dairy/ china china dairy sector - oriental patron dairy sector - fresh.pdf · equity research china...

TRANSCRIPT

Tue, 06 Nov 2012

Equi ty Research China Dairy Sector Dairy/ China

Fresh!

We initiate coverage on the China Dairy sector (3 companies) with positive

outlook and the market size will expect to be double over the next 8-10 years,

implying overall volume growth rate with a high single digit and continuous

product mix toward value-added categories. We recommend China Modern

Dairy (1117 HK, BUY) as our top pick for its fast expansion pace and organic

growth from constant raw milk yield improvement. We also favor Biostime

International (1112 HK, BUY) and seeing it as a niche fast-moving premium

baby product player in China. Its unique Mama100 membership platform

promoted strong consumer loyalty and led to a rising cross selling. As lack of

positive catalysts in short-term and lower-than-expected recovery progress, we

rate Mengniu (2319 HK, HOLD) with neutral.

Upstream: raw milk

Our preference is based on i) strong demand from downstream dairy operators

for high quality raw milk; ii) undergoing industry consolidation and expansion in

standardized large-scale dairy farms pushed by government and targeting to

reach~48mn tons of production in 2013E with a 15% CAGR over 2011-2013E; iii)

supportive government policies, like exemptions on agricultural tax, VAT and

income tax. Raw milk price is projected to trend up moderately due to more

sourcing from large-scale farms which charge premium price and supporting from

increasing feed costs.

Downstream: Liquid milk

Liquid milk accounts for 80% of total dairy industry and is dominated by domestic

brands. The top three players, Mengniu, Yili (600887 CH, NR) and Bright Dairy

(600597 CH, NR) have an aggregate market share of about 68%. High-end liquid

milk sales growth will outpace that of mid-to-low-end driven by consumers’ trade

up after 2008 melamine scandal. Lactic acid drinks, baby and toddler milk and

flavored milk are expected to record the fastest growth rates in 2011-2014E

among liquid milk segment.

Downstream: infant formula

We believe this sub-sector will be fueled by i) the 4th baby boom; ii) atypical

consumer behavior among customs of relatively low price sensitivity; and iii)

Relaxation of China’s one-child policy. In our conservative case projection, we

expect the Chinese infant formula market to grow at a CAGR of 9% between

2012-2020E assuming no change in one-child policy application, and that of 13%

in the scenario with relaxation of one-child policy and outpace the whole dairy

market in China.

Tracy Sun

Analyst

+852 2135 0214

Sector Report

Exhibit1: Recommendat ions summary Company Stock code Rating Closed Price Target Price Upside (%)

China Modern Dairy 1117 BUY 2.02 2.64 +31%

Biostime 1112 BUY 19.98 24.60 +23%

Mengniu 2319 HOLD 23.50 24.20 +3%

Closing price as at 5 November 2012

Source: Bloomberg, OP Research

Tue, 06 Nov 2012

China Dairy Sector

Page 2 of 66

Table of Contents

What are our recommendations? ................................................................................................................. 3

Cast a glance at the China Dairy Industry .................................................................................................... 5

Major players in this markets........................................................................................................................ 7

Upstream: raw milk, the key of dairy industry ............................................................................................... 8

Downstream: Liquid milk, biggest category .................................................................................................12

Downstream: Infant formula, attractive growth prospect ..............................................................................14

China Modern Dairy (1117 HK) – Enjoy the taste of High Growth ................................................................19

Investment thesis .............................................................................................................................20

Financial analysis .............................................................................................................................28

Key risks...........................................................................................................................................30

Valuation ..........................................................................................................................................31

Financial Summary - China Modern Dairy (1117 HK) ........................................................................35

Biostime International (1112 HK) - A premium story .....................................................................................36

Investment thesis .............................................................................................................................37

Robust 1H12 results .........................................................................................................................43

Earning forecast ...............................................................................................................................44

Valuation ..........................................................................................................................................46

Key risks...........................................................................................................................................48

Financial Summary - Biostime (1112 HK) .........................................................................................51

Mengniu Dairy (2319 HK) - No surprise ......................................................................................................52

Investment thesis .............................................................................................................................53

Earnings forecast .............................................................................................................................58

Key risks...........................................................................................................................................59

Valuation ..........................................................................................................................................60

Financial Summary - Mengniu Dairy (2319 HK) ................................................................................63

Tue, 06 Nov 2012

China Dairy Sector

Page 3 of 66

What are our recommendations?

China Modern Dairy (1117 HK) – Enjoy the taste of High Growth (BUY)

TP: HK$2.64

We forecast CMD could enjoy the net profit growth at a CAGR of 34% for

FY12-FY15E. Key earnings drivers should come from i) top line growth boosted

by strong demand from downstream dairy operators for high quality raw milk as

well as 10-year take off agreement with Mengniu to secure the long-term sales

volume growth and premium selling price; ii) operating leverage generates from

its modernization and scale operation; iii) supportive government policies (i.e.

exemption on certain tax and subsidies) for the modernization of dairy farming.

Its advanced breeding, feeding and herd management techniques enable CMD to

produce the high-quality raw milk with a high double digit premium over the

industry average price. CMD targets the milk yield per milkable cow is at about

9.0 tons/annum in FY15E and 9.4 in FY17E, ultimately up to 10 tons/annum,

driven by increasing proportion of mature cows and genetic improvement.

Based on a blending DCF/PEG model, we estimate a fair value of HK$2.64 per

share, which implies 30.7% potential upside. We give a BUY rating.

Biostime International (1112 HK) - A premium story (BUY) TP:

HK$24.60

We project that Biostime could enjoy the net profit growth at a CAGR of 24% for

2011-2014E. Key earnings drivers come from top line growth boosted by infant

formula segment and consequent SG&A/sales ratio decline.

As a player in premium market, Biostime was able to achieve superior margin

over its peer average at 20% over the past five years. All its products are sourcing

from overseas to guarantee quality and safety. Its real time and effective channel

management can monitor distributors’ inventory and sales level, resulting in the

account receivables turnover days at 1 day. Its Mama 100 membership platform

promoted strong consumer loyalty, leading to a rising cross selling and saving the

expense of selling and distribution each year.

Our TP is based on a blending SOTP/DCF model, we estimate a fair value of

HK$24.60 per share, which implies undemanding 2013E PE of 14.5x and

suggests 23.1% potential upside.

Tue, 06 Nov 2012

China Dairy Sector

Page 4 of 66

Mengniu Dairy (2319 HK) - No surprise (HOLD) TP: HK$24.20

We forecast Mengniu net profit to grow at a CAGR of 10.8% for FY11-FY14E and

revenue to rise from RMB37.4bn in FY11 to RMB49.13bn in FY14E, equating to a

CAGR of 10% and led by a 7% CAGR in sales volume and a 3% CAGR of APS

hike.

It appears to us that Mengniu’s high growth era is behind us. Its brand value and

consumer loyalty are undermined after the melamine crisis in 2008 and M1

scandal in 2011. Although the new strategies initiated by new management team

can pave the way for long-term earnings growth, near-term headwind from

internal restructuring is visibility. We like Mengniu’s prudent cost control and

outstanding operating efficiency combined with continuing product mix shift

towards high-value added categories, however, all above are fully reflected in

current valuation, with 21x PE in 2013. We found the Bloomberg-consensus EPS

forecast has been revised down since December 2011 and even speed up after

Mengniu’s interim results, partly due to their concerns about recovery pace and

disappointing result of 1H12. The market bearish mood also reflected our

downside risk cautions.

Based on a blending DCF/PER model, we estimate a fair value of HK$24.20 per

share, which implies 2013E PE of 19.0x and suggests 2.98% potential upside.

We give a HOLD rating.

Tue, 06 Nov 2012

China Dairy Sector

Page 5 of 66

Cast a glance at the China Dairy Industry

Looking back, China dairy industry has growth at a rapid pace in both a

demand and supply perspective driven by continued rising rate of urbanization

and increasing disposable incomes. According to China Dairy Associate, per

capita consumption of major dairy products has increased from 2.7kg per capita

in 2000 to 16.2kg per capita in 2011, a CAGR of 17.8%.

Exhibit 2: Major dairy products per capita consumption in China, 1990-2011

Source: CEIC, OP Research

A structural problem of human being

While the CAGR was impressive, per capita consumption in China falls further

behind other developed countries and remains only one-third of developed

countries globally. We believe the major reason of consumption per capita is a

structural problem due to high prevalence of lactose intolerance of Chinese

people. Lactose intolerance individuals have insufficient level of lactase to digest

lactose, a sugar in milk. It is estimated that 75% of adults worldwide show some

decrease in lactase activity during adulthood. The frequency of decreased

lactase activity ranges from 5% in northern Europe and more than 90% in some

Asian countries. It appears to us that high prevalence of lactose intolerance is the

key bottleneck for liquid milk market growth, while high quality and value added

milk products supply (i.e. yogurt, low lactose milk, low fat milk) is like an antidote

to the genetic composition of Chinese people. The situation of Japanese can

provide us with some guidance on where China’s dairy industry will go. The per

capita of Japanese is more than double of Chinese, and studies show its level of

lactose intolerance is not significantly different in China.

1.7 1.9 1.9 1.8 1.8 1.92.6 2.8 2.6 3.0 2.7

3.6

4.9

7.3 7.7

11.3

13.3

14.6

13.112.713.5

16.2

0

2

4

6

8

10

12

14

16

18

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010

(kg)

1990-2000: 4.7% CAGR2000-2011: 17.8% CAGR

Melamine incident impacted the consumer confidence

Tue, 06 Nov 2012

China Dairy Sector

Page 6 of 66

Exhibit 3: Per capita consumption of dairy product (kg/year)

Source: China Dairy Yearbook, OP Research

Outlook

According to Euromonitor, China dairy industry is estimated to grow at a CAGR of

9% in 2011-2015E. We observed an 81% correlation between the Chinese dairy

market growth and the Chinese GDP per capita growth in 1998-2011. Thus, we

conclude that as a country becomes more developed, the people tend to beef up

dairy product intake as a part of their protein needs. Thanks to the product mix

shift to high-value-added categories, a 10% CAGR growth of China dairy industry

over the next 5 years is achievable.

