current management liability issues of interest to ... management liability issues of interest to...

TRANSCRIPT

Current Management Liability Issues of Interest to Community Bankers

Account Takeover, Allocation of Loss and Loss Prevention Strategies

April 8, 2015 12:00 – 1:00 p.m.

Table of Contents

Presentation Speaker Bios

John L. Bley, Foster Pepper PLLC Peter Marchel, Marchel & Associates Risk Consulting Yan Perng, Foster Pepper PLLC

Presented by:

Current Management Liability Issues of

Interest to Community Bankers

Account Takeover, Allocation of Loss and Loss Prevention Strategies

April 8, 2015

Presented by: John L. Bley, Foster Pepper PLLC Peter Marchel, Marchel and Associates Risk Consulting Yan Perng, Foster Pepper PLLC

Today’s Presentation Will Discuss

Account Takeover Laws Risk Mitigation Strategies Transferring Risk of an Account Take Over Event: Type and

Sufficiency

2

Disclaimer...

This presentation gives overviews and summaries of otherwise very complex and detailed banking laws and regulations.

Depending on the facts and circumstances of a particular matter, the statements in this presentation may or may not specifically apply.

The presenters and their companies make no express or implied warrantees regarding the accuracy of the information presented and directs the users of this information to seek advice from counsel of their choosing regarding any particular matter generally or specifically addressed by this presentation.

3

Overview of an Account Takeover event:

Bank receives a request via internet to execute a wire transfer on behalf of its customer.

Bank wires funds as directed. Customer contacts bank to notify them they did not authorize the wire

transfer.

4

Account Takeover Laws

5

General Rule: The Electronic Funds Transfer Act (for consumers) and Article 4A of the Uniform Commercial Code allocate the risk of loss for unauthorized wire transfers to the bank provided prompt notice is given to the bank.

Exception: On commercial wires the risk of loss can shift to the customer if the bank can show: A commercially reasonable security procedure is in place and The bank accepted a payment order in good faith and in compliance with the

security procedure.

UCC Section 4A-202 (RCW 62A.4-202)

6

Account Takeover Applicable Laws

Statutory law in Washington hasn’t changed substantively in decades Probably not an issue of amending the forms No silver bullet exculpatory language

7

Account Takeover Applicable Laws (cont.)

Standard for “Commercially Reasonable” Not the best available, just needs to be reasonable for the particular customer

and the particular bank. Patco Construction Co. v. People's United Bank, 684 F.3d 197 (1st Cir. 2012).

Deemed reasonable if: the security procedure was refused by the customer; and the customer expressly agreed in writing Choice Escrow & Land Title, LLC v.

BancorpSouth Bank, No. 13-1879 (8th Cir. June 11, 2014).

8

Account Takeover Applicable Laws (cont.)

FFIEC Pronouncement – Supplement to Authentication in an Internet Banking Environment, June 28, 2011

Knowing a “Commercially Reasonable Security Procedure” when I see it Difficult to avoid litigation in material cases since the parties will dispute the

commercial reasonableness of the security procedure A battle between experts

9

Account Takeover Applicable Laws (cont.)

Risk Mitigation Strategies

10

“Security Procedure” standard changes relative to the ongoing sophistication of the fraudsters System of layered security – Use of different controls at different points in the

transaction process so weakness in one control can be compensated for by the strength in a different control Dual customer authorizations Out-of-bank verification procedures “Positive pay” processes Debit locks Transaction value thresholds

Ongoing risk assessment to insure security procedures remain current

11

Risk Mitigation Strategies

Best practices Deposit agreements should reference security procedures (If not, your forms

are profoundly out-of-date) Communicate your security procedures in a constantly current brochure and

incorporate by reference the brochure in the deposit agreement or amended deposit agreement

Implement internal audit procedures to assure bank personnel are following security procedures

12

Risk Mitigation Strategies (cont.)

Risk Mitigation Strategies (cont.)

