ct6 cmp upgrade 2013 2014 - actuarial education … upgrade/ct6-pu-14.pdfthis cmp upgrade lists all...

TRANSCRIPT

CT6: CMP Upgrade 2013/14 Page 1

The Actuarial Education Company © IFE: 2014 Examinations

Subject CT6

CMP Upgrade 2013/14

CMP Upgrade This CMP Upgrade lists all significant changes to the Core Reading and the ActEd material since last year so that you can manually amend your 2013 study material to make it suitable for study for the 2014 exams. It includes replacement pages and additional pages where appropriate. Alternatively, you can buy a full replacement set of up-to-date Course Notes at a significantly reduced price if you have previously bought the full price Course Notes in this subject. Please see our 2014 Student Brochure for more details.

This CMP Upgrade contains: All non-trivial changes to the Syllabus objectives and Core Reading. Changes to the ActEd Course Notes, Question and Answer Bank, and Series X

Assignments that will make them suitable for study for the 2014 exams.

Page 2 CT6: CMP Upgrade 2013/14

© IFE: 2014 Examinations The Actuarial Education Company

1 Changes to the Syllabus objectives and Core Reading

1.1 Syllabus objectives There have been no changes to the syllabus.

1.2 Core Reading Chapter 2 Page 10 The following paragraph has been deleted. It is often convenient to express this result in terms of the value of a statistic,

such as X , rather than the sample values X. So, for example,

( )f XqΩ = ( ) ( )

( )

f X f

f X

q qΩ.

In practice these are equivalent. Chapter 3 Page 4 In Section 1.1, where the exponential distribution is defined, it has been specified that > 0l and > 0x .

Page 5 In Section 1.2, where the gamma distribution is defined, it has been specified that

> 0a , > 0l and > 0x .

Page 7

In Section 2.1, where the Pareto distribution is defined, it has been specified that > 0a , > 0l and > 0x .

CT6: CMP Upgrade 2013/14 Page 3

The Actuarial Education Company © IFE: 2014 Examinations

Page 10 Under the section on Method of Moments, ix has been redefined:

xi = the ith value in the sample Page 11 In Section 2.3, where the Weibull distribution is defined, it has been specified that > 0c , > 0g and > 0x .

Page 16 The section on MLE has been modified to include formulae for the discrete case. A replacement page is provided. Page 19 In the first paragraph of Core Reading, references to estimates have been changed to estimators. Page 20 In the first paragraph of Core Reading, references to estimates have been changed to estimators. In Section 3.6, the word n-denominator has been inserted before sample variance. Pages 27 to 30 Various changes have been made to the section on mixture distributions, to help improve the flow. Replacement pages are provided.

Page 4 CT6: CMP Upgrade 2013/14

© IFE: 2014 Examinations The Actuarial Education Company

Chapter 4 Pages 6 and 7 There have been several modifications to Pages 6 and 7, including a deletion of the discussion on complete and incomplete integrals. Replacement pages are provided. Page 8 Some alterations have been made to the notation used in the discussion of the reinsurer’s conditional claims distribution. A replacement page is provided. Page 10 The second and third paragraphs of Core Reading have been altered. A replacement page is provided. Pages 19 and 20 The following passage has been deleted: The same device as the one used to obtain (1.3) can be used to convert (3.1) to a complete integral. (3.1) can be written as

E(Y) = • • •

- +Ú Ú Ú0 / /( ) ( ) ( )

M k M kkx f x dx kx f x dx M f x dx

= k E(X) k •

-Ú /( / ) ( ) .

M kx M k f x dx

The new mean amount paid by the insurer is

E(Y) = •

- +Ú0( ( ) ( / ) ).k E X y f y M k dy (3.2)

Note that the integral in (3.2) has the same form as that in (1.3). Page 20 The paragraph of Core Reading in the middle of the page has been replaced with: One important general point that can be made is that the new mean claim amount paid by the insurer is not k times the mean claim amount paid by the insurer without inflation.

CT6: CMP Upgrade 2013/14 Page 5

The Actuarial Education Company © IFE: 2014 Examinations

Page 24 Some alterations have been made to the discussion on estimation. A replacement page is provided. Chapter 7 Page 18 At the bottom of the page, the following fragment of a sentence has been deleted: and the distribution of S follows that of N. Pages 19 to 24 Some alterations have been made to the discussion of the compound Poisson distribution and the result concerning the sum of compound Poisson distributions. Replacement pages are provided. Pages 24 to 26 In the discussion on the compound binomial distribution, the distribution of the number of claims has been changed from N ~ bin(n, q) to the more usual N ~ bin(n, p) so that all of the q’s are now p’s and vice-versa. Replacement pages are provided. Chapter 8 Page 3 The second paragraph has been rewritten as: If, for example, ~ ( )N Poi l , SI has a compound Poisson distribution with Poisson

parameter , and the thi individual claim amount is Yi. Similarly, SR has a

compound Poisson distribution with Poisson parameter , and the thi individual claim amount is Zi.

Page 6 CT6: CMP Upgrade 2013/14

© IFE: 2014 Examinations The Actuarial Education Company

Pages 5 and 6 Some small changes have been made to the example in the Core Reading to improve the flow. Replacement pages are provided. Pages 6 and 8 Some changes have been made to the notation used for the PDF of the reinsurer’s conditional claims distribution, to tie in with the changes made to the notation in Chapter 4. Replacement pages are provided. Page 11 Two-thirds of the way down the page, a sentence has been rewritten as: Thus, the distribution of Yj is compound binomial, with individual claim amount

random variable Xj.

At the bottom of the page, the following sentence has been deleted: It was seen in Section 3.5 of Chapter 7 that there is no general result about the distribution of such a sum. Page 13 The first part of Section 3.2 has been altered to: Consider a portfolio consisting of n independent policies. The aggregate claims from the i-th policy are denoted by the random variable Si, where Si has a

compound Poisson distribution with parameters i , and the CDF of the

individual claim amounts distribution is F(x). Notice that, for simplicity, the CDF of the distribution of individual claim amounts, F(x), is assumed to be identical for all the policies. In this example the distribution of individual claim amounts, ie F(x), is assumed to be known but the values of the Poisson parameters, ie the i s, are not known.

CT6: CMP Upgrade 2013/14 Page 7

The Actuarial Education Company © IFE: 2014 Examinations

Page 17 The first part of Section 3.4 has been altered to: Now a different example is considered. Suppose, as before, there is a portfolio of n policies. The aggregate claims from a single policy have a compound Poisson distribution with parameters , and the CDF of the individual claim amounts random variable is F(x). The Poisson parameters are the same for all policies in the portfolio.

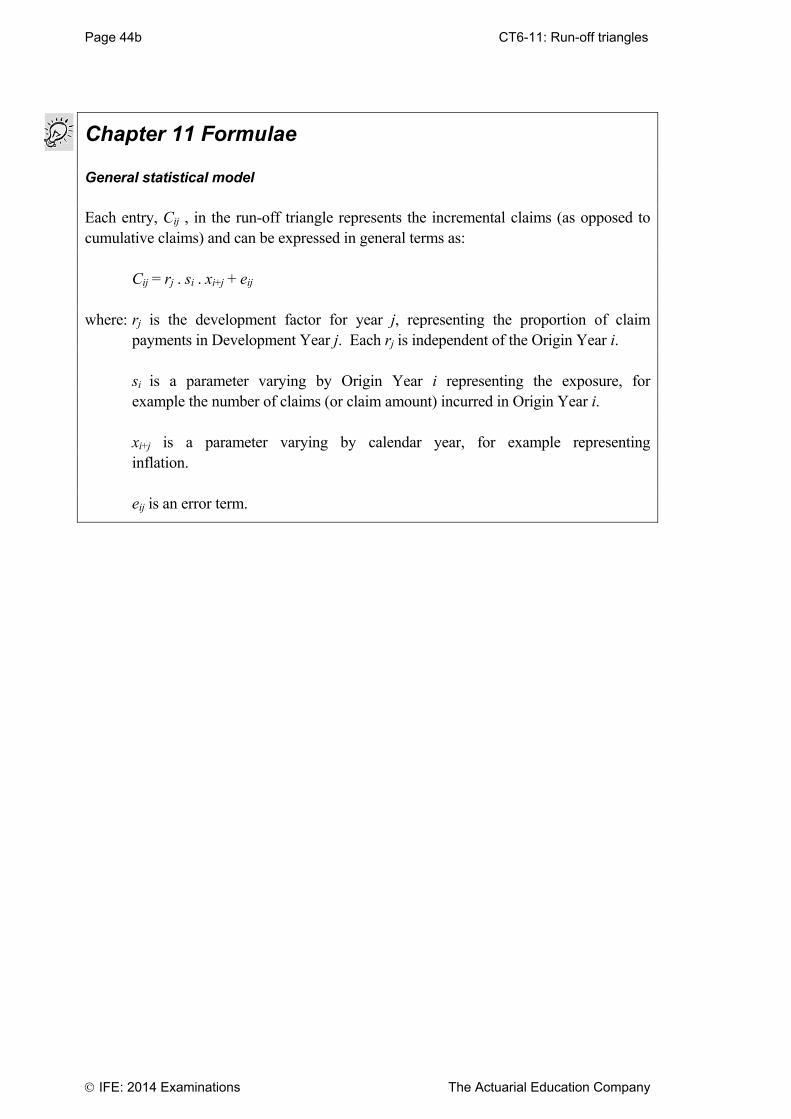

Chapter 11 The origin years in the run-off triangles have been brought more up-to-date. This doesn’t affect the understanding of the material in anyway so we have not provided replacement pages.

