date: june 5, 2020 subject: land value capture policy study

TRANSCRIPT

DATE: June 5, 2020 SUBJECT: Land Value Capture Policy Study The Land Value Capture Policy Study, attached, was brought to the Joint Board and Mayors’ Council Finance Committee on March 12, 2020 and the full Mayors’ Council on May 28, 2020. This study of potential land value capture approaches for TransLink was requested by the Board and Mayors’ Council as part of broader research into a Funding Strategy for TransLink. Materials were developed with external stakeholders throughout Fall 2019 and Spring 2020, prior to the COVID-19 pandemic. The scope of the study was established in collaboration with Metro Vancouver staff and TransLink retained Coriolis Consulting to perform the study based on their expertise on land economics and urban planning. The study:

1) Quantifies the amount of land value uplift that can be created by transit infrastructure in this

region; and 2) Identifies the challenges and opportunities for TransLink to use land value to generate new

revenue for transit investments, increase walking, cycling, and transit ridership, and support transit-oriented affordable rental housing creation.

In the report, Coriolis recommends pursuing both direct participation in strategic land acquisition and urban development, and land-based taxes and charges (e.g. property transfer tax, benefitting area tax, community amenity contributions). Based on feedback from Mayors’ Council in Spring 2020, TransLink will also continue to evaluate a variable-rate Development Cost Charge (DCC). The potential for any of the Land Value Capture mechanisms to be implemented as a part of TransLink’s funding framework will require additional discussion based on the economic conditions of the region during the re-building phase following the pandemic. ATTACHMENT

• Land Value Capture Report by Coriolis Consulting Corp. & Wollenberg Munro Consulting Inc.

Evaluation of Land Value Capture and Urban

Development as Sources of Revenue for TransLink

February 2020

Prepared for:

TransLink

By:

EVALUATION OF LAND VALUE CAPTURE AND URBAN DEVELOPMENT AS SOURCES OF REVENUE FOR TRANSLINK

PAGE I

Table of Contents

1.0 Introduction ........................................................................................................... 1

1.1 Background ........................................................................................................................... 1

1.2 Terms ..................................................................................................................................... 1

1.3 TransLink’s Goals ................................................................................................................ 2

1.4 Study Participants ................................................................................................................ 4

1.5 Professional Disclaimer ....................................................................................................... 4

2.0 Foundations of Land Value Capture ................................................................... 5

2.1 Rationale ............................................................................................................................... 5

2.2 The Factors that Create Urban Land Value........................................................................ 5

2.2.1 Geography and Context ......................................................................................... 6

2.2.2 Local Zoning and Infrastructure ............................................................................. 7

2.2.3 Site Characteristics ................................................................................................ 7

2.3 The Role of Land Owners .................................................................................................... 8

2.4 Approaches Using Taxes, Charges, and Zoning ............................................................ 10

2.4.1 One-Time Taxes and Charges ............................................................................ 10

2.4.2 Recurring Taxes ................................................................................................... 10

2.5 Approaches Using Direct Participation in Strategic Land Acquisition and

Development ....................................................................................................................... 11

2.5.1 Strategic Land Acquisition and Disposition ......................................................... 11

2.5.2 Participation in Urban Development Projects ...................................................... 12

2.6 Other Approaches Not Considered in this Report .......................................................... 14

2.7 Advantages and Disadvantages of Land Value Capture ................................................ 15

2.7.1 Taxes ................................................................................................................... 15

2.7.2 Development Charges and Zoning ...................................................................... 17

2.7.3 Land Acquisition and Disposition ......................................................................... 17

3.0 Approaches Currently Applied in BC ................................................................ 18

3.1 Taxes, Development Charges, and Zoning ...................................................................... 18

3.1.1 Federal Government ............................................................................................ 18

3.1.2 Provincial Government ........................................................................................ 18

3.1.3 Metro Vancouver.................................................................................................. 20

3.1.4 Municipalities ....................................................................................................... 20

3.1.5 TransLink ............................................................................................................. 23

EVALUATION OF LAND VALUE CAPTURE AND URBAN DEVELOPMENT AS SOURCES OF REVENUE FOR TRANSLINK

PAGE II

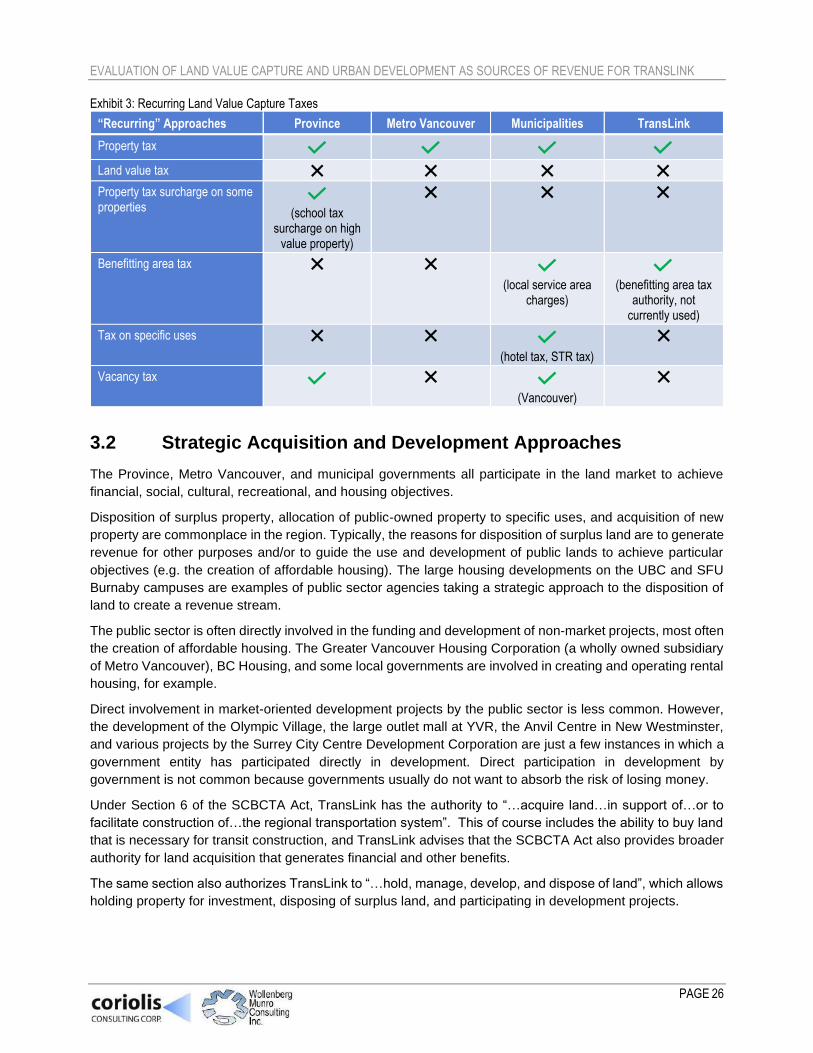

3.1.6 Summary of Taxes, Charges, and Zoning Mechanisms Currently Used in BC .. 25

3.2 Strategic Acquisition and Development Approaches .................................................... 26

4.0 Examples of Approaches Used by Other Agencies Outside of BC ................ 28

4.1 Examples of Approaches to Support Transit Investment .............................................. 28

4.1.1 Canada ................................................................................................................ 28

