date: may 17, 2006 - entertainment network india limited ltd., set india pvt ltd, state bank of...

TRANSCRIPT

Date: May 17, 2006

2

Certain statements in this release concerning our future growth prospects are forward-looking statements,

which involve a number of risks, and uncertainties that could cause actual results to differ materially from

those in such forward-looking statements. The risks and uncertainties relating to these statements include,

but are not limited to, risks and uncertainties regarding fluctuations in earnings, our ability to manage growth,

intense competition in our business segments, change in governmental policies, political instability, legal

restrictions on raising capital, and unauthorized use of our intellectual property and general economic

conditions affecting our industry. ENIL may, from time to time, make additional written and oral forward

looking statements, including our reports to shareholders. The Company does not undertake to update any

forward-looking statement that may be made from time to time by or on behalf of the company.

Disclaimer

3

1. Company Snapshot

2. Business Overview

3. Directors & Management

4. Key Financials FY 2006

5. Ownership Structure & Share Price Performance

6. Future Business Outlook

Agenda

4

Company Snapshot

5

Company Snapshot

Times Innovative Media Private Limited (TIMPL), incorporated on October 27, 2005

Subsidiary:

Radio Broadcasting brand Radio Mirchi

Out-of-home Media brand Times OOH; and

Experiential Marketing brand 3600 Experience

Business:

– ENIL

– TIMPL

29.0%FY06 EBITDA Margin:

Rs. 408.3 mn (US$ 9.1 mn)FY06 EBITDA:

Rs. 1,406.7 mn (US$ 31.3 mn), including other income of Rs. 32.0 mn (US$ 0.7 mn)

FY06 Total Income:

February 15, 2006Listed:

1999Incorporated:

Mumbai, IndiaHeadquarters:

6

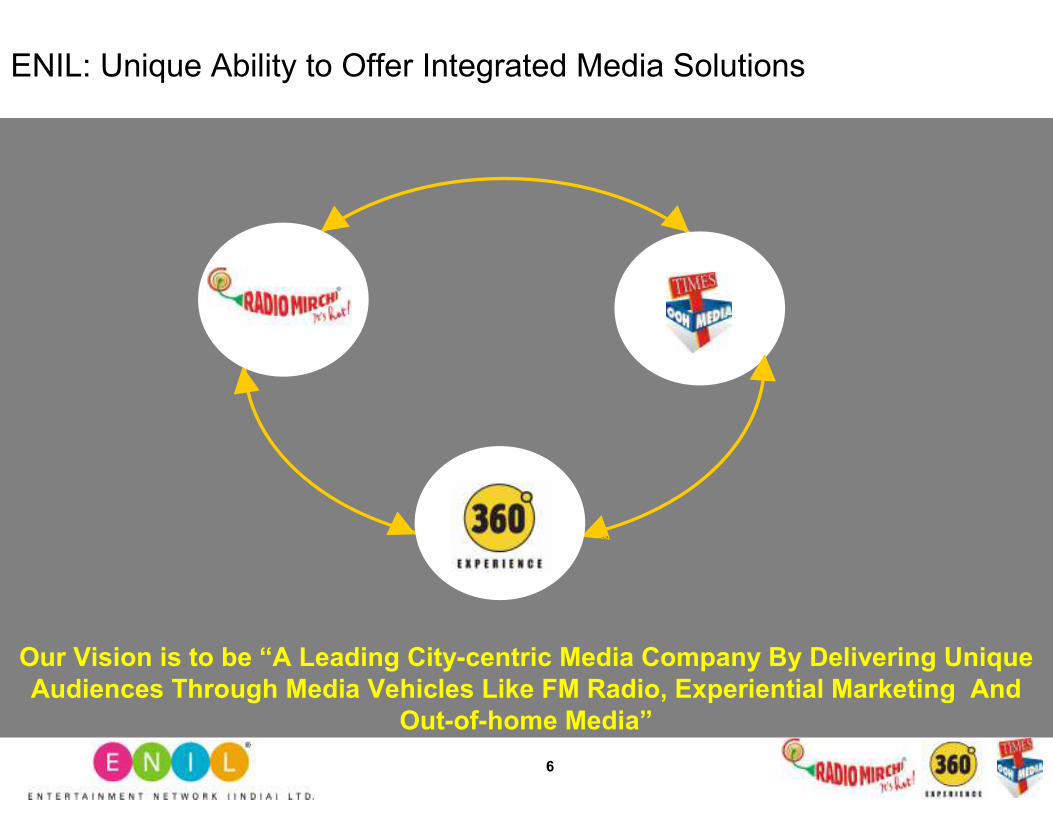

Our Vision is to be “A Leading City-centric Media Company By Delivering Unique Audiences Through Media Vehicles Like FM Radio, Experiential Marketing And

