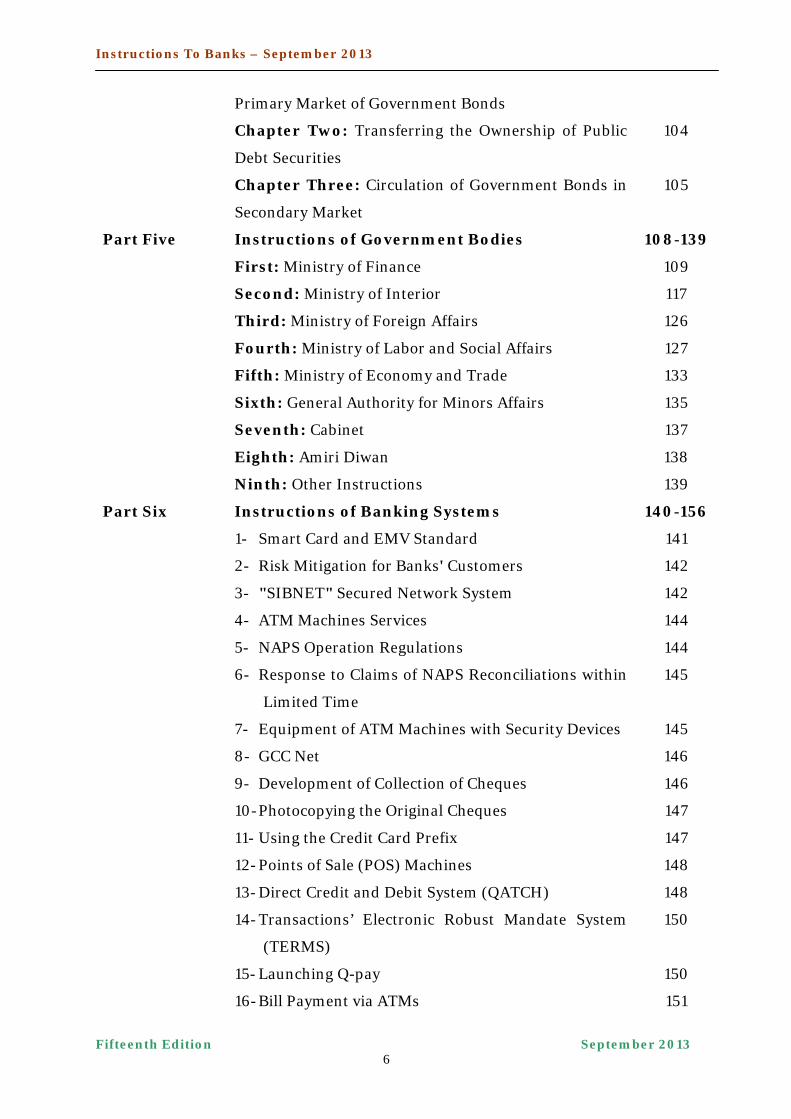

Primary Market of Government Bonds

Chapter Two: Transferring the Ownership of Public

Debt Securities

104

Chapter Three: Circulation of Government Bonds in

Secondary Market

105

Part Five Instructions of Government Bodies 108-139

First: Ministry of Finance 109

Second: Ministry of Interior 117

Third: Ministry of Foreign Affairs 126

Fourth: Ministry of Labor and Social Affairs 127

Fifth: Ministry of Economy and Trade 133

Sixth: General Authority for Minors Affairs 135

Seventh: Cabinet 137

Eighth: Amiri Diwan 138

Ninth: Other Instructions 139

Part Six Instructions of Banking Systems 140-156

1- Smart Card and EMV Standard 141

2- Risk Mitigation for Banks' Customers 142

3- "SIBNET" Secured Network System 142

4- ATM Machines Services 144

5- NAPS Operation Regulations 144

6- Response to Claims of NAPS Reconciliations within

Limited Time

145

7- Equipment of ATM Machines with Security Devices 145

8- GCC Net 146

9- Development of Collection of Cheques 146

10- Photocopying the Original Cheques 147

11- Using the Credit Card Prefix 147

12- Points of Sale (POS) Machines 148

13- Direct Credit and Debit System (QATCH) 148

14- Transactions’ Electronic Robust Mandate System

(TERMS)