4.1.2 USA ...................................................................................................................... 29

4.1.3 Outside North America ........................................................................................ 29

4.2 Examples of Approaches to Support Affordable Housing ............................................. 31

4.3 General Observations ........................................................................................................ 31

5.0 Transit Investment, Rezoning, and Land Value ............................................... 33

5.1 Transit Investment and Densification .............................................................................. 33

5.2 Transit Investment and Price/Rent Premiums ................................................................. 34

5.2.1 Sales Price Premium for Multi-Family Strata Residential Units ........................... 34

5.2.2 Lease Rate Premium for Commercial Space ...................................................... 35

5.2.3 Residential Rents ................................................................................................. 37

5.2.4 Implications for Case Studies .............................................................................. 37

5.3 Transit Investment and Rezoning: Case Studies ............................................................ 37

5.3.1 Summary of the Multi-Family Residential Case Studies...................................... 38

5.3.2 Summary of Commercial Case Studies ............................................................... 39

5.4 Conclusions ........................................................................................................................ 39

6.0 Impacts of Different Approaches ...................................................................... 41

6.1 Impacts on Land Owners, Tenants, and Developers ...................................................... 41

6.1.1 Property Taxes (General, Surcharge, Benefitting Area) ...................................... 41

6.1.2 Development Charges ......................................................................................... 43

6.1.3 Density Bonusing and CACs ............................................................................... 43

6.1.4 Land Acquisition and Disposition ......................................................................... 44

6.1.5 Development ........................................................................................................ 44

6.1.6 Summary of Impacts ............................................................................................ 44

6.2 Impacts on Other Levels of Government ......................................................................... 45

7.0 Stakeholder Perspectives .................................................................................. 47

7.1 Summary of Stakeholder Perspectives ............................................................................ 47

7.2 Response to Stakeholder Input ........................................................................................ 49

8.0 Possible Directions for TransLink ..................................................................... 51

8.1 Aligning Approaches and Objectives ............................................................................... 51

EVALUATION OF LAND VALUE CAPTURE AND URBAN DEVELOPMENT AS SOURCES OF REVENUE FOR TRANSLINK

PAGE III

8.2 Evaluating the Options and Identifying Those to Consider Further in the Near Term52

8.2.1 Capital Gains Tax ................................................................................................ 52

8.2.2 Foreign Purchaser Tax ........................................................................................ 53

8.2.3 Property Transfer Tax .......................................................................................... 53

8.2.4 Revisions to TransLink DCC Framework ............................................................ 53

8.2.5 CAC and Density Bonus Revenue Sharing ......................................................... 54

8.2.6 Across-the-Board Increase in Property Taxes ..................................................... 54

8.2.7 Land Value Tax .................................................................................................... 54

8.2.8 Benefitting Area Tax ............................................................................................ 55

8.2.9 Strategic Land Acquisition and Disposition ......................................................... 56

8.2.10 Participation in Urban Development Projects ...................................................... 56

8.3 Examining the Approaches with Potential in More Detail .............................................. 57

8.3.1 Benefitting Area Tax ............................................................................................ 58

8.3.2 CAC and Density Bonus Revenue Sharing ......................................................... 60

8.3.3 Property Transfer Tax .......................................................................................... 63

8.3.4 Strategic Acquisition and Disposition of Land ..................................................... 64

8.3.5 Participation in Urban Development Projects ...................................................... 65

8.4 Potential Uses of New Revenue ........................................................................................ 67

8.5 Policy Questions to be Addressed ................................................................................... 68

8.5.1 Benefitting Area Tax ............................................................................................ 68

8.5.2 CAC and Density Bonus Revenue Sharing ......................................................... 68

8.5.3 Property Transfer Tax .......................................................................................... 69

8.5.4 Strategic Acquisition and Disposition of Land ..................................................... 69

8.5.5 Participation in Urban Development Projects ...................................................... 69

9.0 Recommendations .............................................................................................. 70

Appendix 1: Case Studies ............................................................................................ 72

A.1 Approach ............................................................................................................................. 73

A.2 Identification of Case Studies ........................................................................................... 73

A.2.1 Multi-Family Residential Case Studies ................................................................ 73

A.2.2 Commercial Case Studies ................................................................................... 74

A.2.3 Summary List of Case Studies ............................................................................ 74

A.3 Data Sources ....................................................................................................................... 74

A.4 Detailed Descriptions of Case Studies ............................................................................. 75

Case Study #1: Strata Multi-family Residential Redevelopment in the Broadway Corridor . 75

EVALUATION OF LAND VALUE CAPTURE AND URBAN DEVELOPMENT AS SOURCES OF REVENUE FOR TRANSLINK

PAGE IV

Case Study #2: Market Rental Multi-family Residential Redevelopment in the Broadway

Corridor ................................................................................................................ 77

Case Study #3: Strata Multi-family Residential Redevelopment in Burquitlam .................... 79

Case Study #4: Strata Multi-family Residential Redevelopment in Fleetwood .................... 80

Case Study #5: Strata Multi-family Residential Redevelopment in Lynn Creek .................. 82

Case Study #6: Commercial Redevelopment in the Broadway Corridor ............................. 83

Case Study #7: Commercial Redevelopment in Surrey City Centre .................................... 85

A.4 Summary of Case Studies and Implications for TransLink ........................................... 87

A.5 Attachments (Pro Formas) ................................................................................................ 88

EVALUATION OF LAND VALUE CAPTURE AND URBAN DEVELOPMENT AS SOURCES OF REVENUE FOR TRANSLINK

PAGE 1

1.0 Introduction

1.1 Background

TransLink funds its share of the capital and operating cost of the regional transit system using a variety of

revenue sources, including transit fares, property tax, fuel tax, parking tax, and the new regional transportation

DCC that came into effect in January 2020.

The region needs more investment in transit infrastructure, requiring additional funding. TransLink is

interested in exploring new sources of revenue that will be sustainable in the long run and that have the

potential to advance regional policies. The new regional TransLink DCC that came into effect in January 2020

is an example of expanding the funding base, by obtaining revenue from new urban development projects.

This report examines the potential for TransLink to generate revenue from two kinds of approaches that are

linked to the increasing value of land and the continuing strong demand for residential and commercial

development in this region:

• One approach is called Land Value Capture, which is a broad term that refers to ways to obtain public

revenue or benefits from growth in the value of urban land. The rationale for land value capture is that

public investment in community building and infrastructure is a key driver of land value growth, so it is

reasonable to capture some of the growth in value to pay for the infrastructure.

• The second approach is a greater role in urban development activity by TransLink. TransLink has lands

that are no longer needed for transportation purposes and lands that could accommodate development

on top of or beside transit infrastructure, and it is acquiring land for future transit investment in places

where there will be future development opportunities. By being more active in urban development,

TransLink could create a new stream of revenues.

TransLink commissioned Coriolis Consulting Corp. and Wollenberg Munro Consulting Inc. to analyze the

potential to generate revenue using these two approaches.

1.2 Terms

1. “Land Value Capture” means any mechanism whereby a public entity obtains benefits or revenue

derived from land value or increases in land value. There is a wide range of land value capture

approaches which can be divided into two groups:

a) One-time forms of capture. These are methods of land value capture that occur at a particular event,

such as the sale of a property, development approval, or rezoning. “One-time” does not mean only

once in the history of a property, but once per major event or transaction.

b) Recurring forms of capture. These are methods of land value capture that are ongoing (usually

annually) and are not linked to specific events or transactions. This group includes property taxes.

