dec 2015 - phillipcapitalbackoffice.phillipcapital.in/backoffice/...dec_2015_20151222181803.pdf ·...

TRANSCRIPT

3GROUND VIEW GROUND VIEW Annual Edition 2016 Annual Edition 20162

1st Nov 2015 Issue 7

VOL 2 . ISSUE 8 . 1ST - 31ST DEC 2015

Vineet Bhatnagar- Managing Director and CEO

EDITORIAL BOARDNaveen Kulkarni, Manish Agarwalla, Kinshuk Bharti Tiwari

COVER & MAGAZINE DESIGN Chaitanya Modak, www.inhousedesign.co.in

EDITORRoshan Sony

RESEARCH

Portfolio StrategyAnindya Bhowmik

Technicals Subodh Gupta

Production Manager Ganesh Deorukhkar

Database Manager Deepak Agrawal

Sr. Manager – Equities Support Rosie Ferns

FOR EDITORIAL QUERIES:

PhillipCapital (India) Private Limited No. 1, 18th Floor, Urmi Estate, 95 Ganpatrao Kadam Marg, Lower Parel West, Mumbai 400 013

SALES & DISTRIBUTION Ashvin Patil, Shubhangi Agrawal, Kishor Binwal, Sidharth Agrawal, Bhavin Shah, Varun Kumar, Narayan Mulchandani

CORPORATE COMMUNICATIONS Zarine Damania

Ground View - Previous Issues

1st June 2015 Issue 4

1st Oct 2015 Issue 6

1st July 2015 Issue 5

1st Apr 2015 Issue 3 1st Feb 2015 Issue 2

Banking, NBFCs Manish Agarwalla, Pradeep Agrawal, Paresh Jain

Consumer, Media, Telecom Naveen Kulkarni, Jubil Jain, Manoj Behera

Cement Vaibhav Agarwal

Economics Anjali Verma

Engineering, Capital Goods Jonas Bhutta, Hrishikesh Bhagat

Infrastructure & IT Services Vibhor Singhal, Deepan Kapadia

Logistics, Transportation & Midcap Vikram Suryavanshi

Midcap Amol Rao

Metals & Automobiles Dhawal Doshi, Nitesh Sharma, Yash Doshi

Agri Inputs Gauri Anand

Oil & Gas Sabri Hazarika

Pharmaceuticals Surya Patra, Mehul Sheth

3GROUND VIEW GROUND VIEW Annual Edition 2016 Annual Edition 20162

From the MD

The road is life...Once again, it is time to reflect on the year that has gone by and also the time to

look forward to the New Year with many aspirations and a few apprehensions. The

second Annual Ground View edition peers into ideas, themes and events that will

shape Indian business landscape over the next twelve months.

This year’s edition is very special for a number of reasons. The most important is

that this GV is as experiential an account of India as it can become, especially in an

environment of hearsay. “The road is life,” said Jack Kerouac in his genre defining

work “On the Road” when he described his incessant cross-country travels across

the US, which ended up inspiring an entire nation. Our analysts have been living

out of suitcases for the last two months and have travelled more than 25,000km

across India, covering 15 states that contribute 75% of India’s GDP – all in an en-

deavour to provide a detailed account of what is actually happening on the ground

in India and its ramifications in the year ahead.

The issue presents 14 Ground View stories (themes) across sectors ranging from

agriculture to technology, which our team believes will shape the country’s fortunes

in 2016. We went to the unexplored northeast to understand the nuances of the

cement sector and to evaluate the seriousness of the government’s initiatives to

build that region. Exploring southern India gave us a glimpse of the vagaries of

the evolving consumption trends; not just the predilection of people, but also their

decision-making process in buying gold. In UP, which is fashioning itself as India’s

new growth engine, we were pleasantly surprised to see the concerted efforts of

both central and state governments to develop infrastructure and the rising con-

sumerism in that state. Western India presented mixed trends across agriculture,

consumption, and the rising divide in rural and urban consumption.

Our cover story, India in 2016: Repairs done, now testing growth engines, penned

by analysts Naveen Kulkarni and Anindya Bhowmik is inspired from the various

sector ground views and it is a take on the structural changes in India, which are in

stark contrast to the short-termism of the markets. While this short-termism is not

a menace in itself as it aids price discovery, structural changes take time to deliver

results. I have no doubt that 2016 will be better than 2015 because we are on the

right path and it is only a matter of time when palpable results will be seen.

It has been very satisfying for our team to provide ground-breaking research

through our “Ground View” magazine and I hope that this special edition will help

you to strategize your portfolios.

Wishing everybody a Merry Christmas and a very happy New Year!

Happy investing !

Vineet Bhatnagar

5GROUND VIEW GROUND VIEW Annual Edition 2016 Annual Edition 20164

49. Model Village Jayapur: Joys of adoption By Naveen Kulkarni & Nitesh Sharma

52. AGRICULTURE: Switching crops- Desperate measures needed By Gauri Anand

58. BFSI: Changing trends By Manish Agarwalla, Pradeep Agrawal, Paresh Jain & Deepak Agarwal

64. CEMENT: North-East India- Building the last frontier By Vaibhav Agarwal

7. Cover story: India 2016: Repairs done, now testing growth engines By Naveen Kulkarni & Anindya Bhowmik

27. Case for Indian Equities By Varun Kumar

29. 2015 - Year in charts By Anindya Bhowmik

35: AUTOMOBILES: Price Elasticity and premiumisation co-exist By Dhawal Doshi and Nitesh Sharma

CONTENTS

5GROUND VIEW GROUND VIEW Annual Edition 2016 Annual Edition 20164

120. Specialty Chemicals conference takeaways: By Surya Patra

123. DIVERSIFIED: Mangalore - The Serene Outlier By Amol Rao

129. Innovations: The value of innova-tion:Few examples from India Inc. By Varun Kumar

131. Warren Buffett’s Not so well known skill By Varun Kumar

132. INDIAN ECONOMY – Trend Indicators

134. PHILLIPCAPITAL INDIA COVERAGE UNIVERSE: Valuation Summary

2016EVENTS

98. E-COMMERCE:

The dawn of financial disci-pline in a sunrise sectorBy Manoj Behera

102. CALENDER

103. INFRA-STRUCTURE: Booming Infra-structure in the state of UP

By Vibhor Singhal

110. POWER: UDAY – a new dawn for discoms? By Jonas Bhutta & Hrishikesh Bhagat

88. CONSUMER: The Great Indian Consumer – Feeling the pinch By Naveen Kulkarni & Jubil Jain

CONTENTS

7GROUND VIEW GROUND VIEW Annual Edition 2016 Annual Edition 20166

BY NAVEEN KULKARNI & ANINDYA BHOWMIK

Structural improvements take time to deliver results, but they deliver sustainable growth and take a lot more courage to implement. Even though the PM has not been able to run the government with as much panache as he showed in his election campaign, India has managed to dart back onto a clear recovery path and achieve a healthy growth rate. 2016 will be better than 2015, even with a marginally better GDP growth. Quality of growth will be superior with rising government capital expenditure, stronger discretionary consumption, and green shoots in private investment. A slew of significant reforms have been announced and are in various stages of implementation – GST, Uday, FDI liberalisation, easing of norms for infra developers, and better ease of doing business. While political noise seems to be taking away the focus from core-development issues, it is only a short-term phenomenon, not a permanent dampener. With an agenda of radical centrism, India is better placed to deliver growth – not just vs. emerging economies, but even vs. developed ones. In a global environment marked by stagnant wages and low nominal GDP growth rate, populist quick fixes of a tax cut here, some hike there will only have ephemeral results. On the other hand, with the right brand of politics, India is steaming ahead and will start becoming visible in 2016. PM Modi’s ‘Make in India’ program aims to position India as an alternate destination to China. India saw higher FDI flows in 2015 and this is likely to accelerate. The year will be a good time for stock picking with attractive valuations, especially in core sectors and ones with medium capitalisation. Strong themes this year are likely to include - government spending, urban discretionary spending gaining momentum, persistence of a strong dollar, and bottom-up market.

India 2016:Repairs done, now testinggrowth engines

COVER STORY

7GROUND VIEW GROUND VIEW Annual Edition 2016 Annual Edition 20166

9GROUND VIEW GROUND VIEW Annual Edition 2016 Annual Edition 20168

“Market liquidity is tight” is a com-

mon refrain of traders and small-scale

businessmen across India, but the

four-wheeler market is now buzzing.

Premiumisation trends across India

are robust, but private investment ac-

tivity is sluggish. Rural growth is now

gloomy, but there seems to be just no

stopping the e-tech boom, which gets

bigger every day. Government infra-

structure spending is gathering pace

even as private construction is slow-

ing down. A boom here, a crisis there

– it seems like never before have so

many contrasting Indias been at play

simultaneously.

“We were safe, there was no flooding

in our area,” said Mr Prabhakar Rao,

a resident of Royapettah in Chennai.