150

15- Launching Q-pay 150

16- Bill Payment via ATMs 151

Instructions To Banks – September 2013

Fifteenth Edition September 2013 7

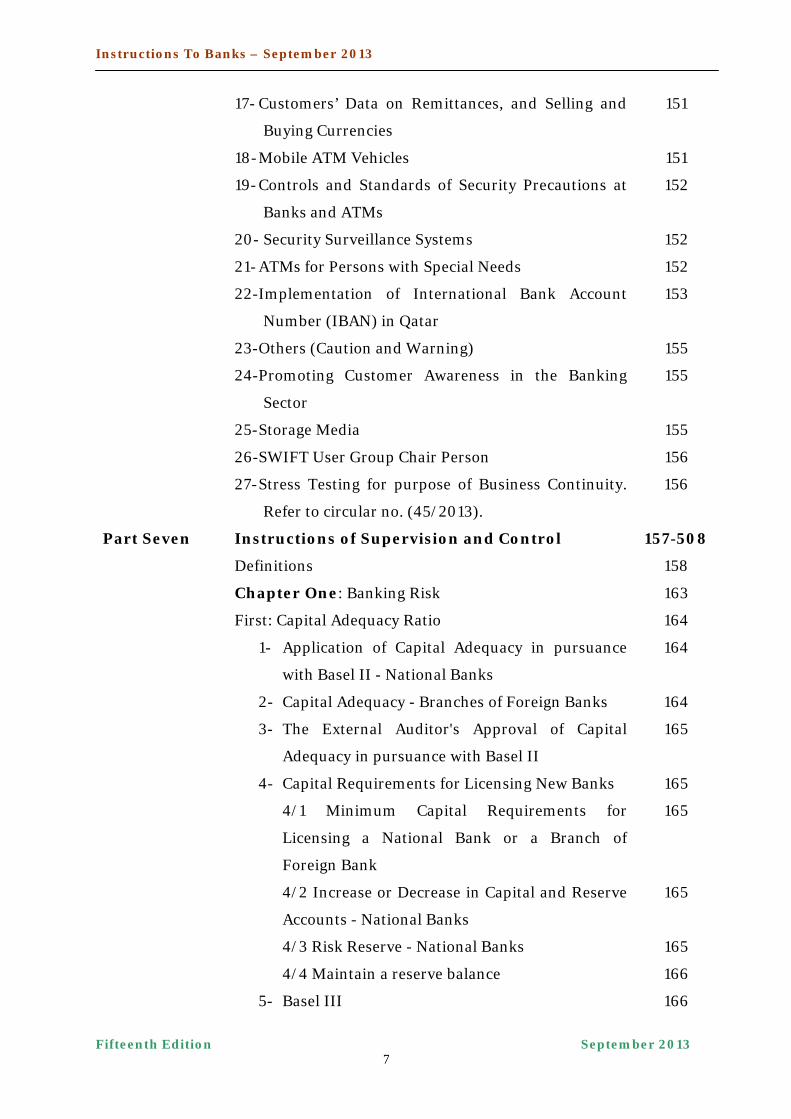

17- Customers’ Data on Remittances, and Selling and

Buying Currencies

151

18- Mobile ATM Vehicles 151

19- Controls and Standards of Security Precautions at

Banks and ATMs

152

20- Security Surveillance Systems 152

21- ATMs for Persons with Special Needs 152

22- Implementation of International Bank Account

Number (IBAN) in Qatar

153

23- Others (Caution and Warning) 155

24-Promoting Customer Awareness in the Banking

Sector

155

25- Storage Media 155

26-SWIFT User Group Chair Person 156

27- Stress Testing for purpose of Business Continuity.

Refer to circular no. (45/2013).

156

Part Seven Instructions of Supervision and Control 157-508

Definitions 158

Chapter One: Banking Risk 163

First: Capital Adequacy Ratio 164

1- Application of Capital Adequacy in pursuance

with Basel II - National Banks

164

2- Capital Adequacy - Branches of Foreign Banks 164

3- The External Auditor's Approval of Capital

Adequacy in pursuance with Basel II

165

4- Capital Requirements for Licensing New Banks 165

4/1 Minimum Capital Requirements for

Licensing a National Bank or a Branch of

Foreign Bank

165

4/2 Increase or Decrease in Capital and Reserve

Accounts - National Banks

165

4/3 Risk Reserve - National Banks 165

4/4 Maintain a reserve balance 166

5- Basel III 166

Instructions To Banks – September 2013

Fifteenth Edition September 2013 8

6- Guidance on Basel Capital Adequacy Pillar II

Application: Supervisory Review and Evaluation

Process (SREP) and Application of Internal

Capital Adequacy Assessment Process (ICAAP)

167

7- Major Shareholders - National Banks 168

Second: Credit and Financing Risk 170

A- Controls on Credit Facility Classification and

Provision Determination

170

First: Instructions on Credit Facility

Classification and Provision Determination

170

A- Definitions 170

1- Credit Facilities 170

2- Rescheduled Credit Facilities 171

B- Credit Facility Classification Categories 171

1- Performing Credit Facilities 171

2- Non-Performing Credit

Facilities

172

C- Indicators of Non-Performing Credit

Facility Classification

172

1- Indicators of Non-Performing

Credit Facilities

172

2- Other Estimating Weakness

Indicators

172

3- Rescheduled Credit Facilities 173

4- Other Considerations for Credit

Facility Classification

174

D- Provision Calculation and Suspended

Interests (Returns)

174

E- Valuation of Collaterals 175

F- General Notes 176

1- minimum requirements that

may be taken into account

while putting up policies and

procedures to classifying the

176

Instructions To Banks – September 2013

Fifteenth Edition September 2013 9

credit facilities

2- Bank should calculate the

provisions in conformity with

the International Financial

Reporting Standards (IFRS)

and the same should be audited

by External Auditor

176

3- Credit Facility Classification

and Provision Determination

179

Second: Reclassification of Credit Facilities 179

Third: Updating and Submission of Provisions

Data on Non-Performing Credit Facilities

179

Fourth: Periodical Data 180

Fifth: Bills Discounted and Past Due

Installments of Loans

180

B- Debt Write-off 181

C- Credit Policies and Concentrations 185

1- Credit Policies 185

2- Credit Concentrations 185

2/1 Definitions 185

2/2 Maximum Limit of Credit

Concentration

188

3- Additional Controls 190

4- Controls on Credit Facilities in terms of

Overdrafts or Overdrawn Current

Accounts (Commercial Banks)

