daewoo international corporation material... · - automotive components - electronic industry -...

TRANSCRIPT

March 2010

DaewooInternationalCorporation

DisclaimerAll information in this presentation regarding the company’s financial result has been

prepared on unconsolidated basis, in accordance with Korean GAAP.

This presentation may contain forward-looking statements. Statements that are not

historical facts, including statements about our belief and expectations, are forward-

looking statements. Actual results may differ materially from those expressed or

implied by these forward-looking statements

ContentsContents

COMPANY PROFILEI

KEY ISSUES

EARNINGS & FINANCIAL POSITION IN 2009II

III

MYANMAR OFFSHORE GAS FIELDSIV

Part I.Part I. COMPANY PROFILECOMPANY PROFILE

CHRONOLOGY

ORGANIZATION & PERSONNEL

SHAREHOLDING STRUCTURE

BUSINESS STRUCTURE

VISION & STRATEGY

5

Completed workout program (Dec.2003)

Spun off from Daewoo Corp. (Dec.2000)

2000 ~ 2003

Discovery of Mya gas field in block A-3 Myanmar (Jan.2006)

Discovery of Shwe Phyugas field in block A-1 Myanmar (Mar.2005)

Discovery of Shwe gas field in block A-1 Myanmar (Jan.2004)

Sales W5t in 2004

Credit Rating in 2004 BBB-(KIS)

2004 ~ 2006

GSPA of 3 Myanmar gas fields (Dec.2008)

Sales W11t in 2008(ranked 20th in sales vol. in KOSPI)

Gas reserves certification-GCA (Aug.2007)

Creit Rating in 2007A(Korea Rating, KIS)

2007 ~ 2008

Credit Rating in 2009A+(NICE)

Declaration ofCommerciality forMyanmar gas fields (Nov.2009)

2009

Chronology

6

Trading Overseas Branches

Overseas Subsidiaries DomesticManagement

5 Groups

16 Sales divisions

56 Sales teams

55 Branches & Agents

13 Trading firms

27 Subsidiaries

15 Resource projects

Busan factory

Daewoo dept. store3 Divisions

14 Teams

1 TFT

INTERNATIONALINTERNATIONAL DOMESTICDOMESTICHQ (Seoul)HQ (Seoul)

497 Koreans: 240 Factory: 595

Dept. store: 240186

Overseas Employees

(January 2010)

Employees Employees Employees

Overseas Network : 110

Total Employees : 16,138

Locals: 14,377

Organization & Personnel

7

(December 2009)

Foreign Investors7,015,980 (7.2%)

KAMCO34,757,710 (35.5%)

Individuals14,498,194

(14.8%)Domestic Institutions

8,905,570 (9.1%)

ESOP473,007 (0.5%)

Shareholding Structure

8 Korean Financial Institutions (Korea EXIM Bank, KDB Asst Mgt, Korea Finance Corp, Woori Bank, others) 32,187,978 (32.9%)

Joint Disposal AssociationSignatories : KAMCO and8 Financial InstitutionsRestriction on independent selling (Stock dividend shares are not restricted : 1,629,588 shares)Number of Shares held : 66,945,688 (68.4%)

Total Shares Outstanding : 97,838,439Total Shares Outstanding : 97,838,439

8

Business Group 1- Hot Rolled Steel- Cold Rolled Steel- Special Steel

Business Group 2- Machinary & Plant- Automotive Components- Electronic Industry- Textile

Business Group 3- Steel Raw Materials- Non-ferrous Metal- Metal

ResourceDevelopment Group- Commodity- Mineral Resource

Development- E&P Operation- Energy Development

Sales (Wb)

▶ Export 5,963.4▶ Trilateral 4,757.7▶ Domestic 426.9

2009 Annual Revenue 11,148b 2009 Operating Profit 171b

Business Structure

Business Group 4- Chemical

9

Monetization ofMyanmar gas

Building-upcore competencies

Foundation for growth

World-class company(2013 ~ 2015)

