dealers business journal january 2015

DESCRIPTION

Independent Dealers, BHPH, Buy Here-Pay Here, Car Sales, Dealer OperationsTRANSCRIPT

www.DealerBusinessJournal.com DEALER BUSINESS JOURNAL | JANUARY 2015 | 1

What do you resolve?Make a plan that will guarantee you keep your New Year’s Resolutions this year.

Part of the processSound processes are the common link between all successful BHPH dealerships.

JANUARY 2015DealerBusinessJournal.com

2 | JANUARY 2015 | DEALER BUSINESS JOURNAL www.DealerBusinessJournal.com

www.DealerBusinessJournal.com DEALER BUSINESS JOURNAL | JANUARY 2015 | 3

CONTENTSVOLUME 12, ISSUE 1 JANUARY 2015

LEEDOM GROUP FEATURES LEGAL4 A Very Happy (and Prosperous) New Year to All! Predictions for 2015 point to a strong year for the dealer

community, so make sure you are dialed in to your business. By Chris Leedom

8 It’s Time to Invest in Training and Compliance With government regulation at an all time high, you

can’t afford not to stay on top of what’s happening in the industry.

By David Brotherton

12 What do you Resolve? Breaking New Year’s resolutions is as much a tradition as

making them for most people. Build a strategy that will ensure your success for 2015.

By Rick Boucher

16 Part of the Process The second installment of a three-part series, this time

we focus on putting processes in place that will put your dealership on the right track.

By Paxton Wright

20 BHPH World Convention 2015 Early registration is now available for the best industry

event on the planet. Get your first glimpse at this year’s agenda and registration info.

24 Know When to Fold Deal Jackets can leave

behind several tells that a dealer’s operations are non-compliant.

By Tom Hudson

26 House of Cards Make sure your credit

reporting house is in order.

By Eric L. Johnson

LEADERSHIP28 Make Each Day a

Masterpiece Five steps to outlining a

plan to reach your goals. By Dave Anderson

32 How’s Your Aim? A suggested technique

on staying focused on where you want to go.

By Jay Gubrud

OPERATIONS34 Leveraging Ratios BHPH operators can

use leveraging ratios to maintain and grow.

By Robert Parnas

36 Lapsed Insurance Protect your investment

and make a profit with these ideas.

By Tim Byrd

IN EVERY ISSUE5 Calendar

6 Industry News

7 News Briefs

30 Ad Index

31 Classifieds

39 Twenty Group Application

4 | JANUARY 2015 | DEALER BUSINESS JOURNAL www.DealerBusinessJournal.com

elcome to 2015! It is exciting to be at the start of another year and our industry certainly is a buzz with opportu-

nity. Over the holiday season I have reflected as to the market landscape, challenges and opportunities present as we look forward in 2015. In past years I have used this first issue of the New Year to present some predictions. So as to not disappoint I am doing the same this year. I believe 2015 will be very interesting for dealers in general. The market landscape—particularly the finance side—is con-tinuing to heat up. For dealers working with national subprime

lenders I think the entire year will be one full of opportunity. The array of lenders serving the subprime market is as thick as it has been in quite some time. For years I talked about the pendulum that swings from BHPH to third-party lenders and it is clear the pendulum is over in the third party lender camp for now. For dealers that offer these programs I would suggest you should have a banner year. The opportunity has not been this strong since 2007. So prediction one would be that many dealers in the traditional retail space that offer subprime financing alternatives will do quite well. I believe this will be the case for at least the next 12 to 24 months. The flip side is for those dealers in the BHPH space. There is no question voluntary surrenders are on the uptick. Adverse selection could occur for dealers in certain markets. I think the challenge is for BHPH dealers to stay consistent to your model and not overreact to the market. Yes, sales volume might be down and it might decrease further. Yes losses due to voluntary surrenders have increased and will go higher. But at the end of the day many dealers have seen this cycle before. Do you think all of those customers surrendering their vehicle to you thanks to a 72 month loan on a Kia at 21 percent are going to stay there for 72 months? No, treat them right and they will be back in about three years in need of financing. I do think this adjustment is different than we have seen in the past and I also predict the repercussions will be worse for these national lenders that are disregarding current auto credits and encouraging repossessions. They are showing double digit asset growth now but I am pessimistic about the long term performance. I believe when rates start to increase or losses begin to mount we will see a handful—or more—of these companies exit the market. It has happened as least twice before. All in all, I think 2015 should be a strong year for the dealer community. The last piece of advice I would offer is to make sure you are extremely dialed in when it comes to your

business. Are your margins in line? Are expenses under control? How is your asset management? All of these items are what make great operators do well in this type of market. And I might add one of the best tools to help you do this is a Dealer Twenty Group. If you have not attended a meeting or joined a group set a New Year’s resolution to do so – then call Leedom and Associates, LLC at 941.371.7999 and request an invitation to an upcoming meeting. You will be glad you did so. Finally, Happy New Year and best wishes for 2015. I look forward to seeing you at an upcoming industry event. Best of luck and make it happen.

CHRIS LEEDOM EXECUTIVE PUBLISHER

CORNER OFFICE

“All in all, I think 2015 should be a strong year for the dealer community...Make sure you are dialed in when it comes to your business.”

WDealer Business Journal3700 S. Tamiami Trail, Sarasota, FL 34239Ph: 800.966.8733Fax: 941.371.2874Executive PublisherChristopher M. Leedom [email protected] WritersDave [email protected]

Rick [email protected]

David [email protected]

Christy [email protected]

Paxton [email protected] QUESTIONS REGARDING SUBSCRIPTIONS CALL 800.966.8733or subscribe online at DealerBusinessJournal.com

ADVERTISING INQUIRIES call 941.371.7999 or [email protected]

DISCLAIMER: The information included in this publication is obtained from sources believed reliable and has been produced with reasonable care in production and editing. It is not intended to be legal, accounting, tax, techni-cal or other professional advice. Readers are advised to consult a professional for application in their particular situation. Copyright 2015 Leedom and Associates, LLC. All Rights Reserved. Content may not be photocopied, reproduced or redistributed without written per-mission. Dealer Business Journal is a publication of Leedom and Associates, LLC.POSTMASTER: Send change of address form to Dealer Business Journal, 3700 S Tamiami Trail, Sarasota, FL 34239

www.DealerBusinessJournal.com DEALER BUSINESS JOURNAL | JANUARY 2015 | 5

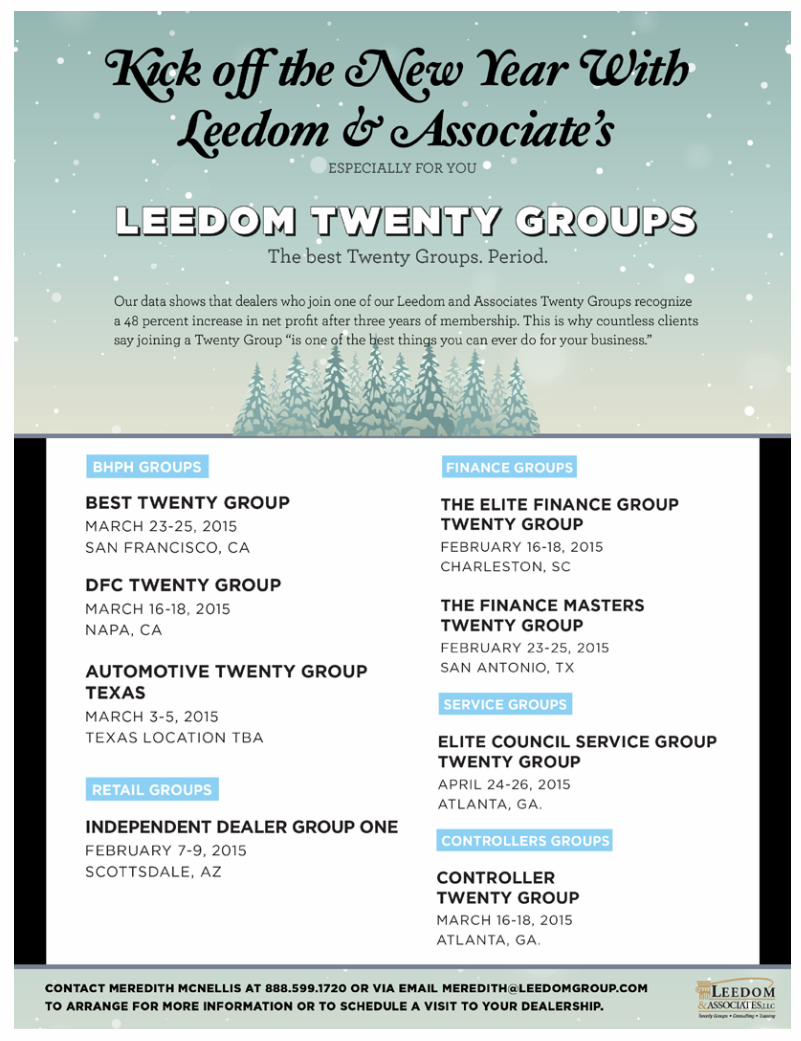

LEEDOM GROUP UPCOMING EVENTS

CALENDARAPRIL 2015

12 April | Leedom Group 21st Annual Buy Here Pay Here World ConventionThe 21st Annual BHPH WORLD Convention will be held April 12-14, 2015 in a brand new destination–New Orleans! This event is the one you