119

107

9289

83

44 44

35

16

Holland Australia Canada EU USA Korea Argentina Japan China

Tue, 06 Nov 2012

China Dairy Sector

Page 7 of 66

Major players in this markets

Exhibit 4: comparison of key operating statistics for domestic dairy players listing in HK markets

Upstream: Raw milk Downstream Liquid Milk/Milk Beverage Downstream Milk Powder

Company China Modern Dairy Mengniu Dairy Yili Bright Dairy Biostime Yashili Feihe Beingmate

Logo

Year Established 2005 1999 1993 1952 1999 1983 1962 1999

Products Raw milk

Liquid Milk/

Ice Cream/

Others

Liquid Milk/

Ice Cream/

Others

Liquid Milk/

Others

Infant formula/

Probiotic

Supplements/

Others

Infant formula/

Nutrition products/

Others

Infant

formula/Nutrition

products/others

Infant

formula/Others

Brands Modern Farming Mengniu Yili Bright Biostime

BM Care

Yashil

Scient Feihe, Firmus Beingmate

Milk sources n.a. Domestic Domestic Mainly Domestic Imported Imported Domestic Mainly

Domestic

Major milk source locations n.a. Inner Mongolia Inner Mongolia Shanghai Europe New Zealand Heilongjiang Heilongjiang

Production Base Anhui/Heibei Mainly Inner Mongolia Mainly Inner Mongolia Shanghai Guangdong

Guangdong

Shanxi

Heilongjiang

Heilongjiang Hangzhou

Source: Company data, OP Research

Tue, 06 Nov 2012

China Dairy Sector

Page 8 of 66

Upstream: raw milk, the key of dairy industry

Impressive growth

Raw milk as the key raw material for the dairy industry, has grown dramatically in

the past 20 years, with total production up to 36.6mn tons in 2011 from 4mn tons

in 1986, representing a CAGR of 11%. China’s primary raw milk production

regions are located between the latitudes of 35 degree and 48 degree in Northern

China where the climate is temperate with a high level of sunshine, and the

environment is more conductive to dairy farming and provides higher quality feed.

Inner Mongolia and Heilongjiang total accounted for 40% of China raw milk

production in 2010, followed by Hebei and Shandong at 12% and 7%,

respectively. Dairy industry giants Mengniu and Yili both are mainly sourcing the

raw milk from Inner Mongolia.

Exhibit 5: Raw milk production in China, 1989-2011

Source: CEIC, OP Research

Exhibit 6: Raw milk production by region, 2010

Source: CEIC, OP Research

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

1989 1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011

1989-2011: 11% CAGR2000-2007: 23% CAGR

(th tons)

Beijing2%

Hebei12%

Shanxi2%

Inner mongolia25%

Helongjiang15%Shandong

7%

Shaanxi4%

Xinjiang4%

Others29%

Tue, 06 Nov 2012

China Dairy Sector

Page 9 of 66

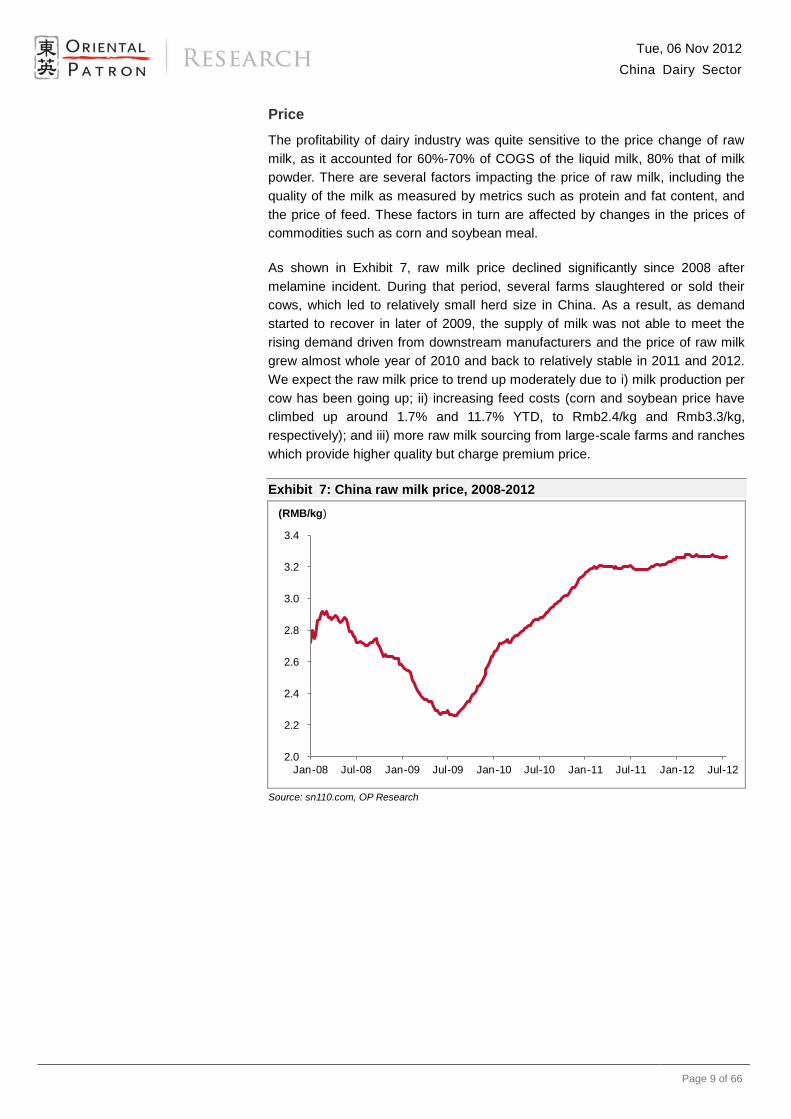

Price

The profitability of dairy industry was quite sensitive to the price change of raw

milk, as it accounted for 60%-70% of COGS of the liquid milk, 80% that of milk

powder. There are several factors impacting the price of raw milk, including the

quality of the milk as measured by metrics such as protein and fat content, and

the price of feed. These factors in turn are affected by changes in the prices of

commodities such as corn and soybean meal.

As shown in Exhibit 7, raw milk price declined significantly since 2008 after

melamine incident. During that period, several farms slaughtered or sold their

cows, which led to relatively small herd size in China. As a result, as demand

started to recover in later of 2009, the supply of milk was not able to meet the

rising demand driven from downstream manufacturers and the price of raw milk

grew almost whole year of 2010 and back to relatively stable in 2011 and 2012.

We expect the raw milk price to trend up moderately due to i) milk production per

cow has been going up; ii) increasing feed costs (corn and soybean price have

climbed up around 1.7% and 11.7% YTD, to Rmb2.4/kg and Rmb3.3/kg,

respectively); and iii) more raw milk sourcing from large-scale farms and ranches

which provide higher quality but charge premium price.

Exhibit 7: China raw milk price, 2008-2012

Source: sn110.com, OP Research

2.0

2.2

2.4

2.6

2.8

3.0

3.2

3.4

Jan-08 Jul-08 Jan-09 Jul-09 Jan-10 Jul-10 Jan-11 Jul-11 Jan-12 Jul-12

(RMB/kg)

Tue, 06 Nov 2012

China Dairy Sector

Page 10 of 66

Policy support

Generally speaking, China’s dairy farming market is still in an early stage and

highly fragmented, as only approximately 7% of dairy herds in China were reared

by large-scale dairy farms which own more than 1,000 cows in 2008 vs.46.9% in

the US. There is great potential for industry consolidation.

After the melamine milk scandal in 2008, the government pushed for

modernization and expansion in standardized large-scale dairy farms as well as

consolidation of the upstream dairy industry. The government has set a target to

reach~48mn tons of cow milk production and 15mn heads of dairy cows in 2013,

which represents 15%/2.1% CAGRs, according to the National Dairy Industry

Development Guideline (2009-2013) . The government has adopted both national

and regional policies to encourage the development of large scale farms by i)

issuing new set of policies to governing the dairy industry; ii) subsidies for

purchasing quality dairy cows from oversea; iii) allowing large-scale operators to

lease agriculture or forestry land; iv) exemptions on agricultural tax, VAT and

income tax.

Those industry’s early movers and large-scale dairy farms, like China Modern

Dairy (1117HK, BUY) will directly be benefited from the industry consolidation

pushed by government, in our view.

Exhibit 8: Milk supply market share by dairy farm size

Source: China Dairy Yearbook, OP Research

1-4 cows25%

5-19 cows32%

20-99 cows18%

100-1000 cows18%

>1000 cows

7%

Tue, 06 Nov 2012

China Dairy Sector

Page 11 of 66

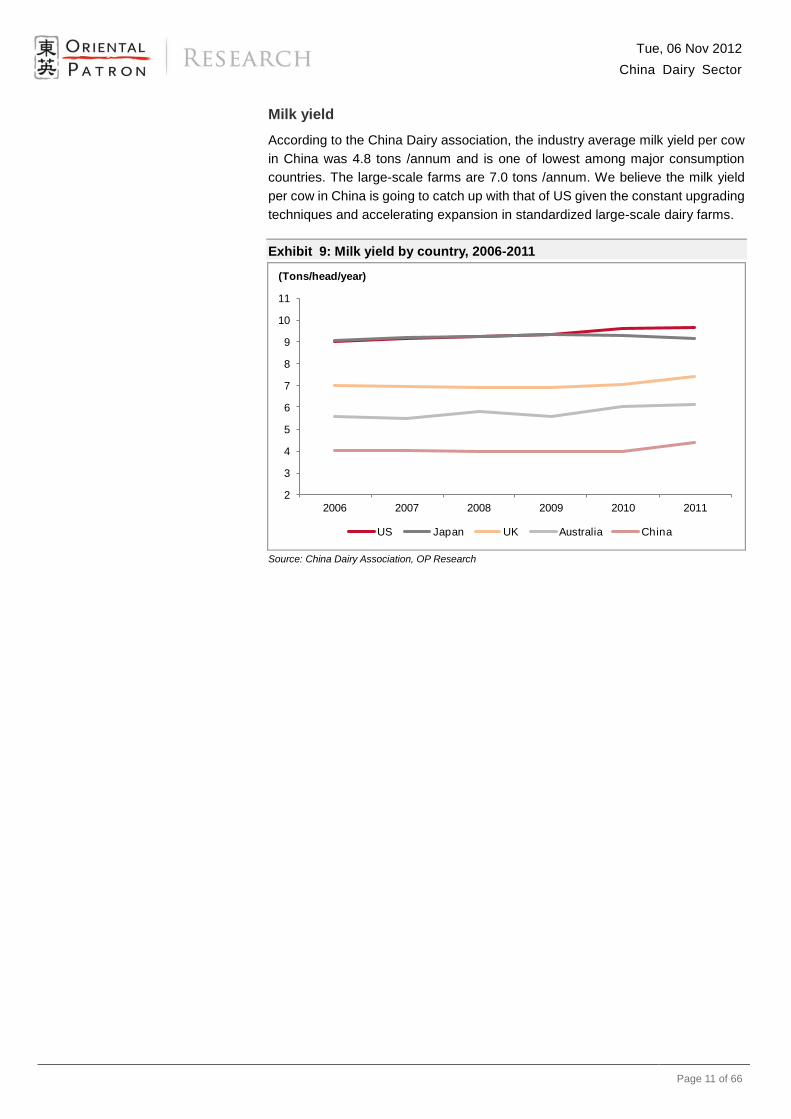

Milk yield

According to the China Dairy association, the industry average milk yield per cow

in China was 4.8 tons /annum and is one of lowest among major consumption

countries. The large-scale farms are 7.0 tons /annum. We believe the milk yield

per cow in China is going to catch up with that of US given the constant upgrading

techniques and accelerating expansion in standardized large-scale dairy farms.