Page 8 CT6: CMP Upgrade 2013/14

© IFE: 2014 Examinations The Actuarial Education Company

2 Changes to the ActEd Course Notes All Chapters The Summary and Formulae Pages have been updated for all chapters in an attempt to better reflect the key material to be revised for the exam. Replacement pages are provided for all chapters. Chapter 2 Page 10 The following paragraph has been deleted:

The notation can get a little confusing here. Remember that X is a sample mean, whereas X refers to the whole group of values of X ie a vector containing all the

values in the sample.

Chapter 3 Page 17 The 1st step in the description of how to find an MLE has been modified to take account of the discrete case: (1) Write down the likelihood function for the available data. If the likelihood is

based on a set of known values x x xn1 2, , , , then the likelihood function will take

the form 1 2( ) ( ) ( )nf x f x f x , where f x( ) is the PDF of X where X is a

continuous random variable (or ( ) ( ) ( )1 2 nP X x P X x P X x= = = in the case

where X is a discrete random variable).

Chapter 4 Pages 6 and 7 There have been several modifications to Pages 6 and 7 to try and improve the clarity, including the deletion of Questions 4.3 and 4.4. Replacement pages are provided.

CT6: CMP Upgrade 2013/14 Page 9

The Actuarial Education Company © IFE: 2014 Examinations

Pages 8 to 10 Some alterations have been made to the notation used in the discussion of the reinsurer’s conditional claims distribution. Replacement pages are provided. Page 36 Solutions 4.3 and 4.4 have been deleted to correspond with the deletion of Question 4.3. Page 37 In Solution 4.5, the “z’s” have been replaced with “w’s” to tie in with the altered notation relating to the reinsurer’s conditional claims distribution. In Solution 4.6, the “z’s” have been replaced with “w’s” to tie in with the altered notation relating to the reinsurer’s conditional claims distribution. Pages 44 and 45 In Solution 4.16, the “y’s” have been replaced with “w’s” to tie in with the altered notation relating to the reinsurer’s conditional claims distribution. Pages 45 and 46 Solution 4.17 has been modified, to improve clarity, as follows: Without the excess, the average amount paid by the insurer in respect of each loss is the

mean of a ( ),Pa a l distribution:

1

la -

With an excess L , the average amount paid by the insurer in respect of each loss is:

1

( )( )L

x L dxx

a

ala

l

•

+-+Ú

Using the substitution y x L= - , this is:

1

0 ( )y dy

L y

a

ala

l

•

++ +Ú

Page 10 CT6: CMP Upgrade 2013/14

© IFE: 2014 Examinations The Actuarial Education Company

We now transform the integrand into the mean of a ( ),Pa La l + distribution:

11

0 0

( )( )

( )

1

Ly L y dy y dy

L L y

L

L

a aa a

a

a

l lal l al l

l ll a

• •- -

++Ê ˆ+ + = Á ˜Ë ¯+ + +

+Ê ˆ= Á ˜Ë ¯+ -

Ú Ú

So, the ratio of the risk premiums will be:

2.5 11 5,000

0.9711 1 5,000 100

L

L L

a al ll la al l

--+ Ê ˆÊ ˆ Ê ˆ= = =Á ˜ Á ˜ Á ˜Ë ¯ Ë ¯ Ë ¯- -+ + +

ie a reduction of 2.9%. Chapter 5 Page 17 The first sentence of the last paragraph has been modified to say:

In fact, what is required is ( | )E X x ( )|E xl= .

Chapter 7 Page 41 In Solution 7.9, the q’s have been changed p’s and vice-versa to tie in with the change to the Core Reading, where N is now presented has having a binomial distribution with parameters n and p. Chapter 8 Page 7 At the top of Page 7, the PDF of the reinsurer’s conditional claim amount distribution is now defined as:

( )

( )1 ( )

XW

X

f w Mg w

F M

+=-

CT6: CMP Upgrade 2013/14 Page 11

The Actuarial Education Company © IFE: 2014 Examinations

Chapter 10 Significant changes have been made to the ActEd notes for this chapter to improve the explanations and examples. Replacement pages are provided for the whole chapter. Chapter 11 The origin years in the run-off triangles have been brought more up-to-date. This doesn’t affect the understanding of the material in anyway so we have not provided replacement pages. Page 11 We have added the following paragraphs to the top of Page 11, before Question 11.7 to help explain the general statistical model: Note that some of the terminology above is being used in a different context to previously. The development factors jr in this general statistical model are defined

differently to the development factors that we have met previously. The development factors that we met previously were used to project forward cumulative claims data. The development factors in the general statistical model are being used to model incremental data. They are defined above as the proportion of claims from a particular accident year that are paid in the jth development year. As such, they are a set of factors that add up to 1. A question may help you to see what is going on.

Page 12 CT6: CMP Upgrade 2013/14

© IFE: 2014 Examinations The Actuarial Education Company

3 Changes to the Q&A Bank Part 2 Questions Question 2.10 The headings in the table have been corrected to j , jY and jP .

(Previously these were incorrectly labelled as i , iY and iP .)

Solution 2.21 Two formulae were incorrectly labelled ( )E Y . These have now been changed to ( )E Z .

CT6: CMP Upgrade 2013/14 Page 13

The Actuarial Education Company © IFE: 2014 Examinations

4 Changes to the X Assignments

This section provides details of changes that have been made to the 2013 X Assignments, so that you can continue to use these for the 2014 exams. However, if you are having your attempts marked by ActEd, you will need to use the 2014 version of the X Assignments. Assignment X2 Solutions We have corrected a typo in Solution X2.6(i):

2 3 31 1 185 35 2 1 3( ) (85 35 ) 3,808E Y - += - =

(Previously, the answer was quoted incorrectly as 133,803 .)

Assignment X3 Questions Question X3.2 has been reworded to say: Define a model for each incremental entry, ijC , in general terms and explain each

element of the formula. Question X3.7 now refers to “Policy Year” not “Accident Year” in the run-off triangle. Assignment X3 Solutions Solution X3.7 now refers to “Policy Year” not “Accident Year”. We have corrected a typo in Solution X3.11(i)(c):

2

2 2

(100 1,300 )( 3) (1 3 )(100 2,600 )

(100 1,300 )

dR

d

2 2

2 2

2

2 2

300 3,900 100 2,600 300 7,800

(100 1,300 )

2,600 3,900 100

(100 1,300 )

(Previously, the denominator was not squared. The final answer is unaffected.)

Page 14 CT6: CMP Upgrade 2013/14

© IFE: 2014 Examinations The Actuarial Education Company

Assignment X4 Solutions We have corrected a typo in the notes (in italics) to solution X4.2:

2 20.005

2

200

10

zn >

(Previously, the subscript of the z was 0.01.) We have added the following new statement (worth [1] mark) to Solution X4.4(i): This reproducibility removes the variability of using different sets of random numbers, which is helpful for comparing different models. Any two of the three statements are now needed to score a maximum of [2] marks on this part.

CT6: CMP Upgrade 2013/14 Page 15

The Actuarial Education Company © IFE: 2014 Examinations

5 Other tuition services In addition to this CMP Upgrade you might find the following services helpful with your study.

5.1 Study material We offer the following study material in Subject CT6:

ASET (ActEd Solutions with Exam Technique) and Mini-ASET

Flashcards

Mock Exam A and Additional Mock Pack (AMP)

Revision Notes

Online Classroom. For further details on ActEd’s study materials, please refer to the 2014 Student Brochure, which is available from the ActEd website at www.ActEd.co.uk.

