darwin professional underwriters,...

TRANSCRIPT

Darwin Professional Underwriters, Inc.Presentation for the Insurance Investor Conference

March 2007

Forward-Looking Statements

The following information includes forward-looking statements. All statements other than historical information or statements of current condition contained herein, including statements regarding our future financial performance, our business strategy and expected developments in the commercial insurance market, are forward-looking statements. The words "expect," "intend," "plan," "believe," "project," "may," "estimate," "continue," "anticipate," "will," and similar expressions of a future or forward-looking nature identify forward-looking statements.

We have based these forward-looking statements on management’s current expectations. These statements are subject to a number of risks, uncertainties and other factors that may cause actual events or results to differ materially from those expressed or implied by any of these statements. These statements should not be regarded as a representation by us, the underwriters or any other person that the anticipated events, future plans or other expectations will be achieved. We undertake no obligation to update publicly or review for any reason any forward-looking statement after the date of this presentation or to conform these statements to actual results or changes in our expectations. All subsequent written and oral forward-looking statements attributable to us or individuals acting on our behalf are expressly qualified in their entirety by this paragraph.

Neither the Private Securities Litigation Reform Act of 1995 nor Section 27A of the Securities Act of 1933 provides any protection to us for statements made in this presentation.

2

Stephen Sills

President and Chief Executive Officer

Darwin Overview

• Specialty insurer focused on professional liability

• $246.3 million of premium written for 2006

– Diversified across D&O, E&O and Medical Malpractice Liability

– Focused on small and middle market business

– Strong presence across the health care industry spectrum

• Founded in 2003 by Stephen Sills and Alleghany Corporation

• Current ownership:

– 55% Alleghany / 35% Public / 10% Management

• Rated “A-” (Excellent) by A.M. Best

Disciplined growth through specialized and proven expertise

4

Darwin Investment Highlights

Deep and proven management team

Attractive market dynamics

Built to identify and underwrite profitable market niches

Select distribution network that understands Darwin’s risk parameters

Technology platform that enhances distribution and supports efficient operations

Integrated, disciplined underwriting culture

Ready for “loose bricks”

Strong capital base

=

5

Continued Superior Growth

Darwin’s Management Team

Name Title Previous Experience Years Experience

Bob Asensio SVP – Chief Information Officer Executive Risk Inc. 25

Paul Martin SVP – Chief Actuary USFG 30

David Newman SVP – Chief Underwriting Officer Lloyds of London 30

Paul Romano SVP – Underwriting Executive Risk Inc. 25

Mark Rosen SVP and General Counsel Executive Risk Inc. 30

Jack Sennott Chief Financial Officer Executive Risk Inc. 20

Stephen Sills Chairman, President & CEO Executive Risk Inc. 30

Management increased its ownership during the IPO

6

Darwin’s Successful IPO

• $96 million initial public offering completed on May 19, 2006

– Priced at $16.00 per share

• Currently trading at ~$25.50

– Market capitalization of ~$435 million

• Offering reduced Alleghany’s ownership from 90% to approximately 55%

• Increased future financial flexibility

7

Shareholder Return

$80

$90

$100

$110

$120

$130

$140

$150

$160

5/19/0

6

5/31/0

6

6/30/0

6

7/31/0

6

8/31/0

6

9/30/0

6

10/31

/06

11/30

/06

12/31

/06

Darwin Professional Underwriters, Inc. S&P 500 Index S&P Property & Casualty Insurance Index

8

Comparison of Darwin’s Cumulative Total Shareholder Return as of December 31, 2006

What’s Unique About our Operating Model?

• Focus on small accounts

– Small business outperforms large business in softer markets

• Select distribution

• Portfolio management of our business

• Separation of “engineering” and “manufacturing”

• “Ground-up” underwriting approach

• Our health care expertise

• Technology geared to handle small accounts and to promote operational efficiency

9

Attractive Market Dynamics, But Rates Softening

• Total market of $20 billion – still room to grow

• Profitable pricing driven by poor industry underwriting results in late 1990s and early 2000s

• Companies without legacy issues are positioned for superior profitability

• As market softens, profits can be protected by writing less price-elastic small account business.

