decoding the iesba code by: ragiema thokan … the iesba code by: ragiema thokan-mahomed ... ifac...

TRANSCRIPT

CP04 - V1 Page 1 of 41

Decoding the IESBA CODE

By: Ragiema Thokan-Mahomed

Acknowledgements

These notes have been produced for the purpose of giving an overview to the

required ethical considerations of the Professional Accountant (SA) in relation to the

IFAC Code of Ethics for Professional Accountants and the SAIPA Code of Conduct.

We acknowledge that the internet has provided useful information, videos and

articles that have been included in these notes for further reading/viewing by the

participants of the course.

I would like to thank the Legal, Ethics and Compliance department at SAIPA- Aysha,

Kabelo, Mulalo and Lindani, for their assistance in researching areas of these notes.

It is comforting to know that I can always rely on your dedication in producing quality

work.

A special thanks to Rashied Small, Faith Ngwenya and my co-presenter Saleem

Kharwa for imparting your knowledge and providing valuable input that I hope will

make this CPD beneficial for our members.

The total Continual Professional Development (CPD) of the attended course is

4.30 Ethics structured hours.

CP04 - V1 Page 2 of 41

Contents

Decoding the IESBA CODE ........................................................................................................... 1

By: Ragiema Thokan-Mahomed ................................................................................................ 1

1. Objectives ................................................................................................................................ 3

2. Decoding the IESBA – Code of Ethics .................................................................................. 3

2.1 Background ...................................................................................................................... 3

2.1.1 Integrity ....................................................................................................................... 8

2.1.2 Objectivity ................................................................................................................. 13

2.1.3 Professional Competence and Due Care (Section 130) ................................... 16

2.1.4 Confidentiality (Section 140) ................................................................................. 18

2.1.5 Professional Behaviour (Section 150) ................................................................. 20

3. Significant amendment to the code ..................................................................................... 22

Section 360................................................................................................................................ 22

4. Identifying reportable irregularities in terms of South African Law ................................... 25

One such example is that of section 29 of the Companies Act which states: ..................... 25

5. Touch, pause, engage ...................................................................................................... 27

6. Case study ......................................................................................................................... 30

THE CASE STUDY THAT FOLLOWS HAS BEEN EXTRACTED FROM THE GUIDE TO QUALITY CONTROL FOR SMALL-AND

MEDIUM-SIZED PRACTICES, THIRD EDITION, PRODUCED BY IFAC. CANDIDATES ARE REQUIRED TO SIT IN GROUPS TO

DISCUSS THE EFFECT OF THE ACTIONS ON THE FUNDAMENTAL PRINCIPLES AND ELABORATE ON SAFEGUARDS TO

THREATS AND POSSIBLE MITIGATION. .................................................................................................... 30

5. Awareness of my duties.................................................................................................... 36

6. Legislative requirements ................................................................................................... 37

7. Holding my ground – tips to achieving success in your practice................................... 40

CP04 - V1 Page 3 of 41

1. Objectives

As an internationally recognised professional, you are required to abide by the

IFAC code of ethics, to ensure that you deliver world class accounting

services in an ethically responsible manner. The following areas have been

identified as the minimum requirements necessary to achieve compliance:

5 Key elements of the code

Significant amendments to the code

Identifying reportable irregularities

Legislative requirements

Awareness of my duties as a professional accountant

2. Decoding the IESBA – Code of Ethics

2.1 Background

The International Ethics Standards Board for Accountants (IESBA) is an independent

standard-setting board that develops, in the public interest, high-quality ethical

standards and other pronouncements for professional accountants worldwide.

Through its activities, the IESBA develops the Code of Ethics for Professional

Accountants, which establishes ethical requirements for professional accountants.

The board also provides adoption and implementation support, promotes good

ethical practices globally, and fosters international debate on ethical issues faced by

accountants. 1

The Code consists of Part A – establishes the fundamental principles of professional

ethics for professional accountants, Part B – applies to professional accountants in

public practice and Part C – applies to professional accountants in business.

Significant changes between the 2015 and the current version (2016) are as follows:

Section 225 and 360 addresses’ the responsibilities of the professional

accountants when they become aware of non-compliance or suspected non-

compliance to laws and regulations committed by a client or employer.

Consequential and conforming changes have been made to Sections 100,

140, 150, 210 and 270 of the Code.

1 www.ethicsboard.org, accessed on 13 January 2017.

CP04 - V1 Page 4 of 41

These changes will be effective from 15 July 2017.2

The IESBA requires that a member body of IFAC shall apply the IESBA Code of

Ethics.

SAIPA prides itself as being one of two accountancy bodies based in South Africa

with accreditation from the International Federation of Accountants (IFAC). We

subscribe to the requirements of the Statements of Members Obligations (SMOs)

and our member policies and professional qualification are founded on the

International Education Standards (IESs).

SAIPA serves on the following IFAC structures:

IFAC Council

Edinburgh Group (EG)

Where our input is required, we are invited to the MOSAIC and PAODC

(Professional Accountancy Organisations Development Committee)

A distinguishing mark of the profession is it acceptance of the responsibility to act in

the public interest (section 100.1). This means that a professional accountant’s

responsibility is not exclusively to satisfy the needs of an individual client or

employer. Serving two masters is likely to cause a few ethical dilemmas. This CPD

serves to provide the Professional Accountant (SA) with a practical guide that will

alert them to possible conflicts of interest and make them mindful of their required

duty of care as a professional accountant.

3

Videos to check out

https://www.youtube.com/watch?v=i9l4vm-ziJo -

inspirational

Articles to read:

http://www.saipa.co.za/page/416470/accounting-ethics-

%E2%80%93-threats-and-safeguards

2 IESBA Handbook of the Code of Ethics for Professional Accountants, 2016 Edition, page 4 3 https://za.pinterest.com/janroberg/tax-stuff/, accessed on 3 February 2017

CP04 - V1 Page 5 of 41

CP04 - V1 Page 6 of 41

Five Key elements of the code

Relevant sections of the code:

Part A – 100.1, 100.8, 100.9

Part C - 300.6, 300.7, 300.13, 300.14, 300.15, 360.1, 360.2, 360.3, 360.4, 360.5, 360.6, 360.7, 360.8,

360.9

These elements can be found in Part A of the code and re-inforce guidelines for

professional accountants to act in the best interest of your client and the public.

Professional accountants are required to adhere to the five fundamental principles. A

professional accountant is therefore required to evaluate the significance of the

threats to compliance with the fundamental principles (section 100.8) by considering

both quantitative and qualitative factors. Where a threat cannot be eliminated,

professional accountants are expected to resign from an engagement or employing

organization (100.9).

IFAC sees the role of the professional accountant as being a beacon of ethics in

every organization. Professional accountants shall not knowingly engage in any

business, occupation, or activity that impairs or might impair integrity, objectivity or

the good reputation of the profession and as a result compromise the fundamental

principles (300.6).

Threats to the fundamental principles are set out in section 300.7.