Best Practices Understand your customer’s needs and systems Monitor customer transactions and analyze and communicate with customer

regarding non-routine transactions Make sure your customer understands your security procedures If customer declines some of the security procedures

Inform the customer of the risks and get it in writing Assess the risks and decide whether or not to continue to serve the customer

13

Transferring Risk of an Account Take Over Event: Type and Sufficiency

14

Mandiant’s Mtrends 2015: A View From the Front Lines

Across the Cyber Threat Landscape Cyber threat actors are exploiting networks for an ever-widening array of economic and political objectives.

NUISANCE

DATA THEFT

CYBER CRIME

HACKTIVISM

DESTRUCTIVE ATTACK

Objective Access &

Propagation Economic,

Political Advantage

Financial Gain Defamation,

Press & Policy Disrupt

Operations Example

Botnets & Spam Advanced

Persistent Th t G

Credit Card Theft Website

Defacements

Delete Data

Targeted

Character Often Automated Persistent Frequently

Opportunistic

Conspicuous Conflict Driven

APT Phishing

78% of observed phishing emails were IT or security related, often attempting to impersonate the targeted company’s IT department or an anti-virus vendor

72% of phishing emails were sent on weekdays

Mon

Tue

Wed

Thur

Fri

Sat

Sun

Time from Earliest Evidence of Compromise to Discovery of Compromise

205 median number of days that threat groups were present on a victim’s network before detection

24 days less than 2013

Longest Presence: 2,982 days

How Compromises Are Being Detected

31%

victims discovered the breach internally

69% victims notified by an external entity

15

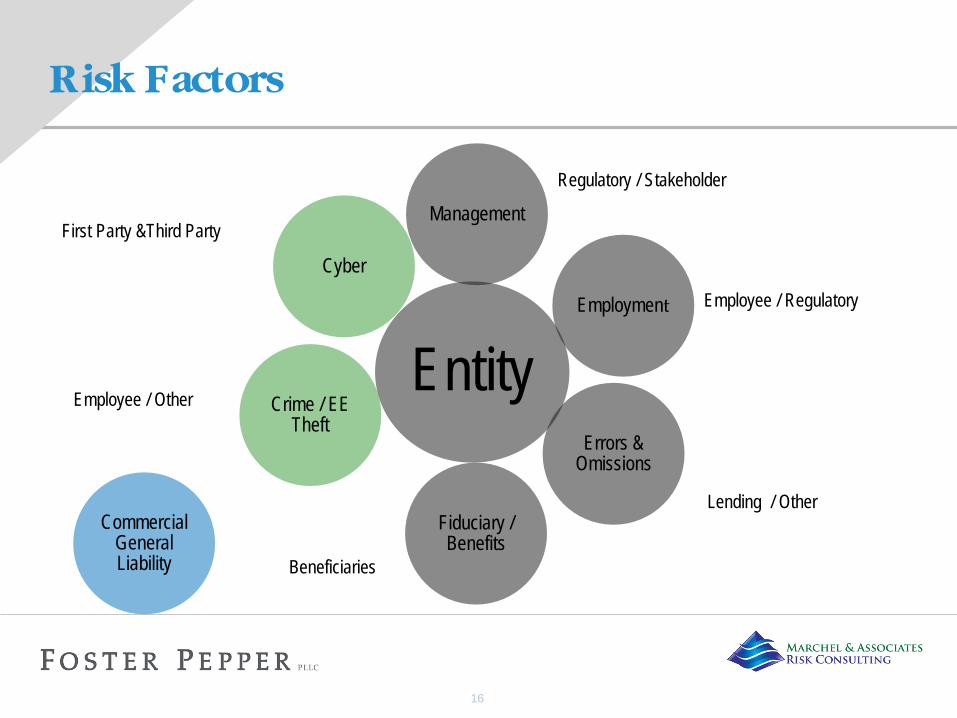

Risk Factors

Entity

Management

Employment

Crime / EE Theft

Fiduciary / Benefits

Errors & Omissions

Cyber

Commercial General Liability

Regulatory / Stakeholder

Employee / Regulatory

First Party &Third Party

Lending / Other

Beneficiaries

Employee / Other

16

Insurance Coverages

RECOGNIZE YOUR POLICY LIMITS AND HOW THEY WILL APPLY

Management Liability

Errors & Omissions (Bankers Professional Liability

Cyber Liability

Account Take Over

Crime Bond

17

Errors & Omissions (Bankers Professional Liability)

Protection for a company and its employees from claims alleging negligence in performing or failing to perform professional services offered to its customers.

