debut of the 2016 2017 hr systems survey results€“2017 hr systems survey results 19th annual...

TRANSCRIPT

October 25, 2016

Debut of the 2016–2017 HR Systems Survey Results

19th Annual EditionEuropean Breakouts

EmployeesService & Solution AreasApplication Services

Business Intelligence

Host & Managed Services

Infrastructure Services

Integration & Cloud Solutions

Research

Strategy

Training

Delivering industry-focused client success by providing consulting, technical, and managed services

for the deployment, management and optimization of next-generation applications and technology.

Industry FocusCommercial

Healthcare

Higher Education

Public Sector

Justice & Public Safety

Sierra-Cedar Fast Facts

Years of Leading

HR Systems Survey &

Thought Leadership

7 19 950+

5

2

Consulting

Projects

1,500+

Sierra-Cedar 2016–2017 HR Systems Survey

Over 19 years of continuous data gathering

The most comprehensive survey in the industry:

● Strategy, Process, and Structure

● Administrative and Service Delivery Applications

● Workforce Management Applications

● Talent Management Applications

● BI/Analytics/Workforce Planning Applications

● Integration and Implementation

● Emerging Technologies and Innovations

● Vendor Landscape

● Workforce and HR Expenditures

● Workforce Usage and Perception

Participate in the 20th Annual Survey Download the 19th Annual White Paper

3

Organization Sizes and Types

4

Data-Driven

Talent-Driven

Top Performers

AggregateSmall<2,500

Medium2,500–10,000

Large10,000+

High TechHealthManu-

facturing

Sierra-Cedar 2016–2017 HR Systems SurveyDemographics: All Respondents

5

Trans./Comm.

Utilities

Higher EdFinance Retail Ag. Mining.

Const.

16% 15% 14% 14%11%

9% 8% 7% 7%

Other

20.6 Million Employees/Contingents

1,528Organizations

Industries

56%

21%

23%

Avg. number of Employees = 13,551

High TechHealthManu-

facturing

Sierra-Cedar 2016–2017 HR Systems SurveyDemographics: EMEA Respondents

6

Trans./Comm.

Utilities

Higher EdFinance Retail Ag. Mining.

Const.

19%22%

7%

15%

7% 8% 9%5%

7%

Other

5.2 Million Employees/Contingents

Avg. number of Employees = 31,160

169Organizations

Industries

33%

20%

47%

EMEA

CultureStrategy Technology

Key Themes for 2016–2017 Survey Results

Relationships

HR Technology Strategy

SMB Opportunity

Enterprise HR Cloud

EE Trust & Transparency

Pathways Forward

Intelligent Systems

Outcome-Focused HR

7

Constant Change

Backlog, Pipeline, Customer Satisfaction

General Ledger, Purchasing, Budgeting, T&E Vendor Management

Project Costing, Contracts, GrantsProjects

FIN

CRM

VMS

Talent Management Excellence

Service Delivery Excellence

Administrative Excellence

Workforce Management Excellence

Workforce Optimization Excellence

SOA, API, ETL

Enterprise Content Enterprise Workflow

Network Security

Enterprise Social

Mobile Access Integration Platform

Workforce OptimizationWorkforce Planning, Workforce Analytics,

Predictive Analytics

Service DeliveryHR Help Desk, Portal

Self Service/Direct AccessEmployee Self Service

Manager Self Service

Workforce ManagementTime & Labor, Absence & Leave Management, Labor

Scheduling, Labor Budgeting, WFM Analytics,

Talent ManagementRecruiting, Performance, Learning, Compensation,

Succession, Career, Talent Profile, Onboarding, TM Analytics

Business Intelligence FoundationReporting/Visualization and BI tools

Administrative Apps Core HRMS, Roles/Competencies (Profile Mgt.), Payroll,

Benefit Admin, Embedded HR Analytics,

Sierra-Cedar HCM Application Blueprint

66%Adoption

90%Adoption

60%Adoption

51%Adoption

39%Adoption

PaaS

Enterprise Data Privacy

72%

87%

91%

91%

55%

71%

65%

67%

66%

70%

59%

59%

39%

54%

48%

51%

32%

44%

35%

39%

28%

32%

33%

36%

Application Adoption Levels by Region

WFMService DeliveryAdmin SocialBI/AnalyticsTM

9

USA

CAN

APAC

EMEA

Top 4 Major HR Initiatives By RegionEveryone is Investing 25% or More of Their Time and Resources Here