don’t want to miss. Each year hundreds of industry insiders - dealers, exhibitors, vendors and executives gather to network and get up to speed on the latest trends and best practices of the industry. This convention is consistently ranked number one for content, venue and industry expertise. We will also have a special New

Dave Anderson’s 90-Day Online Hiring Certification Course!

A dealership-changing 16 hour course!

Make it mandatory for all managers in your organization!

Call 818-735-9503 for enrollment information!

Dave Anderson

Orleans-style celebration so don’t miss out on the fun!Who Attends: Dealer-owners, Spouses, Managers and Key Staff Members, Special Finance and Buy Here-Pay Here Vendors.Location: Hyatt Regency, New Orleans, LADetails: Call 1-855-627-0809 or go to BHPHWORLD.com

Advanced GPS Tracking System

Customer Behavior Analysis Reports

Geofence Technology

Collection Tool

Secure Remote Access & Smart Phone Apps

Full Suite of Tracking Analytics

Backup Battery

Remote Engine Enable/Disable

DMS Integration

Notifications via E-mail & SMS

Live 24/7 Customer Service Support

Call us for more info

(866) 543-5433www.IturanUSA.com

®

Start improving your bottom line today!

KEY FEATURES

Keep up to Date:Stay up with all of the Leedom Group’s upcoming seminars, trainings and sepcial events. Visit LeedomGroup.com and click on Training.

6 | JANUARY 2015 | DEALER BUSINESS JOURNAL www.DealerBusinessJournal.com

DBJ INDUSTRY NEWS SEND YOUR HEADLINES TO [email protected]

INDUSTRY

Ford F-150 keeps top spot on most popular list2014 was once again the year of the truck for car shoppers, as the Ford F-150 retained its place as the most popular nameplate on AutoTrader.com across new, used and CPO ve-hicles. The F-150’s crosstown rival, the Chevrolet Silverado, was the second most popular new and CPO vehicle but it came in third behind the Jeep Wrangler on the used side. Among new cars, trucks and SUVs took seven of the top ten spots, including vehicles like the RAM 1500, GMC Sierra, Jeep Grand Cherokee and Ford F-250. Trucks and SUVs were five of the top ten used cars, and four of the top ten CPO vehicles. “The preponderance of large vehicles indicates an improving economy, as sales of pickup trucks correlate with housing starts and construction,” said Michelle Krebs, AutoTrader.com senior analyst. “Lower gas prices and many new or refreshed entries also helped boost new truck popularity, particularly in the

back half of the year.” Interest in sports cars also surged in 2014 across new, used and CPO vehicles, led by the Corvette. Shopper interest in the iconic Chevrolet grew sharply year-over-year both on the all-new model and used versions. On the CPO side, the Porsche 911 saw the most growth, moving up five places to crack the top ten most popular vehicles of the year. While trucks, SUVs and sports cars enjoyed a boom, mainstream midsize sedans underwent a bit of a bust in 2014 as more car shoppers opted to go for the bigger and faster. CPO saw the most strength in the mainstream midsize category, with the Honda Accord, Toyota Camry and Volkswagen Jetta land-ing in the top 20, but only the Ford Fusion and Honda Accord made the top 20 most popular new vehicles, and the Accord was the lone entry on the used list. “The midsize sedan seg-ment also slumped in 2014 in

terms of sales, and as a result saw the heftiest incentives,” Krebs said. “If gas prices con-tinue to stay low in 2015, it will be interesting to see if this segment remains stagnant, or if the automakers will be able to revive it with freshened products and creative market-ing efforts.” The most popular vehicles

are determined by analyzing the number of car shoppers who click on a listing for a car for sale on AutoTrader.com. This methodology goes beyond search to illustrate which cars shoppers are actively interested in learning more about, and is reflective of the actual vehicles dealers are offering for sale.

2014 MOST POPULAR USED VEHICLES

Rank Make Model Change from 2013

1 Ford F-150 0 2 Jeep Wrangler 1 3 Chevrolet Silverado 1500 -1 4 Ford Mustang 0 5 Ford F-250 1 6 BMW 3 Series -1 7 RAM 1500 0 8 Chevrolet Corvette 2 9 Honda Accord -1 10 Honda Civic -1 11 Jeep Grand Cherokee 4 12 Toyota Tacoma -1 13 RAM 2500 0 14 Chevrolet Silverado 2500 -2 15 Chevrolet Tahoe 1 16 Porsche 911/911Turbo -2 17 Toyota Tundra 5 18 Ford F-350 1 19 GMC Sierra C/K1500 5 20 Infiniti G35/37 -3

COMPILED FROM AUTOTRADER.COM

www.DealerBusinessJournal.com DEALER BUSINESS JOURNAL | JANUARY 2015 | 7

DBJ gets a new look for the new yearHave you noticed the new look for Dealer Business Journal? We are working hard to take DBJ to new levels in 2015, and we want your help to do it. Take a minute to complete our brief online survey at dealerbusinessjournal.com.

Your responses will help shape the editorial content, features, columnists and topic focus for the upcoming year. We also want to encourage dealers and vendors to send in news releases, article ideas and photos. Send submissions to [email protected],

and include News Briefs in the subject line. To put the focus on you, the readers, we also encourage sending ideas for dealer spotlights and interviews. If you have an idea for an article, send your suggestions to us. Your success is our business.

TRENDS

Car shoppers like textingTexting continues to be a preferred method of com-munication for car shoppers when it comes to buying a car and follow-up after the sale, according to a recent Mor-pace Omnibus survey. During the vehicle purchase process, consumer interest in communicating with dealerships via text mes-saging peaked in 2012 with nearly 40 percent of consum-ers being ‘very’ or ‘somewhat

interested.’ Trends over the past two years indicate con-sumers remain engaged, with 37 percent saying they were ‘very’ or ‘somewhat interested’ in the 2014 survey. Just under one-half of consumers (46 percent) are interested in receiving text messages from the dealership with information pertaining to their vehicle, such as service updates, recall notices, etc. Trends remain consistent over

the past two years, with a high of 50 percent ‘very’ or ‘some-what interested’ in 2012. The survey has been conducted by Morpace Inc., a market research and consult-ing company, annually since 2011, and asks 667 to 804 respondents, who text regu-larly, about their preferences regarding dealership commu-nication. For more details on the survey, go to morpace.com.

BRIEFSNEWS

Barnard named President of Manheim North America

Janet Barnard will take on the role as president of Manheim North Amer-ica. Barnard

previously served as executive vice president and chief oper-ating officer. In her new role, Barnard will continue to lead the com-pany’s core vehicle auction business that includes 78 op-erating locations and a team of more than 18,000 employ-ees. As a member of the Cox Automotive leadership team, she has the responsibility for strategic business functions such as Operations, Sales, Customer Experience and Product Development.

Send us your news:We want to share your news. Dealers and vendors can send press releases and news announcements about promotions, mergers, accom-plishments, new products and more by email to [email protected]. Subject line: News Briefs.

www.DealerBusinessJournal.com

DEALER BUSINESS JOURNAL | JANUARY 2015 | 1

Article Titleskjdhfjsidhfishudifhaksdhjkfs

jdImet eseque sus ni autem

laboratione

Article Titleskjdhfjsidhfishudifhaksdhjkfs

jdImet eseque sus ni autem

laboratione

JANUARY 2015DealerBusinessJournal.com

RICK BOUCHER FINANCIAL CONTROL

LEEDOM GROUP

WHATDO YOURESOLVE?