Exhibit 9: Milk yield by country, 2006-2011

Source: China Dairy Association, OP Research

2

3

4

5

6

7

8

9

10

11

2006 2007 2008 2009 2010 2011

US Japan UK Australia China

(Tons/head/year)

Tue, 06 Nov 2012

China Dairy Sector

Page 12 of 66

Downstream: Liquid milk, biggest category

Liquid milk is composed of UHT milk, milk beverage, and yogurt, accounting for

largest portion of total dairy consumption (~80% in 2011).

Still the domestic brands’ market

After the melamine incident in 2008, unlike in the infant formula market, the

domestic brands recovered quickly in liquid milk market, where the foreign brands

were restricted by high transportation costs and have not successfully involved.

The domestic brands still dominate the liquid milk market in terms of sales. The

top three giants Mengniu, Yili and Bright Dairy with aggregate market share of

about 68% in China liquid milk market in 2011.

Shift to premium

We appreciate that the customers’ propensity to upgrade for high-end products

after 2008 melamine scandal. The market share of liquid milk priced above

RMB10/litre was ~24.7% in 2009 from 3.9% in 2005, according to China dairy

yearbook. The rapid consumption growth in the past years was mainly driven by

ASP increment and product mix improvement, in our view. We believe the

high-end liquid milk sales growth will outpace that of mid-to-low-end. Mengniu

(2319 HK, BUY), with 28% of revenue generated from high-end products, is one

of big beneficiaries of this trend.

Industry output slowdown?

Some investors may concern the slowing down of industry sales in 1H12. We

have to admit the domestic production volumes for liquid milk firstly recorded

negative figures for Jul and Aug since 2009. We believe the weak supply is partly

due to i) the hike feeding cost eroded profitability of smaller farms and force them

out of the industry; ii) a series of food safety incidents. However, we positively

detect that industry output rebounded to 13.1% yoy in Sep, according to Dairy

Association of China. We believe that resilience output is largely contributed from

the premium products as customer’s trade up.

Exhibit 10: Liquid milk production volume yoy % growth

Source: CEIC, OP Research

(40)

(20)

0

20

40

60

Feb-08 Aug-08 Feb-09 Aug-09 Feb-10 Aug-10 Feb-11 Aug-11 Feb-12 Aug-12

Tue, 06 Nov 2012

China Dairy Sector

Page 13 of 66

Value-added categories likely cut a figure

As we mentioned before that high prevalence of lactose intolerance is the key

bottleneck for liquid milk market growth, while high quality and value added milk

products supply (i.e. yogurt, low lactose milk, low fat milk) is like an antidote to the

genetic composition of Chinese people. Thus the products, like yogurt, flavored

milk and lactic Acid milk, will grow faster in our point of view.

According to Tetra Pak (the world’s leading food processing and packaging

solutions and suppliers with a 70.2% market share in China), China’s liquid dairy

product consumption is forecasted to rise by round 10.2% (CAGR) in 2011-2014E.

Lactic acid drinks, baby and toddler milk and flavored milk are expected to record

the fastest growth rates in 2011-2014E. Lactic acid drinks is expected to notch up

the highest growth rate, a CAGR of 11.9%, followed by baby and toddler milk with

a CAGR of 9.0%. Flavored milk is expected to record a CAGR of 4.8%. White

milk sales, the biggest category by volume, are expected to post a CAGR of 1.6%

in 2011-2014E.

Exhibit 11: Liquid dairy product sub categories growth

Source: Tetra Pak 2011, OP Research

1.3%

4.5%

9.5%

12.5%

4.5%

3.1%

1.9%

3.2%

2.7%

-0.6%

-5% 0% 5% 10% 15%

white Milk

Flavored Milk

Baby&Toddler Milk

Lactic Acid Drinks

Traditional Cultured Milk

Drinking Yoghurt

Liquid Cream

Sweetened Condensed Milk

Buttermilk

Evaporated Milk2008-2011 CAGR

1.6%

4.8%

9.0%

11.9%

4.1%

4.7%

1.4%

2.6%

4.5%

1.0%

0% 4% 8% 12% 16%

white Milk

Flavored Milk

Baby&Toddler Milk

Lactic Acid Drinks

Traditional Cultured Milk

Drinking Yoghurt

Liquid Cream

Sweetened Condensed Milk

Buttermilk

Evaporated Milk2011-2014E CAGR

Tue, 06 Nov 2012

China Dairy Sector

Page 14 of 66

Downstream: Infant formula, attractive growth prospect

Infant formula market of China experienced a 19% CAGR in the past 10 years,

supported by the urbanization of the Chinese population, the development of the

middle class and the increasing participation of women in the workforce.

Euromonitor forecasts the average market growth of 17% in 2010-2015 and

outpace the whole dairy market of China.

Atypical consumer behavior: low bargaining power among

consumers

The market for infant products is unique: parents are the buyers and the infants

are the consumers, thus the key decision maker is the buyer, not the consumer.

Quality, nutritional value and brand are the three most important considerations

when parents choose products for their children. A market survey conducted by

sina.com (SINA US, NR) indicated that 99% and 95% of parents care most about

quality and nutritional value of infant formula, while 89% also take into account

the brand. Unlike the other consumer goods, price is not a major consideration for

83% of the respondents. That means the bargaining power of consumers in the

infant formula market is relatively low, and we expect that the industry’s margins

are likely to remain solid or even improve.

Exhibit 12: Consumer considerations in purchase of infant formula, 2009

Source: Sina.com, OP Research

99%95%

89%

82%

75%

13%

3%

Quality Nutritional value

Brand Great taste Convenient to feed

Price Others

Tue, 06 Nov 2012

China Dairy Sector

Page 15 of 66

Growth by ASP hike, Foreign brands charge premium

The per capita consumption of infant formula climbed up by 18% in 2011 yoy,

largely driven by ASP increment. The ASP for domestic brand infant formula has

climbed up by 6.8% YTD, followed by foreign brand at 3.6%. As shown in Exhibit

13, its price no matter foreign or domestic kept low single-digit mom growth since

June 2009.

Exhibit 13: Milk powder ASP mom growth by category, 2009- 2011

Source: CEIC, OP Research

The 2008 melamine scandal led to a shift in market shares from local to foreign

brands and foreign brands are structurally more expensive than the domestic

producers at a 25%-35% premium as their perceived higher quality. We believe

improving awareness of food safety and high brand loyalty, in addition with

relatively low price sensitivity, are the key driving forces for sustainable upside

trend. Any growth in the high-end milk market will continue to be seized by foreign

brands due to better brand perceptions and quality raw milk source. Biostime,

Nestle (NESN VX, NR) and Mead Johnson (MJN US, NR) are all the likely

winners, in our view.

Exhibit 14: Milk powder Price by category and Price Premium, 2009- 2011

Source: CEIC, OP Research

-1%

0%

1%

2%

Jun-09 Dec-09 Jun-10 Dec-10 Jun-11 Dec-11 Jun-12

Domestic Brand Infant Formula Foreign Brand Infant Formula

100

150

200

250

May-09 Feb-10 Nov-10 Aug-11 May-12

Adult Milk Powder Foreign Brand Infant Formula

(RMB/kg)

42

46

50

54

May-09 Nov-09 May-10 Nov-10 May-11 Nov-11 May-12

(RMB/kg)

Tue, 06 Nov 2012

China Dairy Sector

Page 16 of 66

The 4th baby boom is happening in the PRC

According to a National Population Development Strategy report, women born

during the third baby boom (1982-1992) have entered their most active

childbearing years (20 to 29 years old). We forecast 2012E-2020E the number of

annual births in the range from 17 to 18.5mn (see Exhibit 15).

Exhibit 15: Birth rate, 1949 - 2011

Source: CEIC, OP Research

Relaxation of China’s one-child policy

After thirty-three years enforcement of the one-child policy, China’s birth rate has

gradually slowed down to around 1.19% in 2011 from 4.34% in 1963 (see

Exhibit15 gray line). Not only has the one-child policy led to a significant decline

in the population growth but it has also impacted by the pyramid of age structure

and the country sex ratio in less desirable ways. The ageing of the population,

4-2-1 family phenomenon and economic sluggish have led several experts to

consider abandonment the one-child policy. The Chinese authorities have taken a

cautious approach, launched several pilot programs and enforce new rules in

different provinces.

In the case of Chinese government could allow all couples to have two children in

2013 and 50% of women in most active childbearing years choose to have the

second child, we project 2012E-2020E number of annual births will increase to

22mn to 23mn based on our model.