No standard policy language - coverage will differ depending on insurance company.

18

Crime Bond

Employee Infidelity Premises Risk (loss or damage resulting from theft) Cash in Transit Forgery or Alteration (checks and securities) Counterfeit Currency Damage to Offices and Content

19

Cyber Loss Exposures

Insurance Company (Second Party)

First Party

Bank

-Damaged hardware, software and computer networks

-Comprised or Stolen data and cyber extortion -Business interruption and extra expenses -Post-breach expenses -Reputational damages

20

Insurance Company (Second Party)

Third Party Customer

Trading Partner Third party exposure

First Party Bank

Customer v. Trading Partner Invasion of privacy, breach of contract Network security E-mail liability Damage to 3rd party Libel network from data Slander breach trademark, copyright Could also implicate D&O and E&O

Liability

21

Cyber Loss Exposures

Cyber Liability – Access to Resources

Remediation expenses

Notification expenses

PR expenses

Fines & penalties

Third party

Experienced Advice

22

Data Breach Life Cycle

Access the Problem

• Discover breach • Contain losses,

secure area • Alert preparedness

team • Notify law

enforcement • Notify regulators

Engage External Resources

• Alert vendor • Call forensics team • Alert public

relations (internal or external)

Comply with Notification

• Draft and send

notification • Active call center • Public disclosure (if

appropriate)

Manage Ongoing Business

• Continue assuring

customers • Continue data

systems monitoring • Resume business

as usual

23

Placement of Risk – example 1

Bond • Employee Infidelity • Premises Risk (loss or

damage resulting from theft)

• Cash in Transit • Forgery or Alteration

(checks and securities) • Counterfeit Currency • Damage to Offices and

Content

Computer Crime Insurance Policy • eFraud • Computer Fraud

Services

Takeover Endorsement • Commercial Account • Retail Account

Cyber Policy • Privacy Breach (1st party) • Privacy (3rd party) • Digital Media Content (3rd party) • Cyber Extortion Event (1st party)

• First Party Insured Event

Endorsement • Business Interruption • First Party Expense

• Designated Defense Counsel

24

Placement of Risk – example 2

Bond • Computer Crime Rider • Email Initiated Funds

Transfer Fraud Rider • Electronic Funds Transfers

Rider

Computer Crime Rider • Computer Systems Fraud • Fraudulent Electronic

Programming • Voice Initiated Transfer Fraud • Telefacsimile Transfer Rider • Destruction of Data or

Programs by Hacker • Destruction of Data or

Programs by Virus

Cyber • Network and Information Security

Liability • Communications and Media Liability • Regulatory Defenses Expenses • Crisis Management Event Expenses • Business Interruption and Additional

Expenses

25

Placement of Risk – example 3

Bond • Computer Crime Rider • Email Initiated Funds Transfer

Fraud Rider • Electronic Funds Transfers Rider

Computer Crime Rider • Computer Systems Fraud • Fraudulent Electronic Programming • Voice Initiated Transfer Fraud • Telefacsimile Transfer Rider • Destruction of Data or Programs by

Hacker • Destruction of Data or Programs by

Virus

Cyber • Content Injury Liability • Privacy Injury Liability

• Privacy Injury Claims • Privacy Regulation Proceeding

• Network Security Liability • Public Relations Event Expense • Network Extortion • Loss of or Damage to Insured Entity’s

Network • Business Interruption and Extra Expense

26

Mitigating Cyber Expenses

Questions to Ask About Insurance: What are the right limits? How do I pick the right coverage / company? What happens when a claim occurs?

27

Factors When Considering Policy Limits

How many records does the bank have? Does the cyber policy have separate limits or are the limits shared

with other coverages (management liability, employment liability, professional liability)?

Size and location of the bank and its customers. Customer profile.

28

Key Takeaways

Implement an account takeover security procedure Conduct ongoing assessment

Risks Ability to mitigate risk

Know your customer’s risk profile and security procedures Make a security procedure brochure and incorporate it by reference

into your deposit agreement; updates to the brochure require signed acknowledgement from the customer

Waivers from your security procedure requirements should be in writing after informing the customer of the risk

29

Key Takeaways (cont.)

