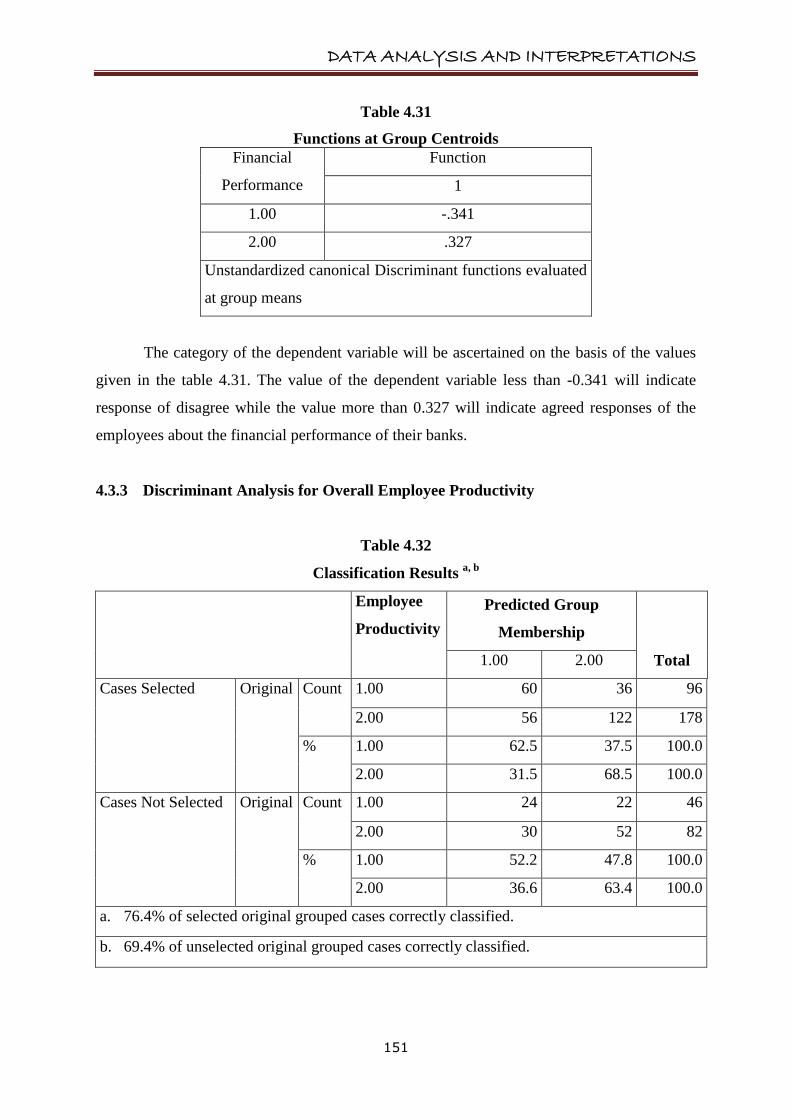

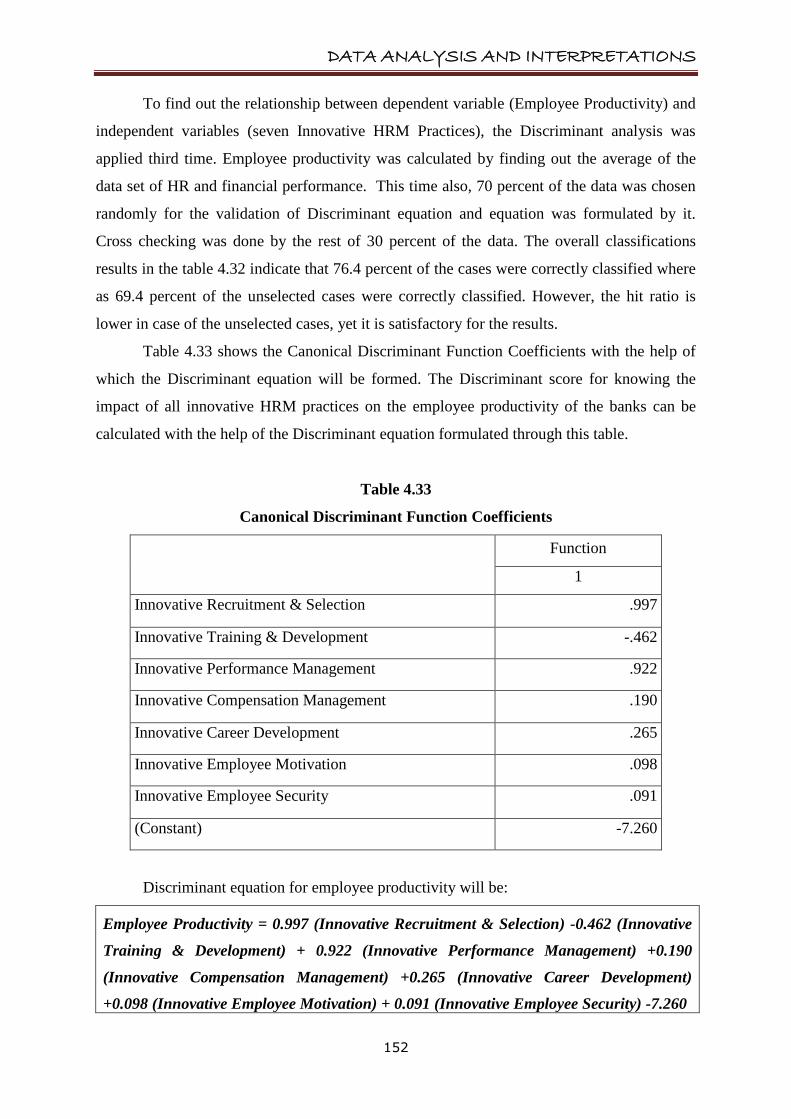

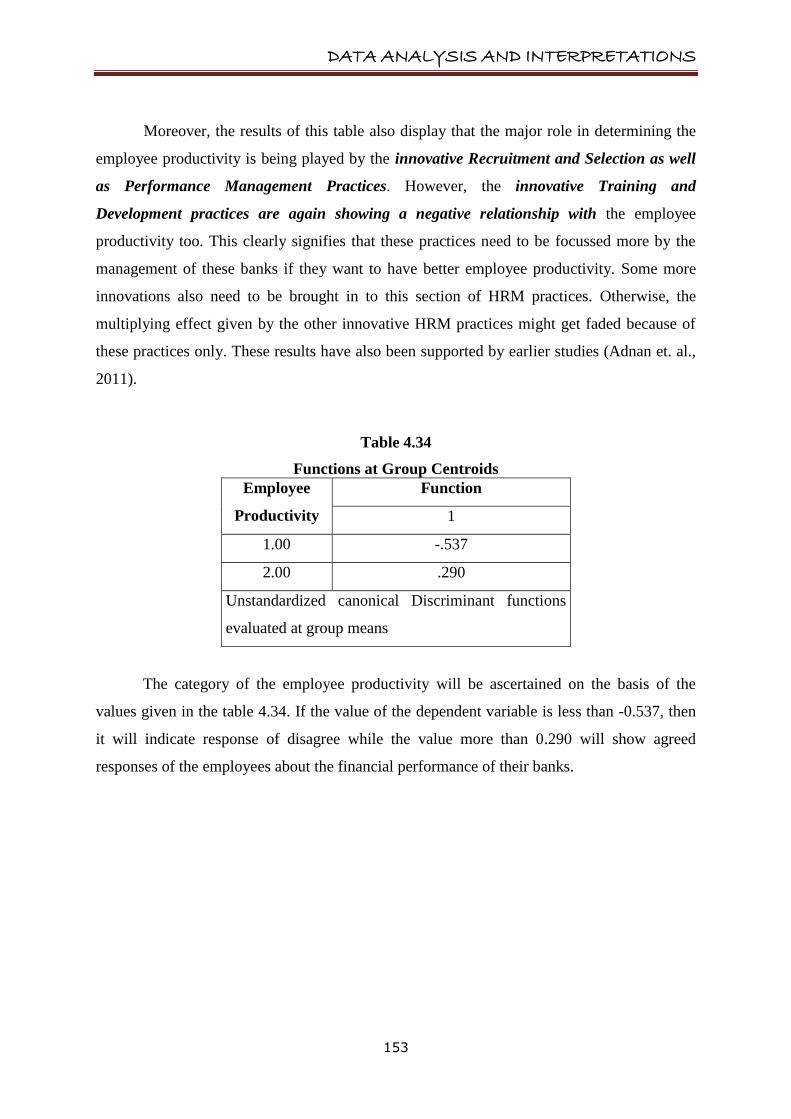

data analysis and interpretations -...

TRANSCRIPT

DATA ANALYSIS AND INTERPRETATIONS

93

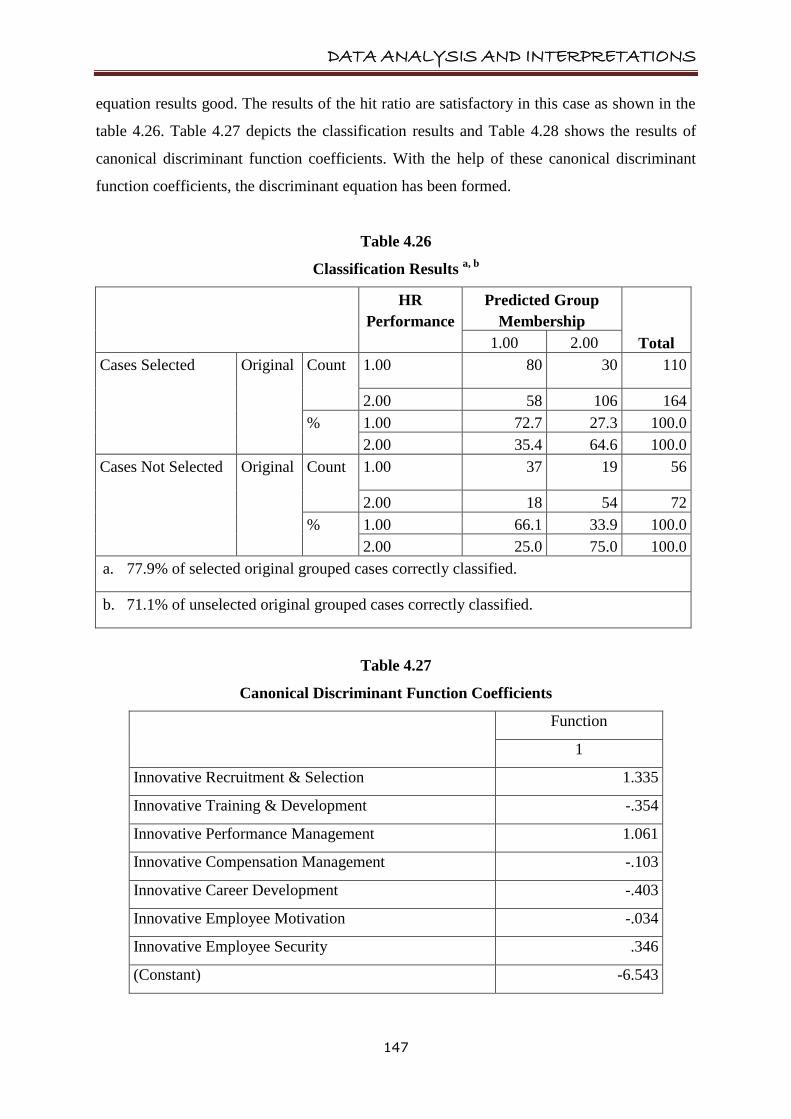

Data collected in this study has been analysed in this chapter and the results have

been discussed regarding the innovative HRM practices, the level of implementation of these

practices, and impact of these practices on employee productivity. The challenging areas of

innovative HRM where the banks are lagging behind have also been revealed in this chapter.

4.1 INNOVATIVE HRM PRACTICES ADOPTED IN PUBLIC AS WELL AS

PRIVATE SECTOR BANKS OF INDIA

The very first objective of the study was to identify the innovative HRM practices

adopted in public and private sector banks of India. After an extensive survey of the literature

and from the responses of the interviews, a list of forty nine innovative HRM practices was

shortlisted under seven heads. These innovative HRM practices have been found in the Indian

Banking sector. All the banks under the study are employing these innovative HRM practices

related to recruitment & selection, training and development, performance management,

compensation management, career development, employee motivation and employee

security.

4.1.1 Innovative Recruitment & Selection Practices

This factor includes all the innovative HR practices which aim at attracting maximum

number of highly talented applicants and selecting the best to achieve competitiveness (Khan,

2010). The nine innovative HRM practices identified under this head were well defined

R&S, selection according to service attitude, holding on policy, availability of bank

communities on social networking sites, checking the profile of candidates on these sites,

selection of professionals just like MBAs, CAs, etc., written exam for R&S, result oriented

policy of R&S, and formal induction of new candidates. These innovative Recruitment and

selection practices have been explained below:

4.1.1.1 Well defined R&S

The respondents of the present study told that one of the major innovative

HRM practices under this head is that there is a well defined recruitment and

selection policy in the banks. This means that everyone is clear about the

recruitment and selection procedure of the banks so that transparency can be

DATA ANALYSIS AND INTERPRETATIONS

94

maintained by the HR department. Earlier, in a few types of banks, there was a

pattern of recruiting people through employee referrals only. But now a days, a

pre defined policy of hiring people is available in banks. Kundu and Malhan

(2009) have also identified this HR practice in one of their studies on service

sector.

4.1.1.2 Selection according to service attitude

Banks are giving due weightage to the service attitude and competence in the

selection procedure. This policy is being adopted by the HR department of the

banks keeping in mind the fact that employees with positive service attitude

will work more efficiently and increase the business ultimately.

4.1.1.3 Holding on policy

One of the major problems that the bank employees were facing in earlier

times was that if they left the organisation due to any work pressure or other

reason, then they were not stopped or hold on by any employer. But now, even

the regional or circle managers of the banks use a “Retention” policy for the

employees so that they may not leave the bank quickly. In this policy, they try

to hold on their employees by solving their issues at regional levels only.

4.1.1.4 Availability of bank communities on social networking sites,

Availability of bank communities on social networking sites is found to be

another innovation in the recruitment process. Popularity of the social

networking sites has forced all the sectors to have this facility enabling the

members of the community to seek the necessary information and to be in

touch with each other.

4.1.1.5 Checking the profile of candidates on these sites

These days, the banks have started using social networking sites for the

purpose of recruitments. With the help of these communities, the HR

department checks the candidate‟s profile on social networking sites to decide

the candidature for the job. All the personal and social information is available

on these sites, with the help of which, cross checking can be done easily.

DATA ANALYSIS AND INTERPRETATIONS

95

4.1.1.6 Selection of professionals.

Banks have also started selecting professionally qualified personnel, e.g.

MBAs, CAs, Agricultural officers etc. for different posts. Earlier, only private

sector banks were employing such professionals for their various departments,

but now, public sector banks have also started using this practice. For example,

advertisements can be seen in the employment newsletters for recruiting the

specialist officers, IT officers, credit managers, and finance managers etc. for

different levels in the State bank of India or even other public sector banks.

This has solved major problems of banks regarding lack of professionally

trained employees in different departments. Moreover, need for giving special

training for such employees has also been reduced to a certain level.

4.1.1.7 Written examination for R&S

There is a policy of written examination in all types of banks for selection of

each level of employees. Earlier the employees were required to appear in the

written examinations only at the entrance level. But now, the provisions have

been changed and they have to take written tests for the higher levels and

internal recruitment also. Moreover, private banks used to recruit their

employees through interviews or campus placements. But now a days, they

have also started conducting written examination for checking the exact

competence and psychology of the candidate.

4.1.1.8 Result oriented policy of R&S

Now a days, the HR department of banks has also started formulating a result

oriented recruitment and selection policy for their banks. This policy helps

them to keep only those employees who are increasing the bank‟s profit and

firing out or demoting the other ones. Even the public sector banks also don‟t

give promotions to those whose past records in terms or branch business are

very poor.

4.1.1.9 Formal induction of new candidates

There has been a formal induction orientation and familiarization process so as

to help new recruits understand the organisation. This also makes the starters

to be comfortable with the work environment of the organisation. Garvey

DATA ANALYSIS AND INTERPRETATIONS

96

(2001), Gomez-Mejia et al. (2003) and Cisco (2006) also argued that without

excellent induction, the execution of organizational strategy may vacillate.

4.1.2 Innovative Training & Development Practices

This factor incorporates all such practices that generate tangible outcome (improved

productivity, quality of products and services, and resource optimization), and intangible

results in terms of enhanced self esteem, high morale, and satisfaction of employees due to

acquisition of additional knowledge, skills, and abilities (Khan, 2010). Executive

development practices have also been considered under this variable. Researchers have

concluded that investment in training yields strategic advantage to the organizations (Kundu,

2000; Bitner & Zeithmal, 2004; Pitkanen 2007 and Blair and Sisakhti, 2007). There are two

situations in which the importance of training is realized or firms will invest in current

employees‟ human capital development through training programs: if it is difficult for firms

to attract talents (Ulrich, Zenger & Smallwood, 1999); and if firms experience low

productivity improvement (Schultz, 1960). Test of trainees, job rotation, customised

training, continuous training need assessment, regular training, encouragement to apply

training learning, and arrangement of special projects are the seven innovative Training

and Development practices found in the present study:

4.1.2.1 Test of trainees

Use of written examination for selecting employees for training is one of the

major innovations mentioned by most of the respondents of the present study.