5.2 Tutorials We offer the following tutorials in Subject CT6:

a set of Regular Tutorials (lasting two or three full days)

a Block Tutorial (lasting two or three full days)

a Revision Day (lasting one full day)

a Taught Course (lasting four full days)

a series of webinars (lasting approximately an hour and a half each)

CT6 Online Classroom. For further details on ActEd’s tutorials, please refer to our latest Tuition Bulletin, which is available from the ActEd website at www.ActEd.co.uk.

Page 16 CT6: CMP Upgrade 2013/14

© IFE: 2014 Examinations The Actuarial Education Company

5.3 Marking You can have your attempts at any of our assignments or mock exams marked by ActEd. When marking your scripts, we aim to provide specific advice to improve your chances of success in the exam and to return your scripts as quickly as possible. For further details on ActEd’s marking services, please refer to the 2014 Student Brochure, which is available from the ActEd website at www.ActEd.co.uk.

CT6: CMP Upgrade 2013/14 Page 17

The Actuarial Education Company © IFE: 2014 Examinations

6 Feedback on the study material

ActEd is always pleased to get feedback from students about any aspect of our study programmes. Please let us know if you have any specific comments (eg about certain sections of the notes or particular questions) or general suggestions about how we can improve the study material. We will incorporate as many of your suggestions as we can when we update the course material each year. If you have any comments on this course please send them by email to [email protected] or by fax to 01235 550085.

© IFE: 2014 Examinations The Actuarial Education Company

All study material produced by ActEd is copyright and is sold for the exclusive use of the purchaser. The copyright is owned

by Institute and Faculty Education Limited, a subsidiary of the Institute and Faculty of Actuaries.

Unless prior authority is granted by ActEd, you may not hire out, lend, give out, sell, store or transmit electronically or

photocopy any part of the study material.

You must take care of your study material to ensure that it is not used or copied by anybody else.

Legal action will be taken if these terms are infringed. In addition, we may seek to take disciplinary action through the

profession or through your employer.

These conditions remain in force after you have finished using the course.

CT6-01: Decision theory Page 25

The Actuarial Education Company IFE: 2014 Examinations

Chapter 1 Summary Zero-sum games In this chapter we study zero-sum two-player games. If we call our players (who are in conflict) Alice and Bob then the term zero-sum tells us that whatever Alice loses, Bob must win; there are no payments to or receipts from third parties. Both Alice and Bob have a number of different strategies open to them. The payoffs from each combination of strategies can be represented in a matrix. The payoffs associated with Alice’s available strategies (labelled I, II, III, etc) determine the columns of the matrix. The payoffs associated with Bob’s available strategies (labelled 1, 2, 3, etc) determine the rows of the payoff matrix. One strategy is said to dominate another if the first strategy is at least as good as the second and in some cases better. Dominated strategies can always be discarded. Problems in Decision Theory usually involve the determination of optimum strategies and the corresponding payoff, or value, of the game. Two criteria that are often used to determine optimum strategies are the minimax criterion and the Bayes criterion. Under the minimax criterion, all players will adopt the strategy that minimises their maximum loss (or maximises their minimum gain). The minimax criterion can be thought of as a ‘best-of-all-evils’ approach. A saddle point is the name given to an entry of a payoff matrix that is the largest in its column and the smallest in its row. If a saddle point exists then each player will adopt the pure strategy, with the options that correspond to the saddle point being chosen. If there is no saddle point, a randomised strategy can be adopted to enable a player to minimise his/her maximum expected loss. This means that the player will vary his or her choice of strategy in a random fashion but in accordance with some fixed set of probabilities. Statistical games A statistical game can be regarded as a game between nature (which controls the relevant features of a population) and the statistician (who is trying to make a decision about the population).

Page 26 CT6-01: Decision theory

IFE: 2014 Examinations The Actuarial Education Company

An example of a statistical game is where a statistician wishes to determine whether a coin is fair (F) or biased (B) towards tails, with nature acting as his/her “opponent”. A decision function sets out the action for the statistician to take based on each outcome of an event, eg the event might be a single toss of the coin and one example of a decision function is: F if the coin toss results in heads and B if the coin toss results in tails. A risk function sets out the expected loss for a particular decision function and a given actual state of nature. In order to calculate the expected loss, probabilities must be assigned to each state of nature. The statistician can then use the minimax criterion to find the decision function that minimises the maximum value of risk function ... ... or the Bayes criterion to find the decision function that minimises the expected value of the risk function.

CT6-02: Bayesian statistics Page 27

The Actuarial Education Company IFE: 2014 Examinations

Chapter 2 Summary Bayesian estimation vs classical estimation A common problem in statistics is to estimate the value of some unknown parameter . The classical approach to this problem is to treat as a fixed, but unknown, constant and use sample data to estimate its value. For example, if represents some population mean then its value may be estimated by a sample mean. The Bayesian approach is to treat as a random variable. Prior distribution of θ

The prior distribution of represents the knowledge available about the possible values

of before the collection of any sample data. The prior PDF of q is denoted ( )f q .

Likelihood function of the sample data A likelihood function is then determined, based on a set of observations

( )1 2, , ... , nx x x x= . The likelihood function is just the same as the joint density (or, in

the discrete case, the joint probability) of X X Xn1 2, , , | . However, the likelihood is

considered to be a function of rather than one of x x xn1 2, , , . Since we are

assuming that the random variables X X n1| , , | are independent, the joint density

function f x x xX n| ( , , , ) 1 2 is equal to the product of the individual density functions

f xX ii |( ) . The likelihood function is therefore:

( ) |1

| ( )i

n

X ii

L x f xqq=

=’

Posterior distribution of θ

The PDF (or probability function) of the prior distribution and the likelihood function are then combined to obtain the PDF (or probability function) of the posterior distribution for .