64%

41% 41%38%

66%

40% 39% 37%

Bus. Procimprovement

HR SystemsStrategy

TalentManagement

ServiceDelivery

WorldwideAverage EMEA

41%

32%

13%

14%

Updated Regularly In Development Updated Rarely No Plans

33%

27%

10%

30%

2016 HR Systems Strategy By Region

11

HR Systems Strategies Increases Value to BusinessOrganizations with a Regularly Updated HR Systems Strategy are twice as

likely to be viewed by all levels of management as contributing strategic

value, versus organizations that have no HR Systems Strategy.

2X

WorldwideAverage EMEA

Remaining Top 10 HR Initiatives By RegionNoticing What Makes Them Different

n=1,528

34%

20% 19% 18% 17% 17%

Bi/WorkforceMetrics

HR AppsIntegration

WorkforceManagement

WorkforcePlanning

All SystemsIngegration

SocialEnablement

32% 32%27% 24% 22% 22%

BI/WorkforceMetrics

Expanding toGlobal HRMS

HR AppsIntegration

SocialEnablement

ReplacingHRMS

MobileEnablement

WorldwideAverage

EMEA

Service Delivery

Core HR

Payroll

Recruiting

Onboarding

Performance

Learning & Skills

Succession

HR Analytics

Business Process Improvement InitiativesWhere do Organizations Plan to Spend Their Time?

13

7%

8%

17%

8%

20%

17%

11%

11%

10%

6%

5%are working on all HR

processes at once

16%are working on non-HR

processes (operational)

Compensation, Benefits, Rewards Administrative

Apps

Talent

Management

Workforce

Optimization

Service Delivery

Self Service/Direct

Access

2016–2017 HR Tech Spending Trends OutlookOutside the US Spending Increases Continue

6%

6%

10%

7%

39%

39%

43%

54%

56%

55%

47%

39%

2016–2017 Regional HR Technology Spending Plans

Increase DecreaseStay the Same

USA

CAN

APAC

EMEA

10% 7% 10% 7% 6% 5% 7% 8% 4% 3% 5%14% 15% 12% 16% 16%

21% 23% 23%29% 33% 37%

Payroll HRManagement

HR Generalist HR BusinessPartner

Benefits WorkforceManagement

HR ITInfrastructure

HR SystemSupport

TalentManagement

HR DataAnalytics

Learning &Development

IncreaseDecrease

Tomorrow’s HR is More Focused and AnalyticalWhat HR roles does your organization plan to increase or decrease this year?

15

24%

13%

23%16%

11% 10%18% 17%

6% 3%10%10%

25%

13%21% 20% 23%

32% 33%41% 45%

39%

Payroll HRManagement

HR Generalist HR BusinessPartner

Benefits WorkforceManagement

HR ITInfrastructure

HR SystemSupport

TalentManagement

HR DataAnalytics

Learning &Development

EMEA

WorldwideAverage

2016 The Enterprise HR Cloud ConversationExpectations are High That On Premise HRMS’s Will Decline

16

52%

43%

54%

31%

44%

35%

38%

24%

On-Premise

72%

63%

59%

50%

66%

51%

53%

41%

TM Cloud

HRMS Cloud

Payroll Cloud

WFM Cloud

SaaS/Cloud

70%

64%

81%

38%

60%

52%

59%

28%

On-Premise

68%

62%

41%

35%

57%

32%

35%

21%

TM Cloud

HRMS Cloud

Payroll Cloud

WFM Cloud

SaaS/Cloud

12 MonthsToday12 MonthsToday

WorldwideAverage

EMEA

HybridsMove ONLY TM or WFM apps to Cloud

Rip & ReplaceMove everything all at onceto the Cloud

Parallel/PatchworkCombination Licensed and Cloud Solutions

Hosting/OutsourceSingle Tenant, or BPO

Multiple Pathways to an HR Tech TransformationTodays State of Replacing HR Technology in EMEA

17

ReactiveFocused

Hig

h R

isk

Lo

w R

isk

Current State60%

more Rip & Replace

in Aggregate

Data

WorldwideAverage

Multiple Pathways to an HR Tech TransformationFuture State of EMEA Replacing HR Technology