2nd Take-off(2007 ~ 2012)

Diversification of business portfolio(Spin-off ~ 2006)

* Global holding company * Achieve AAA Credit rating* Strengthening operation based

on IB / M&A* Raising revenue fromenergy & resource development

* Myanmar gas field development* Increasing Investment in

energy & resource development* Adding higher value to business

through diversification

* Trading performance advances * Enterprise operation integrated* Integrated risk management system built up

Vision & Strategy

“FORBES TOP 500”

Part II.Part II. EARNINGS & FINANCIAL EARNINGS & FINANCIAL POSITION IN 2009POSITION IN 2009

EARNINGS RESULT

SALES BREAKDOWN

NON-OPERATING ITEMS

FINANCIAL POSITION

INVESTMENTS

BORROWINGS

FINANCIAL RATIOS

11

OperatingProfit(%)

20062006

77.71.22%

Sales 6,383.6

Pretax Profit(%)

154.42.42%

Net Profit(%)

112.81.77%

20072007

91.91.18%

7,816.1

128.91.65%

102.01.30%

20082008

156.31.42%

11,045.8

105.00.95%

88.00.80%

20092009

171.31.54%

11,148.0

178.91.60%

124.61.12%

Growth(YoY)

Growth(YoY)

9.60%

0.93%

70.27%

41.60%

(Wb)

Earnings Result

12

20062006

6,384

(Wb)

20072007

7,816

20082008

11,046

20092009

11,148

3,85160.3%

2,27935.7%

2544.0%

4,21854.0%

3,28642.0%

3124.0%

6,14155.6%

4,62541.9%

2802.5%

5,96353.5%

4,75842.7%

4273.8%

1,73327.1%

1,52623.9%

1,09217.1%

77112.1%

1,26219.8%

2,12427.2%

2,10426.9%

1,23615.8%

1,07613.8%

1,27616.3%

3,90735.4%

2,85225.8%

1,61514.6%

1,35412.3%

1,31811.9%

3,92535.2%

2,69224.1%

1,68415.1%

1,26611.4%

1,58114.2%

Sale

s Ty

peSa

les

Type

Sale

s It

emSa

les

Item

Export Trilateral trade Domestic

Steel & Metal Steel raw materialNon-ferrous metal

Chemical Commodities Others

Sales Breakdown

13

107.389.0 88.1

98.0

-49.5 -48.9

-73.2 -92.918.9

-3.1

-66.2

2.4

76.7 37.0 -51.3

Kyobo 86.4 95.3 44.4 135.0

Korea LNG 12.9 11.2 25.6 15.4

Other Equity Method Investments 8.0 -17.5 18.1 -52.4

Net Interest -7.0 -6.8 -3.1 -27.8

Loss on Disposal ofAccounts Receivable

-42.5 -42.1 -70.1 -65.1

Gain/Loss of FX 9.2 -21.8 -83.8 9.5

Other Non-Operating Gain/Loss 9.7 18.7 17.6 -7.1

Fina

ncia

l Co

stO

ther

Equi

ty M

etho

d

2006

2006 2007 2008 2009

7.52007 2008 2009

(Wb)

Non-Operating Items

14

Financial PositionFinancial Position

Total Assets

Total Liabilities

Equities

Non-current Liab.LT Debts

Current LiabilitiesST Debts

Non-current AssetsInvestments

20072006

2,164.11,928.8

1,175.81,019.0

988.3909.8

445.5161.7

336.8205.7

730.3128.1

682.233.4

1,387.31,146.9

1,127.9900.3

2008

2,675.3

1,604.8

1,070.5

473.9157.4

1,130.9282.2

1,628.71,386.6

1,046.4298.3

776.8274.1

800.9202.0

Current AssetsCash & ST Instruments

2009

3,885.2

2,495.5

1,389.7

1,045.9656.7

1,449.6154.6

2,127.81,835.2

1,757.4937.0

(Wb)