Page 28 CT6-02: Bayesian statistics

IFE: 2014 Examinations The Actuarial Education Company

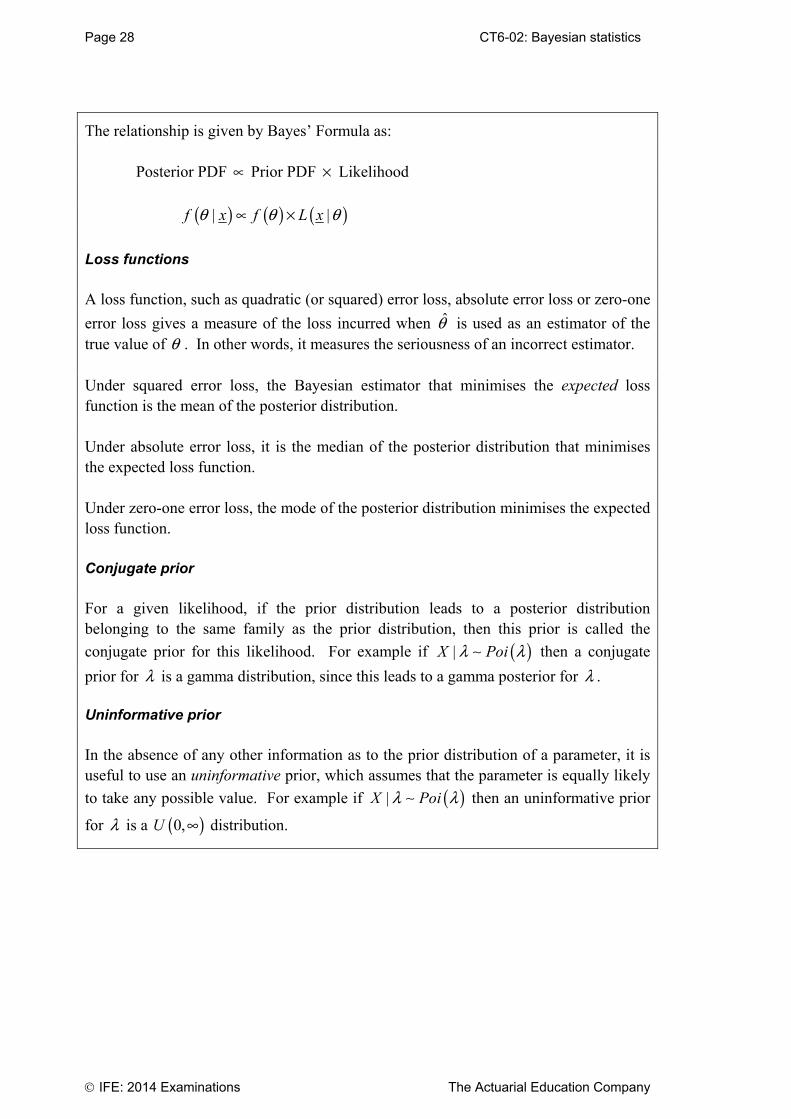

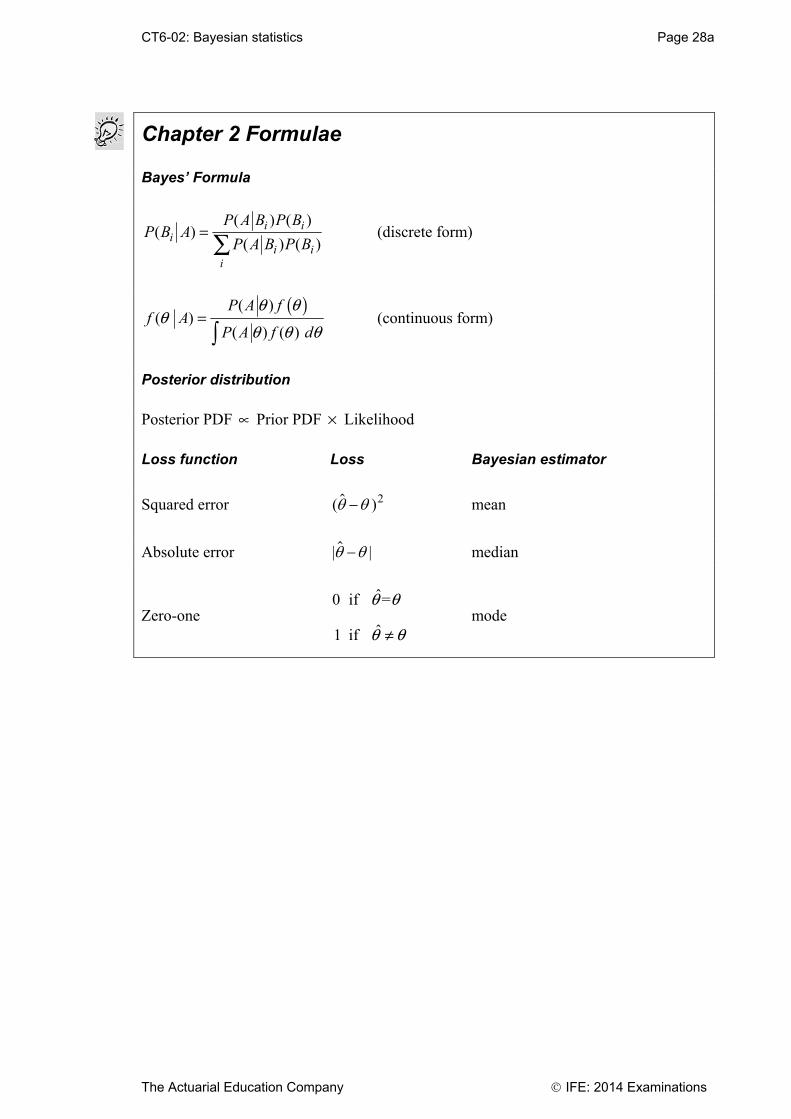

The relationship is given by Bayes’ Formula as: Posterior PDF μ Prior PDF ¥ Likelihood

( ) ( ) ( )| |f x f L xq q qμ ¥

Loss functions A loss function, such as quadratic (or squared) error loss, absolute error loss or zero-one

error loss gives a measure of the loss incurred when q is used as an estimator of the true value of q . In other words, it measures the seriousness of an incorrect estimator. Under squared error loss, the Bayesian estimator that minimises the expected loss function is the mean of the posterior distribution. Under absolute error loss, it is the median of the posterior distribution that minimises the expected loss function. Under zero-one error loss, the mode of the posterior distribution minimises the expected loss function. Conjugate prior For a given likelihood, if the prior distribution leads to a posterior distribution belonging to the same family as the prior distribution, then this prior is called the

conjugate prior for this likelihood. For example if ( )|X Poil l then a conjugate

prior for l is a gamma distribution, since this leads to a gamma posterior for l . Uninformative prior In the absence of any other information as to the prior distribution of a parameter, it is useful to use an uninformative prior, which assumes that the parameter is equally likely

to take any possible value. For example if ( )|X Poil l then an uninformative prior

for l is a ( )0,U • distribution.

CT6-02: Bayesian statistics Page 28a

The Actuarial Education Company IFE: 2014 Examinations

Chapter 2 Formulae Bayes’ Formula

( ) ( )( )

( ) ( )=Â

i ii

i ii

P A B P BP B A

P A B P B (discrete form)

( )( )( )

( ) ( )=Ú

P A ff A

P A f d

q qq

q q q (continuous form)

Posterior distribution Posterior PDF μ Prior PDF ¥ Likelihood Loss function Loss Bayesian estimator

Squared error ( ) 2 mean

Absolute error | | median

Zero-one ˆ0 if =

ˆ1 if

q q

q qπ mode

Page 28b CT6-02: Bayesian statistics

IFE: 2014 Examinations The Actuarial Education Company

This page has been left blank so that you can keep the chapter summaries together as a revision tool.

CT6-03: Loss distributions Page 15

The Actuarial Education Company IFE: 2014 Examinations

3 Estimation

The methods of maximum likelihood, moments and percentiles can be used to fit distributions to sets of data. The fit of the distribution can be tested formally by

using a 2 test. The method of percentiles is outlined in Section 3.7; the other

methods and the 2 test have been covered in Subject CT3, Probability and

Mathematical Statistics. The formulae for the densities, the moments and the moment generating functions (where they exist) for the distributions discussed in this chapter are given in the Formulae and Tables for Actuarial Examinations. We will give a brief summary of the method of moments and of maximum likelihood estimation for those students who have not taken Subject CT3 recently. An example of using the chi square distribution will also be given, in case you have forgotten how to carry out this test.

3.1 The method of moments

For a distribution with r parameters, the moments are as follows:

jm = =Â

1

1 nji

i

xn

j = 1, 2 … r

where jm = E(Xj), a function of the unknown parameter, , being estimated

n = the sample size xi = the ith value in the sample

The estimate for the parameter, , can be determined by solving the equation above. Where there is more than one parameter, they can be determined by solving the simultaneous equations for each mj.

To obtain a method of moments estimator for a parameter, we equate the corresponding sample and population non-central moments. So, for example, if we were trying to estimate the value of a single parameter, and we had a sample of n claims whose sizes were x x xn1 2, , , , we would solve the equation:

1

1( )

n

ii

E X xn =

= Â

ie we would equate the first non-central moments for the population and the sample.

Page 16 CT6-03: Loss distributions

IFE: 2014 Examinations The Actuarial Education Company

If we were trying to find estimates for two parameters (for example if we were fitting a gamma distribution and needed to find estimates for both parameters), we would solve the simultaneous equations:

1

1( )

n

ii

E X xn =

= Â and 2 2

1

1( )

n

ii

E X xn =

= Â

In fact in the two parameter case, estimates are usually obtained by equating sample and population means and variances. If we define the sample variance to have a denominator n , this will give the same estimates as would be obtained by equating the first two non-central moments.

More generally, we use as many equations of the form 1

1( )

nk k

ii

E X xn =

= Â , k 1 2, , as

are needed to determine estimates of the relevant parameters.

3.2 Maximum Likelihood Estimation

The likelihood function of a random variable, X, is the probability (or PDF) of observing what was observed given a hypothetical value of the parameter, . The maximum likelihood estimate (MLE) is the one that yields the highest probability (or PDF), ie that maximises the likelihood function. For the sample in Section 3.1 above, the likelihood function L() can be expressed as:

( ) ( )=

= =’1

|n

ii

L P X xq q for a discrete random variable, X, or

( ) ( )|=

=’1

n

ii

L f xq q for a continuous random variable, X.

To determine the MLE the likelihood function needs to be maximised. Often it is practical to consider the loglikelihood function:

( ) ( ) ( )=

= = =Â1

log log |n

ii

l L P X xq q q for a discrete random variable, X, or

( ) ( ) ( )=

= = Â1

log logn

ii

l L f xq q q for a continuous random variable, X.