Market Opportunity Rate Changefrom 4Q ‘99 – 4Q ‘06

Darwin’s business model accentuates the impact of attractive market dynamics

Source: Council of Insurance Agents and Brokers

10

Darwin’s Distribution of Business by Size

Small Medium Large

As the market softens Darwin’s book increases its weight in small business accordingly.

Hit Rate

9.9%

Hit Rate

12.8%

Submissions

Risks Bound

86% Growth

1,454

Risks Bound

39% Growth Submissions

21,000140

Producers

180 Producers

15,100

2.9% Point Improvement

2,700

Select Distribution Network

Focused DistributionFocused Distribution

• 180 carefully selected distribution partners

• Significant benefits over the “open brokerage” model

• Program administrators provide access to select markets

Key CharacteristicsKey Characteristics

• Technical expertise

• Shared commitment to excellent service

• Ability of Darwin to capture a meaningful portion of distributors’business

Fewer Producers / Greater ProductionFewer Producers / Greater Production

12

2005 2006

Our Business Portfolio – Business Mix

A balanced business, responding to market opportunities

E&O 45.1%

D&O 16.5%

Medical Malpractice

38.4%

Total Premiums: $246.3 million

Total GPW Growth2006 Gross Premiums Written($ in millions)

13

E&O 45.1%

D&O 16.5%

Medical Malpractice

38.4%

D&O – Underweight, Pricing Pressure2006 Gross Premiums Written

Selected Classes Yearof Business Started

Public Accounts 2003Private Accounts 2003Employment Practices 2003Health Care Management Liability 2003Fiduciary 2004Non-profit AccountsFinancial Institutions 2006

D&O Premiums: $40.6 million

D&O GPW Growth

14

($ in millions)

2005

D&O Price Monitoring

-3.3%$12,325,396$12,502,6981472005

Rate ChangeRenewal PremiumExpiring PremiumNo. of RenewalsReport Year

-1.4%$19,647,689$19,199,4323072006

-7.9%$6,361,727$5,709,523462004

Rate change calculated as premium change adjusted to take into account the effect of changes in limit, deductible / attachment, policy term, commission, exposure and claims-made step

As of 12/31/06

15

E&O 45.1%

D&O 16.5%

Medical Malpractice

38.4%

E&O – Overweight, Expanding Classes2006 Gross Premiums Written E&O GPW Growth

E&O Premiums: $111.0 million

Selected Classes Yearof Business Started

Managed Care E&O 2003

Lawyers Professional E&O 2003

Insurance Agents E&O 2003

Miscellaneous Professional E&O 2003

Technology E&O 2005

Municipal Entity and Public Officials E&O 2005

Insurance Company E&O 2006

Psychologists E&O 2006

($ in millions)

16

E&O Price Monitoring

-7.2%$26,886,429$27,464,4382612005

Rate ChangeRenewal PremiumExpiring PremiumNo. of RenewalsReport Year

-7.6%$45,892,196$43,370,1845402006

-0.8%$10,190,035$8,640,302792004

Rate change calculated as premium change adjusted to take into account the effect of changes in limit, deductible / attachment, policy term, commission, exposure and claims-made step