Financial Position

15

36.1

177.6

415.2

63.4

249.1

567.0

271.4

267.4

2007

900.3 1,146.9 1,386.6

2008 2009

1,835.2

120.3

458.8

850.0

406.1

74.5

389.8

538.0

384.3

Other Investments

E&P Investments

Kyobo Life Insurance

Other Equity Method Investments

2006

(Wb)

Investments

16

9.3

205.7

60.5

161.7

67.624.1 228.5

157.4

53.7

2006 2007 2008

• Straight Bonds issued in Feb. 2009 : W149.5 billion of book value as of Dec.31

• Convertible Bonds issued in Jul. 2009 : W356.0 billion of book value as of Dec.31

239.1 289.8

439.6

139.3

151.2

15.3

2009

811.3

505.5

Short-term Borrowings

Trade Finance

Long-term Borrowings

Bonds

(Wb)

Borrowings

17

Sales & Operating ProfitSales & Operating Profit

12t

10t

8t

6t

220b

180b

140b

100b

Sales (LHS)(CAGR: 20% )

Operating Profit (RHS)(CAGR: 30% )

W 6.4t

W 7.8t

W 11.0t W 11.1t

W 78bW 92b

W 156bW 173b

4t 60b2007 2008 20092006

Financial LeverageFinancial Leverage

200

150

100

50

80

60

40

20

Liability-to-Equity (LHS)

Borrowing-to-Equity(RHS)

112 119

150

179

26 29

41

58

0 02007 2008 20092006

10.0

ROE & ROAROE & ROA

15.0

7.5

5.0

2.5

0.0

10.0

12.5

6.0

4.0

2.0

0.0

8.0

ROE% (LHS)

ROA% (RHS)

12.9

10.7

8.5

10.56.2

5.0

3.6 3.9

2007 2008 20092006

P/E & P/BP/E & P/B

40.0

30.0

20.0

10.0

0.0

8.0

6.0

4.0

2.0

0.0

P/E (LHS)

P/B (RHS)

32.936.9

24.5 25.14.1

3.8

2.0 2.3

2007 2008 20092006

Financial Ratios

Part III.Part III. KEY ISSUES KEY ISSUES

KYOBO LIFE INSURANCE SHARES

E&P PORTFOLIO – GEOGRAPHICAL SPREAD

E&P ACTIVITIES (OIL & GAS)

E&P ACTIVITIES (MINERAL RESOURCES)

19

Condensed Financial Information

Kyobo Life Insurance Overview

Founded in 1958 CEO : C. J. Shin since 2000 (33.6% stake)Credit Rating :

Daewoo’s shares : 4.92 million shares→ Book value : W 850b(BPS W 172,758)

as of Dec. 31, 2009

Kyobo Life Insurance Shares

InsuranceFinancial Strength Rating

A2 Moody’s

AAA NICE

Subordinated Bond Credit Rating

AA+KISKorea Ratings

Kyobo Life Insurance Holdings(December 2009)

Kyobo Life Insurance Holdings(December 2009)

Shin Family 40.27 %

Daewoo Int’l 24.00 %

KAMCO 9.93 %

Korea EXIM 5.85 %

Others 19.95 %

TOTAL 100.00 %

Mar.2007 Mar.2008 Mar.2009 Dec.2009

Assets W42.5t W46.2t W50.0t W53.2t

Equities W1.7t W2.4t W2.9t W3.5t

Sales W12.2t W12.3t W12.7t W9.3t

N.Profit W289.3b W433.5b W291.6b W383.5b

Note) Sales and net profit of Dec. 2009 are presented for9 months ended Dec. 31, 2009

20

9 Oil & Gas Projects 6 Mineral Resource Projects

RUSSIARUSSIAWest Kamchatka

CANADACANADAKiggavik (uranium)