Future Plans

ReactiveFocused

Hig

h R

isk

Lo

w R

isk

HybridsMove ONLY TM orWFM apps to Cloud

Rip & ReplaceMove everything allat once to the Cloud

PatchworkReplace asLicense Ends

Hosting/OutsourceSingle Tenant, or BPO

ParallelCombo Licensedand Cloud Solutions

EMEA Plans For Replacing HR Technologies40% of Organizations are planning to replace or evaluating options

19

49%

24% 26%

66%

12%

22%

61%

16%24%

56%

17%

27%

4XMore likely to replace a

vendor if User Experience

Score is low

19

WFM SuitePayrollHRMS TM Suite

Replace in

12–24 MonthsNo Change Evaluating

25%less likely to be

evaluating options

now

Worldwide

Average

17%

58%

12%

13%0%

17%

58%

12%

13%0%

11%

61%

13%

11%

4%

8%

53%25%

10%4%

Payroll Meets Our Needs…

HRMS Meets Our Needs…

WFM Meets Our Needs…

TMS Meets Our Needs…

Does the Technology Meet Your Current Needs?EMEA, 50% More Believe Payroll Never or only Sometimes Meets Needs

20

Always Most Times

½ Time Sometimes Never

Plans for Implementations and Upgrades

21

17%20%

13%17%

9%13%

HRMS Upgrade HRMS Replacement

8%

15%

15%22%

HRMS Upgrade HRMS Replacement

EMEA

HRMS Adoption By Size

22

1%

1%

2%

4%

5%

10%

12%

9%

7%

10%

22%

16%

31%

0%

2%

2%

4%

7%

7%

8%

9%

11%

15%

15%

22%

34%

Paycor

ADP (WN)

Ceridian Dayforce

UltiPro

Infor Cloud/Lawson

Oracle (HCM Cloud)

SuccessFactors (EC)

Oracle (EBS/JD)

ADP (GV/V)

Kronos WFC WFR

Workday

SAP (HCM)

Oracle (PS)

Today 12 months

1%

2%

5%

9%

7%

10%

5%

6%

10%

7%

24%

2%

25%

1%

3%

5%

6%

7%

5%

4%

9%

12%

11%

18%

4%

27%

Today 12 months

12%

15%

6%

13%

3%

2%

4%

3%

18%

5%

15%

3%

6%

12%

15%

5%

12%

2%

2%

2%

3%

18%

5%

11%

3%

7%

Today 12 months

HRMS Adoption– EMEA

23

1%

3%

2%

3%

3%

10%

6%

11%

21%

12%

16%

19%

1%

3%

2%

2%

4%

7%

8%

8%

16%

14%

17%

26%

Epicor

Ceridian Dayforce

Meta4

UltiPro

Kronos (Combined)

Oracle (HCM Cloud)

Oracle (EBS/JD)

Workday

SuccessFactors (EC)

ADP (WN/GV/Vantage)

Oracle (PS)

SAP (HCM)

Today 12 months

Ve

nd

or

Sa

tis

fac

tio

n

User Experience

Good Enough

Zone

We Expect More!

Zone

24

Workday

Ceridian DF

UltiPro

SF (EC)

Oracle

(HCM C)

SilkRoad

Kronos

WFC

Oracle PS

ADP

(WN)

Infor/Lawson

SAP (HCM)

Oracle EBSADP (V)

ADP GV/E

Paycor

Kronos WFR

SumTotal SS

Administrative

Good Excellent

Dis

sati

sfi

ed

Very

Sati

sfi

ed

Poor

High and Low Vendor Satisfaction DriversAre We Forgetting About the Customization Needs?

25

32% 33% 35% 35% 37%

User Experience Ability toCustomize

IntegratedSolution

Best PracticeFunctionality

Service &Support

Top Benefits Correlated with High Vendor Satisfaction

21% 21%25%

38%

66%

Updates/Upgrades

High Costs Not Integrated Lack ofInnovation

Poor UserExperience

Top Challenges Correlated with Low Vendor Satisfaction

40%Greater than

Last Year

Payroll Adoption By Size

26

0%

1%

2%

3%

3%

4%

4%

3%

4%

4%

5%

7%

12%

19%

17%

23%

0%

1%

1%

2%

3%

3%

3%

4%

5%

5%

8%

8%

8%

17%

17%

28%

Paycor

SuccessFactors (EC)