“The drainage system of Royapettah

and old Chennai were constructed

during the colonial times. It is much

better than the rest of Chennai,”

he contends. Tamil Nadu, Andhra

Pradesh, and Puducherry, particularly

Chennai were ravaged by torrential

rains from 1st December 2015. Chen-

nai city saw its highest rainfall in the

last 100 years, causing heavy flooding

and loss of life and property. Chen-

nai Corporation, the city’s governing

body was established way back in

1688 – it is the oldest municipal cor-

poration in India and second-oldest

surviving municipal corporation in the

world. Even with so much history, the

city’s infrastructure is inadequate and

is indicative of the opportunities that

lie ahead.

Within India, different themes are

emerging. A leading consumer du-

rables dealer in Coimbatore says,

“Construction and infrastructure de-

velopment activities have reduced

significantly. Real-estate prices are

declining. Everybody in Tamil Nadu is

waiting for the upcoming elections in

May 2016”. In contrast, Mr Manohar

Agrawal, a leading automobiles deal-

er from Varanasi has become an avid

real-estate investor. He says, “Land

prices have moved up here. A four-

lane Varanasi bypass will come up in

another year; metro is in the works

and many other infra projects are

planned for the city. Things are mov-

ing. The state government function-

ing is picking up steam, as elections

are nearing – Akhilesh needs to show

something before February 2017.”

In this context, it appears that Tamil

Nadu lags UP; but Tamil Nadu con-

tributes +8% to India’s GDP with one

third of UP’s population) compared to

UP’s 8.5% contribution. Tamil Nadu

is also far more industrialised than

UP and its infrastructure is similar to

Gujarat and Maharashtra, which are

leading Indian states. It is these very

contradictions that make a Ground

View all the more important to assess

India’s real prospects.

Contrasting Indias!

9GROUND VIEW GROUND VIEW Annual Edition 2016 Annual Edition 20168

Surging growth in Industry to drive GDP growth in CY16

GFCF growth to be driven by Government focus on Capital Expenditure

Sour

ce: M

oSPI

, Phi

llipC

apita

l Res

earc

h In

dia

Sour

ce: M

oSPI

, Phi

llipC

apita

l Res

earc

h In

dia

Leading with radical centrism

India will always have contrasting stories and has always been a promising investment destination. But it has a history of punching below its weight. With PM Modi’s government well into its second year, the big question is whether India is moving in the right direction and what is its visibility? Ground View dived deep to explore urban and rural India in all its four corners in order to provide an unflinch-ingly real view of what is happening. PM Modi’s course seems one of radical centrism, marked by a strong willingness to reform institutions while taking a pragmatic approach towards solutions. This path will yield sustainable results and consistent growth — 2016 will be better than 2015, even with a similar or marginally better GDP growth. This is because quality of growth will be superior with a sustained uptick in government capital expenditure, stronger discretionary consump-tion, and green shoots appearing in private investment – all these factors will drive a compounding and multiplier effect.

Some stumbles, some learning – course correction

Jagdish Bhagwati, an old friend of PM Modi and professor of eco-nomics at Columbia University, made two interesting observations in a recent media interview – (1) PM Modi is learning and he is always open to suggestions and (2) he has not got the right people into the right place and is openly criticising some ministers. The first point is more crucial than the second, as it is a take on certain mistakes the PM made at the beginning of his tenure such as his stand on trade agreements where he blocked the trade facilitation agreement (TFA) in an environment of rising multilateralism marked by arrangements like the Trans Pacific Pact. According to ace economist Bhagwati, he is now rectifying past mistakes. The second point is more generic and speaks about the incompetence of certain ministers – getting the best people in the right places all the time is just an iterative process.

Even though the PM has not been able to run the government with as much panache as he showed in his election campaign, India has man-aged to dart back onto a clear recovery path and achieve a healthy growth rate. One of the indicators for economic growth is indirect tax revenue growth. Arvind Subramanian, the Chief Economic Advisor to the Government of India, said in a recent media interview, “Indirect tax revenue growth, (is) the actual hard money the government col-lects, which it can only collect if underlying activities are doing well. And that number, even if you take away all the new things, new tax-es (that) have been added, that number is growing at a robust rate of about 11.5-12.0% – and if that number is right, it means that the economy is recovering.” RBI Governor Raghuram Rajan has regularly said that the economy is on a recovery path. In a recent media inter-view he said, “I think there are some signs of things starting to pick up – look at the auto sector, 22% growth year on year, so there are some signs that at least urban demand is starting to get more confident, perhaps on the basis of higher incomes and lower outgos, because of fuel and so on.” He also always emphasizes the government’s focus on structural improvements. While these take more time to deliver results, they deliver sustainable growth and take a lot more courage to implement.

Approval rating still very high for Modi

Sour

ce: M

int-

Inst

avaa

ni, P

hilli

pCap

ital R

esea

rch

Indi

a

11GROUND VIEW GROUND VIEW Annual Edition 2016 Annual Edition 201610

CLEENEX

GV’s annual edition last year titled 2015: Swa-chh Bharat, A year of India cleansing’ had said that 2015 will be a year for reforms and systemic cleansing by reducing graft and black money. The government has managed to achieve quite a few of its objectives – central-government corruption has declined significantly and measures taken to curb black money have yielded results. Even though land acquisition, a major reform, was not approved in the de-sired format in parliament (a good example of Modi’s radi-cal centrism), states are doing their bit to ensure smoother land acquisition for infrastructure projects. A slew of signif-icant reforms have been announced (GST, Uday, FDI liber-alisation), whose implementation will pick up – this, in turn, will help in faster implementation of new projects and we may see further signs of renewal in the investment cycle.

GST

GST, a major indirect taxation reform that was conceptu-alised almost a decade ago, is likely to be passed in the upcoming budget session. It is widely expected to im-prove the efficiency of the system by eliminating the cur-rent regime of cascading taxation. Other palpable benefits include removal of the inverted duty structure, enhancing the tax base by including the unorganised sector under its purview (thereby boosting the government’s revenue con-siderably and improving tax-to-GDP ratio), and increasing the competitiveness of Indian manufactured goods. While the proposed revenue-neutral rate of 18% will push up ser-vices inflation, the overall impact on inflation will be mar-ginal-to-deflating, as goods (accounting for 70% of the CPI basket) will enjoy lower taxes than in the current (CENVAT + VAT + CST) regime.

UDAY

This initiative is the government’s radically centrist attempt to tackle the burgeoning debt burden of the state dis-coms. On the one hand, discoms are not signing new PPAs because of their stressed balance sheets and on the other, banks and financial institutions (who have an aggregate credit exposure of Rs 2.8tn to this sector), are bearing the brunt – the situation has the makings of a financial-sector contagion. If UDAY is successfully implemented by states, it will lead to an operational turnaround of discoms, en-hance accountability of states in future losses, alleviate bal-ance-sheet stress, and ease asset-quality stress for banks. GV team’s discussions with key bureaucrats suggest that UP, Rajasthan, and Jharkhand (accounting for ~40% of dis-com debt) are inclined positively towards this policy.

FDI liberalisation:

The government has further opened up the economy to FDI while enhancing limits in various sectors and in-cluding more sectors under the automatic route. There is a conscious approach to liberalise the economy and encouraging FDI inflows is a means to achieve that end. The government has simplified procedures and en-hanced limits, along with making changes in the lock-in period for some sectors. While the incremental delta of such moves will not be felt immediately (especially in a demand-starved scenario), when growth returns to a fast-er trajectory (medium term), this policy will fructify and enable acceleration.

Easing of norms for infra developers: To encourage private capex in construction, the gov-ernment has undertaken a number of administrative measures such as funding approvals for projects stuck due to lack of funds, extension of concession period to all BOT projects delayed during construction, easing of exit norms to redeploy proceeds for debt retiral, allow-ing full divestment of operational road projects, relaxing norms in lock-in period, improving rural connectivity, and a Road Asset Management System to increase the speed of building new roads.

Ease of doing business:

To improve the overall ease of doing business across the country, DIPP has been collaborating with states to im-prove efficiency and introduce a ranking methodology (based on eight broad parameters) to foster competition. The first year’s rankings (used as baseline) are throwing

Swachh Bharat: Less bumpy from here

11GROUND VIEW GROUND VIEW Annual Edition 2016 Annual Edition 201610

Advanced economies again becoming the driver of global growth

*8 major economies Source: Economist Intelligence Unit

FII outflows became stronger this year

Sour

ce: B

loom

berg

, Phi

llipC

apita

l Res

earc

h In

dia

up surprises; top-ranked states are using these rankings in their investor meets to showcase themselves as investment destinations. As the era of competitive federalism is being unleashed in India, states will be propelled to cut red-tapism (more than ever) and improve their administrative mecha-nisms (so that they do not lag behind in garnering funds).

