de6635-accounting unit 3

DESCRIPTION

ACCOUNTINGTRANSCRIPT

HND Accounting Graded Unit 3

DE66 35

Tutor’s Support Pack

Olive Gardiner

Adam Smith College

January 2007

© COLEG

Accounting – Graded Unit 3 Tutor’s Support Pack

Acknowledgements First published January 2007 © Colleges Open Learning Exchange Group (COLEG) – Material developed by Adam Smith College. No part of this publication may be reproduced without the prior written consent of COLEG, except as authorised in the paper entitled ‘Intellectual Property Rights of COLEG Members’.

Accounting – Graded Unit 3 Tutor’s Support Pack

Accounting – Graded Unit 3 Tutor’s Support Pack

Contents

Tutor materials 1

Introduction to unit 2

Purpose of this unit 2

Assessment 2

Unit specification and assessment exemplars 2

Introduction to this pack 3

Student materials 5

Introduction to unit 6

Purpose of this unit 6

Financial reporting 7

Basic accounts preparation – standard year end adjustments 7

Incorporating long term work in progress adjustments 15

Incorporating revaluation adjustments 20

Incorporating finance lease adjustments 24

Incorporating issues of shares 27

Disclosure 30

Conceptual matters 36

Taxation 37

Appendices 47

Appendix 1 – SSAP 9 47

Appendix 2 – SSAP 21 51

Appendix 3 – FRS 15 55

Appendix 4 – FRS 3 61

Appendix 5 – SSAP25 65

Appendix 6 – FRS 18 – Theoretical matters 67

Accounting – Graded Unit 3 Tutor’s Support Pack

Appendix 7 – Adjusting the accounting profit 82

Appendix 8 – Capital allowances 88

Appendix 9 – Calculating the CT due 97

Appendix 10 – Relief for trading losses 99

Appendix 11 – solutions to revision exercises 104

Accounting – Graded Unit 3 Tutor’s Support Pack

1

Tutor materials

Accounting – Graded Unit 3 Tutor’s Support Pack

2

Introduction to unit Purpose of this unit This Group Award Graded Unit is designed to provide evidence that the candidate has achieved the following aims of the HND Accounting:

• To prepare students for progression to further study in accounting or a related discipline.

• To develop and integrate a range of contemporary vocational skills in addition to those developed at HNC level (ie evaluating and interpreting financial data; applying relevant legislation; providing information for decision-making).

• To enable students to integrate financial accounting with relevant business taxation. Assessment Students will be assessed in this unit by a three-hour written examination and will be allowed access to a taxation text book during the assessment. To achieve this unit, students should attain 50% of available marks with achievement being graded according to marks attained. Prior to undertaking this Group Award Graded Unit, students should have completed the following HND mandatory units:

• Financial Reporting and Analysis (DE5G 35)

• Accounting for Specialised Transactions (DE5E 35)

• Business Taxation (DE5L 35) Unit specification and assessment exemplars The Unit specification will be an essential document in the delivery of the unit. Exemplar instruments of assessment with marking guidelines have been produced to provide examples of the specific evidence required to demonstrate achievement of the aims of the HND Accounting group award which this Graded Unit is designed to cover, and to indicate the national standard of achievement required at SCQF 8.

Accounting – Graded Unit 3 Tutor’s Support Pack

3

Introduction to this pack The purpose of this pack is to provide materials for use in the delivery of this Graded Unit. The main body of the student material consists of grouped revision exercises as per the contents list. Solutions are provided at the end. These are all together in one place – this was felt to be the most appropriate presentation, as they are more easily removed if you so wish. Some revision notes are included in the appendices to give easy reference for those students who have trouble remembering their original teaching materials on these topics. Those delivering the units will know to what extent they wish to make use of these. Note: Users of the pack should note that it is up to date as at the time of writing and reflects the changes in format required by the change in the Companies Act brought into force on 1st January 2005 and reflected in the version of the FRSSE at that date, whereby dividends paid during the year should be debited directly to equity and no longer be shown in the profit and loss account. The pack follows the format as laid down in the FRSSE and FRS 25, showing dividends paid in a simplified reconciliation of shareholders’ funds. It is recognised that there may be further changes in the very near future when the new Companies Act comes into force. As the Unit entitled Financial Reporting and Analysis is based on FRSSE companies, the pack also recognises:

• There is now no requirement for small companies to disclose staff numbers (financial years beginning on or after 1st January 2005).

• There is now no requirement for small companies to disclose wages and salaries, social security costs and other pension costs (financial years beginning on or after 1st January 2005).

Accounting – Graded Unit 3 Tutor’s Support Pack

4

Accounting – Graded Unit 3 Tutor’s Support Pack

5

Student materials

Accounting – Graded Unit 3 Tutor’s Support Pack

6

Introduction to unit Purpose of this unit This Group Award Graded Unit is designed to provide evidence that you have achieved the following aims of the HND Accounting:

• To prepare students for progression to further study in accounting or a related discipline.

• To develop and integrate a range of contemporary vocational skills in addition to those developed at HNC level (ie evaluating and interpreting financial data; applying relevant legislation; providing information for decision-making).

• To enable students to integrate financial accounting with relevant business taxation. Prior to undertaking this Group Award Graded Unit, you should have completed the following HND mandatory units:

• Financial Reporting and Analysis (DE5G 35)

• Accounting for Specialised Transactions (DE5E 35)

• Business Taxation (DE5L 35) You will be assessed in this unit by means of a three hour examination during which you will have access to a taxation text book. In order to achieve the unit you must obtain 50% or more of the available marks. Remember that your result in this unit will provide the grade that will appear on your HND certificate. It is therefore very important that you do yourself justice in your performance in this unit. The following material is designed to help you revise the material you have studied in the mandatory units specified above and to help you practise putting the material together, as you will have to in the examination – and of course in practice.

Accounting – Graded Unit 3 Tutor’s Support Pack

7

Financial reporting Basic accounts preparation – standard year end adjustments Revision exercise 1 The following trial balance was extracted from the accounts of Castlepark at 31st March 20X9. £000 £000 General administrative expenses 29,610 Selling and delivery costs 11,205 Opening stock 79,519 Purchases 503,500 Interest on bank overdraft 2,496 Prepaid expenses 1,729 Bad debts written off 1,755 VAT account 3,229 Trade creditors 66,465 Bank overdraft 29,960 12% debenture stock 9,975 Ordinary share capital, issued and fully paid 78,750 Profit and loss account at 1/4/X8 7,498 Share premium account 29,400 Dividend paid 4,760 Sales (excl. VAT) 608,738 Trade debtors 136,620 Accruals 1,120 Freehold land 30,000 Freehold property:

cost 31,145 accumulated depreciation @ 1/4/X8 3,189

Equipment and vehicles: cost 10,553 accumulated depreciation @ 1/4/X8 4,568

842,892 842,892 Required: From the above trial balance and the information overleaf, prepare a profit and loss account for the year ended 31st March 20X9 and a balance sheet at that date.

Accounting – Graded Unit 3 Tutor’s Support Pack

8

Additional information: 1) Corporation tax has been estimated to be £22,050,000 based on the year's

profit. 2) The 12% debenture stock was issued at the end of the year. 3) The rates to be charged for the year as depreciation are:

Freehold property 2% (of which 25% is to be charged to Administration, 50% to cost of sales and the rest to Distribution)

Equipment and vehicles 15% (of which 50% is to be charged to cost of sales and 50% to Distribution)

4) Closing stock was valued at £72,500,000. 5) Auditors’ fees of £85,000 are to be accrued. 6) The company pays its annual insurance premiums in full on the 1st January every

year. This year’s payment was for £64,000.

Accounting – Graded Unit 3 Tutor’s Support Pack

9

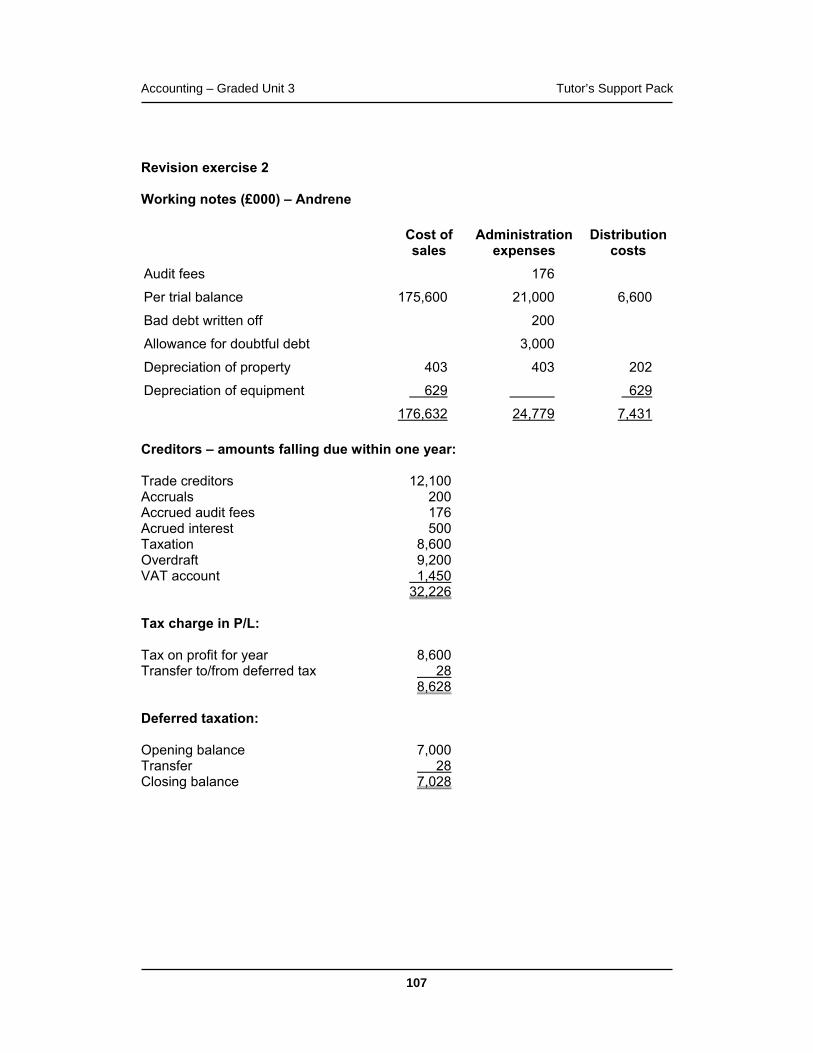

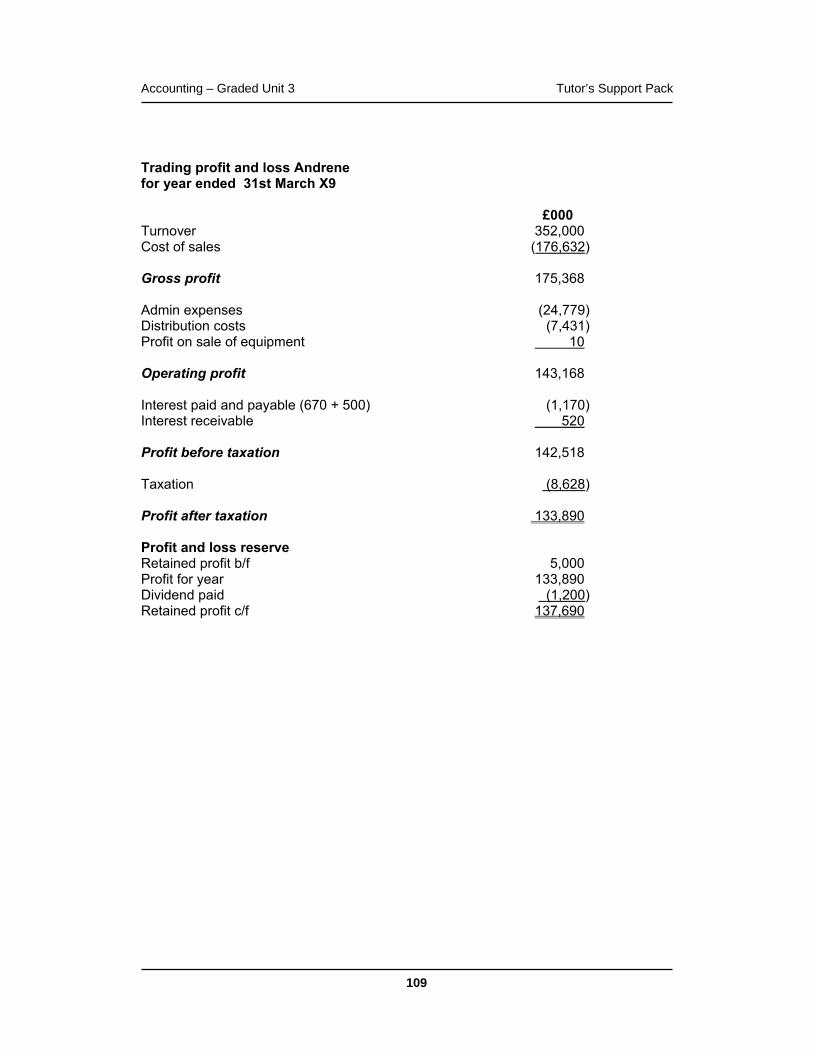

Revision exercise 2 The following trial balance was extracted from the accounts of Andrene at 31st March 20X9. £000 £000 Ordinary share capital, issued and fully paid 23,000 Profit and loss account at 1/4/X8 5,000 General administrative expenses 21,000 Selling and delivery costs 6,600 Cost of goods sold 175,600 Interest on bank overdraft 670 Prepaid expenses 1,500 VAT account 1,450 Investments 31,400 Trade creditors 12,100 Bank overdraft 9,200 Closing stock of finished goods 83,940 10% debenture stock 5,000 Share premium account 3,650 Dividend paid Nov 'X8 1,200 Deferred tax 7,000 Sales (excl. VAT) 352,000 Trade debtors 60,200 Accruals 200 Investment income (rec'd Oct 'X8) 520 Proceeds of the disposal of equipment 50 Purchase of equipment and vehicles 560 Fixed assets, NBV at 1/4/X8 36,500 419,170 419,170 Required: From the above trial balance and the information overleaf, prepare a profit and loss account for the year ended 31st March 20X9 and a balance sheet at that date.

Accounting – Graded Unit 3 Tutor’s Support Pack

10

Additional information: 1) Corporation tax has been estimated to be £8,600,000 based on the year's profit.

£28,000 is to be transferred to the deferred tax account representing the excess of capital allowances over depreciation charges.

2) The 10% debenture stock was in issue throughout the year. 3) The equipment and vehicles disposed of had a written down value of £40,000 and

originally cost £75,000.

The fixed assets at 1/4/X8 were:

Freehold property Equipment and vehicles

Cost or valuation 50,400,000 10,000,000

Accumulated depreciation 18,200,000 5,700,000 The rates to be charged for the year as depreciation are:

Freehold property 2% (of which 40% is to be charged to administration, 40% to cost of sales and the rest to distribution)

Equipment and vehicles 12% (of which 50% is to be charged to cost of sales and 50% to distribution)

4) Audit fees of £176,000 are to be accrued. 5) The accountant has decided that the amount included in debtors relating to FPB plc

(£200,000) should be written off as the company has gone into liquidation. He also considers a general doubtful debt allowance of 5% of the remaining debtors will be required to reflect the expected difficulties being experienced in the sector.

Accounting – Graded Unit 3 Tutor’s Support Pack

11

Revision exercise 3 The following trial balance was extracted from the accounts of Milton at 31st March 20X7. £000 £000 Trade creditors 42,538 Bank overdraft 19,134 Closing stock of finished goods 60,856 12% debenture stock 6,384 General administrative expenses 13,518 Selling and delivery costs 17,171 Cost of goods sold 291,040 Ordinary share capital, issued and fully paid 54,400 Profit and loss account at 1/4/X6 5,454 Interest on bank overdraft 2,698 VAT account 2,066 Investments 26,643 Share premium account 14,224 Dividend paid 3,046 Sales (excl. VAT) 378,000 Trade debtors 98,077 Accruals 475 Investment income 177 Deferred tax 11,592 Fixed assets, NBV at 1/4/X6 21,395 534,444 534,444 Required: From the above trial balance and the information overleaf, prepare a profit and loss account for the year ended 31st March 20X7 and a balance sheet at that date.

Accounting – Graded Unit 3 Tutor’s Support Pack

12

Additional information: 1) Corporation tax has been estimated to be £14,100,000 based on the year's profit.

£120,000 is to be transferred to the deferred tax account representing the excess of capital allowances over depreciation charges.

2) The 12% debenture stock was issued at par at the start of the year. 3) The fixed assets at 1/4/X6 were:

Freehold property Equipment and vehicles

Cost or valuation 19,933,000 6,426,000

Accumulated depreciation 2,041,000 2,923,000

The amounts to be charged for the year as depreciation are:

Freehold property £226,000 (of which £81,000 is to be charged to administration, £56,000 to cost of sales and the rest to selling and distribution expenses)

Equipment and vehicles £605,000 (of which £202,000 is to be charged to Administration, £134,000 to cost of sales and the rest to selling and distribution expenses)

4) The following expenses are to be accrued:

General administrative expenses £23,000

Accountancy services £35,000

Accounting – Graded Unit 3 Tutor’s Support Pack

13

Revision exercise 4 The following trial balance was extracted from the accounts of Panico at 31st March 20X9. £000 £000 General administrative expenses 14,090 Selling and delivery costs 9,980 Purchases 220,960 Ordinary share capital, issued and fully paid 34,800 Profit and loss account at 1/4/X8 4,500 Share premium account 9,600 Dividend paid 6,942 VAT account 1,650 Trade creditors 25,400 Bank 15,980 Opening stock of finished goods 57,025 10% debenture stock 4,800 Corporation tax 35 Deferred tax 807 Sales (excl. VAT) 337,450 Trade debtors 65,955 Fixed assets, NBV at 1/4/X8 28,040 419,007 419,007 Required: From the above trial balance and the information overleaf, prepare a profit and loss account for the year ended 31st March 20X9 and a balance sheet at that date.

Accounting – Graded Unit 3 Tutor’s Support Pack

14

Additional information: 1) The fixed assets at 1/4/X8 were:

Freehold property Equipment and vehicles

Cost or valuation 28,000,000 7,800,000

Accumulated depreciation 5,040,000 2,720,000 The rates to be charged for the year as depreciation are:

Freehold property 2% of cost (50% administration, 30% to cost of sales and 20% to selling and distribution)

Equipment and vehicles 16% of cost (50% to cost of sales and the rest to selling and distribution expenses)

2) Closing stock was estimated to be £85m 3) Corporation tax has been estimated to be £11,500,000 based on the year's profit.

£50,000 is to be transferred to the deferred tax account representing the excess of capital allowances over depreciation charges.

Tax paid in January 20X9 (based on the profit of 20X8) was £8,900,000 which was £35,000 more than originally estimated.

4) The 12% debenture stock was in issue throughout the year. 5) Auditors’ fees of £125,000 are to be accrued.

Accounting – Graded Unit 3 Tutor’s Support Pack

15

Incorporating long term work in progress adjustments The exercises contained in this section relate to organisations with long term work in progress. If you are unsure of the treatment, revision material is contained in appendix 1. Revision exercise 5 The trial balance for Gammon plc, extracted at 31st December 20X6 contains the following balances relating to a contract with Bilt Ltd:

Dr Cr

Bilt: contract account costs so far £450,000

Bilt: payments on account £550,000 You discover the following about the contract:

The contract was started on 1st July 20X6, and is expected to finish in November 20X7. The total contract price is £2m.

Expected costs to completion are £750,000 and the surveyor has confirmed that at the year end the contract was 30% complete. Required: Show how this contract will be reflected in the profit and loss account for the year ended 31st December 20X6 of Gammon plc, and in the balance sheet at that date. You should show all journal entries necessary.

Accounting – Graded Unit 3 Tutor’s Support Pack

16

Revision exercise 6 The following trial balance was extracted from the accounts of Acer at 31st March 20X9. £000 £000 Ordinary share capital, issued and fully paid 37,800 Profit and loss account at 1/4/x8 3,600 General administrative expenses 10,458 Selling and delivery costs 15,210 Cost of goods sold 203,280 Interest on bank overdraft 771 VAT account 1,500 Contract account 50 Investments property 10,212 Trade creditors 31,903 Bank overdraft 14,888 Closing stock of finished goods 58,956 12% debenture stock 4,000 Share premium account 9,785 Dividend paid 7,280 Directors total emoluments 270 Deferred tax 8,694 Sales (excl. VAT) 283,856 Trade debtors 73,526 Investment income 134 Proceeds of the disposal of equipment 48 Purchase of Equipment and vehicles 245 Fixed assets, NBV at 1/4/x8 16,050 396,258 396,258 Required: From the above trial balance and the information on the following page, prepare a profit and loss account for the year ended 31st March 20X9 and a balance sheet at that date.

Accounting – Graded Unit 3 Tutor’s Support Pack

17

Additional information: 1) Corporation tax has been estimated to be £10,580,000 based on the year's profit.

£90,000 is to be transferred to the deferred tax account representing the excess of capital allowances over depreciation charges.

2) The 12% debenture stock was issued at the start of the year. 3) The directors' total emoluments of £270,000 are to be charged as £222,000 to

administrative expenses and £48,000 to distribution costs. 4) The equipment and vehicles disposed of had a written down value of £75,600 and

originally cost £132,600.

The fixed assets at 1/4/x8 were:

Freehold property Equipments and vehicles

Cost or valuation 14,950,000 4,818,000

Accumulated depreciation 1,530,000 2,188,000 The rates to be charged for the year as depreciation are:

Freehold property 2% of cost (50% administration, 30% to cost of sales and 20% to selling and distribution)

Equipment and vehicles 15% of cost (50% to cost of sales and the rest to selling and distribution expenses)

5) Included in stock are 20 items made as a special order for a customer who went

into liquidation before they were delivered. As they are of a specialist nature, they can only be sold for scrap. Their net scrap value is expected to be £1,000 each, although they originally cost £2,500 each to make.

6) The contract account balance of £50,000 represents the balance of £500,000 costs

so far incurred on a long term contract and £550,000 received from the contractee. No other entries have been made in respect of this contract. The details are as follows:

Total contract value £885,000

Value of work certified £600,000

Cost of work certified £400,000

Costs to date £500,000

Estimated cost to complete £ 90,000

The directors wish to recognise attributable profit in accordance with SSAP 9.

Accounting – Graded Unit 3 Tutor’s Support Pack

18

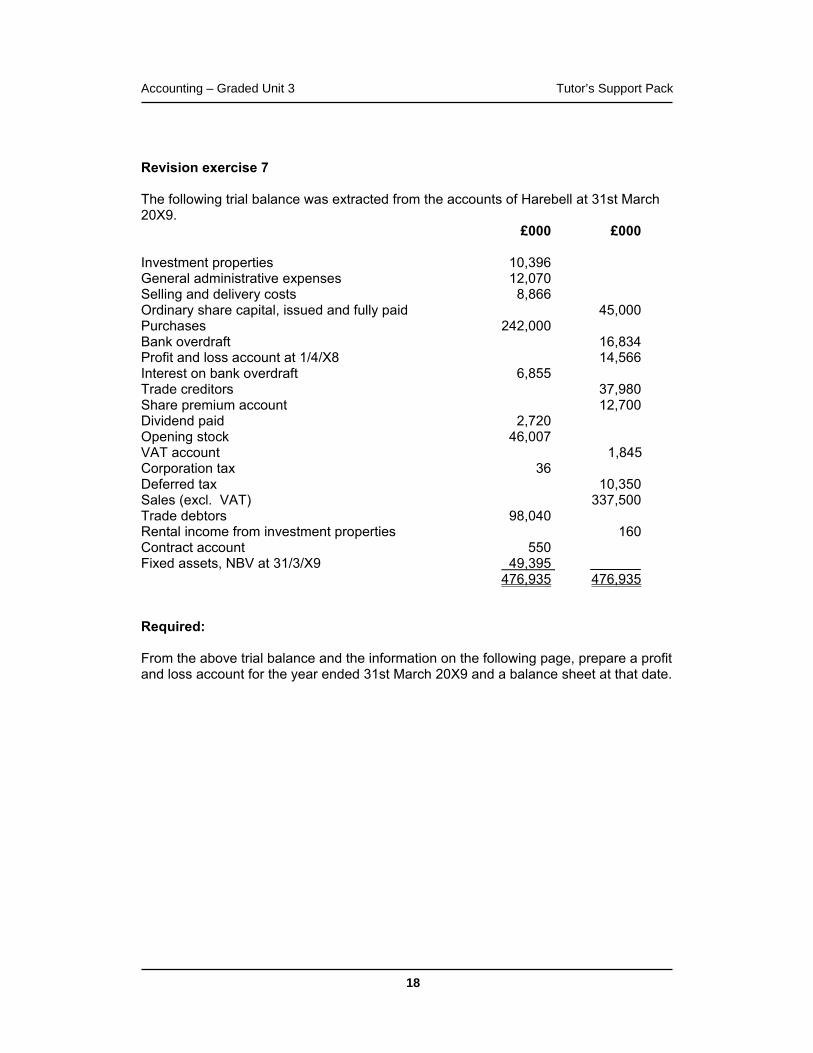

Revision exercise 7 The following trial balance was extracted from the accounts of Harebell at 31st March 20X9. £000 £000 Investment properties 10,396 General administrative expenses 12,070 Selling and delivery costs 8,866 Ordinary share capital, issued and fully paid 45,000 Purchases 242,000 Bank overdraft 16,834 Profit and loss account at 1/4/X8 14,566 Interest on bank overdraft 6,855 Trade creditors 37,980 Share premium account 12,700 Dividend paid 2,720 Opening stock 46,007 VAT account 1,845 Corporation tax 36 Deferred tax 10,350 Sales (excl. VAT) 337,500 Trade debtors 98,040 Rental income from investment properties 160 Contract account 550 Fixed assets, NBV at 31/3/X9 49,395 476,935 476,935 Required: From the above trial balance and the information on the following page, prepare a profit and loss account for the year ended 31st March 20X9 and a balance sheet at that date.

Accounting – Graded Unit 3 Tutor’s Support Pack

19

Additional information: 1) Closing stock was estimated to be £48.5m before taking account of the contract

mentioned below. 2) Harebell has one long term contract underway. The managing director wishes you

to calculate how much profit can prudently be recognised and include this in the accounts. The details are as follows:

Contract value £10m Start date 3 September 20X8

Costs so far £2.8m

Estimated costs to complete £4.0m Estimated completion Nov. 20Y0

Work certified complete £2.25m

(This last amount has been invoiced to the customer and he has paid it. It has not been included in sales however. The only entries in the books have been debits to the contract account of costs incurred, and a credit to the contract account of amount paid.) Profit is earned at a constant rate over the contract.

3) Corporation tax has been estimated to be £12,600,000 based on the year's profit.

£112,000 is to be transferred to the deferred tax account representing the excess of capital allowances over depreciation charges.

Tax paid in January 20X9 (based on the profit of 20X8) was £7,936,000 which was £36,000 more than originally estimated.

4) Audit costs of £234,000 are to be accrued.

Accounting – Graded Unit 3 Tutor’s Support Pack

20

Incorporating revaluation adjustments The exercises contained in this section relate to organisations who revalue their fixed assets in accordance with FRS 15. If you are unsure of the treatment, revision material is contained in Appendix 3. Revision exercise 8 The following trial balance was extracted from the accounts of Bensven at 31st March 20X9. £000 £000 Ordinary share capital, issued and fully paid 30,000 Profit and loss account at 1/4/X8 3,737 General administrative expenses 11,500 Selling and delivery costs 4,900 Cost of goods sold 145,823 Salaries and wages 44,440 Interest on bank overdraft 667 VAT account 1,100 Investments 10,000 Trade creditors 22,160 Bank overdraft 9,618 Closing stock of finished goods 53,517 12% debenture stock 4,000 Share premium account 7,680 Revaluation reserve 2,240 Dividend paid 2,542 Deferred tax 7,050 Sales (excl. VAT) 252,500 Trade debtors 50,216 Investment income (rec'd Oct 'X8) 220 Fixed assets, NBV at 1/4/X8 16,700 340,305 340,305 Required: From the above trial balance and the information on the following page, prepare a profit and loss account for the year ended 31st March 20X9 and a balance sheet at that date.

Accounting – Graded Unit 3 Tutor’s Support Pack

21

Additional information: 1) Corporation tax has been estimated to be £7,640,000 based on the year's profit.

£52,000 is to be transferred to the deferred tax account representing the excess of capital allowances over depreciation charges.

2) The 12% debenture stock was issued at par at the start of the year. 12% is the

market rate for this type of debt. 3) The directors believe that the debtor’s balance of £15,000 relating to a customer

now in liquidation should be written off, and a general allowance of 3% of the remaining debtors figure made.

4) The fixed assets at 1/4/X8 were:

Freehold property Equipment and vehicles

Cost or valuation 12,416,000 8,000,000

Accumulated depreciation 1,916,000 1,800,000 The rates normally charged for the year as depreciation are:

Freehold property 2% (of which 40% is to be charged to administration, 40% to cost of sales and the rest to distribution)

Equipment and vehicles 16% (of which 50% is to be charged to cost of sales and 50% to distribution)

5) Wages and salaries are to be split between cost of sales, administration and selling

and distribution in the ratio 2:2:1. 6) On the first day of the year, the property was revalued by an external surveyor at

£30m. The directors wish to incorporate this value into the accounts. The surveyors have intimated that the buildings have a further 50 years of useful economic life.

Accounting – Graded Unit 3 Tutor’s Support Pack

22

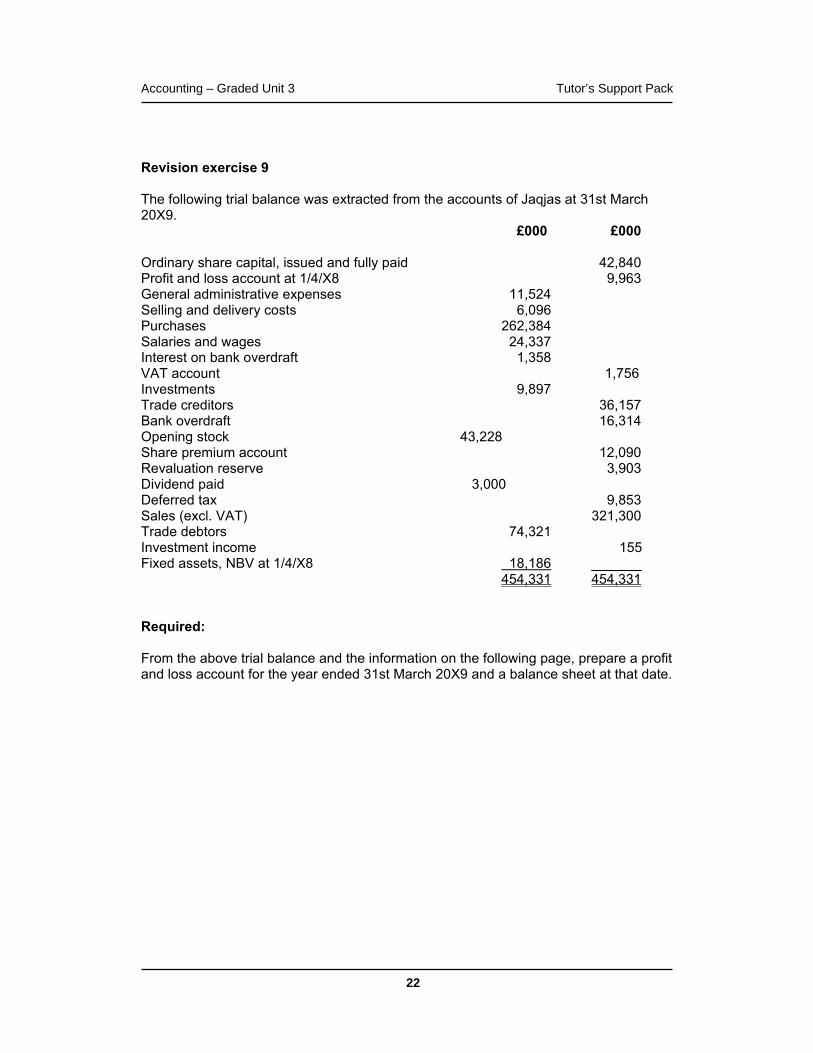

Revision exercise 9 The following trial balance was extracted from the accounts of Jaqjas at 31st March 20X9. £000 £000 Ordinary share capital, issued and fully paid 42,840 Profit and loss account at 1/4/X8 9,963 General administrative expenses 11,524 Selling and delivery costs 6,096 Purchases 262,384 Salaries and wages 24,337 Interest on bank overdraft 1,358 VAT account 1,756 Investments 9,897 Trade creditors 36,157 Bank overdraft 16,314 Opening stock 43,228 Share premium account 12,090 Revaluation reserve 3,903 Dividend paid 3,000 Deferred tax 9,853 Sales (excl. VAT) 321,300 Trade debtors 74,321 Investment income 155 Fixed assets, NBV at 1/4/X8 18,186 454,331 454,331 Required: From the above trial balance and the information on the following page, prepare a profit and loss account for the year ended 31st March 20X9 and a balance sheet at that date.

Accounting – Graded Unit 3 Tutor’s Support Pack

23

Additional information: 1) Corporation tax has been estimated to be £12,000,000 based on the year's profit.

£103,000 is to be transferred to the deferred tax account representing the excess of capital allowances over depreciation charges.

2) The fixed assets at 1/4/X8 were:

Freehold property Equipment and vehicles

Cost or valuation 16,940,000 5,462,000

Accumulated depreciation 1,735,000 2,481,000

The rates to be charged for the year as depreciation are:

Freehold property 2% (of which 45% is to be charged to administration, 35% to cost of sales and the rest to distribution)

Equipment and vehicles 15% (of which 50% is to be charged to cost of sales and 50% to distribution)

3) Wages and salaries are to be split between cost of sales, administration and selling

and distribution in the ratio 1:4:2. 4) On the last day of the year, the property was revalued by an external surveyor at

£26m. The directors wish to incorporate this value into the accounts. 5) Audit fees of £126,000 are to be accrued. 6) Closing stock was estimated to be £55m.

Accounting – Graded Unit 3 Tutor’s Support Pack

24

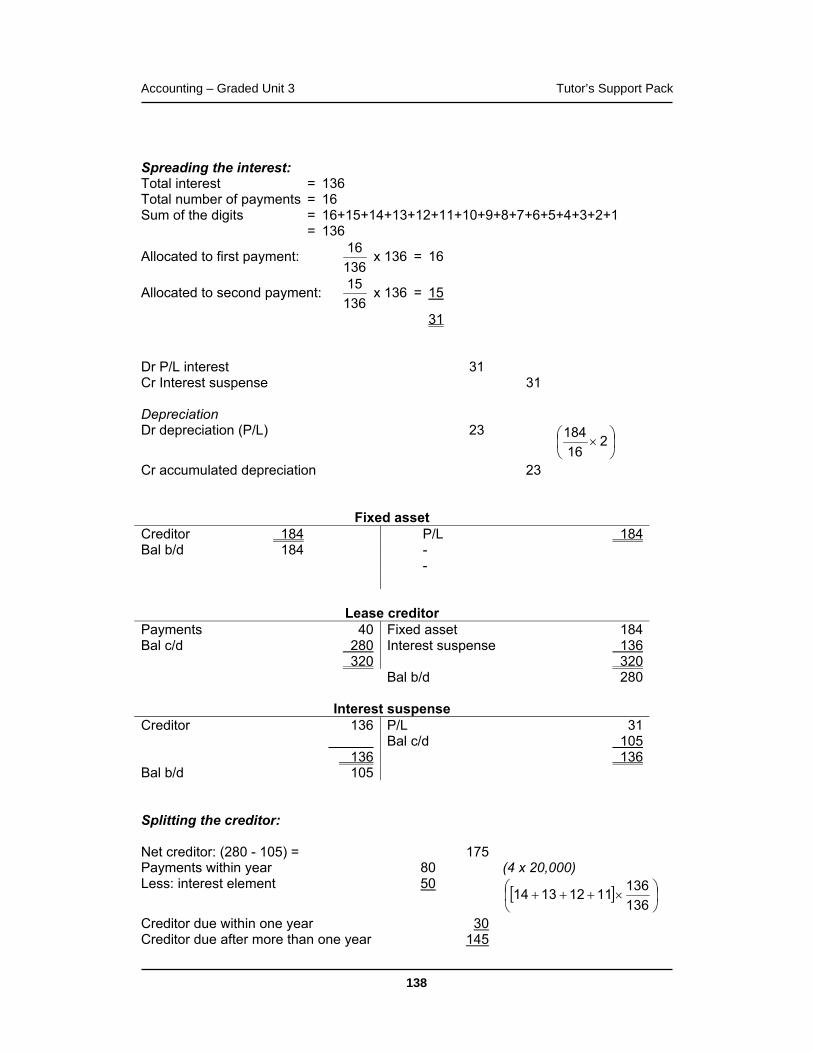

Incorporating finance lease adjustments The exercises contained in this section relate to organisations that lease some of their fixed assets and must therefore account for them in accordance with SSAP 21. If you are unsure of the treatment, revision material is contained in appendix 2. Revision exercise 10 Grant required a new computer system and decided to lease one from Bussols on the following terms:

Cash price: £15,600

Lease terms: Deposit of £3,900 on 1/4/X1 followed by two instalments of £4,680 payable on 1st April in each of the following two years and a final payment of £4,762 payable on 1/4/X4. The interest rate implicit in the lease is 10%.

Grant has decided to depreciate the computer using the straight line method over the life of the lease. Required: a) Make the necessary entries in the books of Grant for 20X1/2 and show extracts

from the Profit and loss account for the year to 31st March 20X2 and the balance sheet at that date. Spread the interest using the actuarial method.

b) Calculate the interest allocation for 20X1/2 under the sum-of-digits method.

Accounting – Graded Unit 3 Tutor’s Support Pack

25

Revision exercise 11 You are the financial accountant of ABC plc, a listed company engaged in the manufacture of garden equipment. The trial balance at 31st March 20X4 was as follows: £000 £000 Ordinary share capital (£1 shares) 8,000 15% debentures 3,000 Profit and loss account 1st April 20X3 5,670 Deferred taxation 1st April 20X3 2,500 Sales 66,980 Staff costs 17,780 Overheads 27,890 Raw materials purchases 12,255 Investments at cost 965 Amounts owing to HMRC – PAYE and NI 275 Dividends received 60 Interest paid (including debenture interest) 850 Ordinary dividend paid 530 Corporation tax underprovided 120 Bank 70 Trade debtors and creditors 29,290 13,760 Freehold land at cost 1,400 Freehold buildings at cost 800 Other fixed assets at NBV (31/3/X4) Plant and m/c 3,520 Motor vehicles 55 Fixtures and fittings 800 Stocks of raw materials 1/4/X3 950 Stocks of finished goods 1/4/X3 2,970 100,245 100,245 Required: Using the additional information provided overleaf, prepare for publication in the corporate report of ABC plc, the profit and loss account for the year ended 31st March 20X4 and a balance sheet at that date.

Accounting – Graded Unit 3 Tutor’s Support Pack

26

Additional information: 1) Staff costs are apportioned 7:1:2 between the production, distribution and

administration functions respectively. 2) Overheads are split as follows: £000

Production 19,200

Distribution 6,610

Administration 2,080 27,890

Production overheads include two instalments in respect of plant and machinery acquired on 1st October 20X3 under a finance lease. The terms of the lease require sixteen quarterly instalments of £20,000 payable in arrears. The fair value of the machinery on 1st October 20X3 was £184,000. The company wishes to use the sum of digits method to account for the lease.

3) In the past, the company has not depreciated its freehold buildings. From 1st April

20X3, depreciation is to be provided retrospectively on these buildings. The buildings were acquired on 1st April 20X0 and have an estimated useful life of 40 years from that date. The depreciation is to be apportioned 80% production and 20% administration.

4) The estimate of £4,200,000 provided for corporation tax payable on the profits of

the previous year was agreed at £4,320,000 and this was paid on the due date. Taxation on the profits of the current year is estimated at £3,000,000.

5) Stock at 31st March 20X4 totalled £3,990,000. 6) The balance on the deferred taxation account at 1 April 20X3 relates to timing

differences due to the difference between capital allowances and depreciation. The required provision based on cumulative timing differences was £1,800,000 at 31st March 20X4.

7) The debentures are redeemable in two equal annual instalments commencing on

30th March 20X5.

Accounting – Graded Unit 3 Tutor’s Support Pack

27

Incorporating issues of shares The exercises contained in this section relate to the accounting for the issue of share capital. If you are unsure of this aspect of your studies, revision notes are contained in Appendix 4. Revision exercise 12 Biscabee have the following shareholders’ funds at 1st January 20X7:

Ordinary share capital (£1 ordinary shares) 150,000 Share premium 75,000 Profit and loss account 560,000 785,000 On 2nd January, the directors decide to make a bonus issue of 1 share for every 3 held. They wish to do this in a way that maximizes distributable profit. Following the bonus issue, the directors decide to raise much needed funding for expansion by means of a rights issue on 5th January. The terms of the issue were as follows:

Two shares at £3.50 each for every 5 shares held. The rights issue was taken up by all shareholders. Required: Prepare journal entries to record the bonus and rights issues, and show the shareholders funds as they would appear on a balance sheet at 5th January, assuming no further profit or loss has arisen.

Accounting – Graded Unit 3 Tutor’s Support Pack

28

Revision exercise 13 The following trial balance was extracted from the accounts of Nordheim at 31st March 20X9. £000 £000 Trade debtors 106,560 General administrative expenses 30,161 Salaries and wages 229,485 Bad debts written off 1,332 VAT account 1,920 Investment property 24,000 Trade creditors 74,640 Ordinary share capital, issued and fully paid 103,200 Profit and loss account at 1/4/X8 20,944 Bank 23,118 Closing stock of finished goods 72,600 8% debenture stock 4,800 Share premium account 3,755 Selling and delivery costs 10,968 Cost of goods sold 600,770 Dividend paid 2,880 Sales (excl. VAT) 912,025 Investment income 360 Suspense account 7,950 Proceeds of the disposal of equipment 144 Purchase of equipment and vehicles 1,584 Fixed assets, NBV at 1/4/X8 26,280 1,129,738 1,129,738 Required: From the above trial balance and the information on the following page, prepare a profit and loss account for the year ended 31st March 20X9 and a balance sheet at that date, including as far as possible, from the information provided, the necessary notes to the accounts.

Accounting – Graded Unit 3 Tutor’s Support Pack

29

Additional information: 1) The 8% debenture stock was issued at the end of the year. 2) Corporation tax has been estimated to be £5m based on the year's profit. 3) The equipment disposed of had a written down value of £180,000 and originally

cost £216,000.

The fixed assets at 1/4/X8 were:

Freehold property Equipment and vehicles

Cost or valuation 14,160,000 32,160,000

Accumulated depreciation 2,040,000 18,000,000 The rates to be charged for the year as depreciation are:

Freehold property 2% (of which 30% is to be charged to administration, 40% to cost of sales and the rest to distribution)

Equipment and vehicles 20% (of which 50% is to be charged to cost of sales and 50% to distribution)

4) Wages and salaries are to be split between cost of sales, administration and selling

and distribution in the ratio 5:3:2. 5) The suspense account represents the cash proceeds of an issue of shares. 4m £1

ordinary shares were issued on 1st January 20X9. No entries have been made in the accounts other than to debit the bank and credit the suspense account with the proceeds.

Accounting – Graded Unit 3 Tutor’s Support Pack

30

Disclosure Revision exercise 14 Belco plc started the year with tangible fixed assets with a net book value of £328,000, made up as follows:

Freehold land cost £90,000

Buildings cost £200,000 accumulated depreciation £20,000

Plant cost £70,000 accumulated depreciation £28,000

Vehicles cost £26,000 accumulated depreciation £10,000 During the year, the land was revalued to £120,000 as a result of a survey by ABC Chartered Surveyors and Co. Other transactions for the year included:

• New plant was acquired at a cost of £50,000

• A vehicle that had originally cost £10,000 and had been depreciated at 20% per year on cost for 3 years was sold for £3,000

• A new vehicle was acquired for £15,000. Belco’s depreciation policy is to charge a full year’s depreciation in the year of acquisition and none in the year of disposal. The rates used as:

Buildings: 2% per annum on cost

Plant: 15% per annum reducing balance method

Vehicles: 20% per annum on cost Required: Prepare the fixed asset schedule and associated notes for Belco plc.

Accounting – Graded Unit 3 Tutor’s Support Pack

31

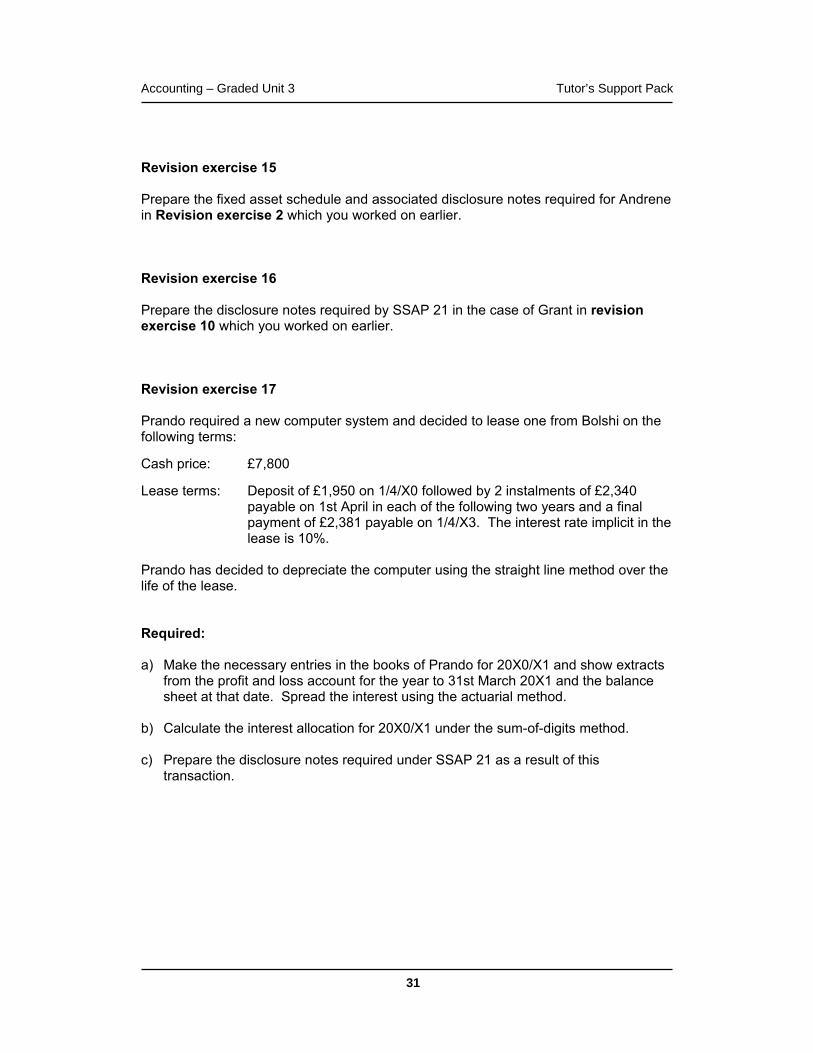

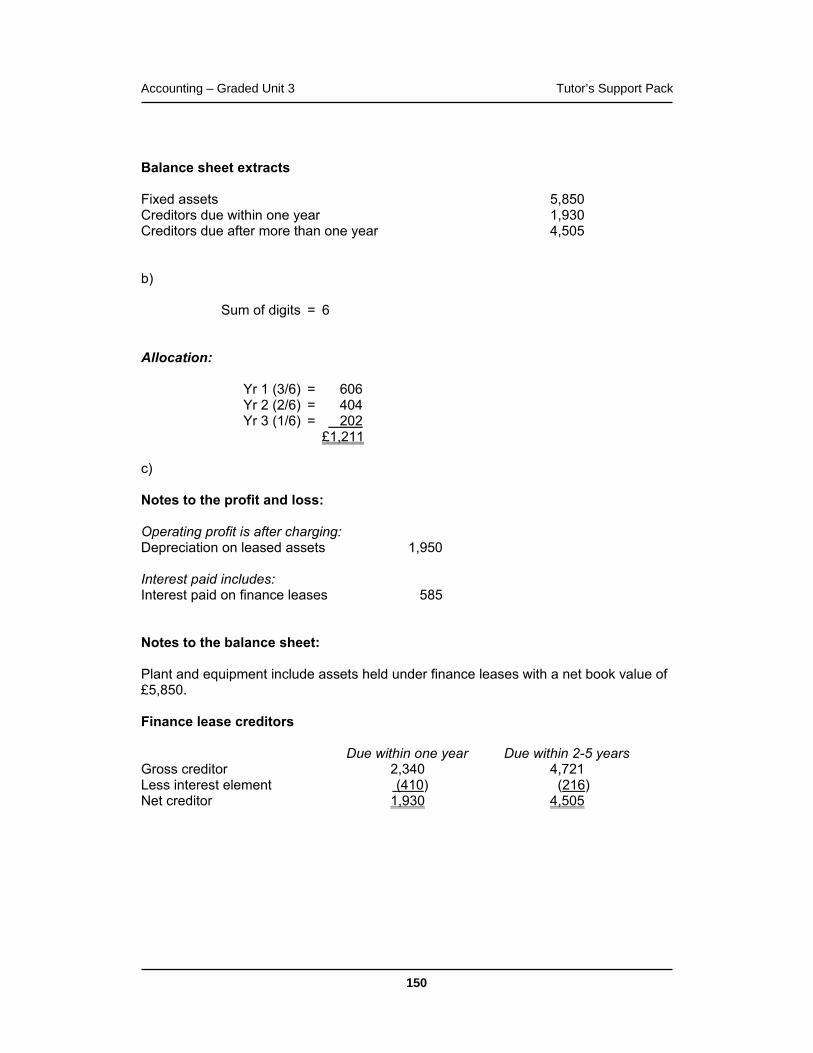

Revision exercise 15 Prepare the fixed asset schedule and associated disclosure notes required for Andrene in Revision exercise 2 which you worked on earlier. Revision exercise 16 Prepare the disclosure notes required by SSAP 21 in the case of Grant in revision exercise 10 which you worked on earlier. Revision exercise 17 Prando required a new computer system and decided to lease one from Bolshi on the following terms:

Cash price: £7,800

Lease terms: Deposit of £1,950 on 1/4/X0 followed by 2 instalments of £2,340 payable on 1st April in each of the following two years and a final payment of £2,381 payable on 1/4/X3. The interest rate implicit in the lease is 10%.

Prando has decided to depreciate the computer using the straight line method over the life of the lease. Required: a) Make the necessary entries in the books of Prando for 20X0/X1 and show extracts

from the profit and loss account for the year to 31st March 20X1 and the balance sheet at that date. Spread the interest using the actuarial method.

b) Calculate the interest allocation for 20X0/X1 under the sum-of-digits method. c) Prepare the disclosure notes required under SSAP 21 as a result of this

transaction.

Accounting – Graded Unit 3 Tutor’s Support Pack

32

Revision exercise 18 The accounts of Biscabee include the following figures: Cost of sales Depreciation of production machinery: owned £85,000 Depreciation of production machinery: leased £24,000 Raw materials used £125,000 Labour costs £140,000 Sundry materials £54,000 Pension contributions on behalf of employees £12,500 Hire of specialist equipment £6,785 Utilities £12,870 Amortisation of development costs £4,500 Research costs £6,000 Administrative expenses Depreciation of office equipment (all owned) £35,000 Labour costs £70,000 Pension contributions £6,750 Stationery £10,453 Telephone £2,560 Insurance £1,400 Directors’ fees £15,000 Audit fees £35,000 Distribution costs Depreciation of fork lift trucks (all owned) £25,000 Labour costs £45,000 Pension contributions £3,750 Sundry expenses £10,000 Required: State which items must be disclosed individually in the notes to the accounts and prepare, as far as the information permits, a suitable disclosure note.

Accounting – Graded Unit 3 Tutor’s Support Pack

33

Revision exercise 19 Biscabee’s stock figure at the end of the year is £450,000. Biscabee is a manufacturing organisation and this figure includes raw materials, work in progress and finished goods in the proportion 2:3:4. Biscabee revalue their head office property every three years in line with the requirements of FRS 15. All other fixed assets are held at cost and depreciated as follows:

Plant and machinery: 10% per annum, straight line

Vehicles: 25% per annum, straight line Required: a) Prepare a suitable note for inclusion in the published accounts relating to the stock

breakdown.

b) Prepare a suitable note for disclosing Biscabee’s accounting policy with regard to stock in line with the requirements of SSAP 9 and FRS 18.

c) Prepare a suitable note for disclosing Biscabee’s accounting policy with regard to fixed assets in line with the requirements of FRS 15 and FRS 18.

Accounting – Graded Unit 3 Tutor’s Support Pack

34

Revision exercise 20 Harebell’s profit and loss account for the year ended 31 December is as follows: Trading profit and loss account for year ended 31 December £000 Turnover 608,738 Cost of sales (511,621) Gross profit 97,117 Admin expenses (31,558) Distribution costs (12,153) Operating profit 53,406 Interest payable (2,496) Profit before taxation 50,910 Taxation (22,050) Profit after taxation 28,860 During the year, Harebell discontinued a major segment of its business. This had accounted for 5% of turnover, 6% of the cost of sales, 6% of administrative expenses and 10% of the distribution costs. Required: Redraft the profit and loss account incorporating the requirements of FRS 3 with regard to discontinued activities.

Accounting – Graded Unit 3 Tutor’s Support Pack

35

Revision exercise 21 Discuss the advantages users may gain from the additional disclosure required by SSAP 25 Segmental Information and briefly state the requirements of that standard.

Accounting – Graded Unit 3 Tutor’s Support Pack

36

Conceptual matters Revision exercise 22 The historic cost model still dominates the production of financial information in the UK, despite attempts to find a more satisfactory model (eg by the introduction of SSAP 16, now withdrawn). FRS 15 and the Draft Statement of Principles both appear to suggest that a modified form of historic cost accounting will be with us for a long time yet. Required: Critically evaluate two alternative models which have been put forward and comment on the reasons for the continuing domination of historic cost accounting. Revision exercise 23 Identify the bodies that influence the setting of accounting standards in the UK and comment specifically on the role of:

• The FRC

• The ASB

• The UITF

• The FRRP. Revision exercise 24 The Statement of Principles emphasises the importance of the concepts of ‘accruals’ and ‘going concern’ in the preparation of financial statements. Required Briefly describe these two concepts and comment on whether you believe they contribute to the relevance of financial information to the users of accounts.

Accounting – Graded Unit 3 Tutor’s Support Pack

37

Taxation Revision exercise 25 Al Cap Ltd Al Cap Ltd is a wine importing company. The most recent annual accounts show the following: £ £

Gross profit 51,929 Bank deposit interest 160 Dividends (net) 140 52,229 Expenses: Rent and business rates 2,740 Light and heat 120 Office salaries 19,660 Repairs to premises (note a) 2,620 Motor expenses 740 Depreciation – motor vans 2,800 equipment 750 Amortisation of lease 120 Loss on sale of equipment 40 Bad and doubtful debts (note b) 680 Professional charges (note c) 375 Interest on bank over draft (note d) 240 Sundry expenses (note e) 770 Salaries 15,450 47,105 Net profit 5,124

Notes: a) Repairs: £

Alterations to flooring in order to install new bottling machine 1,460 Decorations 475 Replastering walls due to damp 685

2,620 b) Bad and doubtful debt £

Trade debts w/o 500 Specific allowance for doubtful debt 180

Accounting – Graded Unit 3 Tutor’s Support Pack

38

c) Professional charges: £ Accountancy 200 Cost of court action for failing to observe Customs regulations 110 Legal cost of obtaining new lease (see below) 20 Debt collection 45 375

d) The overdraft was obtained in order to finance the purchase of stock e) Sundry expenses £

Fine re breach of Customs bonding regulations 250 Subscription to wine retail trade association 50 Donation to police welfare fund 20 Entertaining customers 300 Calendars bearing firm’s name sent to 300 customers 120 Miscellaneous allowable expenses 30

770 f) On 25th March the company took out a lease on a new retail outlet for 99 years. Required: Compute Al Cap’s trading profit before capital allowances.

Accounting – Graded Unit 3 Tutor’s Support Pack

39

Revision exercise 26 You are presented with the accounts of Cornelius Ltd for the year to 31st December 2006. Cornelius runs a small printing business and the managing director wishes to know the trading profit for the year ended 31st December 2006. Calculate Cornelius Ltd’s trading profit for taxation purposes. £ £ Gross profit from trading 25,620 Profit on sale of business premises (1) 1,750 27,370 Advertising 642 Debtors allowance (2) 75 Depreciation 2,381 Light and heat 372 Miscellaneous expenses (3) 347 Motor car expenses (4) 555 Rates 1,057 Repairs and renewals (5) 2,598 Staff wages (6) 12,124 Telephone 351 (20,502) Profit before tax 6,868 Notes: 1) The profit on the sale of premises relates to the sale of a small freehold industrial

unit in which the company stored paper before building the extension 2) The charge for debtors allowance is made up as follows:

£ Write-off of specific trade debts 42 Increase in general allowance for doubtful debtors 50 92 less: recovery of bad debt previously written off (17) Charge to the profit and loss account 75

3) Miscellaneous expenses include: £

Subscription to printers association 45 Contribution to Local Enterprise Agency 50 Gifts to customers Calendars costing £7.50 each (bearing the company’s name) 75 Two food hampers bearing the company’s name 95

Accounting – Graded Unit 3 Tutor’s Support Pack

40

4) A director uses the motor car for 75% business and 25% private use 5) Repairs and renewals comprise the following expenditure:

£ Refurbishing a second hand press (before it could be used in the business) 522 Redecorating administration offices 429 Building extension to enlarge paper store 1,647 2,598

6) Staff wages include an amount for £182 for a staff Christmas lunch Required: Calculate Cornelius Ltd’s trading profit for the year ended 31st December 2006.

Accounting – Graded Unit 3 Tutor’s Support Pack

41

Revision exercise 27 Your Company Ltd An examination of the draft accounts of Your Company for the year ended 31st March 2007 reveals the following details in respect of specific items of expenditure and income. The draft accounts showed a profit of £290,000. Expenditure 1) Throughout the year, two of the directors were seconded to work elsewhere. One

worked for Oxfam – a leading charity – and his salary, paid by your company, was £22,000. The other worked for a subsidiary company in the group and his salary, also paid by your company, was £24,000.

2) Damages of £30,000 were paid to a customer who was injured by a falling crate

while visiting your factory. Only £18,000 was recovered from your public liability insurers.

3) During the year the company purchased freehold offices for £40,000. Your chief

engineer estimated that it would cost £2,000 to get them ready for use. In the event it cost £12,000. The amount spent purchasing the offices was capitalised but the repair expenditure of £12,000 was deducted in the profit and loss account.

4) Bad debts were written off amounting to £6,000.The appropriate ledger account for

the year showed that these all related to specific identified debtors. 5) Because of the overall contraction in trade, a supervisor was made redundant and

given a severance payment of £18,000. His statutory redundancy entitlement was £11,000.

Income 6) Goods were sold to a subsidiary in the Caribbean for £80,000. Had they been sold

to a UK customer the price would have been £120,000 Required: Compute the adjusted trading profit starting with the profits of £290,000 shown by the accounts. Give reasons for your adjustments.

Accounting – Graded Unit 3 Tutor’s Support Pack

42

Revision exercise 28 Able Ltd, a small company, prepares accounts to 31st December. The company's pool of unrelieved expenditure on plant and machinery brought forward on 1st January was £11,000. During the year FYAs of 50% were available to small companies when purchasing plant. During the year ended 31st December the following transactions took place:

15th June Purchased plant for £6,500. 31st August Purchased plant for £12,000. 30th November Sold plant for £2,800 (originally purchased for £4,600). Required: Compute the capital allowances for the year ended 31st December. Revision exercise 29 Flash Ltd, a medium-sized company, prepares accounts to 31st December. At 1st January the tax WDVs are as follows: £ Pool 21,200 Expensive motor car 13,600 The following transactions took place during the year ended 31st December:

10.5.05 Purchased plant for £6,600 25.6.05 Purchased a motor car for £10,600 28.6.05 Purchased an energy saving toilet for £600 15.2.06 Sold the expensive motor car for £9,400 16.2.06 Purchased a motor car for £18,000 18.2.06 Purchased an electrically propelled car for £16,500 Required: Calculate the capital allowances for the year to 31st December.

Accounting – Graded Unit 3 Tutor’s Support Pack

43

Revision exercise 30 XY Ltd trades as a tool manufacturer and makes up accounts each year to 30th June. The company's agreed profits before the deduction of capital allowances for the year to 30th June 2006 were £120,000. At the start of the year, tax written down values were:

General plant and equipment £45,000 Expensive car £20,000 The following purchases and sales of capital items took place during the year:

£ Purchases:

September General plant and equipment 60,000 October Motor car for employee (no private use) 10,000 November Motor car (40% private use by director) 28,000 Sales:

August Plant sold for 25,000 September Employee's car 2,000 November Expensive car sold for 12,000 Required: a) Compute the capital allowances for the accounting year. b) Compute the trading profits for the year.

Accounting – Graded Unit 3 Tutor’s Support Pack

44

Revision exercise 31 Simple Simon Ltd Simple Simon Ltd had the following income and expenditure for the year ended 31st March 2007: Property business income £10,000 Trading income £95,200 Chargeable gains £25,000 Investment income (interest – gross) £18,000 Charges on income £2,000 Dividends plus tax credit £15,000 Required: Calculate Simple Simon’s CT for the year ended 31st March 2007. Revision exercise 32 Peter Pieman Ltd Peter Pieman Ltd had the following income and expenditure for the year ended 31st March 2007: Property business income £70,500 Trading income £465,700 Chargeable gains £10,000 Investment income (interest-gross) £13,200 UK dividends received (gross) £100,000 Required: Calculate Peter Pieman’s CT for the year ended 31st March 2007.

Accounting – Graded Unit 3 Tutor’s Support Pack

45

Revision exercise 33 Charles Ltd has the following PCTCT for the year ended 31st March 2007: £ Trading income 360,000 Property business income 10,000 370,000 less Gift Aid donation (80,000) PCTCT 290,000 Required: What is the corporation tax liability if:

a) no dividends are received from UK companies?

b) £9,000 of dividends are received from UK companies?

c) £45,000 of dividends are received from UK companies? Revision exercise 34 Ross McHugh Ltd has the following results for the two years to 31st March 2007: Year Ended 31.3.06 31.3.07 £ £ Trading profit/(loss) (20,000) 18,000 Interest income 6,000 9,000 Capital loss (2,000) Chargeable gains 7,000 Required: Calculate the PCTCT for the two periods, assuming that the loss is relieved under S393(1) ICTA 1988 showing any losses carried forward at 1st April 2007.

Accounting – Graded Unit 3 Tutor’s Support Pack

46

Revision exercise 35 Duck Soup Ltd has the following results for the year ended 31st March 2007: £ Trading loss before capital allowances (note 1) (96,000) Interest income 3,500 Chargeable gain 14,500 Net loss (78,000) Notes: 1) The trading loss is after charging: £

Depreciation 10,800 Entertaining customers 1,200

2) All other expenses are allowable for corporation tax. 3) The tax written down value of plant and machinery on 1st April 2005 was £16,000.

There were no purchases or sales during the year ended 31st March 2006. 4) Duck Soup Ltd has the following results for the previous year ending 31st March

2006: £

Trading profit 40,000 Interest income 2,000 Chargeable gains -------- 42,000

Required: Compute the allowable trading loss for the year ended 31st March 2007 and show how it can be relieved.

Accounting – Graded Unit 3 Tutor’s Support Pack

47

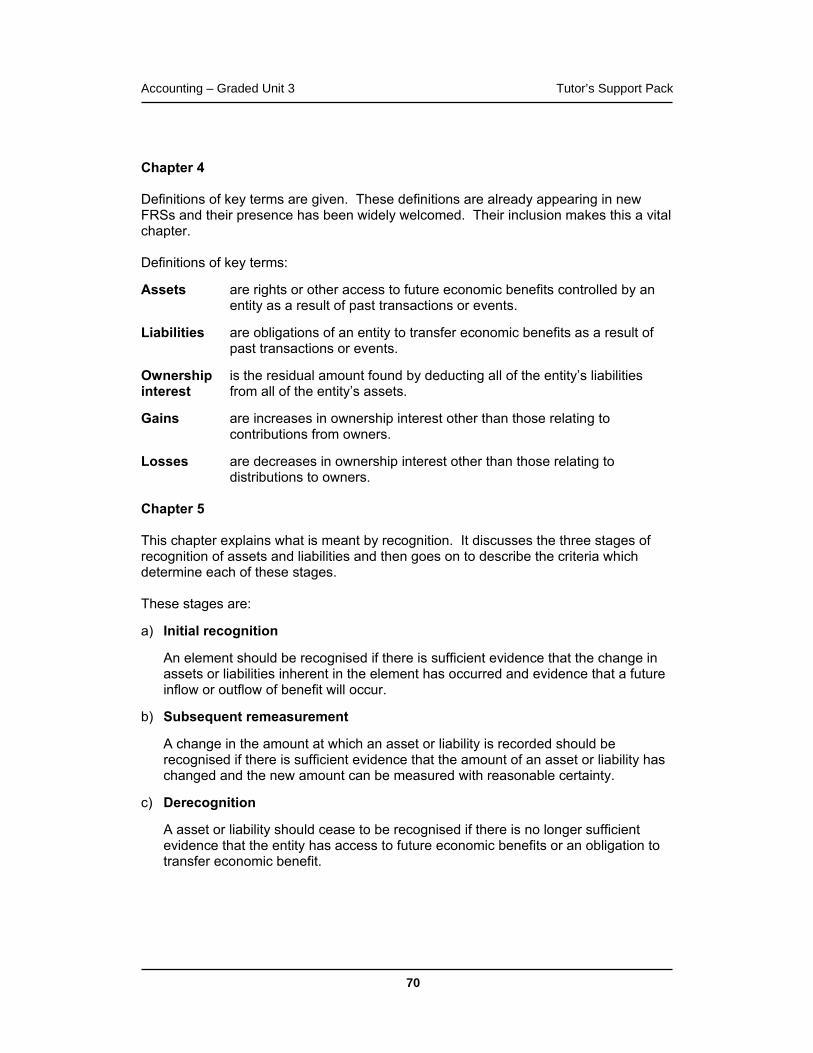

Appendices

Appendix 1 – SSAP 9 SSAP 9 Stocks and long term work in progress This SSAP is based on the accruals/matching concept – costs must be allocated between the cost of goods sold (matched against current revenue) and costs of closing stock (carried in the balance sheet to be matched against future revenue). Main points:

• Stock should be valued at the lower of cost and net realisable value (NRV).

• Costs should include those incurred in the normal course of business in bringing a product or service to its present position and location.

• Costs include direct costs (labour, materials), production overheads and other attributable overheads.

• NRV is the actual or estimated selling price less further costs to be incurred in marketing selling and distribution.

• The principle instances where NRV will be less than cost will be where:

• there have been increases in cost or falls in selling price

• physical deterioration of stock has occurred

• products are obsolescent

• the company has decided to make and sell a product at a loss.

Accounting – Graded Unit 3 Tutor’s Support Pack

48

Long term work in progress The most controversial aspect of SSAP 9 is its regulation concerning work in progress for incomplete long term contracts. Usually long term contracts will exceed one year. According to ‘prudence’, it would seem correct to treat all costs incurred on these contracts simply as WIP (unless it was foreseen that the costs would not be recovered), not recognising any profit until the contract is complete. SSAP 9, however, allows a proportion of profit to be recognised in stages over the life of the contract, provided that:

• it is expected to be profitable in the final analysis

• the contract is far enough advanced to enable the end result to be foreseen with reasonable assurance

• prudent estimates are used. Thus the matching concept, while apparently over-ruling prudence on this occasion, must still be applied prudently! The rules are as follows:

a) Turnover and profit must reflect the proportion of work carried out at the accounting date.

b) Where the outcome cannot be foreseen with reasonable certainty, no profit must be recognised.

c) If there is any expected loss on a contract, provision must be made for the loss as soon as it is foreseen.

For the profit and loss account:

• First ascertain the total estimated profit or loss on a contract.

• Ascertain attributable profit on the basis that it is prudent to recognise such profit.

• Calculate turnover:

The standard does not prescribe a method of calculating turnover. Recognise as turnover the same proportion of the total contract value as applied to the total estimated profit for ascertaining attributable profit to date. This is often given as the amount of work certified.

• Associated costs of achieving the turnover recognised should be deducted from total costs to date in the contract account and charged in the profit and loss account as cost of sales to give, as gross profit, the attributable profit or foreseeable loss on a contract as calculated.

You will be given information to calculate attributable profit or foreseeable loss. You will also be given a basis for recognising either turnover or cost of sales (or both). Given the basis for turnover, take cost of sales as the balancing item. Given the basis for cost of sales, take turnover as the balancing item.

Accounting – Graded Unit 3 Tutor’s Support Pack

49

Foreseeable loss If a loss is foreseen on the contract as a whole, this loss must be taken into account immediately. It is never appropriate to recognise an attributable profit at one stage of the contract if an overall loss is expected on the contract as a whole. Further provisions for foreseeable loss should be included with cost of sales. Remember:

When, in the early stages of a contract, it is not possible to foresee its outcome with reasonable certainty, turnover will equal the costs that are charged to cost of sales. Therefore no profit from the contract will be recognised in the profit and loss account. However, when in the later stages of the contract the outcome can be assessed with reasonable certainty, turnover should include profit prudently recognised as earned at that stage of completion.

For the balance sheet:

• Long-term contracts in the balance sheet will comprise: £

Total costs to date x Less: Amounts transferred to cost of sales in respect of work carried out to date (x) Net costs x Less: any foreseeable losses (if costs remaining need to be further written down) (x) Less: any applicable payments on account (x)

X • Debtors: amounts recoverable on contracts will arise when turnover recognised is

greater than payments on account received and receivable.

• Where payments on account received and receivable are greater than turnover recognised, the excess should first be applied against any net costs remaining in the contract account (as above). Any further excess should be classified as ‘payments on account’ and separately disclosed in ‘creditors’.

• When foreseeable losses exceed net costs, the excess should be included in the balance sheet in either accruals or provisions.

Accounting – Graded Unit 3 Tutor’s Support Pack

50

Disclosure The Companies Act requires that, either on the face of the balance sheet, or in a note to the accounts, the stock figure must be broken down into its components as follows (for all companies except those qualifying as small):

1) Raw materials and consumables

2) Work in progress

3) Finished goods and goods for resale Where amounts recoverable on contracts are included in debtors, these too must be split out in a note to the accounts.

Accounting – Graded Unit 3 Tutor’s Support Pack

51

Appendix 2 – SSAP 21 SSAP21 – Hire purchase and leasing This SSAP covers the appropriate accounting treatment for assets which are used by a business but payment for the asset is spread over time. Principle:

the accounting treatment should reflect the commercial substance of the transaction, not its legal form.

There are basically four types of transaction possible:

• credit sale

• hire purchase

• finance lease

• operating lease. Only in the case of an operating lease does the user of the asset not record the asset as a fixed asset in his books at the start of the agreement. The decision as to whether a lease is an operating lease or a finance lease is an important one, as this will affect the accounting treatment and therefore the reported profit figure and balance sheet ratios such as ROCE, gearing etc. Definition:

a finance lease is a lease that transfers substantially all the risks and rewards of ownership of an asset to the lessee.

Step 1: calculate minimum lease payments (including initial payment) Step 2: discount the answer to step 1 using the rate of interest implicit in the lease Step 3: calculate the fair value of the asset at the start of the lease If the answer to step 2 amounts to 90% or more of the answer to step 3, it is a finance lease.

Accounting – Graded Unit 3 Tutor’s Support Pack

52

Principles of accounting treatment – books of the lessee Operating leases:

• payments are debited to the profit and loss account as incurred

• no asset is recorded in the books. All others:

• asset is recorded at fair value and a corresponding liability set up

• payments are split between repayment of capital amount and payment of finance charges

• finance charges are debited to the profit and loss account

• repayment of the capital amount reduces the balance sheet liability

• depreciation is calculated and charged over the shorter of the lease period and the useful life of the asset.

Acceptable methods of splitting payment between capital repayment and finance charges include:

• straight line: only acceptable for short term credit agreements

• sum of the digits: also known as the rule of 78

• actuarial method: the most accurate and hence the favoured treatment Principles of accounting treatment – books of the lessor Operating leases:

• asset included in fixed assets under "assets held for operating leases" and depreciated in normal way

• rental income credited as operating income to the profit and loss account All others:

• asset treated as sold for fair value and corresponding debtor set up as "net investment in finance leases"

• payments split as for lessee between payment of principle and finance charge

• credit finance charge to profit and loss account; payment of principle reduces the debtor

Accounting – Graded Unit 3 Tutor’s Support Pack

53

Disclosure requirements of SSAP 21 The treatment used in the accounts, including the method chosen to allocate the finance charges, should be disclosed in the accounting policies note to the accounts. Also, in the books of the lessee: • Finance leases and HP:

• Assets

These either show by each major class of assets the gross amounts of assets held and the related accumulated depreciation or integrate these with owned fixed assets and disclose by way of an additional note the NBV of assets held under finance leases and HP agreements.

• Liabilities

The amounts of obligations due under finance leases/HP agreements should be disclosed separately from other liabilities either on the face of the balance sheet or in the notes to the accounts.

These amounts should be shown analysed between due in next year, due in the second to fifth years inclusive, and due thereafter (this analysis can be shown separately or as part of an equivalent analysis of the total liabilities of which they form part).

• Profit and loss account

The total depreciation charge and aggregate finance charges for the period in respect of finance leases and HP contracts should be disclosed by way of note.

• Operating leases:

Disclose by way of a note to the profit and loss account the total operating lease rentals, split between hire of plant and machinery and other.

In the books of the lessor: The standard requires disclosure of the net investment in a) finance leases and b) HP agreements at each balance sheet date. These should be disclosed separately in a note to the accounts analysed between receivable within one year and receivable after one year. For assets held for use in operating leases, the cost/valuation and accumulated depreciation should be shown, either as part of the fixed asset schedule or in a separate table.

Accounting – Graded Unit 3 Tutor’s Support Pack

54

Dealing with finance leases in published accounts Balance sheet:

Step 1: The leased asset should be capitalised in the fixed asset account at fair value (ie list price or PV of minimum lease payments).

Step 2: Calculate and charge depreciation over the lease period.

Step 3: Calculate NBV for balance sheet.

Step 4: Set up a lease creditor for the same amount as the leased asset in step 1.

Step 5: Calculate total finance charge (the difference between the total of the minimum lease payments and the fair value of the asset.

Allocate the finance charge to accounting periods over the term of the lease using either:

• actuarial method

• sum of the digits method; or

• straight line method.

Step 6: Reduce the lease creditor by the difference between the lease payment and the finance charge.

Profit and loss account: Step 1: Annual depreciation charged as normal to cost of sales, administration or

distribution. Step 2: Finance charge allocated to current period included in ‘Interest paid and

payable’ but disclosed separately in the notes.

Accounting – Graded Unit 3 Tutor’s Support Pack

55

Appendix 3 – FRS 15 FRS 15 – Tangible fixed assets FRS 15 came into force in April 2000 and replaced SSAP 12. It is intended to give guidance on the initial valuation of tangible fixed assets for balance sheet purposes and the treatment appropriate for arriving at subsequent carrying value. Definition:

Tangible fixed assets are assets that have physical substance and are held for use in the production or supply of goods and services, for rental to others, or for administrative purposes on a continuing basis in the reporting entity’s activities.

Initial value FRS 15 states that a tangible fixed asset should initially be measured at its cost. In practice, an asset’s cost is:

purchase price less trade discounts or rebates plus any further costs directly attributable to bringing it into working condition for its intended use.

Costs which might be included in the initial valuation include:

• stamp duty and other duties

• legal fees

• delivery and handling costs

• installation costs. If the entity has constructed the fixed asset rather than buying it, it might incur other costs:

• materials

• labour

• architects’/designers’ fees

• direct overheads. Only those costs that are directly attributable to bringing the asset into working condition for its intended use should be included, never an apportioned amount of general overhead. FRS 15 also states that ‘abnormal’ costs should not be included. These might include additional costs caused by faulty workmanship, industrial disputes, design errors, etc.

Accounting – Graded Unit 3 Tutor’s Support Pack

56

One of the more controversial aspects of initial valuation concerns the capitalisation of interest costs. FRS 15 leaves this as optional, but lays down rules which must be followed if interest costs are capitalised. Arguments for:

• finance costs are just as much a cost of constructing a tangible fixed asset as other directly attributable costs

• the accounts are more likely to reflect the true success or failure of projects involving the construction of fixed assets

• failure to capitalise borrowing cost means that profits may be reduced in periods when fixed assets are acquired. This is misleading as capital investment should increase profit in the long run.

Arguments against:

• borrowing costs are incurred in support of the whole of the activities of an enterprise. Any attempt to associate such costs with a particular asset is necessarily arbitrary.

• capitalisation of borrowing costs may lead to the same type of asset having a different carrying value, depending on the method of finance adopted by the enterprise.

• treating borrowing costs as a charge against income results in financial statements giving more comparable results from period to period, thus providing a better indication of the future cash flows of an enterprise.

• capitalisation leads to higher tangible fixed asset values, which could exceed the recoverable amount of the asset.

The rules:

• Only finance costs that are directly attributable to the construction of a tangible fixed asset should be capitalised as part of the cost of that asset.

• The total amount of finance cost capitalised during a period should not exceed the total amount of finance cost incurred during the period.

• Capitalisation should begin when:

i) finance costs are being incurred

ii) expenditures for the asset are being incurred

iii) activities that are necessary to get the asset ready for use are in progress.

• Capitalisation should be suspended during extended periods in which active development is interrupted.

• Capitalisation should cease when substantially all the activities that are necessary to get the tangible fixed asset ready for use are complete.

Accounting – Graded Unit 3 Tutor’s Support Pack

57

Disclosures When finance costs are capitalised, the following disclosures must be made:

i) the accounting policy adopted

ii) the aggregate amount of finance costs included in the cost of the tangible fixed assets

iii) the amount capitalised during the period

iv) the amount recognised in the profit and loss account during the period

v) the interest rate used to determine the amount capitalised. Subsequent expenditure can only be capitalised if it enhances an asset, by, for example, extending its useful economic life, increasing its capacity or achieving a significant improvement in quality of output. Revaluation of fixed assets The Companies Act, 1985 allows tangible fixed assets to be carried either at historic cost or at a valuation. Many entities take advantage of this rule and revalue some of their fixed assets (normally property). Other entities continue to carry all assets at historic cost. There are strong arguments for carrying assets at current value and the ASB wishes to encourage this as it believes this provides more relevant information to users of financial information. However, until the issue of FRS 15 there was no accounting standard that gave guidance on revaluation. This has led to the following problems:

• valuations are not kept up to date

• entities ‘cherry pick’ ie revalue certain assets and not others

• some entities do not depreciate revalued fixed assets. Basic rules:

• revaluation is optional

• if one asset is revalued, so must all assets in that class be revalued

• the carrying value of a revalued fixed asset should be its current value at the balance sheet date (current value = lower of replacement cost and recoverable amount).

Accounting – Graded Unit 3 Tutor’s Support Pack

58

FRS 15 does not insist on annual revaluations but requires the following:

• a full valuation every five years with an interim valuation in year 3 or in other years when there has been a material change in value

Five-yearly valuations should be carried out by a qualified external or internal valuer. If an internal valuer is used, the valuation should be reviewed by a qualified external valuer. Bases of valuation Non-specialised properties should be valued on the basis of existing use value plus directly attributable acquisition costs, if material. Open market value should be disclosed if materially different. Specialised properties should be valued on the basis of depreciated replacement cost. Properties surplus to requirement should be valued at open market value less expected direct selling costs (NRV). All other revalued assets should be valued on the basis of open market value where available, or depreciated replacement cost. Gains and losses on revaluation The Companies Act states that only realised gains can be recognised in the profit and loss account. Revaluation gains are not realised until and unless the asset is sold. They are therefore recognised in the Statement of Recognised Gains and Losses (we shall meet this third primary statement later when we consider FRS 3 requirements) and accounted for using a revaluation reserve. Losses are treated according to the cause:

• revaluation losses which are caused by a clear consumption of economic benefits should be recognised in the profit and loss account (they are akin to depreciation)

• other losses (perhaps caused by a market slump) should normally be recognised in the Statement of Total Recognised Gains and Losses and accounted for in the revaluation reserve until the carrying amount reaches its depreciated historic cost. Any further loss should be shown in the profit and loss account.

Accounting – Graded Unit 3 Tutor’s Support Pack

59

Depreciation Depreciation is redefined by FRS 15 as:

the measure of cost or revalued amount of the economic benefits of the tangible fixed asset that have been consumed during the period.

The depreciable amount should be allocated on a systematic basis over the life of the asset, reflecting as fairly as possible the pattern in which the asset’s economic benefits are consumed by the entity. This is no change from the requirements of SSAP 12. However, there is an attempt to address the problem of companies which did not depreciate certain revalued assets. In the past, many entities did not charge depreciation on revalued properties on the grounds that the assets were being maintained or refurbished regularly so that the economic life of the property was limitless (this treatment was common in the hotel, brewing, public house and retail sectors). It had been expected that FRS 15 would insist on depreciation in all circumstances. The ASB has recognised, however, that there may be rare cases where tangible fixed assets do have very long useful economic lives. FRS 15 says that in these rare cases the entity need not charge depreciation but will have to hold annual impairment reviews instead (FRS 11). These reviews are time consuming, costly and complex and may result in reduced profit (due to showing an impairment loss). This will discourage non-depreciation more effectively than a ban! Disclosure In the note to the accounts, a company must disclose (for each class of assets):

a) the depreciation method used

b) the useful economic lives or rates used

c) the total depreciation charge for the period

d) the effect of any change in estimate of useful economic lives or residual value, if material.

Accounting – Graded Unit 3 Tutor’s Support Pack

60

Fixed asset schedule The Companies Act gives the following schedule as a disclosure note to be used for all major classes of fixed assets. It can also be an excellent working note to help you ensure that you have dealt with all aspects of the accounting.

Land and property

Plant and equipment

Total

£000 £000 £000

At cost/revaluation

Opening balances

Additions

Disposals

Transfers

Revaluations

Closing balances

Depreciation

Opening balances

Disposals

Revaluations

Charge for year

Closing balances

NBV at end

NBV at start

Accounting – Graded Unit 3 Tutor’s Support Pack

61

Appendix 4 – FRS 3 FRS 3 – Reporting financial performance The objective of FRS 3 is stated as:

to require reporting entities falling within its scope to highlight a range of important components of financial performance to aid users in understanding the performance achieved by a reporting entity in a period and to assist them in forming a basis for their assessment of future results and cash flows.

Why was FRS 3 necessary? The profit and loss account is arguably the most significant single indicator of a company's success or failure. It is very important to ensure that it is not presented in such a way as to be misleading. This could happen either through an inadvertent lack of consistency within a company or between different companies; or it could arise as a result of deliberate manipulation of accounting figures by unscrupulous directors. FRS 3 applies to all financial statements intended to give a true and fair view, unless the entity is obliged to prepare accounts under a statutory framework which does not permit such treatment. FRS 3 Profit and loss account A layered format is to be used for the profit and loss account to highlight a number of important components of financial performance:

a) results of continuing operations

b) results of discontinued operations

c) profits or losses on the sale or termination of an operation, costs of a fundamental reorganisation or restructuring and profit or losses on the disposal of fixed assets

d) extraordinary items. The following points must be noted:

a) The analysis of results between continued and discontinued operations should be disclosed to the level of operating profit.

b) All exceptional items (except those in c) below) should be included under the statutory format heading to which they relate and disclosed by way of a note.

c) The following items must be shown separately on the face of the profit and loss account after operating profit and before interest:

i) profits or losses on the sale or termination of an operation

ii) costs of a fundamental reorganisation or restructuring

iii) profits or losses on the disposal of fixed assets.

Accounting – Graded Unit 3 Tutor’s Support Pack

62

Statement of total recognised gains and losses This is a new primary financial statement of equal status with the profit and loss and balance sheet. It shows the profit or loss for the period along with all other movements on reserves which reflect recognised gains and losses attributable to shareholders. It does not deal with the realisation of gains in previous periods, nor with transfers between reserves. This means that the excess of the revalued amount over historical cost will never be recognised in the profit and loss account. Profit or loss on disposal will be calculated as the difference between the net proceeds and the net carrying amount. Earnings per share EPS is now calculated on the profit attributable to equity shareholders after minority interest, extraordinary items, preference dividends and other appropriations in respect of preference shares. If an EPS figure is given based on any other level of earnings, then it cannot be given greater prominence than the proper EPS figure and a reconciliation between the two figures must be disclosed. Required notes:

• Note of historical cost profits and losses

This is a memorandum item which helps comparison between the results of companies which have revalued their assets with the results of those which have not. It shows the results for the period as if no revaluation had been made. The note should be shown immediately after the profit and loss or after the statement of recognised gains and losses.

• Reconciliation of movements in shareholders' funds

This brings together the results of the period, shown in the statement of total recognised gains and losses with all other changes in shareholders' funds in the period, including capital contributed by or repaid to shareholders.

• Prior period adjustments

Prior period adjustments should be accounted for by restating the comparative figures for the preceding period in the primary statement and notes and adjusting the opening balance of reserves for the cumulative effect. The cumulative effect of the adjustments should also be noted at the foot of the statement of total recognised gains and losses of the current period. The effect of prior period adjustments on the results for the preceding period should be disclosed where practicable.

These are rare and limited to occasions where:

a) there has been a change in accounting policy;

b) there has been a fundamental error in the past which must now be corrected.

Accounting – Graded Unit 3 Tutor’s Support Pack

63

Effect of FRS 3 a) Extraordinary items will be much rarer (non-existent? Sir David Tweedie famously

said that after the introduction of FRS 3 “little green men from Mars are extraordinary – all else is exceptional”).

b) A new format has been introduced for the profit and loss splitting continuing

operations and discontinued operations. Disclosure will be much fuller. c) A new statement has been introduced – the statement of recognised gains and

losses. The ASB's aim has been to turn attention away from particular numbers or indicators and to encourage users to make their own judgments about a company's performance. This statement cannot be lost in the notes as the reserve note was under SSAP 6.

Note that one of the main reasons for the FRS was the collapse of Polly Peck. The size of the exchange movements going through reserves was considerable and although they had been disclosed, they had not been highlighted.