Everyone makes a New Year’s resuoltion, but few see them through to completion. The best way to get ready for the new year is to have a month-by-month plan of attack. Make your 2015 resolution be setting up a schedule that you can stick to.

E veryone always has a desire to accomplish a goal for the New Year. Setting a resolution is part of the fun and tradition. When the clock struck midnight, the number one resolution all around the world was probably to lose weight, exercise, and eat

healthy. What about a New Year’s Resolution like that, for your business? Taking the steps for your business to be fiscally fit this year requires discipline and endurance, just like it does to get your body into shape. The best weight loss plans set you up with a daily or weekly schedule of meals and exercise that are just right for your body. Your New Year’s business plan should be built the same way. Make a schedule that can be worked on all year and that will give you twelve months of accomplishment. Think of what kind of shape your dealership would be in on January 1, 2016 if you accomplished these exercises each month of 2015:

JanuarySet up goals for each department that are realistic and ones that you want accomplished

8 | JANUARY 2015 | DEALER BUSINESS JOURNAL www.DealerBusinessJournal.com

INVESTDAVID BROTHERTON BHPH BOOT CAMP

IN TRAINING AND COMPLIANCE

IT’S TIME TO

No one is too big or too small to take the chance they will not get caught in the crosshairs of the CFPB. A dealer’s best bet is to spend the time, energy and expense to ensure full compliance.

www.DealerBusinessJournal.com DEALER BUSINESS JOURNAL | JANUARY 2015 | 9

LEEDOM GROUP

I’ve had the opportunity over the last six months to participate in several meetings and seminars involving increasing

government regulation in general and the CFPB’s assault on the BHPH industry in particular. While I fully understand that lawyers don’t make money unless they scare you, please understand that I am scared. While I am concerned for the industry as a whole, I’m more concerned for the dealers who only pay lip-service to compliance and training and think they can continue to get by doing things the same old way. Times have changed. State and Federal regulators are all gunning for ways to make a splash and are looking for ways to get their pound of flesh.

At this point, I’m sure that most readers of Dealer Business Journal have heard about the Drive Time settlement but there have been various consent orders issued recently against sub-prime lenders like First Investors Financial Services Group and Consumer Portfolio Services that impact our industry as well.

First Investors Financial Services GroupFirst Investors had to pay the CFPB a $2.75 million civil penalty relating to inaccurate credit reporting traced back to a failure in third-party software it had purchased. What is important for everyone to understand is that First Investors was not able to deflect liability by blaming a third party software provider. The

CFPB felt they should have had adequate oversight to make sure that consumers’ credit information was being reported accurately.

Consumer Portfolio ServicesThe FTC got into the act with Consumer Portfolio Services (CPS) who agreed to refund or adjust 128,000 consumer accounts by more than $3.5 million and pay an additional $2 million in civil penalties due to perceived violations of the Federal Trade Commission Act (FTC Act), Fair Debt Collection Practices Act (FDCPA) and the Fair Credit Reporting Act (FCRA). Multiple violations of both laws were alleged including:

•Disclosing the existence of debt to third parties

•Calling customers at work when not permitted to do so

•Debiting customers bank accounts without authorization

•Charged fees not allowed for in the Retail Installment Contract and Security Agreement

•Limited some customers to payment methods that included a service fee earned, in part, by CPS

•Caller-ID spoofing

•Inaccurate credit reporting

•Failed to investigate consumer credit disputes

Drive TimeNot to be outdone, the CFPB came back with a whopping

10 | JANUARY 2015 | DEALER BUSINESS JOURNAL www.DealerBusinessJournal.com

$8 million fine against Drive Time Automotive Group for various collection and credit reporting-related violations including:

• Harassing borrowers at work

• Harassing borrowers’ references

• Making excessive, repeated calls to wrong numbers

• Providing inaccurate repossession information to credit reporting agencies

• Failing to properly handle credit information furnishing disputes

•Not having good enough procedures to ensure they were reporting accurate information

Eight million is a lot of money, even if you are as big as Drive Time. The CFPB made their splash. They got their pound of flesh. Something alarming about all of this is that Drive Time was obviously held to the same standard as CPS – even though

DAVID BROTHERTON BHPH BOOT CAMP

Drive Time originates their own contracts and, as such, is not covered by the FDCPA. While this may be true enough, the CFPB has indicated in its statements that it intends to apply FDCPA to all creditors and will consider it a potential violation of UDAAP (Unfair, Deceptive or Abusive Acts and Practices) and can mandate its inclusion that way.

What you need to doAt this point, we are going to need a lawyer just to sort out all of acronyms but you can rely on this: times have changed and our operations are being held to a higher standard. This applies to everyone. Period. It is time to invest in training in compliance instead of just

talking about it. It is time to do the following:

Invest in a Compliance Management SystemYou have to have one and you really do get what you pay for. Once you have the system, you actually have to use it as well.

Forms ReviewHave your forms reviewed by outside counsel familiar with both state and Federal lending laws on a regular basis. Your DMS programs what you give it. It’s your fault if it isn’t right.

TrainingComprehensive and consistent training should be implemented across the board to equip your team with the knowledge

and oversight necessary to be confident that their actions are appropriate and within the scope of the many regulations we find ourselves held to these days. Don’t look for ways to skirt the issues…look for ways to excel while staying compliant. All of the presentations I’ve been a part of recently have really made an impression. I’ve already completely rewritten our Collector’s Boot Camp to bring it up to standard with what we now all face and we can expect compliance and training to be a regular part of Twenty Group meetings for the foreseeable future. We can still succeed in our business. We simply have to make sure we understand what the rules are that we must live by.

David Brotherton is a consultant and Twenty Group moderator with the Leedom Group Contact him at [email protected]

Times have changed and our operations are being held to a higher standard.

This applies to everyone. Period. It is time to invest in training and compliance

instead of just talking about it.

www.DealerBusinessJournal.com DEALER BUSINESS JOURNAL | JANUARY 2015 | 11

12 | JANUARY 2015 | DEALER BUSINESS JOURNAL www.DealerBusinessJournal.com

RICK BOUCHER FINANCIAL CONTROL

WHATDO YOURESOLVE?Everyone makes a New Year’s resuoltion, but few see them through to completion. The best way to get ready for the new year is to have a month-by-month plan of attack. Make your 2015 resolution be setting up a schedule that you can stick to.

Everyone always has a desire to accomplish a goal for the New Year. Setting a resolution is part of the fun and

tradition. When the clock struck midnight, the number one resolution all around the world was probably to lose weight, exercise, and eat

healthy. What about a New Year’s Resolution like that, for your business? Taking the steps for your business to be fiscally fit this year requires discipline and endurance, just like it does to get your body into shape. The best weight loss plans set you up with a daily or weekly schedule of meals and exercise that are just right for your body. Your New Year’s business plan should be built the same way. Make a schedule that can be worked on all year and that will give you twelve months of accomplishment. Think of what kind of shape your dealership would be in on January 1, 2016 if you accomplished these exercises each month of 2015:

JanuarySet up goals for each department that are realistic and ones that you want accomplished

www.DealerBusinessJournal.com DEALER BUSINESS JOURNAL | JANUARY 2015 | 13

LEEDOM GROUP

14 | JANUARY 2015 | DEALER BUSINESS JOURNAL www.DealerBusinessJournal.com

FebruaryReview and analyze the previous year’s operational results. Were you satisfied with what you found out?

March Review personnel and praise those who deserve it. For those who need more guidance, instruct them and present a clear layout of what is expected.

April Review sales, underwriting and repo’s for the first quarter, committing the time to really dig into it.

May Inspect and test your compliance procedures to make sure policy and procedures are being followed.

June Do an in-depth review and analysis of your Collection Department. Spend a great amount of time with you collection manager and dissect your collection operation.

July This should be the financial review month. Spend the necessary time with your CFO and dissect the first six months and then project the next six months.

AugustTime for vacation. You’ve earned it.

SeptemberReview your January goals with all managers to discuss their accomplishments and or shortfalls

October Meet with your professional accountants and lawyers for year-end preparation for both personal and business.

