customer level exit analysis and lifetime value · customer level exit analysis and lifetime value...

TRANSCRIPT

Customer Level Exit Analysis and Lifetime Value

Caroline StevensonQuantium

Agenda

• Current view of portfolio value• Calculating the components• Customer lifetime value

• Start by determining expected cohort

Calculating Appraisal Value

Year

In Force Exits

New product sales

• Then overlay value, incorporating:– Current profitability– Assumed premium increases– Discount rates

Calculating Appraisal Value

Exit Analysis

• Traditional Modelling based on cohort level analysis– Broad understanding of effects– Separating concurrent drivers?

• Can improve on this with customer level analysis

Improving Exit Experience?Observed Exit Rate Experience by Calendar Year

70

75

80

85

90

95

100

105

110

2002 2003 2004 2005

Calendar Year

Rel

ativ

e Ex

it R

ate

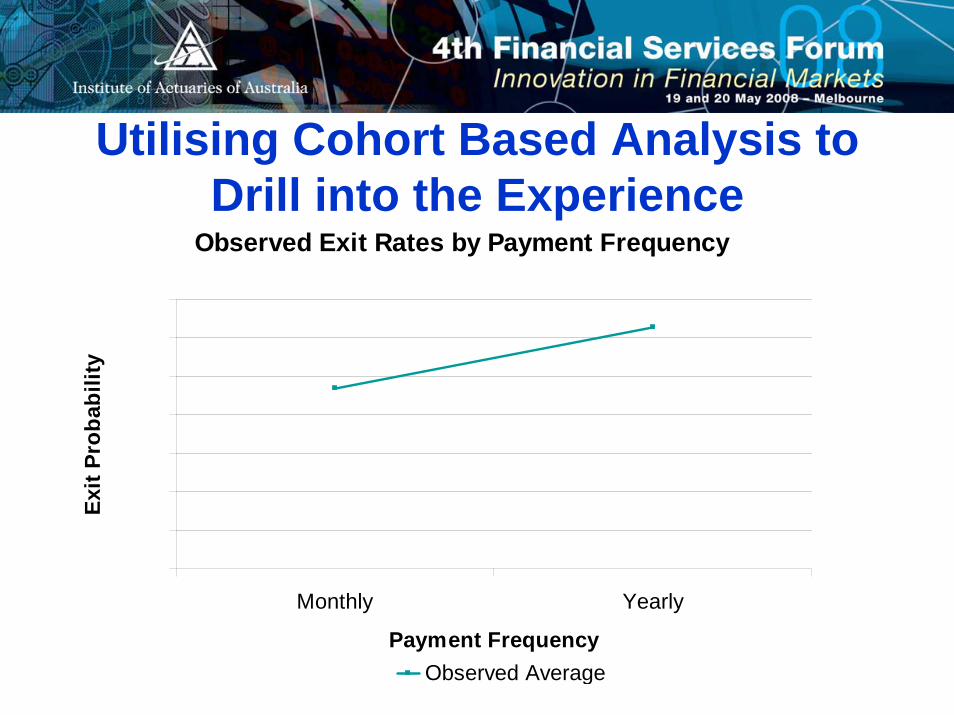

Utilising Cohort Based Analysis to Drill into the Experience

Observed Exit Rates by Payment Frequency

0%

2%

4%

6%

8%

10%

12%

14%

Monthly Yearly

Payment Frequency

Exit

Prob

abili

ty

Observed Average

Analyse how this varies over timeObserved Exit Rate Experience by Year and

Payment Frequency

0%

2%

4%

6%

8%

10%

12%

M YPayment Frequency

Exit

Prob

abili

ty

0%

20%

40%

60%

80%

100%

Prop

ortio

n

2003 2004 2005

RenewalLikelihood

Modelling Exit Experience

• Build GLMs at customer level

Customer Characteristics

OtherData

ProductDetails

PriceData

LapseModel

Relative Propensity to Exit by Payment Frequency

0

20

40

60

80

100

120

Monthly Yearly

Payment Frequency

Rel

ativ

e Pr

open

sity

to E

xit

Pure Effect of Payment Frequency

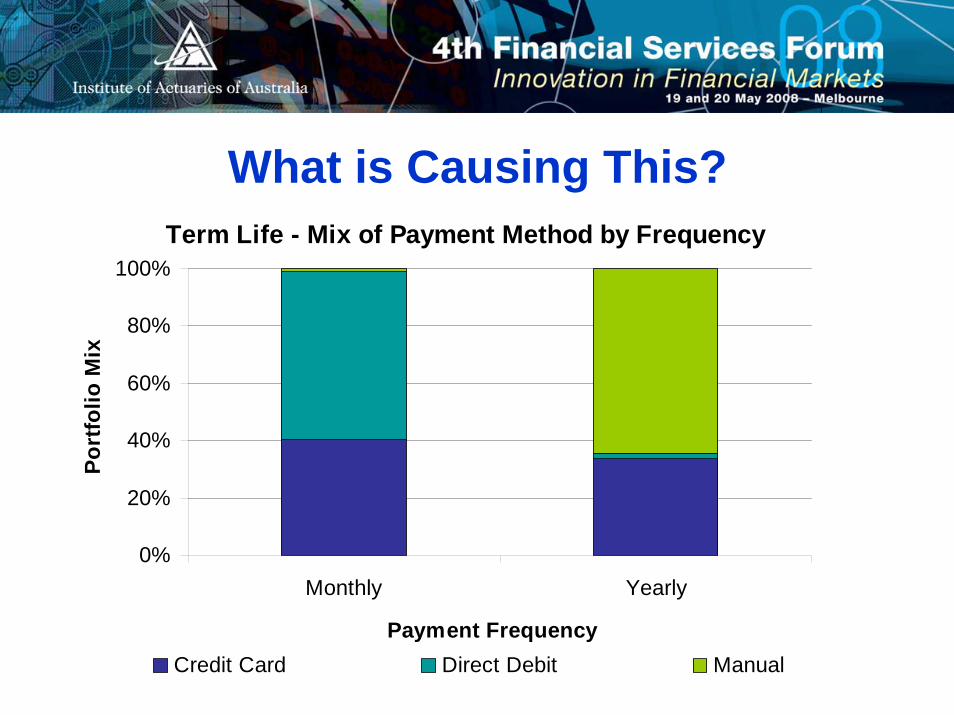