Out-of-home Media”

ENIL: Unique Ability to Offer Integrated Media Solutions

7

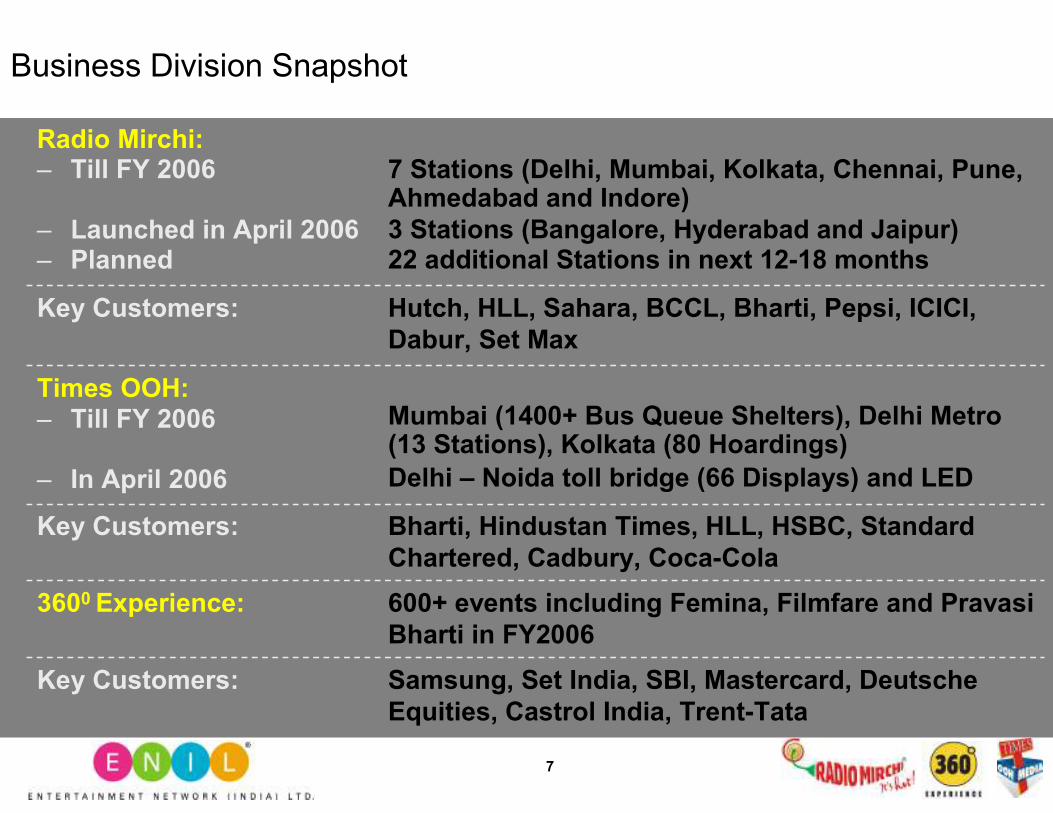

Business Division Snapshot

Samsung, Set India, SBI, Mastercard, Deutsche Equities, Castrol India, Trent-Tata

Key Customers:

600+ events including Femina, Filmfare and Pravasi Bharti in FY2006

3600 Experience:

Bharti, Hindustan Times, HLL, HSBC, Standard Chartered, Cadbury, Coca-Cola

Key Customers:

Mumbai (1400+ Bus Queue Shelters), Delhi Metro (13 Stations), Kolkata (80 Hoardings)

Delhi – Noida toll bridge (66 Displays) and LED

Times OOH:– Till FY 2006

– In April 2006

Hutch, HLL, Sahara, BCCL, Bharti, Pepsi, ICICI, Dabur, Set Max

Key Customers:

7 Stations (Delhi, Mumbai, Kolkata, Chennai, Pune, Ahmedabad and Indore)3 Stations (Bangalore, Hyderabad and Jaipur)22 additional Stations in next 12-18 months

Radio Mirchi:– Till FY 2006

– Launched in April 2006– Planned

8

Business Overview

9

ENIL Key Highlights

• We are operating in high growth industry

• We are well prepared and well positioned for the increasing competition

• We exceeded our set financial goals for FY06

• We have managed to increase our market share in radio to over 50%

• We have maintained our number 1 status in listenership

• We launched 3 new radio stations in Jaipur, Bangalore and Hyderabad within 75

days of the completion of bidding process

• We won Out-of-Home advertising rights of Delhi Metro (13 stations), Kolkata (80

hoardings) and Delhi-Noida toll bridge (66 displays) for total license fee of Rs

340.0 mn (US$ 7.6 mn) payable over a license tenure of 2 - 5 years

• We have identified our challenges for next year and are working towards

addressing them

10

High Growth Projected for Radio Industry

1.6

1.4

1.11.0

0.7

0.6

0.3

0.0

0.5

1.0

1.5

2.0

Thailand New

Zealand

Singapore World

Average

Philipines China India

Ad Spent as a % of GDP Radio Industry Share in Ad Spend

15.3

12.5

9.48.7

6.5

4.4

2.9

-2.0

1.0

4.0

7.0

10.0

13.0

16.0

Philipines New

Zealand

Singapore World

Average

Thailand China India

Source: Zenith Optimedia

Indian Ad Spend: Potential for ad industry to grow to Rs 480 billion ($11 billion) in 10 years

Indian Radio Industry:PWC estimates radio industry to grow at

CAGR of 32% in next 5 years increasing its ad share to 5% and size to Rs. 12 billion

11

• Roll-out of Phase II of privatization

• Fixed License Fee regime changed to OTEF + Revenue share

• Annual license fee 4% of gross revenues

• FDI in Radio increased to 20%

• From existing 12 cities to 91 cities

• From existing 21 stations to approximately 300 stations

• From existing 7 players to 43 players

Growth opportunity for private FM:

From current 3% (Rs 3.7 billion) of Rs 129 billion to 8% (Rs 38.0 billion) of Rs 480 billion in ten years starting FY 07

Radio Industry: Positive Regulatory Reforms

12

We are now present in all the top 13 towns (pop 2 mn +)

Chennai

Delhi

Kolkata

PuneMumbai

Ahmedabad

Lucknow

Kanpur

Jaipur

Hyderabad

Bangalore

Surat

Phase I excluding Indore

Phase II – A+ & A circles

Nagpur

• ENIL won 25 licenses in the Phase II bidding

• Only company to have presence in top 13 towns with population of 2 mn+

• Only incumbent in all the four metros

13

Player Total stations Of top 13 towns

• Adlabs 44 7

• South Asia/Kaal Radio 40 10

• ENIL 32 13

• Radio City 20 11

• Dainik Bhaskar 17 4

• Bag Films 10 0

• Zee/Century 8 0

• Thanthi/Today/Midday 7 1/3/7

• HT/Positive/Raj Pat 4 4/0/1

• Red FM 3 3

FM Radio – Competitive landscape

14

The Radio Station India Tunes To

20.519.0

12.0

2.5

0.0

10.0

20.0

30.0

Radio Mirchi Radio City Red FM Go

Lakhs

Listnership in MumbaiListnership in Delhi

#1 Listenership Share

13.5

17.3

36.8

0.0

10.0

20.0

30.0

40.0

Radio Mirchi Radio City Red FM

Lakhs

Source: MRUC Survey, AC Neilson (ORG-Marg-Wave 8, fieldwork Jan 06 toMar 06. All Sec 12+)

Source: MRUC Survey, AC Neilson (ORG-Marg-Wave 8, fieldwork Jan 06 toMar 06. All Sec 12+)

15

Mirchi a “Must-Have” Media Vehicle

Radio Mirchi Today Reaches More People Than The #1 TV/Print Media Brands

16

• Innovative Content:– Strong relationships with Hindi, Bengali and

Tamil film fraternity

– Exclusive music breaks

– Mature research culture – music/listenership

• Success in Diverse Markets– Experience in establishing superior linkage

between Marketing and Programming

– Customized content in 10 distinct markets

Track Record of Developing Innovative Content & Operating in Diverse Markets

We Are Best Positioned For Success In New Cities Across India

17

Superior Sales Capabilities

• Dedicated 180 member sales team across 10 centers

• Offering unique and innovative solutions to clients– Hutch ‘Pink Campaign’