List the threats:

_______________________

_______________________

_______________________

_______________________

_______________________

The safeguards to these threats can be found in 300.13 and 300.14 which include

those created by the profession, legislation/regulation and the work environment.

Where a professional accountant believes that unethical behaviour will continue he

may seek legal advice and if the situation cannot be remedied, he may conclude that

it is appropriate to resign from the contract (300.15).

NOTES:

CP04 - V1 Page 7 of 41

CP04 - V1 Page 8 of 41

2.1.1 Integrity

“be straightforward and honest in all professional and business relationships”

Relevant sections of the code:

Part A – 110.1, 110.2, 110.3

Part C - 320.3

Professional Accountants are relied upon for the preparation and reporting of

financial information, providing effective financial management and competent

advice. When you provide these services, you do so in the capacity of a reasonable

professional accountant. There will be times when you need to be brave and give

the bad news. You may not always be liked by your clients, but they have instructed

you to provide a service and as such, they need to know that you have applied your

mind and have taken due care in their best

interests.

4To avoid miscommunication ensure that

your mandate has been reduced to writing.

Clients immediately revert to the defensive

when asked to sign a contract and start

calculating what an attorney will cost them

to peruse the lengthy document you have

just presented to them. They often refuse

to sign the agreement arguing that you are

costing them.

A contract or letter of engagement may

scare clients. . The purpose of the written document is to protect your clients as

much as it protects you. If everyone is on the same page, it reduces negligence

claims.

The confirmation of your mandate in writing, indicates that you are a person of your

word and that you have no problem being held to account and that you will carry out

your functions ethically as directed by the engagement letter.

There are general rules that must be followed in order to ensure that you are

covered for a legally binding contract. These include:

Consensus between the parties

Performance must be possible

There must be a clear exchange (of goods or services for a confirmed fee)

The agreement must be enforceable by law

Offer and acceptance

4 http://www.truthliesdeceptioncoverups.info/2013/06/quotes-integrity-and-honor.html, accessed on 2 February 2017

CP04 - V1 Page 9 of 41

There are however clauses that must be included when a professional accountant

takes on specific functions. These are not listed in the IESBA but in the accounting

standards, namely ISRS 4400, ISRS 4410 and ISRE 2400.

1. Compilation engagement (ISRS 4410)

Ask yourself, “Am I being relied upon, for professional services, to provide a

report that may be relied upon in accordance with the accounting standards?”

If the answer is yes, then ensure that your contract has the following inclusions:

It must state the clear purpose and objective of the engagement

Your client’s or employer’s responsibilities must be stated

It must confirm any exclusions to the work agreed upon

There must be a clear reporting line

It must state who may rely on the statements

2. Agreed Upon Procedures Engagement (ISRS 4400)

Agreed upon procedures engagements is a factual findings report for specified

users where no assurance is provided or opinion is expressed.

Separate letter for each engagement

Nature and purpose of the task

It must state who may rely on the reports

Format of the report

Procedure to be followed

The financial information required

3. Review Engagement (ISRS 2400)

Review by an independent professional to express an opinion that the financial

statements, in all material aspects in compliance with the accounting framework

(and to provide negative assurance if required).

The reviewer must assess financial statement risk through the application of

professional judgement/scepticism, analytical procedures and inquiry in order to

obtain evidence for items which were identified to have material risks.

Ensure that your contract has the following inclusions:

It must state the clear purpose and objective of the engagement

Both parties responsibilities must be clearly noted

It must confirm any restrictions on the mandate

There must be a clear reporting line

It must state who may rely on the statements

CP04 - V1 Page 10 of 41

Honesty vs Integrity

There is a difference between integrity and honesty. You

need honesty to have integrity but honestly alone does not

mean that you have integrity.

To be honest requires that you do not to tell lie. A

professional accountant will not advertise for work that he

has no competency to perform. This won’t only have you

facing the disciplinary committee, but you could face

litigation and in the case of SARS, a fine or possible jail

time.

Integrity is a quality that, if tested, proves that you can be

trusted. By following through with an instruction, you have

not just satisfied your client’s need, you have proved that

you are a professional. Clients want to know that they are

paying for professional services. Letters of engagement

provide assurance and assists you in maintaining

reasonable expectations.

Providing assurance

Due care must be exercised when preparing and reporting

on information. You may not be an auditor, but the

information you provide as a professional accountant will

be relied upon and the assumption taken by those who

read your reports is one of an implied assurance (ISRS

4410). Reasonable steps must be taken to maintain the

information that you are responsible for.

Professional accountants are required to clearly describe

the true nature of the business transactions, assets, or

liabilities; classify and record information in a timely and

proper manner; and represent the facts accurately and

completely in all material aspects (Section 320.3). It is imperative that you hold your

independence and are not swayed by intimidation. Your integrity will be questioned

if you are associated with misleading information. Be straight-forward and honest in

all professional relationships. It is important for you to take steps to disassociate

yourself from misleading information.5

5 For further information refer to Section 320, “Preparation and Reporting of Information”, IESBA Code of Ethics 2016.

To protect yourself against

possible negligence claims

it would serve you well to

email your client

confirmation the mandate

they have given you. That

way you have a record of

the interaction between

yourself and your client.

Remember to enable a read

receipt)

If you find yourself trapped

as an employee and

pressured to report

information in a misleading

way, notify HR, your

manager or the audit

committee responsible for

governance. Insist on a

whistle blowing hotline

facilitated by an external

vendor.

CP04 - V1 Page 11 of 41

In summary, Section 110.2 confirms that a professional accountant should not,

knowingly, be associated with information that is materially false; contains

information furnished recklessly; or information that is obscured and contains

omissions.

Videos to check out

https://www.youtube.com/watch?v=Ps6-3zyXWus - motivational

https://www.youtube.com/watch?v=lacwpfPk_HE - inspirational

https://www.youtube.com/watch?v=P4z-2wGkQdo

NOTES:

Preparation and compilation of

financial statements (ISRS 4410)

Review

(ISRS 2400)

Audits

Non-assurance Services

Reasonable Assurance

Moderate Assurance

Level of

cre

dib

ility

Assura

nce t

hro

ugh the

expre

ssio

n o

f an o

pin

ion

CP04 - V1 Page 12 of 41

CP04 - V1 Page 13 of 41

2.1.2 Objectivity

“to not allow bias, conflict of interest or undue influence of others to

override professional and business judgments.”

Relevant sections of the code:

Part A - 120

Part C - 300.2, 300.4, 310.1, 310.2, 310.8, 310.9, 310.10, 320.3, 340

This principle requires that a professional accountant never waivers on their

professional judgment. Bias, conflict of interest and undue influence are factors to

take heed of when assessing if your objectivity has been compromised.

Any conflict of interest is a threat to the principle of objectivity and a professional

accountant shall not allow a conflict of interest to compromise professional or

business judgment 310.1. Examples of situations that may arise can be found in

Section 310.2.

Before accepting a new client relationship reasonable steps must be taken to identify

possible conflicts of interests with existing clients in respect of the nature of the

interests and the relationship between the parties and the nature of the service and

its implication for the relevant parties (310.6) must be considered.