What is Causing This?Relative Propensity to Exit by Payment Method

0

50

100

150

200

250

300

350

Credit Card Direct Debit Manual

Payment Method

Rel

ativ

e Pr

open

sity

to E

xit

What is Causing This?Term Life - Mix of Payment Method by Frequency

0%

20%

40%

60%

80%

100%

Monthly Yearly

Payment Frequency

Port

folio

Mix

Credit Card Direct Debit Manual

We Predict Observed ExperienceObserved & Fitted Exit Rates by Payment

Frequency

0%2%4%6%8%

10%12%14%

Monthly Yearly

Payment Frequency

Exit

Prob

abili

ty

Observed Average Fitted Average

We Test Numerous Factors Sum Insured Tenure

Number of Risks Policyholder Age

$ Sum Insured Tenure in Months

AgeNumber of Risks

Rel

ativ

e la

pses

Rel

ativ

e la

pses

Rel

ativ

e la

pses

Rel

ativ

e la

pses

Relative Propensity to Exit by Calendar Year

80

85

90

95

100

105

110

2002 2003 2004 2005

Calendar Year

Rel

ativ

e Ex

it R

ate

Exit Experience was Deteriorating

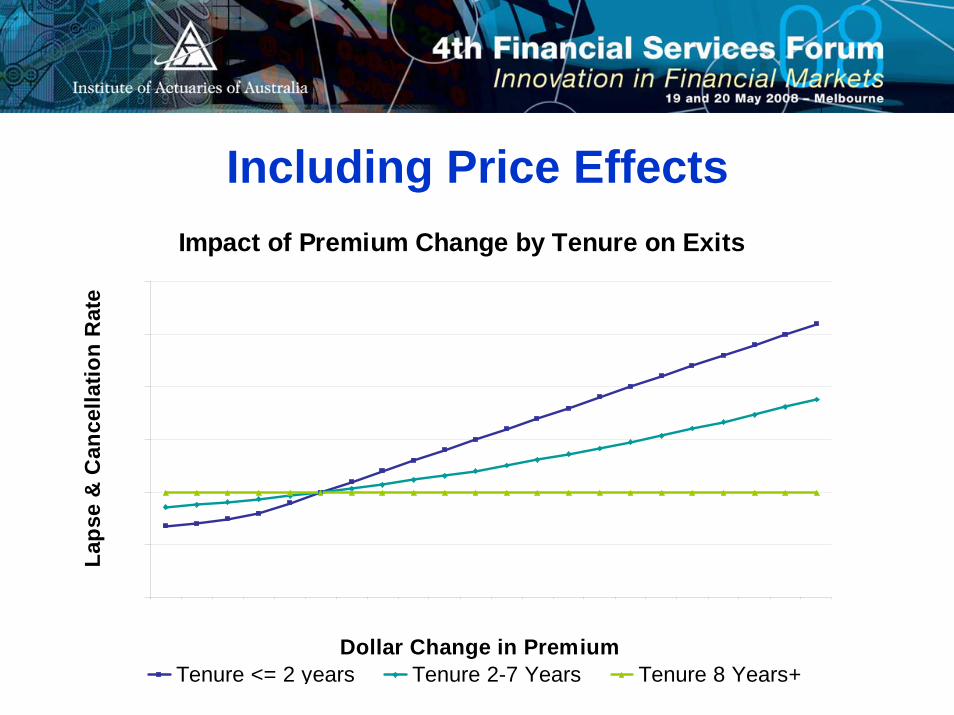

Impact of Premium Change by Tenure on Exits

80

90

100

110

120

130

140

<-50 10 60 150 1kDollar Change in Premium

Laps

e &

Can

cella

tion

Rat

e

Tenure <= 2 years Tenure 2-7 Years Tenure 8 Years+

Including Price Effects

Scenario testing tool

Improved Strategic Insights

• Detection of undistorted trends• Appraisal value calculations need to

incorporate appropriate trends in exit experience

• Targeted pricing action based on desired portfolio outcomes

• Product level v. Customer level view

Returning to Value Calculations

Year

Expected Value Exits

New product sales

Why a Customer Level View?

• Companies moving from product to customer/segment view

• Assess intrinsic value of, and hence justifiable investment in, different customer segments