India’s place in an unspectacular world

The year gone by has been unspectacular from the perspec-tive of stock returns; investors might as well have shoved their money under their mattresses and slept peacefully. Nif-ty fell 5% YTD and some of the major global indices such as S&P 500 and FTSE 100 virtually stagnated. However, a lot has changed in the last 11 months, which will have sig-nificant ramifications on medium- to long-term returns. In 2016, developed nations will contribute more than emerg-ing economies to the world economic growth for the first time since the 2008 financial crisis. Emerging economies, led by China, will face challenging times. China might do well by warding off an economic crisis – it has already failed to restructure its state-owned enterprises and bring down debt levels. India’s situation is more cheerful, but political noise takes away the focus from core-development issues – this has made it lose some of its sheen. However, this is only a short-term phenomenon, not a permanent dampener.

With an agenda of radical centrism, India is better placed to deliver growth – not just vs. emerging economies, but also vs. developed ones. Globally, there is a lot of disen-chantment with centrist pragmatism; populism in different forms is making headway. Some of the interesting exam-ples are xenophobic right-wing populism in the US with Trump garnering decent favourability ratings despite mak-ing statements that would usually not go down well with

Americans and France’s Marine Le Pen getting a boost in in French regional elections, or the left-wing politics of Jer-emy Corbyn in the UK. In a global environment marked by stagnant wages and low nominal GDP growth rate, populist quick fixes of a tax cut here, some hike there will only have ephemeral results. On the other hand, with the right brand of politics, India is streaming ahead and will start becoming visible in 2016. This will ensure India will continue to be a sought-after investment destination for global funds.

Challenging times for global businesses, but good times ahead for India

Developed markets will deliver better growth in 2016, but in its a intertwined world for companies, improving developed economies do not necessarily usher good times for all. Many global corporations have counted on emerging markets for growth and some firms such as HSBC were planning to shift headquarters to Hong Kong – such decisions are likely to take a back seat now. Corporate behaviour is quite different from fund managers’ behaviour – the latter tend to change investment destinations overnight. The focus of global cor-porations is on long-term growth strategy and corporations will not pull out money from their established businesses in China or promising destinations such as India.

In his endeavour to market India as an attractive investment destination to the world, PM Modi undertook whirlwind tours of the world. His ‘Make in India’ program aims to po-sition India as an alternate destination to China. India saw higher FDI flows in the 2015 and this is likely to accelerate, with ecommerce alone likely to garner US$ 10bn in 2016 vs. US$ 8bn in 2015. Foxconn and Xiaomi have announced plans to set up units in India under Make in India. Foreign direct investments will pick-up further and FII inflows should gain traction as the year progresses.

13GROUND VIEW GROUND VIEW Annual Edition 2016 Annual Edition 201612

Nominal GDP growth with NIFTY

Market expectation on the trajectory of Fed rate hike in CY16Govt capex has picked up this year

Sour

ce: M

inist

ry o

f Fin

ance

, Phi

llipC

apita

l Res

earc

h In

dia

Sour

ce: B

loom

berg

, Phi

llipC

apita

l Res

earc

h In

dia

India Equities: You are known by the company(ies) you keepThe nominal GDP growth rate in 2016 will be better than 2015 (quantum will be determined by global factors) and it will keep the markets interested. The year will be a good time for stock picking with attractive valuations, especially in core sectors and ones with medium capitalisation. The four big-gest themes for 2016 are likely to be:

1. Government spending will be a major driver of GDP: Gross tax collections for the first seven months of FY16 were up 23%. Tax revenue momentum has been strong and FY16 will close on a strong note. Revenue collection will be strong in 2016 despite a strong base in 2015 – rise in certain taxes (such as service tax) will help. This will significantly increase the government’s ability to spend in 2016. Government spending on the capital account was up 61% in 7MFY16, es-tablishing a strong base – 2016 will see this trend continuing. The infrastructure sector is already seeing a lot of activity – road orders are picking up and railway orders are gathering steam. These reinvigorated sectors will see further traction in 2016. With a pick up in government spending, public sector banks should see an improvement in credit growth.

2. Urban discretionary spending will gain momentum: Declining interest rates, rising incomes, and decreasing out-go (due to lower fuel and interest costs coupled with the government’s implementation of the seventh pay commis-sion) will mean improved spending capacity. Disposable in-comes in urban areas will rise and will lead to an increase in the consumption of discretionary products. Both small-tick-et and large-ticket discretionary consumption will benefit. Four-wheeler automobiles, consumer durables, and eating out will gain traction.

3. Persistence of a strong dollar: Fed rate hike will keep the dollar strong. Export-based plays will see continued interest, but valuations and business fundamentals will be a concern in sectors such as IT and pharmaceuticals.

4. Bottom-up market: Themes 1, 2, and 3 are a continuance of 2015 themes - to some extent are priced-in by the markets. While the 2016 real GDP growth rate will be better than 2015,

13GROUND VIEW GROUND VIEW Annual Edition 2016 Annual Edition 201612

Credit growth at historical low Consolidation in growth in stress assets

Industry credit vs project announcement + stalled project revival (adjusted for lag)

Sour

ce: R

BI, P

hilli

pCap

ital R

esea

rch

Indi

a

Sour

ce: P

hilli

pCap

ital R

esea

rch

Indi

aSo

urce

: CM

IE, P

hilli

pCap

ital R

esea

rch

Indi

a

it will not be materially different – because private invest-ment spending will continue to lag. The broader market is not likely to see huge appreciation; therefore, stock picking based on earnings growth in conjunction with valuations will be critical. Quality midcap stocks with earnings growth will perform well.

Swachh banks: Waiting for upswing in credit cycle

“We are beginning to see an end of the NPA cycle. Slip-pages are down sequentially as well as yoy and therefore, we believe that we are now getting to the bottom of the pile, so to speak. So, going forward, the prognosis should be good,” said Arundhati Bhattacharya, Chairman of SBI in a conference after SBI announced its 2QFY15 results. 2015 was a particularly rough year for Indian banks. The NPA cycle was expected to bottom in the early part of the year, but con-tinued to surge. Credit growth hit a 20-year low and demand in the credit ecosystem is yet to come back. In fact, the credit to industry, which accounts for 40% of the total credit, is even lower at 6% yoy.

Project announcements impact credit growth with a lag of around two years. Lack of new project initiatives over the last few years has exhausted the industrial capex pipeline, thus severely affecting corporate credit growth. New project an-nouncements (private and government) in FY13/14 were Rs 5.2/5.8tn, down from the peak of Rs 22tn in FY09. However, the rate improved in FY15 to Rs 10.2tn. Credit growth should see positive traction from FY17 onwards.

The recovery is unlikely to be V-shaped (like in earlier cy-cles), as decline in commodity prices and subdued corpo-rate toplines have impacted working-capital demand. Credit growth in 2016 is likely to be in the range of 12-14%, indicat-ing a significant increase from 9% in CY15.

The rate of slippages in the banking system has decelerat-

ed significantly. Growth in stressed assets in H1FY16 has been 3% and now the stressed-asset-to-loan-book ratio is stabilising. “We hope that over the next year, say by March 2017, a full clean-up will have been done by banks...the idea is to put the real assets back on track with whatever needs to be done,” said Dr Raghuram Rajan in a recent policy-announcement confer-ence.

A plethora of measures have been announced last year (5/25 scheme, UDAY, strategic debt restructuring, and management takeover trend under SDR). A hands-on approach by the RBI and the centre (by evaluating banks on certain KPIs) will deter-mine capital infusion by the centre. As such, the focus of PSU banks will be on improving their bottomline rather than chasing credit. CY16 should be marked by moderation in stressed-asset creation rather than subliminal credit growth.

15GROUND VIEW GROUND VIEW Annual Edition 2016 Annual Edition 201614

Unsold real estate inventory by citites

Sour

ce: L

iase

s For

as

Building the multipliers: Roads and Rails

Mr Ramnath recently quit his lucrative job at Goldman Sachs to work for the Nagpur Metro project. He says, “Apart from the clichéd ‘Indian infrastructure has tremendous potential’, I would say that the more critical aspect here is better plan-ning. Often, long-term planning takes a back seat and even newly developed projects’ short comings are seen within a few years. Better planning and adherence to international standards present the real outsized opportunity.” Mr Ram-nath’s view is an apt description of India’s infrastructure plan-ning – in the recent Chennai floods, the suburbs (with mod-ern infrastructure) were more impacted than the old city (with colonial infrastructure), which managed to deal with the situ-ation much better. However, the focus on better implementa-tion is getting more importance than before. Metro projects have been implemented with global standards. The National Highways Authority of India (NHAI) is awarding projects with far greater efficacy than before.

The roads sector is witnessing maximum traction within the infrastructure space. Not only has NHAI awarding kept up its pace, it has cleared many bottlenecks to revive stuck projects. In many cases, it has gone to the extent of altering the con-cession agreement – an unprecedented move in the sector. YTD, NHAI has awarded 3,000km of projects – moving stead-ily towards its target of 5,100km for FY16. Similarly, MoRTH has awarded ~1,000km of projects (its target is 2,500km for FY16). All in all, the road sector seems to be progressing well towards its total target of 7,500km of awards (4,000km award-ed already).