List the safeguard to consider to eliminate threats (_____):

Where required, consent must be obtained from your client or employer to reduce

the threat of a conflict of interest. Consent may be implied, but a professional

accountant must have sufficient evidence to deduce and confirm that no objection

will be taken later (310.9). You are encouraged to reduce everything to writing even

if the disclosure is made verbally (310.10).

CP04 - V1 Page 14 of 41

Section 340 refers to situations which could compromise your objectivity as a

professional accountant and include, having shares in a company that you are an

employee of; receiving a profit-related bonus; or where a close family relative has

interests in a business where you are the accounting officer.

You are required to be conscious of any pressure from peers or employers and self-

interest threats that can diminish your ability to remain objective. To avoid losing

your designation, you must remain resolute in your principles and the code of ethics

by ensuring that you do not use confidential information for personal gain.

When faced with inducements by family or close friends, the professional accountant

must evaluate the situation. These may come in the form of preferential treatment,

hospitality, gifts or inappropriate appeals. The nature and intent must be considered

and if the conduct is determined not to be unethical and only business as usual, then

there is no significant threat. If the evaluation confirms that the threat is significant,

safeguards must be established.

What actions can be taken to mitigate against possible threats:

If a professional accountant is expected to offer inducements to influence the

decision-making process, whether the pressure is internal or external, he must follow

the ethical conflict resolution as contained in sections 100.19 to 100.25 of Part A of

the code.

A professional accountant shall not offer an inducement to improperly influence

professional judgment of a third party. Where a matter involves a conflict with your

client or employer, the professional accountant must consult with those responsible

for governance such as the board or audit committee.6

6 100.21

CP04 - V1 Page 15 of 41

Self assessment

Susan is a professional accountant for a SMME, George’s Construction. Susan

requests records to support the payables and receivables but George, the owner,

never has time to provide the information to Susan. George suggests that Susan

refer to the numbers available on pastel. What should Susan do?

Videos to check out

https://www.youtube.com/watch?v=Ps6-3zyXWus - motivational

Notes:

CP04 - V1 Page 16 of 41

2.1.3 Professional Competence and Due Care (Section 130)

to maintain professional knowledge and skill at a level required to ensure that

a client or employer receives competent professional service based on current

developments in practice, legislation and techniques and act diligently and in

accordance with the applicable technical and professional standards.

Relevant sections of the code:

Part A – 130.1, 130.2, 130.3, 130.4, 130.4, 130.5, 130.6

Part C – 330.1, 330.2, 330.3, 330.4

There is a requirement that a professional accountant attain the necessary

competence and act diligently in discharging his assignment. He must maintain his

professional and technical knowledge through Continuous Professional Development

(CPD) and ensure that his professional staff have the appropriate training and

supervision.

A professional accountant may not mislead his employer or client as to his level of

expertise or experience.7 Where appropriate, clients/employers must be notified of

any inherent limitations that the professional accountant may have.8

There are identified threats are listed in section 330.2 as:

Insufficient time to complete the relevant duties

Incomplete, restricted or inadequate information for performing the duties

properly

Insufficient experience, training and education

Inadequate resources for proper performance

List the safeguards (_____):

7 330.1 8 130.1 – 130.6

Where a professional

accountant cannot

eliminate a threat or

reduce it to an acceptable

level, he must determine

if refusing is appropriate

and clear reasons must

be communicated to the

client or employer

(Section 330.4)

CP04 - V1 Page 17 of 41

Videos to check out

The Office: Accounting web episodes

Notes:

CP04 - V1 Page 18 of 41

2.1.4 Confidentiality (Section 140)

to respect the confidentiality of information acquired as a result of

professional and business relationships and, therefore not disclose any such

information to third parties without proper and specific authority, unless there

is a legal or professional right or duty to disclose, nor use the information for

the personal advantage of the professional accountant or third parties.

Relevant sections of the code:

Part A – 140.1, 140.2 140.3, 140.4

Part C -

Confidentiality is important for many reasons. The inability to properly secure and

protect confidential information can lead to the loss of clients and diminish the

integrity of the professional accountant.

Confidential information that lands in the wrong hands, can be used to confer

unlawful movement (e.g. extortion or segregation), which can in turn may result in

expensive litigation.

Section 140 notes that a professional accountant has an obligation to refrain from

disclosing confidential information without proper and specific authority unless there

is a legal or professional right or duty to disclose. Furthermore, the professional

accountant my not use the confidential information to their personal advantage or the

advantage of third parties9. Professional accountants are in a unique position to

know about fraud and misconduct and have the technical competence to recognise

and report it. Even if in a social context, the confidentially principle must remain in-

tact.

It is required that reasonable steps be taken to ensure that the staff of the

professional accountant respect the duty his obligation to uphold confidentiality.

A professional accountant is expected to comply with this principle beyond the

relationship with his client or employer.10

9 140.1 10 140.6

The Protection of Personal Information Act (POPI), places a burden on any

person who is in possession of the personal information of another:

To have the requisite authority to be in possession of the information.

To protect the information from further distribution

To notify relevant persons of a breach of their personal information

Harsh penalties of up to 10 million or imprisonment up to 10 years await those

who breach the provisions of the act.

CP04 - V1 Page 19 of 41

11

When is the disclosure of confidential information required?

a.

b.

c.

Videos to check out

https://www.youtube.com/watch?v=_ITU377uuJY – secure your

information

https://www.youtube.com/watch?v=Gz2JNm7ubUU

Notes:

11 Act 4 of 2013

CP04 - V1 Page 20 of 41

2.1.5 Professional Behaviour (Section 150)

to comply with relevant laws and regulations and avoid any action

that discredits the profession.

Relevant sections of the code:

Part A – 150.1 and 150.2

Part C - 300.5

The principle of professional behaviour imposes an obligation on professional

accountants to comply with relevant laws and regulations and to avoid any action

that may bring discredit to the profession. This includes actions which a reasonable

and informed third party, having knowledge of all relevant information, would

conclude negatively affects the good reputation of the profession (150.1).

In terms of the SAIPA code of conduct, professional behaviour means that members

should act in a manner consistent with the good reputation of the Institute and the

accounting profession, refraining from any conduct that might bring the Institute

and/or the accounting profession into disrepute (150.2). Members should conduct

themselves professionally with due consideration towards clients, third parties, other

members of the accountancy profession, staff, employers and the general public.

Professional Accountants should be honest and not:

(a)

(b)

What does it mean to be a professional Accountant (SA)12

I am capable of managing my own work;

I am responsible for the quality of the work I perform;

I am able to exercises professional judgement; and

I am capable of leading a team and managing functions adapted to my skill

set.

The more senior your position, the greater your ability and opportunity to influence

events, practices and attitudes. You are therefore expected to encourage an ethics-

based culture (300.5).

