ctc 475 review bonds bonds not straightforward because bonds can be bought and/or sold between the...

Post on 19-Dec-2015

218 views

TRANSCRIPT

CTC 475 Review CTC 475 Review

BondsBonds Not straightforward because bonds can Not straightforward because bonds can

be bought and/or sold between the be bought and/or sold between the date of issuance and the date of date of issuance and the date of maturitymaturity

P=Vr(P/AP=Vr(P/Ai,ni,n)+F(P/F)+F(P/Fi,ni,n)) Find PFind P Find FFind F Find IFind I Cash flow frequency, i and n must matchCash flow frequency, i and n must match

CTC 475 CTC 475

Comparing AlternativesComparing Alternatives

ObjectivesObjectives

Know the steps for comparing Know the steps for comparing alternativesalternatives

Know how to determine the possible Know how to determine the possible set of alternatives set of alternatives

Know how to develop cash flows Know how to develop cash flows using the same planning horizonusing the same planning horizon

Steps for Comparing AlternativesSteps for Comparing Alternatives

1.1. Determine the feasible alternativesDetermine the feasible alternatives

2.2. Define the planning horizonDefine the planning horizon

3.3. Develop the cash flow profilesDevelop the cash flow profiles

4.4. Specify the MARRSpecify the MARR

5.5. Compare the alternativesCompare the alternatives

6.6. Perform supplementary analysesPerform supplementary analyses

7.7. Select the preferred alternativeSelect the preferred alternative

Determine Feasible AlternativesDetermine Feasible Alternatives

Alternatives can consist of various Alternatives can consist of various investment proposalsinvestment proposals

Proposals can be:Proposals can be: Mutually exclusiveMutually exclusive IndependentIndependent Contingent upon another proposalContingent upon another proposal

Mutual ExclusiveMutual Exclusive

At most one project out of the group At most one project out of the group can be chosen:can be chosen:

If I have proposals A, B, and C------- If I have proposals A, B, and C------- only A or B or C can be chosen (not a only A or B or C can be chosen (not a combination)combination)

IndependentIndependent

All, none or any combination may be All, none or any combination may be selectedselected

Total number of alternatives = 2Total number of alternatives = 2mm where m is the number of proposalswhere m is the number of proposals

If there are 4 proposals, the total If there are 4 proposals, the total number of options is 2number of options is 244 = 16 = 16 alternativesalternatives

ContingentContingent

The choice of a project is conditional The choice of a project is conditional on the choice of another projecton the choice of another project

If A is contingent on B then A can’t be If A is contingent on B then A can’t be implemented unless B is also implemented unless B is also implementedimplemented

Example of Defining Example of Defining Alternatives and Developing Alternatives and Developing

Cash Flow ProfilesCash Flow Profiles

Steps 1 and 3 Steps 1 and 3

(planning horizon is the same)(planning horizon is the same)