0

5

10

15

20

25

30

35

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

1949 1952 1955 1958 1961 1964 1967 1970 1973 1976 1979 1982 1985 1988 1991 1994 1997 2000 2003 2006 2009

Annual Birth (LHR) Birth rate (RHS)

(%) (mn)2010-2020 The 4th

Baby Boom

1952-1957 The 1st

Baby

1962-1970 The 2nd

Baby

1982-1992The 3th

Baby Boom

Tue, 06 Nov 2012

China Dairy Sector

Page 17 of 66

Case study: China baby formula market

Without projecting the relaxation of China’s one-child policy, as shown in Exhibit

16, our rough calculation reveals that the infant formula market can reach

Rmb95bn in 2015 based on the assumptions of :1) low-single digit growth of ASP;

2) gradually increase in penetration rate; 3) the average consumption volume per

children under three years ago is 2-3.5 cans per month. One-child policy

relaxation’s assumption will further bring approximately Rmb28bn increment in

2015E to RMB123bn. On our conservative case projection, Chinese infant

formula market is to grow at a CAGR of 9% between 2012-2020E assuming no

change in one-child policy application, and that of 13% in the scenario with

relaxation of one-child policy.

Exhibit 16: China infant formula sales forecast-Scenario 1: One-child policy

2012E 2013E 2014E 2015E

Age (years) 1 2 3 1 2 3 1 2 3 1 2 3

Population 18 16 16 18 18 16 17 18 18 17 17 18

No. of cans consumption per month 3.50 2.50 2.00 3.50 2.50 2.00 3.50 2.50 2.00 3.50 2.50 2.00

Average ASP 144 144 144 153 153 153 162 162 162 170 170 170

Duration of consumption (months) 6 12 12 6 12 12 6 12 12 6 12 12

Penetration rate 35% 35% 35% 38% 38% 38% 41% 41% 41% 43% 43% 43%

Infant formula market value (mn) 63,095 76,150 88,854 95,263

Source: OP Research

Exhibit 17: China infant formula sales forecast-Scenario 2: Two-Children policy

2012E 2013E 2014E 2015E

Age (years) 1 2 3 1 2 3 1 2 3 1 2 3

Population 18 16 16 23 18 16 22 23 18 22 22 23

No. of cans consumption per month 3.50 2.50 2.00 3.50 2.50 2.00 3.50 2.50 2.00 3.50 2.50 2.00

Average ASP 144 144 144 153 153 153 162 162 162 170 170 170

Duration of consumption (months) 6 12 12 6 12 12 6 12 12 6 12 12

Penetration rate 35% 35% 35% 38% 38% 38% 41% 41% 41% 43% 43% 43%

Infant formula market value (mn) 63,095 82,669 106,716 123,842

Source: OP Research

Exhibit 18: China Infant formula sales forecast, 2012E- 2020E

Source: OP Research

50,000

70,000

90,000

110,000

130,000

150,000

170,000

2012E 2013E 2014E 2015E 2016E 2017E 2018E 2019E 2020E

Two-child policy One-child policy

(RMB mn)

Tue, 06 Nov 2012

China Dairy Sector

Page 18 of 66

Exhibit 19: Infant formula retail price of major brands in China market

Source: Walmart , Taobao.com, Watsons, OP Research

0

100

200

300

400

500

600

700

(RMB/900g)

Tue, 06 Nov 2012

China Dairy Sector

Page 19 of 66

China Modern Dairy (1117 HK) – Enjoy the taste of High Growth

We see strong total revenue growth prospects ahead; total revenue could maintain a CAGR of 42% from FY12-FY15E.

CMD will continue benefits from the policy of exemption on agricultural tax.

The company’s cash can catch up with CAPEX and generate positive free cash flow in FY14.

China modern dairy (CMD) is largest large-scale modern farm operator in China,

with 20 scalable farms and 159,347 dairy cows. Its duplicable business model

speeds up its expansion pace and target to 27 by FY15E with 240,000 cows. Its

high capital intensive and long-term pay-back business model creates a high

entry barrier for new rivals.

The advanced breeding, feeding and herd management techniques enable CMD

to produce the high-quality raw milk. And the price commands a high double digit

premium over the industry average level. To ensure the quality of raw milk, CMD’s

farms are strategically located closed to downstream milk processing plants.

CMD targets the milk yield per milkable cow is at about 9.0 tons/annum in FY15E

and 9.4 in FY17E, ultimately up to 10 tons/annum, driven by increasing proportion

of mature cows and genetic improvement. Continuing improvement in milk yield

will further boost the production volume growth, in our view. Thanks to its

economies of scale, cash cost of raw milk per ton declined by 7.24% in FY12

despite of surging commodities’ price.

A 10-year off-take agreement with Mengniu is mutually beneficial for both parties,

in our view. Sales to Mengniu accounted for 96.4% of its total sales in FY12, and

represented 12% of Mengniu’s raw milk demand.

Initial BUY. We forecast CMD could enjoy the net profit growth at a CAGR of 34%

for FY12-FY15E. Based on a blending DCF/PEG model, we estimate a fair value

of HK$2.64 per share, which implies 30.7% potential upside. We give a BUY

rating.

Initial Coverage

BUY

Close price: HK$2.02

Target Price: HK$2.64 (+30.7%)

Key Data

HKEx code 1117

12 Months High (HK$) 2.45

12 Month Low (HK$) 1.51

3M Avg Dail Vol. (mn) 3.33

Issue Share (mn) 4,800.00

Market Cap (HK$mn) 9,696.00

Fiscal Year 06/2012

Major shareholder (s) Advanced Dairy (24.01%)

Source: Company data, Bloomberg, OP Research Closing price are as of 5/11/2012

Price Chart

1mth 3mth 6mth

Absolute % 0.0 -4.3 -0.5

Rel. MSCI CHINA % -7.1 -13.8 -6.0

PE

Company Profi le Established in 2005, China modern dairy is

the largest modernized dairy farm operator

in China. It operated 20 scalable farms in

China with 159,347 dairy cows. Two more

new farms are under construction, planning

to reach a total of 27 by FY15E. Its milk

yield of 8.09 against the industry average of

4.8. Sales to Mengniu accounted for

96.4% of its total sales in FY12, and

represented 12% of Mengniu’s raw milk

demand.

Exhibit 20: Forecast and Valuation Year to Jun (RMB mn) FY10A FY11A FY12A FY13E FY14E

Revenue 590 1,113 1,678 2,685 3,832

Growth (%) 77% 89% 51% 60% 43%

Net Profit 107 225 398 541 732

Growth (%) 152% 109% 77% 36% 35%

Diluted EPS (RMB) 0.025 0.052 0.082 0.112 0.151

EPS growth (%) n.a. 103% 60% 36% 35%

Change to previous EPS (%) n.a. n.a. n.a. n.a. n.a.

Consensus EPS (RMB)

0.119 0.164

ROE (%) 7.5 4.8 7.9 9.7 11.5

P/E (x) 64.7 31.9 20.0 14.7 10.9

P/B (x) 4.8 1.5 1.6 1.4 1.3

Yield (%) 0.0 0.0 0.0 0.0 0.7

DPS (HK$) 0.000 0.000 0.000 0.000 0.015

Source: Bloomberg, OP Research

0.0

0.5

1.0

1.5

2.0

2.5

3.0

Nov/11 Feb/12 May/12 Aug/12

HK$1117 HK MSCI CHINA

0

10

20

30

40

50

60

Jan/11 Jul/11 Jan/12 Jul/12

Forward P/E Ratio

+1std.

avg.

-1std.

Tue, 06 Nov 2012

China Dairy Sector

Page 20 of 66

Investment thesis

The largest dairy farming company

As China largest large-scale modern farm operator, China modern dairy (CMD)

established in 2005 and has been recognized by the China Dairy Association as

the best-in-class dairy farm operator in China. It operated 20 scalable farms in

China with 159,347 dairy cows. Two more new farms are under construction,

planning to reach a total of 27 by FY15. According to the China Dairy yearbook,

the number of milkable cows was 14.4mn in 2011.By milkable cow size, China

Modern Dairy’s market share was only ~1%, despite its position the largest dairy

farm operator in China.

Exhibit 21: The top-four largest dairy farms in China

Company No. of farms No. of Dairy Cows No. of Milkable Cows

China Modern Dairy 20 159,347 70,793

Beijing Sanyuan Luhe Dairy Farming 25 45,000 23,000

Huishan 50 109,000 45,000

Shanghai Dairy Group 18 37,000 19,000

Source: Company data, OP Research

Standardized farm, speed up its expansion pace

CMD’s dairy farms are designed and constructed using a modern and scientific

layout to maximize yield and productivity, making the farms easily duplicable and

scalable to speed up its expansion pace. Thanks to its duplicable business model,

the number of farms of CMD has surged to 20 in FY12 from 3 in FY08, while the

number of cows is rapidly increasing from 24,358 in FY08 to 159,347 in FY12, a

CAGR of 60%. In FY13E, CMD plans to complete the construction of two farms

located in Bengbu farms (Anhui province), and targets to 27 by FY15E with

240,000 cows in total.

Exhibit 22: Number of cows and farms, FY08-FY12

Source: Company data, OP Research

14,964 20,427 26,607

46,267

70,793

9,394

23,532

45,584

61,309

88,554

3

6

11

16

20

0

5

10

15

20

25

10,000

50,000

90,000

130,000

170,000

FY08 FY09 FY10 FY11 FY12

No. of Milkable cows No. of Heifers and calves No. of farms

Tue, 06 Nov 2012

China Dairy Sector

Page 21 of 66

Exhibit 23: Layout of CMD’s standard dairy farm design

Source: Company data, OP Research

High entry barrier from capital intensive

Building up a large scale-farms is quite capital intensive, with around RMB300mn

capital expenditure comprising of RMB180mn for fixed asset investment and

RMB120mn for purchase 6000 heifers (RMB20,000/head). As the production of

raw milk will not commence in the first 2 years, thus a single farm will generate

positive free cash flow till third year based on our model. High capital investment

requirement and long-term pay-back time create a high entry barrier for new

rivals.

Exhibit 24: Free cash flow of a single large-scale farm

Source: Company data, OP Research

-400

-300

-200

-100

0

100

200

300

Year1 year2 Year3 Year4 Year5 Year6 Year7 Year8 Year9 Year10 Year11

Payback

Tue, 06 Nov 2012

China Dairy Sector

Page 22 of 66

Raw milk provider, premium quality oriented

Frequent quality scandals that happened in the past years have make consumers

more willing to pay for high-quality and health dairy products. Modern and

scientific practices and advanced breeding, feeding and herd management

techniques enable CMD to produce the high-quality and safe raw milk. Somatic

cell Count and Microbe Count are two of the major indicators used to determine

milk quality. As shown in Exhibit40, the quality of CMD’s raw milk is significantly

higher than China and EU standard, and higher than China’s other large scale

farms. Meanwhile, CMD’s protein and fat content of raw milk are 3.1% and 3.7%,

richer than China’s industry standards which are 2.8% and 3.1%, respectively.