12 Issue 28, Professional Accountant (SA) Official Journal

CP04 - V1 Page 21 of 41

Self assessment

Robert is a Professional Accountant (SA) and a registered tax practitioner on the

SAIPA RCB list. His letter of engagement notes that he will perform various

functions for his client Peter, including his tax returns. During tax season, Robert’s

business starts thriving and he takes on more work than he can handle. Robert

neglects his responsibility to Peter who incurs a penalty from SARS. Peter is furious

and immediately demands his e-profile. Robert refuses to transfer the e-profile as

Peter still has an outstanding amount for the management accounts that were done.

a. Discuss the fundamental principles that were breached.

b. What should Robert have done?

Videos to check out

https://www.youtube.com/watch?v=14bCsM16bYo&t=8s

https://www.youtube.com/watch?v=pmVF23QXY10 – dealing with

difficult people

Notes:

CP04 - V1 Page 22 of 41

3. Significant amendment to the code

Relevant sections of the code:

Part C - 360.1 – 360.37

The additional sections discuss the manner in which a professional accountant

should respond to non-compliance with laws and regulations.

Section 360

This section sets out a framework to guide professional accountants in what actions

to take in the public interest when they become aware of a potential illegal act,

known as non-compliance with laws and regulations (NOCLAR) by clients and

employers.

a. If you become aware of non-compliance or suspected non-compliance with

the laws and regulations, in the course of carrying out your professional

activities, you are expected to13:

b. The definition of non-compliance includes acts of omission or commission,

intentional or unintentional, committed by your client or employer which are

contrary to the prevailing laws (360.2)

c. The laws must have a direct effect on the determination material amounts and

disclosures in your clients or employers financial statements.

d. Where the laws have no direct effect, but compliance may be fundamental to

the operation of the business, why should a professional accountant still

ensure compliance?14

e. List the objectives of the professional accountant in responding to non-

compliance:

13 360.1 14 350.5, 360.7

CP04 - V1 Page 23 of 41

f. The responsibility of those entrusted with governance is to ensure that

business activities are conducted in accordance with laws and regulations.15

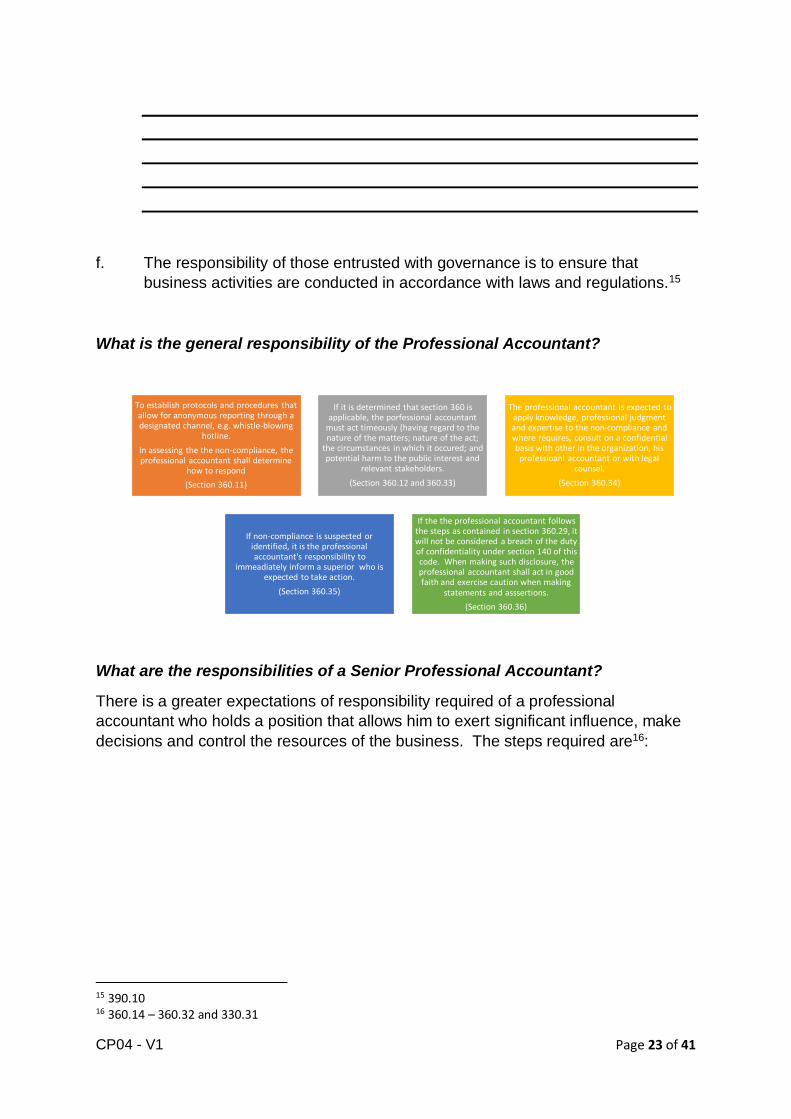

What is the general responsibility of the Professional Accountant?

What are the responsibilities of a Senior Professional Accountant?

There is a greater expectations of responsibility required of a professional

accountant who holds a position that allows him to exert significant influence, make

decisions and control the resources of the business. The steps required are16:

15 390.10 16 360.14 – 360.32 and 330.31

To establish protocols and procedures that allow for anonymous reporting through a designated channel, e.g. whistle-blowing

hotline.

In assessing the the non-compliance, the professional accountant shall determine

how to respond

(Section 360.11)

If it is determined that section 360 is applicable, the porfessional accountant

must act timeously (having regard to the nature of the matters; nature of the act;

the circumstances in which it occured; and potential harm to the public interest and

relevant stakeholders.

(Section 360.12 and 360.33)

The professional accountant is expected to apply knowledge, professional judgment and expertise to the non-compliance and where requires, consult on a confidential basis with other in the organization, his professioanl accountant or with legal

counsel.

(Section 360.34)

If non-compliance is suspected or identified, it is the professional accountant's responsibility to

immeadiately inform a superior who is expected to take action.

(Section 360.35)

If the the professional accountant follows the steps as contained in section 360.29, it will not be considered a breach of the duty of confidentiality under section 140 of this code. When making such disclosure, the professional accountant shall act in good faith and exercise caution when making

statements and asssertions.

(Section 360.36)

CP04 - V1 Page 24 of 41

Section 360.32 and 360.37 notes that where there is an identified or suspected act of

non-compliance, the professional accountant is encouraged to document the

following:

The matter;

The results of discussions with the professional accountant’s superior,

management and, where applicable, those charged with governance and

other parties;

How the professional accountant’s superior has responded to the matter;

The courses of action the professional accountant considered, the judgments

made and the decisions that were taken.

How the professional accountant is satisfied that he has fulfilled the

responsibility of disclosing to those in charge of governance and his

determination of any further action required in the public interest.