A key feature of the order awards this year has been NHAI’s success in awarding some of its long-pending projects. For ex-ample, it awarded the Eastern Peripheral Expressway – a pro-ject envisaged to decongest the national capital and provide a ring-road structure for heavy vehicles – albeit four years after it was first put up for bidding. Similarly, it awarded the Agra-Eta-wah project (which was terminated) to IRB Infra on a BOT basis.

Roads and infrastructure projects have a multiplier effect, as connectivity improves the overall system efficiency and encour-ages private investment. Private spending is sluggish, but as more infrastructure projects kick off, it will also see improve-ment.

Private investment anaemic: Where art jobs?

With real-estate-construction activity taking a back seat, the sector’s woes will persist because of the sheer number of de-velopers present. The system has more capacity than required, contends Mr Ashutosh Limaye, Head of Research at JLL, a leading real-estate consultant. The real-estate sector was a ma-jor contributor to job creation in the last investment cycle, but in the current situation, the sector will do well to just avert crisis

over next six months. By the end of 2016, the cycle should have bottomed and some pickup in activity is likely.

“Property developers in the top-seven cities have re-duced new project announcements. Supply correction has taken place according to the demand correction. Apart from NCR and Navi Mumbai, other major cities are unlikely to see a major crisis, but the situation in NCR is quite grim,” says Mr Limaye. He adds that property prices will appreciate slowly and expects price appreciation of around 5% annually in the medium term. Investor activity in the sector has reduced to around 15% of transactions from giddy levels of 50% around 3-4 years ago. However, alluding to sales growth of 28% yoy in the first six months of FY16, he contends that the worst is over.

Last time, the private-investment cycle was led by power, steel, and cement. All these sectors are now struggling. Power has excess capacity and it is grappling with low load factors, as many plants are unable to execute pur-chase agreements with distribution companies. UDAY reforms will come to the rescue, but the system still has excess capacity and is unlikely to see a major upswing in investments in the medium term. The metals and mining sectors are struggling because of excess global capacity and low prices. Investment in the steel sector is not likely to revive any time soon. Cement is seeing consolidation and it may not see revival in investment.

However, green shoots should start appearing for private investments led by construction and infrastructure devel-opment. Industrial capex in traditional sectors will happen with a lag, but capital spending in new-age sectors such as technology, will pick up in 2016.

15GROUND VIEW GROUND VIEW Annual Edition 2016 Annual Edition 201614

Funding in ecommerce and as % of FDI

Jeff Bezos, founder of Amazon on his visit to India. Pic Courtesy: Amazon

Sour

ce: M

inist

ry o

f Com

mer

ce, P

hilli

pCap

ital R

esea

rch

Indi

a

Age of the Unicorns: A healing touch for anaemic private investments?

Unicorns have long been revered in India. A unicorn was depicted

on ancient seals of the Indus-valley civilisation. In today’s context,

the term unicorn was coined by Aileen Lee, a venture capitalist,

to describe a private technology company valued at over US$

1bn. Globally, there are 145 unicorns of which eight live in India –

namely Flipkart, Snapdeal, InMobi, Paytm, Quickr, Ola, MuSigma,

and Zomato. Three more are likely to join the family – Shopclues,

Oyo Rooms, and Big Basket.

In 2015 (till date), FDI in ecommerce totalled at US$ 7bn, up 50%

yoy and constituting around 25% of India’s total FDI. In 2016, this

is likely to rise 25% at least to US$ 10bn, with Amazon’s plan

of making India its biggest market outside of the US.

Mr Neeraj Singla’s traditional family business is khaini (fla-

voured tobacco). While the business has generated tremen-

dous cash for years, now it is declining. Mr Singla wants

to invest aggressively in mobile applications. According to

him, “Investments for trialling ideas is not substantial, but if

an idea shows promise, then there is no problem in investing

any amount.” Like Mr Singla, many traditional Indian busi-

nesses are looking at investing in technology. Reliance Jio’s

first major product was Jio Chat and Bharti Enterprises has

invested in Hike Messenger. According to the grapevine,

the next-generation Ambanis, Akash and Isha, who are now

part of Jio, are keen on new age start-ups. Entrepreneurial

activity in ecommerce is rising at a fast clip; increasingly,

students from the prestigious Indian Institute of Technology

are seeing start-ups as the holy grail of success.

“There is a Silicon Valley coming up in Powai,” says the lead

character in a very successful online sitcom, TVF Pitchers.

The lure of start-ups is big and this is just the beginning, as

investors in the segment are long-term holders with a lot

of experience and patience to guide promising start-ups.

Wannabe entrepreneurs from IITs are modelling themselves

on global luminaries like Steve Jobs, going to the extent of

matching their eccentricities. However, a lot of good can

come out of this fast-developing ecosystem. Many jobs

(jobs as in employment, not the man) will be created, and

technology start-ups provide the best avenues for chan-

nelizing the energy and restlessness of the Indian youth.

17GROUND VIEW GROUND VIEW Annual Edition 2016 Annual Edition 201616

Make in India is gathering steam

One of PM Modi’s most-quoted campaign slogans is

“Make in India”, which was envisaged to be the prime

job-creating platform for India’s youth. This year, under

Make in India, the centre’s prime focus was on easing pro-

cesses through de-licensing and deregulation (such as sin-

gle-window clearance), opening up critical sectors such as

railways, defence, and construction, and wooing foreign

capital. While time will tell if the initiative is successful, it

has already started seeing investments coming in under

its flagship.

Xiaomi has partnered with Foxconn to set up a manufac-

turing unit in India. Alstom and GE have signed an esti-

mated Rs 400bn (US$ 6bn) agreement to set up manufac-

turing plants for railway locomotives. Powergrid has also

started complementing this initiative by having a Make in

India clause in its transmission projects tenders.

Indian consumer feeling the pinch

“Sales managers of FMCG companies have stopped going

to the market, they have lost touch with developments on the

ground. Targets keep rising irrespective of the demand scenar-

io and retail schemes have made a mess of the channel. The

whole system seems to be on steroids and corrective actions

are required. I am glad that the top management of some com-

panies have woken up. Still, a lot needs to be done, but its

better late than never,” sighs Ghanshyam Agarwal a leading re-

tailer, wholesaler, and distributor for multiple FMCG companies

in Kanpur, Uttar Pradesh.

A heady mix of low price growth and high channel incentives

has clogged the distribution channels, as FMCG sales manag-

ers scrambled to meet targets by resorting to revenue-at-any-

cost schemes. Complicated channel schemes, based on out-

FMCG growth trend

* Sales growth for Q1/Q2FY16 excludes Nestle**Volume growth is calculated as average of volume growth of Britannia, Dabur, Colgate, Emami, HUL, Marico, Asian Paints

Chandrababu Naidu signing deal with Xiaomi under the Make in India programme

17GROUND VIEW GROUND VIEW Annual Edition 2016 Annual Edition 201616

lets count and targets, have made a mess of the channels of

leading companies such as Hindustan Unilever. Undercutting

by distributors is rampant. HUL is now taking stock of the sit-

uation by optimising the schemes and outlet count. Howev-

er, while companies take stock, the system’s liquidity seems

to have evaporated, as wholesale channels have significantly

reduced inventory to combat price and scheme uncertain-

ty. Demand scenario has continued to remain uninspiring,

which has further aggravated channel woes.

Inventory destocking by the wholesale channel is a lead indi-

cator of the demand scenario and it also indicates that times

are going to be challenging. Receivables in the system are

rising across India and across companies, but the trading en-

vironment in the southern market is more sluggish than in

the northern part of India. A number of factors have been

attributed to lower liquidity in the market – these include

falling real estate prices, falling gold prices, slower income

growth in the southern market, and waning consumer confi-

dence in some parts.

Even though there are systemic problems for consump-

tion, trends (premiumisation, discretionary consumption,

and growth in categories such as food) remain robust. 2016

should be good for categories of consumption that are

helped by lower interest rates and deflationary trends.

Urban discretionary consumption strengthening; automobiles gathering pace

“Rural growth was twice as fast as urban about two years

ago; it is still growing faster than urban, but slowing down.

Now it is around 1.5 times the urban growth rate. In some

pockets, the pace of slowdown is alarming. Urban should

pick up soon,” says a leading distributor of consumer goods

Auto growth trend

Trend in urban CPI

Trend in advertising revenue growth

in Allahabad, UP. He believes that decline in the system’s

liquidity is because of slower growth in rural subsidies such

as MNREGA and that MSP prices are having an impact

now. In Punjab, land prices had soared in the last 10 years

and many farmers sold some of their land and enjoyed the

wealth effect. This phenomenon is waning and rural growth

has become quite sluggish in large-ticket discretionary pur-

chases in the states of Punjab and Haryana.