• Strong emphasis on training

• Mirchi Activation: Pioneers in the radio space

18

8,500 9,00010,500

12,00013,500

15,500

17,500

0

4000

8000

12000

16000

20000

2004 2005 2006 2007E 2008E 2009E 2010E

Indian OOH Industry Growth

Source: PWC report - The Indian Entertainment and Media Industry

PWC estimates Out-of-Home media industry to grow at CAGR of 14% in next 5 years increasing its ad share to 7% and

size to Rs. 17.5 billion

• Tendered PropertiesIncreasing tender of properties to organized players

• Long term ContractsOpportunities for acquiring or taking long term rights for attractive sites in selected cities

• Technology & InnovationBring in technology based innovative OOH solutions like Light-emitting diode (LED) screens

Indian Out of Home Industry and Growth Drivers

Rs. In mn

19

Bus SheltersTill Dec 2008

South Mumbai & West Mumbai (except Central) : Target Quality: Affluent Population Mass1400+Sites : Choice & Coverage

DND Flyover

Mumbai

Metro Stations

Metro CP : 7 Stations Till 2007Metro Dwarka : 6 Stations Till 2011

Delhi

80+ Hoardings : spread across city Till 2011

Kolkata

66 displays : spread across flyway Till 2008

Must-Win Market

Must-Win Market

Must- Presence Market

Multi City- Multi MixTimes OOH Media : Ability to Offer Integrated Marketing Solutions

20

• Imported 4 LED screens

– Put up 1 LED screen at Sahara Mall –Gurgaon

• Planned Rs. 350.0 mn (US$ 7.8 mn) over the time

• Positives of LED

– Dynamic - Television Outdoors, Motion and sound

– Aesthetic - Superior quality of color, Weather Proof

– Flexible - Scalable to any dimension– Three Revenue Streams

Branding

Multiple Clients

Content Sales

Focus on new technology – LED Video Walls

21

• Focus on big ticket events:

Conceptualizing, marketing and

execution

– Filmfare Awards, International Film

Festival of India, 2004, Femina Miss

India

– Ability to raise sponsorships

• Marquee client list:

– Bennett Coleman & Co Ltd, Samsung

India Ltd., SET India Pvt Ltd, State

Bank of India, Mastercard, Deutsche

Bank, Castrol India

• Now focusing on “wellness” not “illness”

approach

360o

Fashion & Lifestyle Third Party

• Produce and manage Filmfare awards & Femina Miss India Pageant (Internal clients – Times Group)