191

5- Purchasing Loans from Inside and Outside

Qatar

194

6- Credit Facilities Granted to Construction

Sector

195

7- Personal Guarantees against Credit

Facilities

195

8- Statement of Account on Credit Facilities

Granted to Customers

195

Instructions To Banks – September 2013

Fifteenth Edition September 2013 10

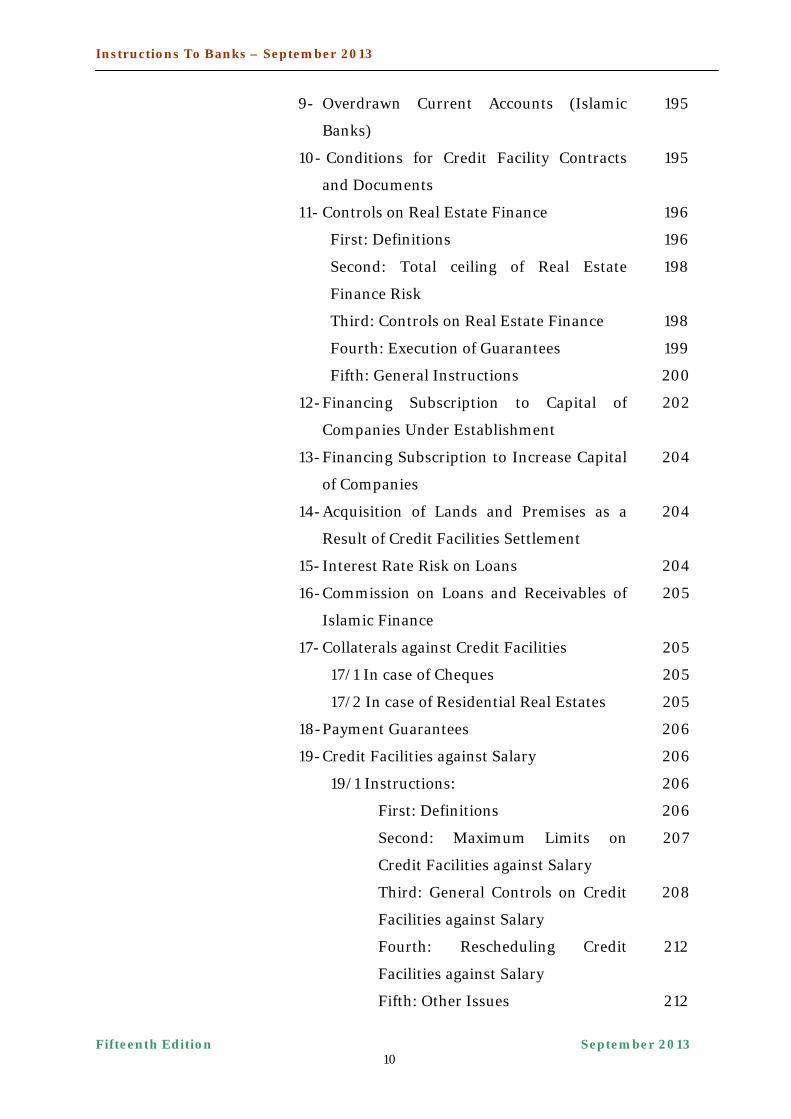

9- Overdrawn Current Accounts (Islamic

Banks)

195

10- Conditions for Credit Facility Contracts

and Documents

195

11- Controls on Real Estate Finance 196

First: Definitions 196

Second: Total ceiling of Real Estate

Finance Risk

198

Third: Controls on Real Estate Finance 198

Fourth: Execution of Guarantees 199

Fifth: General Instructions 200

12- Financing Subscription to Capital of

Companies Under Establishment

202

13- Financing Subscription to Increase Capital

of Companies

204

14- Acquisition of Lands and Premises as a

Result of Credit Facilities Settlement

204

15- Interest Rate Risk on Loans 204

16- Commission on Loans and Receivables of

Islamic Finance

205

17- Collaterals against Credit Facilities 205

17/1 In case of Cheques 205

17/2 In case of Residential Real Estates 205

18- Payment Guarantees 206

19- Credit Facilities against Salary 206

19/1 Instructions: 206

First: Definitions 206

Second: Maximum Limits on

Credit Facilities against Salary

207

Third: General Controls on Credit

Facilities against Salary

208

Fourth: Rescheduling Credit

Facilities against Salary

212

Fifth: Other Issues 212

Instructions To Banks – September 2013

Fifteenth Edition September 2013 11

19/2 Rate of Interest or Return on Credit

Facilities against Salary

213

20- Customers’ Obligations Due to Qatar

Development Bank (QDB) against Housing

Loans

214

21- Granting Credit Facilities in Foreign

Currency

214

22- Credit Facilities granted to Governmental

Bodies and Entities

215

D- Financing Policies in Islamic Banks 217

1- Article no. (105) of QCB Law 217

2- Sharia Supervisory Board 217

3- International Finance 218

4- Local Finance 219

5- Unimplemented Part of Istisna Contracts 219

6- Controls on Tawarruq Finance (Islamic

Banks)

220

7- Overdrawn Current Accounts (Islamic

Banks)