Know your insurance program. Know your limits. Review policy and limits annually. Know how to report a claim. Know how to interact with the insurance company.

30

Thank you!!

Make it a great 2015!

John L. Bley Yan Perng

FOSTER PEPPER PLLC 1111 Third Avenue, Suite 3400

Seattle, WA 98101-3299 Phone: 206-447-4400 [email protected] [email protected]

www.foster.com

Peter Marchel Marchel & Associates Risk Consulting

Phone: 425-788-4349 Mobile: 206-940-5992

Fax: 425-788-0263 [email protected]

www.Marchelassociates.com

31

SEATTLE T 206.447.8915

F 206.749.2115

SERVICES

Business Financial Institutions (Chair)

PRACTICE OVERVIEW John chairs the firm’s Financial Institutions practice and his practice includes regulatory intervention, regulatory compliance and enforcement prevention, regulatory relations, legislative relations, expert witness testimony, strategic planning, corporate governance, and mergers and acquisitions.

Regulatory Intervention. Represent financial institutions (banks and non-banks) before federal and state financial institutions regulators concerning pending or existing regulatory enforcement actions, these include either "safety and soundness" or "consumer compliance" actions. Services include (a) drafting responses to reports of examination, (b) negotiating the elements of cease and desist orders, (c) advising boards concerning implementation and compliance strategies with such orders, (d) negotiating civil money penalty and license revocation orders, (e) devising management work plans and other strategies designed to satisfy and lift regulatory orders.

Regulatory Compliance and Enforcement Prevention. Practice is similar to "Regulatory Intervention" except it is preventative in nature. Work with management and boards to identify and correct safety and soundness or compliance issues before such issues become subject to enforcement actions. Such issues include but are not limited to compliance strategies with numerous pronouncements on (i) safety and soundness matters such as lending limits rules, credit quality policies, loan portfolio risk management pronouncements and anti-money laundering laws and rules and (ii) consumer compliance matters, primarily in the residential and consumer lending area, including laws dealing with truth-in-lending, truth-in-savings, RESPA, safekeeping of customer information, sharing of customer information, and applicable state consumer protection laws and licensing regimes such as the Washington Mortgage Broker Practices Act and the Consumer Loan Act.

Regulatory Relations. Assist management with regulatory approvals for new banks, bank holding companies, trust administration, non-depository operating subsidiaries, sub-chapter S conversions and other such activities. Assist financial institutions and their trade associations influence the administrative rulemaking process.

Legislative Relations. Assist clients and their trade associations draft bills and devise advocacy strategies concerning proposed legislation before state and federal legislative bodies.

John L. Bley MEMBER

1

John L. Bley MEMBER

SEATTLE T 206.447.8915 F 206.749.2115 [email protected]

Expert Witness Testimony. Provide consulting and testimony services as an expert witness in the areas of predatory lending, corporate governance, audit committee best practices and internal audit, securities fraud, FINRA arbitrations, state and federal regulatory safety and soundness enforcement processes and consumer compliance enforcement processes.

Strategic Planning. Facilitate board and/or management strategic planning initiatives for bank or commercial enterprises. Such processes are tailored to the needs and desires of the client but can include (a) devising, implementing, and analyzing board questionnaires (b) interviewing board members and members of the CEO's direct reports to determine board and management's view of the strengths, weakness, opportunities and threats confronting the organization, (c) facilitating board and/or management strategic planning sessions, tailored to the scope and needs of the client, (d) working with management and the board to implement "Strategic Action Plans" to facilitate implementation of the strategic strategies identified during the strategic planning sessions.

Corporate Governance. Advise on sound governance procedures especially in the areas of best audit committee practices and codes of ethics, focusing primarily on small (less than one billion dollars) non-public banks.

Mergers and Acquisitions. Assisting in the negotiation of mergers and branch acquisitions, including drafting and negotiating agreements and securing applicable regulatory approvals.