Exhibit 25: Milk quality ratios comparison

China Modern

Dairy

Other large scale

farms in China

China

Standard

EU

Standard

Microbe Count <50k/ml N/A <=2,000k/ml <=100k/ml

Somatic Cell Count <300k/ml 592k/ml N/A <=400k/ml

Note: Generally a lower somatic cell count indicates better animal health, while a lower microbe plate count indicates improved sanitation.

Source: China Dairy Statistical Summary 2010

Unlike the individual farmers and small scale farms, CMD’s farms are strategically

located closed to downstream milk processing plants (1-3 hours transportation

time) and directly deliver to milk processor after the raw milk produced. This

“one-stop” procedure shortens the transportation process and reduces the risk of

contamination and product tampering, thus secures the quality of raw milk.

Exhibit 26: The pipeline of raw milk delivery

Source: Company data, OP Research

High quality combined with consumer’s low price sensitivity enables CMD to

charge a high double digit premium over the industry average price. We expect

the ASP hike 1% in FY13E-15E supporting by rising feed cost, in line with the

management guidance. Based on our sensitivity analysis, every 1% increase in

raw milk price could boost by 3.6% in net profit in FY13E (see exhibit 33).

Individual

farmers

Milk collation

stations

Intermediated

stationsTraders Agents Truck drivers Producers

China Modern

DairyProducers

VS.

Tue, 06 Nov 2012

China Dairy Sector

Page 23 of 66

Exhibit 27: Raw milk price(RMB/kg), 2008-2012

Source: sn110.com, Company data, OP Research

Higher milk yield

According to the China Dairy association, the industry average milk yield per cow

in China was 4.8 tons /annum and the average milk yield per cow for large-scale

farms was 7.0 tons/annum. Thanks to the continuous importing high quality

heifers and scientific breeding and feeding herd management, CMD’s average

milk yield per milkable cow achieved 8.09 tons/annum and the mature farms

average was 9.0 tons/annum in FY12. CMD targets the milk yield per milkable

cow is 9.0 tons/annum in FY15E and 9.4 in 2017E, ultimately up to 10

tons/annum, in the view of management. This is mainly driven by:

Heifers become milkable cows and increasing proportion of mature cows

(4-5 years old) with higher milk yield. According to the management, the

average age of CMD’s cows was around 3.5 years.

Genetic improvement and advanced herd upgrade the milk yield in the

subsequent lactation period. CMD imported its first generation Holstein

dairy heifers (>8tons/annum milk yield) from New Zealand and Australia,

and imported semen from high-quality bulls (born by the milkable cow with

15 tons/annum milk yield) from several international suppliers, to improve

the yield of the next few generations and ultimately to 10 tons/annum.

Continuing improvement in milk yield will further boost the production volume

growth, in our point of view.

2.0

2.5

3.0

3.5

4.0

4.5

2008 2009 2010 2011 2012

Industry average China Modern Dairy

Tue, 06 Nov 2012

China Dairy Sector

Page 24 of 66

Exhibit 28: Economics of a Dairy Farm: Milk yield

Source: Company data, OP Research

Exhibit 29: Average milk yield (tons/head/year), FY2008-FY2012

Source: Company data, OP Research

3

4

5

6

7

8

9

10

1 4

Breeding –

No Milk

Produced

Rapid Yield

Improvement

–Cows

Maturing

Gradual Yield

Improvement –

Improvements in

Herd Quality,

Feed Mix etc.

Year

Milk Y

ield

(to

ns/a

nn

um

)

6.10

6.90

7.30 7.56

8.09

9.00

9.40

4.0

6.0

8.0

10.0

2008 2009 2010 2011 2012 2015E 2017E

Tue, 06 Nov 2012

China Dairy Sector

Page 25 of 66

Scale operation bring cost efficiency

The milk quality and yield are primarily determined by the nutritional composition

of the feed. Feed cost, as the largest and fixed expense, account for 88.3% of

farm operating expense in FY12. The cash cost of raw milk per ton declined by

7.24% from RMB3,190 in FY10 to RMB2,959 in FY12 despite of surging

commodities’ price, indicating CMD’s constant improvement in milk yield and

reduction on feed transportation.

Cost advantages also came from CMD’s economies of scale and market leading

position as well as good relationships with the upstream suppliers, which lower

the purchase price for feed but can still guarantee the quality. CMD’s feeding

includes concentrates and forages. Concentrates, representing 60% of total feed

consumption, consist of corn, soybean meal, beer pulp and cotton meal; forages,

accounting for 40% of total feed consumption, consist of corn silage, sheep grass

and alfalfa. In order to ensure and improve the quality of raw milk, CMD

purchases concentrates from large national supplier, like Jilin COFCO (accounts

for 10% of concentrates), and sources forages from local farmers. CMD also plan

to improve the labor efficiency, the long-term target ratio of 60:1 dairy cows to

employees in the coming 5 years from 30:1 in FY2010.

Exhibit 30: Cash cost of raw milk per ton (RMB), FY2010-FY2012

Source: Company data, OP Research

We do not expect the cash cost of raw milk per ton to rise substantially over the

next three years, as i) CMD optimizes of the feed mix and uses cheaper

substitutes with a similar content; ii) the major raw material price of corn and

soybean (accounting for 36% of total feed cost) declined from the peak since mid

of 2012 and downward trend will continue, in our point of view. We estimate 5%

increment of the blended feed cost price in line with the trend of inflation. Our

sensitivity analysis reveals that CMD’s earnings are not highly affected by feed

cost fluctuations, and every 1% hike in feed costs price would lead to a 2.7% drop

in net profit (see exhibit 33).

3,190

2,841

2,959

2010 2011 2012

Cash cost= Farm operating

expense + labor cost

Tue, 06 Nov 2012

China Dairy Sector

Page 26 of 66

Exhibit 31: Feed cost constructure

Source: Company data, OP Research

Exhibit 32: Raw material price, 2011-2012

Source: Bloomberg, OP Research

10-year agreement, strategic partnership with Mengniu

In October 2008, CMD entered into a 10-year off-take agreement with Mengniu.

Under the agreement, both parties shall discuss annual procurement volume of

raw milk 3 months prior to each calendar year and mengniu is required to

purchase all raw milk production of CMD in the upcoming calendar year if the

parities fail to reach an agreed amount. This agreement also allows CMD to sell

up 30% of daily raw milk production to third parties, except for Inner Mongolia Yili

(600887 CH, NR) and Bright dairy (600597 CH, NR). The pricing of the raw milk

sold to Mengniu is determined by a formula, base price plus upward adjustment.

Base price refers to the price of Mengniu buys raw milk from other mid-to

large-scale dairy farms or, if no relevant comparison, use other comparable dairy

farms in nearby regions with adjustments. The upward adjustment depends on

certain quality standards.

Corn30%

Soybean meal6%

Alfalfa20%

Others 44%

2,000

2,500

3,000

3,500

4,000

4,500

Jan-09 Oct-09 Jul-10 Apr-11 Jan-12 Oct-12

(Soybean Meal (RMB/Ton))

1.0

1.5

2.0

2.5

3.0

Jan-09 Jul-09 Jan-10 Jul-10 Jan-11 Jul-11 Jan-12 Jul-12

(Corn (RMB/KG))

Tue, 06 Nov 2012

China Dairy Sector

Page 27 of 66

CMD’s strategic partnership with Mengniu is mutually beneficial for both parties,

in our view. Long-term partnership ensures CMD’s strong demand from market

leading player. For Mengniu, CMD’s high quality raw milk can reduce consumer’s

concerns about its product safety, especially for high-end products, i.e. deluxe

milk.

From FY08 to FY12, sales to Mengniu accounted for 98.9%, 99.6%, 97.6%, 97.4%

and 96.4% of CMD’s total sales, respectively. So far, CMD’s supply represented

12% of Mengniu’s raw milk demand from 10% in FY11.

Tue, 06 Nov 2012

China Dairy Sector

Page 28 of 66

Financial analysis

We forecast CMD could enjoy the net profit growth at a CAGR of 33% for

FY12-FY15E, corresponding to net profit of RMB541mn (or RMB0.11/share) for

2013E, RMB732mn (or RMB0.15/share) for 2014E, and RMB956mn (or

RMB0.20/share) for 2015E.

Key earnings drivers should come from i) top line growth boosted by strong

demand from downstream dairy operators for high quality raw milk as well as

10-year take off agreement with Mengniu to secure the long-term sales volume

growth and premium selling price; ii) operating leverage generates from its

modernization and scale operation; and iii) government policies supporting (i.e.

exemption on certain tax and subsidies) for the modernization of dairy farming.

We see strong total revenue growth prospects ahead, and total revenue could

maintain a CAGR of 42% from FY12-FY15E, driven by i) a 35% CAGR in raw milk

sales volume (led by a 5% CAGR in improvement of milk yield and the rest

generate from the increment of milkable cows; ii) a 1% CAGR of raw milk selling

price, tracking on the trend of feed price and strong consumption of high quality

milk products; iii) contribution from own brand products and selling excess cows

which are project to happen in FY15E on our model.

Our base case’s assumptions are 1% hike of ASP and 5% increase of feed cost.

The sensitivity analysis reveals that our net profit is not quite sensitive to the

change of feed cost and ASP. Assuming no change in feed cost, we estimate that

1% increase in ASP would boost the FY13E net profit by 3.6%. On the cost side,

we estimate that 1% increase in feed costs would drag down the net profit by 2.7%

in net profit of FY13E. We conclude CMD can improve its net profit margin if they

can adjust ASP in-line with change of feed cost.