223

8- Commission on Receivables of Islamic

Finance

223

9- Conditions for Credit Facility Contracts

and Documents

223

E- Credit Risk Management 224

First: Establishing an Appropriate Credit Risk

Management Environment

224

Second: Operating under Sound Credit-Granting

Process

227

Third: Establishing an Appropriate

Administration System for Credit Risk

Management, Measurement and Monitoring

234

Fourth: Ensuring Adequate Controls over Credit

Risk

238

- Updated Credit Risk Management 239

Instructions To Banks – September 2013

Fifteenth Edition September 2013 12

System

F- Financing Customers' Trading in Securities 240

G- Instructions to Members of Board of Directors 241

1- Ceilings and Conditions on Credit

Facilities to Members of Board of Directors

241

2- Credit Facilities to Relatives of Members of

Board of Directors

243

3- Transactions of Members of Board of

Directors with the Bank

243

4- Membership of Board of Directors 244

5- Bonuses given to Members of Board of

Directors

246

H- Country Risk Concentration (National Banks) 248

1- Definitions 248

2- Maximum Limits for Country Risk 249

3- Country Risk Management 250

4- Country Credit Facility Classification and

Provision Determination

250

5- Financial Data 251

Third: Bank Investments 252

A- Controls and Ceilings on Bank Investments 252

First: Securities Portfolio 252

1- Investments in Equity Instruments 252

2- Investments in Debt Instruments and

Sukuk

252

3- Investment Ceilings to a Bank's Capital

and Reserves

253

Second: Investment in Associates 253

Third: Investment in Real Estates (Islamic

Banks)

254

Fourth: General Instructions 254

B- Notes on Investment Ceilings 255

C- Purchasing Shares by the Issuing Banks

(Treasury Shares)