This helps the employees to be free from any kind of biasness.

4.1.2.2 Job rotation

There is also a provision of job rotation for giving the employees proper

exposure of different departments. With job rotation, an employee is given an

opportunity to perform different jobs, which enriches his skills, experience and

ability to perform different jobs. However, the jobs offered under job rotation

are more or less of the same nature. As a result, he will be skilled to a new job

which is more or less similar to his earlier job. In HDFC Bank, all employees

are involved in the Job Rotation Schedule. In HDFC Bank, the staffs get

rotated in every 6 months and the officers get rotated in every 3 years.

DATA ANALYSIS AND INTERPRETATIONS

97

However, flexibility and due consideration is given to those employees who

have physical difficulty. For such employees, there is no job rotation for

example: Deaf and Dumb. Job rotation is positively associated with

continuous improvement on problem-solving skills that enhances employee

human capital (Marler, 1998).

4.1.2.3 Customised training

Special and separate/customised training programs have also been designed

for different levels of employees in the banks. State bank of India is practising

this practice for more than one and a half decades. Other banks are also

following this innovative HR practice. However, the frequency might be low

in their cases.

4.1.2.4 Continuous training need assessment

In some of the banks, continuous training need assessment of employees by

the HR department is also practised. With the help of continuous training need

assessment, only those employees are sent for the training, who are actually in

the need of the training. Aggarwala (2003) has also explored this innovative

practice in one of her studies.

4.1.2.5 Regular training

One of the major problems, which were earlier found in the banking sector,

was that the training intervals were very high. Even the employees were

trained only once in a decade or even in the entire job life. But now,

innovations in HRM have called for the need for regular training for the bank

employees too. The employees of a few banks are now sent on yearly basis for

training so that they can have their work related doubts resolved and can

groom themselves regularly.

4.1.2.6 Encouragement to apply training learning

Employees are also being encouraged to apply the techniques learnt in their

training program. They are given a chance to apply the information acquired

by them during the training practically so that they may not forget it ever.

DATA ANALYSIS AND INTERPRETATIONS

98

4.1.2.7 Arrangement of special projects

To make the learning effective, some banks have the practice of selecting the

staff for special project teams meant for bank‟s effectiveness. Private sector

banks like HDFC and YES bank are sending their employees for special

projects training so that they can get some specialised skills and knowledge.

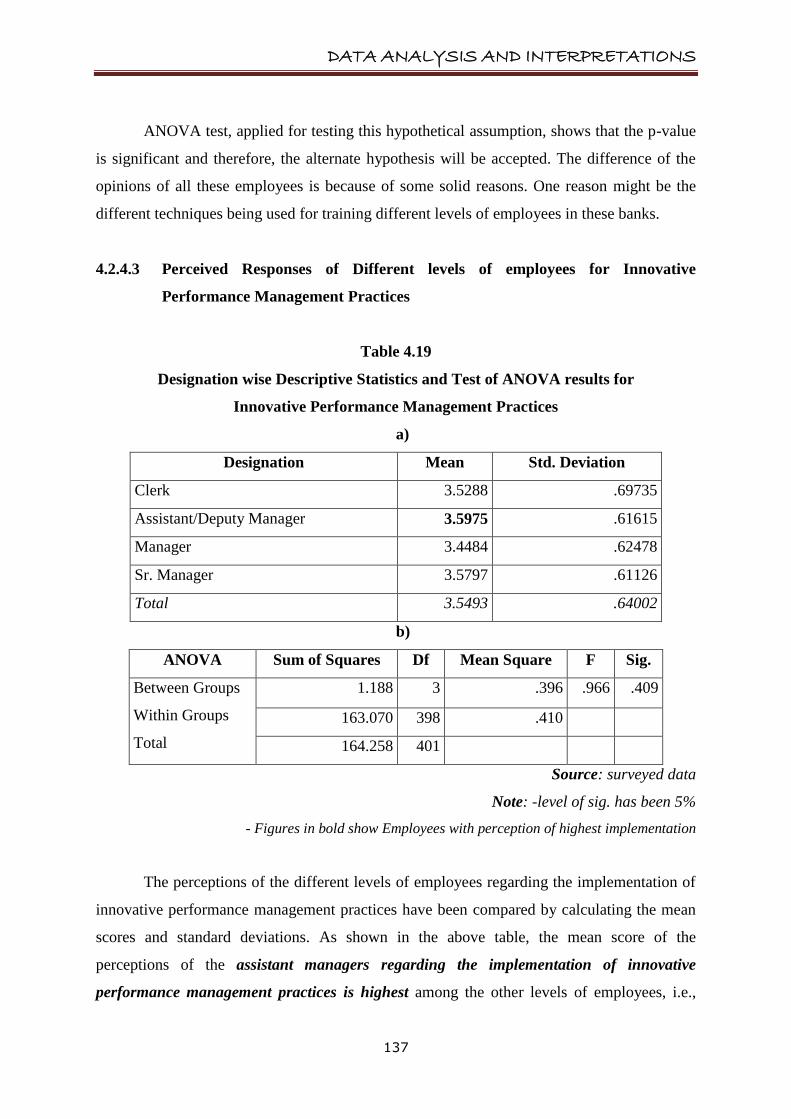

4.1.3 Innovative Performance Management practices

Performance is defined as the record of outcomes produced on a specified job

function or activity during a specified time period (Bernardin and Russell 1993). This

category of HR practices includes the new practices related to goal achievement in an

efficient manner and their appraisals. Appraising is a general process of facilitating

interpersonal relationship between employees and managers through performance related

discussions to analyze matching up of employees‟ performance with organizational goals

(Wilson & Western, 2000). Job assessment related practices have also been categorised under

this head. In the present study, six innovative HRM practices related to Performance

Management were found which are: Formation of performance matrix, goal review based

appraisal, appraisal on fair objective data, 360 degree performance appraisal, option to

challenge the appraisal and full awareness of the performance appraisal policy.

4.1.3.1 Formation of performance matrix

The very common innovative HR practice of performance management has

been that the performance matrix or some other competency mapping models

being used for employee‟s performance reviews. All private sector banks

under the study are following this innovation in the performance management

practices for a long time. This has enhanced the performance as well as the

morale of their employees.

4.1.3.2 Goal review based appraisal

The respondents under the study also disclosed that goal reviews and

competency review systems, the two common methods, are being used for

appraising the performance of employees. This helps to match the

performance of the employees with the earlier set goals of the individuals and

organisations.

DATA ANALYSIS AND INTERPRETATIONS

99

4.1.3.3 Appraisal on fair objective data

In this study, it was found that the employees are being assessed for their fair

objective data. These data may relate to their deposits, advances, NPAs, or

profit per employee. These objective and fair data helps the employers to

appraise the employees without any biasness and good performers are

benefitted from this.

4.1.3.4 360 degree performance appraisal

Another innovation is that they are reviewing the performance from multiple

sources e.g. superiors, juniors, peers etc., i.e., 360 degree performance review

system, which was not prevalent earlier, is being implemented in most of the

banks. The same practice has also been discussed by Aggarwala (2003) in her

study on innovative HRM practices.

4.1.3.5 Option to challenge the appraisal

These days, the employees of a few banks have the power to challenge their

appraisal done by the HR department or by their superiors, if they disagree on

some issue. But for this, they need to represent to the higher levels with solid

proofs and logics. A few banks have a modified policy of discussing the

performance appraisals with their employees. Ukko et al. (2007) found that

performance oriented discussions between employees and managers are

directly related to organizational performance.

4.1.3.6 Full awareness of the performance appraisal policy

Moreover, there is a complete awareness of the Performance Appraisal policy

of HR department among all the staff members so that they are well aware of

what they have done and what they should not have done. Bernardin and

Russel (1993) and Landy & Far (1980) have also favoured this innovation in

their studies mentioning that wider communication of performance appraisal

policies within organizational is essential to make employees clear about their

specific role expected as contribution in organizational performance. Effective

managers need to incorporate performance review and feedback as part of

their day-to-day communications with employees (Webb, 2004).

DATA ANALYSIS AND INTERPRETATIONS

100

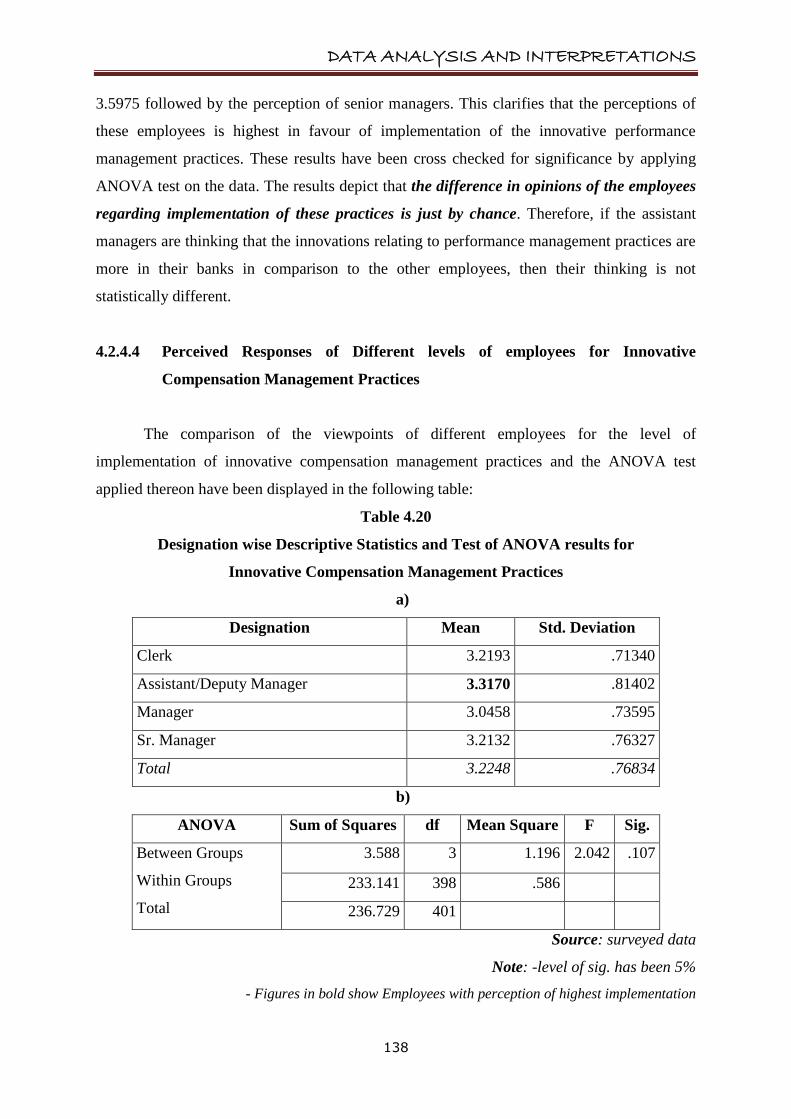

4.1.4 Innovative Compensation Management Practices

Compensation is all forms of financial returns and tangible services and benefits

employees receive as part of an employment relationship (Milkovich and Newman 1999).

This variable comprises of all innovations in the practices linked to payment and

remuneration of the employees. This variable plays a major role in the employee

development and retention as the financial incentives are the best motivating factors for them.

An effective set of choices about compensation systems plays a major role in determining

firm performance (Dreher and Dougherty 2005). Abbasi and Hollman (2000) in their study

have identified lack of recognition and lack of competitive compensation systems as some

reasons for employee turnover in the organization. Announcing special incentive to the

talented employees, special increments on regular basis, special festival advance, and

customised perks have been four innovations under this head found during the present study.

4.1.4.1 Announcing special incentive to the talented employees

Special incentives are given to talented employees to encourage better

performance. Using incentive compensation to stimulate better performance

and provide promotion opportunities through an internal labour market

increases satisfaction and self-actualization (Harel & Tzafrir, 2001). The same

has been confirmed by Gerhart & Milkovich (1992) in one of their studies.

4.1.4.2 Special increments on regular basis

One major innovative practice of compensation has been identified that is

there has been a provision of special increments for better performance of the

employees. This gives the employees an enough salary growth. Park et al.

(1994) and Trevor et al. (1997) found that salary growth had a pronounced

effect on turnover. Particularly, salary growth effects on turnover were

greatest for high performers, that is, high salary growth significantly reduced

turnover of high performing employees.

4.1.4.3 Special festival advance

These days, the HR department has also started one new scheme of providing

special festival advances to the bank employees on either discounted rates or

DATA ANALYSIS AND INTERPRETATIONS

101

without any interest so that they can fulfil their family requirements on the

festivals without bearing any special burden. The HR personnel of these banks

are of the view that, due to provision of this scheme, the employees are

demanding fewer leaves in the festive season. This helps them in managing

their staff effectively.

4.1.4.4 Customised perks

In last couple of years, the perks have also been customised to the individual

needs. This practice is gaining popularity in other Indian organisations too

(Aggarwala, 2003). Banks under the study are also using this innovative HR

practice as per the responses of the experts.

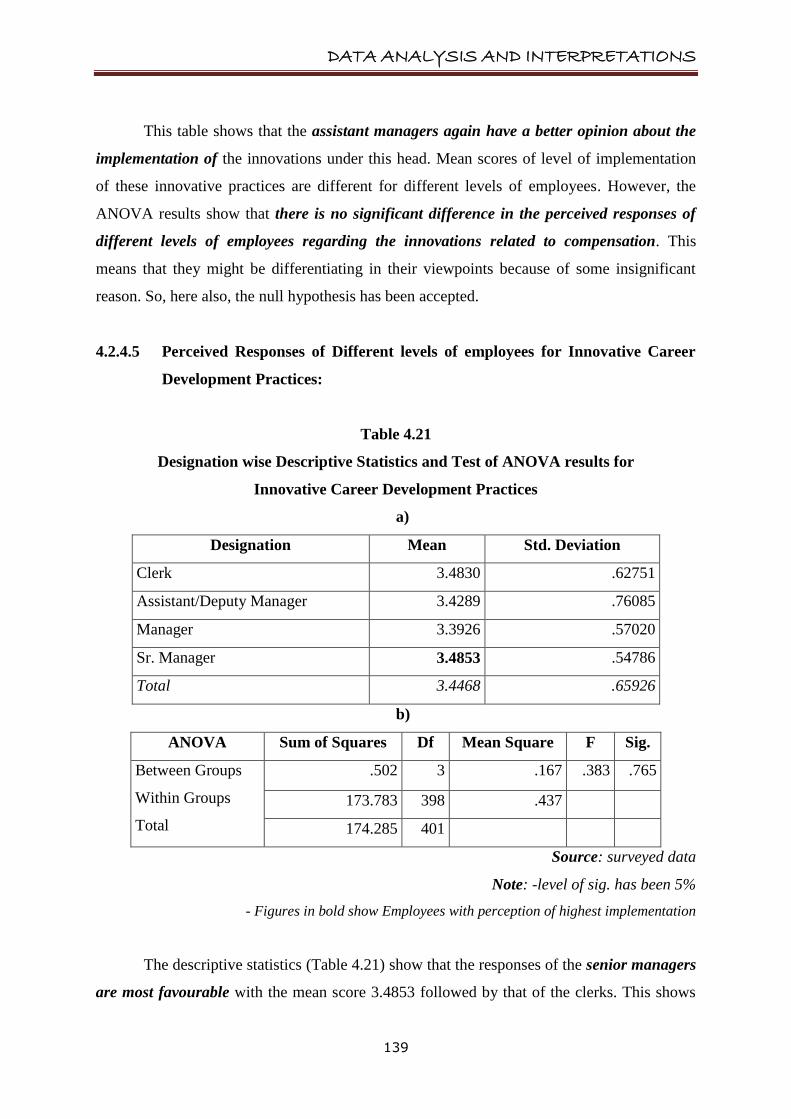

4.1.5 Innovative Career Development Practices

Those innovative HRM practices which include both organizational actions and

individual efforts aimed at setting career goals, formulating and implementing strategies and

monitoring the results are categorised under this head (Greenhaus 1987). These help the

employees to groom themselves and manage their careers. Verburg et al. (2007) have

identified career development itself as an ideal innovative HRM practice in one of their

researches. Availability of educational opportunities at workplace, easy approval to the job

applications, preference to seniority in promotions, promoting on the basis of merit, and

providing faster promotions are the five innovative Career Development related innovative

practices.

4.1.5.1 Availability of educational opportunities at workplace

Education related opportunities are being provided at the work place for the

career enhancement of the bank employees. This has increased their

dedication towards work in their present organisations. Moreover, they feel

that their management is concerned about their career development and

enhancement. This enhances their morale for work.