Urban demand is likely to pick up in 2016 in a meaningful

way. Earlier, while Dabur was focussing its energy towards

urban products, Hindustan Unilever contended that rural

demand would lead to a revival, as urban demand con-

tinued to remain sluggish through 2015. However, now

signs of a pickup in urban demand are becoming more

visible. Auto sales are picking up and are likely to sustain

19GROUND VIEW GROUND VIEW Annual Edition 2016 Annual Edition 201618

C O M P A N I E S 2 0 1 6 Operating Outperformers

According to PhillipCapital

India Research, the following

companies will deliver operational

outperformance in 2016. A

significant number of companies are

from the mid-cap space, indicating

the year is likely to belong to

medium capitalisation companies.

Bank of Baroda

Sour

ce: C

ompa

ny, P

hilli

pCap

ital I

ndia

Res

earc

h Es

timat

es

Plays on government spending

Bank of Baroda: Savvy PSU

BOB has a diversified portfolio and lower concentra-

tion of lending to leveraged corporate groups. Banks

with lesser exposure to stressed assets will see a faster

turnaround. The new management seems to be pro-

active in cleaning up the balance sheet and focusing

on profitable businesses. The strategy articulated by

the bank includes – containing asset quality and fo-

cusing on recovery, improvement in spread by reduc-

ing low-margin buyer’s credit, introducing risk-based

pricing model, and reducing dependency on syndi-

cate loans. The bank is likely to reach +15% RoE in the

next three years. The loan book may remain subdued

as the bank trims non-profitable business such as buy-

er’s credit. Earnings should fall 30% in FY16 followed

by 72% earnings growth in FY17.

momentum in 2016 aided by improving incomes, lower

inflation, and lower interest costs. Seventh Pay Commis-

sion (for government employees) has announced a pay

hike of 24% yoy. While the pay hike is lower than the

Sixth Pay Commission, which led to significant increase

in auto sales, still it is good enough to boost auto sales.

Another lead indicator of urban discretionary consump-

tion is advertising spend on television. Television adver-

tising revenue growth in 2015 was around 20% yoy. This

was driven by discretionary products such as personal

care, foods, and consumer durables. In 2016, advertis-

ing growth will remain robust at around 16% yoy. New

product launches, rising contribution of tech companies,

and margin cushion for FMCG companies ensure strong

growth and visibility.

Urban demand will gather further steam with consum-

er durables, four wheeler automobiles, eating out, and

personal care becoming key drivers of consumption.

19GROUND VIEW GROUND VIEW Annual Edition 2016 Annual Edition 201618

ITD Cementation

NCC

NCC: Trinity’s other play

NCC is witnessing remarkable improvement in its profitabil-ity on margin expansion and reduction in interest expenses. Over the last six quarters, its EBITDA margins have expand-ed by 330bps – to 8.8% in 2QFY16 from 5.5% in 4QFY14. Margins should improve further to 8.75% in FY16 and 9.25% in FY17 on lower competitive intensity.

However, the biggest delta for NCC will be from reduction in interest expenses. In September 2014, the company raised Rs 6bn via a rights issue, and used the entire pro-ceeds to reduce debt. Debt levels came down to Rs 20bn in 4QFY15 from Rs 27bn in 2QFY15 – and leverage to 0.6x in FY15 from 1.4x in FY14. Reduction in debt, as well as im-provement in credit rating (due to lower leverage levels) will lead to interest savings of Rs 1.3bn in FY16. In FY17, cash proceeds from the sale of power plants, and improvement in operating cash flows, should lead to further debt reduction of Rs 3bn and interest coverage ratio improving to 1.6x in FY17 from 0.9x in FY15.

Sour

ce: C

ompa

ny, P

hilli

pCap

ital I

ndia

Res

earc

h Es

timat

es

Sour

ce: C

ompa

ny, P

hilli

pCap

ital I

ndia

Res

earc

h Es

timat

es

ITD Cementation: Trinity in play

ITDC is the perfect turnaround story to play in this cycle. Over the last four years, the company was reeling under the pres-sure of delayed payments by various government bodies (es-pecially NHAI) and a countrywide lack of order inflows. How-ever, in the last 12 months, many of its claims were cleared (including Rs 3bn with NHAI) leading to easing of WC cycle. ITDC has grabbed multiple large orders, taking its orderbook to 3x book-to-sales (4.3x including L1) and its operating mar-gins have improved by 320bps, over the last three quarters.

Over CY14-17, ITDC should report a robust topline CAGR of 34%, margin expansion of over 420bps, and earnings CAGR of 99%. Its presence in segments such as MRTS and ports will lead to high and sustained growth, along with margin expansion as competitive intensity is much lower in these segments than others (such as roads, buildings). Its working capital situation, which has improved dramatically over last six months (debtor/inventory days down to 63/166 in 1HCY15, from 94/240 in CY14) should sustain at current levels, keeping leverage under check.

21GROUND VIEW GROUND VIEW Annual Edition 2016 Annual Edition 201620

Dalmia Bharat: A play on asset sweating

DBL’s capacity CAGR of 35% over the last 10 years was driven by both organic and inorganic growth. However, volumes are still in a ramp-up mode. It is all set to deliver consistent vol-ume growth of +20% yoy over the next few fiscals (Q3FY16 could be lacklustre due to the floods in Tamil Nadu). DBL will ramp up utilisation in Karnataka and northeast, and is likely to achieve its aggressive FY16/17 targets. Channel checks suggest that DBL has already started aggressive efforts to build its dealer network for its Belgaum plant across its target markets (Maharashtra and Karnataka). It expects minimum capacity utilisation for all the new plants at 50%+. Other highlights:

• Remains committed to cost efficiencies; is amongst the most cost efficient producer of cement in India current-ly.

• Immediate focus will be asset sweating and net debt reduction. Asset sweating will help volume growth and drive operating earnings.

• DBL’s region-mix remains very favourable. All markets (barring east India) are stable in terms of cement pric-

ing.

Dalmia Bharat

Sour

ce: C

ompa

ny, P

hilli

pCap

ital I

ndia

Res

earc

h Es

timat

es

Aurobindo Pharma

Sun Pharma

Sun Pharma: It’s back!

Sun Pharma will see strong growth momentum in US sales led by scheduled launch in gGleevec with 180-days exclusivity in February 2016. Additionally, a near-exclusivity scenario for gGleevec through-out FY17 would boost SUNP’s earnings by over 50% yoy for the next five quarters despite ongoing Halol plant issues. It expects synergy benefit of US$ 280mn, which will be a key earning booster in FY18. Negatives of Ranbaxy’s integration are already priced in.

Sour

ce: C

ompa

ny, P

hilli

pCap

ital I

ndia

Res

earc

h Es

timat

esSo

urce

: Com

pany

, Phi

llipC

apita

l Ind

ia R

esea

rch

Estim

ates

Dollar Plays

Aurobindo Pharma: #Approved

With 20 ANDA approvals YTD (highest within peers), and likely approval of few big-ticket injectables, Aurobindo is set to deliver strong US sales in H2 vs. H1. Additionally its robust ANDA pipe-line of 168 drugs will power US sales in the near future. Profitable growth in its European operation (led by site transfer of product sourcing from Actavis to its own greenfield plant) from FY17 would drive value growth over FY15-18.

21GROUND VIEW GROUND VIEW Annual Edition 2016 Annual Edition 201620

Bottom up plays Tata Com: It‘s all about adding value to data

TCom has made a paradigm shift in its data business strat-

egy from an ‘infrastructure-deployment-led approach’ to

an asset-light partnering approach in order to leverage

on its existing global infrastructure and vast new-age en-

terprise product suite. TCom’s capex intensity will remain

low and revenue/profitability growth trajectory will remain

robust. Currently, the new services are yet to gain traction

as the company has significantly scaled its capability in

executing complex projects, which take higher gestation

to yield results. Its data-services segment is showing im-

mense traction, but the revenue growth is likely to remain

lumpy in the medium term. Asset sale (Neotel and Data

Center businesses) will also help in significantly delever-

aging the balance sheet.

Tata Com

Praj Industries: Scaling up

Praj aspires to be a major player in the environ-

ment, energy, and agri-process-led applications

providing integrated solutions including plant,

equipment, and products. The worst is behind for

the company and 57% yoy growth in order book

in 1HFY16 should support its revenue growth. An

increased business scale will cover fixed cost and

improve margins along with monetisation of R&D

through contract research and commercial success

of second-generation ethanol. Praj has significant-

ly de-risked its business from oil-price volatility

— its order book has only 9% exposure to pure

fuel-based ethanol plant orders.