255

Instructions To Banks – September 2013

Fifteenth Edition September 2013 13

Fourth: Trading in Foreign Exchange and Money

Market Instruments in favor of the Bank

257

1- Controls on Trading in Foreign Exchange,

Derivatives and Money Market Instruments in

favor of the Bank

257

2- Foreign Exchange Transactions, Forwards,

Futures, Options, and Others

257

3- Ceilings of Interest Rate Gap 258

4- Instructions of Board of Directors on Trading in

Foreign Exchange and Money Market

Instruments

258

Fifth: Concentrations of Deposits and Credit Facilities

at Banks and Financial Institutions

259

1- Definitions 259

2- Rating Banks and Financial Institutions 260

3- Maximum Credit Concentration Limits for

Banks and Financial Institutions

260

4- Additional Controls on Deposits and Credit

Facilities

260

5- Periodical Data 262

6- Periodical Statements on Credit Concentrations

for Banks and Financial Institutions

262

Sixth: Liquidity Management 263

1- General Instructions on Bank’s Liquidity

Management

264

2- Maturity Ladder of Assets and Liabilities 264

3- Cash Flows for Customer Deposits 264

Seventh: Banking Ratios and Indicators 265

A- Liquidity Ratio 265

1- Definitions 265

2- Calculation of Liquidity Ratio 265

B- Credit Ratio 267

C- Ratio of Overdraft To Credit Facilities 268

D- Ratio of Assets in Foreign Currencies To 269

Instructions To Banks – September 2013

Fifteenth Edition September 2013 14

Liabilities in Foreign Currencies

E- Ratio of Fixed Assets for Bank's Use To bank's

Capital and Reserves

270

Eighth: Risk Management 271

Ninth: Islamic Financial Services in Conventional

Banks

272

Tenth: Recognition of the True Sale of Assets 274

Chapter Two: Banking Managerial Risk 275

First: Corporate Governance 276

A- Corporate Governance 276

1- Definitions 276

2- Roles and Responsibilities of Board of

Directors

276

2/1 Set and Develop Strategies, Objectives

and Policies

277

2/2 Organizational Structure Set-Up 277

2/3 Committees Constitution and

delegation of powers and authorities

278

2/4 Monitor the Implementation of

Policies and Performance and Risk

Assessment

280

2/5 Appointment of Internal Auditing

Staff and Monitoring

281

2/6 External Auditor Approval 282

2/7 Responsibility Towards Shareholders

and Other Parties

283

2/8 Board Responsibility towards QCB 283

3- Roles and Responsibilities of Executive

Management

284

3/1 Assist in Setting up and Development

of Strategies, Objectives and Policies

284

3/2 Assist in Forming the Organizational

Structure

284

3/3 Conduct Transactions and Implement 284

Instructions To Banks – September 2013

Fifteenth Edition September 2013 15

Policies

3/4 Submit Reports to the Board of

Directors

286

3/5 Preparation of Financial Statements 286

3/6 Development of Professional

Aptitude and Skills

287

3/7 Responsibility towards Internal and

External Auditors

287

3/8 Responsibility towards QCB 287

4- General Provisions 288

B- Core Principles for Banks' Remuneration

Policy/System

288

Second: Bank Senior Appointments 290

1- Appointment of General Manager/Chief

Executive Officer of the Bank

290

2- Bank Senior Appointments 290

3- Movement of Senior Staff 291

4- Official Vacations and Tasks of the General

Manager/Chief Executive Officer

291

5- Employment of Relatives 291

Third: Authorized Signatories 292

1- Statements and Correspondences 292

2- Names and Signature Forms of the Board of

Directors and General Management Members

292

Fourth: Internal Auditing 293

Fifth: Outsourcing (Outsourcing Regulations) 294

Sixth: Consolidated Supervision of National Banks,

Their External Branches and Subsidiaries

296

1- Definitions 296

2- Corporate Governance 297

2/1 Roles and Responsibilities of the Bank's

Board of Directors

297

2/2 Roles and Responsibilities of the Bank's

Executive Management

301

Instructions To Banks – September 2013

Fifteenth Edition September 2013 16

3- Concentration Risks 301

3/1 Credit Risks for Parties of Interrelated

Interests within the Banking Group

301

3/2 Customer's Credit Concentrations 302

3/3 Credit Concentrations at Banks 303

3/4 Investment Risk Concentrations 303

3/5 Real Estate Financing Concentrations 303

3/6 Credit Concentrations and Transactions

between the Bank and the Subsidiaries

304

4- Assessment of Debts and Other Assets 304

5- Capital Adequacy Ratio 304

6- Liquidity Risk 305

7- Other Risks for Assets and Provisions 305

8- Risk Management 305

9- Other Issues 305

10- Consolidated Statements and Reports for Bank

and its Group

306

Chapter Three: Modern Technology and E-Banking

Services Risks

307

Chapter Four: Relation with Customers 309

First: Customers' Investments 310

1- Investment Activity for Customers 310

1/1 Investment Business 310

1/2 Organizational Instructions 310

1/3 Relation with Customers 311

1/4 Internal Controls to Banks 312

2- Managing and Marketing Investment Portfolios

and Accounts for Customers

312

2/1 Definitions 312

2/2 Managing Investment Account 313

2/3 Issuing and Managing Investment Portfolios 315

2/4 Marketing Investment Mutual Funds and

Portfolios for Others

318

2/5 Investment Mutual Funds 320

Instructions To Banks – September 2013

Fifteenth Edition September 2013 17

2/6 Other Regulations and Instructions 325

2/7 Other Investments Issues 327

2/8 Details of the Periodical Data for Investment

Portfolios and Mutual Funds

327

2/9 Auditing Investment Portfolios and Mutual

Funds

327

2/10 Disclosure Through Advertising for

Introducing or Marketing Investment Products

328

2/11 QCB’s Non Objection to Investment

Portfolios and Products Issuance and Marketing

329

2/12 Real Estate Funds 329

3- Banks' Transactions on behalf of Customers in

Foreign Exchange, Commodities and Metals

330

4- Customers' Investments in Foreign Companies'

Stocks

331

Second: Customers' Deposit Accounts 332

1- Regulations for Opening Personal Deposits

Accounts

332

1/1 Completion of Data, Documents and

Contracts

332

1/2 Customers Data in Forms, Contracts and

Accounts

332

1/3 Documents to be attached to the Account

Opening Forms and Contracts

333

1/4 Contracts to be Concluded 333

1/5 Customer Accounts Statements 334

1/6 Opening more than one main account for a

customer

334

2- Account Opening Procedures 335

2/1 Opening Current Account 335

2/2 Customers are not permitted to use Cheques

for drawing from the Saving Accounts

335

3- Deposits at Islamic Banks/Mudaraba

Percentages and Profit Rates

335

Instructions To Banks – September 2013

Fifteenth Edition September 2013 18

4- Introducing New Type of Deposits 336

5- Opening an Account for Companies Applying for

License to Work in Free Zones of Science and

Technology Oasis

336

6- Resident and Non-Resident Accounts 336

7- Using Personal Accounts for Commercial

Purposes

337

8- Promoting Customer Awareness in the Banking

Sector

338

Third: Marketing Products of Insurance 339

Fourth: Providing Service Counters in Banks for

Persons with Special Needs

341

Fifth: Special Need Customers (Blinds) 342

Sixth: Commissions and Fees on Personal Accounts

and Services

343

1- Limits of Commissions and Fees 343

2- Commission and Fees Disclosure 343

Chapter Five: Dormant Deposits and Unclaimed

Accounts

344

First: General Instructions 345

Second: Dealing with Dormant Deposits and

Unclaimed Accounts

345

1- Dormant Deposits Accounts 345

2- Unclaimed Banking Cheques and Transfers 346

3- Unpaid Shareholders' Profits 347

4- Customers' Accrued and Unpaid Investments 348

5- Other Funds not remitted to Owners 348

6- Contents of Unclaimed Safe Boxes 349

7- General Rules 350

Chapter Six: External Auditor 351

1- Appointing and Changing the External Auditor 352

2- Conditions Required for External Auditor 353

2/1 Registration and License 353

2/2 Professional Efficiency and Experience 353

Instructions To Banks – September 2013

Fifteenth Edition September 2013 19

2/3 Neutrality and Independency 353

2/4 Honesty, Creditability and Secrecy 354

3- External Auditor’s Tasks and Duties 354

4- External Auditor's Responsibilities Towards

QCB

355

5- External Auditor's Reports 356

5/1 The Annual Public Disclosure Report 356

5/2 Quarterly Financial Reports 356

5/3 Internal Control Letters and

"MANAGEMENT LETTERS"

357

6- External Auditor's Special Tasks 357

7- Contracting with External Auditor 357

8- External Auditor for Mutual Funds 358

9- Credit facilities Classification and Provision

Determination (External Auditor)