• Recently started building brands / properties such as the FDCI Fashion awards

• Conducted over 600 events in fiscal 2006

• Focus on moving towards big events

360° Experience: Move towards Large Ticket Business

2004200420042004 2005200520052005

22

• Rapid roll-out of stations

• Talent identification, training and retention

• Retaining and growing absolute listenership numbers

• Cost management – especially w.r.t marketing and payroll

• Music royalty regime – rationalization

• Development of listenership research standards and spread

across the country

Key Challenges facing ENIL

23

Board of Directors And Management

24

• Mr. Deepak M Satwalekar – Non-Executive and Independent Director

– MD and CEO , HDFC Standard Life

– Director on the board of Infosys, Asian paints, Nicholas Piramal & others

• Mr. N Kumar – Non-Executive and Independent Director

– Vice Chairman, Sanmar Group

– Director on the board of Bharti tele, The India Cement, MRF Ltd & others

• Ms. Rama Bijapurkar – Non-Executive and Independent Director

– Marketing Consultant

– Director on the board of Infosys, Godrej Consumer, Crisil, UTI Bank & others

• Mr. Ravi Dhariwal – Non-Executive Director

– Executive Director, BCCL

– Director on the board of BCCL, TIML

• Mr. A.P. Parigi – Managing Director and Chief Executive Officer

Board Driven company with emphasis on best corporate governance practices

Board of Directors

25

Strong & Experienced Management Team

Kaushik Ghosh, Senior Vice President, Marketing

Sharath Chandra, COO, ENIL International

Deputy CEO

Prashant Panday

Experience 17 years overall51/2 at ENIL

CFO

HarvinderjitSingh Bhatia

Experience16 years overall,

5 at ENIL

Business Head Times OOH

Farid Kureshi

Experience16 years overall,

4 at ENIL

SVP Legal & CS

Anil Fernandes

Experience15 years overall,

3 at ENIL

SVP, People Innovation

Prasad Swaminathan

Experience10 years overall,41/2 at ENIL

EVP, Regulatory Affairs

Ravi Narula

Experience33 years overall51/2 at ENIL

Tapas Sen, Executive Vice President, Programming

Nandan Srinath, COO, ENIL India

CEOAP Parigi

Experience

34 years overall

51/2 years at ENIL

Col. (Retd.) Nataraja Thiagarajan, Chief Technical Officer

26

Key Financials FY 2006

27

ENIL Financials - Key Highlights

• Initial Public Offer of 13.2 mn shares of Rs.10/- each at a premium of Rs. 152/-

aggregating issue proceeds of Rs. 2,138.4 mn

• Investment of Rs. 40.0 mn in 100% subsidiary Times Innovative Media Pvt.

Limited (TIMPL)

• One Time Entry Fee of Rs.1,301.0 mn for 25 new radio licenses and Migration fee

of Rs. 815.2 mn for existing 7 stations for 10 years

– Amortization of annual migration fee Rs.81.5 mn accounted in fourth quarter

• The Company granted 109,360 options at an exercise price of Rs.90/- each under

ESOS

• Written back provision for license fees of Rs. 98.8 mn no longer required

28

Consolidated Results in line with Analyst Expectations…

15.1%13.6%15.0%Margin (%)

212.4226.0230.0PAT

29.0%24.7%26.4%Margin (%)

408.3412.0415.0EBITDA

998.41,255.01,140.0Operating Expenses

1,406.71,667.01,555.0Total Income

ActualENAMJMMSIn Rs. mn

• TIMPL Actual results are for 5 months period from October 27, 2005 to March 31, 2006, as compared to annualised numbers in the Analyst report

• EBITDA Margins of 29% in FY06

• Exceptional item of Rs. 98.9 mn not included in PAT

29

ENIL Standalone - Strong Financial Performance

550

762

1202

0

200

400

600

800

1000

1200

1400

FY04 FY05 FY06

Revenue in Rs. Million

-245

-122

381

-300

-200

-100

0

100

200

300

400

FY04 FY05 FY06

EBITDA in Rs. Million

30

ENIL Standalone - How did we Spend…

21%

19%

19%

16%

7%

5%

5%3% 3% 2%

31

ENIL Standalone: Key Financials FY 2006

(5.29)

(23.5%)

(179.3)

(16.1%)

(122.6)

884.8

762.3

FYE 2005

(Audited)

5.48Recurring EPS (Rs.)

16.4%Margin (%)

196.6PAT

31.8%Margin (%)

381.4EBITDA

820.5Operating Expenses

1,201.9Total Income

FYE 2006

(Audited)In Rs. mn

• Increase in airtime sales of 57% in FY06 over FY05

• EBITDA Margins of 32% in FY06

• Exceptional item of Rs. 98.9 mn not included in PAT

32

Ownership Structure and Share Price Performance

33

Ownership Structure

By Category Top Shareholders

FII Holding increased from 12.45% at the time of allotment to 18.07%

72%

18%

6% 2% 1%1%

Promoters FIIs

Individuals Corporates

Directors & Employees Others 1.32%0.63Citigroup

1.62%0.77Morgan Stanley

1.68%0.80Macquarie

2.64%1.26HSBC (ME)

7.13%3.39BCCL

9.48%4.51Fidelity

64.18%30.52TIML

% HoldingShares (mn)

1. Total Paid up capital (in no. of shares) as on 31st March, 2006 (after exercise of Green Shoe Option) is 47,563,665

2. Others include Mutual Funds, Banks, HUF, Clearing Members, NRIs and Trusts Data as of March 31, 2006

34

Share Price Performance (1)

• 48.6% gain against Allotment price of Rs.162 per share

• Market Cap. :Rs. 11,446.2 mn

• Promoters holding : Rs. 8,162.3 mn200

220

240

260

280

15-Feb 1-Mar 16-Mar 31-Mar 18-Apr 2-May 15-May

Price (Rs.)