REPRESENTATIVE WORK

− Negotiated and drafted acquisition documents for community bank transactions. − Defended numerous federal and state regulatory investigations and enforcement orders. − Negotiated and drafted numerous marketing and servicing agreements on behalf of third party service providers of financial

institutions. − Facilitated numerous strategic planning processes for boards of directors and executives of community banks. − Acted as expert witness on bank governance and securities fraud litigation in federal and state litigation and FINRA arbitrations.

RECOGNITION

− The Best Lawyers in America® - Banking and Finance Law, 2013-2015 − Best in the Business: Leading Lawyers in the Puget Sound Region, Seattle Business magazine

+ Banking and Finance, 2013-2014

ACTIVITIES − Washington Finance League − Conference of State Bank Supervisors − American Bar Association, Business Law, Member − Washington Bar Association, Business Law, Member − RiverBank, Director and Audit Committee Chair − Youth Softball Coach

QUOTED − "Empowering Consumers is Consumer Protection," Testimony before Washington State Senate Financial Institutions, Housing &

Consumer Protection Committee, February 2005

2

John L. Bley MEMBER

SEATTLE T 206.447.8915 F 206.749.2115 [email protected]

PUBLICATIONS − “So, What Are you Going to do Next?” Community Bankers of Washington Quarterly, Winter 2014 − “Credit Crisis Cause and Effect – What to Expect for Northwest in 2009,” Foster Pepper News Alert, November 2008 − “When State Regulators Come Knocking,” Co-Author, Scotsman Guide, October 2009 − “Empowering the State System - State Regulators Support Initiatives to Reduce Regulatory Burden,” The IntegraAdvisor,

August 2004 − “Supporting State Banking Systems: A Dedicated Approach to Economic Vitality,” The IntegraAdvisor, February 2003 − “Are You Ready for the Regulators? Economic Uncertainty Demands Proactive Management of Credit Risk,” IntegraAdvisor,

July 2002

PRESENTATIONS − “Creating and Implementing Your Cyber Response Plan,” Current Management Liability Issues of Interest to Community

Bankers series, Co-Presenter, November 2014 − “The Honorable Privilege of Serving as an Outside Director of a Community Bank: Practical Tips and Best Practices,” Speaker,

Community Bankers of Washington: 24th Annual Membership Convention & Trade Show, September 2014 − “Retribution: What FDIC Enforcement and Receivership Actions Tell Us about the Stand or Care,” Speaker, Washington

Bankers Association: Northwest Executive Leadership Conference, September 2014 − “Interactive Director Self Evaluation,” Speaker, Conference of State of Bank Supervisors (CSBS) Bank Directors Seminar,

September 2013 − Foster Pepper Bankers Briefing, Moderator, 2008-2014 − “Bank Audit Committee Best Practices,” Speaker, Oregon Bankers Association Directors College, February 2012 − “General Session - Legal Panel,” Panelist, CBW 21st Annual Convention and Trade Show, September 2011 − “An Interactive Mock Board Session: Governance & Audit Committee Best Practices,” Speaker, Oregon Bankers Association

106th Anniversary Convention, June 2011 − “CSBS State-Federal Supervisory Forum,” Speaker, 2011 CSBS State-Federal Supervisory Forum, May 2011 − “Update on State Charter Banks and the Anatomy of a Bank Failure,” Speaker, 2010 Real Estate & Land Use Seminar, April

2010 − “Board Governance Best Practices,” Speaker, Northwest Bank Directors College, February 2010 − “Interactive Mock Board Session – Meeting with the Regulators: Mock Board Case Study Issues,” Panelist, GSBC and CSBS

Bank Directors Seminar, September 2009 − Moderated Regulator Panel, Western Independent Bankers (WIB) Annual CFO, Investments and Operational Risk Conference,

May 2009 − “Interactive Mock Board Session,” Speaker, WIB/AABD Annual Directors Conference, November 2008 − “Directors & Regulatory Hotspots,” Presenter, Western Independent Bankers Webinar, September 2008 − “The Status of Banking in Washington,” Speaker, 2008 Commercial Lending Institute, September 2008 − “Directors & Red Flags in Board Reports,” Presenter, Western Independent Bankers Webinar, April 2008 − “Mastering Disaster - Dealing with Problem Credits,” Moderator, March 2008 − “Board Governance Best Practices,” Presenter, Northwest Bank Directors College, February 2008 − “Director Compensation & Executive Compensation in Today's Environment,” Speaker, WIB/AABD 2007 Annual Bank