359

10- Legal Issues related to External auditors 359

Chapter Seven: Banks' Relation with QCB 362

First: Centralizing Banking Credit Risk Reporting 363

Second: Banks' Correspondence with QCB 370

1- The Designation Codes for Supervision and

Control Department

370

2- Regulating Banks' Correspondence with

Supervision and Control Department

370

3- Organizational Structure of the Supervision and

Control Department

370

4- QCB Inspectors' Reports 371

5- Bank’s Organizational Structure 371

6- QCB Organizational Structure 371

Third: License, Registration and Fees - Banks 372

1- License for Banks 372

1/1 Banking License Application Forms 372

1/2 Granting or Rejection of licensing

application

372

1/3 Promulgate the decision to grant the license 372

Instructions To Banks – September 2013

Fifteenth Edition September 2013 20

1/4 The QCB may license foreign financial

institutions to open branches

373

1/5 The financial institution shall commence

conducting the licensed services, businesses or

activities

373

1/6 Amending Licensing conditions 373

1/7 License Renewal 373

2- Fees Received by QCB 373

2/1 Fees Received by QCB according to Annex

no. (26)

373

2/2 Method of Collecting the Annual Fees 373

3- Bank’s Articles of Association and Incorporation 374

4- Main Data for Bank’s Registration 374

5- Opening Branches and ATMs 375

6- Data for Starting Branch Activity and Operating

ATMs

375

7- Revoke or Cease License 375

Fourth: Banks' Working Hours and Official Holidays 376

Fifth: Undertaking from the Headquarters 378

Sixth: Classification of Headquarters and Branches

Activities

379

Seventh: Back Office Activity of Branches of Foreign

Banks

381

Eighth: Security and Safety in Banks and ATMs 383

A- Security and Safety Instructions 383

B- Standards and Specifications of Security

Precautions at Banks and ATMs

387

1- IT Room 387

2- Safe Boxes Room 387

3- Main Branch and Branches 387

4- ATMs 388

C- Controls and Standards of Security

Precautions at Banks and ATMs

389

D- Security Surveillance Systems 391

Instructions To Banks – September 2013

Fifteenth Edition September 2013 21

Ninth: Reporting on Extraordinary Cases to QCB 393

Tenth: Compliance Function 394

Eleventh: Business Continuity 396

A- Business Continuity Plan Guidelines 396

B- Business Continuity Management Guidelines 399

Twelfth: Restricted Activities for Banks 407

Chapter Eight: End of Year Financial Statements and

Additional Instructions

408

First: Monthly Statement of Assets and Liabilities 409

1- Monthly Statement of Assets and Liabilities 409

1/1 Monthly Balance Sheet 409

1/2 Monthly Balance Sheet

Implementation

410

A- Technical Instructions of the

monthly balance sheet

410

B- All banks should comply with the

following

410

C- New amendments have been made

to the monthly balance sheet and

some tables required from bank and

its branches inside Qatar

411

D- Monthly tables attached to the

balance sheet

411

2- End of Year Financial Statements 411

2/1 International Accounting Standards 411

2/2 Accounting Standards for Islamic Banks 415

2/3 Accounting Classification of Deposits at

Banks (Islamic Banks and Islamic Branches of

Commercial Banks)

423

2/4 Evaluation of Shares in Companies

according to Shareholder's Equities (All banks)

425

2/5 Consolidated Financial Statements 425

Second: Calculation and Distribution of Profits between

Depositors and Shareholders of Islamic Banks

430

Instructions To Banks – September 2013

Fifteenth Edition September 2013 22

1- Method for Distributing Profits 430

2- Distribution of Payment out of Profits to

Depositors

431

3- Loss Bearing 431

4- The Ratio of Mudarba and Contracts Signed with

Depositors

431

5- Forms for Non-Objection from QCB 432

Third: Additional Instructions 433

Chapter Nine: Other Banking Issues 436

1- Embezzlement Crimes 437

2- Activities Designed to be Conducted Abroad

(National Banks)

437

3- Cash 437

4- Contracts signed with customers 437

5- Insurance 438

6- Gathering information relating to Basel II

Framework

438

7- The Sole Official Document for Personal

Identification

438

8- Automatic Enrolment 438

9- Arab Union for the Blind 438

10- Warning of Banking Electronic System Breaches 439

11- Shareholders General Assembly (National

Banks)

440

12- ATM Robbery through Electronic Devices 440

13- Naming Contingency Officers 441

14- ATM Fraud 441

15- Fraud Attempts 441

16- Licensed Exchange Houses operating in Syria 442

17- Banks Using Holy Names and Places in Kingdom

of Saudi Arabia

442

18- Other Account Receivables within the Credit

Facilities

442

19- Special Places for QCB Inspectors 443

Instructions To Banks – September 2013

Fifteenth Edition September 2013 23

20- Qatarization of Posts in The Banking

System

443

21- Changing deposits, CDs and Transactions among

Banks

443

22- ATMs for Persons with Special Needs 443

23- Reporting on Stolen Currency Notes 444

24-Presence of Companies’ Representatives Inside

Banks

444

25- Debt Securities Issuance 445

Chapter Ten: Anti-Money Laundering (AML) and

Combating Financing of Terrorism (CFT)