Sour

ce: C

ompa

ny, P

hilli

pCap

ital I

ndia

Res

earc

h Es

timat

es

Sour

ce: C

ompa

ny, P

hilli

pCap

ital I

ndia

Res

earc

h Es

timat

es

Praj Industries

23GROUND VIEW GROUND VIEW Annual Edition 2016 Annual Edition 201622

Bharti Airtel

Bharti Airtel

Plays on urban discretionary spending

Bharti Airtel: Capital productivity will improve

Bharti has secured most of the spectrum for data services and sustainability of voice services. Capex for FY16, including spectrum-related spending, has peaked and capex intensity will decline. Apart from decline in domestic capex intensity, capital spend-ing for Africa will also decline with sale of passive infrastructure assets. As capex intensity declines and data revenues grow at a fast clip, rising EBID-TA growth will result in significant improvement in capital productivity. Bharti’s superior spectrum assets and ubiquitous data and voice network will translate into market share gains, furthering the case for asset sweating, resulting in improving return ratios.

Sour

ce: C

ompa

ny, P

hilli

pCap

ital I

ndia

Res

earc

h Es

timat

es

Allcargo Ltd

Allcargo Ltd

The synergized business model provides cost effective

logistic solutions and is ready to exploit attractive

opportunities in new businesses with entry into costal

shipping and third party logistics (3PL). It is also

focusing on e-commerce and supply chain logistics and

will develop land bank of 200acres for ICD/warehousing

after GST. It has done upfront capex in CFS and project

business and has marginal routine capex leading to de-

leveraging of balance sheet with expected cash flow

generation of ~Rs 10bn over two years. Its presence

across the critical value chain in logistics, Allcargo

would be a major beneficiary of increased global trade

and recovery in domestic industrial activity.

Sour

ce: C

ompa

ny, P

hilli

pCap

ital I

ndia

Res

earc

h Es

timat

es

23GROUND VIEW GROUND VIEW Annual Edition 2016 Annual Edition 201622

Jubilant Foodworks:

Stuff it to heart’s content

Demand will improve in the next few quarters as

lower CPI and turnaround in industry growth will

stimulate individual/corporate discretionary con-

sumption. Jubilant Foodworks has a very high op-

erating leverage; a 1% increase in SSSG increases

EBIT by 8%. The company has already taken a

price hike of 3-4% in this quarter and improve-

ment in both SSSG and operational performance

will start in 3QFY16.

Jubilant Foodworks

Sour

ce: C

ompa

ny, P

hilli

pCap

ital I

ndia

Res

earc

h Es

timat

es

Bajaj Auto: Structural rider

Volume growth will remain strong led by the rag-

ing success of its newly-launched Avenger, which

dealers highlighted will clock 4-5x volume vs.

older version. Additionally, premiumisation story

in two wheelers is more structural, which will ben-

efit Bajaj’ Pulsar portfolio. Aggressive product

launches with four new two-wheelers until FY17

end will only mean significant market share gains.

While exports have been struggling recently,

African/LatAm markets are in nascent stages

of growth with two-wheeler penetration low at

4%/6% only, which would lead to sustained ex-

ports growth. All this would lead to a robust 18%

CAGR in earnings until FY17.

Bajaj Auto

Sour

ce: C

ompa

ny, P

hilli

pCap

ital I

ndia

Res

earc

h Es

timat

es

25GROUND VIEW GROUND VIEW Annual Edition 2016 Annual Edition 201624

C O M P A N I E S 2 0 1 6 Operating Underperformers

HUL: A lever less

Due to a further fall in crude prices, HUL’s de-

tergents category (growth driver in the past) will

continue to face severe deflationary and compe-

tition headwinds. Other categories such as sham-

poos, soaps, and oral care will continue to see

heightened competition, which will put pressure on

margins and sales. Channel checks suggest that the

winter-care portfolio will be impacted by some sup-

ply issues in north India. Hence, sales growth may

throw negative surprises in the near term. Operat-

ing profit growth will be lower in FY17 vs. FY16 due

to huge gross margin improvement in FY16, which

will not be the case in FY17.

HUL

Sour

ce: C

ompa

ny, P

hilli

pCap

ital I

ndia

Res

earc

h Es

timat

es

Maruti Suzuki

Maruti Suzuki: It’s all about the market share

Maruti will see strong growth in volumes with ro-

bust momentum across regions, further strength-

ening market share. This is just the beginning

of a recovery cycle in passenger cars. Maruti’s

strong launch pipeline means it will post over

15% growth in volumes in FY17 and benefits from

the Seventh Pay Commission will be an added

positive.

Sour

ce: C

ompa

ny, P

hilli

pCap

ital I

ndia

Res

earc

h Es

timat

es

The following companies are likely to face operational

headwinds in 2016 leading to deterioration in key

performance indicators as compared to 2015

25GROUND VIEW GROUND VIEW Annual Edition 2016 Annual Edition 201624

Apollo Tyres

Lupin

Lupin: Challenging times

Lupin’s US portfolio has already seen over

15% price erosion and its key product

launches (Welchol, Renagel, Renvela) are

delayed by one year to Q4FY17 or be-

yond, which worsens its already weakened

near-term US pipeline. Recent acquisition

of Gavis in the US is the only respite, but

slippage in guidance for Gavis’ ANDA

approvals (20 p.a.) and growth are likely. Its

ambitious long-term R&D spend and lack of

any major drug launches in the US will drag

down operating efficiency in the near future.

Apollo Tyres: Losing grip

Channel checks suggest that Chinese compe-

tition is rapidly taking away market share in the

Truck-Bus-Radial (TBR) space given the pric-

ing advantage (25-30% cheaper). Moreover,

Apollo has taken up to 10% price cuts and is

contemplating further cuts in order to combat

this competition. Heightened competition and

increased pricing pressures will lead to margins

remaining strained and benefits generated

from lower raw material prices are likely to

reverse in FY16/17.

27GROUND VIEW GROUND VIEW Annual Edition 2016 Annual Edition 201626

LIC Housing Finance: Base(rate) is the spoil-

sport

Its stellar core performance so far in FY16 was ac-

centuated by improvement in margins. Decline in

cost of funds and stability in lending yields added

to NIM expansion – up 27bps yoy in H1FY16. The

re-pricing benefit on the liability side has already

being reaped, as proportion of term loan from

banks has been reduced to 15% from the highs

of 34% of total borrowing. The lending yield was

held up due to change in portfolio mix towards

high-yielding LAP. With transmission of policy rate

cut, the bank has reduced its base-rate in a more

aggressive manner in the previous quarter, mak-

ing the mortgage market more competitive. The

problems of asset quality and poor capital position

have forced most of the PSBs to focus on secured

businesses such as mortgages. Heightened com-

petitive intensity would exert pressure on the mar-

gin, translating into moderation in core earnings.

NII growth is likely to be 14% /30% in FY17/16 and

PAT growth at 14%/23%.

LIC Housing Finance

Marico

Marico: Parachute missing

Fall in prices of copra, Parachute coconut oil

(past growth driver) continues to face severe de-

flationary and competition headwinds. Increase

in premium for Rice Bran Oil vis-a-vis palm oil,

which has seen a collapse in prices, makes sig-

nificant price hikes difficult in its edible oils port-

folio. While other categories like value-added

hair oils and new innovations such as Saffola

Oats will perform well, absence of price hike in

its crucial coconut oil and edible oils portfolios

and overall slowdown in volumes will put pres-

sure on sales. Sales growth may throw negative

surprises led by price cuts and heightened com-

petitive activity. Operating profit growth is likely

to be lower in FY17 vs. FY16 as further gross

margin expansion is improbable.

Naveen Kulkarni ([email protected])

Anindya Bhowmik ([email protected])

27GROUND VIEW GROUND VIEW Annual Edition 2016 Annual Edition 201626

Total real returns on US stocks, bonds, bills, gold and the dollar, 1802-2012

So if this basket can outperform the most-admired

fund basket in the world for a sustained period, why

not be bullish on the Nifty?

Consider another approach. Let’s begin with basic

principles – with the merit of the asset-class itself.

The adjacent chart definitively drives the point that

equities have been, by far, the most productive invest-

ment.

The simple case for Indian equities

Nifty vs Berkshire Peformance in USD

Sour

ce: B

loom

berg

Sour

ce: B

loom

berg

How can we make a simple case for investing in Indian equities? There can be many approaches but allow me to share a rather interesting one – I won’t bore you with the usual ‘next trillion dollar opportunity’ drivel, but will try and make an argument with a focus on the ‘look and feel’ of the India story.

Think about the most admired investment compa-

ny in recent years – it has to be Berkshire Hathaway.

Berkshire is the platinum standard of equity investing

and for good reasons. If any equity basket has outper-

formed Berkshire, wouldn’t it be worthy of attention?

Well, as it turns out, Nifty has outperformed Berkshire

over 2000-15 and that too in USD terms.

However, this is in the US, a cynic might counter. Sure,

but best Indian corporates have performed as well as

the best US corporates. Consider the performance of

HDFC Bank’s stock vs. Apple’s (in terms of local currency).

HDFC Bank has been in lockstep with the stock of the

most valuable company in the world over a long period,

indicating the bank’s strength.

BY VARUN KUMAR

29GROUND VIEW GROUND VIEW Annual Edition 2016 Annual Edition 201628

HDFC Bank vs Apple Stock Price Performance, Local Currency

HDFC Bank vs Apple Market Cap (USD)

India’s break from slow growth phase happened in 80s.