NG HR (Preceda/Moore)

Oracle (HCM Cloud)

Ceridian Dayforce/HR

Ultipro

HR BPO (NG, Aon, Infosys)

Kronos WFR

ADP (Vantage)

Infor/Lawson

ADP (WN)

Oracle (EBS/JD)

Workday

SAP (HCM)

ADP (GV)

Oracle (PS)

Today 12 months

1%

1%

1%

2%

8%

10%

1%

3%

8%

2%

3%

2%

18%

3%

8%

21%

1%

0%

1%

7%

7%

1%

4%

7%

4%

3%

3%

12%

4%

7%

21%

Today 12 months

18%

1%

0%

2%

8%

15%

1%

4%

5%

2%

22%

0%

10%

2%

3%

4%

17%

0%

0%

1%

7%

13%

0%

5%

4%

2%

21%

1%

7%

2%

3%

5%

Today 12 months

Payroll Adoption – EMEA

27

1%

1%

3%

3%

2%

3%

2%

4%

4%

4%

5%

5%

1%

5%

7%

12%

10%

22%

26%

1%

1%

1%

1%

1%

1%

2%

2%

3%

3%

3%

3%

4%

5%

5%

7%

8%

12%

22%

Unit 4

Epicor

Workday

Ceridian Dayforce

Aggregators…

HRO/BPO

Raet

Ramco

Oracle (HCM Cloud)

Ultipro

SuccessFactors (EC)

ADP (Vantage)

CeridianHR

Oracle (EBS/JD)

NGA HR (P/M/R)

ADP (WN)

Oracle (PS)

ADP (GV)

SAP (HCM)

Today 12 months

Higher Cloud Adoption = More Needs Met?

28

31%24%

20% 21%17%

8% 9% 8%

Payroll HRMS WFM TMS

Our HR Systems Always Meets Our Needs

High Cloud Low Cloud

JAN FEB MAR APR MAY JUN JUL AUG SEP OCT NOV DEC JAN FEB MAR APR

Implementations Timelines Continue to Decrease40% decrease in all Implementation timelines in the last 3 years

Length of Time for New HRMS Deployments In Months

Large Licensed On-premise = 15.5 Months

Large SaaS = 13 Months

Medium Licensed On-premise = 11.1 Months

Medium SaaS = 11.4 Months

Small SaaS = 6.9 Months

HRMS + An average of 2.0 other HR modules implemented

HRMS + An average of 2.1 other HR modules implemented

HRMS + An average of 1.9 other modules implemented

Small Licensed On-premise = 7 Months

Updates and Upgrades

SaaS HRMS Update Average # of Weeks

Week

1

Week

2

Week

3

Week

4

Week

5

Week

6

Week

7

Week

8

Large = 6.0 Weeks

Medium = 6.7 Weeks

Small = 3.8 Weeks

JAN FEB MAR APR MAY JUN JUL AUG SEP OCT NOV DEC

Large = 7.6 Months

Medium = 6.6 Months

Small = 5.3 Months

Licensed HRMS Upgrade Average # of Months

30

2016 Change Management Practices By RegionEMEA Better Prepared for Cloud with Change Management Practices

33%

34%

25%

8%

Consistent culture of change mangement Key projects that meet criteria Sporadically, with no criteria Never

31

27%

38%

27%

8%

Change Management Increases Strategic Value of HROrganizations with a Culture of Change Management are twice as likely to

be viewed by all levels of management as contributing strategic value,

versus organizations that never use change management.

4X

WorldwideAverage EMEA

35%43%

65% 47%

EMEA Aggregate

Enterprise Integration Strategy?

2016 Integration Strategies MatterIn Implementation Years, Integration Costs can reach 40% of Expenditures

32

10%

5%

8%

24%

14%

39%

None

Other

Integrationplatform

Into TM Suite

Into core HR

Case by Case

EMEA Approach to Integrating HR Technology

38%Spend 10–25% of

their HR Technology

budgets on

Integration

Yes or Developing No Strategy/Unknown

Data Privacy & Protection StrategiesIn EMEA only 40% of Organizations Feel Prepared in this Area?

10%

30%

46%

15%

EMEA Data Privacy Process Maturity

Transformational

Effective

Efficient

Noprocess/Manual

High Cloud

21%more likely to be

confident in Data

Privacy processes

EMEA

What Is HR Analytics?