2. “Urban Development” means direct participation in the urban land market and in the creation of new

residential or commercial projects. There are three main ways in which TransLink could be involved in

urban development:

a) Disposition of surplus lands. TransLink has property that was acquired in the past but is no longer

needed for transportation purposes. This includes entire sites, portions of sites, or the air rights above

transit facilities. These lands could be made available to the market for urban development. Prior to

the disposition of such lands, TransLink has the opportunity to capture value associated with

EVALUATION OF LAND VALUE CAPTURE AND URBAN DEVELOPMENT AS SOURCES OF REVENUE FOR TRANSLINK

PAGE 2

rezoning. Disposition of sites or air rights is a form of land value capture, as it takes advantage of

market-wide gains in land value that have occurred since acquisition and benefits from any land value

increases that result from transit investment and upzoning. This differs from other forms of land value

capture in that it only applies to property that is owned by TransLink rather than to all properties in

an area subject to a tax or development charge.

b) Strategic acquisition and subsequent disposition of lands. TransLink acquires property for

transportation construction. In some cases (such as new transit stations) there can be opportunities

to acquire more land than the minimum needed for construction, in order to take advantage of the

new accessibility that will be provided by transit service and to ensure that the post-construction

development sites are optimized in terms of size and configuration. In these cases, TransLink can

benefit from land value gains due to accessibility, rezoning, and market uplift between the time of

acquisition and disposition (which usually will span several years). Strategic acquisition/disposition is

also a form of land value capture, benefitting from market-wide gains in land value and from transit

investment and upzoning. This approach involves more risk than the disposition of already-owned

surplus property, as it requires new capital investment in property and it usually requires holding land

for several years.

c) Development. There may be cases in which TransLink can best meet its goals by participating in

development projects on its lands, rather than just marketing them to developers. While there is

additional risk involved in development, there is the potential to earn developer profit and the potential

to shape development projects to achieve regional goals such as supporting transit-oriented

affordable housing or enhancing the transit experience for riders. Participation in development

projects is the one approach considered in this report that is not technically a form of land value

capture. The gain in land value of owned property is land value capture, but the separate (albeit

related) decision to be an equity participant in a project is a business decision intended to earn a

profit (not to capture land value). We include development participation because TransLink is

interested in exploring this possible source of revenue and because any disposition of surplus

property carries with it the possibility to be involved in development on the property.

1.3 TransLink’s Goals

The main focus of this work is to identify possible new sources of revenue to pay for transit investment and

transit operations. Generating revenue is not the only reason to consider land value capture and involvement

in urban development, though.

The region has many land use-transportation integration priorities, as outlined in TransLink’s Regional

Transportation Strategy and Metro Vancouver’s Regional Growth Strategy. In particular, there is strong

evidence that affordable rental housing in transit-oriented locations is an excellent strategy for addressing

housing affordability, because transit-oriented housing can reduce household transportation cost, reduce

commuting time (which can be an important benefit to lower income households trying to improve their

circumstances), and reduce construction cost by reducing the need for costly underground parking.

Affordable, transit-oriented housing is also good for building public transit ridership, as lower income

households (and particularly renters) tend to be high transit users.

In addition to building ridership, facilitating urban development at transit stations provides the higher density,

proximity, physical infrastructure, and placemaking that support walking and cycling.

EVALUATION OF LAND VALUE CAPTURE AND URBAN DEVELOPMENT AS SOURCES OF REVENUE FOR TRANSLINK

PAGE 3

Consistent with its mandate to advance the Regional Transportation Strategy and Regional Growth Strategy,

TransLink is looking to this study to help it understand opportunities and challenges for using land value

capture to support three regional goals:

1. Identify new sources of revenue for regional transportation purposes that can be applied to:

• New investment in transportation infrastructure.

• Repaying existing debt for past investments in infrastructure.

• Transit operating costs.

2. Support transit-oriented affordable rental housing. Metro Vancouver needs more affordable rental

housing, especially in transit-oriented locations because renters tend to be more likely to use transit and

they benefit from the reduced cost of living that transit offers over car ownership. Being involved in the

urban land market, either through the terms of sale/lease of TransLink surplus sites or direct participation

in development, gives TransLink the ability to facilitate the construction of more rental units. Consistent

with the Metro Vancouver Transit-Oriented Affordable Housing Study1, “transit-oriented affordable rental

housing” generally refers to housing with these characteristics:

a. Rental tenure.

b. Affordable to households with incomes in range of $35,000 to $60,000 per year (about 50% to 80%

of regional median household income). Household income below $35,000 is considered very low and

generally requires non-market, public sector subsidized housing solutions. Household income above

$60,000 is in the moderate range and is generally able to support market rent in some parts of the

region.

c. In proximity to rapid transit or the Frequent Transit Network, allowing access to employment with

reasonable commute times and without having to rely on owning a private vehicle.

The emphasis is on affordable, transit-oriented rental housing because households in this segment are

above-average users of transit, are not having their needs met by market rental housing, and are capable

of paying enough rent to make new construction financially viable without ongoing subsidy provided land

(or density) is available at little cost.

3. Increase walking, cycling, and transit use. Increasing the non-automobile number of trips requires

supportive infrastructure (e.g. bike lanes) and it requires that transit be well-integrated with adjacent

development so that it is convenient for pedestrians and cyclists. Being involved in urban development

creates the opportunity to directly influence the form and character of development so that it is transit

supportive.

Land value capture can also be used to achieve other goals. For example, land value capture can be a tool

for wealth distribution, for reducing land values or housing prices (usually as part of a broader strategy to

make housing more affordable), or for reducing investment in property solely for capital appreciation

purposes. This report for TransLink is not intended to consider ways to achieve these kinds of outcomes.

This report focuses on the possible use of land value capture and possible involvement in urban development

as mechanisms for achieving TransLink’s three primary goals listed above.

1 Coriolis Consulting Corp. and Wollenberg Munro Consulting Inc., “Reducing the Barrier to High Land Cost: Strategies for Facilitating More Affordable Rental Housing Construction in Metro Vancouver. Phase 2 of the Transit-Oriented Affordable Housing Study.” March 2019.

EVALUATION OF LAND VALUE CAPTURE AND URBAN DEVELOPMENT AS SOURCES OF REVENUE FOR TRANSLINK

PAGE 4

1.4 Study Participants

TransLink established a staff Working Group to manage this project and provide direction to the consultants.

TransLink invited Metro Vancouver to participate on this team, particularly regarding ways in which TransLink

might use land value capture to support affordable rental housing at transit-oriented locations in the region.

Representatives of local government and the development industry participated in two rounds of workshops

to review the consultant team’s work and also provided written comments on the first draft of the report.

The consultant team completed all of the technical analysis and provided independent opinions and

recommendations, as contained in this final report. The opinions expressed in this report do not necessarily

reflect the opinions of TransLink, Metro Vancouver, or any of the stakeholders who provided input.