-

1.6

3.2

4.8

6.4

8.0

Share

s (Million)

Price (15/05/06) : Rs. 240.7

All time High : Rs. 287.5

All time Low : Rs. 197.0

Weighted Average : Rs. 239.8

Share Price

Volume

1. Share Price as traded on National Stock Exchange till May 15, 2006

19-Apr-06Fourth quarter and annual results above expectations

35

Media Companies Market Performance...

38.8x11,446240.7162.015-Feb-06ENIL

46.9x3,80084.970.004-Apr-01Mid-day Multimedia

NM15,640257.270.019-May-04NDTV

66.3x24,720527.7530.001-Sep-05HT Media

46.3x14,820295.2320.022-Feb-06Jagran Prakashan

1,12,530

13,290

Market Capital

(Rs. mn)

25-Nov-93

10-Jan-01

Listed On

152.3x272.830.0Zee Telefilms

50.5x333.9120.0Adlabs Films

P / E(1)

(x)

Price

15/05/06 (Rs.)

Allotment Price (Rs.)

1. Price / earning (P / E) multiple is calculated by dividing current price with reported LTM ordinary EPS

Stock Market is Valuing expected robust growth in Indian Media Industry

Source: Economic Times, BSE

36

Future Business Outlook

37

• Expand our footprint in radio broadcasting

– Rapid roll-out of 22 new stations

– Explore opportunities to become FM radio broadcasters in international

markets

• Maintain market leadership in fast growing radio industry

– Continuously invest in brand building and programming innovation

– Launch Visual Radio through mobile phones

– Leverage our footprint to capture additional income

– Exploit additional revenue streams like Mirchi Activation

Bright Future Outlook - ENIL

38

• Focus on Out-of-Home media growth

– Expansion of the network of out-of-home media sites managed by us

– Explore opportunities to lease sites on a long-term basis

– Introduce innovative technology and processes

• Establish long-term client relationships for Experiential Marketing

– Establish ourselves as a provider of innovative solutions

– Create own event properties at an appropriate time

– Focus on Life style, Fashion shows and Exhibitions

Bright Future Outlook - TIMPL

39

• News & Current Affairs

• FDI/FII cap

• Multiple frequencies

• Tradability

• Limitation on share transfer of main promoter for 5 years

Radio Industry: Pending agenda

Thank You

41

Back-ups

42

ENIL Consolidated: Key Financials FY 2006 (Above the Line Items)

29.0%

71.0%

19.7%

32.4%

14.3%

4.6%

100.0%

2.3%

1.2%

13.0%

83.5%

% of

Revenue

408.3EBITDA

17.0Out of Home Media

998.4Total Operating Expenses

276.9Employee Costs

455.7Administration and Other Exp.

64.3License Fee

Production Expenses:

201.5Other Production expenses

32.0Other Income

1,406.7

183.6

1,174.1

FYE 2006

(Unaudited)

Total Income

Event Income

Airtime Sales

In Rs. mn

43

ENIL Consolidated: Key Financials FY 2006 (Below the Line Expenses)

3.0%42.7 Depreciation

15.1%212.4PAT

17.7%Effective Tax rate (%)

3.2%45.6Taxation(1)

18.3%258.0 PBT

5.8%81.5 Amortisation of Migration Fee

26.1

408.3

FYE 2006

(Unaudited)

1.9%Interest

Less:

29.0%EBITDA

% of

RevenueIn Rs. mn

Note:

1. For ENIL tax calculated as per provisions of Section 115JB of Income Tax Act, 1961 (Minimum Alternate Tax), TIMPL tax is calculated at normal tax rates