As of 12/31/06

17

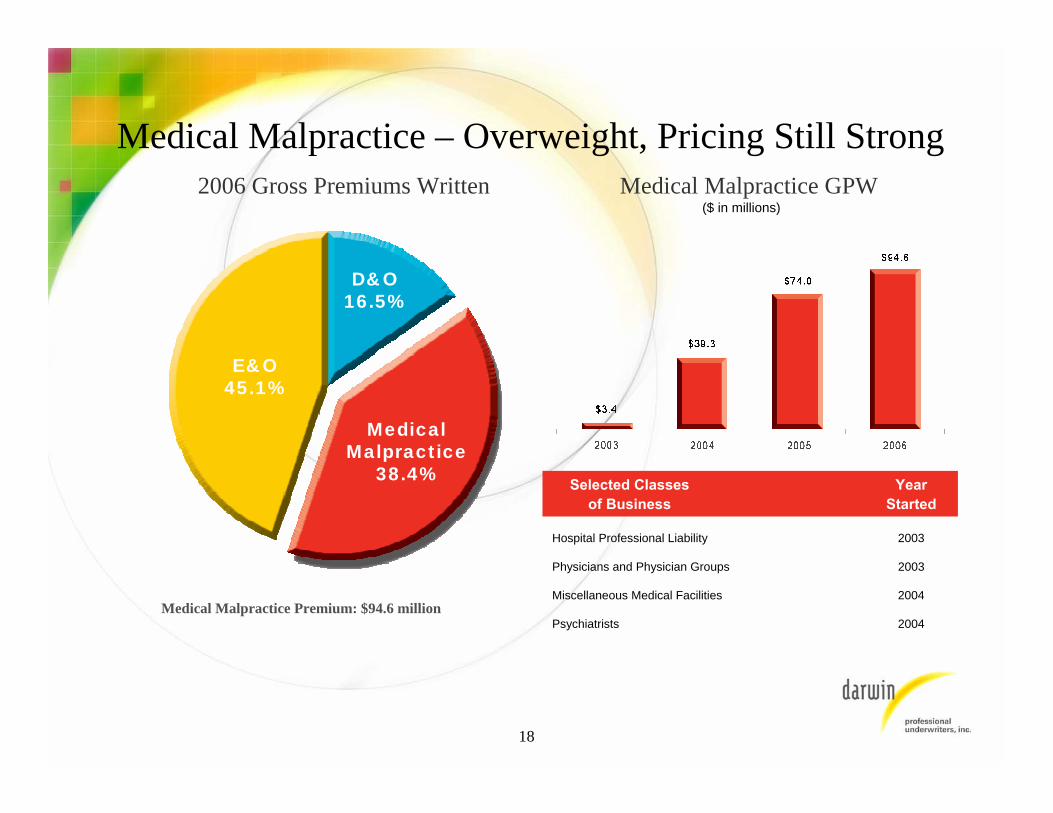

Medical Malpractice – Overweight, Pricing Still Strong2006 Gross Premiums Written Medical Malpractice GPW

Medical Malpractice Premium: $94.6 million

Selected Classes Yearof Business Started

Hospital Professional Liability 2003

Physicians and Physician Groups 2003

Miscellaneous Medical Facilities 2004

Psychiatrists 2004

($ in millions)

18

E&O 45.1%

D&O 16.5%

Medical Malpractice

38.4%

Medical Malpractice Price MonitoringAs of 12/31/06

Rate change calculated as premium change adjusted to take into account the effect of changes in limit, deductible / attachment, policy term, commission, exposure and claims-made step

+3.6%$32,846,829$29,150,9171092005

Rate ChangeRenewal PremiumExpiring PremiumNo. of RenewalsReport Year

-2.2%$41,449,736$38,861,9781872006

+4.4%$4,062,486$2,937,42682004

19

Health Care Spending in the U.S.A significant part of the U.S. GNP and projected to grow.

2005 2015

$336

$792

($ in Billions)

$3,960

$1,976

Total HC spending is estimated at over 22% of GNP

Projected Health Care Spending in the U.S. Projected Prescription Drug Spending in the U.S.

Medicare Spending

Total Health Care spending

20

($ in Billions)

Demonstrated Expertise in Health Care Industry

Focus on health care encompasses all business lines

2006 Gross Premiums Written Health Care GPW($ in millions)

21

E&O 45.1%

D&O 16.5%

Medical Malpractice

38.4%

• Service differentiation with key producers

• Drives cost advantages

• Difficult-to-serve markets become profitable

• Promotes real-time underwriting / pricing refinements

• Enhances tactical flexibility

• Everything has been created in the past three years

• Senior management is committed to technology-based corporate strategy

• Technology permeates every aspect of our business

• Single operating platform

• Seamless interactivity between claims, underwriting, actuarial and finance

• (i-bind)sm extends Darwin’s operating systems to its producers

Why Our Technology is SuperiorWhy Our Technology is SuperiorBenefits of Superior TechnologyBenefits of Superior Technology