November Departmental preparation for year-end including inventory requirements for New Year.

DecemberBe thankful for the staff that has aided you all year, the ability to make wise decisions and above all being in good health and the desire for success.

Follow these steps and your new year will be more than happy. It will be profitable!

Rick Boucher is a professional Twenty Group Moderator and consultant with over 30 years of experience in the auto business. Rick has owned and operated dealerships and served as CFO for several large BHPH organizations. He provides outsourced “CFO/Controller” services for small to mid-sºize dealerships. As a Certified Public Accountant, he also provides consulting services relating to finance and accounting. Contact him at [email protected]

RICK BOUCHER FINANCIAL CONTROL

Make a schedule that can be worked on all year and will give you twelve months of accomplishment. Your new year will be more than happy—it will be profitable!

www.DealerBusinessJournal.com DEALER BUSINESS JOURNAL | JANUARY 2015 | 15

CLAconnect.com/dealerships

FIND OPPORTUNITYTune up your tax plan with professionals who aren’t afraid to get their hands dirty.

Advisory Outsourcing Audit and Tax

©20

15 C

lifton

Lars

onAl

len

LLP

It’s time to changeyour approach to F&I complianceWITH THIS SPECIAL OFFER...

Subscribe to Spot Delivery and, at no additional charge, we will send you a copy of your choice of any of our legal compliance books, CARLAW, CARLAW IIStreet Legal or CARLAW III Reloaded.

To order, visit us atwww.counselorlibrary.com/offer/spot

or call us at 877-464-8326.Also follow us on:

Join Dealer Business Journal and the Leedom Group in 2015 to reach the best and brightest stars of the business. Call 800-966-8733 ext 3 or email [email protected] for a copy of the 2015 Media Kit.

16 | JANUARY 2015 | DEALER BUSINESS JOURNAL www.DealerBusinessJournal.com

PAXTON WRIGHT DEALER OPERATIONS

PROCESSPART OF THE

The second installment of a three part series on enhancing your people, process and product.

www.DealerBusinessJournal.com DEALER BUSINESS JOURNAL | JANUARY 2015 | 17

LEEDOM GROUP

In part 1 of “Enhance your People, Process, and Product,” we focused our attention on the value of people.

Having the right people, in the right job, is critical to your businesses success. In the December 2014 issue of Dealer Business Journal, I offered practical insights on hiring, developing and retaining your people. Maximizing the performance of your people can have a significant, positive impact on your dealership’s productivity and bottom line.

Just as I stated last month, my objective is to motivate each of you to do the following: • Ask yourself the tough questions. • Honestly evaluate your dealerships “Three P’s.” • Be brave enough to take action and make changes By doing so, you can get on track to creating a more efficient and profitable dealership! In this editorial, the second of a three part series, I’d like to shift the focus away from people and onto process.

ProcessWhen evaluating the most successful BHPH dealerships, those with large portfolios, market share, and profits, they tend to have one thing in common: sound processes. It is incredibly important to refine and solidify your sales, underwriting, and collections processes before you ever begin to think about growth. I can tell you from experience, one of the biggest mistakes I see dealers make, is growing too fast. With accelerated growth comes the challenge

of adapting new, and enhancing old, policies and procedures. The key is to establish clearly defined and documented processes. The dealers that do this well, and get it right the first time, are able to repeat their processes and thus their results, over and over again. These are the kinds of dealerships that succeed in the long term. For numerous BHPH dealers (and many of my customers) their focus is almost always on the number of sales or the sales process. In fact, I can hear them now, “Without

18 | JANUARY 2015 | DEALER BUSINESS JOURNAL www.DealerBusinessJournal.com

the sell there is nothing to collect.” Certainly, we all agree that without selling a car and originating a loan, there is no payment to be collected. I’m willing to concede that point, if you are willing to concede, that selling a car is generally the easiest part of the BHPH process. Depending on your underwriting policies and down payment requirements, a loan approval can become a virtual certainty for the customer. However, for the dealer, there is no certainty that the payments will be collected. So, if only for a moment, allow me to rearrange your priorities and place improving the collections process right at the top. After all, cash flow is the heartbeat of your business. If you are successful at developing a solid and repeatable collections process, you will always have cash coming in, even when sales are down. Tackling the specifics of how best to collect your portfolio of loans, isn’t really practical in this forum. Almost every dealership manages their delinquency and charge-offs differently based on their capital structure. For example, dealers with limited cash

flow, have a tendency to be less patient with customers and repo more frequently than a dealer with a line of credit that permits loans to remain in their borrowing base up to 45 days past due. Instead, ensure that your collections process includes the constant monitoring of Key Performance Indicators (KPIs), those that provide immediate feedback and deliver the best results. While refining your collections process through the utilization of KPIs, be sure to establish baselines, thresholds, and targets for each indicator. Make certain the KPI data is verifiable and be transparent with the outcomes. Sharing results with your collections team will pay huge dividends in the long run. When employees clearly understand the strategic goals of your organization and how they can contribute to attaining those goals, good things tend to happen. While there are countless key performance indicators you could adopt for monitoring the effectiveness and efficiency of your collections process, contact me directly to identify the KPIs best suited for your business. Next month, we will take a close look at the

third and final “P,” product. Once your people and processes are dialed-in, you must fill your lots with the right product in order to maximize your portfolio’s profitability. Understanding your local market, competition, and customer is essential in determining the right mix of inventory and pricing. Simply put, in the BHPH world, your inventory plays a vital role in the type of customers you attract, the number of cars you sell, the performance of your portfolio, and ultimately, the profits or losses of your dealership.

Paxton Wright is a professional Twenty Group Moderator and consultant with over 10 years of experience in lending, finance and BHPH operations. Paxton has worked with numerous lenders and understands BHPH financing and how to fund BHPH dealerships. He has deep operational knowledge and consults on an array of topics including credit facilities, asset sales, portfolio performance as well as general dealership operations. He is a recognized industry leader and has been featured at numerous national conventions as a speaker. Contact him at [email protected]

If you are successful at developing a solid and reputable collections process, you will always have cash coming in, even when sales are down.

PAXTON WRIGHT DEALER OPERATIONS

www.DealerBusinessJournal.com DEALER BUSINESS JOURNAL | JANUARY 2015 | 19

20 | JANUARY 2015 | DEALER BUSINESS JOURNAL www.DealerBusinessJournal.com

www.DealerBusinessJournal.com DEALER BUSINESS JOURNAL | JANUARY 2015 | 21

22 | JANUARY 2015 | DEALER BUSINESS JOURNAL www.DealerBusinessJournal.com

SUNDAY APRIL 12TH

VENDOR SPOTLIGHTS 1:00 PM - 4:00 PMThese sessions provide a unique opportunity to learn more about some of the best products and services in the industry. Our presenters are hand-picked and there are multiple sessions available. From compliance to software to Twenty Groups these sessions allow you to gather information and ask questions about top rated products and services.

FIRST TIME ATTENDEE MEET AND GREET 5:00 PM - 5:30 PM

WELCOME RECEPTION 5:30 PM - 8:00 PM

MONDAY APRIL 13TH

BREAKFAST 7:30 AM - 9:00 AM

GENERAL SESSION 9:00 AM - 12:00 PMChris Leedom, President, Leedom GroupOur Convention Chairman and Founder will offer our key note address. Mr. Leedom is recognized as one of the foremost authorities in the BHPH business. Chris is both an industry expert and a dealer-owner so he has a unique perspective on the marketplace. He will share with our convention attendees how the market is changing, the impact of third party lenders, and how to compete for the long haul. Since 1995 his comments have served as a bellweather of what is to come.

Jim Jackson, CEO—Oak Motors, IndianaWe have invited Jim Jackson to speak to our general session attendees. Jim has served as the CEO of Oak Motors, a large BHPH operation based in the Indianapolis market. Jim is unique in that he has served as a coach to many dealers in the industry and now is a sitting CEO. He will offer his thoughts and observations on what it takes to operate in the BHPH business at the highest levels. What drives peak performance? How do you motivate your team and custoemrs toward success?

LUNCH 12:00 PM - 1:00 PMLunch is held in our Grand Expo hall where you will have access to over 80 vendors and sponsors. These companies represent the best products and services in the business. This is another opportunity to work the Grand Expo Hall.