1.5 Professional Disclaimer

This document may contain estimates and forecasts of future growth and urban development prospects,

estimates of the financial performance of possible future urban development projects, opinions regarding the

likelihood of approval of development projects, and recommendations regarding development strategy or

municipal/regional policy. All such estimates, forecasts, opinions, and recommendations are based in part on

forecasts and assumptions regarding population change, economic growth, policy, market conditions,

development costs, and other variables. The assumptions, estimates, forecasts, opinions, and

recommendations are based on interpreting past trends, gauging current conditions, and making judgments

about the future. As with all judgments concerning future trends and events, however, there is uncertainty

and risk that conditions change or unanticipated circumstances occur such that actual events turn out

differently than as anticipated in this document, which is intended to be used as a reasonable indicator of

potential outcomes rather than as a precise prediction of future events.

Nothing contained in this report, express or implied, shall confer rights or remedies upon, or create any

contractual relationship with, or cause of action in favour of, any third party relying upon this document.

In no event shall Coriolis Consulting Corp. or Wollenberg Munro Consulting Inc. be liable to TransLink or any

third party for any indirect, incidental, special, or consequential damages whatsoever, including lost revenues

or profits.

EVALUATION OF LAND VALUE CAPTURE AND URBAN DEVELOPMENT AS SOURCES OF REVENUE FOR TRANSLINK

PAGE 5

2.0 Foundations of Land Value Capture

2.1 Rationale

Land value capture is already in use, or is being considered, as a revenue-generating tool in many urban

regions around the world. There is extensive interest in this tool because there is a compelling case for the

public sector to capture some of the value that the public sector creates via community building and

infrastructure investment and then reinvest this value to create further public benefit.

The rationale for land value capture can be summarized in this way:

• The value of urban land is based heavily on how it can be used and its access to urban infrastructure.

• Increases in land value (as distinct from the value of improvements) are almost entirely due to public

actions, such as zoning, infrastructure investment, and the creation of the legal and economic framework

within which communities develop. The public sector should benefit from these actions rather than all of

the benefit accruing to private owners of land.

• Investment in land is not as productive for the economy as investments that create jobs and income, so

taxation policy should generally discourage passive land investment in favour of more active forms of

investment.

• In urban areas, land should be used to its maximum potential, not left vacant or under-used, so property

tax policy should encourage development.

• Land cannot move, so tax avoidance is not a concern.

It is important to note that “land value capture” makes a distinction between land value and total property

value. The value of each urban property is the sum of its land value and its improvements value.

Improvements mainly refers to buildings. Most users of urban land tend to “bundle” land and improvements,

in the sense that a person puts a value on their home, or a business is willing to pay a certain rent to occupy

space in a particular location. But it is possible to un-bundle the value into its land and improvements

components. Land value capture focuses on the land portion, because this is the part of property value that

is created mainly by public sector actions and this is the passive part of property investment that is

comparatively unproductive for the economy, whereas improvements value is created by private investment

in new construction which creates economically and socially useful space for housing and employment.

Land value capture perhaps sounds like a new form of taxation, but in BC property owners are already

exposed to several kinds of land value capture taxes and charges that go by other names. Property tax,

property transfer tax, and the new Provincial school tax surcharge are just some of the ways that many land

owners are taxed (on the value of land and improvements). Developers already deal with other forms of land

value capture, including Development Cost Charges and Community Amenity Contributions. So, the idea is

not new. The purpose of this report is to explore how TransLink might use land value capture to achieve its

goals.

2.2 The Factors that Create Urban Land Value

In order to understand the rationale for public sector land value capture, it is important to consider how urban

land value is created in the first place.

EVALUATION OF LAND VALUE CAPTURE AND URBAN DEVELOPMENT AS SOURCES OF REVENUE FOR TRANSLINK

PAGE 6

The factors that determine land value can be divided into three broad categories:

1. Geography and context:

• An urban area’s natural geographical setting, climate, physical environment, and topography

determine the appeal of the area as a place to live, work, develop, and invest. These factors also

affect the amount of land that is physically suitable for urban use.

• The international, national, and provincial contexts create the overall market for urban land in a

region, by driving the demand for housing and employment space. Population growth, job growth,

low mortgage rates, the draw of our Provincial health care and school systems, and local and non-

local real estate investment interest are examples of contextual forces that contribute to property

demand, putting upward pressure on land value.

2. Local zoning and infrastructure:

• The supply of developable land is partly determined by geography, but local land use regulation

defines how land can be used, which has a huge impact on land value by establishing allowable uses

and densities.

• Local/regional infrastructure (including water and sewer systems, transportation networks, and

community facilities) creates the context within which urban development can occur.

3. Individual site characteristics:

• While the above factors create the contextual market for urban land, the unique qualities and

immediate surroundings of each site determine the site’s value in the market context.

• Site size, views, soil conditions, accessibility, and topography are just a few of the individual features

that make some sites more valuable than others.

These factors are examined in more detail below.

2.2.1 Geography and Context

Natural Setting and History

What we now call Metro Vancouver was one of the early major urban settlements in BC after European

colonists began to arrive in large numbers. As this region developed, it gained increasing prominence as a

gateway and major urban centre with a large concentration of employment, a convergence of road and rail

networks, a port, and a concentration of specialized services in health care, education, management, and the

professions. The region’s natural advantages (natural environment, gateway, climate, scenic quality) and in

more recent days its culturally diverse population and its placement in the international time zone system

have positioned it well for economic ties to Asia, the US, and Europe.

The region also has features which impose a hard constraint on land availability. The ocean, mountains, and

US border hem the region into a relatively small area.

This momentum of geography and history set the region on a long arc of strong demand and constrained

supply, causing long term growth in the value of land.

International Context

In the modern world, people, goods, companies, and capital are highly mobile. Global economic,

environmental, social, and political forces create the impetus for some people to want to live in or invest in

places other than where they currently live. This mobility affects many countries including Canada, which

welcomes newcomers and new investment that add to the demand for urban land in attractive locations.

EVALUATION OF LAND VALUE CAPTURE AND URBAN DEVELOPMENT AS SOURCES OF REVENUE FOR TRANSLINK

PAGE 7

National Context

Canada as a nation state and a national economy has major competitive advantages that lead to the demand

for urban land, including:

• A framework of property rights and the rule of law.

• A comparatively safe, tolerant, and culturally diverse community structure.

• An extensive network of air, marine, rail, transit, and highway infrastructure.

• A system of immigration and offshore investment management.

• A strong central bank and national banking system.

This national context attracts and supports population growth, business growth, and local and non-local

investment, all of which contribute to growth in urban land value.

Provincial Context

The Province of BC is responsible for key elements of the context that supports land value growth, including:

• The health care system.

• K to 12 public education.

• Post-secondary education.

• Regional infrastructure including highways, bridges, and transit.

• Economic development initiatives that attract investment and companies.

This Provincial framework contributes to land value growth in many communities, although there are declines

in some due to challenges such as the reduction of output in the forestry sector. The effect of the Provincial

education and health care system is magnified in Metro Vancouver, as it has the largest concentration of

post-secondary institutions and specialized health care facilities and services.

The Province also has a significant influence on the supply of developable land in Metro Vancouver, via the

Agricultural Land Reserve which protects farmland but also has the effect of shrinking an already-constrained

supply of land for development for urban use.