4.1.5.2 Easy approval to the job applications

This study identified that one latest innovation in the career development of

employees is that the applications sent for the career opportunities outside the

DATA ANALYSIS AND INTERPRETATIONS

102

bank are being approved by the HR department and regional managers

quickly. Earlier the top management, especially of Public sector banks, were

either verbally denying the approval of such applications or delaying the

process, to discourage the employees from applying outside the bank. But now

a days, these applications are easily approved so that employees can think of

their career development.

4.1.5.3 Preference to seniority in promotions

Seniority is given proper weightage in the promotion decisions in banking

sector. Even transfers on promotions are also affected by the seniority. E.g.

Central bank of India has a promotion provision to give favourable and closest

transfer to the employees who are senior among others in the promotion

process.

4.1.5.4 Promoting on the basis of merit

Banks are also organising written tests and interviews for the promotion

process so that merit can be one of the criteria for promotions. A well-planned

career development system along with internal advancement opportunities

based on merit, results in high motivation among employees, which has an

impact on firm performance (Milkovich and Boudreau, 1998).

4.1.5.5 Providing faster promotions

Fast track promotion process is also one common innovative practice

identified in the study. Earlier the employees had to wait for years to get

promotions. But these days, they get faster promotions, even in two to three

years. This helps them to develop their career in their own bank and they don‟t

even think of leaving the bank for getting better opportunity outside in other

banks or organisations.

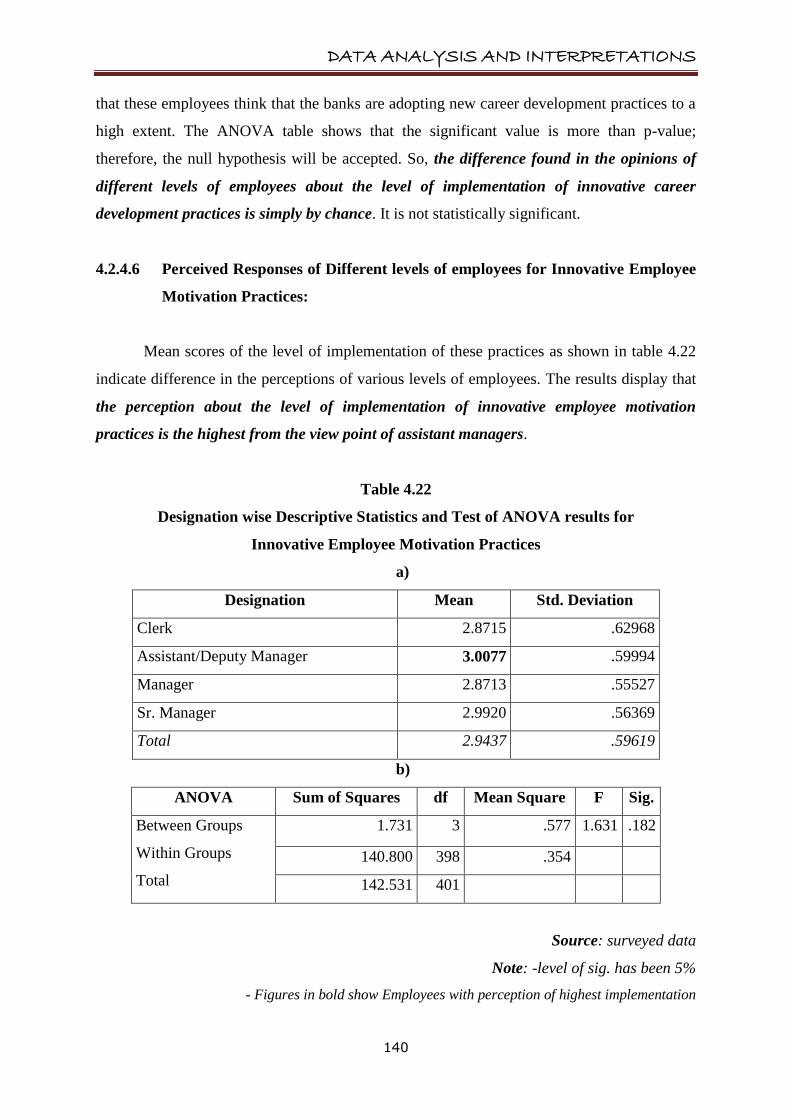

4.1.6 Innovative Employee Motivation Practices

The effectiveness of skilled employees will be limited if they are not motivated to

perform their jobs (Delaney and Huselid, 1996). This factor of HR practices includes all those

innovations relating to motivation of the employees through new ways. This also includes the

DATA ANALYSIS AND INTERPRETATIONS

103

innovative HRM practices related to retention, team building, etc. In the present

investigation, eleven innovative motivation practices have been identified. Accordingly, the

employees can be motivated in the new ways by using music at work place, providing day

care centres, work autonomy, making available ESOPs, providing loans at discounted

rates, giving an option of flexible working hours, approving leave applications easily,

organising stress management programs, encouraging team building attitude, giving best

employee awards, arranging family get-togethers.

4.1.6.1 Using music at work place

Use of music at workplace, to improve the performance, is one major

innovation found in the study. State bank of India has introduced the concept

of playing light music in its branches so that a calm and soothing environment

can be provided to the employees as well as the customers. Other banks too

have started following this practice.

4.1.6.2 Providing day care centres

There is an arrangement of day care centres in the surveyed banks for the

children of employees, so that they have no difficulty in maintaining work life

balance. In these day care centres, they can drop their children while they are

at work. This won‟t even divert their minds towards their family while

working. Young mothers remain satisfied when their little ones are not far

away from them. This definitely raises the efficiency of the women

employees.

4.1.6.3 Work autonomy

In the last few years, greater work autonomy is also being provided to the

bank employees. This helps them to work according to their best possible

capability without any interference and they try to give their best. This is a

kind of brain storming exercise through which the employers can get best out

of the minds of their employees.

4.1.6.4 Making available ESOPs

Availability of Employee Stock Option Plans is a practice which has been

innovated in the banking sector for a last few years so that the employees feel

DATA ANALYSIS AND INTERPRETATIONS

104

that they are also the owners of the banks. This feeling makes the employees

more loyal to their organisation.

4.1.6.5 Providing loans at discounted rates

Availability of loans and advances at discounted rates to all the employees is

also another common innovative HRM practice leading to motivation of the

employees. They can get loans on simple interest for getting vehicles,

constructing house or even educating their wards. This helps the employees

financially and motivates them to increase their efficiency.

4.1.6.6 Giving an option of flexible working hours

Some of the banks are also providing flexible working hours to enhance the

productivity of employees. Banking hours are generally common everywhere,

but a few banks have started giving an option of flexible working hours in two

different shifts so that the employees can work according to their comfort.

This practice was also identified by Kundu & Malhan (2009) in one of their

studies. Bame (1993) found that employee turnover was lower when

employees had shorter work hours and were given a choice of work schedules,

even though their workload was higher. He concluded that firms that provide

flexible work schedules to their employees had the advantage of reducing

employee turnover.

4.1.6.7 Approving leave applications easily

These days, there is an easy availability of leave on demand in case of urgency

which was the common HR issue among the bank employees. However, this

practice prevails in a few banks only. Keeping in mind the benefits of this

innovative practice, other banks have also started this practice for motivating

and retaining their employees in their organisations.

4.1.6.8 Organising stress management programs

Arrangement of stress management programmes, art of living classes, yoga

sessions etc. are distinct innovations which have not been there in the banking

system earlier. These practices are the best boosters and relaxers for the bank

employees who are mostly under work pressure.

DATA ANALYSIS AND INTERPRETATIONS

105

4.1.6.9 Encouraging team building attitude

By encouraging team building attitude in the employees, the HR department of

banks has started a new practice of motivating them. They work in teams and

learn new skills. This increases their confidence and hence they feel more

motivated.

4.1.6.10 Giving best employee awards

Announcement of best employee awards was a common practice in the private

sector banks, but these days, the public sector banks have also started the same

practice to motivate their employees. A few banks have recently introduced

the practice of writing the best employee‟s name on the display board in the

regional centres or even in the branches of their banks. Better-motivated

employees lead to higher individual achievement and improved organizational

performance (Huselid, 1995; Pfeffer, 1994; Delaney et al., 1989).

4.1.6.11 Arranging family get-togethers

Family get-togethers have become so common in the banking sector that the

employees working there feel closer to each other. These informal family get-

togethers help them to be relaxed for some time. Even, a few of the

respondents were of the view point that with the help of these family get-

togethers, they can live their social lives easily among their own colleagues.

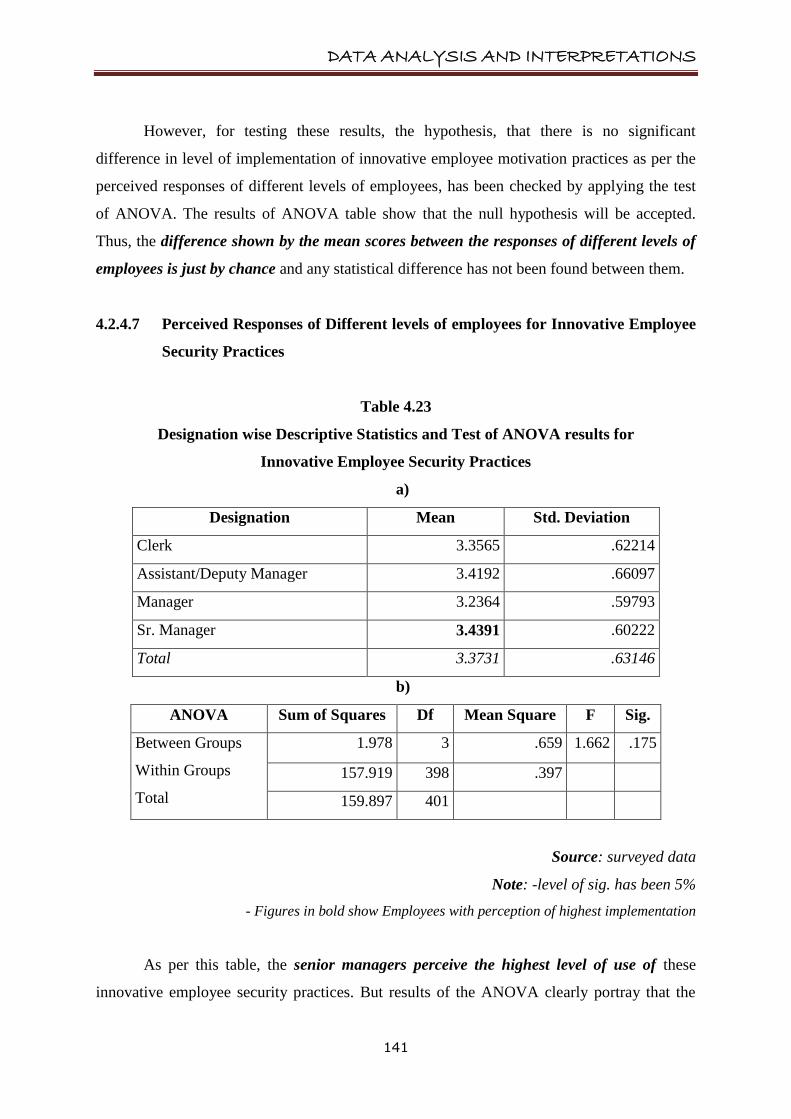

4.1.7 Innovative Employee Security Practices

The practices which make the employee feel highly secured in his present job are the

best suited for this category. These practices when implemented through new ways may help

an employee to feel most satisfied in his job. A total of seven Innovative Employee Security

practices found in the present study were provision of sabbatical leaves (part time leave from

bank with 50% or less salary in case of crisis), sufficient retirement benefits, option of

voluntary retirement, insurance of dependents, security to the employee that he would be

last to leave the organisation if some uneven happens, proper grievances procedures, full

support from the regional or central office.

DATA ANALYSIS AND INTERPRETATIONS

106

4.1.7.1 Provision of sabbatical leaves

One innovative practice adopted by the HR department of the banks is that

there is a provision of “sabbatical leaves” (part time leave from bank with

50% or less salary in case of crisis) for employees. This helps in reducing the

employee turnover rate in the banks. Infosys started giving sabbatical leaves

to its employees in India so that they may get job security. This was followed

by HDFC bank and then the others also started using this HRM practice.

4.1.7.2 Sufficient retirement benefits

Providing proper retirement benefits is one other innovative practice revealed

by the HR employees under the study. Unlike earlier days, now the employees

get enough gratuities, pension and other retirement benefits which can secure

their rest of the life after leaving the job.

4.1.7.3 Option of voluntary retirement

Another innovation explored under this study was that for last few years, VRS

has also become common in banking sector. Now, the employees of the banks

can also enjoy the benefits of this scheme if they need earlier retirements from

their work. This doesn‟t interrupt their other retirement benefits.

4.1.7.4 Insurance of dependents

Banks also give the facility of dependent‟s insurance which gives a sense of

security in the minds of employees for their family too. This motivates them

by satisfying their social as well as security needs.

4.1.7.5 Job security

Earlier the bank employees were even asked to leave the bank in case of any

default being made by the employees. But now, their genuine grounds are

taken in to notice and they are ensured for the job security, even in the private

sector too. This gives surety to an employee that he would be the last one to be

asked to leave the organisation if any financial problem arises. It has been

argued that the provision of job security encourages employees to work

harder. Ichniowski and his associates also noted, "Workers will only expend

DATA ANALYSIS AND INTERPRETATIONS

107

extra effort. . . if they expect. . . a lower probability of future layoffs" (1994:

10).

4.1.7.6 Proper grievances procedures

There is a provision of written as well as operational grievances procedures.

The existence of the formal mechanism of dispute resolution reduces

employees' fear of being unfairly treated and increases their perception of

equitable treatment resulting in a more dedicated workforce and better

performance (Arthur, 1992).

4.1.7.7 Full support from the regional or central office

The HR department as well as the controlling office is supporting the

employees on the genuine grounds. This full support from the top level

enhances the feeling of security and motivation among the employees and they

work harder. Firth et al. (2004) found that emotional support from supervisors

and self-esteem mediated the impact of stressors on stress reactions, job

satisfaction, commitment to the organization and intention to quit.

.

DATA ANALYSIS AND INTERPRETATIONS

108

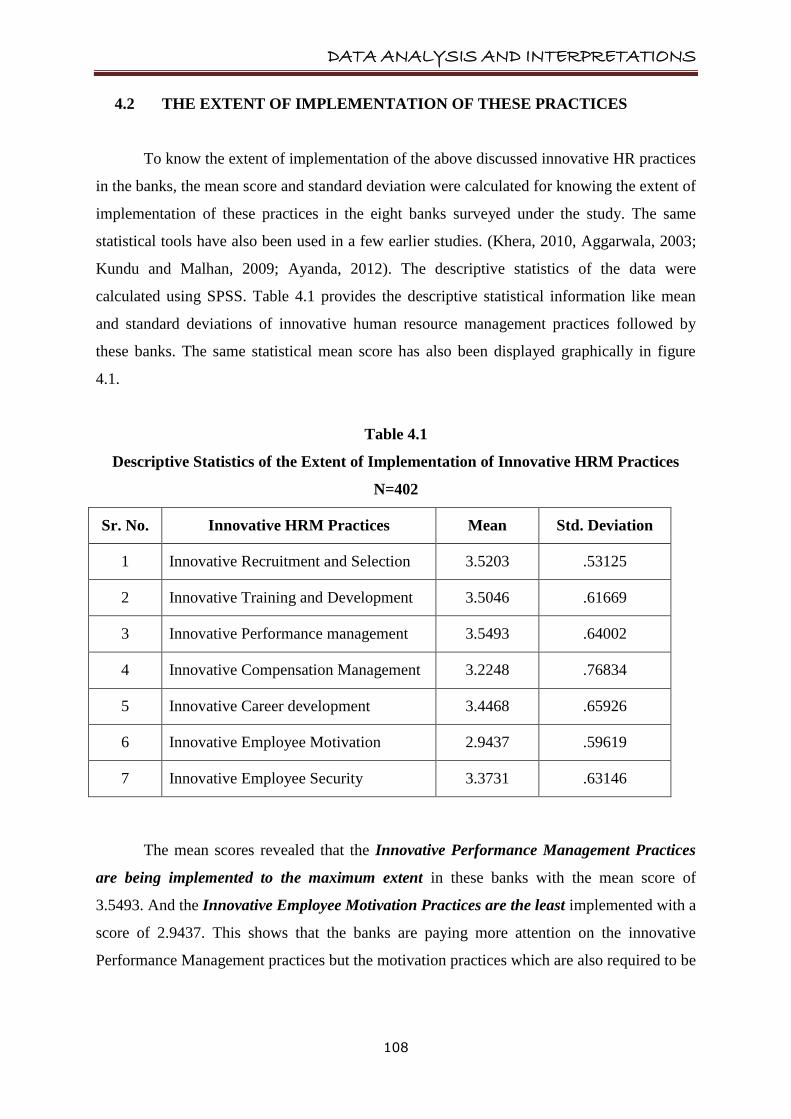

4.2 THE EXTENT OF IMPLEMENTATION OF THESE PRACTICES

To know the extent of implementation of the above discussed innovative HR practices

in the banks, the mean score and standard deviation were calculated for knowing the extent of

implementation of these practices in the eight banks surveyed under the study. The same

statistical tools have also been used in a few earlier studies. (Khera, 2010, Aggarwala, 2003;

Kundu and Malhan, 2009; Ayanda, 2012). The descriptive statistics of the data were

calculated using SPSS. Table 4.1 provides the descriptive statistical information like mean

and standard deviations of innovative human resource management practices followed by

these banks. The same statistical mean score has also been displayed graphically in figure

4.1.