446

First: Regulations 447

1- Legal Basis for the regulations 447

2- Objectives of the regulations 447

3- Definitions 448

4- General Provisions 453

5- Key AML/CFT Principles 454

6- General AML and CFT Responsibilities 454

7- Board of Directors 459

8- Money Laundering Reporting Officer [MLRO]

and Deputy

460

8.1 Appointment 460

8.2 Eligibility to be MLRO and Deputy 461

8.3 General Responsibilities of MLRO 461

8.4 Particular Responsibilities of MLRO &

Deputy

462

8.5 Reporting by MLRO to the Board 462

9- Risk Based Approach 464

9.1 Risk Based Approach – General 464

9.2 Assessment Methodology to mitigate ML/FT

threats

465

9.3 Risk profiling business relationship 465

10- Customer Risk 465

11- Product Risk 468

Instructions To Banks – September 2013

Fifteenth Edition September 2013 24

11.1 Risk assessment of product risk 468

11.2 Policies & procedures for product risk 468

11.3 Products with fictitious, false or no names 468

11.4 Correspondent banking relationships 468

11.5 Shell Banks 470

11.6 Payable Through Accounts 470

11.7 Power of Attorney 471

11.8 Bearer shares and Share warrants to bearer 471

11.9 Wire transfers 471

11.10 Non-profit organization 473

12- Interface or delivery channel risk 474

12.1 Risk assessment for interface risk 474

12.2 Policies and procedures for interface risk 474

12.3 Non-face-to-face business relationship and

New Technology

475

12.4 Reliance on Third Party 475

13- Jurisdiction Risk 476

14- Know Your Customer (KYC) 478

14.1 General Principle of KYC 478

14.2 Customer Acceptance Policy and

procedures

478

14.3 Customer Due Diligence (CDD) – Basic

requirements

479

14.4 General requirements on extent of CDD 480

14.5 General requirements for on-going

monitoring

480

14.6 FIs unable to complete CDD procedure for

customer

481

14.7 Timing of customer due diligence 481

14.8 Circumstances when CDD may be

completed at a later stage

482

15- Customer Identification Documentation 482

16- Enhanced CDD and on-going monitoring 484

17- Simplified Customer due diligence 486

Instructions To Banks – September 2013

Fifteenth Edition September 2013 25

18- Reporting 487

19- Tipping off 490

20- Screening and training requirements 491

21- Documents, Record Keeping and Retention 493

22- Internal & External Auditing 494

23- Sanctions 494

24-Approved forms to be used 494

25- Regulations effective from 494

A- Miscellaneous issues for guidance 494

B- Typologies 497

C- Guidance by International Bodies 498

Second: FATF Statement on AML and CFT 499

Third: Financial Information (FIU) Unit's Guidance

and STR Forms

500

Fourth: National Anti money laundering and Terrorism

Financing Committee Guidance on Mechanism to

revise matching of names, persons, and entities with

Security Council Sanctions Lists

501

Chapter Eleven: Qatar Exchange 502

1- Disclosure of Profit Distributions by Qatar

Exchange

503

2- Controls on Conducting Financial Brokerage

Activity in Qatar Exchange

503

3- Conducting Financial Brokerage Activity in

Qatar Exchange

507

Part Eight Other Instructions 509-517

First: Banks' Correspondences with QCB 510

1- Official Language for Correspondence 510

2- Regulating the banks' Correspondence with QCB 510

3- Response to Correspondences 512

Second: Banking Consumer Services Protection

Department

513

Third: The Law of the QCB and the Regulation of

Financial Institutions (Law no. (13) of 2012)

514

Instructions To Banks – September 2013

Fifteenth Edition September 2013 26

Fourth: FIU Instructions 515

Fifth: Other Instructions 517

1- Ernst & Young Appointment (National Banks) 517

2- Delegation of Liaison Officer 517

3- Imposing Financial fines for delayed and

inaccurate data sent to QCB

517

Part Nine Qatar Credit Bureau 518-522

1- Compliance Officer Nomination 519

2- Appointment of Qatar Credit Bureau CEO and

the Approval of the Organizational Structure

519

3- Compliance officers cooperation with Ernest and

Young

519

4- “eDATE” program Installation and Application 519

5- Qatar Credit Bureau/Credit Reports: 520

6- Data Update/Concealment 521

7- Storage Devices 522

Part Ten Instructions 0f Financial Stability and Statistics 523-536

Instructions of Financial Stability and Statistics

Department

524

1- Data Relating to Financial Stability and

Statistics Department

524

A- Monthly Data 524

B- Quarterly Data 525

C- Consumer loans (Biannual Data) 525

2- Assignment of Liaison Officer in each Bank for

Coordination Purposes

525

3- Establishing Data Base at Financial Stability

Department for Banking System Employees in

Qatar (Biannually)

525

4- Accounts for Charity Purposes (Monthly) 526

5- Banking Lending Survey (Quarterly) 526

6- Transactions outside Qatar (National Banks)

(Quarterly)