Need to Consider Path for Each Customer

• At each point in time, consider product take-up/lapse

• Dynamically adjusting for customer characteristics

Credit Card

Credit Card

CC & TA

CC & TA

CC, TA & HL

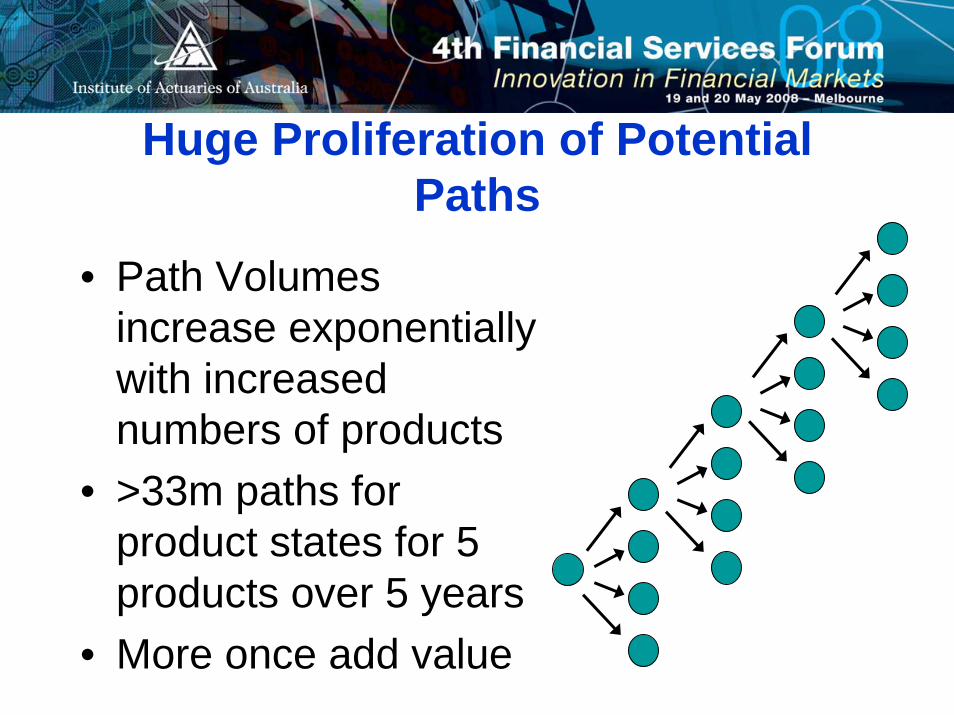

Huge Proliferation of Potential Paths

• Path Volumes increase exponentially with increased numbers of products

• >33m paths for product states for 5 products over 5 years

• More once add value

Other Products Important Even for Single Product View

Value from Transaction Account over Time

8

10

12

14

16

18

20

22

1 4 7 10 13 16 19 22 25 28 31 34 37 40 43 46 49Month

Expe

cted

val

ue

All Products Single Product View

Value from Three Products over Time

8

18

28

38

48

58

68

78

1 4 7 10 13 16 19 22 25 28 31 34 37 40 43 46 49Month

Expe

cted

val

ue

All Products Product 1 Product 2 Product 3

Potential Error at Customer Level

Customer Level

Shortfall

Need for Stochastic Approach

• Simple Markov Chain approaches only consider current state