WORKSHOPS 1:00 PM - 4:50 PMWe will have over 20 workshops featuring leading experts, trainers and others with deep knowledge of the industry. From benchmarks to legal issues, to collections and business development concepts these ses-sions provide a plethora of opportunities to take back ideas and strategies to put to work in your business.

RECEPTION 5:00 PM - 6:30 PM

BHPH - THE BIG EASY 6:30 PM - 9:00 PMOnce again we will host a special celebration of all things BHPH. This is a chance to unwind after a long day of learning and networking with other dealers and industry insiders. This event is most defi-nitely the best party on the planet for this industry. Come join us in the Big Easy for the Big Party!

CALL NOW 1-855-627-0809 OR VISIT BHPHWORLD.COM

www.DealerBusinessJournal.com DEALER BUSINESS JOURNAL | JANUARY 2015 | 23

TUESDAY APRIL 14TH

BREAKFAST 8:00 AM - 9:00 AM

GENERAL SESSION 9:00 AM - 10:00 AMWe will feature an invited motivational/business speaker to address our attendees. Each year this is one of the most exciting sessions that offers fresh perspectives and information you can use in your business.

MIMOSA/BLOODY MARY BREAK 10:00 AM - 10:45 AM

EXPERT PANEL 11:00 AM - 12:00 PMWe will invite some of the leading experts from various disciplines within the industry to offer their thoughts on the current marketplace and to answer all of your questions. This is a live interactive session with commentary and questions flowing from the audience so come join the conversation.

SUNDAYAPRIL 12TH

MONDAYAPRIL 13TH

TUESDAYAPRIL 14TH

VENDOR SPOTLIGHTS 1:00 PM - 4:00 PM

FIRST TIME ATTENDEE MEET & GREET 5:00 PM - 5:30 PM

WELCOME RECEPTION 5:30 PM - 8:00 PM

BREAKFAST 7:30 AM - 9:00 AM

GENERAL SESSION 9:00 AM - 12:00 PM

LUNCH 12:00 PM - 1:00 PM

WORKSHOPS 1:00 PM - 4:50 PM

RECEPTION 5:00 PM - 6:30 PM

BHPH - THE BIG EASY 6:30 PM - 9:00 PM

BREAKFAST 8:00 AM - 9:00 AM

GENERAL SESSION 9:00 AM - 10:00 AM

MIMOSA/BLOODY MARY BREAK 10:00 AM - 10:45 AM

EXPERT PANEL 11:00 AM - 12:00 PM

CALL NOW 1-855-627-0809 OR VISIT BHPHWORLD.COM

24 | JANUARY 2015 | DEALER BUSINESS JOURNAL www.DealerBusinessJournal.com

KNOW WHEN TO FOLD

TOM HUDSON LEGAL OPINION

When it comes to compliance, a deal jacket can be the tell of a bad hand.

Friends who play poker tell me that sometimes they find themselves up against a player who unknowingly

betrays the cards he holds by some “tell,”—the player’s posture, facial expression, the way he holds his cards or with some other non-verbal communication. That thought came to mind recently when I was doing a compliance review of deal jackets for a dealership. I realized that whenever I ran across certain things in a deal jacket, I could “tell” that the

dealership’s compliance was not going to be up to snuff. These indicators almost never fail me. Would you care to know what they are, so that maybe you can look through a few of your dealership’s deal jackets in search of them? I’m glad to share. Here are a few examples.

Side NotesI frequently see “side notes” in deal jackets. It may be possible to use these things correctly, but I have never seen it done.

When state law permits deferred down-payments, dealers who want to accept them should reflect them in the buyer’s retail installment sales contract. Using a “note” makes no sense—the dealer is not lending money to the buyer, but rather is deferring part of the purchase price in a credit sale. Using side notes raises several state and federal disclosure issues, most of which can be resolved by including the required payments in the retail

www.DealerBusinessJournal.com DEALER BUSINESS JOURNAL | JANUARY 2015 | 25

LEGAL & LEGISLATIVE

installment sales contract. So, the use of side notes is usually a “tell.”

Financing RepairsBuy-here, pay-here dealers sometimes finance repairs to their customers’ vehicles. They tell me that it is important to keep the car running so the buyer will keep paying. Usually, this practice is done with little or no regard for the laws and regulations that apply to it. If the repairs are done by the transmission shop down the street, and the dealer pays for the repair and then “tacks it onto the end of the contract,” or adds it to the account balance, the dealer has engaged in a loan transaction that, depending on its terms, could raise state and federal disclosure issues, finance charge cap issues and licensing issues. If the repairs are done by the dealership, then the dealer is selling those repairs to the buyer on credit. Again, documentation and disclosure issues arise. In some states, the laws that apply to the credit sale of the vehicle will be different from the laws that apply to the credit sale of repairs (especially when the repairs are not “goods” but are instead are all or primarily “services.”).

Financing repairs? Always a tell.

Dueling Arbitration AgreementsWhen I see an arbitration agreement in a deal jacket, the first thing I do is look for a few more things. I’ve seen deal jackets with a “free-standing” arbitration agreement and an arbitration agreement in the retail installment sales contract, in the buyers order, and in some other document, like a GAP addendum. “What’s the problem?” you ask. “Isn’t that just a belt and suspenders sort of deal?” The problem is that all of the arbitration agreements are different, with contradictory and varying terms. A court faced with multiple arbitration agreements is likely to throw up its hands and not enforce any of them. As a result, when the dealer needs the arbitration agreement most–to pull the rug out from under a class action plaintiff’s lawyer–it isn’t enforceable. So, multiple arbitration agreements are always a tell.

Pinching Pennies, Spending Dollars This one takes several forms. Dealers are, shall we say, frugal.

They will cheerfully take someone’s copyrighted buyers order or retail installment contract to their friendly local printer and have a few thousand of them printed so they can avoid paying 50 or 75 cents a form to some forms vendor. Or, they will bring home from Twenty Group meetings forms that have been shared by other dealers in the group, roll out the copying machine and run off a batch. Often, the forms reflect the laws of other states. Then they use the forms year after year, oblivious of the possibility that the forms have become obsolete because state or federal laws, or both, have changed. When I look at the bottom left-hand corner of a retail installment contract and see a 10-year-old print date, or I see a reference on the back of a contract used by a Mississippi dealer a provision that says that the parties elect Florida law to govern the contract, that’s a tell. What’s my takeaway when I spot a tell?

I tentatively conclude that the dealer has no compliance program and has gotten no compliance advice from a competent compliance lawyer. I start asking about written policies – privacy, red flags, risk based pricing, underwriting, collections and all the rest. The usual response is that these don’t exist, and in many cases the dealer does not know that they are required. In other words, I’m looking at a dealer who, if he cannot up his game, needs to fold.

Tom Hudson, Esq. is the author of several compliance-related books that are available online at www.counselorlibrary.com. He is also the publisher of Spot Delivery®, a monthly legal newsletter for auto dealers, and the Editor in Chief of CARLAW®. Reach him by phone at (410) 865-5411 or by email at [email protected].

26 | JANUARY 2015 | DEALER BUSINESS JOURNAL www.DealerBusinessJournal.com

ERIC L. JOHNSON CFPB UPDATE

H O U S EC A R D Sof

Get your credit reporting house in order, so it won’t fall like a

I’m a huge fan of the Netflix series House of Cards and, must admit that I binge watched Season 2. The series is

coming back with Season 3 in February and I couldn’t be more excited. If you haven’t seen the show, it’s the story of Frank Underwood (played by Kevin Spacey), a Democrat from South Carolina who, after being passed over for appointment as Secretary of State initiates an elaborate plan to propel himself into the Presidency; all without a single vote. The series is primarily about manipulation, power, and how doing something bad

is ok provided it’s for the greater good. Lies, deception and betrayal are not only commonplace, they are survival traits. The episodes have many twists and turns, the writing is excellent and the characters are all deeply flawed. Frank has some great one-liners too that he’ll dryly roll out in his Southern accent such as “Let’s see if he stays with the herd or joins the pack” and “You will be cleaved from the herd and left to die in the wilderness.” Frank Underwood’s voice and words of wisdom were still fresh on my mind when I recently attended a CFPB field hearing in