Table 4.1

Descriptive Statistics of the Extent of Implementation of Innovative HRM Practices

N=402

Sr. No. Innovative HRM Practices Mean Std. Deviation

1 Innovative Recruitment and Selection 3.5203 .53125

2 Innovative Training and Development 3.5046 .61669

3 Innovative Performance management 3.5493 .64002

4 Innovative Compensation Management 3.2248 .76834

5 Innovative Career development 3.4468 .65926

6 Innovative Employee Motivation 2.9437 .59619

7 Innovative Employee Security 3.3731 .63146

The mean scores revealed that the Innovative Performance Management Practices

are being implemented to the maximum extent in these banks with the mean score of

3.5493. And the Innovative Employee Motivation Practices are the least implemented with a

score of 2.9437. This shows that the banks are paying more attention on the innovative

Performance Management practices but the motivation practices which are also required to be

DATA ANALYSIS AND INTERPRETATIONS

109

implemented to a high extent are lagging behind. Recruitment and selection are on the second

rank in the order of implementation of these practices in the banking sector.

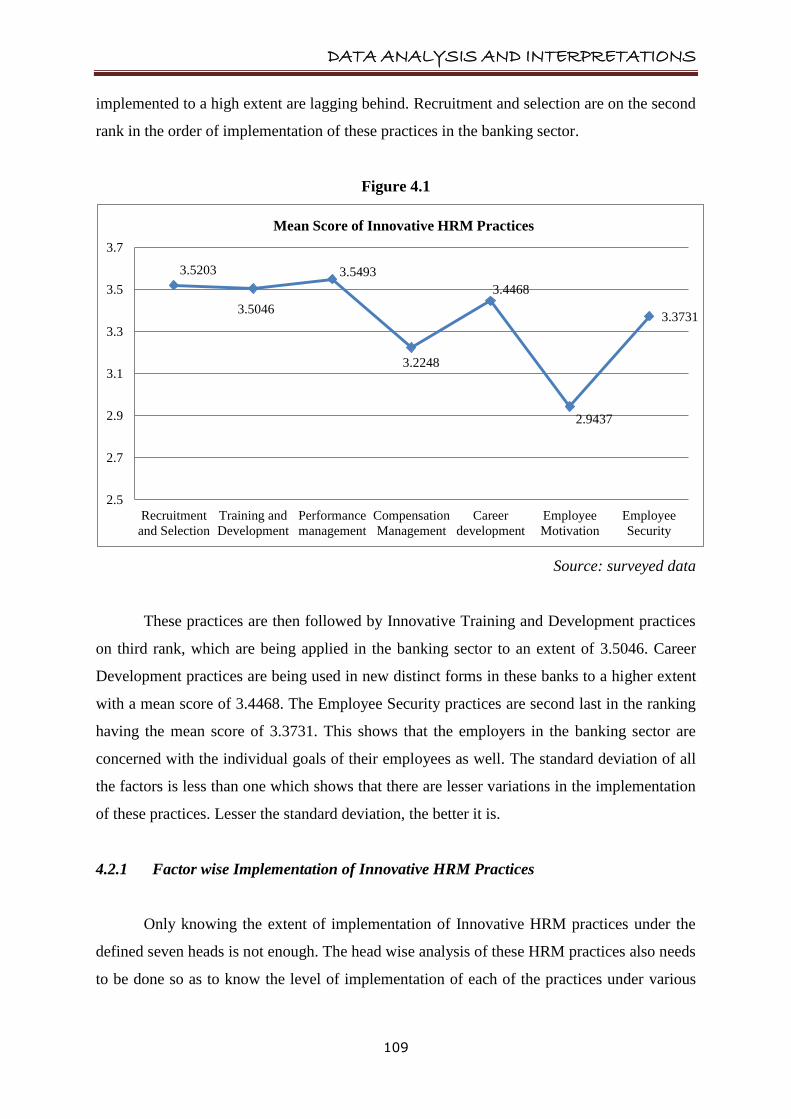

Figure 4.1

Source: surveyed data

These practices are then followed by Innovative Training and Development practices

on third rank, which are being applied in the banking sector to an extent of 3.5046. Career

Development practices are being used in new distinct forms in these banks to a higher extent

with a mean score of 3.4468. The Employee Security practices are second last in the ranking

having the mean score of 3.3731. This shows that the employers in the banking sector are

concerned with the individual goals of their employees as well. The standard deviation of all

the factors is less than one which shows that there are lesser variations in the implementation

of these practices. Lesser the standard deviation, the better it is.

4.2.1 Factor wise Implementation of Innovative HRM Practices

Only knowing the extent of implementation of Innovative HRM practices under the

defined seven heads is not enough. The head wise analysis of these HRM practices also needs

to be done so as to know the level of implementation of each of the practices under various

3.5203

3.5046

3.5493

3.2248

3.4468

2.9437

3.3731

2.5

2.7

2.9

3.1

3.3

3.5

3.7

Recruitment

and Selection

Training and

Development

Performance

management

Compensation

Management

Career

development

Employee

Motivation

Employee

Security

Mean Score of Innovative HRM Practices

DATA ANALYSIS AND INTERPRETATIONS

110

heads. For this purpose, descriptive statistics of all forty nine innovative practices have been

conceded.

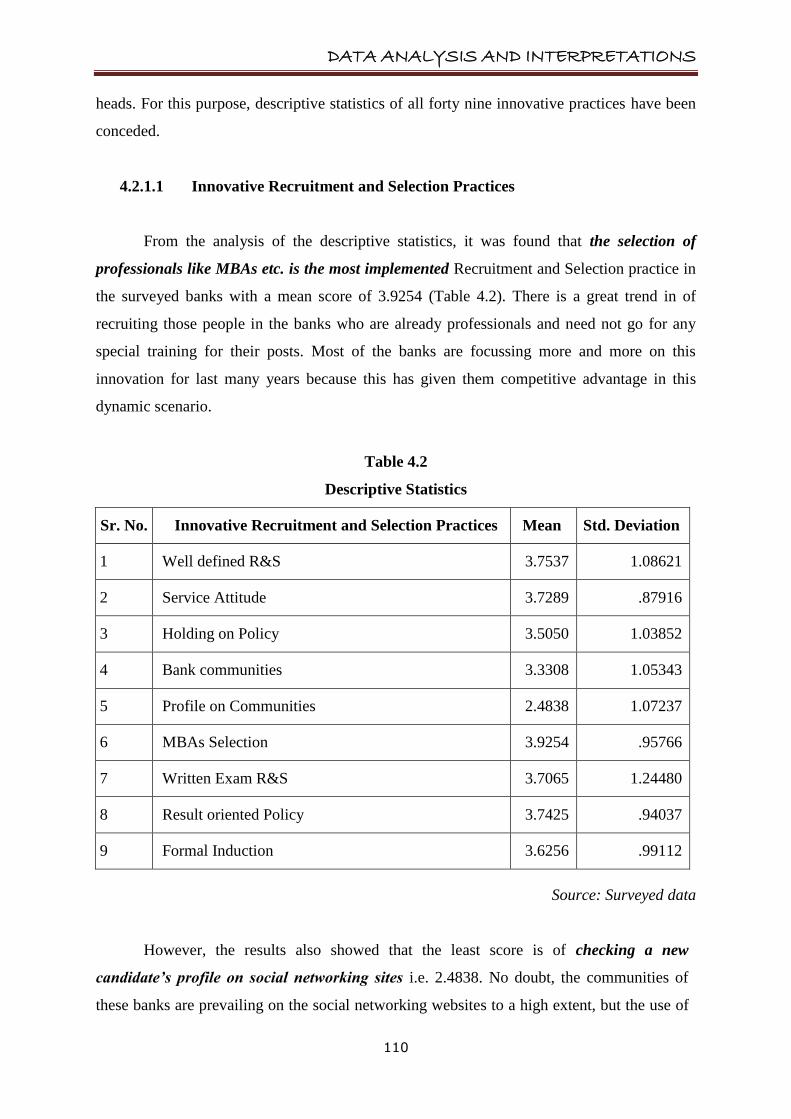

4.2.1.1 Innovative Recruitment and Selection Practices

From the analysis of the descriptive statistics, it was found that the selection of

professionals like MBAs etc. is the most implemented Recruitment and Selection practice in

the surveyed banks with a mean score of 3.9254 (Table 4.2). There is a great trend in of

recruiting those people in the banks who are already professionals and need not go for any

special training for their posts. Most of the banks are focussing more and more on this

innovation for last many years because this has given them competitive advantage in this

dynamic scenario.

Table 4.2

Descriptive Statistics

Sr. No. Innovative Recruitment and Selection Practices Mean Std. Deviation

1 Well defined R&S 3.7537 1.08621

2 Service Attitude 3.7289 .87916

3 Holding on Policy 3.5050 1.03852

4 Bank communities 3.3308 1.05343

5 Profile on Communities 2.4838 1.07237

6 MBAs Selection 3.9254 .95766

7 Written Exam R&S 3.7065 1.24480

8 Result oriented Policy 3.7425 .94037

9 Formal Induction 3.6256 .99112

Source: Surveyed data

However, the results also showed that the least score is of checking a new

candidate’s profile on social networking sites i.e. 2.4838. No doubt, the communities of

these banks are prevailing on the social networking websites to a high extent, but the use of

DATA ANALYSIS AND INTERPRETATIONS

111

checking the candidate‟s profile on these sites is still occasional. Moreover, there is a great

variance in the results as the standard deviation of many of these practices is more than or

near to one. All other innovative practices under this head like formal induction, well

defined policy, written exam, etc. are being implemented to high extent as shown in the

figure 4.2.

Figure 4.2

Source: Surveyed data

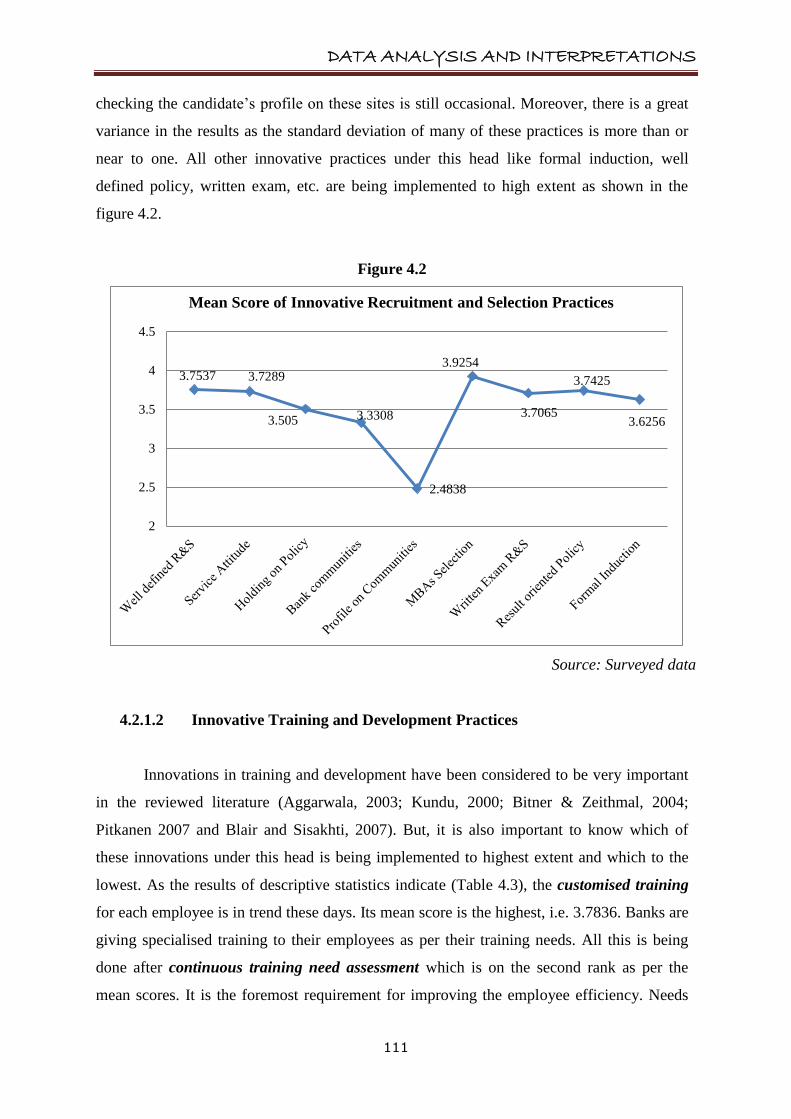

4.2.1.2 Innovative Training and Development Practices

Innovations in training and development have been considered to be very important

in the reviewed literature (Aggarwala, 2003; Kundu, 2000; Bitner & Zeithmal, 2004;

Pitkanen 2007 and Blair and Sisakhti, 2007). But, it is also important to know which of

these innovations under this head is being implemented to highest extent and which to the

lowest. As the results of descriptive statistics indicate (Table 4.3), the customised training

for each employee is in trend these days. Its mean score is the highest, i.e. 3.7836. Banks are

giving specialised training to their employees as per their training needs. All this is being

done after continuous training need assessment which is on the second rank as per the

mean scores. It is the foremost requirement for improving the employee efficiency. Needs

3.7537 3.7289

3.505 3.3308

2.4838

3.9254

3.7065

3.7425

3.6256

2

2.5

3

3.5

4

4.5

Mean Score of Innovative Recruitment and Selection Practices

DATA ANALYSIS AND INTERPRETATIONS

112

based training has also been said to be important in the earlier researches (Kundu, 2000;

Bitner & Zeithmal, 2001; Aggarwala, 2003; Kundu & Malhan, 2009).

Table 4.3

Descriptive Statistics

N=402

Sr. No. Innovative Training and Development Practices Mean Std. Deviation

1 Trainee test 3.3694 1.36887

2 Job rotation 3.5336 1.09953

3 Customised Training 3.7836 .85796

4 Continuous Training 3.3943 1.00219

5 Regular training 3.4975 .96121

6 Encouragement Apply 3.7152 .87375

7 Special projects 3.2388 1.02473

Source: Surveyed data

Figure 4.3

Source: Surveyed data

3.3694

3.5336

3.7836

3.3943

3.4975

3.7152

3.2388

2.9

3

3.1

3.2

3.3

3.4

3.5

3.6

3.7

3.8

3.9

Mean Score of Innovative Training and Development Practices

DATA ANALYSIS AND INTERPRETATIONS

113

Tendency of sending the employees for special projects of training is still low with a

mean score of 3.2388 as compared to other innovations under this variable. This may be

because of the reason that the main focus of Indian banks is still on giving training through

the old methods as those are acceptable at all levels of these organisations. The mean score

for the innovative practice of conducting written tests of the trainees before sending them for

the training is also very low. Probably this may be due to the fact that only a few banks have

started this practice.