2.2.2 Local Zoning and Infrastructure

Local governments and regional agencies also make a significant contribution to the forces that create and

increase land value. The planning and zoning framework governs land use, height, and density which affect

the value of land. Local government provides infrastructure and amenities, regional agencies provide the

water system (Metro Vancouver Water Department), sewer networks (GVS&DD), electricity (BC Hydro),

natural gas (FortisBC), and transportation/transit infrastructure (TransLink).

2.2.3 Site Characteristics

The national, provincial, and regional/local contexts create an overall market for urban land in Metro

Vancouver, driving demand for housing and employment space and delimiting the supply of land for

development. Within this regional market, site specific factors determine the market value of individual parcels

of land. These include:

• The specific zoning regulations that apply to each site.

EVALUATION OF LAND VALUE CAPTURE AND URBAN DEVELOPMENT AS SOURCES OF REVENUE FOR TRANSLINK

PAGE 8

• Accessibility by road and transit for residential and commercial uses and by rail, sea, or air for many

industrial uses.

• Services and utilities to the site.

• Nearby amenities and services (e.g. schools, shopping, parks, recreation/community centres).

• Soil conditions and topography.

• Special features such as views or waterfront.

These features determine the value of land. Investments in improvements increase total property value but

do not change the value of the land.

2.3 The Role of Land Owners

In the breakdown of factors that drive land value, all of them can be considered contextual, inherent in the

site itself, or the result of actions by others (mostly local government) that directly benefit the parcel of land.

The land owner does not really have a direct ability to cause land value to rise. Certainly land owners can

invest in improvements, which increase the total value of the property, but this does not change the value of

the land. The land owner can seek rezoning, but local government makes this decision. Therefore, many

commentators treat land value gain as a sort of windfall for the owner: the owner benefits from public

decisions (such as rezoning, transit investment, nearby public amenities such as parks) without having

directly paid for them. However, the characterization of the land value gain as a pure windfall makes it sound

accidental, which is not entirely true:

• Land owners have usually made deliberate decisions about where and when to buy land for housing,

business use, development, or investment. They may not cause land value gain, but they make a choice

that presumably includes some thought about where there is an opportunity. An investment in land

involves taking risk, weighing options, and making choices. This is different than finding money on the

sidewalk. While land values have risen rapidly in Metro Vancouver during the last decade, there have

Urban Land Value

International, national, provincial context, and geography

Local zoning, infrastructure and facilities

Individual site characteristics

EVALUATION OF LAND VALUE CAPTURE AND URBAN DEVELOPMENT AS SOURCES OF REVENUE FOR TRANSLINK

PAGE 9

been periods of decline or very low growth (e.g.

1981 to 1988, 1995 to 2002, 2008 to 2009, 2018

to 2019), indicating that there is risk.

• Owners of houses or residential strata units may

have made tradeoffs when they acquired their

homes. For example, suppose two households

each have a house purchase budget of

$1,000,000. One opts for a small, older home

near the region’s core so family members can

walk to work, school, or shopping. This purchase

involves $800,000 of land value and $200,000

of improvements. The other opts for a suburban

location because of a higher priority on larger,

newer space. This purchase involves $200,000

in land value and $800,000 in improvements,

and also means that this household drives more.

Now suppose land values in both cases rise by

25% over some period. The first household will

realize a higher land value gain and, if a land

value tax mechanism were in place, would pay

more tax. This may be perceived as inequitable

considering the tradeoff that was made at the

outset.

• Developers or land owners who seek rezoning

would receive a windfall if extra density is

available at no cost. But if they exchange cash or amenities to obtain increased density there is no land

value windfall as long as the amount they pay is commensurate with the value of the density.

The conversation about land value capture in Metro Vancouver is in part stimulated by the rapid rise in land

values over the last decade or so.

The trend in Metro Vancouver house prices from 2005 to 2018 as indicated by the Greater Vancouver Real

Estate Board’s MLS Home Price Index2 is summarized in Exhibit 1.

Exhibit 1: Average Annual % Increase in Metro Vancouver Housing Prices by Type of Property (2005 to 2018)

Average Annual Increase in Metro Vancouver

Single detached 8.7%

Strata apartment 9.1%

Source: MLS Home Price Index, Greater Vancouver Real Estate Board.

All owners of residential property in the region have seen significant percentage increases in the land value

component of the total value. The dollar value increases are much larger in some areas (such as the west

side of Vancouver) because values were higher to start with, but the percentage gains are high across the

region.

2 The index is based on the estimated annual change in the sales price of a benchmark property within each submarket.

An investment in land involves taking risk, weighing options, and making

choices. If land value goes up it's not the same as the lucky accident of finding money on the sidewalk.

Household "A" purchases $1 million modest older house on lot with

higher land value ($800,000 land; $200,000 improvements)

Household "B" purchases $1 million newer house on lot with lower land

value ($200,000 land; $800,000 improvements)

Land Value Capture impacts Household "A"more than

Household "B" because "A" has higher land value

EVALUATION OF LAND VALUE CAPTURE AND URBAN DEVELOPMENT AS SOURCES OF REVENUE FOR TRANSLINK

PAGE 10

2.4 Approaches Using Taxes, Charges, and Zoning

This section summarizes the main forms of land value capture that involve taxes and charges applied to

urban areas. The approaches are divided into one-time and recurring methods.

2.4.1 One-Time Taxes and Charges

There are several commonly used ways to derive revenue from land value at a point in time, usually at a

transaction or at a development milestone. These include:

• Taxes on the transfer of property ownership at time of sale. These are sometimes called stamp taxes

and in BC are called Property Transfer Tax.

• Income tax or capital gains tax on the increase in property value when sold. Different jurisdictions

treat capital gains differently. In Canada most capital gains are taxed favourably compared to income and

gains on principal residences are exempt from taxation.

• Fees charged on new development at the time of permit approval, mainly to raise revenue to pay the

capital cost of community infrastructure. These are variously called development levies, impact fees, or

development charges. In BC, they are called DCCs or (in the City of Vancouver) DCLs.

• Public benefits in exchange for new development entitlements (density), usually at rezoning. Many

jurisdictions use density bonusing or negotiated contributions at the time of rezoning to obtain public

benefits or amenities. These are commonly called Community Amenity Contributions (CACs) or density

bonusing in BC.

There are some important features of these one-time approaches:

• Property transfer taxes are paid by the purchaser and do not require a cash outlay by the existing owner.

• Capital gains tax occurs when the owner sells, meaning the sales proceeds provide the cash used to pay

the tax.

• Fees paid at development approval are paid by developers as part of the process of creating a new

project and tend to come out of what otherwise would be land value.

• Public benefits at rezoning are an exchange of density, which creates new land value, for amenities and

infrastructure that use some of the new value to address the needs and impacts of growth.

2.4.2 Recurring Taxes

The second major group of land-based revenues consists of different kinds of ongoing taxes on property.

These include:

• Tax on Property Value or Land Value. Almost all jurisdictions levy annual tax on the value of land,

improvements, or (most commonly) both. The most common approach is for land and improvements to

be taxed at the same rate, although there are a few jurisdictions that allow different tax rates for land and

improvements.

• Property Tax Surcharge. Some jurisdictions apply a property tax surcharge to some categories of

property, such as property above a certain value or in a particular location. The BC School Tax surcharge

on high value residential property is an example of a value-based surcharge and the BC Speculation and

Vacancy Tax is an example of a surcharge on a particular group of properties based on location and

occupancy.