Oklahoma City on medical debt collection. The CFPB took the opportunity to discuss the release of their report/study that “describes characteristics of the medical and non-medical collections tradelines on consumers’ credit reports and the processes by which they appear and disappear.” Much like in House of Cards where you’ve got to pay close attention to see the strings being pulled that much of the time you didn’t even know were there, so too must you play close attention prior to and at a CFPB field hearing. There are strings being pulled

on other CFPB regulated entities that will greatly affect Buy Here-Pay Here dealers: new required accuracy reports by the consumer reporting agencies (CRAs) to the CFPB. The CFPB only had a short paragraph in its press release that it will be requiring “major credit reporting companies to provide regular accuracy reports to the Bureau as part of ongoing examinations.” The reports are intended to highlight key risk areas for consumers including disputes filed with the CRAs. In addition, Director Cordray’s

26 | JANUARY 2015 | DEALER BUSINESS JOURNAL www.DealerBusinessJournal.com

www.DealerBusinessJournal.com DEALER BUSINESS JOURNAL | JANUARY 2015 | 27

LEGAL & LEGISLATIVE

prepared remarks only briefly mentioned the new reporting requirement. The invited speakers at the field hearing didn’t discuss the new requirement in their prepared remarks. Finally, the brief comments from the audience didn’t address the reporting requirement at all. Everyone was so focused on the medical debt collection issues and the new CFPB debt collection report that they missed the massive strings the CFPB will be pulling on the CRAs to serve up the bad actors’ heads on a silver platter. The CFPB has labeled the “accuracy reports” which the CRAs must complete a “Consumer Reporting Agency Data Request.” A sample accuracy report is available on the CFPB’s website. The information requested from the CRAs includes:

• Names of the 25 furnishers with the largest number of consumer disputes, the number of disputes received by the CRA as to each such furnisher and the number of tradelines actively reported;

• Names of furnisher industries (e.g. bank cards, student loans, collection/debt buyers, auto finance) and the number of disputes received by the CRA about furnishers in each industry;

• Names of the 10 furnishers in each industry with the largest number of consumer disputes;

• Information about the outcome of disputes (e.g. data modified, information verified, data deleted, tradelines removed); and

• Information about collection account disputes, which includes the total number of such disputes and the percentage of collection disputes by portfolio types (e.g. medical, credit card, retail, telecom).

The CFPB also expects the CRAs to do more than just complete and submit the new accuracy report form. In its press release, the CFPB states that “[i]f a credit reporting company continuously experiences an outsized number of consumer disputes about information from a particular furnisher, the CFPB expects the credit reporting agency to investigate, identify if there is a problem, and take appropriate action.” Among the actions a CRA may take includes declining to accept information from the “troubled” furnisher. Director Cordray briefly explained in his prepared remarks that access to the required reporting information on a regular

basis will “help us prioritize our work, and it will help us protect consumers even more effectively in the field.” You know what that means—if the CFPB gets that accuracy report from the CRAs that a company furnisher has an outsized rate of consumer disputes relative to its peers in a particular industry, they will do something about it. How does a shiny new Civil Investigative Demand or enforcement action sound? In your name is among the top 10 with the largest number of consumer disputes, I can easily see Director Cordray, in his

best Frank Underwood droll saying “You will be cleaved from the herd and left to die in the wilderness”. So, do you have your credit reporting and furnishing house in order or will it fall like a house of cards?

Eric L. Johnson is a partner in the Oklahoma City, OK office of Hudson Cook, LLP. He is a frequent speaker and writer on a variety of consumer credit topics. Prior to pursing his legal career, he spent many years working in various departments for his family’s car dealership. Eric can be reached at (405) 602-3812 or [email protected].

The CFPB also expects the credit reporting agencies to do more than just complete and submit the new accuracy report form. CRAs must also investigate, identify problems and take action when it receives a large number of consumer disputes from a particular furnisher.

28 | JANUARY 2015 | DEALER BUSINESS JOURNAL www.DealerBusinessJournal.com

Five steps to outlining a plan that will help your team reach your big picture goals.

Leaders of organizations spend much time giving thought to, creating, and communicating

annual visions for their enterprises; then breaking them down into monthly forecasts for their teams to achieve. These “big pictures” provide essential direction, unity, and meaning in the workplace. While longer term planning is vital, the bulk of organizational discussion focuses on the question, “Where do we want to go?” and not nearly enough on the rubber-meets-the-road proposition: “What must we execute daily to get there?” This out-of-balance approach is

MASTERPIECEMAKE EACH DAY A

somewhat understandable because vision casting and goal setting is fun, creative and inspiring. Strategic and tactical planning, on the other hand, is mundane and harder work. It requires deeper thinking, more specificity, and often results in the awakening that a change in the daily routine of people is needed; change that can bring both pain and discomfort. The reality is, in order to consistently achieve goals you’ve never reached before, your team must consistently do daily what they’ve never done before; including executing like they’ve never executed before. In short, the goal

must be to make each day a masterpiece. I first heard the mantra, “Make each day a masterpiece” from the late UCLA men’s basketball coach John Wooden. Wooden was known for his intensely structured practices that required perfecting basic drills to the point of exhaustion. Wooden famously observed, “I don’t worry about game day. We practice so intensely in-between the game days, focusing on making each day a masterpiece, the games tend to take care of themselves.” Indeed they did; Coach Wooden’s teams won ten national championships in 12 years, including an astonishing

seven in a row, and four undefeated seasons sprinkled in for good measure. Following are five thoughts for helping you and your team make each day a masterpiece: Redirect more of your focus and energy away from lag measures and to the daily lead measures that create them. Lag measures are outcomes; lead measures are the essential activities that create them. Lag measures are the result; lead measures foretell the result. There’s far too much discussion in dealerships about the “numbers” and anemic focus on managing the daily activities necessary

DAVE ANDERSON LEARN TO LEAD

www.DealerBusinessJournal.com DEALER BUSINESS JOURNAL | JANUARY 2015 | 29

to make them reality.

Identify and

communicate the key lead measures

for each position. We’re not talking 40

things, or 14 things, but the two or three things most essential for creating the desired result; the lag measure. The wrong

strategy question for reaching a

lag measure is: “What’s everything we can do to achieve the outcome?,” because you don’t have the time or energy to do everything that would contribute to the goal; and some of the activities would bring only a modicum return and siphon time from higher return lead measures. The right strategy question is: “What are the fewest battles necessary to win the war?” This narrows your focus to the highest leverage daily actions.

Outline key lead measures in PSP’s. A PSP is a Personalized Success Profile that outlines, in writing, the key lead measures each team member must execute as a daily priority. PSP’s eliminate gray areas, and provide clear direction about each day’s most important tasks. They can be updated as needed; seasonally, or in response to market shifts. PSP’s become a coaching tool for managers to help their team grow and should include: • The two or three key daily lead measures most relevant

to creating the desired lag measure.

• Essential weekly activities: these are tasks that don’t have to be done every day, but should be executed at some point during the week.

• Essential monthly activities: these are responsibilities that needn’t be done daily or weekly, but should be completed at some point during the month.

Train people to execute with excellence the lead measures you’ve outlined

30 | JANUARY 2015 | DEALER BUSINESS JOURNAL www.DealerBusinessJournal.com

in their PSP’s. If

one of your salesperson’s lead

measures is “X shown appointments” daily, your responsibility is to provide the training and support systems so he can make effective phone calls, set and confirm appointments, and follow up effectively with no-shows. In fact, as with John Wooden’s championship teams, this skill should be continually drilled on and perfected. Hold people accountable for daily execution of the lead measures you’ve outlined as non-negotiable. A lead measure is a daily behavioral

standard not a behavioral suggestion,

which means those who don’t execute it, should be quickly held accountable for their failure. At the end of the day, people do what they’re held accountable for and somewhere along the line that is going to have to involve consequences built into a system of progressive discipline that gives the required credibility to the daily tasks you have outlined as non-negotiable. In my The Five Disciplines of Execution (5DX) workshop, I present a strategy that has each team member post his or her lead measure results on a scoreboard during an early-morning Rhythm of Accountability Meeting (a five-minute, roll-call-style stand-up gathering).

“I am convinced that a more ferocious focus on identifying and executing key daily lead measures is the next step already-successful entities need to become great.”