To determine is further action is required, the nature and extent of it, will depend on

the following factors17:

17 360.22

Obtaining an understanding of

the matter

•The nature of the act

•The application of the relevant laws and regulations

•Potential consequence to stakeholders and the public interest

•exercising knowledge, professional judgment and expertise required of a professional accountant to investigate any non-compliance and to consult, on a confirdential basis, with others within the organization, professioanl body or with legal counsel

Addressing the matter

•By notifying their immediate superior and if necessary the next level of authority

•Appropriate steps must be taken as noted in 360.17

•Disclosure may be required to the external auditor if there is a legal obligation to enable the suditor to perfom his audit

Determining whether further action is needed

•To assess the appropriateness of the response to those in charge of governance

• In assessing the response, consider if it is timely, if the appropriate action was taken to rectify, remedy or mitigate the consequence of non-compliance.

Documentation

•The senior professional accountant must document the investgation of the matter and the recourse taken.

CP04 - V1 Page 25 of 41

What further action may be taken?18

In determining if the appropriate action was taken one must consider if a reasonably

informed third party, weighing all the specific fact and circumstances available to the

professional accountant at the time, would be likely to conclude that the professional

accountant has acted appropriately in the public interest.19

4. Identifying reportable irregularities in terms of South African Law

In some jurisdictions, such as South Africa, there are specific regulations that govern

how to address the non-compliance. When encountering non-compliance, a

professional accountant has the responsibility to20:

One such example is that of section 29 of the Companies Act which states:

Independent Reviewers need to be aware of the definition of a Reportable

Irregularity in terms of the regulations in order to comply with the reporting

obligations placed on them.

18 360.25 19 360.24 20 360.3

CP04 - V1 Page 26 of 41

Regulation 29(1) (b) of the Companies Act defines a reportable irregularity (RI) as

follows:

"Any act or omission committed by any person responsible for the management of a

company, which

1. unlawfully has caused or is likely to cause material financial loss to the

company or to any member, shareholder, creditor or investor of the company

in respect of his, her or its dealings with that entity; or

2. is fraudulent or amounts to theft; or

3. Causes or has caused the company to trade under insolvent circumstances.”

Who should a member report to?

A member who identifies a reportable irregularity in terms of Regulation 29 of the

Companies Act, must report directly to the Companies and Intellectual Property

Commission (CIPC).

The member must ensure that irregularities identified are recorded immediately and

are in detail enough to allow CIPC to check whether there is any evidence of same.

Members who send first reports need to follow up with the second report as per

section 29(8) (c).

During February 2016 the CIPC raised concerns that the Independent Reviewers

were not following through with the first reports they provided.

The Process as per the Regulation 29(8):

1. The independent reviewer must as soon as reasonably possible but not later

than 20 business days from the date on which the report referred to in sub

regulation (6) was sent to the Commission—

(a) take all reasonable measures to discuss the report referred to in sub-

regulation (6) with the members of the board of the company;

(b) afford the members of the board of the company an opportunity to make

representations in respect of the report; and

(c) send another report to the Commission, which report must include—

(i) a statement that the independent reviewer is of the opinion that—

(aa) no reportable irregularity has taken place or is taking place; or

(bb) the suspected reportable irregularity is no longer taking place

and that adequate steps have been taken for the prevention or

recovery of any loss as a result thereof, if relevant; or

(cc) the reportable irregularity is continuing; and

CP04 - V1 Page 27 of 41

(ii) detailed particulars and information supporting the statement referred

to in subparagraph (i)

Was the matter disclosed to the appropriate authority?

Disclosure must wither be required by law or if the professional accountant thought it

necessary for investigation by the appropriate authority in the public interest.21

In determining the nature and extent of the actual or potential harm, due

consideration must be taken of the relevant stakeholders. Examples of situations

that may determine if disclosure is appropriate can be found in section 360.29.

List the external factors to consider before making a disclosure:

5. Touch, pause, engage

Relevant sections of the code:

Part A – 100.9, 100.19, 100.20, 100.24

Part C – 310.3

By IFAC standards, professional accountants are required to identify, evaluate and

address each matter requiring their skills, so as to act in a diligent manner with

professional competence. You are also required to resolve conflict in compliance to

the fundamental principles.22 If your evaluation of the situation does not yield an

acceptable level, it is important that you put into place safeguards in place to

eliminate or mitigate against the threat.

21 360.28 22 100.19

CP04 - V1 Page 28 of 41

Being aware of your responsibilities and the consequence of your advice, makes you

a better professional. Your knowledge and skills have been developed for the

duration of your studies and articles, but to place yourself in the category of a

professional, you must understand how to conduct yourself in a manner that will not

just blemish your name or tarnish the reputation of your entire fraternity.

To determine if there is a compromise of the fundamental principles, use the

following test23:

Qualitative and quantitative measures must be considered when evaluating the

significance of the threat.

When initiating the conflict resolution process, what factors must be considered?24

You must now weigh the consequences for each likely course of action and

determine the appropriate way forward.

Where a threat cannot be eliminated, professional accountants are expected to

decline or discontinue the professional activity and where necessary resign from the

engagement or employing organization (100.9).

After exhausting all relevant possibilities, if the ethical conflict remains resolved, a

professional accountant shall refuse to remain associated with the matter causing

the conflict (100.24).

23 310.3 24 100.20

Would a reasonable and informed professional

accountant perform in the same manner

Weigh all the facts and circumstances

conclude that compliance to the

fundamental principles are compromised

CP04 - V1 Page 29 of 41

25

25 http://tigerhawk.blogspot.co.za/2008/06/old-school-accounting.html accessed on 2 March 2017

Ensure that you

have documented

the substance of the

issue, details of the

discussion held, and

the decisions made

concerning the issue

(Section 100.22)

CP04 - V1 Page 30 of 41

6. Case study

THE CASE STUDY THAT FOLLOWS HAS BEEN EXTRACTED FROM THE GUIDE TO QUALITY CONTROL FOR

SMALL-AND MEDIUM-SIZED PRACTICES, THIRD EDITION, PRODUCED BY IFAC.26 CANDIDATES ARE

REQUIRED TO SIT IN GROUPS TO DISCUSS THE EFFECT OF THE ACTIONS ON THE FUNDAMENTAL

PRINCIPLES AND ELABORATE ON SAFEGUARDS TO THREATS AND POSSIBLE MITIGATION.

M.M. and Associates

General

Marcel Mooney is a sole practitioner, practicing as M.M. and Associates and

employing four staff. The practice performs a large number of review

engagements (some of which are on behalf of family members or close

personal friends), several small audits, and three medium-sized audits. The

more substantial audit clients include a retirement home, a local

government agency, and the largest motorcycle dealership in town. The

local government agency has had a lot of negative publicity lately with

allegations of corruption against senior managers. Marcel has known the

managers for many years and feels these charges are unfounded. The

retirement home is almost a year behind in payment of its fees for last

year’s audit, and the firm needs to begin scheduling the field work soon.

Marcel, 48, started his practice in 1990 with no staff. The firm has grown

gradually over the last 18 years. Marcel is a dynamic individual and keeps

life around the office interesting. If something looks like fun, Marcel is

usually in the middle of it. He is an excellent marketer and promotes the

firm wherever he goes. Marcel earns a good living, and has no plans to

retire. M.M. employs Deborah D’Alessandro, who has three years of

experience with the firm and hopes to qualify as a professional accountant

next year; an accounting technician, Bob Morton; and two students

recently enrolled in a program of professional accounting studies, who are

new to the firm. Bob has one year of experience and started with the firm

four months ago. His enthusiasm makes up for his lack of experience.