EVALUATION OF LAND VALUE CAPTURE AND URBAN DEVELOPMENT AS SOURCES OF REVENUE FOR TRANSLINK

PAGE 11

• Benefitting Area Surcharge. Some jurisdictions apply a tax surcharge to properties that benefit from a

specific public sector capital project. These are sometimes called betterment taxes, special service area

taxes, local improvement taxes, or special assessment districts. Several jurisdictions in the US levy

additional property taxes on property in defined transit service areas.

These recurring charges are paid by the owners or users of the property out of their income or wealth, not

out of proceeds from disposition or development of the property. The taxpayer must have a source of income,

have cash on hand, or borrow to cover the cost of the tax, unless there is some system of exemption or

deferment.

2.5 Approaches Using Direct Participation in Strategic Land

Acquisition and Development

Land value capture mechanisms are intended to derive revenue from all urban property that benefits from

investments in infrastructure or from land use decisions. Land value capture by a public entity does not have

to be associated with any direct participation in the land market or in urban development projects. However,

direct participation in the urban land market, or in development projects, is another way that the public sector

can reap benefits from infrastructure investments and zoning changes.

2.5.1 Strategic Land Acquisition and Disposition

All levels of government are involved in acquiring and selling/leasing land for a wide range of purposes

including generating revenue, supporting housing, and meeting civic social, recreational, and cultural

objectives. Agencies involved in delivering transportation infrastructure are of necessity involved in the land

market because they require property for permanent use for stations and corridors as well as temporary use

during construction for staging and storage. This need for property creates an opportunity to take advantage

of subsequent gains in land value due to increased accessibility after a new line goes into service, changes

in zoning, and general growth in land value in an overall rising market.

Public agencies with long term involvement in transportation infrastructure delivery also end up with

properties that were needed in the past but are no longer needed for transportation purposes and so are

partly or entirely surplus. Depending on where they are and how long they have been held, the value of these

properties may be significantly higher than original acquisition cost.

Under the general heading of strategic land acquisition and disposition, there are several ways in which a

transportation agency can earn revenue or achieve other objectives such as encouraging transit ridership or

supporting affordable housing:

• Disposition of property that has become surplus to the agency’s functional transportation requirements.

Sites once needed for storing/maintaining transit vehicles or transfer stations may no longer be required

due to changes in technology, transportation networks, or other factors.

• Disposition of sites required for temporary use during major construction once construction is complete.

• When acquiring land for new infrastructure, acquisition of more than the bare minimum needed for transit

use. There are several ways to create these opportunities:

o The potential for air rights development over transit infrastructure can be maximized if care is taken

in acquiring sufficient land to create the physical ability for such development and if care is taken in

the siting and design of transit infrastructure.

EVALUATION OF LAND VALUE CAPTURE AND URBAN DEVELOPMENT AS SOURCES OF REVENUE FOR TRANSLINK

PAGE 12

o If the land required for transit construction necessitates the acquisition of a part of a property, it can

be financially advantageous to acquire the entire property either to ensure that post construction

there is a workable development site or to avoid the situation that it costs more to acquire a partial

property (because of negative impacts on the residual portion) than to just buy the whole site.

o If the land required for transit construction is adjacent to property that is a strong candidate for land

assembly that creates additional, better development potential.

These opportunities create the potential to generate three kinds of land value gain:

• Usually considerable time passes between acquisition and subsequent disposition of surplus property. In

strong land markets, the growth in land value can exceed a public agency’s cost of capital meaning that

even if the funds to buy land must be borrowed the eventual sale will produce a net gain.

• The area around new transit stations is often a candidate for changes in land use and increases in density,

which usually add to land value. Even when much of the land value lift caused by rezoning is captured

by local government, in the form of development levies or mechanisms such as CACs, a portion of the

lift accrues to land owners.

• New transit infrastructure improves accessibility, which tends to add a price premium on residential and

commercial space in the vicinity of the transit. This price premium translates to increased land value for

the owner.

In many cases, land acquired by a transit agency can benefit from all three of these gains so it can become

very attractive to make early strategic investments in land when planning for major new infrastructure projects.

In addition to generating revenue, land acquisition also creates the potential to achieve other objectives.

When an agency disposes of developable land, via sale or lease, there is an opportunity to influence land

use and the form and character of development in ways that can support affordable housing or that support

transit ridership. Mechanisms to achieve objectives regarding affordable housing and transit ridership support

include:

• Terms of sale or lease of land to developers. TransLink could, for example, require the inclusion of

affordable rental housing units when it disposes of development sites and could require that the physical

design of projects be supportive of walking, cycling, and transit use.

• Zoning. When TransLink seeks rezoning of property prior to disposition it could work with local

governments to include zoning provisions regarding affordable rental housing or to require design

elements that are supportive of walking, cycling, and transit use.

• Funding. TransLink could apply some of the proceeds from strategic land acquisition/disposition to

investments in affordable housing (directly or by contributing to other initiatives such as the regional

affordable fund being proposed by Metro Vancouver as one of the outcomes of its Transit-Oriented

Affordable Housing work).

There are tradeoffs, of course, because incorporating rental housing results in less land value (unless local

government is willing to provide significantly more new density for rental than it would for strata). It is up to

the agency to decide which objectives to advance and how to prioritize different potential public benefits.

2.5.2 Participation in Urban Development Projects

If a transit agency sells or leases surplus lands to the development sector, the agency benefits from gains in

land value that have occurred since the time of acquisition, especially if new transit infrastructure has been

built in that time and if allowable land use and density have changed. A private developer who acquires the

EVALUATION OF LAND VALUE CAPTURE AND URBAN DEVELOPMENT AS SOURCES OF REVENUE FOR TRANSLINK

PAGE 13

land then benefits from any land value growth between the time of site acquisition and the completion of the

project, and also (in a successful project) earns a developer profit.

By directly participating in development projects, a public agency can tap some or all of this revenue potential.

TransLink could be involved in urban development projects in various ways:

• Rather than sell or lease surplus sites or development parcels to developers, TransLink could take on

the role of developer either alone or in partnership with other developers.

• TransLink could be the developer of rentable space within or adjacent to new transit infrastructure (e.g.

retail space as part of the station or rentable space in the air rights above a station).

• TransLink could take ownership of space within a development project in lieu of being paid for a

development parcel. In this case, TransLink would not be a developer but would take on some

development risk by taking space instead of cash.

Direct participation in development projects is not technically a form of land value capture. The land value

capture is realized when a surplus property is made available for development, either to an arms-length

developer or to an internal development division. Participating in the actual development on the surplus

property would be a separate business decision by TransLink that involves injecting new equity and/or

deciding to invest the value of the land into the project in order to make a profit in addition to capturing the

(increased) value of the land. Of course, non-profit developers work on a different business model, but

presumably TransLink would only become directly involved in development projects as a means of generating

revenue (i.e. profit) to be applied to the organization’s investment objectives.

Direct participation in development is very different from land value capture as it involves significant possible

risk, including:

• Market risk. Large scale, high density development projects typically involve two or more years between

commencement and completion. During this time market conditions can change. If prices and the rate of

sale or lease-up increase, then developers benefit. But the market can go soft, reducing or eliminating

profit and creating the risk of loss.