CT6-03: Loss distributions Page 17

The Actuarial Education Company IFE: 2014 Examinations

If l() can be differentiated with respect to , the MLE, expressed as q , satisfies the expression:

ˆ( )d

ld

= 0

Where there is more than one parameter, the MLEs for each parameter can be determined by taking partial derivatives of the loglikelihood function and setting each to zero. The determination of MLEs when the data is incomplete is covered in Chapter 4. The steps involved in finding a maximum likelihood estimate (MLE) are as follows: (1) Write down the likelihood function for the available data. If the likelihood is

based on a set of known values x x xn1 2, , , , then the likelihood function will take

the form 1 2( ) ( ) ( )nf x f x f x , where f x( ) is the PDF of X where X is a

continuous random variable (or ( ) ( ) ( )1 2 nP X x P X x P X x= = = in the case

where X is a discrete random variable). (2) Take natural logs. This will usually simplify the algebra. (3) Maximise the log-likelihood function. This usually involves differentiating the

log-likelihood function with respect to each of the unknown parameters, and setting the resulting expression(s) equal to zero.

(4) Solve the resulting equation(s) to find the MLEs of the parameters. Check that the values you have found do maximise the likelihood function. This will usually involve differentiating a second time. Note that where there are two or more parameters to estimate, checking for a maximum is complicated and is very unlikely to be required for the Subject CT6 exam. We will now look at the distributions described above and consider how the parameters can be estimated in each case.

3.3 The exponential and gamma distributions

It is possible to use the method of maximum likelihood (ML) or the method of moments to estimate the parameter of the exponential distribution.

Page 18 CT6-03: Loss distributions

IFE: 2014 Examinations The Actuarial Education Company

Example An insurance company uses an exponential distribution to model the cost of repairing insured vehicles that are involved in accidents. Find the maximum likelihood estimate of the mean cost, given that the average cost of repairing a sample of 1,000 vehicles was £2,200. Solution Let X X Xn1 2, , , denote the individual repair costs (where n 1 000, ).

The likelihood of obtaining these values for the costs, if they come from an exponential distribution with parameter is:

L e e ex

i

nn x n nxi i

1

(where xn

xii

n

1

1

denotes the average claim amount).

To find the MLE, we need to find the value of that maximises the likelihood, or, alternatively, the value that maximises the log-likelihood:

log logL n n x

Differentiating to look for stationary points:

log Ln

n x

Setting this to zero gives:

/ 1 x ie / , 1 2 200

The second derivative is

2

2 20log L

n , which shows that this is a maximum.

Alternatively you can note that the likelihood function is continuous and is always

positive (by necessity) and that n n xe 0 as 0 or . So any stationary point that we find must be a maximum.

CT6-03: Loss distributions Page 27

The Actuarial Education Company IFE: 2014 Examinations

5 Mixture distributions

The exponential distribution is one of the simplest models for insurance losses. Suppose that each individual in a large insurance portfolio incurs losses according to an exponential distribution. What we’re thinking of here is that the amounts of Mr Ferrari’s insurance claims over a period of years can be assumed to have an exponential distribution with a certain value of . Practical knowledge of almost any insurance portfolio reveals that the means of these various distributions will differ among the policyholders. Thus the description of the losses in the portfolio is that each loss follows its own exponential distribution, ie the exponential distributions have means that differ from individual to individual. So, although Mr Trabant’s claims also have an exponential distribution, the value of is different for him. So rather than having identically distributed claim amounts X Exp~ ( ) , what we have are claim amounts whose distributions are conditional on

the value of , ie X Exp| ~ ( ) .

A description of the variation among the individual means must now be found. One way to do this is to assume that the exponential means themselves follow a distribution. In the exponential case, it is convenient to make the following assumption. Let i = 1 / i be the reciprocal of the mean loss for the i-th

policyholder. Assume that the variation among the i can be described by a

known gamma distribution Ga( , ) , ie assume that ~ ( , )Ga where

f ( )( )

exp( )

1 , 0 .

Take particular note that this is a PDF in with known values of and .

(There are no x ’s in the above PDF.) This formulation has much in common with that used in Bayesian estimation. Indeed, the fundamental idea in Bayesian estimation is that the parameter of interest (here, ) can be treated as a random variable with a known distribution.

Notice, however, that the purpose here is not to estimate the individual i , but

to describe the aggregate losses over the whole portfolio.

Page 28 CT6-03: Loss distributions

IFE: 2014 Examinations The Actuarial Education Company

Estimation of the individual i can be treated by Bayesian estimation, when the

Ga( , ) distribution would be referred to as a prior distribution. In this problem

of describing the losses over the whole portfolio, the Ga( , ) distribution is

used to average the exponential distributions; the Ga( , ) distribution is

referred to as the mixing distribution and the resulting loss distribution as a mixture distribution. So we are trying to achieve something different from what we achieved in Chapter 2. There we were looking for a point estimate of the parameter value, using information from a prior distribution as well as from our random sample. Here we are trying to find the overall distribution of the actual claim amounts, assuming the given make-up of the different values for different policies in the portfolio. The random variable X represents the amount of a single randomly selected claim and E X( ) represents the mean claim amount for all risks in the portfolio.

To find the overall distribution of claim amounts, we need to work out the marginal distribution of X . This is obtained by integrating the joint density function f X , over

all possible values of . The PDF of the mixture (or marginal) distribution of X is

( )Xf x = •Ú ,0

( , )Xf x dl l l

= •

ΩÚ0 ( ) ( | )X

f f x dl ll l l

= •

- - ¥ -Ú 1

0

exp( ) exp( )( )

x da

ad l dl l l laG

= •

- +Ú0

exp ( ) ( )

x da

ad l d l laG

We now make the integrand look like the PDF of a ( )+ +1,Ga xa d distribution:

( )Xf x = ++¥

+ 1

( 1)

( ) ( )x

a

ad aa d

GG

( )( )

• ++- +

+Ú1

0

exp ( ) 1

xx d

aad

l d l laG

CT6-03: Loss distributions Page 29

The Actuarial Education Company IFE: 2014 Examinations

Integrating the PDF over all possible values of l will give us 1, so that

( )Xf x = ++¥

+ 1

( 1)

( ) ( )x

a

ad aa d

GG

= ++ 1( )x

a

aadd

, > 0x

which can be recognised as the PDF of the Pareto distribution, Pa( , ) . This

result gives a very nice interpretation of the Pareto distribution: Pa( , ) arises

when exponentially distributed losses are averaged using a Ga( , ) mixing

distribution. In order to see what is going on here, you might like to compare this with the corresponding process for finding an unconditional probability from a conditional one in the discrete case. In order to calculate an unconditional probability P X( ) , we can

write: P X x P X x Y y P Y y P X x Y y P Y y( ) ( | ) ( ) ( | ) ( ) 1 1 2 2

where the summation is taken over all possible values of Y . Here we carry out the same process, except that probabilities are replaced by probability density functions, and summation is replaced by integration. The parameter can take any value in a continuous range of possibilities, so we integrate over all possible values. Example Another generalisation of the Pareto distribution uses the idea of a mixture distribution discussed earlier. We’ve seen that if losses are exponential with mean 1/ l and ~ ( , )Gal a d , then the mixture distribution of losses is ( , )Pa a d .

This can be generalised if it is assumed that the losses are ( , )Ga k l and

~ ( , )Gal a d . If = 1k then losses are exponential with mean 1/ l since

( ) ( )∫1, 1/Ga Expl l and the ( , )Pa a d mixture distribution is obtained exactly as

before.

Page 30 CT6-03: Loss distributions

IFE: 2014 Examinations The Actuarial Education Company

For general k , the PDF of the mixture distribution of the loss, X , is

( )Xf x = •

ΩÚ0 ( ) ( | )X

f f x dl ll l l

= • - -- ¥ -Ú 1 1

0exp( ) exp( )

( ) ( )

kkx x d

k

aad ll dl l l

aG G

= - • + - - +Ú

11

0exp( ( ) )

( ) ( )

kkx

x dk

aad l d l l

aG G

We now make the integrand look like the PDF of a ( )+ +,Ga k xa d distribution:

( )Xf x = ( )

( )( )

( )+- • + -

++ +

- +++ Ú

11

0exp( ( ) )

( ) ( )

kkk

k

k xxx d

k kx

aaa

aa dd l d l l

a ad

GG G G

Integrating the PDF over all possible values of l will give us 1, so that

( )Xf x = -

++ >

+

1( ), 0

( ) ( ) ( )

k

k

k xx

k x

a

aa da d

GG G

which can be recognised as the PDF of the generalised Pareto distribution,

( ), ,Pa ka d .

In the Tables the parameter is called . This is the situation referred to in Section 2.1. If we regard the generalised Pareto as the result of mixing together Gamma k( , ) distributions whose parameters come from a

Gamma( , ) distribution, then we can find the mean of the generalised Pareto by

calculating:

1

0

1( )

( )

kE X e da a d ld l l

l a

•- -= ¥

GÚ

where k / is the mean of the Gamma k( , ) distribution.