Source: http://www.nber.org/papers/w10376.pdf

Sour

ce :

PwC

India’s GDP (PPP) Projection

Should you worry about the noise on reforms? I believe

concerns are overblown and the evidence is in India’s

history. While the commonly held belief is that India’s

growth turned over a new leaf after the 1991 reforms,

some serious academics have argued that the growth

turned around much before, in the 1980s. This camp has

people like Princeton Professor Atul Kohli and Harvard

Professor Dani Rodrik and current Chief Economic

Advisor Arvind Subramanian. Dani Rodrik and Arvind

Subramanian’s paper shows that the breakthrough in

growth came in 1980 itself – seen in the chart.

So where is the opportunity then? It is in the fact

that HDFC Bank is much smaller than Apple and that

there is a headroom for growth in the years to come.

That growth headroom will come from (clichéd, but true)

GDP growth over the next few decades (PwC projections).

The reason for this break was not big-

bang reforms but simply the government’s

pro-business attitude, which helped in

the ease of doing business (compared

with constrained License Raj days) and

unleashed productivity growth in Indian

companies – this can also be seen in the

chart. Given bottlenecks in the economy

today and the focus of the government on

ease of business, this attitude shift itself

can do wonders. Reforms would be a big

icing on the cake.

Varun Kumar ([email protected])

29GROUND VIEW GROUND VIEW Annual Edition 2016 Annual Edition 201628

India’s break from slow growth phase happened in 80s.

Source: http://www.nber.org/papers/w10376.pdf

BELOW: Most brokerages (including us) were bullish on Indian equi-ties’ prospects in 2015 as seen in their December 2015 predictions

Sour

ce: F

inan

cial E

xpre

ss

Last year saw a consensus in bullishness about the prospects of Indian equities. At the beginning of the year, we were also expecting a healthy 18% EPS growth for our model portfolio, propelled by favourable tailwinds. However, a plethora of global factors unseated these tailwinds and we are poised to end the year with a negative Nifty return.

2015 - YEAR IN CHARTS

BY ANINDYA BHOWMIK

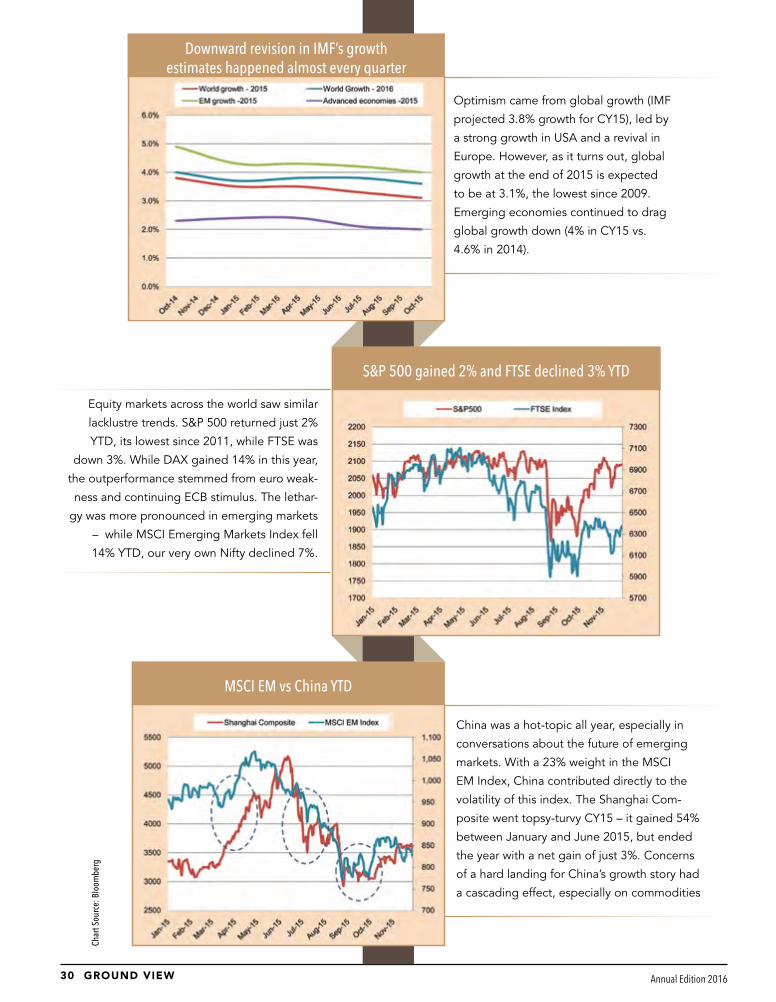

31GROUND VIEW GROUND VIEW Annual Edition 2016 Annual Edition 201630

China was a hot-topic all year, especially in

conversations about the future of emerging

markets. With a 23% weight in the MSCI

EM Index, China contributed directly to the

volatility of this index. The Shanghai Com-

posite went topsy-turvy CY15 – it gained 54%

between January and June 2015, but ended

the year with a net gain of just 3%. Concerns

of a hard landing for China’s growth story had

a cascading effect, especially on commodities

MSCI EM vs China YTD

Downward revision in IMF’s growth estimates happened almost every quarter

Optimism came from global growth (IMF

projected 3.8% growth for CY15), led by

a strong growth in USA and a revival in

Europe. However, as it turns out, global

growth at the end of 2015 is expected

to be at 3.1%, the lowest since 2009.

Emerging economies continued to drag

global growth down (4% in CY15 vs.

4.6% in 2014).

Equity markets across the world saw similar

lacklustre trends. S&P 500 returned just 2%

YTD, its lowest since 2011, while FTSE was

down 3%. While DAX gained 14% in this year,

the outperformance stemmed from euro weak-

ness and continuing ECB stimulus. The lethar-

gy was more pronounced in emerging markets

– while MSCI Emerging Markets Index fell

14% YTD, our very own Nifty declined 7%.

S&P 500 gained 2% and FTSE declined 3% YTD

Char

t Sou

rce:

Blo

ombe

rg

31GROUND VIEW GROUND VIEW Annual Edition 2016 Annual Edition 201630

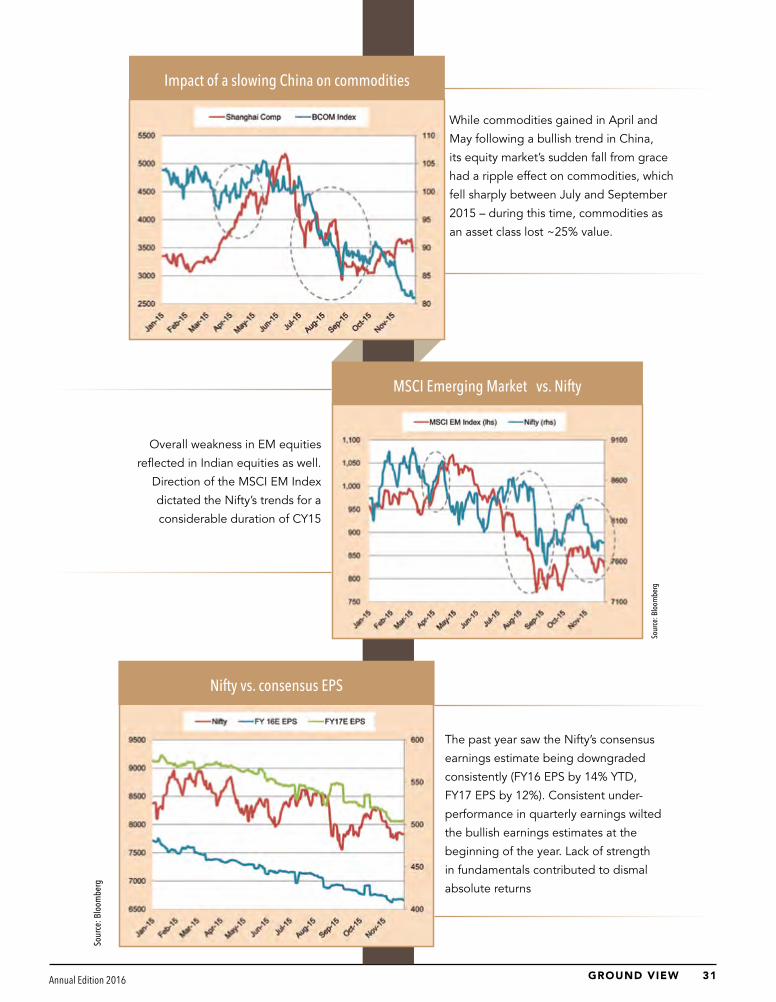

Impact of a slowing China on commodities

The past year saw the Nifty’s consensus

earnings estimate being downgraded

consistently (FY16 EPS by 14% YTD,

FY17 EPS by 12%). Consistent under-

performance in quarterly earnings wilted

the bullish earnings estimates at the

beginning of the year. Lack of strength

in fundamentals contributed to dismal

absolute returns

Overall weakness in EM equities

reflected in Indian equities as well.