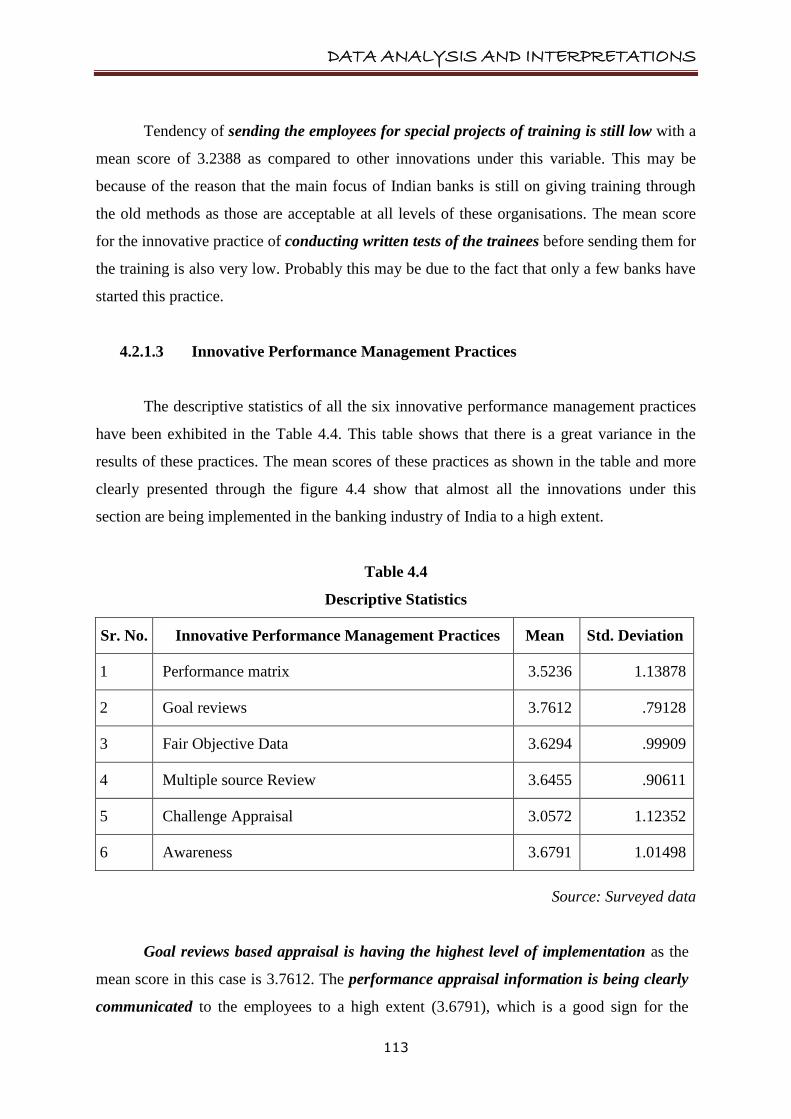

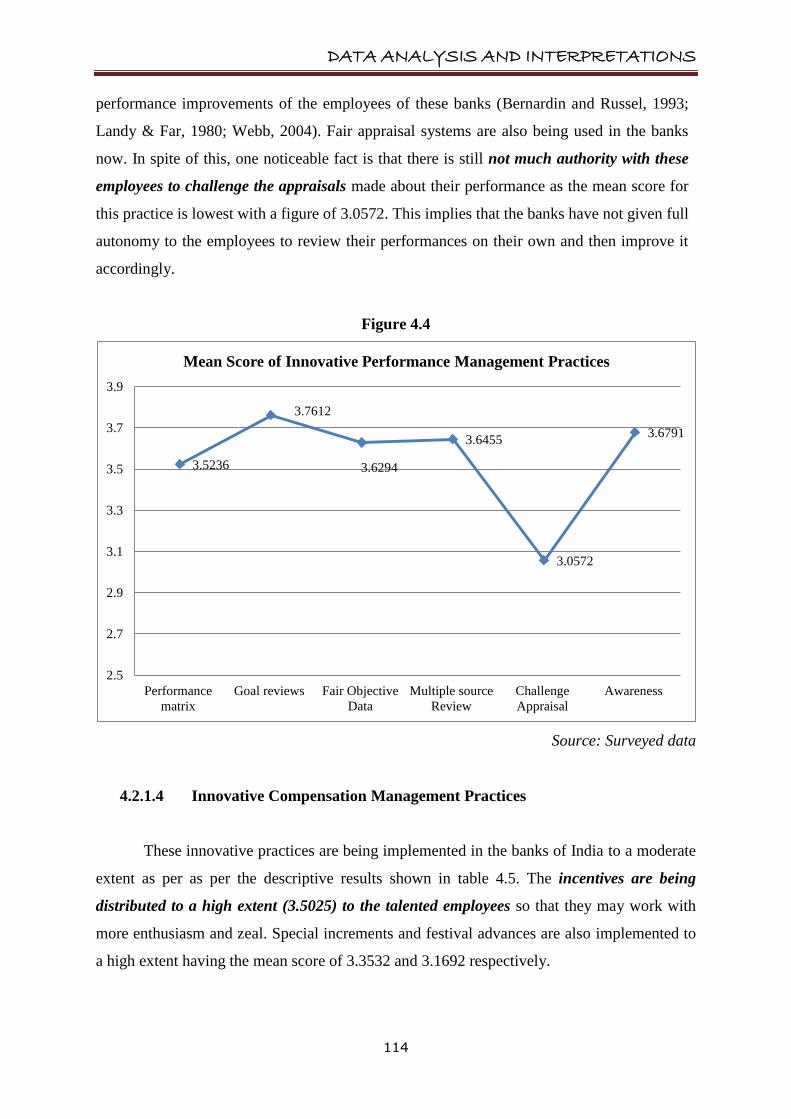

4.2.1.3 Innovative Performance Management Practices

The descriptive statistics of all the six innovative performance management practices

have been exhibited in the Table 4.4. This table shows that there is a great variance in the

results of these practices. The mean scores of these practices as shown in the table and more

clearly presented through the figure 4.4 show that almost all the innovations under this

section are being implemented in the banking industry of India to a high extent.

Table 4.4

Descriptive Statistics

Sr. No. Innovative Performance Management Practices Mean Std. Deviation

1 Performance matrix 3.5236 1.13878

2 Goal reviews 3.7612 .79128

3 Fair Objective Data 3.6294 .99909

4 Multiple source Review 3.6455 .90611

5 Challenge Appraisal 3.0572 1.12352

6 Awareness 3.6791 1.01498

Source: Surveyed data

Goal reviews based appraisal is having the highest level of implementation as the

mean score in this case is 3.7612. The performance appraisal information is being clearly

communicated to the employees to a high extent (3.6791), which is a good sign for the

DATA ANALYSIS AND INTERPRETATIONS

114

performance improvements of the employees of these banks (Bernardin and Russel, 1993;

Landy & Far, 1980; Webb, 2004). Fair appraisal systems are also being used in the banks

now. In spite of this, one noticeable fact is that there is still not much authority with these

employees to challenge the appraisals made about their performance as the mean score for

this practice is lowest with a figure of 3.0572. This implies that the banks have not given full

autonomy to the employees to review their performances on their own and then improve it

accordingly.

Figure 4.4

Source: Surveyed data

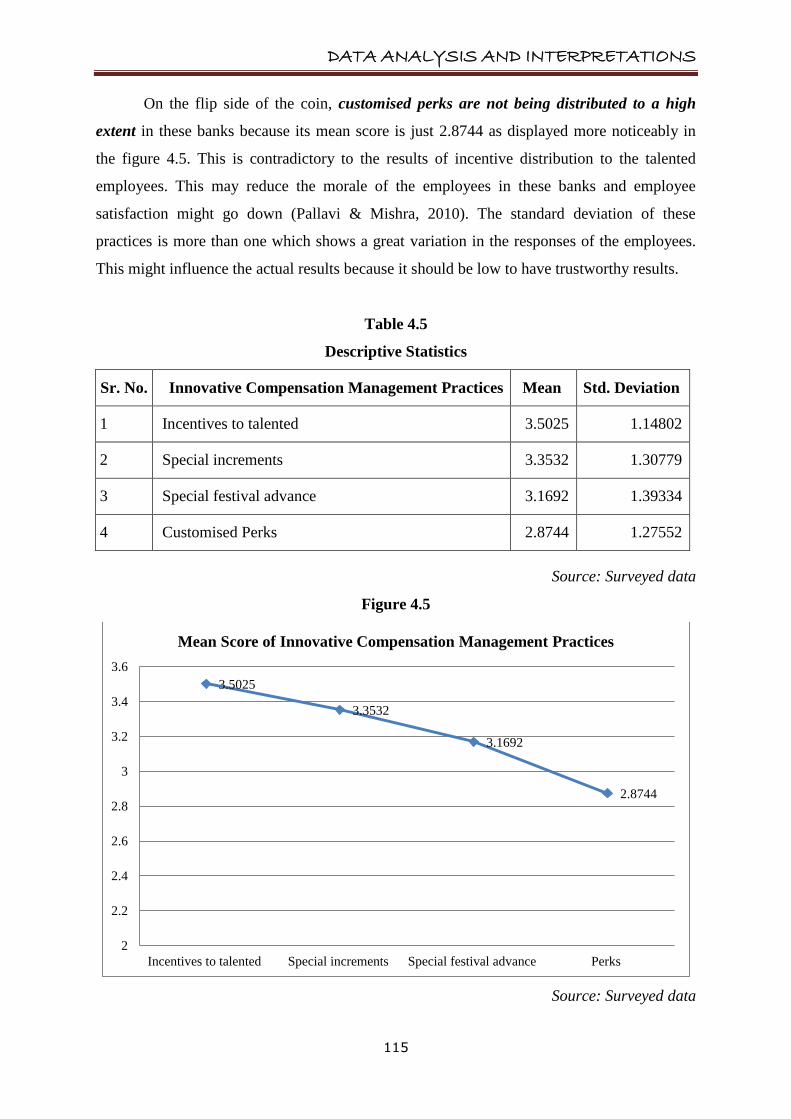

4.2.1.4 Innovative Compensation Management Practices

These innovative practices are being implemented in the banks of India to a moderate

extent as per as per the descriptive results shown in table 4.5. The incentives are being

distributed to a high extent (3.5025) to the talented employees so that they may work with

more enthusiasm and zeal. Special increments and festival advances are also implemented to

a high extent having the mean score of 3.3532 and 3.1692 respectively.

3.5236

3.7612

3.6294

3.6455

3.0572

3.6791

2.5

2.7

2.9

3.1

3.3

3.5

3.7

3.9

Performance

matrix

Goal reviews Fair Objective

Data

Multiple source

Review

Challenge

Appraisal

Awareness

Mean Score of Innovative Performance Management Practices

DATA ANALYSIS AND INTERPRETATIONS

115

On the flip side of the coin, customised perks are not being distributed to a high

extent in these banks because its mean score is just 2.8744 as displayed more noticeably in

the figure 4.5. This is contradictory to the results of incentive distribution to the talented

employees. This may reduce the morale of the employees in these banks and employee

satisfaction might go down (Pallavi & Mishra, 2010). The standard deviation of these

practices is more than one which shows a great variation in the responses of the employees.

This might influence the actual results because it should be low to have trustworthy results.

Table 4.5

Descriptive Statistics

Sr. No. Innovative Compensation Management Practices Mean Std. Deviation

1 Incentives to talented 3.5025 1.14802

2 Special increments 3.3532 1.30779

3 Special festival advance 3.1692 1.39334

4 Customised Perks 2.8744 1.27552

Source: Surveyed data

Figure 4.5

Source: Surveyed data

3.5025

3.3532

3.1692

2.8744

2

2.2

2.4

2.6

2.8

3

3.2

3.4

3.6

Incentives to talented Special increments Special festival advance Perks

Mean Score of Innovative Compensation Management Practices

DATA ANALYSIS AND INTERPRETATIONS

116

4.2.1.5 Innovative Career Development Practices

For the enhancement of the career of the employees, these banks have started using

innovations in a last few years. All the innovative career development practices are being

used in the banks under the study to a high extent (Table 4.6). Seniority and Merit based

promotions are the most implemented practices as their mean score are 3.5672 and 3.5410

respectively. These banks are also giving faster promotions which were not available in the

banking sector earlier.

Table 4.6

Descriptive Statistics

Sr. No. Innovative Career Development Practices Mean Std. Deviation

1 Educational opportunities 3.4005 1.06347

2 Easy approval 3.1878 1.06353

3 Seniority promotion 3.5672 .93849

4 Faster promotions 3.4913 1.01266

5 Merit promotion 3.5410 1.10154

Source: Surveyed data

Moreover, a lot of internal educational opportunities are also being provided in these

banks. In spite of this, 3.1878 is the mean score of another practice which shows that the level

of implementation of easy approvals of the applications of the employees for outside exams

is not very high. This might be because of the fear of losing employees if they get selected

anywhere else. A more comprehensive picture of these results has been demonstrated through

figure 4.6.

DATA ANALYSIS AND INTERPRETATIONS

117

Figure 4.6

Source: Surveyed data

4.2.1.6 Innovative Employee Motivation Practices

The descriptive data results of these practices as shown in table 4.7 exhibit that some

of these practices namely discounted rates on the loans (3.8383), easy leave sanctions

(3.6331), development of team building attitude (3.5908), best employee awards (3.3794)

and greater work autonomy (3.1555) are being implemented to a great extent. Day care

centres are the foremost need of the women employees but the extent of implementing this

innovative practice in these banks is very low with a mean score of 1.8507. Even they need

flexible working hours so that they can make a work life balance. But the banks are still not

doing much effort to implement these improved motivational practices.

Figure 4.7 is portraying a clear picture of these results. Furthermore, there is a great

pressure on any kind of employee when he/she works for a long time. To release this pressure

and make the employees more comfortable, stress management programs, family get-

togethers and use of music at the work place are the best ways. But, the analysis of results

showed that the extent of application of these practices in the banks is in the range of

occasionally to moderate.

3.4005

3.1878

3.5672

3.4913

3.541

2.9

3

3.1

3.2

3.3

3.4

3.5

3.6

Educational

opportunities

Easy approval Seniority promotion Faster promotions Merit promotion

Mean Score of Innovative Career Development Practices

DATA ANALYSIS AND INTERPRETATIONS

118

Table 4.7

Descriptive Statistics

Sr. No. Innovative Employee Motivation Practices Mean Std. Deviation

1 Music use 2.1903 1.13732

2 Day Care Centres 1.8507 1.11557

3 Work Autonomy 3.1555 .95083

4 ESOPs 2.9378 1.15392

5 Discounted Rates 3.8383 1.15667

6 Flexible working 2.7400 1.35209

7 Easy leave 3.6331 1.04468

8 Stress mgt 2.6866 1.15884

9 Team building 3.5908 1.00428

10 Best employee 3.3794 1.31403

11 Family GTs 2.3781 1.11611

Source: Surveyed data

Figure 4.7

Source: Surveyed data

2.1903

1.8507

3.1555

2.9378

3.8383

2.74

3.6331

2.6866

3.5908

3.3794

2.3781

1.5

2

2.5

3

3.5

4

Mean Scores of Innovative Employee Motivation Practices

DATA ANALYSIS AND INTERPRETATIONS

119

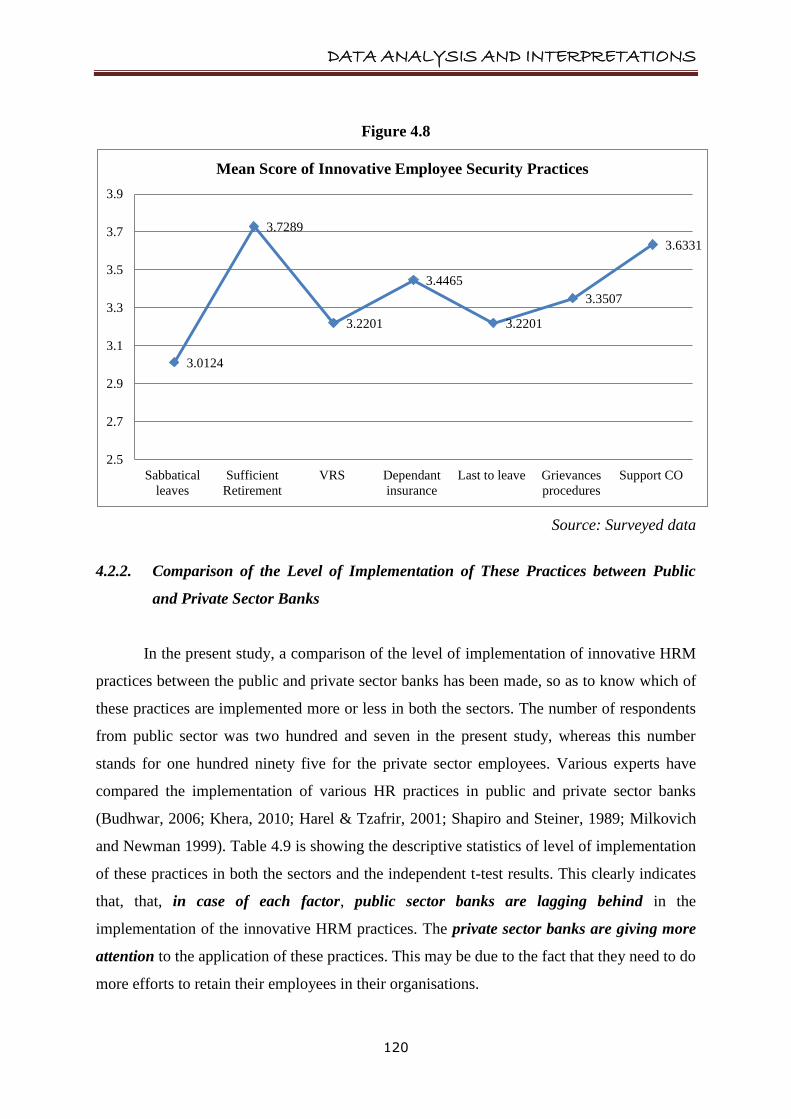

4.2.1.7 Innovative Employee Security Practices

The descriptive results of seven innovative employee security practices have been

displayed in the table 4.8. The results indicate this clearly that all these new practices related

to the employee security are being applied in the banking sector to a high extent.

Table 4.8

Descriptive Statistics

Sr. No. Innovative Employee Security Practices Mean Std. Deviation

1 Sabbatical leaves 3.0124 1.19375

2 Sufficient Retirement benefits 3.7289 1.05633

3 VRS 3.2201 1.14069

4 Dependant‟s insurance 3.4465 1.28399

5 Last to leave 3.2201 1.28367

6 Grievances procedures 3.3507 1.04696

7 Support from Central office 3.6331 1.15033

Source: Surveyed data

The level of implementation is found to be highest in case of practice of sufficient

retirement benefits, followed by support from central office, dependent‟s insurance and

grievance procedures respectively. Employees are being supported by the central offices

(3.6331) when they are stuck up in problem. One more observable fact is that the practice of

giving sabbatical leaves to the employees in these banks has been adopted up to a high

extent. Its mean score is the lowest among the all innovative practices of this factor i.e.