If you follow the algebra through (use the usual procedure of making the integral look

like another gamma distribution), you should find that you get the formula k 1

as

required.

CT6-03: Loss distributions Page 30a

The Actuarial Education Company IFE: 2014 Examinations

Question 3.15

The annual number of claims from an individual policy in a portfolio has a Poisson( )

distribution. The variability in among policies is modelled by assuming that over the portfolio, individual values of have a Gamma( , ) distribution. Derive the mixture

distribution for the annual number of claims from each policy in the portfolio.

Question 3.16

Claim numbers from individual policies in a portfolio have a Bin n p( , ) distribution. The

parameter p varies over the portfolio with a Beta( , ) distribution. Find the mixture

distribution.

Page 30b CT6-03: Loss Distributions

IFE: 2014 Examinations The Actuarial Education Company

This page has been deliberately left blank

CT6-03: Loss distributions Page 33

The Actuarial Education Company IFE: 2014 Examinations

Chapter 3 Summary Loss distributions Individual claim amounts can be modelled using a loss distribution. Loss distributions are often positively skewed and long-tailed. The (cumulative) distribution function of X is denoted by F xX ( ) . It is defined by the

equation: F x P X xX ( ) ( ) .

The (probability) density function of X is denoted by f xX ( ) . It is defined by the

equation: f x F xX X( ) ( ) , wherever this derivative exists.

Distributions such as the exponential, normal, lognormal, gamma, Pareto, generalised Pareto, Burr or Weibull distribution are commonly used to model individual claim amounts. Once the form of the loss distribution has been decided upon, the values of the parameters must be estimated. This may be done using the method of maximum likelihood, the method of moments or the method of percentiles. Goodness of fit can then be checked using a chi square test. Method of maximum likelihood The steps involved in finding a maximum likelihood estimate (MLE) are as follows: (1) Write down the likelihood function for the available data. (2) Take natural logs. This will usually simplify the algebra. (3) Maximise the log-likelihood function. This usually involves differentiating the

log-likelihood function with respect to each of the unknown parameters, and setting the resulting expression(s) equal to zero.

(4) Solve the resulting equation(s) to find the MLEs of the parameters. (5) Differentiating the log-likelihood function a second time to check that the estimates are indeed maxima.

Page 34 CT6-03: Loss distributions

IFE: 2014 Examinations The Actuarial Education Company

Method of moments The method of moments involves equating population and sample moments to solve for the unknown parameter values. For example, if there is just one parameter to estimate, we could equate the population mean with the sample mean. If there are two parameters to estimate, we could equate the first two non-central population moments with the equivalent non-central sample moments. Equivalently, we could equate the first two central population moments with the equivalent central sample moments, noting that (for equivalence) we would need to use the n-denominator sample variance. Method of percentiles The method of percentiles involves equating population and sample percentiles to solve for the unknown parameter values. For example, if there is just one parameter to estimate, we could equate the population median with the sample median. If there are two parameters to estimate, we could equate the population lower and upper quartiles with the sample lower and upper quartiles. Mixture distributions Let X be a random variable representing losses on an insurance portfolio. Suppose that the distribution of X depends on the value of an unknown parameter l where l is itself a random variable. For example l may vary by policyholder. The mixture distribution of X is also known as the marginal or unconditional distribution of X. It represents the overall distribution of losses, once the effects of the different l s have been averaged out.

CT6-03: Loss distributions Page 34a

The Actuarial Education Company IFE: 2014 Examinations

Chapter 3 Formulae Moment generating function of X

M t E eXtX( ) ( )

PDF of a mixture (or marginal) distribution

( )Xf x = ( ) ( | )Xall

f f x dl lll l lΩÚ

Gamma distribution Parameters: 0 0,

f x x eXx( )

( )

1 , x 0 X Gamma X~ ( , ) ~ 2 2

2

Note that the exponential distribution is a special case of the gamma distribution where

1a = . Lognormal distribution Parameters: , 0m s-• < < • >

2

12

1 log( ) exp

2X

xf x

x

mss p

È ˘-Ê ˆ= -Í ˙Á ˜Ë ¯Í ˙Î ˚, 0x >

Pareto distribution Parameters: 0, 0a l> >

1( )

( )Xf x

x

a

aal

l +=+

, 0x > ( ) 1XF xx

all

Ê ˆ= - Á ˜Ë ¯+

Page 34b CT6-03: Loss distributions

IFE: 2014 Examinations The Actuarial Education Company

Generalised Pareto distribution Parameters: 0, 0, 0ka l> > >

1( )

( )( ) ( )( )

k

X k

k xf x

k x

a

aa l

a l

-

+G +=

G G +, 0x >

Burr distribution Parameters: 0, 0, 0a l g> > >

1

1( )

( )X

xf x

x

a g

g aagll

-

+=+

, 0x > ( ) 1XF xx

a

gl

lÊ ˆ= - Á ˜Ë ¯+

Weibull distribution Parameters: 0, 0c g> >

1( ) cx

Xf x c x eggg - -= , 0x > ( ) 1 cx

XF x eg-= -

CT6-04: Reinsurance Page 5

The Actuarial Education Company IFE: 2014 Examinations

So the graph looks like this:

We are now in a position to consider the statistical calculations relating to reinsurance arrangements.

1.1 Excess of loss reinsurance

In excess of loss reinsurance, the insurer will pay any claim in full up to an amount M, the retention level; any amount above M will be borne by the reinsurer. In this section “the company” refers to the direct writer. The excess of loss reinsurance arrangement can be written in the following way: if the claim is for amount X then the insurer will pay Y where: Y = X if X M Y = M if X M . The reinsurer pays the amount Z X Y .

Question 4.1

Write down an expression for Y if only a layer between M and 2 M is reinsured.

Page 6 CT6-04: Reinsurance

IFE: 2014 Examinations The Actuarial Education Company

The insurer’s liability is affected in two obvious ways by reinsurance: (i) the mean amount paid is reduced; (ii) the variance of the amount paid is reduced. Both these conclusions are simple consequences of the fact that excess of loss reinsurance puts an upper limit on large claims. The mean amounts paid by the insurer and the reinsurer under excess of loss reinsurance can now be obtained. Observe that the mean amount paid by the insurer without reinsurance is

E(X) = •Ú0 ( )x f x dx (1.1)

where ( )f x is the PDF of the claim amount X. With a retention level of M the

mean amount paid by the insurer becomes

= + >Ú0( ) ( ) P( )M

E Y xf x dx M X M . (1.2)

This is because 0

( ) ( ) ( )M

M

E Y x f x dx M f x dx•

= +Ú Ú , from the definition of Y .

Similarly, we can calculate ( )2E Y using:

( )

( )

2 2 2

0

2 2

0

( ) ( )

( )

M

M

M

E Y x f x dx M f x dx

x f x dx M P X M

•

= +

= + >

Ú Ú

Ú

Then ( ) ( ) ( ) 22var Y E Y E YÈ ˘= - Î ˚ .

More generally, the moment generating function of Y, the amount paid by the insurer, is

( )YM t = ( )tYE e = + >Ú0 ( ) P( ).M tx tMe f x dx e X M

CT6-04: Reinsurance Page 7

The Actuarial Education Company IFE: 2014 Examinations

Question 4.2

Find ( )E Y when X has a Pareto distribution with parameters 200 and 6, and

M 80 .

Under excess of loss reinsurance, the reinsurer will pay Z where: Z = 0 if X M£ Z = X–M if X M> . With a retention level of M the mean amount paid by the reinsurer becomes:

( )( ) ( )M

E Z x M f x dx•

= -Ú , from the definition of Z (1.3)

Similarly, we can calculate ( )2E Z using:

( ) ( )22 ( )M

E Z x M f x dx•

= -Ú

Then ( ) ( ) ( ) 22var Z E Z E ZÈ ˘= - Î ˚ .

More generally, the moment generating function of Z , the amount paid by the reinsurer, is:

( ) ( ) ( )0

0( ) ( )

M t x MtZ tZ M

M t E e e f x dx e f x dx• -= = +Ú Ú

Page 8 CT6-04: Reinsurance

IFE: 2014 Examinations The Actuarial Education Company

1.2 The reinsurer’s conditional claims distribution

Now consider reinsurance (once again) from the point of view of the reinsurer. The reinsurer may have a record only of claims that are greater than M. If a claim is for less than M the reinsurer may not even know a claim has occurred. The reinsurer thus has the problem of estimating the underlying claims distribution when only those claims greater than M are observed. The statistical terminology is to say that the reinsurer observes claims from a truncated distribution. In this case the values observed by the reinsurer relate to a conditional distribution, since the numbers are conditional on the original claim amount exceeding the retention limit. Let W be the random variable with this truncated distribution. Then: = - >|W X M X M

Suppose that the underlying claim amounts have PDF f x( ) and CDF F x( ) .