526

Instructions To Banks – September 2013

Fifteenth Edition September 2013 27

7- Financial Stability and Statistics Administrative

Structure

526

8- Stress Testing 526

Part Eleven Sanctions and Financial Penalties 537-554

First: Chapter 9 of The Law of the QCB and the

Regulation of Financial Institutions (Law no. (13) of

2012) regarding Sanctions and financial Penalties

538

A- First Chapter: Sanctions 538

B- Second Chapter: Financial Penalties 542

Second: Imposing Sanctions and Financial

Penalties

543

1- Impose Standard Financial Penalties 543

2- 543

2/1 Capital Adequacy of Foreign Branches 543

2/2 Real Estate Financing Controls 543

2/3 Credit against Salary 544

2/4 Finance by Tawaroq 544

2/5 Credit Risk Department 544

2/6 The Ratios of International Financing and

Real Estates Investments (for Islamic Banks)

544

2/7 Liquidity Ratio 545

2/8 Credit Ratio 545

2/9 Overdraft to Credit Facilities Ratio 546

2/10 The Ratio of the Assets in Foreign

Currencies to the Liabilities in Foreign

Currencies

547

3- Procedures for Repurchases Operations

(REPOs)

547

4- Required Reserve Ratio 547

5- Dividend Coupons and Payment Orders issued

by Banks and Companies

548

Instructions To Banks – September 2013

Fifteenth Edition September 2013 28

6- Cheque Issuance, its Legal Form, and Cheques

with no Fund

548

7- Clearing at QCB 548

8- Fines for Electronic Clearing 548

9- Statistics of Balance of Payments 548

10- Non-Negotiable Cheque 549

11- Cash Dealing (Cash deposited at QCB) 549

12- Currency Counting Machines Upgrades 549

13- Mutilate Banknotes 549

14- Security Companies 549

15- Banking Systems Instructions (Banking

Electronic Instructions)

549

16- Overdraft Current Accounts (Islamic Banks) 551

17- Conditions and Documents for Credit

Agreement

552

18- Financing of Subscription in Capital of

Companies under Construction

552

19- Financing Customers’ Trade in Securities 552

20- Interest Risks on Loans 552

21- Credit Facilities granted to Governmental Bodies

and Entities

552

22- Using Personal Accounts for Commercial

Purposes - circular no. (225/2007)

552

23- Anti-money Laundering and Terrorism

Financing

552

24-Corporate Governance for Banks and Financial

Institutions

553

25- Inter-Bank Payments System 553

26-Modern Technology and Electronic Banking

Services Risks

553

Instructions To Banks – September 2013

Fifteenth Edition September 2013 29

27- Commissions and Fees on Personal Banking

Accounts and Services

553

28- Imposing financial fine on delayed and

inaccurate data sent by banks

553

29-Circular no. (63/2011) dated 22/8/2011

(interest/return on credit against salary)

553

30- Bonuses given to Members of Board of

Directors

554

31- Controls and Ceilings on Bank Investments 554

32- Banks Main Registration Data 554

Part Twelve Periodical Data 555-576

First: Capital Adequacy Ratio 556

1- Basel II Capital Adequacy Ratio for National

Banks

556

2- Capital adequacy for Branches of Foreign Banks

computing or not computing Basel Capital

Adequacy Ratio at their H.O.

556

3- Approved Electronic System for Capital

Adequacy

557

4- Capital Adequacy Calculation Reports 557

5- Basel III: Item no. (5) in page no. (155) 557

6- Major Shareholders 557

Second: Credit and Financing Risk 559

1- Provisions for Credits Classified as Substandard,

Doubtful or Bad, and Financial Investment

Evaluation Forms

2- Debts Write off 559

3- Credit Concentrations 559

4- The Overdraft Accounts and the Overdrawn

Accounts (Commercial Banks)

561

5- Real Estate Financing Net Risk Ratio 562

Third: Bank's Investments and Credit Concentration

for Banks and Financial Institutions

563

Instructions To Banks – September 2013

Fifteenth Edition September 2013 30

Credit Concentrations for Banks and Financial

Institutions

563

Fourth: Banking Ratios and Indicators 564

1- Liquidity Ratio and Management 564

2- Credit Ratio 564

3- Overdraft to Credit Facilities Ratio 565

4- The Ratio of International Financing and Real

Estate Investments

565

5- Ratio of assets in Foreign Currencies to

Liabilities in Foreign Currencies

566

6- Cash Flows for Customer Deposits 567

Fifth: Customers' Investments 568

Sixth: Banking Credit Risk System 569

Seventh: End of Year Financial Statements and

Calculation and Distribution of Profits between

Depositors and Shareholders of Islamic Bank

570

1- Assets and Liabilities Monthly Statement 570

2- Consolidated Financial Statements 570

2/1 For Conventional Banks 570

2/2 For Islamic Banks 570

3- Calculation and Distribution of Profit between

Depositors and Shareholders of Islamic Banks

570

4- Financial Statements of Investment Funds 571

Eighth: Other Periodical Data 572

1- Main Data for Bank’s Registration 572

2- Obligatory Reserve Requirement 572

3- Monthly Movement of Defaulted Debts 572

4- Credit Risk System (updated credit risk

management system)

572

5- Financial Stability and Statistics Data 573

5/1 Monthly Data 573

Instructions To Banks – September 2013

Fifteenth Edition September 2013 31

5/2 Quarterly Data (as from the first Quarter of

2009)

574

5/3 Biannual Data 575

6- Consolidated Supervision Instructions on

National Banks, their External Branches and

Subsidiaries

575

7- Treatment of Bad Debits 576

8- Major Shareholders 576

9- Qatarization in the Banking System 576