Business Intelligence/HR AnalyticsHRMS Embedded HR Analytics solutions Reach Tipping Point

11%25% 21% 24%

34%

55%

40%

98%

DedicatedHR/BI

Solutions

BI VisualizationTools

StatisticalTools

Emb TMAnalytics

Emb WFMAnalytics

Emb HRMSAnalytics

Platform BISolution

Microsoft Excel

If they have a BI/HR analytics solution, what is in use?

39%of Organizations are doing

some form of BI/HR Analytics

with one of these tools

38%increase in Adoption

from last year

n = 681

35

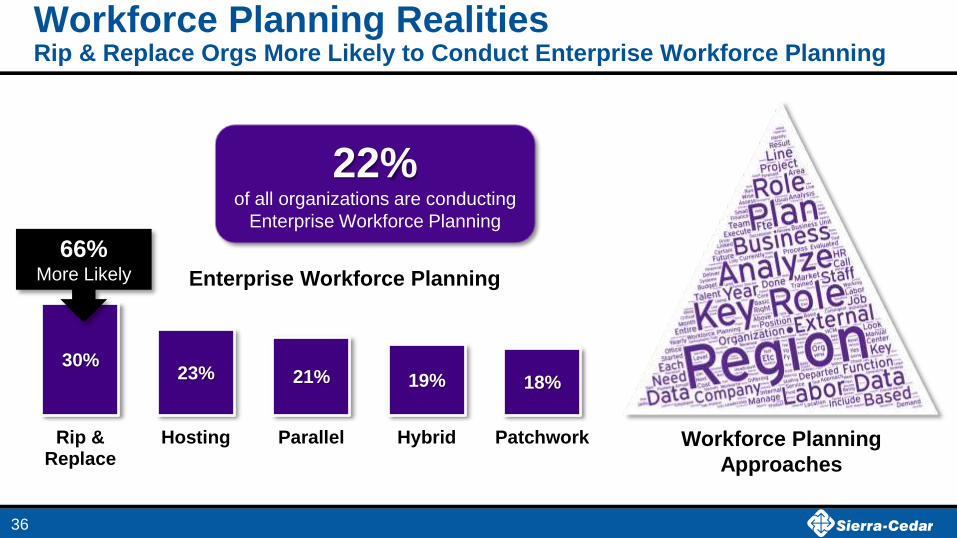

Workforce Planning RealitiesRip & Replace Orgs More Likely to Conduct Enterprise Workforce Planning

30%23% 21% 19% 18%

Rip &Replace

Hosting Parallel Hybrid Patchwork

Enterprise Workforce Planning

36

66%More Likely

22%of all organizations are conducting

Enterprise Workforce Planning

Workforce Planning

Approaches

Modern HR Changes EverythingRethink Implementations, Change Management, and Cost Assumptions

37

Traditional OnPremise World Modern Cloud World

=/< 25% implementation done by SIs

takes 25% longer and costs more

=/> 60% implementation done by SIs

is 20% faster & within budget

Licensed 2X more likely to conduct BPI efforts

before Implementation Work vs SaaS

8% lower UE and VS scores

10% lower Business Outcome averages

4X more likely to be viewed as contributing

strategic value to their organizations

SI’s Extra Hands & Extra Work SI’s Strategic Partners

Negotiate Lowest Cost Negotiate Better Relationships

Project-Based Change Management Continuous Change Management

Cloud Tech, 1½X more likely to

Always Meet Needs

IT = 8%, Ops = 9%, HR = 15%

% Expenditures & Budgets Allocated % Expenditures & Budgets Allocated

IT = 7%, Ops = 5%, HR = 24%

2016 Business Systems: On the Move to Cloud25% Increase in Organizations Evaluating Cloud Solutions from Last Year

38

31%

17%

17%

17%

15%

7%

7%

5%

10%

8%

14%

17%

15%

21%

19%

48%

59%

63%

52%

58%

Sales/CRM

OperationsSystems

MarketingSystems

FinancialSystems

VendorMgmt

Non-HR Systems in the Cloud Today?