3.0124. However, VRS and last to leave practices are implemented more than the above said

practices. It was also found during the survey that many of the employees were unaware

about this practice. Further, a high degree of variance is shown through the results of the

standard deviation of these practices. This again shows that the responses for these practices

vary more when checked statistically.

DATA ANALYSIS AND INTERPRETATIONS

120

Figure 4.8

Source: Surveyed data

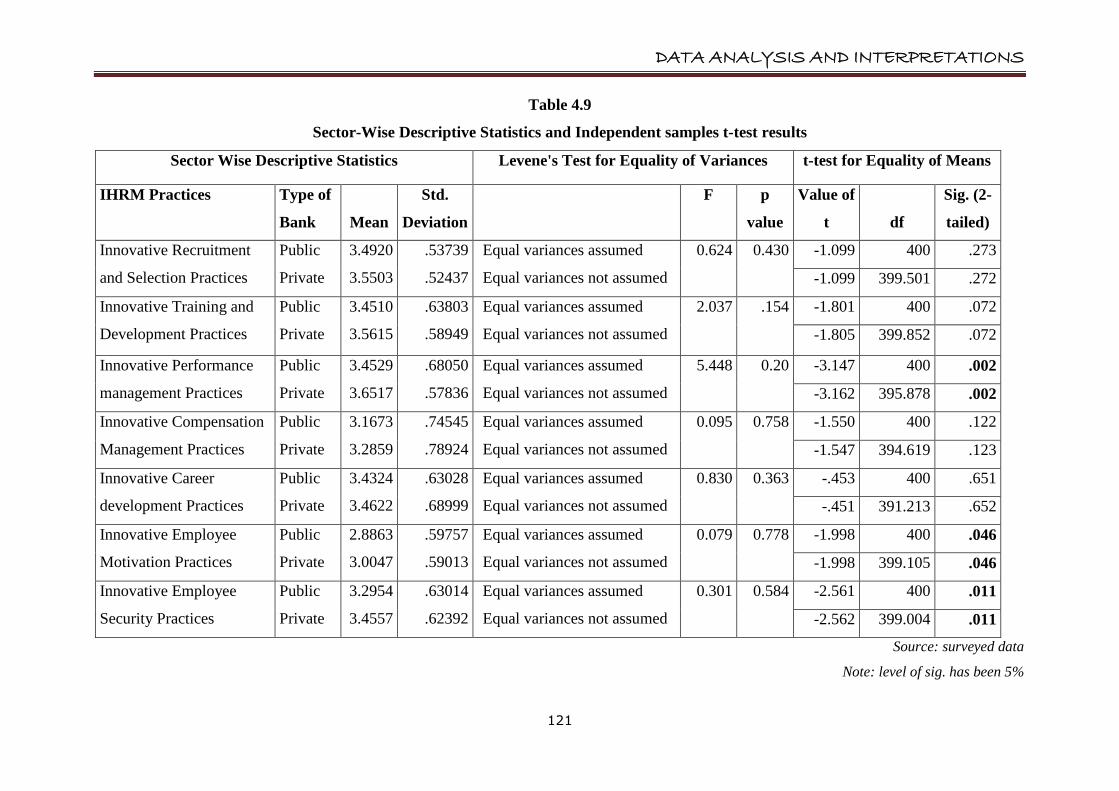

4.2.2. Comparison of the Level of Implementation of These Practices between Public

and Private Sector Banks

In the present study, a comparison of the level of implementation of innovative HRM

practices between the public and private sector banks has been made, so as to know which of

these practices are implemented more or less in both the sectors. The number of respondents

from public sector was two hundred and seven in the present study, whereas this number

stands for one hundred ninety five for the private sector employees. Various experts have

compared the implementation of various HR practices in public and private sector banks

(Budhwar, 2006; Khera, 2010; Harel & Tzafrir, 2001; Shapiro and Steiner, 1989; Milkovich

and Newman 1999). Table 4.9 is showing the descriptive statistics of level of implementation

of these practices in both the sectors and the independent t-test results. This clearly indicates

that, that, in case of each factor, public sector banks are lagging behind in the

implementation of the innovative HRM practices. The private sector banks are giving more

attention to the application of these practices. This may be due to the fact that they need to do

more efforts to retain their employees in their organisations.

3.0124

3.7289

3.2201

3.4465

3.2201

3.3507

3.6331

2.5

2.7

2.9

3.1

3.3

3.5

3.7

3.9

Sabbatical

leaves

Sufficient

Retirement

VRS Dependant

insurance

Last to leave Grievances

procedures

Support CO

Mean Score of Innovative Employee Security Practices

DATA ANALYSIS AND INTERPRETATIONS

121

Table 4.9

Sector-Wise Descriptive Statistics and Independent samples t-test results

Sector Wise Descriptive Statistics Levene's Test for Equality of Variances t-test for Equality of Means

IHRM Practices Type of

Bank Mean

Std.

Deviation

F p

value

Value of

t df

Sig. (2-

tailed)

Innovative Recruitment

and Selection Practices

Public

Private

3.4920

3.5503

.53739

.52437

Equal variances assumed

Equal variances not assumed

0.624 0.430 -1.099 400 .273

-1.099 399.501 .272

Innovative Training and

Development Practices

Public

Private

3.4510

3.5615

.63803

.58949

Equal variances assumed

Equal variances not assumed

2.037 .154 -1.801 400 .072

-1.805 399.852 .072

Innovative Performance

management Practices

Public

Private

3.4529

3.6517

.68050

.57836

Equal variances assumed

Equal variances not assumed

5.448 0.20 -3.147 400 .002

-3.162 395.878 .002

Innovative Compensation

Management Practices

Public

Private

3.1673

3.2859

.74545

.78924

Equal variances assumed

Equal variances not assumed

0.095 0.758 -1.550 400 .122

-1.547 394.619 .123

Innovative Career

development Practices

Public

Private

3.4324

3.4622

.63028

.68999

Equal variances assumed

Equal variances not assumed

0.830 0.363 -.453 400 .651

-.451 391.213 .652

Innovative Employee

Motivation Practices

Public

Private

2.8863

3.0047

.59757

.59013

Equal variances assumed

Equal variances not assumed

0.079 0.778 -1.998 400 .046

-1.998 399.105 .046

Innovative Employee

Security Practices

Public

Private

3.2954

3.4557

.63014

.62392

Equal variances assumed

Equal variances not assumed

0.301 0.584 -2.561 400 .011

-2.562 399.004 .011

Source: surveyed data

Note: level of sig. has been 5%

DATA ANALYSIS AND INTERPRETATIONS

122

Generally, employees leave the private sector organisations early due to lack of job

security. Therefore, the private sector banks are redesigning more and more HRM practices

and implementing them to a greater extent so as to give more comfortable work culture to

their employees, resulting in greater productivity and efficiency. On the flip side, the public

sector banks are still implementing few of their old styles of working due to less attrition rate.

To analyse this difference more clearly, a graphic presentation has also been made in figure

4.9.

Figure 4.9

Source: Surveyed data

Independent samples t-test was applied to check whether this difference between the

implementation of these innovative HRM practices is by chance or there is significant

difference between both the sectors. For this hypothesis 3.1 was checked individually for

each of the seven HRM factors. The level of significance has been checked at 5%.

3.492 3.451

3.4529

3.1673

3.4324

2.8863

3.2954

3.5503 3.5615 3.6517

3.2859 3.4622

3.0047

3.4557

2

2.2

2.4

2.6

2.8

3

3.2

3.4

3.6

3.8

R&S T&D Perf. Mgmt. Comp.Mgmt Career Dev. Motivation Emp. Sec.

Sectorwise comparison of Means

Public

Private

DATA ANALYSIS AND INTERPRETATIONS

123

4.2.2.1 Comparison of the Level of Implementation of Innovative Recruitment and

Selection Practices between Public and Private Sector Banks

The results of t-test reveal that the p-value of this factor is more than 0.05.

Therefore, this difference exists by chance only. In other words, there is no

significant difference between the implementation of these practices among

Indian public and private sector banks, when tested statistically. However, the

minor difference in absolute figures as shown in table 4.9 might be due to some

non significant reasons just like common written test for recruitment and

selection of employees in public sector banks. Some other reason might be the

biasness among the responses of the employees.

4.2.2.2 Comparison of the Level of Implementation of Innovative Training and

Development Practices between Public and Private Sector Banks

The results of t-test clearly signify that the null hypothesis is again to be accepted

as the p-value of this innovative HRM practice is also more than 0.05. This

clearly dictates that there lies no significant difference between the

implementation of innovative Training and Development practices in the public

and private sector banks of India. The same results were concluded in some

earlier studies too (Boyne et al. 1999; Budhwar 2000; Harel and Tzafrir 2001;

Budhwar and Boyne 2004).

4.2.2.3 Comparison of the Level of Implementation of Innovative Performance

Management Practices between Public and Private Sector Banks

T-test results (Table 4.9) show that the significance value of innovative

performance management practices is less than 0.05. Therefore, the alternate

hypothesis will be accepted here, i.e. there is a significant difference between

the public and private sector banks in the implementation of the innovative

Performance Management practices. Budhwar and Boyne (2004) also proved

the same results in their study. This implies that the private sector banks are

following more innovations in the performance management practices in

comparison to the public sector banks.

DATA ANALYSIS AND INTERPRETATIONS

124

4.2.2.4 Comparison of the Level of Implementation of Innovative Compensation

Management Practices between Public and Private Sector Banks

As shown in the table 4.9, the p-value, of test of significance regarding the

difference of implementation of innovative compensation management practices

in public and private sector banks, is also more than 0.05. Thus, the null

hypothesis is accepted and there lies a difference by chance only if tested

statistically. Here, also the private sector banks have been implementing the

innovative compensation management practices more than public sector banks.

But this difference is not a statistically significant difference.

4.2.2.5 Comparison of the Level of Implementation of Innovative Career

Development Practices between Public and Private Sector Banks

The significant value of t-test, applied for testing the hypothesis, that there is no

significant difference in the implementation of innovative career development

practices in public and private sector banks, is also more than 0.05. This means

that the null hypothesis is again accepted here. Thus, there may be a minor

difference between the implementation of innovative career development

practices in public and private sector banks. But this difference is simply by

chance only as the statistical results of t-test reveal that both the banks are

applying these practices to an approximate same level.

4.2.2.6 Comparison of the Level of Implementation of Innovative Employee

Motivation Practices between Public and Private Sector Banks

The t-test results disclose that alternate hypothesis will be accepted for this factor

as the p-value is less than 0.05. Therefore, the difference between the

implementation of innovative employee motivation practices among both the

banks is significant statistically. This difference shows that the private sector

banks are motivating their employees with more innovative ideas so that they can

retain them in the long term. However, the public sector banks are lagging behind

significantly in this practice implementation also.

DATA ANALYSIS AND INTERPRETATIONS

125

4.2.2.7 Comparison of the Level of Implementation of Innovative Employee Security

Practices between Public and Private Sector Banks

The results of t-test reveal that there is a significant difference in the

implementation of innovative employee security practices also in the both types

of banks. This is because here also the p-value is less than 0.05. One of the major

reasons of this difference may be the fact that private sector banks are quicker in

responding to the changing and competitive environment. This has made them

adopt more innovations for providing employee security.

4.2.3 Inter-bank Comparison of the Level of Implementation of These Practices

A further comparison of the level of implementation has been made between all the

surveyed eight banks for each of the seven innovative HRM practices, so that a clear picture

can be displayed and analysed. Out of 402 respondents of this present study, 53 were of State

Bank of India, 52 of Punjab National Bank, 52 of Central Bank of India, 50 of Oriental Bank

of Commerce, 49 of ICICI Bank, 50 of HDFC bank, 48 of Axis bank and 48 of Yes Bank.

4.2.3.1 Inter-Bank Comparison of the Level of Implementation of Innovative

Recruitment and Selection Practices

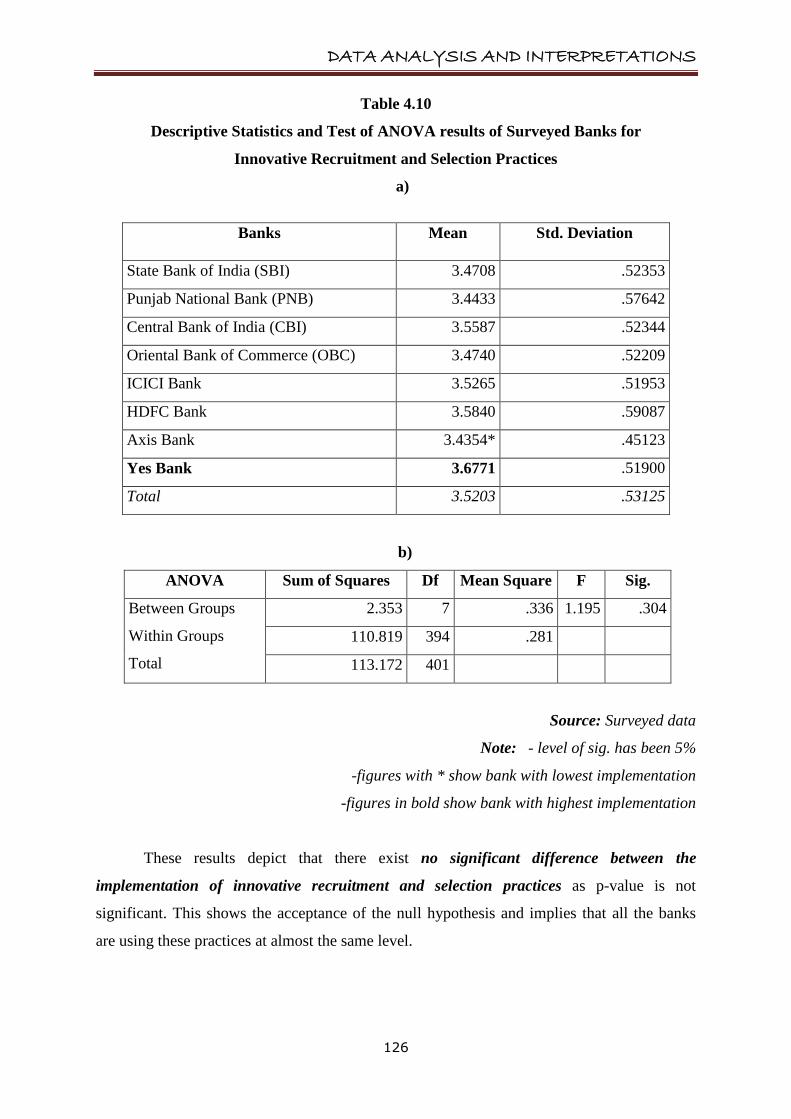

Table 4.10 explains the descriptive statistical and ANOVA test results of the surveyed

banks for innovative recruitment and selection practices. This table shows that although all

the eight banks are implementing the innovative recruitment and selection practices to more

than moderate extent but less than high extent, yet, the YES bank is implementing these

practices at the highest level with a mean score of 3.6771 when compared among all the eight

banks. However, the lowest scoring bank is the Axis bank whose mean score is 3.4354. There

is a difference among all the eight banks in the implementation of these innovations but to

check whether these results are significant or not, ANOVA test has been applied.

DATA ANALYSIS AND INTERPRETATIONS

126

Table 4.10

Descriptive Statistics and Test of ANOVA results of Surveyed Banks for

Innovative Recruitment and Selection Practices

a)

b)

ANOVA Sum of Squares Df Mean Square F Sig.

Between Groups

Within Groups

Total

2.353 7 .336 1.195 .304

110.819 394 .281

113.172 401

Source: Surveyed data

Note: - level of sig. has been 5%

-figures with * show bank with lowest implementation

-figures in bold show bank with highest implementation

These results depict that there exist no significant difference between the

implementation of innovative recruitment and selection practices as p-value is not

significant. This shows the acceptance of the null hypothesis and implies that all the banks

are using these practices at almost the same level.