Direction of the MSCI EM Index

dictated the Nifty’s trends for a

considerable duration of CY15

MSCI Emerging Market vs. Nifty

Nifty vs. consensus EPS

While commodities gained in April and

May following a bullish trend in China,

its equity market’s sudden fall from grace

had a ripple effect on commodities, which

fell sharply between July and September

2015 – during this time, commodities as

an asset class lost ~25% value.

Sour

ce: B

loom

berg

Sour

ce: B

loom

berg

33GROUND VIEW GROUND VIEW Annual Edition 2016 Annual Edition 201632

Falling global commodity prices and

the Indian government’s prudent

fiscal policy has been able to rein in

inflation. CPI inflation has been less

than 5.5% for CY15, below the RBI’s

target at the beginning of the year of

6% by January 2016.

On the other hand, FDI flows have

been very strong this year – cumu-

lative total inflow between January

and September 2015 was US$

27bn, a strong 18% like-to-like

increase over 2014.

FDI flows (in mn USD)

Inflation vs 10 Yr yieldCh

art S

ourc

e: B

loom

berg

Net foreign equity inflow per month vs. movements in monthly Nifty chart

Foreign flows into equity started slow-

ing from the start of 2015. Net foreign

equity this year was at US$ 752mn until

November vs. ~US$ 1.5bn in 2014

33GROUND VIEW GROUND VIEW Annual Edition 2016 Annual Edition 201632

This has helped the RBI to start the easing

cycle – repo rate cuts for 2015 totalled

125bps. However, banks have been slow

in passing on the benefits – the base rate

came down by only 70bps in this period.

SBI and HDFC: Repo rate vs. base rate

Trend of new project additions (in Rs bn)

Char

t Sou

rce:

Blo

ombe

rg

Sour

ce: B

loom

berg

With the demand environment not improv-ing, the trend of new project addition has seen a marked slowdown. The strong mo-mentum seen in project announcements in the latter end of last year has seen a marked slow-down, which is understandable under the context of demand paucity.

The real-estate sector continued to

suffer in 2015 – unsold inventory

levels in eight major city regions

increased 18% yoy in terms of

area and 24% in terms of months

required to sell.

Unsold stock (msf)

35GROUND VIEW GROUND VIEW Annual Edition 2016 Annual Edition 201634

Robust tax collection in FY16 fiscal (led by windfall gains due to excise on petroleum products) at 22% yoy enabled the gov-ernment to maintain spending momen-tum. Cumulative capital expenditure has increased by 29% yoy and has been a key driver in moving the economy

Despite facing opposition, the govern-ment has been intent on passing key re-forms – although the land acquisition bill had to be scrapped from re-introduction after passing ordinance on it thrice, other key reforms in the government’s legisla-tive agenda were implemented – these include:

a Hiking FDI limits in Insurance a Coal mining billa Mines and minerals development billa Regional Rural Banks Billa Undisclosed foreign income and assets bill

GST and Real Estate Regulation Bill is also likely to be passed by the legislature in the on-going winter session.

Also, a large number of incremental re-form initiatives were undertaken this year. Prominent ones were:

a UDAYa Liberalizing FDI norms for various sectorsa E-biz portal introduction – single win-dow clearance platforma Deferring GARR by two yearsa Market-rate based gas price revision

mechanisma New exit policy for stressed private players in road sectora Increased allocation in road sector and front-loading expenditure in road constructiona Fostering competitiveness among States to excel in ease of doing busi-nessa Jan Dhan scheme to ensure financial inclusion

Key events that could sway the markets include:

• Passing the GST legislation and its speedy implementation

• Acceptance of 7th Pay Panel Recom-mendations in Budget

• Bankruptcy bill Amendment• Real Estate (Regulation And Develop-

ment Bill)• MSME Development Bill• Execution uptick under AMRUT• Revising the PPP model of infrastruc-

ture development according to Kelkar Committee report.

Notwithstanding the gloomy outlook of other emerging economies, India has been strengthening structurally and the positive momentum will definitely be carried forward next year. The economy should take longer strides in 2016, which will draw out a stronger 2016 for Indian equity markets.

Anindya Bhowmik ([email protected])

However, as the year ends, a few structural pieces

seem to be falling into place and could give a

much-needed boost to the economy in 2016.

Inventory in months

High inventory pile-up has caused new pro-

jects off-take to slow and the entire real-es-

tate-based ecosystem – builders, real estate in-

vestors, and workers – has suffered as a result.

Unsold inventory levels across the country are

now above 36 months. Only NCR region has

seen marginal decrease sequentially.

Trend in Cumulative Tax collection and Capital Expenditure

35GROUND VIEW GROUND VIEW Annual Edition 2016 Annual Edition 201634

BY DHAWAL DOSHI & NITESH SHARMAA U T O M O B I L E S

Price elasticity and premiumisation co-exist“Diwali is Diwali. I have seen 40 Diwalis and it is never different. People take loans during bad times but never stop spending in Diwali” – says a 2W, 4W and consumer electronics dealer in Nagpur.

Festive cheer was seen majorly across 10

states and 20 cities (barring a few places)

that GV visited, with strong momentum in

sales during the festive season. However,

this mood was not prevalent before the

festive season and is not likely to persist

after it. Weak monsoons, implying rural

weakness, and asset price (real estate and

gold) weakness impacted most markets while

states seeing higher infrastructure activity are

seeing strong demand pull. The prominent

theme – improving urban and weak rural

demand – continues.

Tractors: Continue to languish; strong

competitive intensity is impacting smaller

players

Deficient and inconsistent monsoon leading

to crop failures/lower yields, and oversupply

led by easy financing (highlighted in the No-

vember 2015 Ground View issue) have led to

subdued tractor volumes over the last year.

This is further exacerbated due to higher

repossessed stocks by various financing com-

panies (Madhya Pradesh market has seen

very high tractor repossessions over the last

one year; Punjab is seeing strong tractor re-

financing trends, limiting fresh sales). Dealer

interactions suggest demand revival is still

a while away with no major improvement in

demand until September 2016. Even this is

dependent on normal monsoons next year.

Increasing competitive intensity and chang-

ing terms of trade are also seen as deterrents

to dealer profitability. Credit periods offered

for down payments to be made by farmers,

exchange schemes, and price under-cutting

(Sonalika sells 15-20% cheaper compared

to its competitors across various markets) is

also seen as a deterrent to dealer profita-

bility. Few dealers said that profit pressures

and inventory pushing by few companies

Sonalika and TAFE has seen market share gainsSo

urce

: Cris

il, P

hilli

pCap

ital I

ndia

Res

earc

h

37GROUND VIEW GROUND VIEW Annual Edition 2016 Annual Edition 201636

has forced them to surrender their dealerships – four tractor dealers that GV interacted with have sur-rendered their dealerships in the last three months in Punjab and Maharashtra). Increasing competi-tive intensity is visible in TAFE and Sonalika’s market share gains even as other manufacturers are losing share over the last five years.

Two-wheelers: Contra trends visible: price elasticity and pre-miumisation co-exists

Two-wheeler industry saw contra

trends with both price elastic

market and premiumisation

coexisting. Falling farm incomes

have taken a toll on the industry

growth – a significant impact is

visible in the leader’s volumes.

After the festive season, the mood

will again be driven by income

levels in rural markets. With lower

sowing for rabi crops, retail sales

are expected to be impacted.

However, dealers that had seen a

strong growth in the festive season

are currently operating with low

inventory – therefore, it is possible

that companies will report strong

wholesale sales for a few months

ahead. Weak farm incomes have

made the markets price sensitive

– this helped Bajaj Auto (with its

CT100 and Platina) to gain market

share in quite a few places. Dull

and price sensitive markets led

HMSI to offer cash discounts (in

addition to other schemes) on

some of its motorcycles in a failed

bid to attract volumes.

The negative mood changed as

GV travelled from the agri-belts

with weak farm incomes towards

semi-urban and urban areas.

These areas are seeing rising

aspirations and premiumisation.

Product quality and features mat-

tered more than the price. Here,

Bajaj Auto’s Pulsar and Avenger

families are performing relatively

better than peers in most markets.

Dealers believe strong new-launch

momentum will continue for

Bajaj Auto with four new launch-

es including Project X by FY17.

Demand for Royal Enfield contin-

ued to be strong, but the waiting

period reduced with improving

supplies.

Scooters continue to do well with

strong demand, notwithstanding

subdued rural outlook. Activa

maintained its top position;

Jupiter came across as a strong

competitor to the incumbent with

good product quality feedback,

even from competing dealers.

Hero’s new launches (Maestro

Edge and Duet) received strong

response, but supply continues

to be a constraint. Hero’s Duet

was launched in the south; most

western and northern dealers GV

interacted with were yet to get the

first consignment. On the other

hand, Maestro Edge was yet to be

launched in the southern markets.