Cloud in 12–24 Months EvaluatingCloud today No Plans

38%

13%

19%

16%

13%

7%

8%

6%

4%

8%

21%

17%

26%

23%

23%

34%

62%

49%

58%

57%

Sales/CRM

OperationsSystems

MarketingSystems

FinancialSystems

VendorMgmt

WorldwideAverage EMEA

Worldwide

Average

Mobile-enabled HR Process Adoption Overall Mobile Adoption Has Doubled in the Last Three Years

39%47%

Organizations that UseMobile-enabled HR Technology

39

2016 12 Months

33%40%

Organizations that UseMobile-enabled HR Technology

2016 12 Months

EMEA

Social Continues to Grow in EMEATwitter Hits 50% in Aggregate, and 30% in EMEA, & New Tools Show Up

40

Strategic Use in 12 months

No plansNot allowedEvaluating Use

Strategic Use Today Individual use only

0%

3%

15%

34%

39%

46%

43%

66%

65%

2%

3%

3%

7%

9%

3%

7%

8%

9%

9%

12%

22%

21%

13%

18%

23%

14%

16%

4%

7%

2%

3%

9%

4%

1%

4%

25%

29%

25%

19%

7%

14%

20%

3%

60%

45%

33%

16%

22%

14%

5%

11%

2%

Tumblr

Snapchat

Corporate SN

YouTube

Collaboration

Social Tools Use and Plans

Strategic Social Technology Use by GenerationsOne of the Only Areas Where Differences Show Up in Technology Adoption

71%

64% 65%

55%

48%

42%

35%

11% 5%

Older Workforce Equal Generations Younger Workforce

41

Ve

ry

Va

lua

ble

No

Va

lue

So

me

Va

lue

The Value Placed On Emerging Tech FeaturesEMEA Values Them More Than Aggregate

42

Voice Interface Robotics/Artificial Intelligence

Experience API Gamification/Badges

PredictiveAnalytics

EMEA

Worldwide

Average

Wrapping Up: Takeaways

Enterprise HR Systems Strategy, You Need One

Multiple Pathways to the Modern HR Tech Environment, but

Payroll and Workforce Management Solutions need addressed to

reach an Enterprise HR Cloud

Vendors and Buyers Need to Build Stronger Relationships in this

new HR Future.

Emerging Technology is about Achieving Outcomes

43

Thank you!

44

Visit Sierra-Cedar Website Get Full Survey Details and Sign Up To Participate Next Year!

45

www.Sierra-Cedar.com/annual-survey

Sierra-Cedar 2016–2017 HR Systems SurveyDemographics: International and Global Organizations

78%

4%12%

6%

Global37%

Non-Global

63%

The average global organization

has operations in over

25different countries.

335Organizations with

HQ outside the US

550Global Organizations

46

High TechHealthManu-

facturing

Sierra-Cedar 2016–2017 HR Systems SurveyDemographics: EMEA Respondents

47

Trans./Comm.

Utilities

Higher EdFinance Retail Ag. Mining.

Const.

19%22%

7%

15%

7% 8% 9%5%

7%

Other

5.2 Million Employees/Contingents

Avg. number of Employees = 31,160

169Organizations

Industries

33%

20%

47%

EMEA

Survey Methodology

Sierra-Cedar follows rigorous standards in the form of a nine-step survey

methodology, independently validated in 2011 by the Mercer Survey Quality

group. Each year, this annual reach provides a wealth of knowledge that is

shared openly with the HR systems community. All participants are kept strictly

anonymous, and only aggregate data is used.

48

Stacey HarrisVice President Research and Analytics, Sierra-Cedar

Background:

● Oversee the Annual HR Systems Survey and its safekeeping for the Industry

● HR and OE Practitioner for over 10 years in finance, retail, and franchised businesses.

● Director of Research at Bersin & Associates, Launched the HR research practice

● VP of Research for Brandon Hall Group

● Major Research and Papers: The High Impact HR Organization, The HR Framework, Employee Engagement: A Changing

Marketplace, and Relationship Centered Learning

● Feel free to connect at: www.linkedin.com/in/staceyharris

● @StaceyHarrisHR

Metrics tell such a great story and are fabulous for supporting proposed

initiatives. The data provided underscored what we have been hearing and

seeing as trends in HR—especially as they relate to social media.

Leslie KrugHRIT

Why Organizations Participate?

● To obtain a personalized benchmarking snapshot filtered by size, region, or industry

● They like conducting a review of their own enterprise HR system environment annually

● They need data to build their own HR Technology strategy or business case for change

● They believe it is important to support the broader HR technology community

50