The forum this provides for quickly recognizing those performing well, and exposing those who do not, is a cultural game-changer; especially when one understands the dynamics of reporting to, and being held accountable by, an entire team and not just the boss. The clients who have installed 5DX in their culture attest to the incredible impact it has had on focus, morale, momentum and results. Based on my experience in helping good organizations become great, I am convinced that a more ferocious focus on identifying and executing key daily lead measures is the next step already-successful entities need to become great. Any journey to greatness starts with the understanding that, when

DAVE ANDERSON LEARN TO LEAD

all is said and done attaining greatness won’t depend upon brilliance of your plan, but on the consistency of right actions; that corporate vision and monthly forecasts aren’t “destination things”; they’re daily things.

Dave Anderson is President of LearnToLead which provides in-person and virtual training to many of the world’s best dealerships. Dave speaks to dealer groups over 125 times each year and has given seminars in 15 countries. He has spoken at eleven NADA Conventions and is the author of twelve books. Follow Dave on Twitter @DaveAnderson100 and visit his website at learntolead.com for free articles and videos on sales and leadership.

CLIFTONLARSONALLEN 15

COUNSELOR LIBRARY 15

DAVE ANDERSON 5

ADVERTISER INDEX

ITURAN 5

PAYMAXXPRO 2, 31

ADVERTISING INQUIRIES CALL 800.966.8733 OR EMAIL [email protected]

www.DealerBusinessJournal.com DEALER BUSINESS JOURNAL | JANUARY 2015 | 31

Paymaxx Pro has launched 3 new ways to accept payments 24/7!• Pay by Phone• Text to Pay• Paymaxx Pay WebCall us today for details!

877-527-5658

Quality Custom Software

• Manage Inventory, Sales, & In-House

• IRS Forms 8300 &1099-C• Report customer’s credit to

major credit bureaus• Accounts receivable analysis• Paymaxx Pro Online

Payments• Passtime – Manage Tracking

Devices• RouteOne- Access to

Multiple Lenders• Banker’s Systems Plain

Paper ContractFor a free demo please call

713-827-0777 / 866-550-0777Visit our website at

www.AutoActionDMS.com

STATE OF THE ART SOFTWARE SHOULD NOT COST A FORTUNE.

Car-Ware’s DMS software provides dealer’s with advanced technology and excellent customer service. Call us today at (855) 504-5949 or visit www.car-ware.com for more details.

Serving Dealers for 25 years. Inventory, Sales,

Bookkeeping, Collections, Bi-lingual Support, Prospect Management ~ CRM

800-989-6096 carsplusdms.com

FEX DMS is the industry’s leading web-based dealer

management software solution. The BHPH

module allows dealers to service their portfolios with integrated communication

tools, from automated dialing to texting, managed

by a comprehensive queuing technology.

FEX DMS maintains the industry’s most robust EPS platform, including

the public pay portal myFEXaccount.com

WANT TO PLACE A CLASSIFIED AD?Dealer Business Journal’s Classified Ad section is an easy, and affordable, way to reach over 20,000 dealers around the country. Perfect for small vendors, dealer-to-dealer, help wanted and more. Three sizes to choose from. To place your ad call Meredith McNellis at 800-966-8733, ext. 3.

LEEDOM GROUP UPCOMING EVENTS

CLASSFIEDS

32 | JANUARY 2015 | DEALER BUSINESS JOURNAL www.DealerBusinessJournal.com

Be intentional with your performance and you will get where you want to go.

AIM?HOW’S YOUR

You don’t close your eyes when you are driving, never use your signals or pretend there

are no other drivers on the road! However, I believe, some people treat their jobs this way. They think their job and the company they work for will always be there, but this is not necessarily true. When you are driving your car, you are aiming it as you travel down the road. You have a starting point, route, and destination. As you drive each day you pay attention to your surroundings, road conditions, laws, other drivers, etc. That is how you get where you want safely and on time. The same is true in the office, each day you can successfully AIM to keep yourself there. Here is a three step technique I

recommend you think about and put into action every day!

Awareness. Be aware of what is going on around you. This is important when driving and doing business. Be curious and ask questions. Seek out what is happening in other departments, your industry, and pay attention to competitors and coworkers. Read industry publications, peruse the internet, have lunch with someone from a different department or attend association meetings for your industry. Keep your finger on the pulse of your department, company or industry. Know the size and nature of your customer base. Pay attention to your competitors, even if you are in accounting. Gain a better understanding of how your function affects other

JAY GUBRUD PERFORMANCE IMPROVEMENT

www.DealerBusinessJournal.com DEALER BUSINESS JOURNAL | JANUARY 2015 | 33

AIM?departments. If you don’t, you may end up paying the price after a shift takes place. I can’t tell you how many people have suffered in the last year because they didn’t do this.

Impeding. Are you helping things flow? Are you flexible? Are you facilitating or impeding progress, relationships or innovation? Think of that person who drives slowly in the fast lane on the highway – don’t be that person. This may require some folks to increase their self awareness and enhance their sensitivity. Make connections and get out of the way. Don’t be one of those leaders who is so set on being the center of power and influence that they are strangling the progress of their organization. Give credit to others. Be the one to connect ideas, things or people and gets out of the way.

Mutual benefit. Are you seeking to conduct yourself in a mutually beneficial way? Do you create win/win situations and relationships? Do you truly understand other people’s perspectives? One thing our company has done to create win/win situations with our clients in this

tough economic climate is to offer value added features at no cost. These are things they would have incurred addition expense in the past and helps with tighter budgets. It has been highly successful! A reasonable expectation for mutual benefit is 80 percent of the time. I believe we have to look out for ourselves sometimes (20 percent) to best serve others. If we always look out for other people more than ourselves we become martyrs. Implementing this simple technique into your everyday to-do list is easy and beneficial for you and your co-workers. It doesn’t take much to improve the contributions you’re making to the company. Your boss will take notice of the effort and your position will become even more valued.

Jay Gubrud is a catalyst for performance improvement. He is a dynamic professional speaker, trainer, author and consultant who has been presenting across industries and audiences for over seventeen years. His programs challenge participants to eliminate the everyday roadblocks to their success. Jay has an innate ability to relate the trials of life and business in a way that everyone can relate to … Cars and Driving! Find out more at www.jaygubrud.com.

PROFESSIONAL DEVELOPMENT

34 | JANUARY 2015 | DEALER BUSINESS JOURNAL www.DealerBusinessJournal.com

My last article addressed various issues relating to changing

industry and business cycles. A side topic of this related to managing numerous ratios and key data which drives the BHPH business. Some ratios relate to the measurement of leveraging of one’s operations. Many BHPH operators closely monitor different leveraging and related ratios on an ongoing basis. Financial leverage is often measured as the ratio of total debt to total assets or based upon a variation of such a computation. Essentially, many view financial leverage as a measure of the use of borrowed funds necessary to maintain or grow operations. Whether recognized or not, most BHPH operators compute at least one form of a leveraging type ratio, which is their borrowing base type ratio as defined

Buy Here-Pay Here operators can use financial leveraging ratios to maintain or grow operations.

RATIOSLEVERAGING

ROBERT PARNAS ACCOUNTING PRINCIPLES

www.DealerBusinessJournal.com DEALER BUSINESS JOURNAL | JANUARY 2015 | 35

customer notes….essentially your cost of generating a customer note will require a portion of borrowed funds or that debt is being essentially acquired to fund expenses. Also, declining profits and/or losses will reduce equity with debt levels often rising. Some operator’s distribute profits from the company, which essentially could increase debt to equity ratios or change the trends. In a nutshell, among numerous other ratios, consider documenting leverage ratios. Changes in trends may spur on the thought processes and insight regarding the reasons for changes in the company’s operations. Keep in mind that there could be a lot of reasons for trend changes, but unless you document and compute such trends, you won’t have a place to start your assessment.