Three Proposals-A,B,CThree Proposals-A,B,C

EOYEOY AA BB CC

00 -$20K-$20K -$30K-$30K -$50K-$50K

11 -$4K-$4K $4K$4K -$5K-$5K

22 $2K$2K $6K$6K $10K$10K

33 $8K$8K $8K$8K $25K$25K

44 $14K$14K $10K$10K $40K$40K

55 $25K$25K $20K$20K $10K$10K

Number of AlternativesNumber of Alternatives

2233 = 8 alternatives = 8 alternatives

AlternativesAlternatives

AA BB CC Initial Initial InvestmenInvestmentt

00 00 00 $0$0

00 00 11 $50K$50K

00 11 00 $30K$30K

00 11 11 $80K$80K

11 00 00 $20K$20K

11 00 11 $70K$70K

11 11 00 $50K$50K

11 11 11 $100K$100K

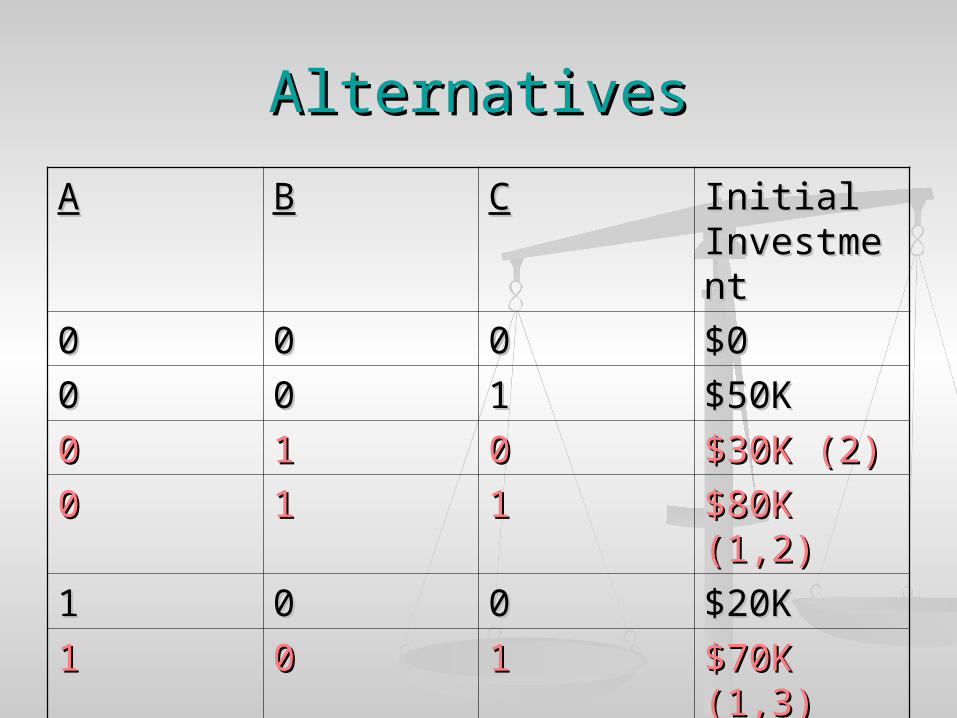

RestrictionsRestrictions

1.1. Budget for initial investment is Budget for initial investment is $50K$50K

2.2. Proposal B is contingent on proposal Proposal B is contingent on proposal A (can’t do B unless A is A (can’t do B unless A is implemented)implemented)

3.3. Proposals A and C are mutually Proposals A and C are mutually exclusive (A & C can’t be exclusive (A & C can’t be implemented together)implemented together)

AlternativesAlternatives

AA BB CC Initial Initial InvestmenInvestmentt

00 00 00 $0$0

00 00 11 $50K$50K

00 11 00 $30K (2)$30K (2)

00 11 11 $80K (1,2)$80K (1,2)

11 00 00 $20K$20K

11 00 11 $70K (1,3)$70K (1,3)

11 11 00 $50K$50K

11 11 11 $100K $100K (1,3)(1,3)

Remaining AlternativesRemaining Alternatives

Null or “Do Nothing”Null or “Do Nothing” C onlyC only A onlyA only A and BA and B

Cash Flow ProfilesCash Flow Profiles

EOYEOY NullNull CC AA A&BA&B

00 $0$0 -$50K-$50K -$20K-$20K -$50K-$50K

11 $0$0 -$5K-$5K -$4K-$4K $0$0

22 $0$0 $10K$10K $2K$2K $8K$8K

33 $0$0 $25K$25K $8K$8K $16K$16K

44 $0$0 $40K$40K $14K$14K $24K$24K

55 $0$0 $10K$10K $25K$25K $45K$45K

Planning Horizon (PH)Planning Horizon (PH)

Period of time over which service is Period of time over which service is requiredrequired

Period of time over which receipts Period of time over which receipts continue to occurcontinue to occur

Period of time over which reasonably Period of time over which reasonably accurate cash flow estimates can be accurate cash flow estimates can be providedprovided

Planning horizon, working Planning horizon, working life of equipment and life of equipment and

depreciable life are not depreciable life are not necessarily the samenecessarily the same

When comparing When comparing Alternatives-----Alternatives-----

The Planning Horizon must The Planning Horizon must be the samebe the same

Methods: Methods:

Least common multiple (LCM)Least common multiple (LCM) Shortest lifeShortest life Longest lifeLongest life Some determined lifeSome determined life