PERUPERU8 (oil)

MYANMARMYANMARA-1 (gas)

(Operator)

VIETNAMVIETNAM11-2 (gas)

MYANMARMYANMARA-3 (gas)

(Operator)

MYANMARMYANMARAD-7

(Operator)

OMANOMANKOLNG

MADAGASCARMADAGASCARAmbatovy (nickel)

UZBEKISTANUZBEKISTAN35 (Operator)UZBEKISTANUZBEKISTAN

36 (Operator)

E&P Portfolio - Geographical Spread

AUSTRALIAAUSTRALIAWhite Cliff (nickel)

BOLIVIABOLIVIACorocoro (copper)

AUSTRALIAAUSTRALIAMarree (uranium)

AUSTRALIAAUSTRALIANarrabri (coal)

21

E&P Activities (Oil & Gas)ProjectProject EquityEquity ReserveReserve History & StatusHistory & Status RemarksRemarks

Peru block 8(oil field) 11.7% 40 MM bbl - 1996: Participation (operator : Pluspetrol)

- Production: 15,000 bbl/day (crude oil)

- Earnings: US$ 9.6mm in 2009US$ 15.5mm in 2008 US$ 10.0mm in 2007

Oman KOLNG

(LNG plant)

20%(1% of OLNG) 14 TCF

- 1997: Participation (operator : Shell)- 2000: Production (dividend since 2002)- Annual capacity : 6.6mmMT

- Earnings: US$ 12.0mm in 2009US$ 23.2mm in 2008US$ 12.0mm in 2007

Vietnam offshore block 11-2(gas field)

4.9%(6.5% of KC)

0.9 TCF23 MM bbl

- 1992: Participation (operator : KNOC)- Dec 2006: commercial gas production- Production : 140mmscf/day (Gas)

4,100 bbl/day (Condensate)

- Earnings: US$ 2.2mm in 2009US$ 5.1mm in 2008US$ 3.4mm in 2007

Myanmar offshore block A-1(gas field)

51% (*Operator)

3.3 ~ 5.6TCF

- Jan 2004: Discovery of Shwe gas field- Mar 2005: Discovery of Shwe Phyu gas field- Aug 2006: Certification of reserves in Shwe &

Shwe-Phyu gas fields (from GCA)- Dec 2008: GSPA (CNUOC)

- EPCIC Contractor Selection &Declaration of Commercialityin Nov. 2009

- Gas Sales in 2013

Myanmar offshore block A-3(gas field)

51% (*Operator)

1.3 ~ 2.2TCF

- Jan 2006: Discovery of Mya gas field- Aug 2007: Certification of reserves in Mya

gas field (from GCA)- Dec 2008: GSPA (CNUOC)

- EPCIC Contractor Selection &Declaration of Commercialityin Nov. 2009

- Gas Sales in 2013

Myanmar offshore block AD-7

100% (*Operator) n/a

- Feb 2007: Signed Production sharing contract- 2007: 2D seismic acquisition & interpretation- 2008: 3D seismic survey

Uzbekistanblock 35 & 36

100% (*Operator) n/a

- Feb 2008: Signed Exploration Agreement - Satellite Image Analysis, Gravity & Magnetic Survey in 2009

Russia West Kamchatka

offshore block

4%(10% of KC) n/a

- Dec 2005: Participation (operator: Gazprom)- 2005~2007: 2D & 3D seismic acquisition &

interpretation - Jul 2008 : Drilled explanatory well

- Jul 09, operator replacement(Rosneft → Gazprom)

Note) “KC” : Korean Consortium, “TCF” : Trillion Cubic Feet, “KNOC” : Korea National Oil Corporation, “GCA” : Gaffney, Cline & Associates