Robert Parnas, CPA, is Principal, Dealerships, with CliftonLarsonAllen LLP and can be reached at [email protected].

in the finance company loan document. Most often, this is computed on a monthly basis and is essentially based on the ratio of certain customer receivables aged as stipulated in the loan agreement as a percent of funds borrowed on a credit line. The BHPH operator should track their actual borrowing base percentage trends on a monthly basis for internal management purposes. What is your monthly trend of your borrowing base percentage? This should be continually documented and reviewed. Consideration of numerous factors should be made when evaluating trends. For example, some operators may borrow up to their line limits in the interest rates are favorable to invest in their company or to pay down other debt. On the other hand, some may need to increase line borrowings if sales decrease or delinquency increases to be able to fund operations as it is often difficult to scale operations. Also, during some certain business cycles, operators will slow sales or not force sales and begin to pay down their line of credit as collections are made and purposefully “de-leverage” their borrowing base dollar amount borrowed

and monthly borrowing percentage in a strategic manner if collections are favorable. Thus, when an operator collects cash, there is a subsequent decision to either pay down debt, invest in other assets or a combination thereof. Other leveraging ratios would include total debt to equity, often considering subordinated debt as equity and not including in total debt. The operator could calculate monthly trends of debt to equity type ratios to

determine if the operation is becoming more leveraged. Total debt would likely include all unsubordinated liabilities. Some operators may analyze trends with and without including changes in invested capital during the year depending on the circumstances in order to evaluate trends. In most leveraging ratios, you would want to ensure that intercompany balances of the finance

company and sales company are eliminated, thus excluding the liability from total debt. Also, special type items are handled for management purposes, such as deferred revenue from the sale of extended service contracts, in a different fashion, perhaps adjusting such items for the internal computation to an amount approximating the estimated warranty amount. Most operators would not likely calculate such ratios if not included in

their covenants. Such ratios are important to monitor on a monthly basis and trends should be documented with other ratios commonly reviewed. Rising debt to equity ratios may be an indication that delinquency is rising and/or that collection levels are declining. Other scenarios or combinations thereof include usage of debt to acquire assets, such as inventory, equipment or

Whether recognized or not, most BHPH operators compute at least one form of a leveraging type ratio, which is their borrowing base type ratio as defined in the finance company loan document.

BUSINESS OPERATIONS

36 | JANUARY 2015 | DEALER BUSINESS JOURNAL www.DealerBusinessJournal.com

Automobile sales have traditionally been broken down into three main areas. These areas

are most clearly defined by the economic circumstances of the buyer: Primary, Secondary/Sub-Prime, and Buy Here-Pay Here. Many franchise dealers who had chosen to stick with the primary credit buyer soon found themselves expanding with a Special Finance manager in F&I. This allowed for a greater number of sales, which had been traditionally lost to “Whoever can get ‘em done!” Savvy dealers looked at this and realized that in many cases the finance companies were making more profit on the car than they were. Brick, mortar, signs, floor plan, etc...and less profit. Being the entrepreneurs that dealers are the thought of, “I can do this myself” has entered the minds of many of us. Hence, Buy Here-Pay Here and Lease Here-Pay Here offices have been springing up in franchise stores across the country. Those who have ventured into the Buy Here-Pay Here

or Lease Here-Pay Here business have discovered a very different animal than what they are use to. Although very lucrative, they are finding there are problems and challenges that are unique to the BHPH business. One of the greatest challenges is in the area of lapsed insurance. In fact, it is estimated that 50 percent of the BHPH books of business are uninsured. Most BHPH operations have a full time employee whose primary job is collection calls for lapsed insurance. Stacks of lapsed insurance notifications are on their desk. They spend hours tracking down customers trying to get them to renew their coverage. To put this in perspective, you are paying someone many man hours to call your customers and demand they go down the street and pay an insurance agent to cover your investment—and if they don’t, you’re going to repossess their vehicle. Primarily this is because the alternative of unprotected collateral is more than you can swallow. Some dealers find themselves with customers

Protect your investment and make a profit by owning a reinsurance company

INSURANCELAPSEDTIM BYRD DEALER REINSURANCE

www.DealerBusinessJournal.com DEALER BUSINESS JOURNAL | JANUARY 2015 | 37

who are paying them well, but have lapsed their insurance. So, they look the other way in hopes that nothing will happen. This is called “assuming the risk,” as well as other things. What is the solution? A collateral protection product. There are two main products available in the market place Collateral Protection Insurance or CPI, and Debt Cancellation Coverage or DCC (called Loss Damage Waiver or LDW for leases and rentals). Neither product covers liability. CPI is primarily used as a force-placed insurance product. The customer buys full coverage insurance and lets it lapse. The lender then turns to a CPI provider to protect its interests against loss and passes the cost on to the consumer. This is an insurance product and in some states you must have a Property and Casualty insurance license to sell it. Force placing a BHPH customer can be challenging at best. DCC is a waiver, like GAP is a waiver in most states. It is an insured product, but not an insurance product. Debt Cancellation Coverage cancels the customer’s loan balance (minus a deductible) if their car is totaled or stolen. It does not require an insurance license. DCC is usually sold to the customer at time of sale. In some states it would be added to the loan as a line item. In most states it would be a recurring payment collected alongside the customer’s car payment.

CPI can be purchased from a provider or reinsured. DCC is only available as a reinsurance product. Owning a reinsurance company gives a dealer the great advantage of turning a huge problem into a profit center. One reinsurance company can be used for many different products such as warranties and service contracts. One of many advantages of offering collateral protection, such as DCC, is that at point of sale the customer is onboard and the premium collected is transferred to the dealer’s dealer-owned reinsurance company trust account. Each dealer’s reinsurance company is stand alone. Only a dealer/lender’s premium goes into the trust and only the dealer/lender’s customer’s claims come out of the trust. Therefore, just like an insurance company, any premium collected that is not used to pay claims becomes underwriting profit for the stockholders (owners) of the reinsurance company. This arrangement also benefits the customer as a DCC is an agreement in which for a fee (typically less than collision insurance coverage), the lender is agreeing to forgive all the customer’s debt should their vehicle be deemed a total loss. Insurance companies rarely pay off the debt completely and can take several weeks to come to a decision. The customer can often end up with no car and still owing on their last car. When most

primary consumers have an issue with their vehicle, it is an inconvenience; however, with the BHPH customer, it can be a crisis. Being without a vehicle for an extended period of time waiting on an insurance company may force a customer to go to the next BHPH dealer down the street and buy from them, resulting in a lost customer. Owning a reinsurance company and offering DCC would allow a dealer/lender to act quickly to get the customer into another car and continue making their payments, which is the lifeblood of BHPH. In summary, there are alternatives to fighting insurance companies and customers. As a savvy entrepreneur, you realized that with your own finance company you could eliminate problems and make more profit. With a reinsurance company you can also eliminate problems and make more profit.

Tim Byrd is Founder and President of DealerRE a Tim Byrd & Associates company, a managing agency located in Gloucester, Virginia. An Auto Industry Expert on Dealer Owned Reinsurance Companies, BHPH Operations and F&I Development. A 25+ year veteran of the car business, Tim is a trusted advisor to many car dealers and can be reached at www.DealerRE.com or by calling 804-824-9533.

BUSINESS OPERATIONS

38 | JANUARY 2015 | DEALER BUSINESS JOURNAL www.DealerBusinessJournal.com

• BHPH

• LHPH

• Controllers

• Finance Company

• Retail

• Service

•• Three Meetings per Year

• Carefully Monitored Expenses

• Full Financial Composite

• Dedicated Group Assistant

It’s your dealership -- Isn’t it worth having experienced talent?

IT TAKES ATEAM

Call 1-888-599-1720,Email [email protected] or,Visit www.TwentyGroups.com

APPLYTODAY!

Seven of the last ten NIADA Quality Dealers of the Year have been or still are members of the nationally recognized Leedom Twenty Group Program.

• Best Idea Session

• Access to Training

• Expert Advice

• Consulting

• Networking

• Proprietary Online Online Forum

www.DealerBusinessJournal.com DEALER BUSINESS JOURNAL | JANUARY 2015 | 39

• BHPH

• LHPH

• Controllers

• Finance Company

• Retail

• Service

•• Three Meetings per Year

• Carefully Monitored Expenses

• Full Financial Composite

• Dedicated Group Assistant

It’s your dealership -- Isn’t it worth having experienced talent?

IT TAKES ATEAM

Call 1-888-599-1720,Email [email protected] or,Visit www.TwentyGroups.com

APPLYTODAY!

Seven of the last ten NIADA Quality Dealers of the Year have been or still are members of the nationally recognized Leedom Twenty Group Program.

• Best Idea Session

• Access to Training

• Expert Advice

• Consulting

• Networking

• Proprietary Online Online Forum

40 | JANUARY 2015 | DEALER BUSINESS JOURNAL www.DealerBusinessJournal.com