Directors Conference, November 2007 − “Corporate Structures,” Speaker, Bank Directors Seminar, September 2007 − “Directors and Regulatory Hot Spots,” Speaker, The Western Independent Bankers Directors Series 2007, June 2007 − “The Director's Role in Compliance,” Speaker, The Utah Bankers Association Current Issues in Banking for Bank Directors,

April 2007

3

John L. Bley MEMBER

SEATTLE T 206.447.8915 F 206.749.2115 [email protected]

− “BSA Overview on Enterprise Risk Assessment,” Speaker, Northwest Summit for Financial Professionals, March 2007 − “Where the $OX Might Not Fit,” Speaker, Small Bank Board Governance and Audit Committee Best Practices, Northwest Bank

Directors College, February 2007 − “Challenges in the Board Room: Fiduciary Duty, Ethics and Legality,” Speaker, WBA CEO/Bank Directors Conference,

December 2006 − “Today’s Regulatory Environment,” Speaker, Today’s Regulatory Environment: Basic Real Estate Finance, November 2006 − “Managing Payment Shock: Review and Commentary on the Interagency Guidance on Nontraditional Mortgage Products Risks,”

Speaker, OBA Compliance Committee, November 2006 − “West Coast Law Update -- State Consumer Lending Enforcement Actions,” Speaker, WIB/CBA 28th Annual Regulatory

Compliance Conference, October 2006 − “The Board's Role in Compliance,” Speaker, CSBS Bank Directors Seminar, September 2006 − “Enterprise Risk Assessment,” Speaker, FDIC Bank Secrecy Act/Anti-money Laundering Seminar, September 2006 − Bank Regulatory Panel, Moderator, WICBA Annual Membership Convention, September 2006 − “Washington Bankers Association: Key Regulatory Issues Affecting Directors,” Presenter, Regulatory Issues Impacting

Directors, September 2006 − “Corporate Governance for Credit Unions,” Presenter, NASCUS 40th Annual Conference & Symposium, August 2005 − “Agent Assisted Lending & FDIC Audits Presentation and Dialogue,” Presenter, 2005 CFSA Annual Meeting, March 2005 − “What Isn't Predatory Lending,” Presenter, 2004 CFSA Annual Meeting, February 2005 − “Agent Assisted Lending & FDIC Audits Presentations and Dialogue,” Presenter, 2004 CFSA Annual Meeting, February 2004 − “Current Privacy Issues,” Presenter, 2003 AFSA/NACCA Administrators/Industry Day, September, 2003 − “Agency Audits: What Are The Traps?” Presenter, Payday Lending Regulatory Summit, June, 2003 − “The Sarbanes-Oxley Act of 2002,” Presenter, Western Independent Bankers 2003 Annual Cashiers/CFOs Conference

Workshops on Directors & the Audit Committee, June 2003 − “The Sarbanes-Oxley Act of 2002,” Presenter, Western Independent Bankers 46th Annual Conference, March 2003 − “Agency Audits: What are the Traps?” Presenter, 2003 CFSA Annual Meeting, February 2003 − “The Sarbanes-Oxley Act of 2002,” Presenter, Public Company Accounting Reform and Investor Protection, February 2003 − “Bank Directors Duties from a Legal Perspective,” Presenter, IntegraAdvisors, August 2002 − “Public Company Accounting Reform and Investor Protection, The Sarbanes-Oxley Act of 2002,” Presenter, IntegraAdvisors,

August 2002

EXPERIENCE − Foster Pepper PLLC

+ Member, 2009-Present + Of Counsel, 2006-2008

− IntegraAdvisors, LLC, CEO, 2002-2006 − Washington State Department of Financial Institutions, Director, 1993-2002 − Washington State Division of Banking

+ Supervisor of Banking, 1991-1993 + Deputy Supervisor of Banking, 1988-1991

− Graham & Dunn PC, Attorney, 1985-1988

BAR ADMISSIONS − Washington, 1985

4

John L. Bley MEMBER

SEATTLE T 206.447.8915 F 206.749.2115 [email protected]