Deborah is constantly reminding Bob to ask the client more questions and

to document more completely. In several cases, Bob has missed key

26 This publication may be downloaded free of charge from the Publications and Resources area of the IFAC website: http://web.ifac.org/publications.

CP04 - V1 Page 31 of 41

matters in the file and Deborah has had to go back to the client and obtain

further information.

Marcel, like many other practitioners, is always reluctant to turn down new

clients, sometimes even those with poor reputations. He feels everyone has

a right to professional services. Recently Marcel took on Mark Spitzer as an

audit client. Mark owns the local restaurant, which has ties to community

members with questionable reputations. Mark also has a history of

problems with tax authorities resulting in fines, penalties, and, in one case,

a suspended jail sentence. Deborah is not looking forward to the audit and

the working environment she’ll have to endure to get the work done.

Despite the firm’s smaller size, and Marcel’s somewhat casual attitude towards

policy development, the firm has no history of complaints or allegations, and a

majority of the clients would report they are satisfied with the firm’s service.

Firm Planning Process

The firm’s planning process consists of a day spent by Marcel reflecting on

the past year and the preparation of a simple budget. The budget is

usually last year’s numbers adjusted for known client gains and losses. It

also addresses capital requirements, staffing costs, and office expenses.

Since the competitors in town seem to be performing fewer audit and

review engagements, Marcel sees this as an opportunity to increase his

share of the assurance market. He has thought about registering with the

regulatory body in order to be able to conduct listed entity audits. Marcel

normally discusses his firm’s revenue plan with Deborah and together they

plan staffing and other resources such as identifying equipment and

furniture requirements for the next year.

Human Resources

The hiring process is informal. When one of the staff members announces that

he or she is leaving the firm, Marcel may place an advertisement in the local

newspaper or review the resumes recently received from people looking for

positions. When a candidate is found, Marcel interviews this individual and then

makes a decision. Marcel tries to check out the references or qualifications of

candidates, but sometimes he does not complete the process owing to the

pressures of client meetings and engagements. Deborah assists Marcel with

staff scheduling when a time conflict arises and finds work for staff that are not

busy.

Since junior staff never seem to stay with the firm very long, Marcel is reluctant

to spend time and money training them. Besides, he believes “on the job”

CP04 - V1 Page 32 of 41

training is the best training. Furthermore, he does not often conduct

performance appraisals, and retains only brief notes on file for any of the

personnel, with the exception of statutory personal information required to

prepare the necessary annual income reporting slips.

Professional Standards

Marcel is concerned about the new independence rules. He fears they

may prevent him from performing some assurance engagements. For

example, when Deborah questioned the firm’s independence on a new

audit client, Magnificent Dollar Stores (a business owned in part by

Marcel’s sister-in-law), he responded “I hardly know the woman. There’s

no threat.”

Marcel spends his time managing or attracting clients, so he has not kept

up -to- date with the new professional standards as much as he would like.

He feels the new standards are too complicated and time-consuming for

working practitioners and their clients to understand. He barely has time to

keep up with all of the tax changes. Marcel relies heavily on Deborah to

ensure the engagement files meet professional standards.

Marcel resists leading-edge technology, but after some pressure he recently

purchased notebook computers for Deborah and Bob, who wanted to start

using electronic working paper software. The students share a desktop

computer. Marcel has considered becoming a member of a local group of small

firms who provide training on new standards, but hasn’t yet had time to contact

the group and investigate the advantages and costs associated with joining the

affiliation.

As a result of comments received during the last practice inspection two

years ago, M.M. purchased a subscription to certain resource library

materials, including an audit and review manual which includes examples of

standardized templates. Despite the negative comments Marcel’s attitude

towards practice inspection is just to obtain ‘a passing grade’ without having

to engage in additional procedures that he feels will only consume the limited

time available to his personnel that don’t result in fee generation for the firm.

Planning and File Reviews

Since Marcel knows his clients well, he feels that planning meetings are rarely

needed. The approach used most commonly in the firm is simply to do

CP04 - V1 Page 33 of 41

whatever was done last year. Marcel performs his own file reviews.

Engagement personnel are briefed by Marcel before beginning field work.

Engagement letters are obtained, but for existing clients this is usually done

after the engagement is complete. Standard templates are used most of the

time. Staff is expected to do their best to complete the file and then hand it in

for review. Deborah reviews her own work, and Bob’s and the students’ work,

before giving the file to Marcel to sign off. Marcel is not naturally inclined

towards the patient work of reviewing files and gets frustrated when there is

too much paper in the file. He would like to spend time doing careful reviews,

but sometimes the amount of paper the employees put in the file makes this

too time-consuming.

After Marcel heard about the new quality control standards, he asked Deborah

to study them and report back to him with recommendations about what the

firm should do. The one condition he gave her was that the changes should be

kept to the minimum required because compliance rules tend to cut into

billable hours. Deborah feels uncomfortable with this approach. She also

knows that the firm has no formal process for determining if, and when, an

engagement quality control review should be completed on a file, but she is

aware that this forms only one component of the standards requirements.