ENER

GY

RES

OU

RC

ES

PRO

DU

CTI

ON

DEV

ELO

PMEN

TEX

PLO

RA

TIO

N

22

ProjectProject EquityEquity ReserveReserve RemarksRemarks

MadagascarAmbatovy

(nickel)

2.75% (10% of KC) 125 MM tons

- 2006: Participation - Operator: Sherritt (Canadian)- Parties: Sherritt 40%, Sumitomo 27.5%,

KC 27.5% (KORES 21%) - Production in 2010 (Production period : 27 years)- Annual Capacity : Nickel 60,000 MT, Cobalt 5,600 MT

AustraliaNarrabri

(coal)5.0% 230 MM tons

- Aug 2009: Participation- Operator : Whitehaven (Australian)- Parties : Whitehaven 70%, KORES 2.5%- Annual Capacity : 6 mm MT ( Production in 2010)

Canada Kiggavik(uranium)

1.7% 104 MM lbs

- 1983: Participation - Parties: AREVA (Canada) 64.8%, JCU Canada 33.5%- 1997: Completion of pre-feasibility study- 2005: Reorganize project team- 2006~2007: Conduct viability study- 2008~2011 : Environmental assessment study, F/S

AustraliaWhite Cliff

(nickel)

25%(50% of KC) n/a

- 2008: Participation - Parties: White Cliff Nickel 50% (Australian)

KC 50% (KORES 25%, DWIC 25%)- Exploration in progress

AustraliaMarree

(uranium)

10%(20% of KC) n/a

- 2008: Participation - Parties: Scimitar 50% (Australian)

KC 50% (KORES 20%, DWIC 10% , others)- Exploration in progress

BoliviaCorocoro(copper)

5%(11% of KC) n/a

- 2008: Participation - Parties: COMIBOL 55% (Bolivian)

KC 45% (KORES 23%, LS-Nikko 7%, others)- Exploration in progress

Note) “KC” : Korean Consortium / “KORES” : Korea Resources Corporation

E&P Activities (Mineral Resources)M

INER

AL

RES

OU

RC

ES

DEV

ELO

PMEN

TEX

PLO

RA

TIO

N

Part IV.Part IV. MYANMAR GAS FIELDSMYANMAR GAS FIELDS

MYANMAR OFFSHORE BLOCKS

MYANMAR GAS FIELDS

MILESTONE PLANS

DEVELOPMENT CONCEPT – OVERVIEW

GAS SALES & PURCHASE AGREEMENT (GSPA)

FINANCING PLAN

24

1. Project : Myanmar block A-1 (since Aug 2000) Area: 2,119 km2

Contract Type: Production sharing Ownership: Daewoo International 51% (Operator)

ONGC Videsh 17%, MOGE 15%, KOGAS 8.5%, GAIL 8.5%

2. Project : Myanmar block A-3 (since Feb 2004)

Area: 3,441 km2

Contract Type: Production sharing Ownership: Daewoo International 51% (Operator)

ONGC Videsh 17%, MOGE 15%, KOGAS 8.5%, GAIL 8.5%

3. Project : Myanmar block AD-7 (Feb 2007)

Area: 1,684 km2

Contract Type: Production sharing

Ownership: Daewoo International 100% (Operator)