Suppose that the reinsurer is only informed of claims greater than the retention M and has a record of w = x M. What is the PDF g(w) of the amount, w, paid by the reinsurer? The argument goes as follows:

(using Bayes' Formula)

(using the definition of the CDF)

( ) ( | )

( )

1 ( )

( ) ( )

1 ( )

w M

M

P W w P X w M X M

f xdx

F M

F w M F M

F M

+

< = < + >

=-

+ -=-

Ú

Differentiating w.r.t. w, the PDF of the reinsurer’s claims is

( )

( )1 ( )

f w Mg w

F M

+=-

, 0w > . (1.4)

Note that this is just the original PDF applied to the gross amount w M+ , divided by the probability that the claim exceeds M .

Question 4.5

Using the notation above, if X is Exp( ) , find the distribution of W.

CT6-04: Reinsurance Page 9

The Actuarial Education Company IFE: 2014 Examinations

Question 4.6

What if ( ),X Pa a l ?

It is also possible that the reinsurer is aware of all the claims that are made under the original policies. In this case the distribution of the reinsurer’s outgo may include those claims on which it does not in fact pay anything. In this case we are looking at the unconditional distribution of the reinsurer’s outgo Z , where:

Z X M

Z X M X M

0

The calculation of the mean and variance of the reinsurer’s outgo in this case will be similar to the corresponding calculations for the insurer.

Example If claims from a portfolio have a N ( , )500 400 distribution, and there is a retention limit

of M 550 , find the mean amount paid by the reinsurer on all claims. Solution

We want 550

0 550

( ) 0 ( ) ( 550) ( )X XE Z f x dx x f x dx•

= ¥ + -Ú Ú , where f xX ( ) is the PDF of

the N ( , )500 400 distribution. The first integral equals zero. Substituting ux

500

20

in the second integral, we get:

[ ]

2

2

1

2

2.5

1

2

2.5

1( ) (20 50)

2

120 50 1 (2.5) 0.0401

2

u

u

E Z u e du

e

p

p

• -

•-

= -

È ˘Í ˙= - - -F =Í ˙Î ˚

Ú

The first term in square brackets can be evaluated directly.

We will give some general formulae later in this chapter which will enable us to calculate these types of integrals relatively quickly.

Page 10 CT6-04: Reinsurance

IFE: 2014 Examinations The Actuarial Education Company

If we now use W to denote the amount payable by the reinsurer on claims in which it is involved, ie W Z Z X M X M | |0 , then:

E WE Z

P Z

E Z

P X M( )

( )

( )

( )

( )

0

This follows from equation (1.4).

1.3 Proportional reinsurance

In proportional reinsurance the insurer pays a fixed proportion of the claim, whatever the size of the claim. Using the same notation as above, the proportional reinsurance arrangement can be written as follows: if the claim is for an amount X then the company will pay Y where Y X 0 1 . The parameter is known as the retained proportion or retention level; note that the term retention level is used in both excess of loss and proportional reinsurance though it means different things. As the amount paid by the insurer on a claim X is =Y Xa and the amount paid

by the reinsurer is ( )= -1Z Xa , the distribution of both of these amounts can be

found by a simple change of variable.

Question 4.7

Claims occur as a generalised Pareto distribution with parameters 6, 200 and k 4 . A proportional reinsurance arrangement is in force with a retained proportion of 80%. Find the mean and variance of the amount paid by the insurer and the reinsurer on an individual claim.

CT6-04: Reinsurance Page 23

The Actuarial Education Company IFE: 2014 Examinations

And for Year 2:

6

21210 1210 1710

( ) 199.075 1710 5

E YÊ ˆ= - ¥ =Á ˜Ë ¯

So the percentage increase from Year 0 to Year 1 is 7.2%, and the percentage increase from Year 1 to Year 2 is 6.9%.

Note that these figures are less than 10%, as expected.

Question 4.15

What is the limit of ( )nE Y as n tends to infinity?

Page 24 CT6-04: Reinsurance

IFE: 2014 Examinations The Actuarial Education Company

4 Estimation

Consider the problem of estimation in the presence of excess of loss reinsurance. Suppose that the claims record shows only the net claims paid by the insurer. A typical claims record might be x x M x M x x1 2 3 4 5, , , , , , , ... (4.1)

and an estimate of the underlying gross claims distribution is required. As before, we wish to estimate the parameters for the distribution we’ve assumed for the claims. The method of moments is not available since even the mean claim amount cannot be computed. On the other hand, it may be possible to use the method of percentiles without alteration; this would happen if the retention level M is high and only the higher sample percentiles were affected by the (few) reinsurance claims. The statistical terminology for a sample of the form (4.1) is censored. In general, a censored sample occurs when some values are recorded exactly and the remaining values are known only to exceed a particular value, here the retention level M. Maximum likelihood can be applied to censored samples. The likelihood function is made up of two parts. If the values of 1 2, , ... , nx x x are recorded

exactly these contribute a factor of

11

( ) ( ; )n

iL f xq qP=

If a further m claims are referred to the reinsurer, then the insurer records a payment of M for each of these claims. These censored values then contribute a factor

21

( ) Pr( )m

L X Mq P= > ie [Pr( )]mX M>

The complete likelihood function is

P1

( ) ( ; ) [1 ( ; )]n

miL f x F Mq q q= ¥ -

where F(.; ) is the CDF of the claims distribution.

CT6-04: Reinsurance Page 31

The Actuarial Education Company IFE: 2014 Examinations

Chapter 4 Summary Reinsurance Reinsurance is insurance for insurance companies. By using reinsurance, the insurer seeks to protect itself from large claims. The mean amount paid by the insurer is reduced, and the variance of the amount paid by the insurer is reduced. Reinsurance may be proportional or non-proportional (ie individual excess of loss). Proportional reinsurance Under proportional reinsurance, the insurer and the reinsurer split the claim in pre-defined proportions. For a claim amount X , the amount paid by the insurer is Y Xa= and the

amount paid by the reinsurer is ( )1Z Xa= - where a is known as the retained

proportion or retention level, 0 1a< < . Non-proportional reinsurance (individual excess of loss) Under individual excess of loss, the insurer will pay any claim in full up to an amount M , the retention level; any amount above M will be met by the reinsurer. For a claim amount, X , the amount paid by the insurer is:

X if X M

YM if X M

£Ï= Ì >Ó

The amount paid by the reinsurer is:

0 if X M

ZX M if X M

£Ï= Ì - >Ó

Page 32 CT6-04: Reinsurance

IFE: 2014 Examinations The Actuarial Education Company

Reinsurer’s conditional claims distribution It may be the case that the reinsurer is only informed of claims greater than the retention level M . In this case, the reinsurer observes claims from a truncated (or conditional) distribution. Let W be the random variable associated with this distribution, then: | 0 |W Z Z X M X M= > = - >

The PDF of the reinsurer’s conditional distribution is given by:

( )

( )1 ( )

XW

X

f w Mg w

F M

+=-

Excesses When a policy excess applies, the policyholder pays for the first part of each loss up to an excess level L ; any amount greater than L will be met by the insurer. The positions of the policyholder and the insurer as far as losses are concerned are the same as those of the insurer and the reinsurer respectively under individual excess of loss reinsurance. When a policy excess applies, the insurer’s conditional distribution takes the same form as that of the reinsurer’s conditional distribution above. Inflation and individual excess of loss reinsurance If claims are inflated by a factor of k but the retention level remains fixed at M then the amount paid by the insurer is:

kX if kX M

YM if kX M

£Ï= Ì >Ó

The amount paid by the reinsurer is:

0 if kX M

ZkX M if kX M

£Ï= Ì - >Ó

CT6-04: Reinsurance Page 33

The Actuarial Education Company IFE: 2014 Examinations

Chapter 4 Formulae Claim amounts paid by insurer and reinsurer

Suppose that X is the amount of an original claim having PDF ( )Xf x , Y is the amount

paid by the insurer and Z X Y= - is the amount paid by the reinsurer. Under a proportional reinsurance treaty with a retained proportion of :

[ ]

2

3

3

3/ 2 3/ 22

( ) ( )

var( ) var( )

skew( ) skew( )

skew( ) skew( )( ) ( )

var( ) var( )