44

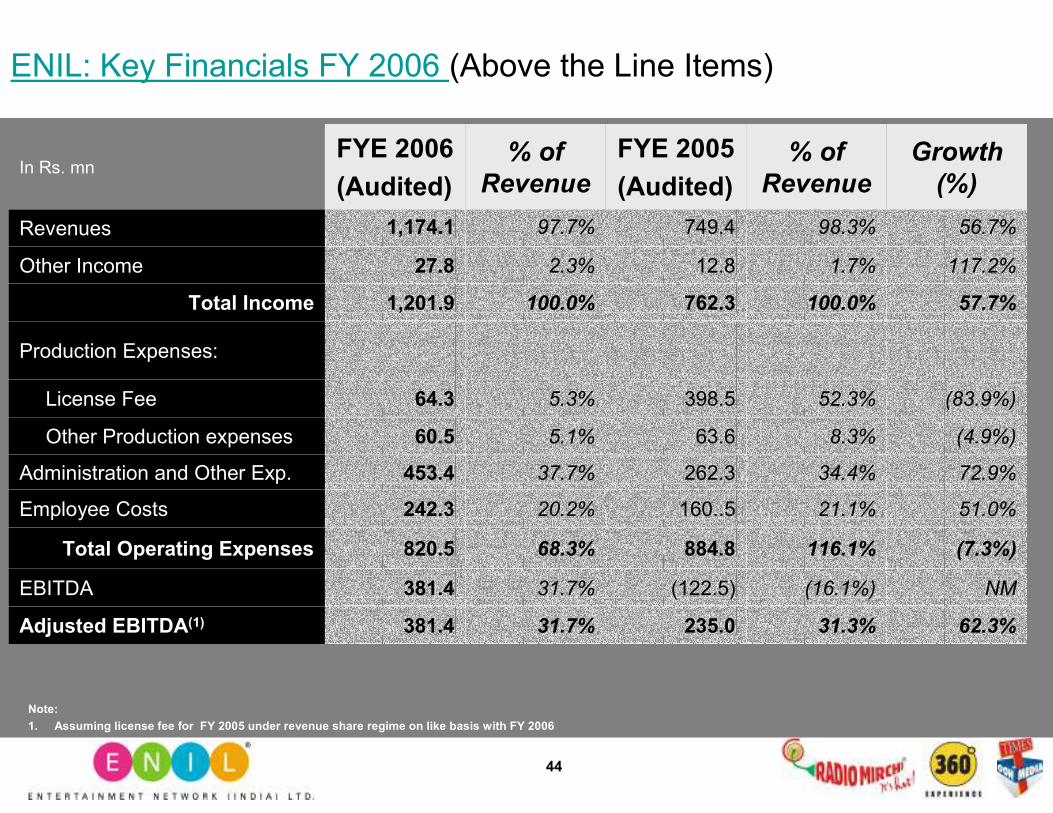

ENIL: Key Financials FY 2006 (Above the Line Items)

235.0

(122.5)

884.8

160..5

262.3

63.6

398.5

762.3

12.8

749.4

FYE 2005

(Audited)

31.3%

(16.1%)

116.1%

21.1%

34.4%

8.3%

52.3%

100.0%

1.7%

98.3%

% of

Revenue

62.3%

NM

(7.3%)

51.0%

72.9%

(4.9%)

(83.9%)

57.7%

117.2%

56.7%

Growth

(%)

31.7%

31.7%

68.3%

20.2%

37.7%

5.1%

5.3%

100.0%

2.3%

97.7%

% of

Revenue

381.4Adjusted EBITDA(1)

1,201.9Total Income

381.4EBITDA

820.5Total Operating Expenses

242.3Employee Costs

60.5Other Production expenses

453.4Administration and Other Exp.

Production Expenses:

64.3

27.8

1,174.1

FYE 2006

(Audited)

License Fee

Other Income

Revenues

In Rs. mn

Note:

1. Assuming license fee for FY 2005 under revenue share regime on like basis with FY 2006

45

ENIL: Key Financials FY 2006 (Below the Line Expenses)

(23.5%)16.4%Margin (%)

21.7%53.441.8 Depreciation

NM(179.3)196.6PAT

NM15.3%Effective Tax rate (%)

NM0.135.5Taxation(1)

NM(179.2)232.1 PBT

(100%)0.3Preliminary Expenses w/off

(23.5%)19.3%Margin (%)

(100%)NA81.5 Amortisation of Migration Fee

25.9

381.4

FYE 2006

(Audited)

793.1%2.9Interest

Less:

NM(122.6)EBITDA

Growth

(%)

FYE 2005

(Audited)In Rs. mn

Note:

1. Tax calculated as per provisions of Section 115JB of Income Tax Act, 1961 (Minimum Alternate Tax)