Myanmar Offshore Blocks

25

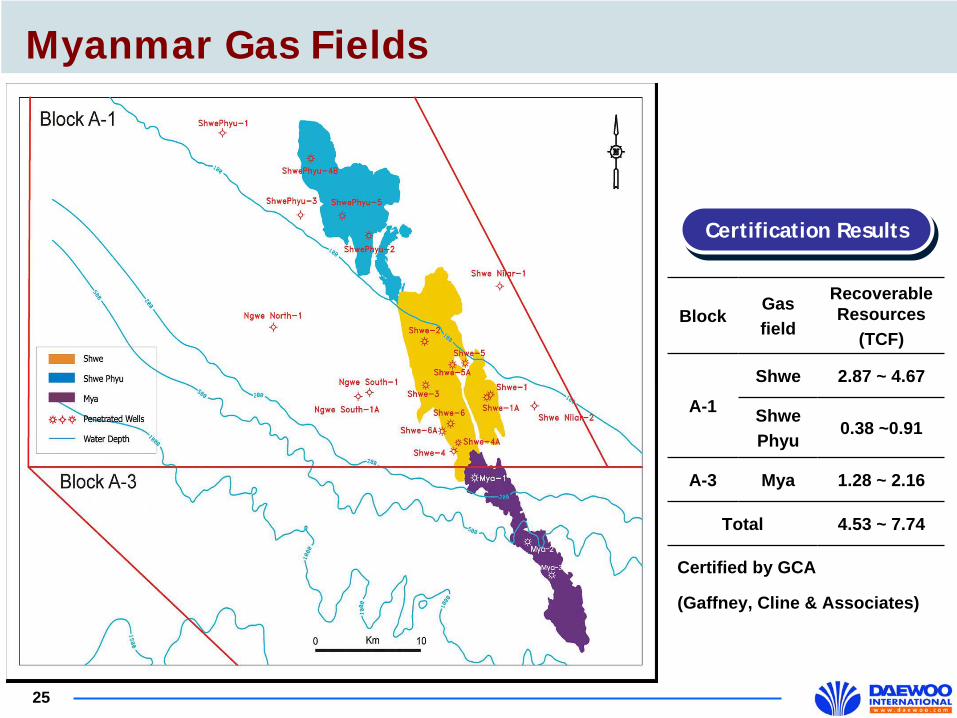

Myanmar Gas Fields

Certification ResultsCertification Results

BlockGasfield

Recoverable Resources

(TCF)

A-1

Shwe 2.87 ~ 4.67

ShwePhyu

0.38 ~0.91

A-3 Mya 1.28 ~ 2.16

Total 4.53 ~ 7.74

Certified by GCA

(Gaffney, Cline & Associates)

26

Gas Sales MOU

Jun.2008

GSPA

Dec.2008

Declaration of

Commerciality /

EPCIC contractor

Selection

Nov.2009

EPCIC Period

2009~2013

Initial Gas Supply

May 2013

Construction & Fabrication

Procurement

Detailed Engineering

Installation & Hook-up

Gas Supply

20092009 20102010 20112011 20122012 20132013

※ GSPA : Gas Sales & Purchase Agreement, EPCIC : Engineering, Procurement, Construction, Installation & CommissioningFDP : Field Development Plan

Milestone Plans

Gov.’t Approval

of FDP /

EPCIC Contract

Feb.2010

27

Development Concept - Overview

880k

m

Chinese Border

40”X

825

km

28

Signing DateSigning Date

• 24th December 2008

Contract PartiesContract Parties

• Seller : Daewoo International Corp./ONGC/MOGE/GAIL/KOGAS

• Buyer : China National United Oil Corporation

* Guaranteed by China National Petroleum Corporation

Main ContentsMain Contents

• The sales of natural gas produced in Blocks A-1/A-3 to CNUOCthrough pipeline for about 30 years

• Daily supply during the Plateau Period : 500 mmscf• Gas sales price : floating with oil price & price index

Gas Sales & Purchase Agreement (GSPA)

29

Financing Plan

Procuring corporate financing from foreign financial institutions

Credit risk will be covered by Overseas Investment Insurance

Upstream and Offshore MidstreamUpstream and Offshore Midstream

Daewoo’s CAPEX : US$ 1.7 b (including production platform, offshore pipeline and onshore pipeline)

Expected Pre-Production CAPEXExpected Pre-Production CAPEX

Financing Investment

Debt Service Gas Sales Revenue

Overseas InvestmentInsurance

DAEWOOINTERNATIONAL

Gas Fields

InsuranceCompany

Syndicated Loan

Lead Arranger(Security Package)

Thank you!