• Necessary to track individual paths due to impact of factors such as product tenure

• Proliferation of paths lead to requirement for a simulation approach

Expected Portfolio Value

02468

10121416

2 2 2 2 2 2 2 2 2 2 2 2 2 2 2 2

Freq

uenc

y of

Occ

urre

nce

Understanding Portfolio Value

Deterministic mean Stochastic

mean

• Deterministic approaches can lead to incorrect conclusions, due to tenure effects

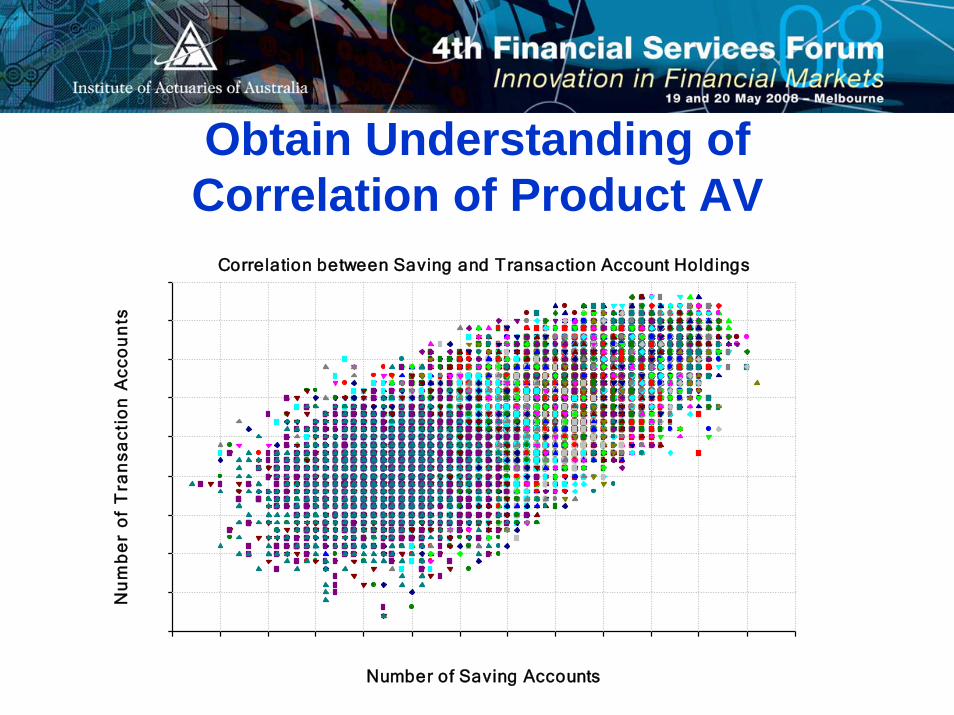

Obtain Understanding of Correlation of Product AV

Correlation between Saving and Transaction Account Holdings

30

35

40

45

50

55

60

65

70

75

85 90 95 100 105 110 115 120 125 130 135 140 145 150Number of Saving Accounts

Nu

mb

er

of

Tra

nsa

ctio

n A

cco

un

ts

Conclusions

• Cohort level analysis of AV components can lead to incorrect conclusions

• Single product view of value is flawed• Organisations moving to customer level

view• Need to adapt and go beyond current

AV approaches, drawing on customer level modelling and simulation