Exhibit 33: Sensitivie Analysis of net profit change to change of Feed cost (%) and change of ASP (%)

Change of Feed cost (%)

2.3 3.0% 4.0% 5.0% 6.0% 7.0%

Change of ASP (%)

-1.0% -2.0% -4.6% -7.3% -9.9% -12.6%

0.0% 1.7% -1.0% -3.6% -6.3% -8.9%

1.0% 5.3% 2.7% 0.0% -2.7% -5.3%

2.0% 8.9% 6.3% 3.6% 1.0% -1.7%

3.0% 12.6% 9.9% 7.3% 4.6% 2.0%

4.0% 16.2% 13.6% 10.9% 8.2% 5.6%

Source: OP Research

The management expects the gain arising from changes in fair value less costs to

sell of dairy cows will decline to RMB70mn and RMB50mn in FY13/14E as fair

value changes will decrease with herd maturation. Meanwhile the cow

import-related government grants will slowdown as cow imports will cease. These

two items will drop down CMD’s operating profit margin and net profit margin in

FY13/14E.

We group the farm operating expenses, staff cost, depreciations and other

expenses as the operating expenses. The EBIT margin (excluding the non-cash

fair value of biological assets) is forecasted to be 19.4%, 19.5% and 19.6% in

FY13E, FY14E and FY15E, respectively, largely due to i) its economies of scale

further drop down the farm operating expenses, especially the cash cost of raw

Tue, 06 Nov 2012

China Dairy Sector

Page 29 of 66

milk per ton (commodity price increase is largely hedged by higher milk yield); ii)

staff cost ratio drops to 7.0% in FY13E, 6.9% in FY14E and 6.8% in FY15E on

operating leverage; iii) depreciation ratio accounts for 3.7%-5.3% of sales for

FY13E to FY15E.

Exhibit 34: Operating expense breakdown , FY13E

Source: Company data, OP Research

Income tax rate=0%

The Chinese government has implemented a plenty of policies to support the

development of large-scale dairy farms, including exemptions on agricultural tax,

VAT and income tax. The management expects CMD will continue benefits from

this tax policy, thus we expect the income tax expense to be equal to zero in our

model.

CAPEX

CMD is still in the stage of high growth, and large capital investment is required.

In FY13, CMD plans to complete the construction of two farms located in Bengbu

farms (Anhui province), and targets to have 180,000 cows from 159,347 in FY12,

11,000 of net increment would be imported. The management expects to be

self-sufficient in the supply of heifers by FY14E. We believe it is

achievable. Based on 15% organic cattle growth and 180,000 cows target base,

CMD can transfer excess heifers from mature farms to meet 6,000 cows per new

farm’s requirement. The excess cows could be sold to other dairy farms as

CMD’s another mid-term revenue contributor. By FY15E, CMD targets to lift up

the number of cows to 240,000 by expanding the size and utilization rate of the

existing farms, and the total number of farms will reach 27. The management

indicated that the capital expenditure (CAPEX) for building a large-scale dairy

farm with 10,000 dairy cows comprises is approximately RMB300mn, comprising

of RMB180mn for fixed asset investment and RMB120mn for purchase of heifers.

We forecast the annual CAPEX of RMB1.2bn, RMB0.9bn, and RMB0.8bn, for

FY13-FY15E, respectively. We believe the company’s cash can catch up with

CAPEX and generate positive free cash flow in FY14E, in line with management

guidance.

Feed costs

Other farm operating expenses

Employee benefits expense

Depreciation

Other expenses

Tue, 06 Nov 2012

China Dairy Sector

Page 30 of 66

Key risks

Line-up of famous brand, but strong reliance on this single customer.

Based on the 10 year off-take agreement, over 95% of CMD’s revenue is

contributed by its largest customer, Mengniu Dairy. CMD only has the

flexibility of selling no more than 30% of raw milk to other dairy processors

(excluding Yili and Bright Dairy) and directly to end-customers, which could

potentially hinder CMD’s ability to expand the customer base. The

management expects the sales to Mengniu will continue to represent a large

portion of its annual sales of milk produced in the future. CMD is directly

subjected to Mengniu’s operating risks.

Significantly reliance on one product, raw milk. Over 95% of revenue is

generated from raw milk. The management also anticipates the production of

raw milk will continue to be CMD’s primary business. Its sales volume is

highly dependent on and sensitive to fluctuation in raw milk production

volume and pricing.

Feed cost inflation. Feed cost accounted for 60.4% of total sales, and 88.3%

of total farm operating expense in FY12. Like most agricultural products, the

cost and supply of feed are largely subjected to market condition, which may

be affected by adverse weather conditions, various plant diseases, pests and

other acts of nature. The company may be unable to obtain sufficient

quantities of feed or purchase with high cost in unfavorable environment,

which will erode the margin.

Outbreak of any major diseases among cows The quality and healthy of

the dairy cows the important factors in production of raw milk. Any major

outbreak of any illness and disease (such as foot and mouth disease, bovine

tuberculosis) among cows could significantly impact on the raw milk

production capacity and volume. The company carries insurance to hedge

the losses related to cow diseases, will receive government compensation in

the event of an outbreak of a disease. However, it might be not sufficient to

cover all of the losses, including damage of the brand value and relation with

the upstream players.

Tue, 06 Nov 2012

China Dairy Sector

Page 31 of 66

Valuation

DCF Model

Given its cash flow-generative business nature and no direct listed peers for

comparison, we use DCF-based methodology to derive the 12-month target price

of HK$2.62for CMD. We use cost of equity of 10.2%, based on the assumptions

are:i) risk free rate of 3%; ii) market risk premium of 9%; iii) beta of 0.8 to reflect

its stock’s volatility relative to the Hang Seng Index; iv) 2% terminal growth rate

from 2023 onward, in line with our long-term growth assumption for China

consumer players.

We also conduct sensitivity analysis to quantify how target price changes in

different scenarios of cost of equity and terminal growth rate.

Exhibit 35: Sensitivity analysis of target price to Cost of Equity and Terminal growth rate assumption

Perpetual growth rate (%)

2.3 1.0% 1.5% 2.0% 2.5% 3.0%

Cost of Equity (%)

9.2% 2.84 2.98 3.14 3.33 3.55

9.7% 2.60 2.73 2.87 3.02 3.21

10.2% 2.40 2.50 2.62 2.76 2.91

10.7% 2.21 2.31 2.41 2.52 2.65

11.2% 2.05 2.13 2.22 2.31 2.42

11.7% 1.90 1.97 2.04 2.13 2.22

Source: OP Research

PEG Model

We also derive our 12-month target price of HK$2.67 from a PEG-based

methodology. The FY13 P/E multiple is 0.6x, based on a 25% discount to the

China dairy sector average on back of its unique business risk of strong reliance

on its single customer and high sensitivity to major diseases among cows.

Based on a blending DCF/PEG model, we estimate a fair value of HK$2.64 per

share, which implies 30.7% potential upside. We give a BUY rating.

Tue, 06 Nov 2012

China Dairy Sector

Page 32 of 66

Appendix

Company information

As of 30 June 2012, CMD operated 20 farms across China with 159,347 dairy

cows (70,793 milkable cows) producing 431,394 tonnes of raw milk annually. The

farms are located in the provinces of Anhui, Shandong, Hebei, Sichuan, Shaanxi,

Inner Mongolia, Heilongjiang, and Hubei. All of farms have a designed capacity of

10,000 dairy cows each and are strategically located within approximately 200

kilometers from Mengniu processing factories to ensure the quality and reduce

transportation expense.

Exhibit 36: China Modern Dairy farms distribution (As of 30 June 2012)

Source: Company data, OP Research

Shangzhi Farm

Tongliao Farm

Saibei Farm, I, II & III

Chabei Farm, I, II & III)

Wenshang Farm

Bengbu Farm III& IV

Maanshan Farm

Hengsheng Farm

Helingeer Farm

Baoji Farm I

Baoji Farm II

Hongya Farm

Bengbu Farm I&II

Feidong Farm I&II

TongshanFarm

Tue, 06 Nov 2012

China Dairy Sector

Page 33 of 66

Exhibit 37: Sales volume of raw milk, FY08-FY12

Source: Company data, OP Research

Exhibit 38: Shareholding Structure

#Jinmu owned by Ms.Gao Lina, Mr Sun yugang and other management

Source: Company data, OP Research

55,888

96,306

158,081

288,620

431,394

0

100,000

200,000

300,000

400,000

500,000

FY08 FY09 FY10 FY11 FY12

(tonne)

Yinmu15%

Xinmu15%

Advanced Dairy company

24%

Cystal Dairy Holdings (CDH)

8%

Jinmu5%

Public Shareholders

33%

Tue, 06 Nov 2012

China Dairy Sector

Page 34 of 66

Management profile

Mr. WOLHARDT Julian Juul (39) - Chairman, non-executive Director

He is currently a partner of KKR Asia Limited focusing on private equity

transactions in the Greater China region. He has been actively involved in

advising on investments Yageo Corporation (2327 TT), Tianrui Group Cement

Company limited and International Far Eastern Leasing Company limited since

he joined KKR Asia limited in 2006. Before joining KKR Asia limited, Mr. Wolhardt

was with Morgan Stanley Private Equity from 1998 to 2006. He is also a

non-executive director of Mengniu.

Mr. Deng Jiuqiang (61) - Founder, Executive director

He has more than 10 years experience in dairy industry and 15 years of

experience in dairy-related industries in China. He joined the Group in December

2006 and was appointed as an executive Director of the Company on 14

November 2008. Mr. Deng was a co-founder and former vice chairman of inner

Mongolia Mengniu Dairy (Group) Company Limited, a subsidiary of Mengniu from

August 1999 to May 2008. He has ceased to hold any positions with Mengniu

since May 2008. Mr. Deng was also the founder of Inner Mongolia Jiuqiang

Machinery Company Limited and has been its chairman since 1999.

Ms. Gao Lina (55) - Executive Director, CEO

Ms. Gao is one of the founders of the Group and has significant experience in

cross-border trading, resource integration and administrative management. Prior

to joining the Group, Ms. Gao was the general manager of Taian Foreign General

Trade Corporation between October 1993 to June 2005.

Mr. Han Chunlin (40) - Executive Director, COO

Mr. Han has more than 15 years of experience in food and beverage industry in

China and join the Group in September 2008. Mr. Han worked as the marketing

vice general manager of Nowara Shinnosuke (Fujian) Food industry Company

from February 2006 to July 2008. From January 1999 to September 2004, he

served at the liquid milk Department of Mengniu as marketing manager. Prior to

that, Mr Han was a branch-plant manager at Milk Powder Department of Inner

Mongolia Yili Industrial Group Company Limited from July 1994 to January 1999.