Technology drives competitive advantage

Growth TechnologyExpense Control ProfitabilityDrives

Drives Drives

22

Executing the Vision

Effective Effective DistributionDistribution

Strong Capital Strong Capital Base to Support Base to Support

GrowthGrowth

Expanded Classes Expanded Classes of Businessof Business

Profitable Profitable Underwriting Underwriting OpportunitiesOpportunities

.72:1

9

180

1%+

Underwriting

Leverage

Select

Distribution

Partners

New Classes

of Business

Added Since

2003

Darwin

Market

Share of

$20B Market

23

Jack Sennott

Senior Vice President and Chief Financial Officer

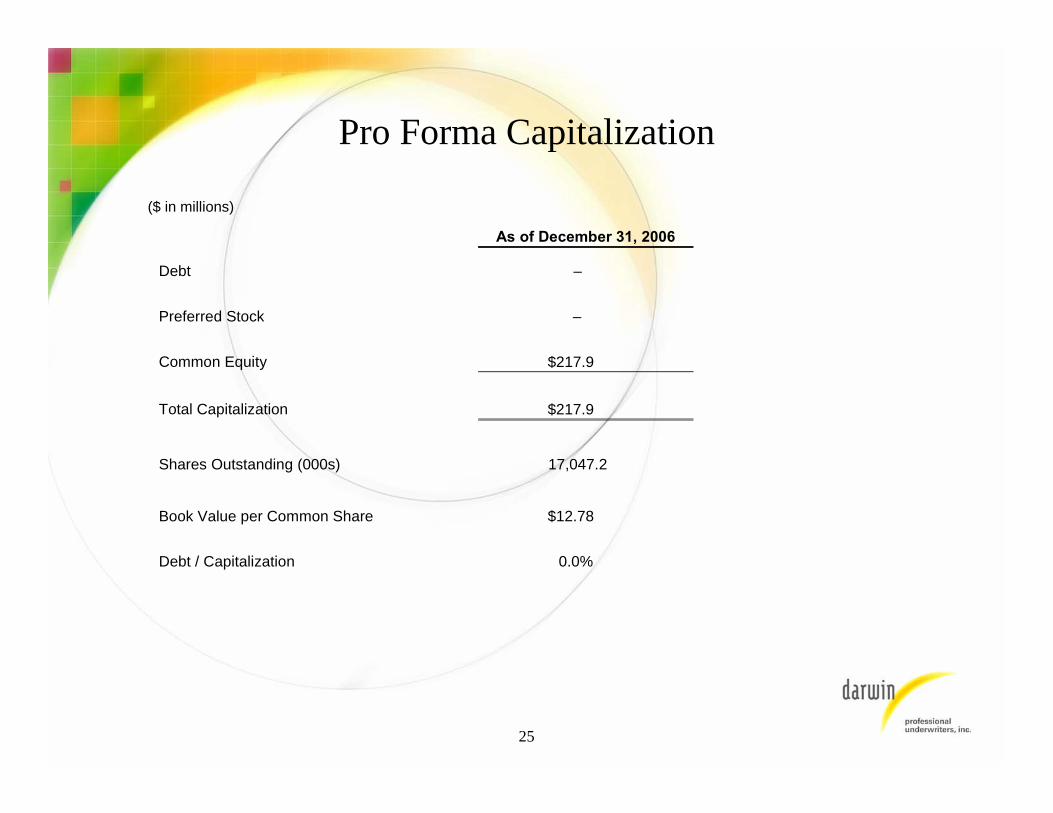

Pro Forma Capitalization

($ in millions)

As of December 31, 2006

Debt –

Preferred Stock –

Common Equity $217.9

Total Capitalization $217.9

Shares Outstanding (000s) 17,047.2

Book Value per Common Share $12.78

Debt / Capitalization 0.0%

25

GAAP Financial Results

As of December 31, 2005 vs 2004 2006 vs 2005 2004 2005 2006 ∆ ∆

Gross Premiums Written

$100,455 $165,824 $246,252 65.1% 48.5%

Net Premiums Written $70,500 $100,650 $157,004 42.8% 56.00%

Net Operating Income(1) $47 $3,821 $15,957 NM 417.6%

GAAP Underwriting Ratios:

Loss Ratio 64.3% 69.2% 66.9%

Expense Ratio 35.6% 28.1% 27.4%

Combined Ratio 99.9% 97.3% 94.3%

(1) Excludes realized gains and losses after taxes.