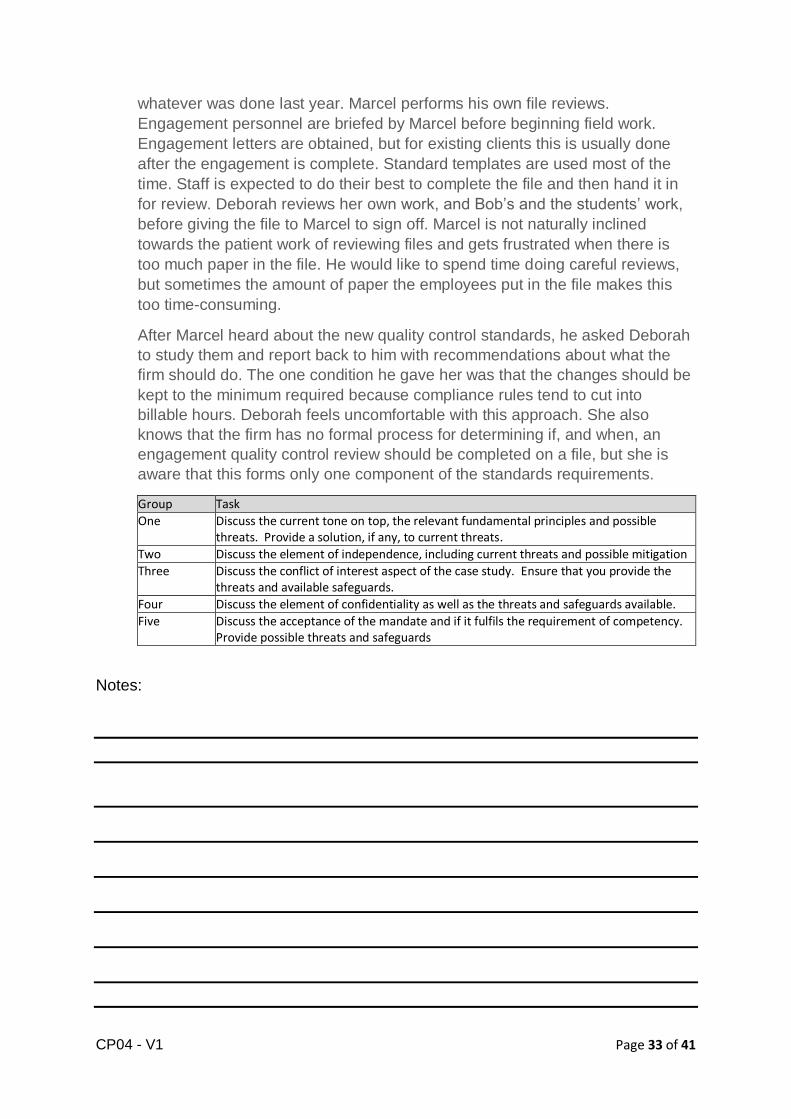

Group Task

One Discuss the current tone on top, the relevant fundamental principles and possible threats. Provide a solution, if any, to current threats.

Two Discuss the element of independence, including current threats and possible mitigation

Three Discuss the conflict of interest aspect of the case study. Ensure that you provide the threats and available safeguards.

Four Discuss the element of confidentiality as well as the threats and safeguards available.

Five Discuss the acceptance of the mandate and if it fulfils the requirement of competency. Provide possible threats and safeguards

Notes:

CP04 - V1 Page 34 of 41

CP04 - V1 Page 35 of 41

CP04 - V1 Page 36 of 41

5. Awareness of my duties

Relevant sections of the code:

Part A – 100.9, 100.19, 100.24

Part C – 310.3

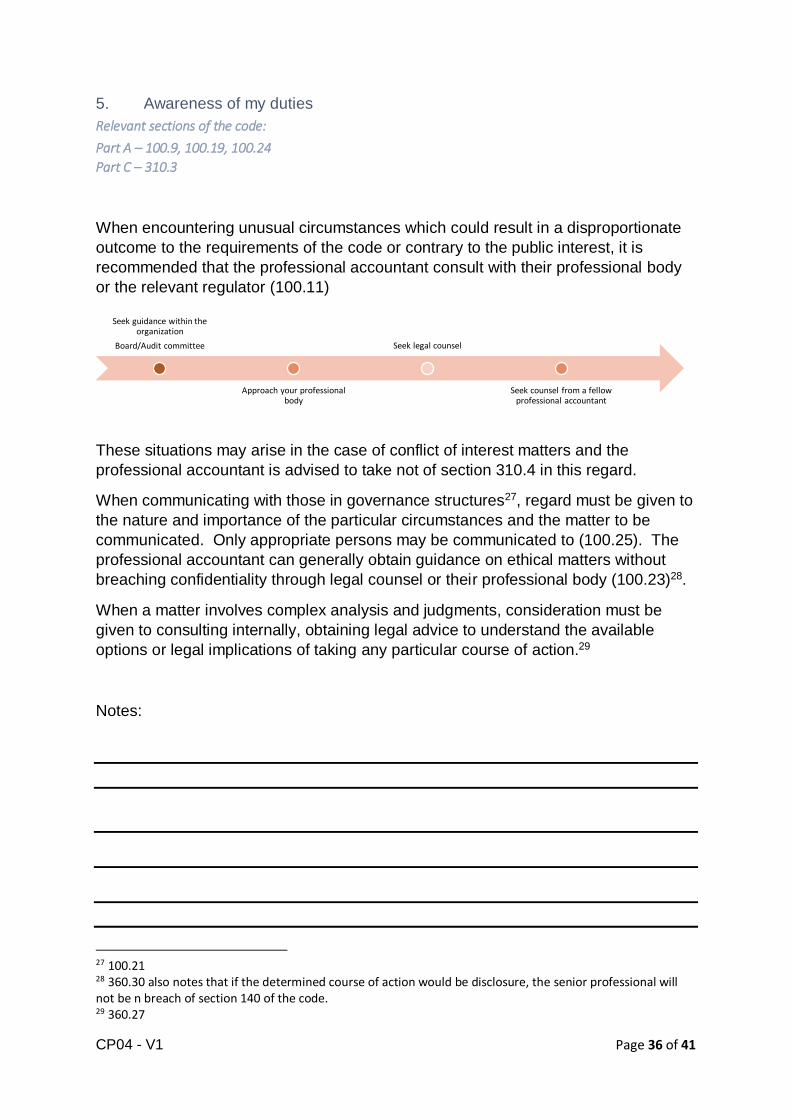

When encountering unusual circumstances which could result in a disproportionate

outcome to the requirements of the code or contrary to the public interest, it is

recommended that the professional accountant consult with their professional body

or the relevant regulator (100.11)

These situations may arise in the case of conflict of interest matters and the

professional accountant is advised to take not of section 310.4 in this regard.

When communicating with those in governance structures27, regard must be given to

the nature and importance of the particular circumstances and the matter to be

communicated. Only appropriate persons may be communicated to (100.25). The

professional accountant can generally obtain guidance on ethical matters without

breaching confidentiality through legal counsel or their professional body (100.23)28.

When a matter involves complex analysis and judgments, consideration must be

given to consulting internally, obtaining legal advice to understand the available

options or legal implications of taking any particular course of action.29

Notes:

27 100.21 28 360.30 also notes that if the determined course of action would be disclosure, the senior professional will not be n breach of section 140 of the code. 29 360.27