Company Milestone

Exhibit 39: China modern dairy milestone

2005-09 Commenced business under the name of “leading farming”

2006 First farm became operational in Maanshan, Anhui province.

2007-2008 New dairy farms in Hebei and Shandong provinces commenced operation

2008-07 Modern Farm was incorporated and acquired all the business and assets of Leading farming for RMB202mn

2008-11 First round of Equity Financing for purchases of heifers and as general working capital

2008-12 Second round of Equity Financing for purchase of heifers

2008-12 Acquisition of Helingeer Modern Farm in Inner Mongolia

2009-03 and 2009-06 Third and fourth rounds of Equity Financings for construction of dairy farms in Feidong

2009-2010 New dairy farms in Sichuan, Shanxi, Hubei, and Henglongjiang provinces commenced operation

2010-11 Listed on the Main Board of The Stock Exchange of Hong Kong Limited

Source: Company data, OP Research

Tue, 06 Nov 2012

China Dairy Sector

Page 35 of 66

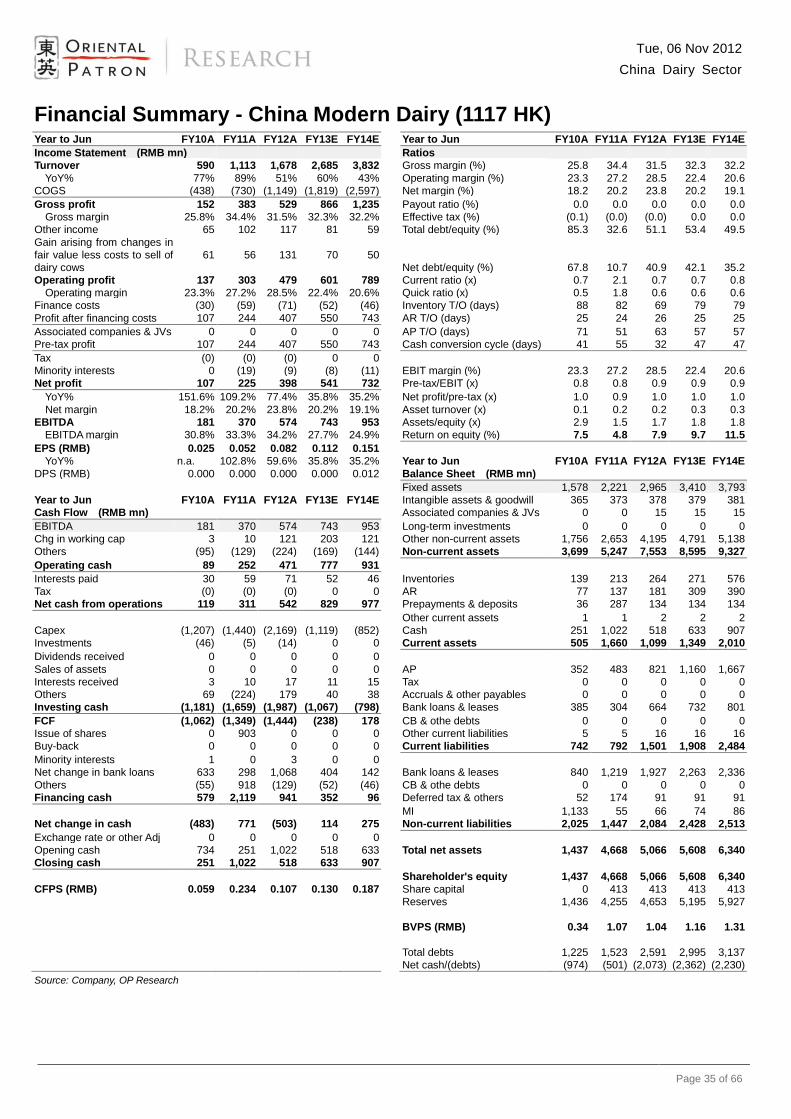

Financial Summary - China Modern Dairy (1117 HK) Year to Jun FY10A FY11A FY12A FY13E FY14E

Year to Jun FY10A FY11A FY12A FY13E FY14E

Income Statement (RMB mn)

Ratios

Turnover 590 1,113 1,678 2,685 3,832

Gross margin (%) 25.8 34.4 31.5 32.3 32.2

YoY% 77% 89% 51% 60% 43%

Operating margin (%) 23.3 27.2 28.5 22.4 20.6

COGS (438) (730) (1,149) (1,819) (2,597)

Net margin (%) 18.2 20.2 23.8 20.2 19.1

Gross profit 152 383 529 866 1,235

Payout ratio (%) 0.0 0.0 0.0 0.0 0.0

Gross margin 25.8% 34.4% 31.5% 32.3% 32.2%

Effective tax (%) (0.1) (0.0) (0.0) 0.0 0.0

Other income 65 102 117 81 59

Total debt/equity (%) 85.3 32.6 51.1 53.4 49.5

Gain arising from changes in

fair value less costs to sell of

dairy cows

61 56 131 70 50

Net debt/equity (%) 67.8 10.7 40.9 42.1 35.2

Operating profit 137 303 479 601 789

Current ratio (x) 0.7 2.1 0.7 0.7 0.8

Operating margin 23.3% 27.2% 28.5% 22.4% 20.6%

Quick ratio (x) 0.5 1.8 0.6 0.6 0.6

Finance costs (30) (59) (71) (52) (46)

Inventory T/O (days) 88 82 69 79 79

Profit after financing costs 107 244 407 550 743

AR T/O (days) 25 24 26 25 25

Associated companies & JVs 0 0 0 0 0

AP T/O (days) 71 51 63 57 57

Pre-tax profit 107 244 407 550 743

Cash conversion cycle (days) 41 55 32 47 47

Tax (0) (0) (0) 0 0 Minority interests 0 (19) (9) (8) (11)

EBIT margin (%) 23.3 27.2 28.5 22.4 20.6

Net profit 107 225 398 541 732

Pre-tax/EBIT (x) 0.8 0.8 0.9 0.9 0.9

YoY% 151.6% 109.2% 77.4% 35.8% 35.2%

Net profit/pre-tax (x) 1.0 0.9 1.0 1.0 1.0

Net margin 18.2% 20.2% 23.8% 20.2% 19.1%

Asset turnover (x) 0.1 0.2 0.2 0.3 0.3

EBITDA 181 370 574 743 953

Assets/equity (x) 2.9 1.5 1.7 1.8 1.8

EBITDA margin 30.8% 33.3% 34.2% 27.7% 24.9%

Return on equity (%) 7.5 4.8 7.9 9.7 11.5

EPS (RMB) 0.025 0.052 0.082 0.112 0.151 YoY% n.a. 102.8% 59.6% 35.8% 35.2%

Year to Jun FY10A FY11A FY12A FY13E FY14E

DPS (RMB) 0.000 0.000 0.000 0.000 0.012

Balance Sheet (RMB mn)

Fixed assets 1,578 2,221 2,965 3,410 3,793

Year to Jun FY10A FY11A FY12A FY13E FY14E

Intangible assets & goodwill 365 373 378 379 381

Cash Flow (RMB mn)

Associated companies & JVs 0 0 15 15 15

EBITDA 181 370 574 743 953

Long-term investments 0 0 0 0 0

Chg in working cap 3 10 121 203 121

Other non-current assets 1,756 2,653 4,195 4,791 5,138

Others (95) (129) (224) (169) (144)

Non-current assets 3,699 5,247 7,553 8,595 9,327

Operating cash 89 252 471 777 931 Interests paid 30 59 71 52 46

Inventories 139 213 264 271 576

Tax (0) (0) (0) 0 0

AR 77 137 181 309 390

Net cash from operations 119 311 542 829 977

Prepayments & deposits 36 287 134 134 134

Other current assets 1 1 2 2 2

Capex (1,207) (1,440) (2,169) (1,119) (852)

Cash 251 1,022 518 633 907

Investments (46) (5) (14) 0 0

Current assets 505 1,660 1,099 1,349 2,010

Dividends received 0 0 0 0 0 Sales of assets 0 0 0 0 0

AP 352 483 821 1,160 1,667

Interests received 3 10 17 11 15

Tax 0 0 0 0 0

Others 69 (224) 179 40 38

Accruals & other payables 0 0 0 0 0

Investing cash (1,181) (1,659) (1,987) (1,067) (798)

Bank loans & leases 385 304 664 732 801

FCF (1,062) (1,349) (1,444) (238) 178

CB & othe debts 0 0 0 0 0

Issue of shares 0 903 0 0 0

Other current liabilities 5 5 16 16 16

Buy-back 0 0 0 0 0

Current liabilities 742 792 1,501 1,908 2,484

Minority interests 1 0 3 0 0 Net change in bank loans 633 298 1,068 404 142

Bank loans & leases 840 1,219 1,927 2,263 2,336

Others (55) 918 (129) (52) (46)

CB & othe debts 0 0 0 0 0

Financing cash 579 2,119 941 352 96

Deferred tax & others 52 174 91 91 91

MI 1,133 55 66 74 86

Net change in cash (483) 771 (503) 114 275

Non-current liabilities 2,025 1,447 2,084 2,428 2,513

Exchange rate or other Adj 0 0 0 0 0 Opening cash 734 251 1,022 518 633

Total net assets 1,437 4,668 5,066 5,608 6,340

Closing cash 251 1,022 518 633 907

Shareholder's equity 1,437 4,668 5,066 5,608 6,340

CFPS (RMB) 0.059 0.234 0.107 0.130 0.187

Share capital 0 413 413 413 413

Reserves 1,436 4,255 4,653 5,195 5,927

BVPS (RMB) 0.34 1.07 1.04 1.16 1.31

Total debts 1,225 1,523 2,591 2,995 3,137

Net cash/(debts) (974) (501) (2,073) (2,362) (2,230)

Source: Company, OP Research

Tue, 06 Nov 2012

China Dairy Sector

Page 36 of 66

Biostime International (1112 HK) - A premium story

The total revenue could maintain a CAGR of 31% from 2011-2014E

the blended gross profit margin further erode to 65.1%, 64.7% and 64.4% in 2012E- 2014E, largely due to the product mix changes

Selling & distribution expense ratio is projected to decline to around 32% in 2012E-2015E, driven by the effective cross selling marketing.