($ in thousands)

26

Overview of Loss ReservesBy Statutory Line of Business - 12/31/06 By Category – Total $263.5 Million

Darwin’s loss reserves are predominantly IBNR

27

Medicalliability,

claims-made

Other liability,claims-made

38.4%60%

ULAE: 3.0%

$7.8 Million Case: 12.6%

$33.1 Million

IBNR: 84.4%

$222.6 MillionOther liability,

occurrence

1.61%

Darwin Underwriting Results

65.0%

67.0%

54.8%

44.8%

Current Booked Loss Direct /

LAE Ratio

65.0%

67.0%

65.0%

65.0%

Initial Booked Loss Direct /

LAE Ratio

5.0%$10.6M$210.7M2006

10.2%$42.1M$412.9MTOTAL

19.3%$25.4M$131.8M2005

8.7%$5.7M$65.0M2004

7.8%$0.4M$5.4M2003

Case Incurred Loss / LAE

Ratio

Gross Case Incurred

Loss / LAE

Gross Earned PremiumReport Year

December 31, 2006

28

A+, A, A-15.0%

AA+, AA, AA-13.1%

BBB+1.2%

AAA70.7%

Short-term Investments

17.4%

Fixed Maturities

82.6%

Conservative Investment Portfolio12/31/06 Investment Portfolio Fixed Maturity Ratings and Breakdown

Current Tax-Equivalent Yield: 5.53%Average Duration: 3.99 Years

29

Market Value: $399.4 Million

10%

20%

30%

2006 – 2008 NPW Growth

Potential (CAGR)

ImpliedUnderwriting Leverage at 12/31/08 (3)

0.5x

0.7x

0.9x

Next Steps

(1) Underwriting leverage defined as NPW / equity. Comparable data from SNL Financials.(2) Simple average excluding Darwin.(3) Underwriting leverage defined as 2008E NPW/ 2008E equity. 2008E NPW based on potential 3-year CAGR.

2008E equity based on an assumed growth per annum of 9% for purposes of this page.

Growth Potential of DarwinGrowth Potential of Darwin

Our capital base will support strong premium growth

Underwriting Leverage Underwriting Leverage (1)(1) of of Comparable SmallComparable Small--cap Specialty Companiescap Specialty Companies

30

NATL TWGP JRVR ACAP DR

0.7x0.6x

0.8x

1.5x1.5x

Avg. 1.1x (2)

0.0x

0.5x

1.0x

1.5x

2.0x

ROE Target for Current Capital Base

Underwriting Underwriting Leverage Leverage (1)(1)

Investment Investment Leverage Leverage (1)(1)

90% Combined Ratio 90% Combined Ratio (Target for Medium Term)(Target for Medium Term)

Targets Targets STET STET

Darwin Darwin Year End 2006Year End 2006

0.7x

1.0x

1.7x

2.0x–

IllustrativeIllustrativeROE ROE

–

Note: Peer group includes ACAP, TWGP, NATL and JRVR. Based on financial data at and for the period ended 12/31/06.(1) Underwriting leverage defined as NPW / equity. Investment leverage defined average invested assets / equity.(2) Based on current tax-equivalent yield of 5.53%.

9.6%

2.0%

1.7%(2)

13.3%

31

Key Financial Considerations

• Pricing set in a hard market

• Strategy in place as market softens

• Expansion of premium base within current product classes

– Additional growth opportunities through “loose bricks”

– Fully deploy current capital base

• Target 90% combined ratio

– Conservative reserving philosophy – target 60% loss ratio

– Declining expense ratio as we add business

– Realization of investment in technology platform, including (i-bind)sm underwriting system

• Investment income from increased asset base

– Extending investment horizon as reserves build

– Positioned to benefit from rising rates

• Target medium-term ROE of 13%

32

Building Blocks for Success

33