ExampleExample

Alternatives A, B & C have 3, 6, and Alternatives A, B & C have 3, 6, and 5-year lives5-year lives Least common multiple = 30 yearsLeast common multiple = 30 years Shortest life = 3 yearsShortest life = 3 years Longest life = 6 yearsLongest life = 6 years Standard planning horizon could be 5 Standard planning horizon could be 5

years (or 4 years or some other number)years (or 4 years or some other number)

Problems in standardizing the PHProblems in standardizing the PH

LCM-usually assume cash flow LCM-usually assume cash flow patterns repeatpatterns repeat

Shortest Life-Must estimate the Shortest Life-Must estimate the unused portions of the alternatives unused portions of the alternatives (salvage value)(salvage value)

Longest Life-Must estimate cash flow Longest Life-Must estimate cash flow patterns between the shortest and patterns between the shortest and longest lifelongest life

Example of Standardizing the PH Example of Standardizing the PH and Developing Cash Flow Profilesand Developing Cash Flow Profiles

Steps 2/3Steps 2/3

Alternative 1 (use existing Alternative 1 (use existing equipment) PH=3 yearsequipment) PH=3 years

Alternative 2 (buy new $50K) PH=6 Alternative 2 (buy new $50K) PH=6 yearsyears

Alternative 3 (buy new $75K) PH=5 Alternative 3 (buy new $75K) PH=5 yearsyears

Standardizing PH-ExampleStandardizing PH-ExampleEOYEOY Alt 1 (3 Alt 1 (3

yrs)yrs)Alt 2 (6 Alt 2 (6 yrs)yrs)

Alt 3 (5 Alt 3 (5 yrs)yrs)

SalvSalvgg

SalvSalvgg

SalvSalvgg

00 00 00 -50K-50K 50K50K -75K-75K 75K75K

11 45004500 00 20K20K 35K35K 20K20K 55K55K

22 45004500 00 20K20K 25K25K 25K25K 40K40K

33 45004500 00 20K20K 15K15K 30K30K 25K25K

44 20K20K 5K5K 35K35K 10K10K

55 20K20K 00 40K40K 00

66 20K20K 00

Example-LCMExample-LCMEOYEOY Alt 1Alt 1 Alt 2Alt 2 Alt 3Alt 3

00 00 -50K-50K -75K-75K

11 45004500 20K20K 20K20K

22 45004500 20K20K 25K25K

33 45004500 20K20K 30K30K

44 45004500 20K20K 35K35K

55 45004500 20K20K -35K (40K-75K-35K (40K-75K

66 45004500 -30K (20K--30K (20K-50K)50K)

20K20K

77 45004500 20K20K 25K25K

88 45004500 20K20K 30K30K

………….... 45004500 *-30K@ yrs *-30K@ yrs 12,18,2412,18,24

*-35K@yrs *-35K@yrs 10,15,20,2510,15,20,25

3030 45004500 20K20K 40K40K

Example-Shortest LifeExample-Shortest Life

EOYEOY Alt 1Alt 1 Alt 2Alt 2 Alt 3Alt 3

00 00 -50K-50K -75K-75K

11 4,5004,500 20K20K 20K20K

22 4,5004,500 20K20K 25K25K

33 4,5004,500 35K35K (20K+15K(20K+15K

))

55K55K (30K+25K(30K+25K

Example-Longest LifeExample-Longest Life

EOYEOY Alt 1Alt 1 Alt 2Alt 2 Alt 3Alt 3

00 00 -50K-50K -75K-75K

11 45004500 20K20K 20K20K

22 45004500 20K20K 25K25K

33 45004500 20K20K 30K30K

44 45004500 20K20K 35K35K

55 45004500 20K20K 40K40K

66 45004500 20K20K 45004500

Next lectureNext lecture

Methods for Comparing Methods for Comparing Alternatives:Alternatives: Ranking (PW, AW, FW)Ranking (PW, AW, FW) Incremental (all)Incremental (all)

Supplementary Supplementary AnalysesAnalyses

Selling the AlternativeSelling the Alternative