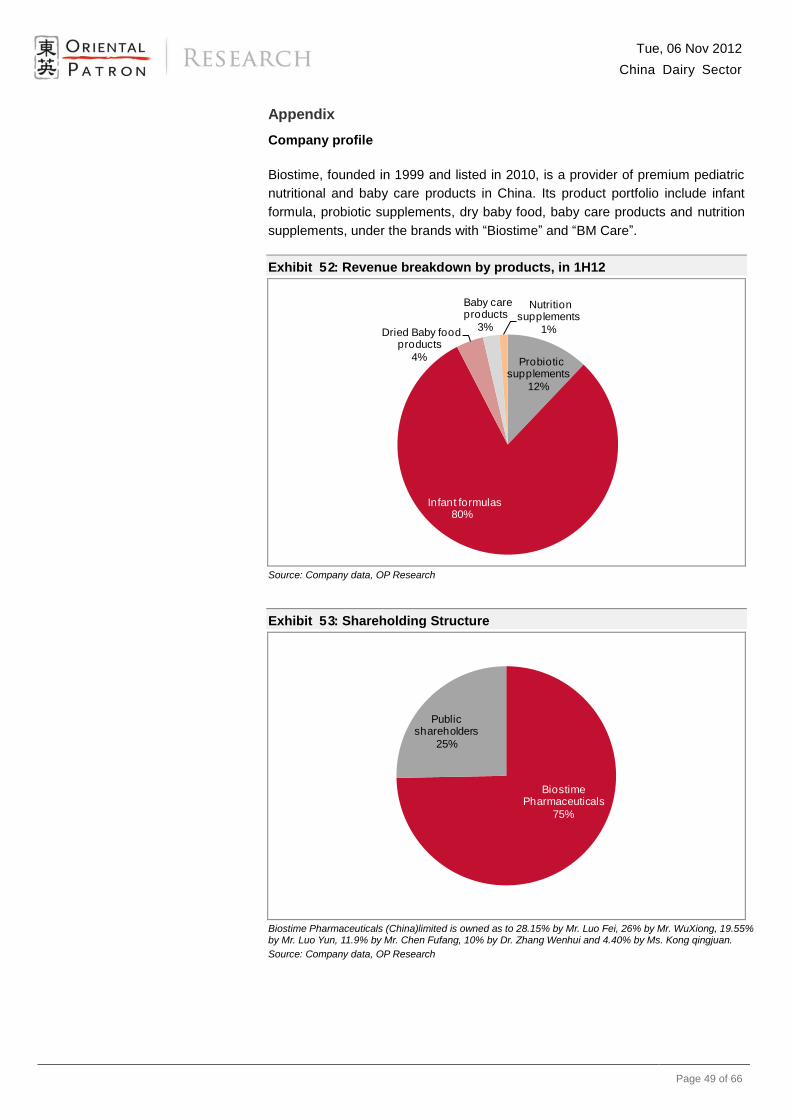

As a player in premium market, Biostime international (Biostime) is a provider

of premium pediatric nutritional and baby products in China, with 85% market

share in children probiotic supplement and 44% in that of supreme infant formula

market. Biostime was able to achieve superior margin over its peer average at 20%

over the past five years. As the fast growing segment, Infant formula has replaced

the probiotic supplement and become the largest revenue contributor, accounting

for over 80% of total revenue. All its products are sourcing from overseas to

guarantee quality and safety.

Its real time and effective channel management can monitor distributors’

inventory and sales level, leading to the account receivables turnover days at 1

day, while its POS machines can track sales information and consumer purchase

behavior. Its Mama 100 membership platform promoted strong consumer

loyalty, resulting in a rising cross selling and saving the expense of selling and

distribution each year. We believe Biostime can better grasp the market trend to

better prepare the orders through this effective channel management and Mama

100 membership.

Initial BUY with undemanding valuation We forecast Biostime could enjoy the

net profit growth at a CAGR of 24% for 2011-2014E. Key earnings drivers come

from top line growth boosted by infant formula segment and consequent

SG&A/sales ratio decline driven by effective cross selling marketing strategy. Our

TP is based on a blending SOTP/DCF model, we estimate a fair value of

HK$24.60 per share, which implies undemanding 2013E PE of 14.5x and

suggests 23.1% potential upside.

Initial Coverage

BUY

Close price: HK$19.98

Target Price: HK$24.60 (+23.1%)

Key Data

HKEx code 1112

12 Months High (HK$) 22.95

12 Month Low (HK$) 10.35

3M Avg Dail Vol. (mn) 0.67

Issue Share (mn) 602.29

Market Cap (HK$mn) 12,033.83

Fiscal Year 12/2011

Major shareholder (s) Biostime Pharm. (74.7%)

Source: Company data, Bloomberg, OP Research Closing price are as of 5/11/2012

Price Chart

1mth 3mth 6mth

Absolute % 3.3 8.9 -5.1

Rel. MSCI CHINA % -3.8 -0.6 -10.6

PE

Company Profi le Biostime international holdings Ltd. provides

pediatric nutrition and baby care products.

Their products include probiotic supplement

for children, infant formulas, dried baby food,

and nutritional supplements. The products

under the brand names “Biostime” and

“BMcare”.

Exhibit 40: Forecast and Valuation Year to Dec (RMB mn) FY10A FY11A FY12E FY13E FY14E

Revenue 1,234 2,189 3,078 4,024 4,924

Growth (%) 121% 77% 41% 31% 22%

Net Profit 266 527 644 824 1,000

Growth (%) 145% 98% 22% 28% 21%

Diluted EPS (RMB) 0.580 0.864 1.054 1.347 1.636

EPS growth (%) 142% 49% 22% 28% 21%

Change to previous EPS (%) n.a. n.a. n.a. n.a. n.a.

Consensus EPS (RMB)

1.100 1.385 1.650

ROE (%) 16.0 26.7 27.7 27.4 26.5

P/E (x) 27.9 18.7 15.3 12.0 9.9

P/B (x) 4.5 5.0 4.2 3.3 2.6

Yield (%) 1.4 3.8 2.7 3.4 4.1

DPS (HK$) 0.273 0.761 0.529 0.676 0.821

Source: Bloomberg, OP Research

0.0

5.0

10.0

15.0

20.0

25.0

Nov/11 Feb/12 May/12 Aug/12

HK$1112 HK MSCI CHINA

0

5

10

15

20

25

Feb/11 Aug/11 Feb/12 Aug/12

Forward P/E Ratio

+1std.

avg.

-1std.

Tue, 06 Nov 2012

China Dairy Sector

Page 37 of 66

Investment thesis

A player in premium market

Biostime international (Biostime), founded in 1999 and listed in 2010, is a

provider of premium pediatric nutritional and baby products in China. With 85%

market share in children probiotic supplement market, Biostime leveraged its

solid market position and started to expand its business to baby formula in July

2008 and baby care products in 1H10. Its blended gross profit margin is higher

than the peers approximately by 20%.

Exhibit 41: Gross profit margin comparison, 2007-2011

Source: Company data, OP Research

Infant formulas, the main catalyst

According to Nielson, Biostime has become the No.1 infant formula player in the

supreme tier segment (over Rmb300/can) with a market share of 44% in 1H11(vs.

32% in 1H10). In high-tier segment (RMB 200-300/can), Biostime have 7.4%

market share and ranked 6th

in 1H11. Infant formula, as the fast growing segment,

has replaced the probiotic supplement and became the largest revenue

contributor, accounting for 80.3% of total revenue with 65% gross profit margin in

1H12.

30%

40%

50%

60%

70%

80%

90%

2007 2008 2009 2010 2011

Biostime Yashili Feihe Beingmate

Tue, 06 Nov 2012

China Dairy Sector

Page 38 of 66

Exhibit 42: Infant formula industry in China in 1H11

Source: AC Nelson, OP Research

Under the 4-2-1 phenomenon, today’s China parents, especially the generation

born in 1980s, who exhibit relatively lower price sensitivity and higher value

awareness are willing to spend on premium products for their children. This

consumption preference shift was more visible in infant formula, especially after

the scandal happened on late 2008. As such, we estimate Biostime to maintain

fast growth momentum for revenue with 31% CAGR in 2012-2015E driven by i)

the 4th baby boom and potential one-child policy relaxation; ii) the effect from

“dragon baby” concept; iii) launching stage 4 infant formula by the year end of

2012.

Probiotic supplement, traditional and dominate the market

As Biostime’s traditional product, probiotic supplement was firstly launched in

China in 2001 and contributed approximately 12.6% of total revenue with 76.4%

gross profit margin in 1H12. According to Euromonitor, Biostime has a 85%

market share in children’s probiotic supplement sector in China in 2009. The

company soured probiotic from Lallemand, a leading bacteria producer in France,

and packed products in Guangzhou plant which has an annual capacity of 103mn

sachets with 84% utilization rate.

The revenue generated from probiotic supplements grew at a CAGR of 9% in

2008-2011. We expect the Biostime to maintain a relatively stable growth and

register a 7% CAGR of revenue in 2012-2015E driving from rising custom base of

mama 100 active members and conversion rate of member points.

Nestle1%

Wyeth9%

Beingmate19%

Ausnutria25%

Biostime44%

Others2%

Supreme tier

Mead Johnson,

27%

Dumex, 13%

Abbott, 11%

Wyeth, 11%

Beingmate, 10%

Biostime, 7%

Others, 21%

High tier

Tue, 06 Nov 2012

China Dairy Sector

Page 39 of 66

Real time and effective channel management

Biostime’s products are sold through 87 nationwide sales offices to connect the

371 regional distributors, which further place the products to 8,321 VIP baby

specialty stores (69.7% of products sold in 1H12), 3,336 supermarkets (23.1% of

products sold in 1H12) and 601 pharmacies with Mama 100 Member zone.

Biostime plans to further expand its distribution channels, aiming to cover 10,000

VIP baby specialty stores, 800 pharmacies with Mama100 Member’s Zones, and

4,000 supermarkets by the end of 2012.

All the end retailers have to sign contracts with Biostime and regional distributors

are only responsible for logistics and can only delivery products to the contractual

retail outlets. The company also requires the regional distributors to settle the

payment before delivering products, resulting in the account receivables turnover

days at 1 day in 1H12. Its real-time logistics management system can monitor

distributors’ inventory and sales level, while its POS machines, installed in their

retail outlets, can track sales information and consumer purchase behavior. We