• Cost risk. Developers use various methods to reduce risk of increasing construction cost, but there is

always exposure to delay, mistakes, material or labour issues, and other factors that can increase cost.

If costs rise more than sales prices, then profitability is impaired.

• Approvals risk. The process of obtaining municipal development approvals involves risk related to

municipal requirements (e.g. off-site works, sustainability features, design) and timing. Risk can be

significantly mitigated by resolving zoning-related matters before committing to a project but there are

still risks inherent in the development permit and building permit phase of a development project,

particularly for large projects and projects that involve any significant opposition from the public or specific

stakeholder groups.

• Financing risk. Almost all development projects require construction financing. Depending on the terms

of such financing, there is a risk that interest rates rise during construction.

• Physical risk. Development projects can encounter soil contamination, problematic geotechnical or

hydrological conditions, or damage during construction (e.g. fire, excavation collapse) that increase cost.

These can be mitigated by thorough due diligence work before committing to a project, but some risk

always remains.

• Partner risk. An agency may prefer to work with a developer partner rather than be fully responsible for

a project. This has the advantage of adding expertise to the team, spreading risk, and reducing the need

EVALUATION OF LAND VALUE CAPTURE AND URBAN DEVELOPMENT AS SOURCES OF REVENUE FOR TRANSLINK

PAGE 14

for agency equity or borrowing, but it comes with a new set of risks associated with the legal and financial

structure of the deal. A partner may become insolvent, act outside the terms of agreements, cause

negative publicity, or do other things that impair the financial or reputational position of the public sector

partner. These risks can be mitigated by careful partner selection and robust legal agreements, but these

risks cannot be completely eliminated.

Because of the risks involved, the decision to participate directly in urban development projects requires

caution and considerable advance work to ensure that the potential benefits are significant enough to warrant

the risks. A transit agency can mitigate the risks of being involved in development by:

• Focusing on projects that are at transit locations. Market risk is lower in high demand locations.

• Focusing on projects that include high-demand product.

• Extensive due diligence, appropriate provision for contingency, and detailed risk assessment.

Direct participation in development can generate revenue to apply to transit, affordable housing, and other

objectives. In addition, direct participation in development would enable TransLink to create affordable rental

housing and to design projects to incorporate features that support walking, cycling, and transit use.

2.6 Other Approaches Not Considered in this Report

TransLink asked us about four other approaches, which are not considered in this report for the following

reasons:

1. Cash-in-Lieu of Off-Street Parking. Off-street parking is an expensive component of high density

residential and commercial construction. In transit-oriented locations, demand for parking is lower and

developers are usually interested in reducing municipal zoning requirements for off-street parking when

the cost saving is greater than any loss in revenue.

Reduced parking requirements can be implemented by changing zoning requirements, without requiring

any contribution from developers. Alternatively, there are systems in which a reduced parking

requirement can be obtained in exchange for a cash-in-lieu payment, with the funds applied to transit

investment.

This means of generating revenue is not considered in this report for these reasons:

• Development regulation in BC is completely the responsibility of local government and is not likely to

be restructured to give other agencies a role in defining zoning requirements such as parking.

• Cash-in-lieu of parking is a revenue generating tool but it is not a land value capture mechanism. If

the cash payment is equal to what the cost of parking would have been, there is no impact on

development economics so there is no transfer of land value (and developers are not likely to build

less parking if they have to pay for it anyway). If the cash payment is less than the cost of the parking,

this can actually put upward pressure on land value by reducing development cost.

2. Hotel and Short-Term Rental Tax. Some local governments impose taxes on specific uses. However,

these are not land value capture mechanisms so they are not considered in this report:

• Hotel taxes are based on room revenue, so they are a tax on revenue not on value. There may be

an indirect effect on the value of hotel properties by reducing net operating income, but this is not the

aim.

• Taxes or fees on short term rentals are a means of regulating the use, not taxing value.

3. Tax Increment Financing. Another approach that is often mentioned is called Tax Increment Financing

(TIF). TIF works like this:

EVALUATION OF LAND VALUE CAPTURE AND URBAN DEVELOPMENT AS SOURCES OF REVENUE FOR TRANSLINK

PAGE 15

• A public agency with property tax authority borrows money (either as a loan or by issuing a bond) to

pay for some form of infrastructure that is expected to cause land values and property tax revenues

to rise.

• To provide security for the lender or bondholders, the agency pledges to apply growth in property tax

revenue in the benefitting area to repayment. This pledge is a way to reduce the risk of default.

So, TIF is not land value capture per se. It is just a means of using increased value (i.e. the growth in

property taxes in a specific area) as security to obtain financing. There is no “new money”; the gains in

property tax revenue caused by infrastructure investment are going to occur whether or not TIF is used;

the TIF is simply an allocation of new taxes to the specific purpose of repaying borrowed funds.3 This

approach can make sense if a local government can only obtain financing by pledging the future tax

growth in a defined area. In jurisdictions that do not have difficulty borrowing, it makes more sense for a

lender or bond buyer to have repayment obligations secured by the entire tax base of the agency, not

just the portion of the tax base inside the TIF area. For these reasons, TIF is not directly relevant to

TransLink’s situation and is not considered in this policy analysis report.

4. Penalties on Low Density Development. Some stakeholders have suggested applying a charge or tax

on low density development as a disincentive to development that is not transit-oriented. Such a charge

would be an indirect form of land value capture, in the same way that DCCs put downward pressure on

a developer’s ability to pay for land. The existing property tax system in BC acts as a kind of disincentive

to maintaining under-developed properties (because property is taxed based on its development

potential) but the use of triple net leases can diminish the effectiveness of this disincentive because the

tax is passed to tenants. There are two reasons why we do not include this kind of charge in this report.

First, such a charge is mainly intended as a disincentive to influence urban development patterns. We

take the view that if there is a desire to limit low density development, this should be accomplished directly

by regional planning policy and by municipal land use planning rather than indirectly by a charge levied

by a regional transportation agency that has no direct statutory role in land use planning or development

regulation. Second, in Metro Vancouver there is a diminishing supply of land available for new low density

residential development. While a charge of this type may be an effective influence on land use, it is not

likely a sustainable long term revenue stream.

2.7 Advantages and Disadvantages of Land Value Capture

2.7.1 Taxes

Governments have a variety of ways to raise tax revenue from individuals and corporations, including income

tax, sales tax (such as PST or gasoline tax in BC), value added tax (such as GST in Canada), user fees, and

property tax. Each of these revenue tools has advantages and disadvantages in terms of fairness,

progressiveness (i.e. rising progressively with income in order to make the tax burden more equitable in its

impact), economic efficiency (minimizing negative impacts of taxation on the economy), the ability to modify

behaviour (e.g. using a carbon tax to reduce fuel consumption), and other factors.

With this wide variety of tax measures available, it is important to consider whether there are particular

advantages and disadvantages to taxing the value of land.

3 There are special circumstances in which a TIF-like instrument creates new revenue for a local government. For example, in Alberta municipalities can create Community Revitalization Levy districts in which the Province agrees that any growth in what would have been the Provincial share of property tax is transferred to the municipality. In this case, it is not the “TIF” that is creating new local money, it is the willingness of the Province to transfer revenue to the municipality.

EVALUATION OF LAND VALUE CAPTURE AND URBAN DEVELOPMENT AS SOURCES OF REVENUE FOR TRANSLINK

PAGE 16

The idea of taxing land is not new. In the late 1700’s, Adam Smith advocated taxing land as a means of

generating revenue without reducing total economic output because it does not impede productivity. George

Henry, a 19th century economist, proposed that taxes on income reduce incentive to work and taxes on

production are a disincentive to productivity, but taxes on land do not discourage productive economic activity.

Land investment is passive; capital tied up in land does not generate economic benefits the same way that

investments in business do. Taxing land value can recoup some of the investment that caused land value

gains. Taxing land value can also lead to reductions in land value and house prices, although the advantage

of a lower upfront price (which would lower the requirement for down payment and result in lower mortgage

costs) can be offset by higher ongoing taxation costs.

Note that these are arguments for taxing land but not improvements, which do contribute to productive

capacity and provide benefits such as housing. Taxing land can encourage investment in improvements

(because the tax burden would be spread over more space).

One of the main arguments against recurring taxation of land value is that this tax is unrelated to income or

ability to pay. This concern is often articulated with regard to homeowners whose homes have risen in value

but whose incomes have not. The

counterarguments are that such people can

sell their homes and move to lower value

accommodation or that, in places such as

BC, some households are eligible to defer

property tax (at a very favourable interest

rate) until time of sale. But there is still some

social and political objection to tax policy that

forces people to sell their home, take on

debt, or see their equity decline.

Business owner/occupiers may also face

financial challenges if their taxes rise,

because their business may not generate

enough income to cover the new cost.

Another possible concern is that increased

property taxes can in some cases be passed

on to residential and commercial renters.

The effect of changes in land value on tax revenues depends on the structure of the tax. For example:

• Property taxes in BC are primarily determined by the budget requirements of local government and the

Province. The budget identifies how much property tax revenue is needed, and then this tax burden is

distributed across the assessment base. Changes in value affect how much tax each property pays, but

do not necessarily affect the total tax revenue stream.

• Taxes that are applied to property based on its value (e.g. the Provincial School Tax Surcharge or the

sliding scale used in the Provincial Property Transfer Tax) are affected by changes in land value. Rising

land values will produce more revenue and falling land values will produce less, unless the rates or rate

classes are adjusted.

• Taxes on the proceeds from property disposition (e.g. capital gains tax) are affected by the total volume

and value of dispositions.

When choosing and designing a land value capture approach, there are ways to reduce vulnerability of the

revenue stream to changes in land value.

• can recoup some of the investment that caused the land value gain

• can lead to reductions in land value, which can aid housing affordability

• can encourage investment in improvements

•resilient to changes in land value, as tax rates can be adjusted accordingly

Advantages

...of taxing land value (i.e. not improvement

value).

• land value is unrelated to income or the ability to pay

• may not be affordable for business owners/occupiers

• increased taxes may be passed along to renters

Disadvantages

...of taxing land value.

EVALUATION OF LAND VALUE CAPTURE AND URBAN DEVELOPMENT AS SOURCES OF REVENUE FOR TRANSLINK

PAGE 17

2.7.2 Development Charges and Zoning

These approaches apply to new urban development, not to land owners in general. They have two main

advantages:

• These approaches draw revenue from a new group of payers, rather than continuing to charge transit

riders, auto users, and land owners in general. The charges are paid by developers, but the ultimate

impact tends to be a reduction in the value of development land from what it otherwise would be.

However, owners of development property generally enjoy land value gains even though some of the

value is captured by development fees or zoning related contributions.

• There is a clear link between those who benefit (i.e. land owners benefit from land value gains due to

transit investment and upzoning) and those who pay (i.e. some of the potential land value gain is captured

by the public sector).

There are some disadvantages of land value capture approaches that rely on urban development:

• Because the pace of development varies over time, the revenue stream from development charges or

zoning-based contributions will also vary. This form of land value capture is inherently less regular than

property tax.

• Because of land economics, there is some risk that charges on development or zoning impact the viability

of new development if the charges are not carefully calibrated to continue to provide incentives for

developers and for land owners. If the pace of development is reduced, there will be impacts on

affordability. This risk can be managed by ensuring that charges are set appropriately.

• If land values fall, revenues from these sources could fall, in part because of changes in the value of

density and in part because reduced financial performance of projects could reduce their ability to absorb

cost.

2.7.3 Land Acquisition and Disposition

Participation in the land market has these advantages:

• The agency making the investment in transit can directly capture value by controlling property that will

rise in value due to transit investment and upzoning.

• Disposition of surplus lands and air rights provides capacity for new development that would not otherwise

be available, in transit-oriented locations.

• Control over land disposition allows a degree of control over the form and character of development,

which can support affordable housing, transit ridership, cycling, and walking.

• Strategic acquisition and assembly can create attractive development sites that are better than those that

result from a minimalist approach to land acquisition for transit infrastructure.

There are two potential disadvantages of land value capture via direct involvement in the land market:

• New acquisitions require a source of capital. This means (in the short run) diverting capital that could

otherwise have been used to fund transit or repay debt. Of course, the long term objective is that this

investment pays dividends that can be applied to transit.

• There is risk if the land market declines. In a growing region, this risk tends to be cyclical so it may be

that the main concern is one of timing. Revenue from property disposition may be less predictable and

may have to be postponed to avoid disposition during a downturn.

EVALUATION OF LAND VALUE CAPTURE AND URBAN DEVELOPMENT AS SOURCES OF REVENUE FOR TRANSLINK

PAGE 18

3.0 Approaches Currently Applied in BC

3.1 Taxes, Development Charges, and Zoning

3.1.1 Federal Government

The Federal Government at present has only one significant form of land value capture, which is tax on gains

from the sale of real property. The gains are considered a capital gain or income, with different tax rates,

depending on the nature of the taxpayer and its business. Personal principal residence property is exempt

from taxation.

In the 2019 federal election, some political parties proposed ways in which the federal government might

engage in additional forms of land value capture, including:

• A tax on foreign property owners, at time of purchase or possibly a recurring tax.

• A wealth tax on high net worth individuals, with such tax applying to all forms of wealth including real

property.

The introduction of either or both of these new forms of taxation might, depending on their magnitude, impact

property values and affect the ability of other levels of government to implement land value capture

mechanisms.

3.1.2 Provincial Government

The Province of BC employs a wide range of land value capture taxes to obtain revenue and to achieve other

policy objectives.

One time

The Province’s one-time sources of land value capture include:

a) A 20% tax at time of purchase on the value of property acquired by foreign purchasers.

b) The Property Transfer Tax, which applies to most title transfers of real property (there are various

exemptions such as newly built homes priced below a defined threshold and homes purchased by first

time buyers). This tax is on a sliding scale: 1% on the first $200,000 plus 2% on the portion between

$200,000 and $2,000,000 plus 3% on the portion over $2,000,000 plus (for residential property only) an

additional 2% on the portion over $3,000,000.

c) Tax on the gains from sale of real property, either as income tax or capital gains tax depending on the

nature of the taxpayer and the nature of the taxpayer’s business. Gains on sale of personal principal

residence property is exempt.

Recurring

The Province employs several recurring means of land value taxation:

a) A large share of annual property tax in BC is paid to the Province. In BC, property tax is levied on 100%

of the value of land and 100% of the value of improvements, so it is not solely a land value capture