EDUCATION

− J.D./M.B.A., Willamette University, 1985 − B.A., Pacific Lutheran University, 1980

5

Peter M. Marchel, Esq. JD, MBA, CDR, RPLU, CPCU, AIM, AIS President, Marchel & Associates Risk Consulting (425) 788 – 4349 [email protected] Peter Marchel is President and Founder of Marchel & Associates Risk Consulting a Pacific Northwest based independent insurance advisor for banks, credit unions, insurance companies, insurance agencies and companies seeking capital from the market. Some of the Services offered: Risk Consulting, prevention as well as Insurance review and analysis, Insurance Placement, Program Development, Insurance Management Issues, Policy Enforcement (Claims Advocacy, Mediation and Arbitration) and Expert Witness Testimony. Peter has more than 24 years experience in Legal and Insurance matters. His background is unique; from working on Insurance Opinions as a former Law Clerk to a State Supreme Court Justice, to arguing insurance cases before the court on behalf of both defendants and plaintiffs as a Trial Attorney. His experience as in-house Counsel and General Counsel for both insurance companies and insurance brokerages has brought a unique and valuable perspective to his clients. Peter, consults with clients and their counsel on complex claims, as well as assistance with policy language, structuring program audits, and development of financial risk solutions. Peter has developed D&O programs for over 200 different publically traded companies in the United States and Canada. Peter holds numerous insurance designations (RPLU, CPCU, AIM, and AIS). Peter has also taught Finance, Investments and Insurance Law at the College level at Crichton College, Memphis, TN., where he served as an adjunct professor.

SEATTLE T 206.447.6233

F 206.749.2140

SERVICES Business

PRACTICE OVERVIEW Yan is a first year associate in the firm’s Business and Intellectual Property practices.

RECOGNITION − 2014 AIPLA Giles Sutherland Rich Memorial Moot Court Competition

+ Best Appellate Brief + Western Regional Competition Winner + National Competition Semifinalist

− Finalist, 2012 Peterson Wampold Rosato Luna Knopp Mock Trial Competition − Best Brief & Semifinalist, 2011 Hillis Clark Martin & Peterson Appellate Advocacy

Competition

ACTIVITIES − Seattle IP Inn of Court, Associate Member, September 2014-Present − Snohomish County Legal Services, Paralegal Volunteer, 2011 − Asia Pacific American Legal Resource Center, Legal Intern Volunteer, 2011

PUBLICATIONS − “NLRB: Employers Cannot Ban Employees From Using Company’s Email System for Union-

Related Communications,” Co-author, Foster Pepper News Alert, December 2014

EXPERIENCE − Foster Pepper PLLC

+ Associate, 2014-Present + Summer Associate, 2013

− U.S. Court of Appeals Federal Circuit, Judicial Clerk Extern for the Hon. Chief Judge Randall Rader, 2013

− University of Washington Center for Commercialization, Copyright and Trademark Legal Extern, 2012

− Patterson Buchanan Fobes Leitch & Kalzer, Inc., P.S., Summer Associate, 2012

Yan Perng ASSOCIATE

1

Yan Perng ASSOCIATE

SEATTLE T 206.447.6233 F 206.749.2140 [email protected]

− Center for Advanced Study & Research on Intellectual Property, Teaching Assistant, 2012-2013 − Office of Oregon Senator Jeffrey Merkely, Legislative Assistant Intern, 2011 − Taiwan Legislature & National Chiao-Tung University, Research Assistant, 2010 − Asia FM (Broadcasting Network), Radio DJ, 2008-2011 − Videoland Television Network, Performing Artist, 2004-2008

BAR ADMISSIONS − Washington, 2014

EDUCATION

− J.D., University of Washington School of Law, 2014 + Moot Court Honor Board + VP of Professional Development, Minority Law Student Association + Entrepreneurial Law Clinic + Technology Law and Policy Clinic

− B.S. Biochemical Engineering, National Taiwan University, 2008

LANGUAGES − Chinese (Mandarin), fluent

2