Banks Mean Std. Deviation

State Bank of India (SBI) 3.4708 .52353

Punjab National Bank (PNB) 3.4433 .57642

Central Bank of India (CBI) 3.5587 .52344

Oriental Bank of Commerce (OBC) 3.4740 .52209

ICICI Bank 3.5265 .51953

HDFC Bank 3.5840 .59087

Axis Bank 3.4354* .45123

Yes Bank 3.6771 .51900

Total 3.5203 .53125

DATA ANALYSIS AND INTERPRETATIONS

127

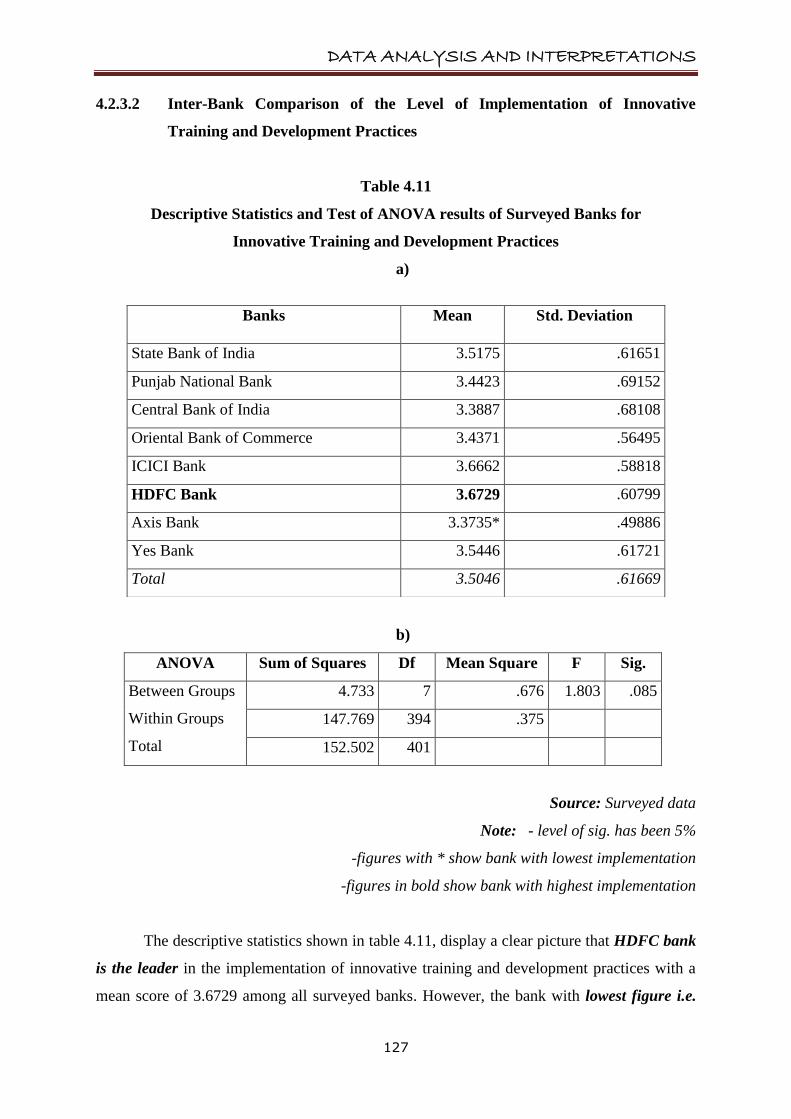

4.2.3.2 Inter-Bank Comparison of the Level of Implementation of Innovative

Training and Development Practices

Table 4.11

Descriptive Statistics and Test of ANOVA results of Surveyed Banks for

Innovative Training and Development Practices

a)

b)

ANOVA Sum of Squares Df Mean Square F Sig.

Between Groups

Within Groups

Total

4.733 7 .676 1.803 .085

147.769 394 .375

152.502 401

Source: Surveyed data

Note: - level of sig. has been 5%

-figures with * show bank with lowest implementation

-figures in bold show bank with highest implementation

The descriptive statistics shown in table 4.11, display a clear picture that HDFC bank

is the leader in the implementation of innovative training and development practices with a

mean score of 3.6729 among all surveyed banks. However, the bank with lowest figure i.e.

Banks Mean Std. Deviation

State Bank of India 3.5175 .61651

Punjab National Bank 3.4423 .69152

Central Bank of India 3.3887 .68108

Oriental Bank of Commerce 3.4371 .56495

ICICI Bank 3.6662 .58818

HDFC Bank 3.6729 .60799

Axis Bank 3.3735* .49886

Yes Bank 3.5446 .61721

Total 3.5046 .61669

DATA ANALYSIS AND INTERPRETATIONS

128

3.3735 is Axis bank. Table reveals the differences in the mean scores of implementation of

this practice among all the eight banks. However, claiming that these differences are due to

some facts will be statistically wrong. Therefore, another hypothesis has been checked in this

study by applying ANOVA. The results of ANOVA table depict that the null hypothesis will

be accepted again as p-value is not significant. It means that the innovative training and

development practices are being implemented at same level among all the surveyed banks. If

some difference lies, then that may be due to chance only.

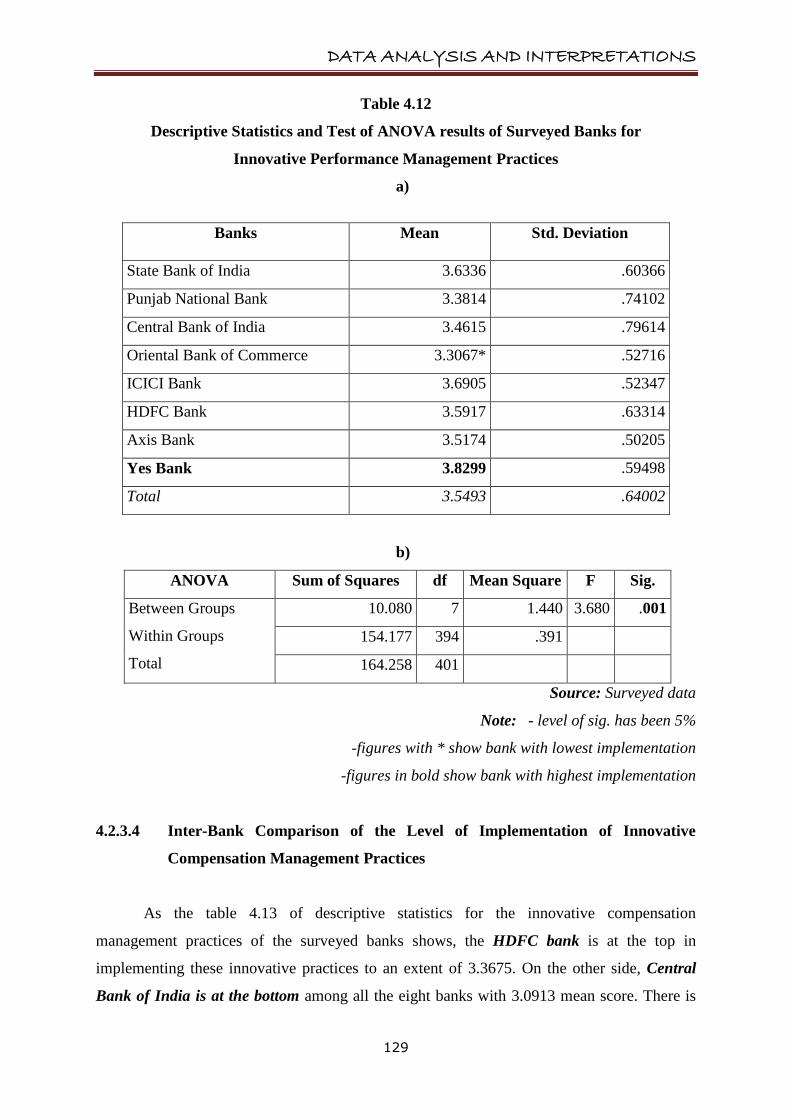

4.2.3.3 Inter-Bank Comparison of the Level of Implementation of Innovative

Performance Management Practices

Table 4.12 (a) shows the mean scores and standard deviations of all the surveyed

banks for implementing these innovations. As per the results of this table, YES bank is

implementing these innovative practices to an extent of 3.8299 which is the highest score

among all eight banks. Oriental Bank of Commerce is the lowest in the race with a mean

score of 3.3067. There is variation in the level of implementation of these practices among all

the surveyed banks.

Despite the above results, it can‟t be said that there lies a significant difference among

all the surveyed banks in implementing innovative performance management practices until

and unless it is statistically proved by applying ANOVA. The results of ANOVA in the table

4.12 (b) show that the p-value is less than 0.05. This proposes the acceptance of alternate

hypothesis, i.e. there is a significant difference in the level of implementation of innovative

performance management practices in all the eight banks. Therefore, the differences shown

in the descriptive statistics table are statistically proven. This may be because of the reason

that the all banks are not paying similar attention to the innovations in the appraisal criteria of

their employees. Traditional methods are still being used in some banks; which has been

confirmed in the earlier results of public private sector comparison of these practices.

DATA ANALYSIS AND INTERPRETATIONS

129

Table 4.12

Descriptive Statistics and Test of ANOVA results of Surveyed Banks for

Innovative Performance Management Practices

a)

b)

ANOVA Sum of Squares df Mean Square F Sig.

Between Groups

Within Groups

Total

10.080 7 1.440 3.680 .001

154.177 394 .391

164.258 401

Source: Surveyed data

Note: - level of sig. has been 5%

-figures with * show bank with lowest implementation

-figures in bold show bank with highest implementation

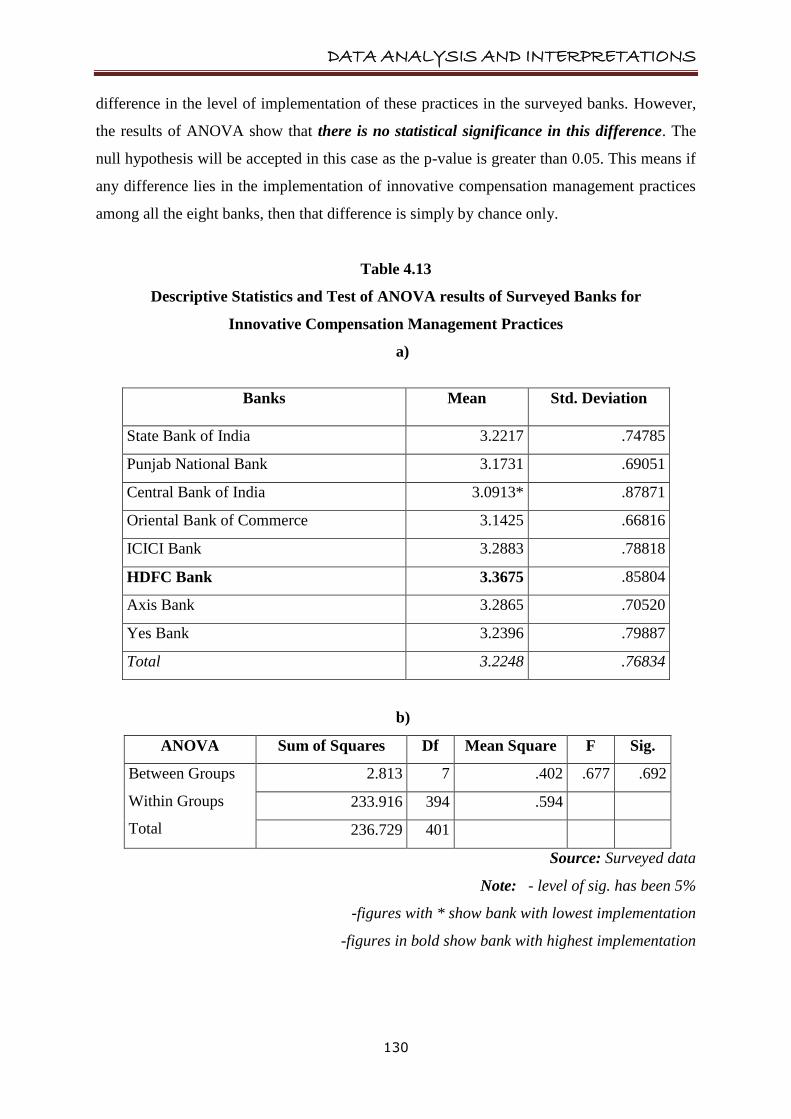

4.2.3.4 Inter-Bank Comparison of the Level of Implementation of Innovative

Compensation Management Practices

As the table 4.13 of descriptive statistics for the innovative compensation

management practices of the surveyed banks shows, the HDFC bank is at the top in

implementing these innovative practices to an extent of 3.3675. On the other side, Central

Bank of India is at the bottom among all the eight banks with 3.0913 mean score. There is

Banks Mean Std. Deviation

State Bank of India 3.6336 .60366

Punjab National Bank 3.3814 .74102

Central Bank of India 3.4615 .79614

Oriental Bank of Commerce 3.3067* .52716

ICICI Bank 3.6905 .52347

HDFC Bank 3.5917 .63314

Axis Bank 3.5174 .50205

Yes Bank 3.8299 .59498

Total 3.5493 .64002

DATA ANALYSIS AND INTERPRETATIONS

130

difference in the level of implementation of these practices in the surveyed banks. However,

the results of ANOVA show that there is no statistical significance in this difference. The

null hypothesis will be accepted in this case as the p-value is greater than 0.05. This means if

any difference lies in the implementation of innovative compensation management practices

among all the eight banks, then that difference is simply by chance only.

Table 4.13

Descriptive Statistics and Test of ANOVA results of Surveyed Banks for

Innovative Compensation Management Practices

a)

b)

ANOVA Sum of Squares Df Mean Square F Sig.

Between Groups

Within Groups

Total

2.813 7 .402 .677 .692

233.916 394 .594

236.729 401

Source: Surveyed data

Note: - level of sig. has been 5%

-figures with * show bank with lowest implementation

-figures in bold show bank with highest implementation

Banks Mean Std. Deviation

State Bank of India 3.2217 .74785

Punjab National Bank 3.1731 .69051

Central Bank of India 3.0913* .87871

Oriental Bank of Commerce 3.1425 .66816

ICICI Bank 3.2883 .78818

HDFC Bank 3.3675 .85804

Axis Bank 3.2865 .70520

Yes Bank 3.2396 .79887

Total 3.2248 .76834

DATA ANALYSIS AND INTERPRETATIONS

131

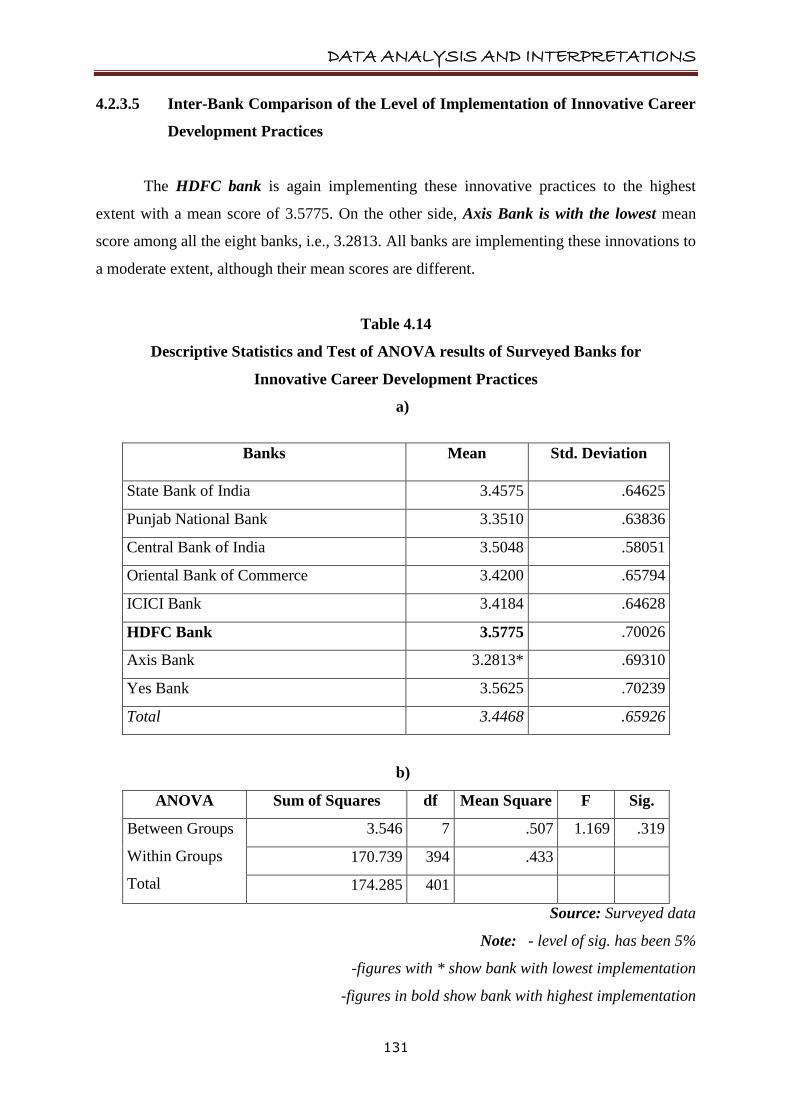

4.2.3.5 Inter-Bank Comparison of the Level of Implementation of Innovative Career

Development Practices

The HDFC bank is again implementing these innovative practices to the highest

extent with a mean score of 3.5775. On the other side, Axis Bank is with the lowest mean

score among all the eight banks, i.e., 3.2813. All banks are implementing these innovations to

a moderate extent, although their mean scores are different.

Table 4.14

Descriptive Statistics and Test of ANOVA results of Surveyed Banks for

Innovative Career Development Practices

a)

b)

ANOVA Sum of Squares df Mean Square F Sig.

Between Groups

Within Groups

Total

3.546 7 .507 1.169 .319

170.739 394 .433

174.285 401

Source: Surveyed data

Note: - level of sig. has been 5%

-figures with * show bank with lowest implementation

-figures in bold show bank with highest implementation

Banks Mean Std. Deviation

State Bank of India 3.4575 .64625

Punjab National Bank 3.3510 .63836

Central Bank of India 3.5048 .58051

Oriental Bank of Commerce 3.4200 .65794

ICICI Bank 3.4184 .64628

HDFC Bank 3.5775 .70026

Axis Bank 3.2813* .69310

Yes Bank 3.5625 .70239

Total 3.4468 .65926

DATA ANALYSIS AND INTERPRETATIONS

132

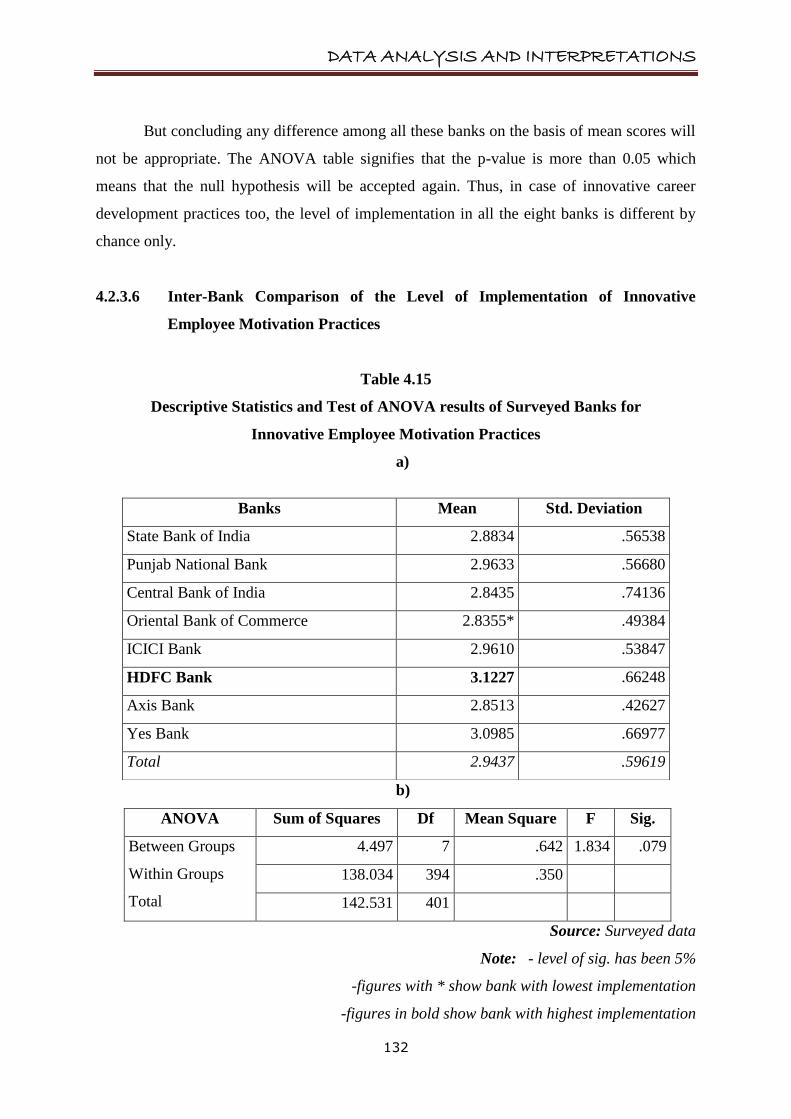

But concluding any difference among all these banks on the basis of mean scores will

not be appropriate. The ANOVA table signifies that the p-value is more than 0.05 which

means that the null hypothesis will be accepted again. Thus, in case of innovative career

development practices too, the level of implementation in all the eight banks is different by

chance only.

4.2.3.6 Inter-Bank Comparison of the Level of Implementation of Innovative

Employee Motivation Practices

Table 4.15

Descriptive Statistics and Test of ANOVA results of Surveyed Banks for

Innovative Employee Motivation Practices

a)

b)

ANOVA Sum of Squares Df Mean Square F Sig.

Between Groups

Within Groups

Total

4.497 7 .642 1.834 .079

138.034 394 .350

142.531 401

Source: Surveyed data

Note: - level of sig. has been 5%

-figures with * show bank with lowest implementation

-figures in bold show bank with highest implementation

Banks Mean Std. Deviation

State Bank of India 2.8834 .56538

Punjab National Bank 2.9633 .56680

Central Bank of India 2.8435 .74136

Oriental Bank of Commerce 2.8355* .49384

ICICI Bank 2.9610 .53847

HDFC Bank 3.1227 .66248

Axis Bank 2.8513 .42627

Yes Bank 3.0985 .66977

Total 2.9437 .59619

DATA ANALYSIS AND INTERPRETATIONS

133

The level of implementation of innovative employee motivation practices has also

been checked with the help of the mean scores and ANOVA test. The descriptive statistics in

table 4.15 (a) clearly depicts that HDFC bank is the leader in the implementation of

innovative employee motivation practices with a mean score of 3.1227 among all eight banks

followed by YES bank having the mean score of 3.0985. However, the bank with the lowest

score is the Oriental Bank of Commerce. Difference in the mean scores is clear from the

table. Guest, 1997 proposed that performance at individual level depended upon high

motivation, possession of the necessary skills and abilities and an appropriate role and

understanding of that role. The motivation techniques can be used to retain employees and

improve job performance if combined with compensation techniques. Therefore, the banks

need to concentrate more on these practices for improving the employee performance. The

ANOVA results shown in the table 4.15 (b) convey that the p-value is more than 0.05.

Therefore, the differences in the level of implementation of the innovative employee

motivation practices shown by descriptive statistics were by chance only and there is no

statistical significance of these differences among the eight banks.

4.2.3.7 Inter-Bank Comparison of the Level of Implementation of Innovative

Employee Security Practices

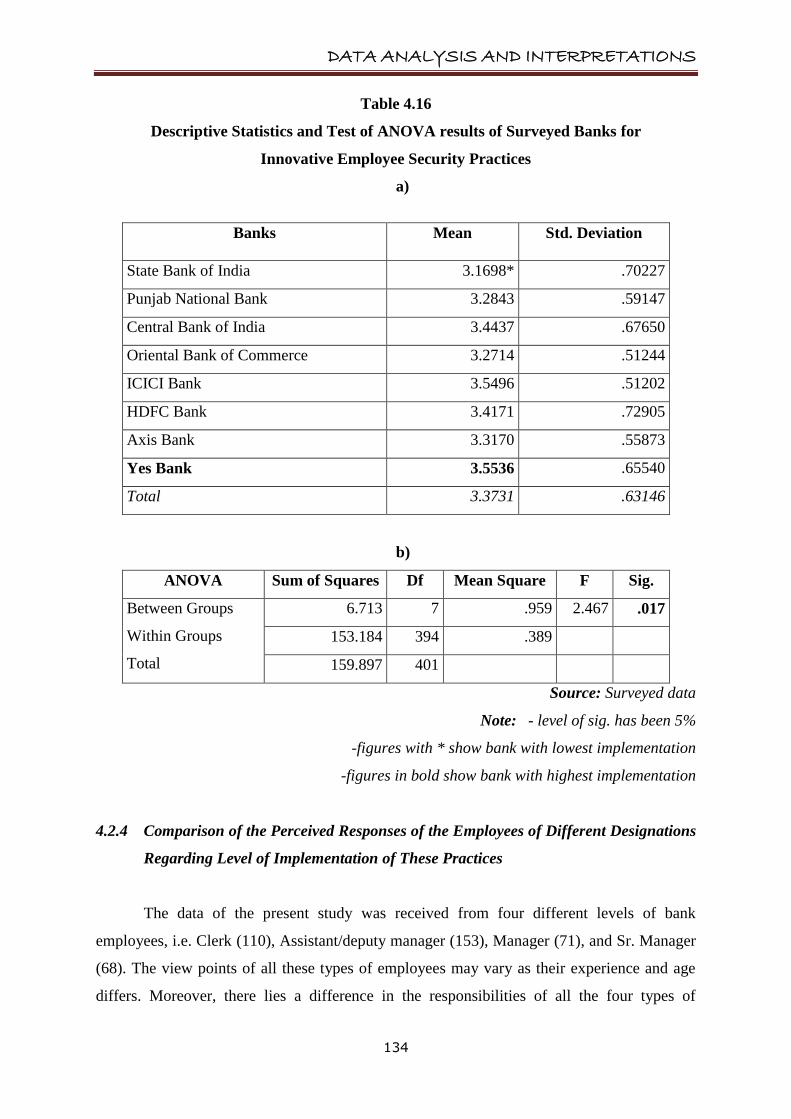

The descriptive scores of this factor (table 4.16) dictate that the YES bank is leading

with a mean score of 3.5536, while the no. 1 bank of India, the State bank of India is the

least scorer in adopting new and improved employee security practices in its bank whose

mean is 3.1698. For statistical analysis of this difference, ANOVA test has been applied.

ANOVA test results clarify that the p-value is significant. Therefore, the alternate hypothesis,

which claims that there is a significant difference between the implementation of employee

security practices among all eight banks, has been accepted. This means that the difference

shown by the mean scores of this factor is statistically proved. Thus, State Bank of India,

along with other public sector banks needs to concentrate more on the employee security

practices so that they can also compete in this dynamic environment.

DATA ANALYSIS AND INTERPRETATIONS

134

Table 4.16

Descriptive Statistics and Test of ANOVA results of Surveyed Banks for

Innovative Employee Security Practices

a)

b)

ANOVA Sum of Squares Df Mean Square F Sig.

Between Groups

Within Groups

Total

6.713 7 .959 2.467 .017

153.184 394 .389

159.897 401

Source: Surveyed data

Note: - level of sig. has been 5%

-figures with * show bank with lowest implementation

-figures in bold show bank with highest implementation

4.2.4 Comparison of the Perceived Responses of the Employees of Different Designations

Regarding Level of Implementation of These Practices

The data of the present study was received from four different levels of bank

employees, i.e. Clerk (110), Assistant/deputy manager (153), Manager (71), and Sr. Manager

(68). The view points of all these types of employees may vary as their experience and age

differs. Moreover, there lies a difference in the responsibilities of all the four types of

Banks Mean Std. Deviation

State Bank of India 3.1698* .70227

Punjab National Bank 3.2843 .59147

Central Bank of India 3.4437 .67650

Oriental Bank of Commerce 3.2714 .51244

ICICI Bank 3.5496 .51202

HDFC Bank 3.4171 .72905

Axis Bank 3.3170 .55873

Yes Bank 3.5536 .65540

Total 3.3731 .63146

DATA ANALYSIS AND INTERPRETATIONS

135

employees because of their scale and designation. This might lead to a variance in the

opinions of these employees regarding the implementation of these innovations in the HRM

practices in their banks. Therefore, a comparison has also been made between the viewpoints

of all these employees designation wise to have more clarity on the implementation. These

viewpoints have been compared for each of the seven innovative HR practices under this

study along with their hypothetical tests.

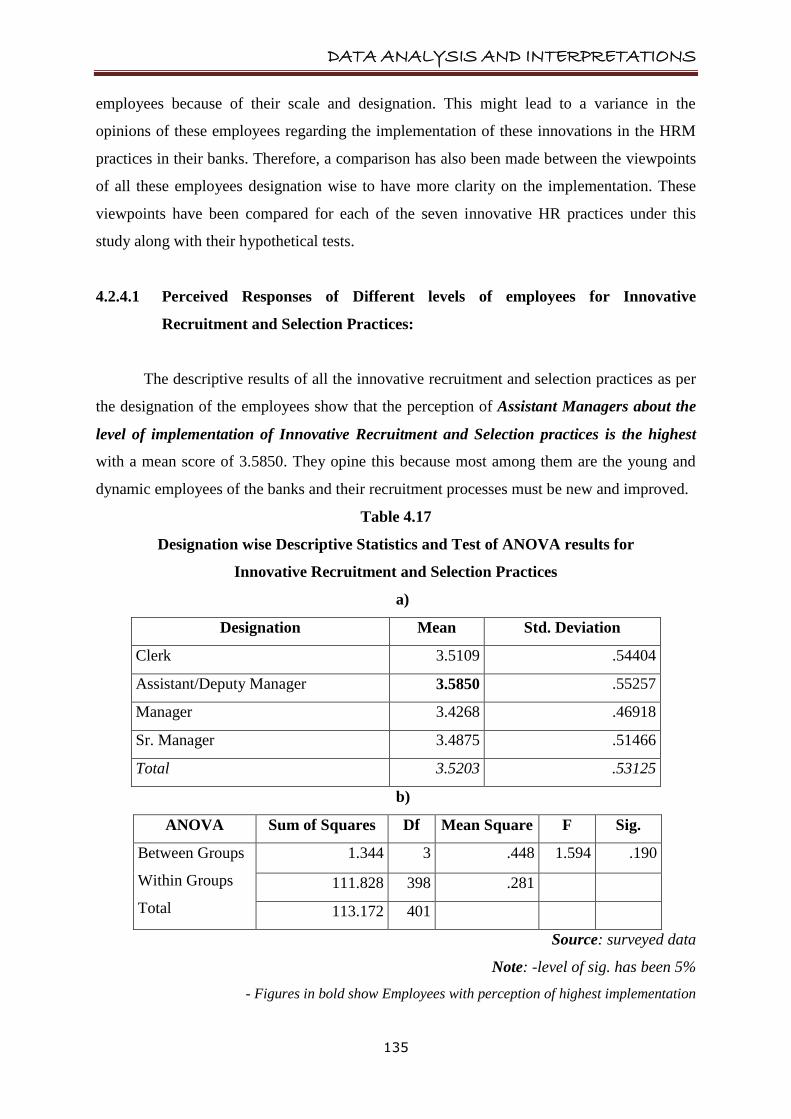

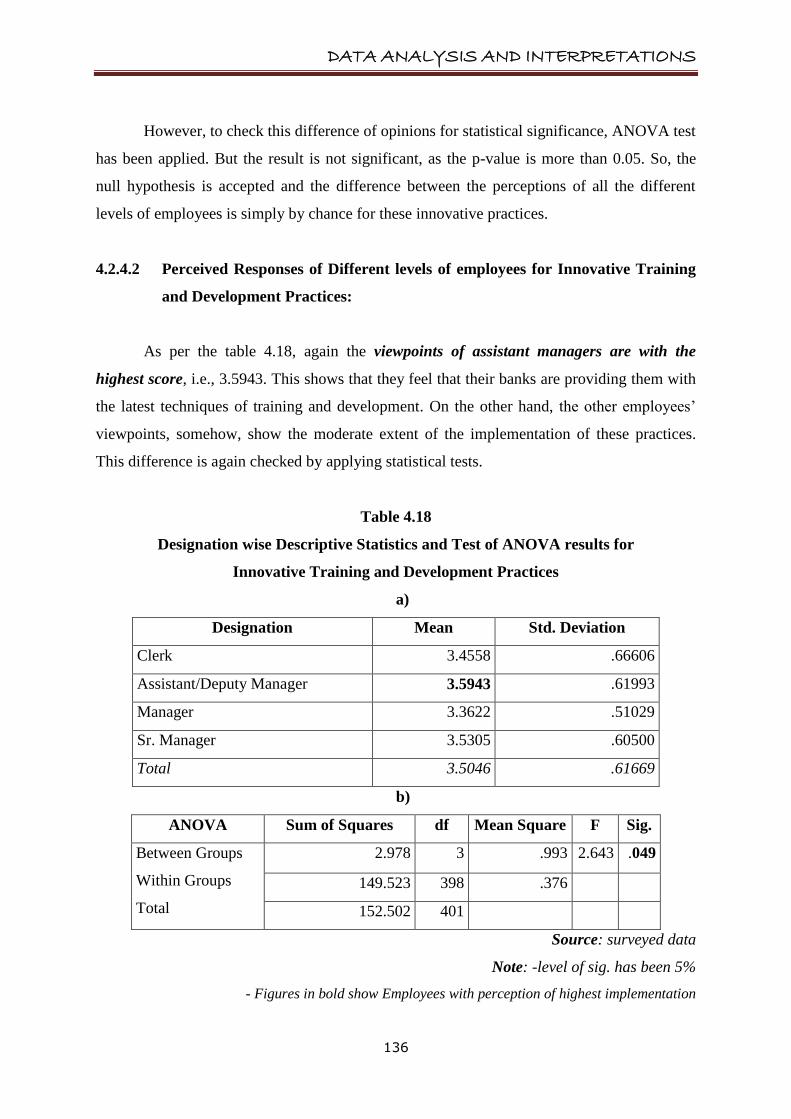

4.2.4.1 Perceived Responses of Different levels of employees for Innovative

Recruitment and Selection Practices:

The descriptive results of all the innovative recruitment and selection practices as per

the designation of the employees show that the perception of Assistant Managers about the

level of implementation of Innovative Recruitment and Selection practices is the highest

with a mean score of 3.5850. They opine this because most among them are the young and

dynamic employees of the banks and their recruitment processes must be new and improved.

Table 4.17

Designation wise Descriptive Statistics and Test of ANOVA results for

Innovative Recruitment and Selection Practices

a)

Designation Mean Std. Deviation

Clerk 3.5109 .54404

Assistant/Deputy Manager 3.5850 .55257

Manager 3.4268 .46918

Sr. Manager 3.4875 .51466