Seek guidance within the organization

Board/Audit committee

Approach your professional body

Seek legal counsel

Seek counsel from a fellow professional accountant

CP04 - V1 Page 37 of 41

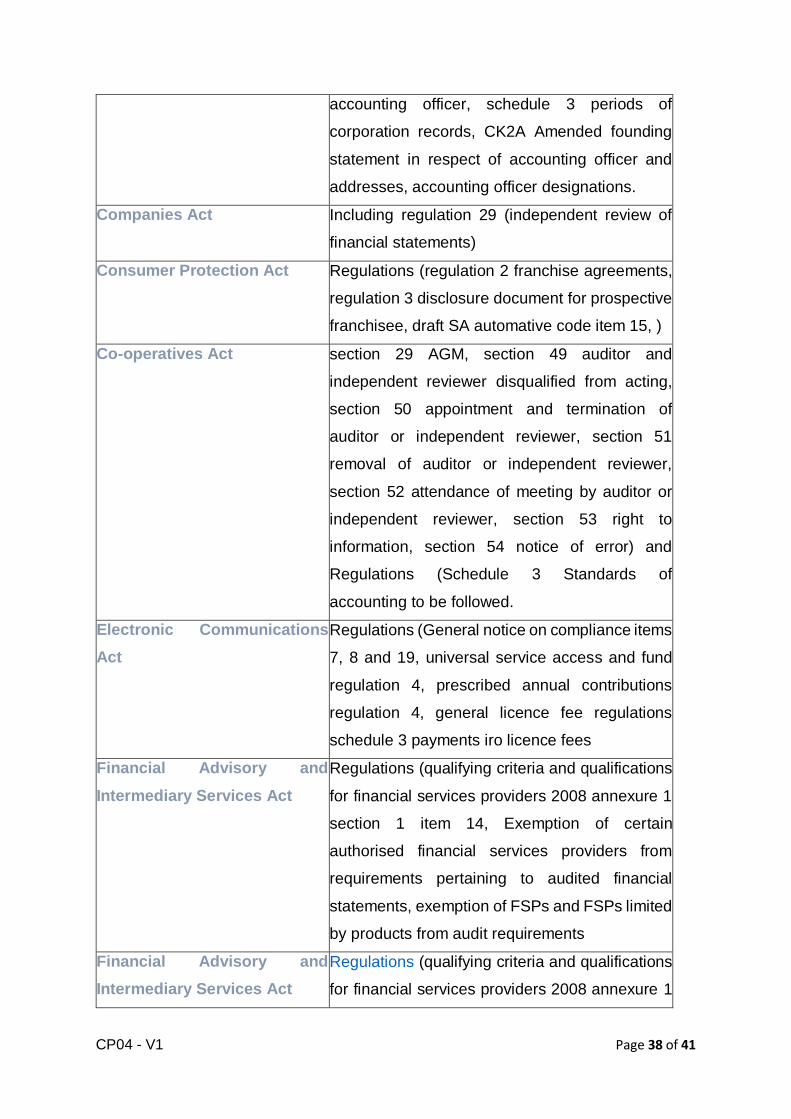

6. Legislative requirements

Cognisance must be taken of relevant legislation. We note the following list of

legislation that are applicable to Accounting Officers or Tax Practitioners:

Accounting officer references

Banks Act section 85 certification of returns and other

documents and Regulation 4 – certification of

returns

Bills of Exchange Act section 72B prevention of fraud

Broad-Based Black Economic

Empowerment Act

Including regulations framework for accreditation

and verification by all verification agencies

appendix 6 item 5.4.9.9. Current validity

questionable; Draft BBBEE Forest Code 0000

item 4.7 Current validity questionable; financial

sector code 000 item 4.5; agriculture code item

2.6)

Close Corporations Act section 12 founding statement, section 15

registration of amended founding statement,

section 58 annual financial statements, section

59 appointment of accounting officers, section 60

qualifications of accounting officers, section 61

right of access and remuneration of accounting

officers, section 62 duties of accounting officers,

section 63 joint liability for debts of corporation,

section 66 application of the Companies Act,

section 73 repayments, payments of damages

and restoration of property by members and

others) and Regulations (regulation 15

registration of founding statement, regulation 16

registration of amended founding statement,

regulation 16A annual return, regulation 21

accounting officer, regulation 21A reporting by

CP04 - V1 Page 38 of 41

accounting officer, schedule 3 periods of

corporation records, CK2A Amended founding

statement in respect of accounting officer and

addresses, accounting officer designations.

Companies Act Including regulation 29 (independent review of

financial statements)

Consumer Protection Act Regulations (regulation 2 franchise agreements,

regulation 3 disclosure document for prospective

franchisee, draft SA automative code item 15, )

Co-operatives Act section 29 AGM, section 49 auditor and

independent reviewer disqualified from acting,

section 50 appointment and termination of

auditor or independent reviewer, section 51

removal of auditor or independent reviewer,

section 52 attendance of meeting by auditor or

independent reviewer, section 53 right to

information, section 54 notice of error) and

Regulations (Schedule 3 Standards of

accounting to be followed.

Electronic Communications

Act

Regulations (General notice on compliance items

7, 8 and 19, universal service access and fund

regulation 4, prescribed annual contributions

regulation 4, general licence fee regulations

schedule 3 payments iro licence fees

Financial Advisory and

Intermediary Services Act

Regulations (qualifying criteria and qualifications

for financial services providers 2008 annexure 1

section 1 item 14, Exemption of certain

authorised financial services providers from

requirements pertaining to audited financial

statements, exemption of FSPs and FSPs limited

by products from audit requirements

Financial Advisory and

Intermediary Services Act

Regulations (qualifying criteria and qualifications

for financial services providers 2008 annexure 1

CP04 - V1 Page 39 of 41

section 1 item 14, Exemption of certain

authorised financial services providers from

requirements pertaining to audited financial

statements, exemption of FSPs and FSPs limited

by products from audit requirements)

Financial Services Board Act Regulations (Levies item 12 levies on

intermediaries).

Independent Communications

Authority of South Africa Act

Regulations (compliance procedure manual

regulation form 2)

Inspection of Financial

Institutions Act

section 9 disclosure to certain affected parties.

Act to be replaced by the Financial Sector

Regulation Bill

Justices of the Peace and

Commissioners of Oaths Act

section 7 Powers of commissioners of oaths and

Regulations (designation and manner of oath

Mutual Banks Act

section 43 annual financial statements and

section 86 certification of returns and other

documents

National Credit Act Section 58A additional requirements for

cancellations and regulations 65 (annual

financial statements, 67 (responsibility for

assurance engagements, and form 40D

Non-profit Organisations Act section 17 accounting records and reports and

section 18 duty to provide reports and information

Pension Funds Act regulation 32 application for registration as

administrator

Preferential Procurement

Policy Framework Act

Regulations (2011 regulations, including

regulation 10 Broad-based black economic

empowerment status level certificates, ending 1

April 2017

CP04 - V1 Page 40 of 41

Sectional Titles Act Regulations (Annexure 8 management rule 32

record of rules and their availability, 42 audit, 50

when to be held, 56 AGM)

South African Schools Act section 43 audit or examination of financial

records and statements

Tax practitioner references

Customs and Excise Act Rule 119A customs modernisation

Tax Administration Act section 69 secrecy of taxpayer information and

general disclosure, section 70 disclosure to other

entities, section 229 understatement penalty

percentage table, section 234 criminal offences

relating to non-compliance, and chapter 18

registration of tax practitioners and reporting of

unprofessional conduct) and Regulations

(definition of registered user, and item 4, in rules

for electronic communication).30

7. Holding my ground – tips to achieving success in your practice

Document the substance of any issue that could potentially result in a breach

of the fundamental principles.

Keep evidence where permission was sought and consequently given in a

conflict of interest situation.

Ensure that your letter of engagement contains the necessary clauses.

Whistle-blow internally using the Protected Disclosure Act.

Never withhold an e-profile in order to leverage for outstanding fees.

If your mandate has been terminated, do not inflate the final bill or reverse

discounts (unless they were a mechanism for preferential payments in terms

of your agreement).

30 Table courtesy of the Contemporary Gazette as at February 2017

CP04 - V1 Page 41 of 41

Notes: