dcd intelligence presentation istanbul - december 2014_np

TRANSCRIPT

Darran Blatch

Lead Consultant

DCD Intelligence

Market Dynamics in the Turkish

Data Center Sector

A brief introduction

About DCD

DatacenterDynamics is a full service B2B information provider focusing on data center industry, headquartered in UK.

DCD provides a unique series of events tailored specifically to deliver enhanced knowledge and networking opportunities to professionals who design, build and operate data centres. Every year, 49 established annual conferences are held in key business cities across the world.

In 2013, more than 30,000 senior data center professionals attended a DCD event, creating the most powerful forum in the industry today.

About me

Lead Consultant, DCD Intelligence.

Previously worked for IDC and IHS.

Worked for over 26 years in ITC.

At DCD Intelligence (DCDi), we specialize in providing research, data and analysis on the global data center industry. Our research covers the full spectrum of companies and organizations involved in the industry, including service providers, equipment and technology vendors and end users from a range of industry sectors. We provide a diverse selection of “off the shelf” and customized research products that include reports, white papers, market forecasts, presentations and company case studies. Our research employs a full spectrum of research methodologies, from desk research techniques through to industry-wide surveys and face-to-face and phone interviews with clients.

With all our research we strive to incorporate our core values

Quality Integrity Collaboration

About DCD Intelligence

2011

2012

2014

2011-2014 DCD Intelligence Global Census

Quantitative snapshots of the scope and direction of the global data center industry

From ALL sides of the industry

Enables comparisons between markets to track individual market developments and forecasting

It brings the industry together to help raise money for charity (“Engineers without Borders”)

2013

A snapshot of data centers today

In 2007 the number of data centers globally was roughly the same as the

number of oil fields (c. 70,000)

In 2014 the number of data centers globally is roughly the same as the number of branded gas

stations in all of the G7 nations combined (c. 200,000)

In seven years the number of data centers has almost trebled

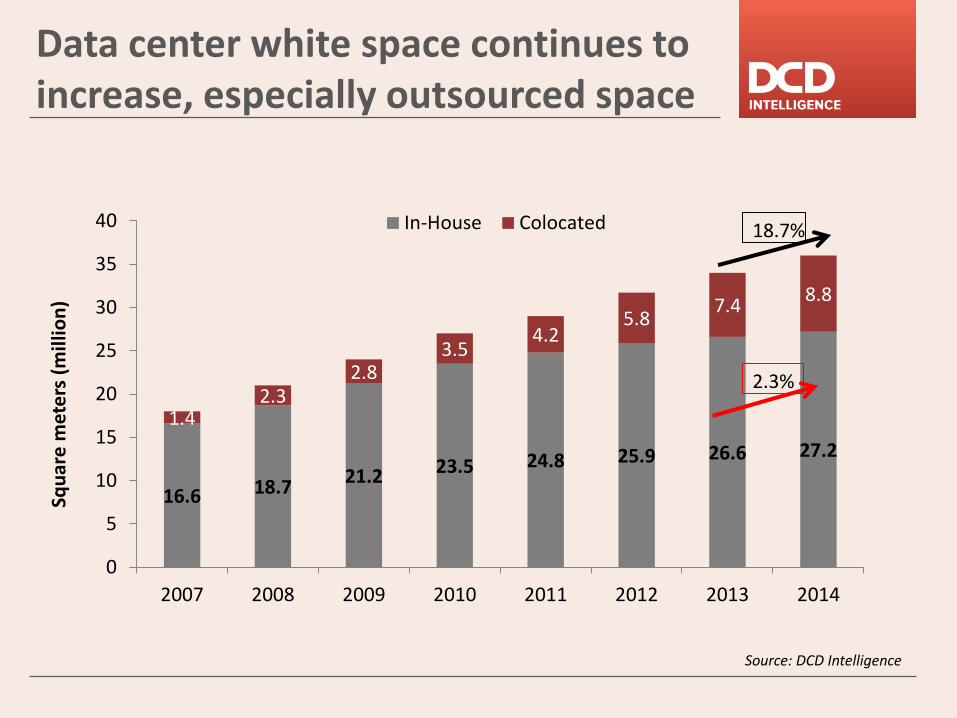

Data center white space continues to increase, especially outsourced space

Source: DCD Intelligence

Squ

are

met

ers

(m

illio

n)

18.7%

16.6 18.7 21.2 23.5 24.8 25.9 26.6 27.2

1.4 2.3

2.8 3.5

4.2 5.8

7.4 8.8

0

5

10

15

20

25

30

35

40

2007 2008 2009 2010 2011 2012 2013 2014

In-House Colocated

2.3%

(*) derived from BP Statistical Review of World Energy 2013 (**) Based on Census 2013 population projections of maximum stated capacity including end user reporting of outsourced footprint

Data centers 375 TWh**

China 3,500 TWh(*) USA 4,250 TWh(*)

Japan 1,100 TWh(*)

UK 360 TWh(*)

India 1,050 TWh(*)

If the data center industry was a country, it would be the 11th largest electricity consumer

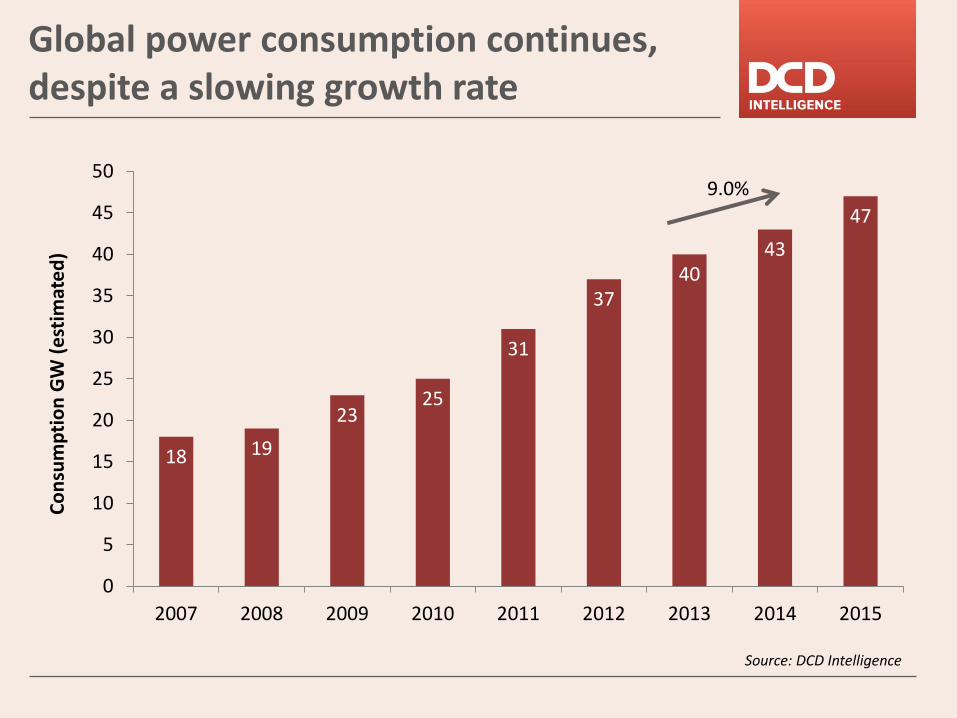

Global power consumption continues, despite a slowing growth rate

Source: DCD Intelligence

9.0%

18 19

23 25

31

37 40

43

47

0

5

10

15

20

25

30

35

40

45

50

2007 2008 2009 2010 2011 2012 2013 2014 2015

Co

nsu

mp

tio

n G

W (

est

imat

ed

)

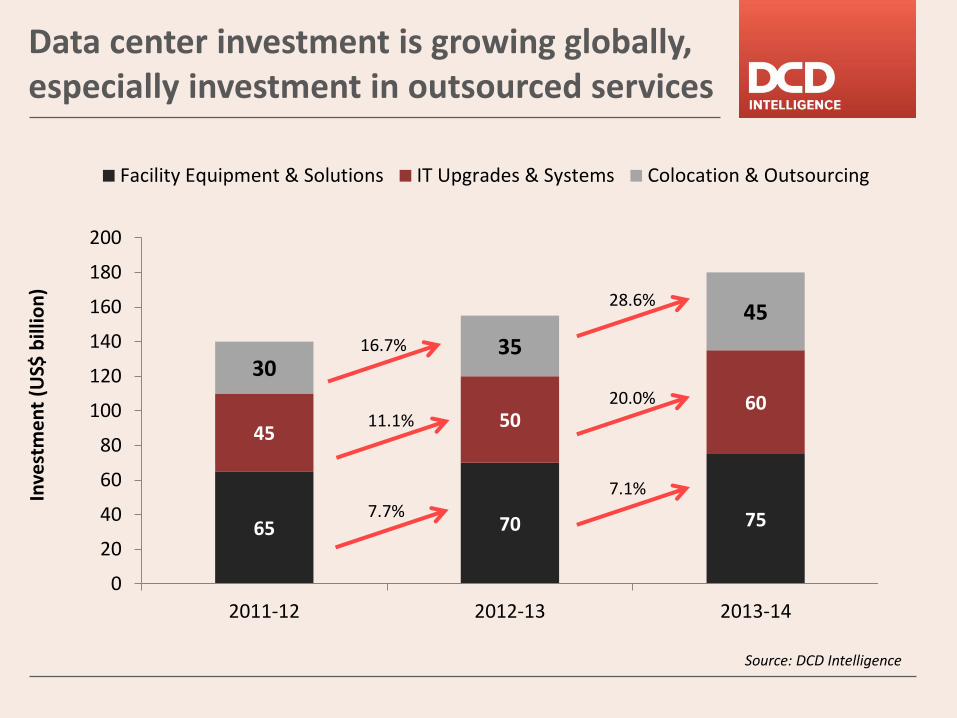

Data center investment is growing globally, especially investment in outsourced services

Source: DCD Intelligence

Inve

stm

en

t (U

S$ b

illio

n)

65 70 75

45 50

60

30 35

45

0

20

40

60

80

100

120

140

160

180

200

2011-12 2012-13 2013-14

Facility Equipment & Solutions IT Upgrades & Systems Colocation & Outsourcing

11.1%

28.6%

16.7%

20.0%

7.7% 7.1%

What is driving the demand for data centers?

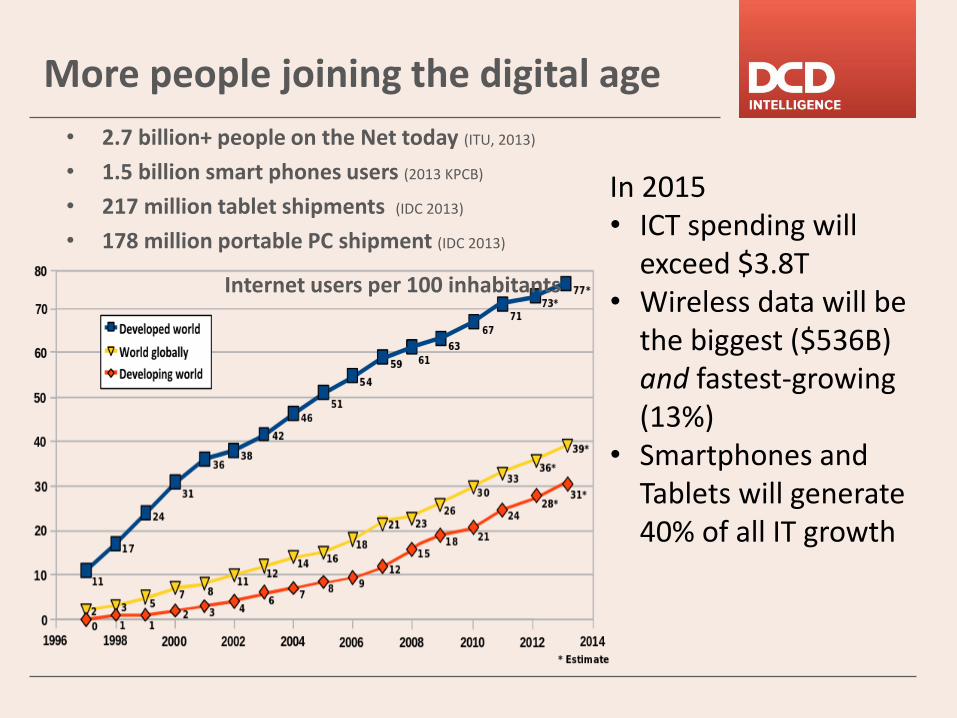

• 2.7 billion+ people on the Net today (ITU, 2013)

• 1.5 billion smart phones users (2013 KPCB)

• 217 million tablet shipments (IDC 2013)

• 178 million portable PC shipment (IDC 2013)

More people joining the digital age

Internet users per 100 inhabitants

In 2015 • ICT spending will

exceed $3.8T • Wireless data will be

the biggest ($536B) and fastest-growing (13%)

• Smartphones and Tablets will generate 40% of all IT growth

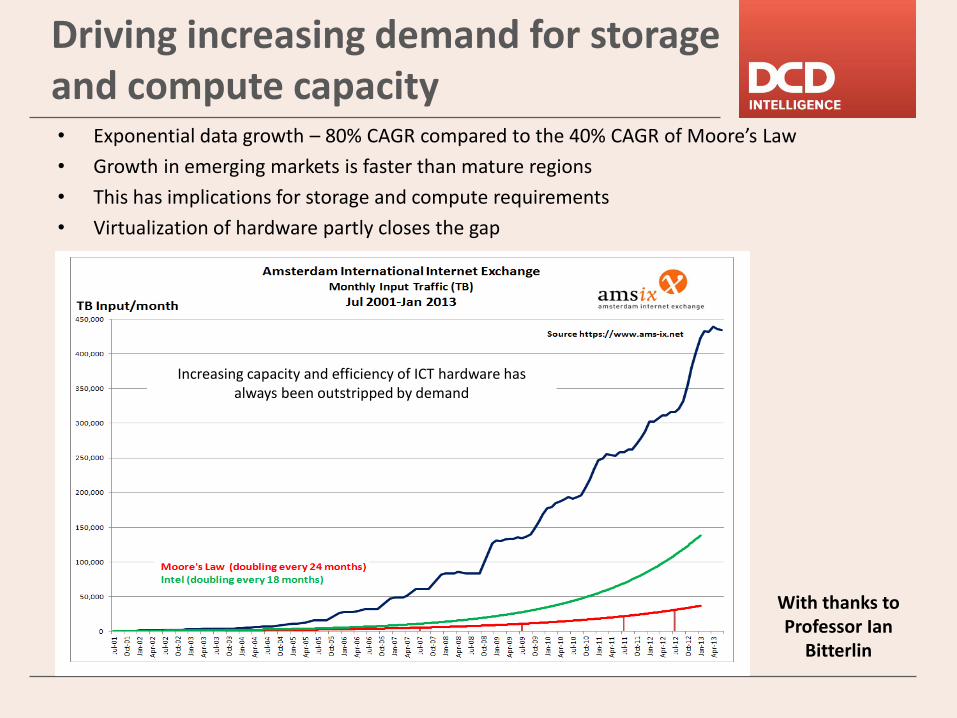

Increasing capacity and efficiency of ICT hardware has always been outstripped by demand

Driving increasing demand for storage and compute capacity • Exponential data growth – 80% CAGR compared to the 40% CAGR of Moore’s Law

• Growth in emerging markets is faster than mature regions

• This has implications for storage and compute requirements

• Virtualization of hardware partly closes the gap

With thanks to Professor Ian

Bitterlin

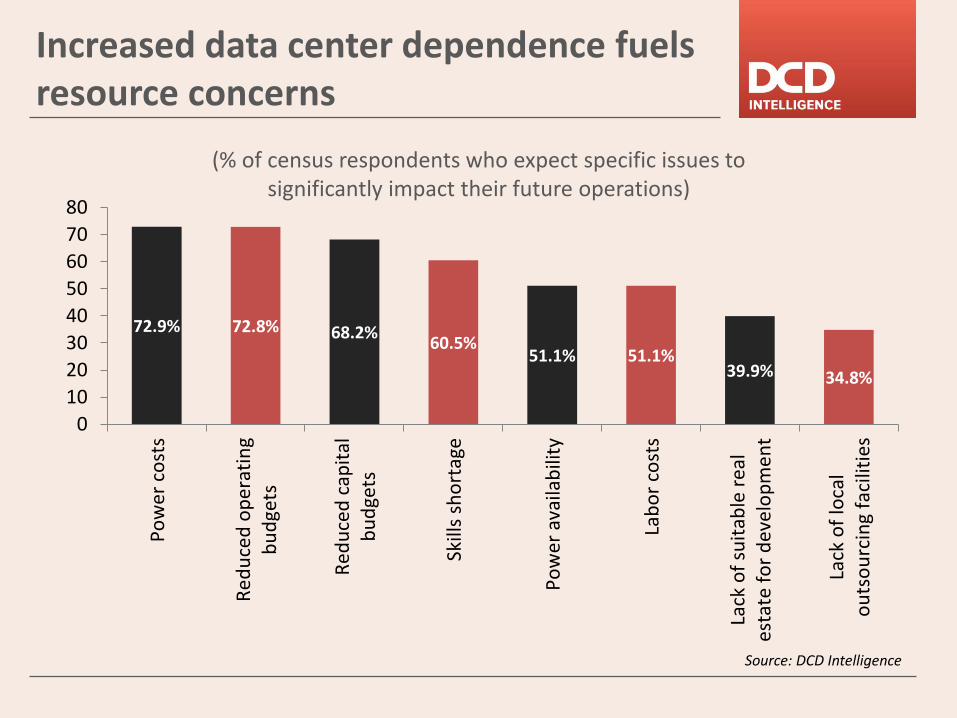

Increased data center dependence fuels resource concerns

72.9% 72.8% 68.2% 60.5%

51.1% 51.1% 39.9% 34.8%

0

10

20

30

40

50

60

70

80

Po

wer

co

sts

Re

du

ced

op

erat

ing

bu

dge

ts

Red

uce

d c

apit

alb

ud

gets

Skill

s sh

ort

age

Po

wer

ava

ilab

ility

Lab

or

cost

s

Lack

of

suit

able

rea

les

tate

fo

r d

eve

lop

me

nt

Lack

of

loca

lo

uts

ou

rcin

g fa

cilit

ies

Source: DCD Intelligence

(% of census respondents who expect specific issues to significantly impact their future operations)

Turkey data center market metrics

Turkey: data center space, 2011-14 (square metres)

Source: DCD Intelligence

Square metres

2011 2012 2013 2014 % average

y-o-y increase

In-house 416,350 425,220 430,700 436,150 1.6%

Colocated & third party

133,650 144,780 159,300 173,850 9.2%

Total 550,000 570,000 590,000 610,000 3.5%

Turkey: power consumption, 2011-13 (MW)

Source: DCD Intelligence

5.1%

3.0%

Growth of around 4% in 2014 (to 880 MW)

780

820

845

740

760

780

800

820

840

860

2011 2012 2013

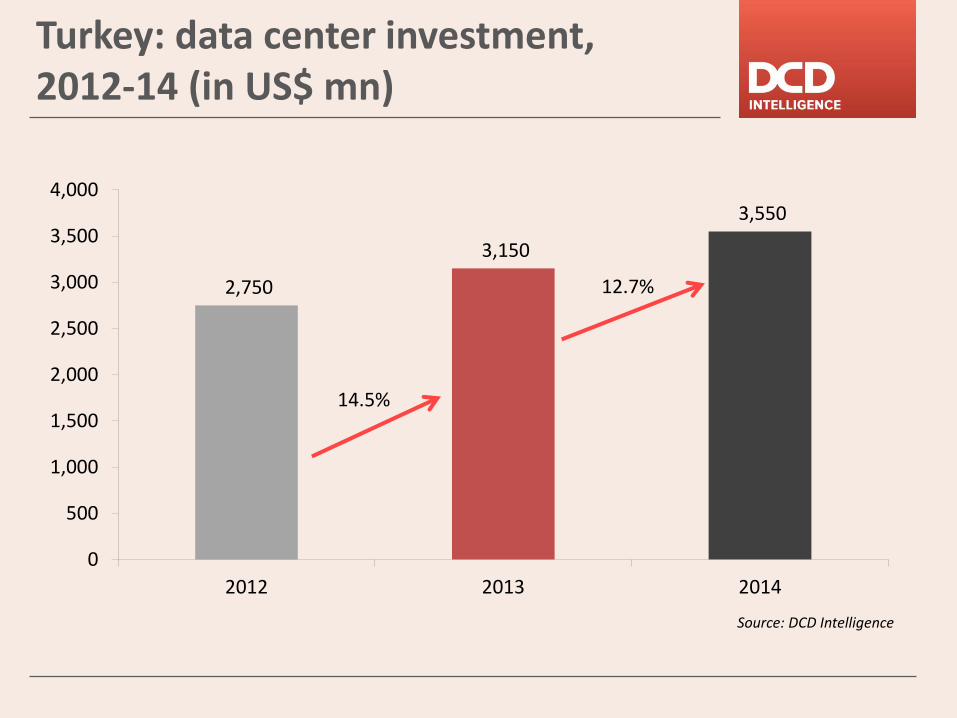

Turkey: data center investment, 2012-14 (in US$ mn)

Source: DCD Intelligence

14.5%

12.7% 2,750

3,150

3,550

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

2012 2013 2014

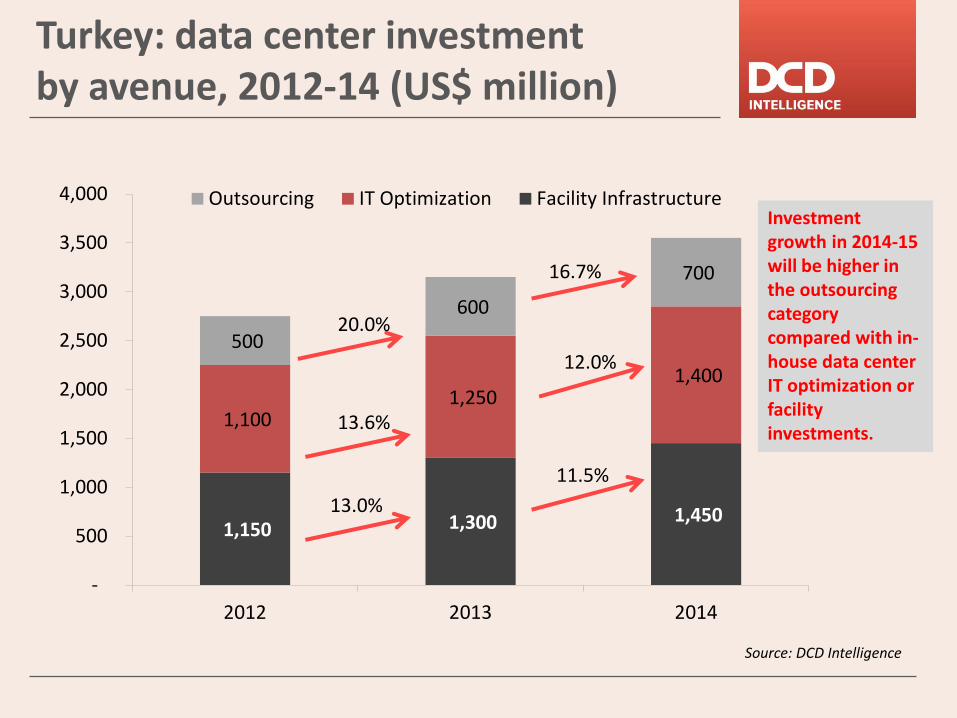

Turkey: data center investment by avenue, 2012-14 (US$ million)

Source: DCD Intelligence

20.0%

13.6%

13.0%

Investment growth in 2014-15 will be higher in the outsourcing category compared with in-house data center IT optimization or facility investments.

16.7%

12.0%

11.5%

1,150 1,300 1,450

1,100 1,250

1,400

500

600

700

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

2012 2013 2014

Outsourcing IT Optimization Facility Infrastructure

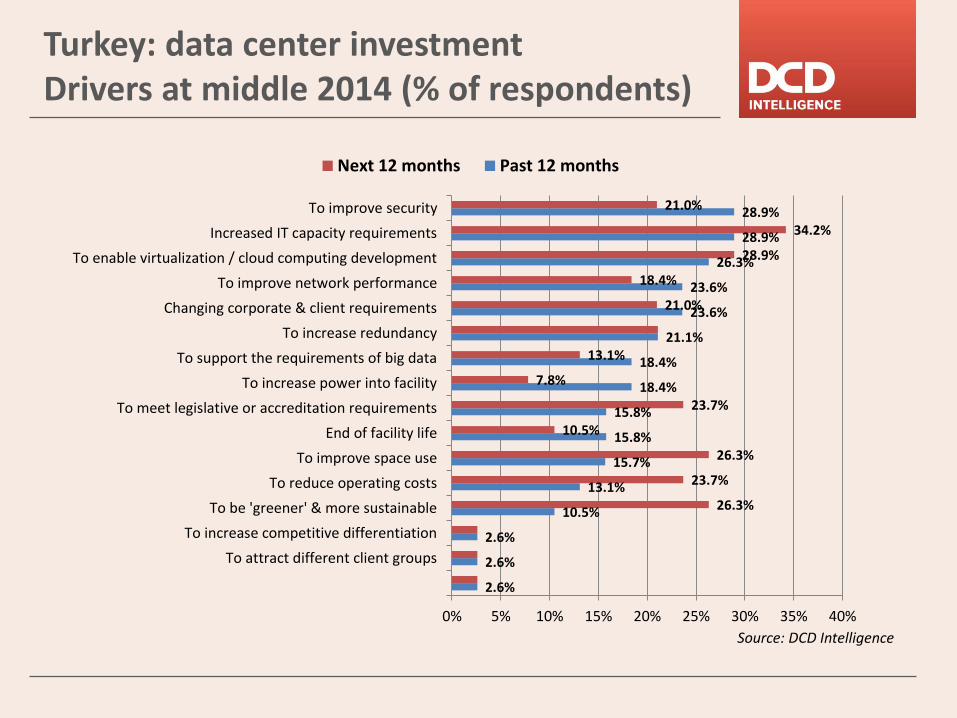

Turkey: data center investment Drivers at middle 2014 (% of respondents)

Source: DCD Intelligence

2.6%

2.6%

2.6%

10.5%

13.1%

15.7%

15.8%

15.8%

18.4%

18.4%

21.1%

23.6%

23.6%

26.3%

28.9%

28.9%

26.3%

23.7%

26.3%

10.5%

23.7%

7.8%

13.1%

21.0%

18.4%

28.9%

34.2%

21.0%

0% 5% 10% 15% 20% 25% 30% 35% 40%

To attract different client groups

To increase competitive differentiation

To be 'greener' & more sustainable

To reduce operating costs

To improve space use

End of facility life

To meet legislative or accreditation requirements

To increase power into facility

To support the requirements of big data

To increase redundancy

Changing corporate & client requirements

To improve network performance

To enable virtualization / cloud computing development

Increased IT capacity requirements

To improve security

Next 12 months Past 12 months

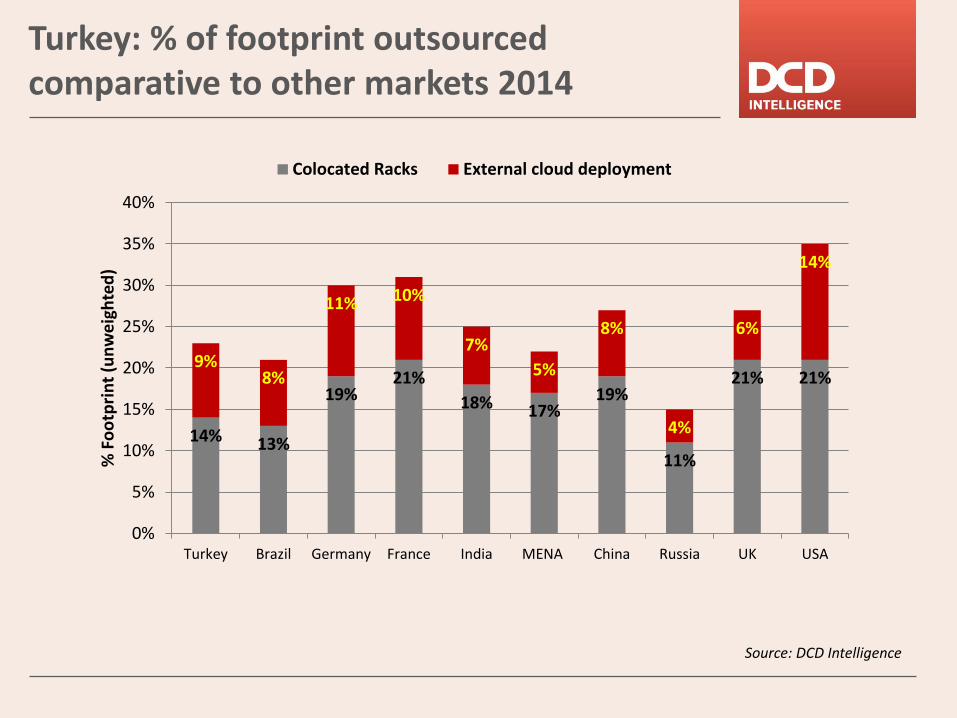

Turkey: % of footprint outsourced comparative to other markets 2014

Source: DCD Intelligence

14% 13%

19% 21%

18% 17% 19%

11%

21% 21% 9%

8%

11% 10%

7%

5%

8%

4%

6%

14%

0%

5%

10%

15%

20%

25%

30%

35%

40%

Turkey Brazil Germany France India MENA China Russia UK USA

% F

oo

tpri

nt

(un

we

igh

ted

)

Colocated Racks External cloud deployment

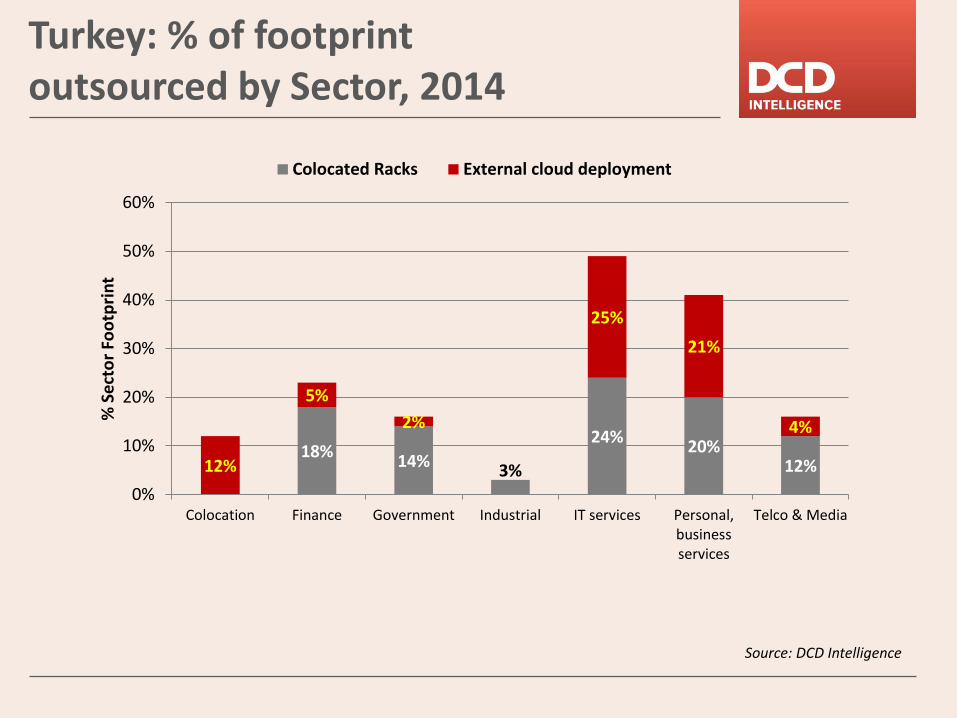

Turkey: % of footprint outsourced by Sector, 2014

Source: DCD Intelligence

18% 14%

3%

24% 20%

12% 12%

5%

2%

25%

21%

4%

0%

10%

20%

30%

40%

50%

60%

Colocation Finance Government Industrial IT services Personal,businessservices

Telco & Media

% S

ect

or

Foo

tpri

nt

Colocated Racks External cloud deployment

A hub market is based on the intersection of several factors

Geographic & access to

populations

Networks & connectivity

A corporate hub

Enterprise Culture

Resource Availability

Technological & skills base

Hubs create & support each other e.g. Financial, corporate, transport & technological hubs reinforce one another

The siting of a number of data centers in close proximity to each other does not in itself create a ‘hub’

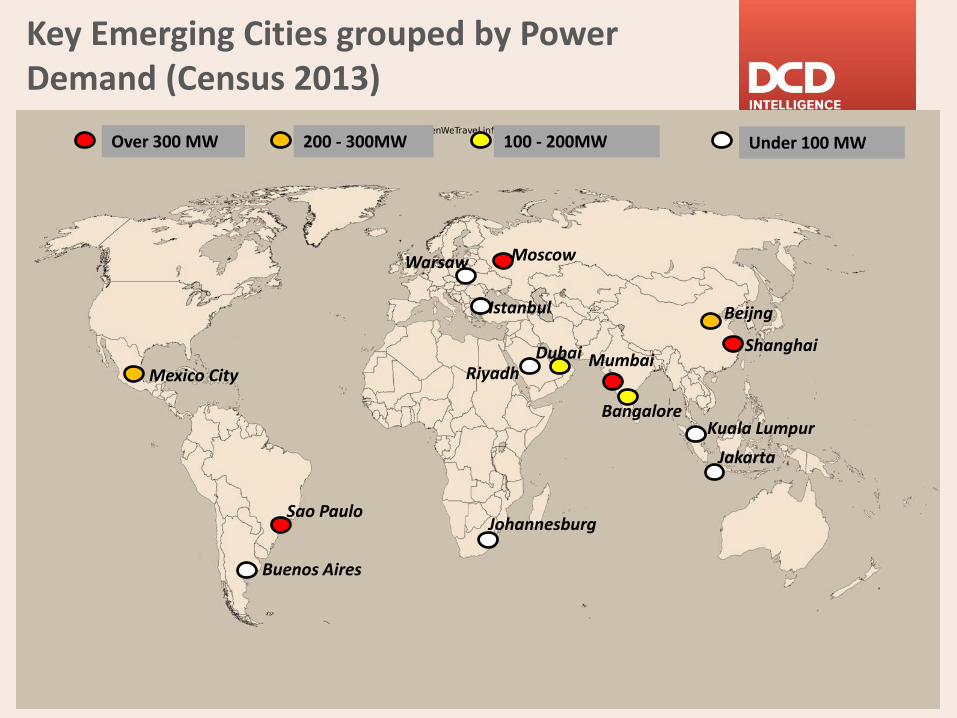

Key Emerging Cities grouped by Power Demand (Census 2013)

Shanghai

Jakarta

Dubai

Sao Paulo

Moscow

Riyadh Mexico City Mumbai

Johannesburg

Bangalore Kuala Lumpur

Beijng

Warsaw

Buenos Aires

Istanbul

Over 300 MW 100 - 200MW 200 - 300MW Under 100 MW

Emerging City Concerns about Availability of Capital:

15% 16%

11%

23%

17%

9% 6%

14%

17%

9% 13%

16%

12%

7% 9%

0%

5%

10%

15%

20%

25%

Bangalore

Beijing

Buenos Aires

Dubai

Istanbul

Jakarta

Johannesburg

KualaLumpur

Mexico City

Moscow

Mumbai

Riyadh

Sao Paulo

Shanghai

Warsaw

% indicating significant concern about CAPEX shortage

% Fearing that shortage of capital will have significant impact on their operation over the next 12 to 18 months

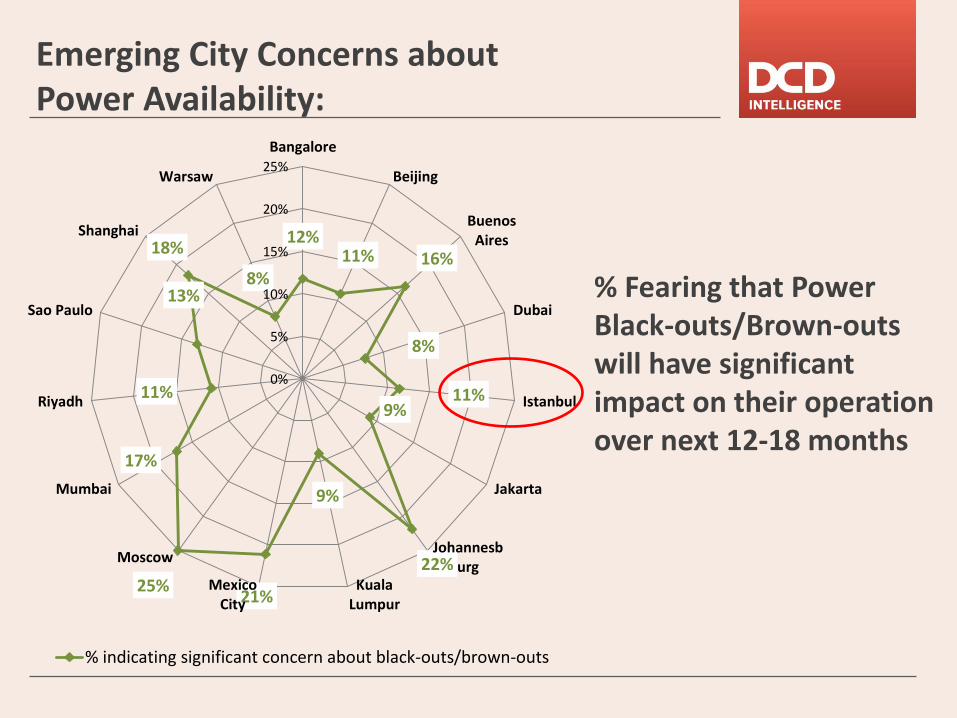

Emerging City Concerns about Power Availability:

12% 11% 16%

8%

11% 9%

22%

9%

21% 25%

17%

11%

13%

18%

8%

0%

5%

10%

15%

20%

25%

Bangalore

Beijing

BuenosAires

Dubai

Istanbul

Jakarta

Johannesburg

KualaLumpur

MexicoCity

Moscow

Mumbai

Riyadh

Sao Paulo

Shanghai

Warsaw

% indicating significant concern about black-outs/brown-outs

% Fearing that Power Black-outs/Brown-outs will have significant impact on their operation over next 12-18 months

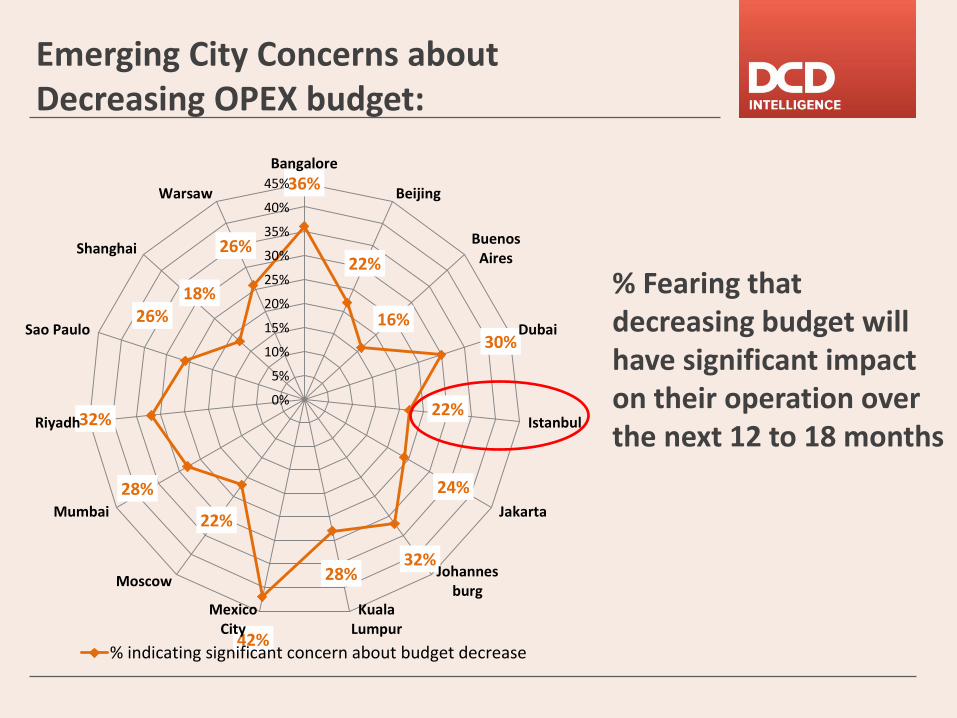

Emerging City Concerns about Decreasing OPEX budget:

36%

22%

16% 30%

22%

24%

32% 28%

42%

22%

28%

32%

26% 18%

26%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Bangalore

Beijing

BuenosAires

Dubai

Istanbul

Jakarta

Johannesburg

KualaLumpur

MexicoCity

Moscow

Mumbai

Riyadh

Sao Paulo

Shanghai

Warsaw

% indicating significant concern about budget decrease

% Fearing that decreasing budget will have significant impact on their operation over the next 12 to 18 months

Emerging City Concerns about Power Costs:

22%

35%

33%

22%

29%

42%

50%

31%

43%

7%

42%

22%

33% 20%

14%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

Bangalore

Beijing

BuenosAires

Dubai

Istanbul

Jakarta

Johannesburg

KualaLumpur

MexicoCity

Moscow

Mumbai

Riyadh

Sao Paulo

Shanghai

Warsaw

% indicating significant concern about power costs

% Fearing that Power Costs will have significant impact on their operation over the next 12 to 18 months

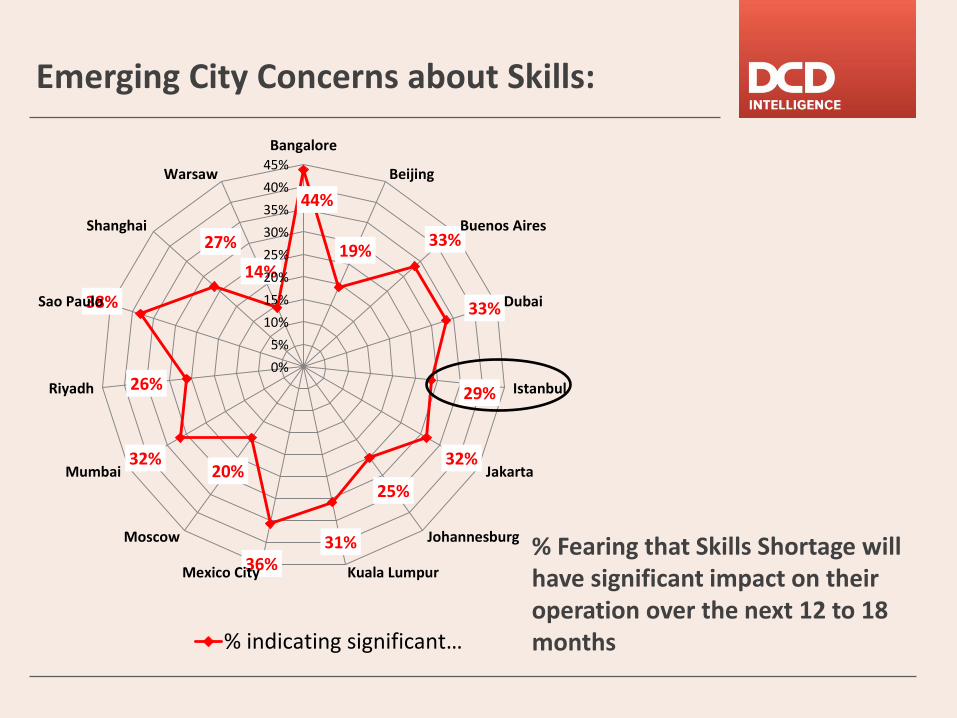

Emerging City Concerns about Skills:

44%

19% 33%

33%

29%

32%

25%

31% 36%

20% 32%

26%

38%

27%

14%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Bangalore

Beijing

Buenos Aires

Dubai

Istanbul

Jakarta

Johannesburg

Kuala LumpurMexico City

Moscow

Mumbai

Riyadh

Sao Paulo

Shanghai

Warsaw

% indicating significant…

% Fearing that Skills Shortage will have significant impact on their operation over the next 12 to 18 months

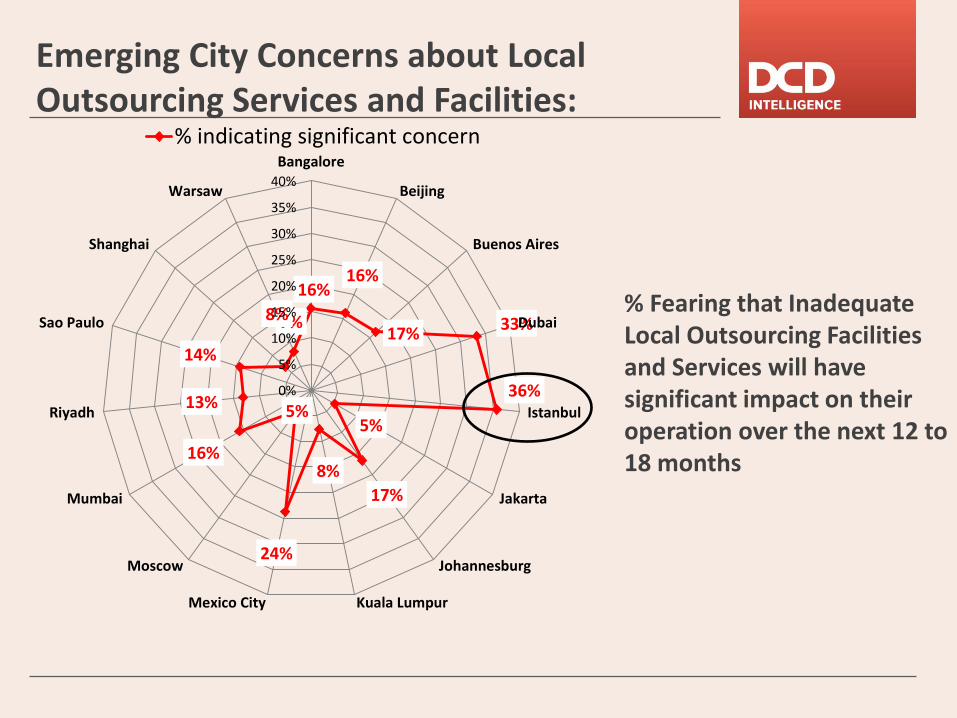

Emerging City Concerns about Local Outsourcing Services and Facilities:

16% 16%

17% 33%

36%

5%

17%

8%

24%

5%

16%

13%

14%

7% 8%

0%

5%

10%

15%

20%

25%

30%

35%

40%

Bangalore

Beijing

Buenos Aires

Dubai

Istanbul

Jakarta

Johannesburg

Kuala LumpurMexico City

Moscow

Mumbai

Riyadh

Sao Paulo

Shanghai

Warsaw

% indicating significant concern

% Fearing that Inadequate Local Outsourcing Facilities and Services will have significant impact on their operation over the next 12 to 18 months

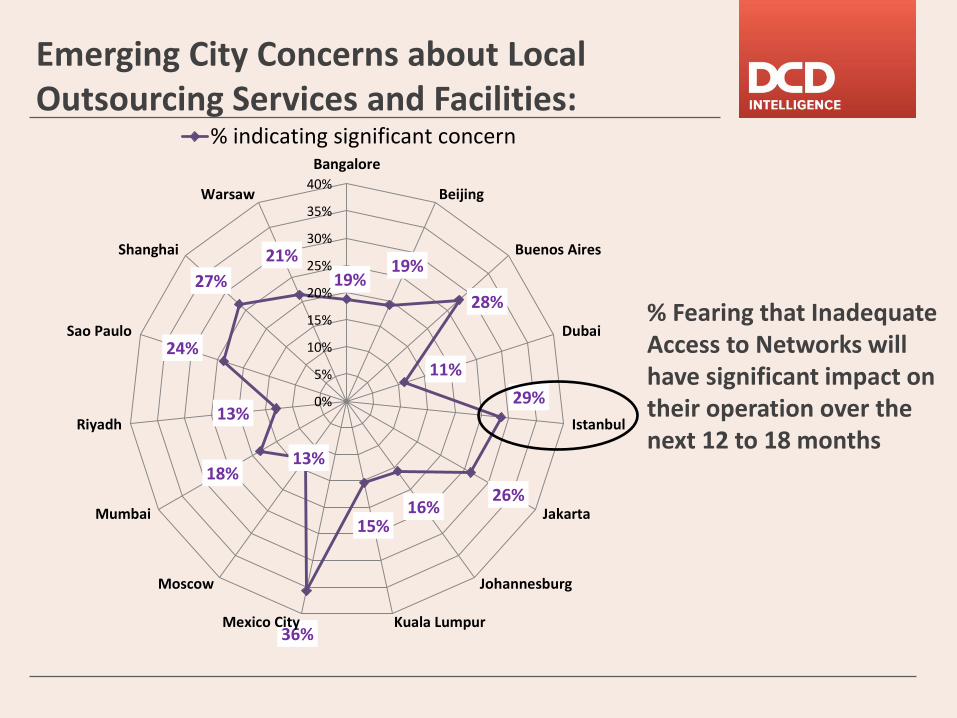

Emerging City Concerns about Local Outsourcing Services and Facilities:

19% 19%

28%

11%

29%

26% 16%

15%

36%

13% 18%

13%

24%

27%

21%

0%

5%

10%

15%

20%

25%

30%

35%

40%

Bangalore

Beijing

Buenos Aires

Dubai

Istanbul

Jakarta

Johannesburg

Kuala LumpurMexico City

Moscow

Mumbai

Riyadh

Sao Paulo

Shanghai

Warsaw

% indicating significant concern

% Fearing that Inadequate Access to Networks will have significant impact on their operation over the next 12 to 18 months

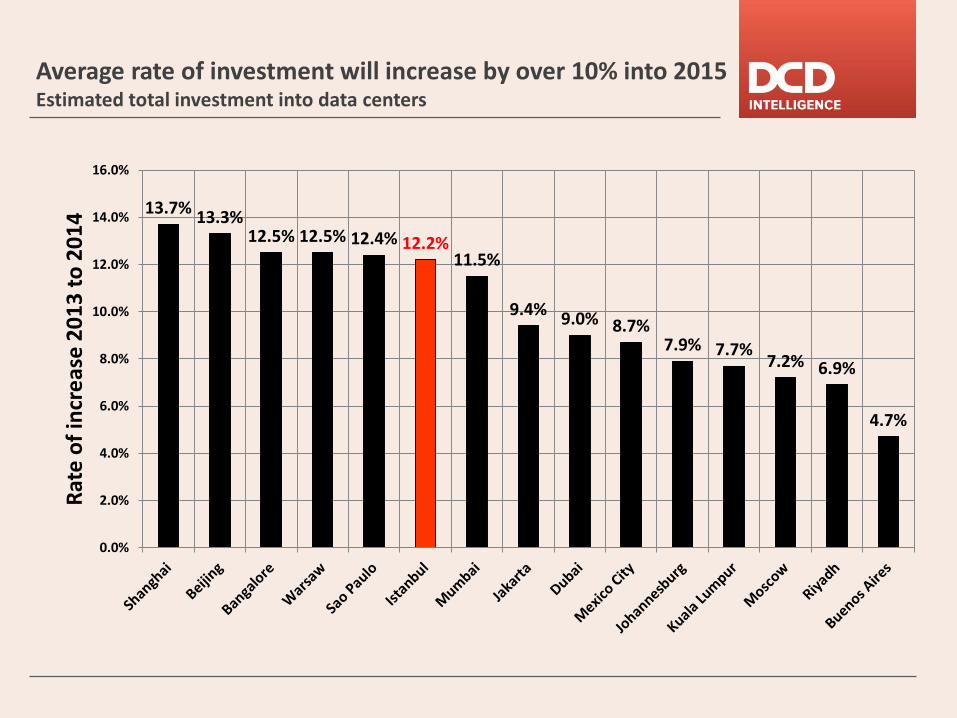

Average rate of investment will increase by over 10% into 2015 Estimated total investment into data centers

13.7% 13.3%

12.5% 12.5% 12.4% 12.2% 11.5%

9.4% 9.0% 8.7%

7.9% 7.7% 7.2% 6.9%

4.7%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

Rat

e o

f in

cre

ase

20

13

to

20

14

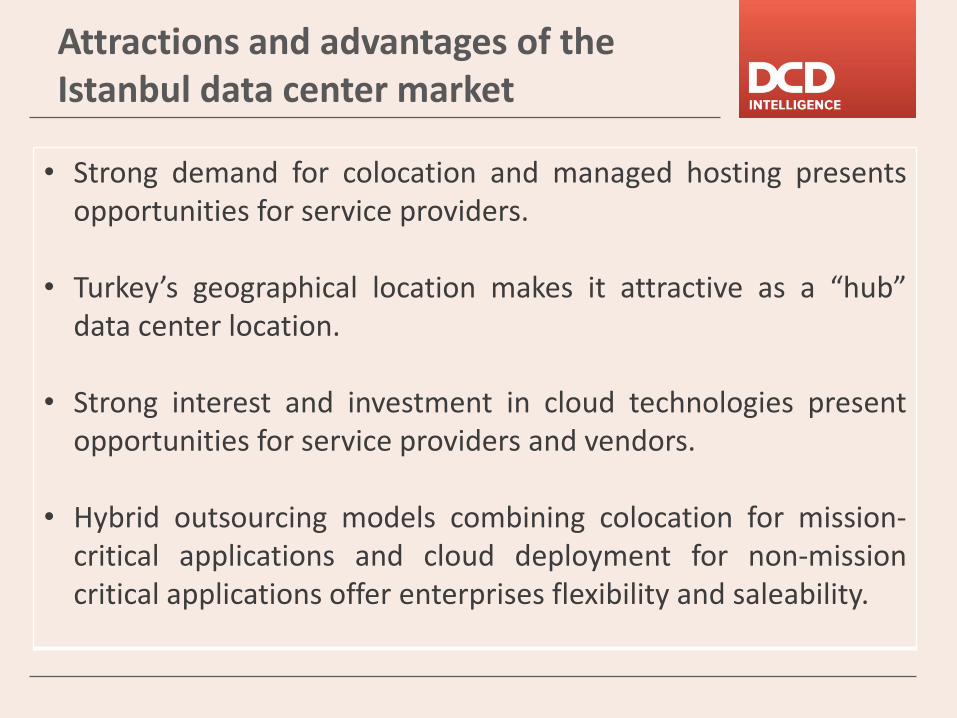

Attractions and advantages of the Istanbul data center market • Strong demand for colocation and managed hosting presents

opportunities for service providers.

• Turkey’s geographical location makes it attractive as a “hub” data center location.

• Strong interest and investment in cloud technologies present opportunities for service providers and vendors.

• Hybrid outsourcing models combining colocation for mission-critical applications and cloud deployment for non-mission critical applications offer enterprises flexibility and saleability.

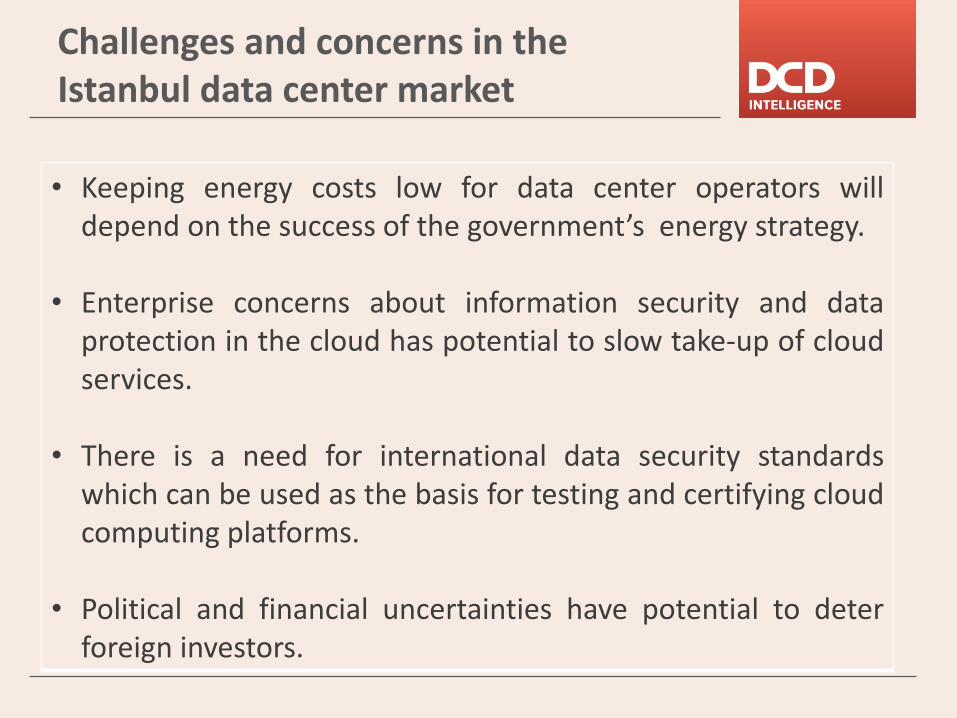

Challenges and concerns in the Istanbul data center market • Keeping energy costs low for data center operators will

depend on the success of the government’s energy strategy. • Enterprise concerns about information security and data

protection in the cloud has potential to slow take-up of cloud services.

• There is a need for international data security standards which can be used as the basis for testing and certifying cloud computing platforms.

• Political and financial uncertainties have potential to deter foreign investors.