E Y E X

Y X

Y X

Y XCoeff of skew Y Coeff of skew X

Y X

a

a

a

a

a

=

=

=

= = =È ˘Î ˚

Under an individual excess of loss treaty with a retention level of M :

X if X M

YM if X M

£Ï= Ì >Ó

and 0 if X M

ZX M if X M

£Ï= Ì - >Ó

We have:

( )0

0

( ) ( ) ( )

( ) 1

MX XM

MX

E Y x f x dx M f x dx

x f x dx M F M

•= +

È ˘= + -Î ˚

Ú ÚÚ

( ) ( )2 2 2

0( ) 1

MXE Y x f x dx M F MÈ ˘= + -Î ˚Ú

( ) ( ) ( ) 22var Y E Y E YÈ ˘= - Î ˚

( ) ( ) ( )0

( ) 1MtY tx tM

Y XM t E e e f x dx e F MÈ ˘= = + -Î ˚Ú

Page 34 CT6-04: Reinsurance

IFE: 2014 Examinations The Actuarial Education Company

And:

( )( ) ( )XME Z x M f x dx

•= -Ú

( ) ( )22 ( )XME Z x M f x dx

•= -Ú

( ) ( ) ( ) 22var Z E Z E ZÈ ˘= - Î ˚

( ) ( ) ( )0

( ) ( )M t x MtZ

Z X XMM t E e f x dx e f x dx

• -= = +Ú Ú

Note that ( ) ( ) ( )E X E Y E Z= + but var( ) var( ) var( )X Y Zπ + since Y and Z are not

independent. If X takes a lognormal or normal distribution, the following results will help with the integration: Lognormal distribution

2 2½( ) [ ( ) ( )]U

k k kX k k

L

x f x dx e U Lm s+= F -FÚ

where log

kL

L km s

s-= - and

logk

UU k

m ss-= -

( ) 0F -• = (0) ½F = ( ) 1F • =

Normal distribution

( ) [ ( ) ( )] [ ( ) ( )]U

XL

x f x dx U L U Lm s f f= F -F - -¢ ¢ ¢ ¢Ú

where

LL

and

UU

( ) ( ) 0

CT6-04: Reinsurance Page 34a

The Actuarial Education Company IFE: 2014 Examinations

Distribution of reinsurer’s claim amounts on claims in which it is involved Let |W X M X M= - > , so that W represents the amount paid by the reinsurer given

that the reinsurer is involved in the claim. Then the PDF of W is:

( )( )

1 ( )X

WX

f w Mg w

F M

+=-

and: ( )

( )( 0)

E ZE W

P Z=

> where:

0 if

if

X MZ

X M X M

£Ï= Ì - >Ó

Using the PDF above of W it can be shown that: 1. if ~ ( )X Exp l , then |X M X M- > is ( )Exp l

2. if ~ ( , )X Pareto a l , then |X M X M- > is ( , )Pareto Ma l + .

Estimation of parameters from a censored sample

The likelihood function of a vector of parameters q , based on a sample of n exact

observations and m censored observations known to exceed M is:

[ ]1

( ) ( ) ( )n

mX i

i

L f x P X Mq=

È ˘= >Í ˙Í ˙Î ˚’

assuming that the observations are realisations of n m+ IID random variables.

Page 34b CT6-04: Reinsurance

IFE: 2014 Examinations The Actuarial Education Company

This page has been left blank so that you can keep the chapter summaries

together as a revision tool.

CT6-05: Credibility theory Page 27

The Actuarial Education Company IFE: 2014 Examinations

Chapter 5 Summary Direct vs collateral data Claim numbers or aggregate claim amounts can be estimated using a combination of direct data (ie data from the risk under consideration) and collateral data (ie data from other similar, but not necessarily identical, risks). Credibility premium and credibility factor

Let X be an estimate of the expected number of claims/aggregate claim amount for a particular risk for the coming year based on direct data. Let m be an estimate of the expected number of claims/aggregate claims for a particular

risk for the coming year based on collateral data. The credibility premium (or credibility estimate of the number of claims/aggregate claim amount) for this risk is:

( )1CP ZX Z m= + -

where Z is a number between 0 and 1 and is known as the credibility factor. The closer it is to 1, the more weight is given to the direct data. The problem remains as to how to calculate Z . There are two approaches: Bayesian credibility and empirical Bayes credibility theory (EBCT). Bayesian credibility The problem of interest is to estimate a parameter (for example a parameter representing the mean number of claims or mean claim amount) and then to express the estimator as a credibility premium. Following the approach developed in Chapter 2, we combine the prior PDF and the likelihood of the sample data using Bayes’ formula to obtain the posterior PDF. A Bayesian estimator of the parameter is obtained to minimise the expected value of some loss function.

Page 28 CT6-05: Credibility theory

IFE: 2014 Examinations The Actuarial Education Company

The Bayesian estimator is then shown to be in the form of a credibility premium:

Bayesian estimator = ( )1CP ZX Z m= + -

where X is the MLE of the parameter based on the sample data and m is an estimator

based on the prior distribution. Z is the credibility factor, a number between 0 and 1 that shows how much weight the Bayesian estimator places on the sample data and how much on the prior distribution. Example formulae are given for the following three models (combinations of likelihood and prior) on the next page:

1. Poisson/gamma model

2. Normal/normal model

3. Binomial/beta model.

CT6-05: Credibility theory Page 28a

The Actuarial Education Company IFE: 2014 Examinations

Chapter 5 Formulae Credibility formula

P Z X Z ( )1

Poisson/gamma model Definitions: X j represents the number of claims in the j th year

Prior distribution: ~ ( , )Gamma

Likelihood: X Poissonj | ~ ( )

Posterior: | ~ ( , )ix Gamma x nl a b+ +Â

Credibility factor: Zn

n

Credibility premium: ( ) (1 )n X

E X Z X Zn

a alb b+= = + -+

Normal/normal model

Definitions: X j represents the (total) claim amount in the j th year

Prior distribution: ~ ( , )N 22

Likelihood: X Nj | ~ ( , ) 12 (1

2 constant)

Posterior: 2 2 2 21 2 1 22 2 2 21 2 1 2

| ~ ,n x

x Nn n

ms s s sqs s s s

Ê ˆ+Á ˜+ +Ë ¯

Credibility factor: Zn

n

12

22

Credibility premium: 2 22 12 22 1

( ) (1 )n X

E X Z X Zn

s m sq ms s

+= = + -+

Page 28b CT6-05: Credibility theory

IFE: 2014 Examinations The Actuarial Education Company

Binomial/beta model Definitions: X j represents the number of claims on a portfolio of m policies

in the j th year (j = 1 to n)

Prior distribution: ( ),p beta a b

Note that p is the probability of a claim on a single policy in a single year.

Likelihood: ( )| ,jX p Bin m p

Posterior: 1 1

| ,n n

j jj j

p x Beta x mn xa b= =

Ê ˆ+ + -Á ˜

Ë ¯Â Â

Credibility factor: mn

Zmna b

=+ +

Credibility premium: ( ) ( )| 1j jx x

E p x Z Zmn mn

a aa b a b

+= = + -

+ + +Â Â

Conditional expectation results For any random variables X and Y (for which the relevant moments exist) and for any function f (apart from some special cases of no practical interest):

( ) [ ( | ) ]E X E E X Y=

[ ( ) | ] ( )E f Y Y f Y=

[ ( ) ] [ ( ( ) | ) ] [ ( ) ( | ) ]E X f Y E E X f Y Y E f Y E X Y= =

If two random variables 1X and 2X are conditionally independent given a third random

variable Y , then: 1 2 1 2( | ) ( | ) ( | )E X X Y E X Y E X Y=

CT6-06: Empirical Bayes Credibility theory Page 41

The Actuarial Education Company © IFE: 2014 Examinations

Chapter 6 Summary Empirical Bayes credibility This approach to credibility theory assumes that the number of claims or aggregate claim amount for each risk are dependent on an underlying risk parameter . However, no assumptions are made about the form of the distribution of q . The credibility premium can be expressed in terms of a credibility factor, which depends on the mean and variance of the conditional claim distribution. These quantities can be estimated based on data derived from a number of different risks. Empirical Bayes Credibility Theory Model 1 Definitions: ijX represents the number of claims (or aggregate claim amount)

for risk ( 1... )i i n= in year ( 1... )j j N= .

Assumptions: For each risk i , the distribution of ijX depends on a parameter iq

whose value is the same for each j but is unknown.

|ij iX q are i.i.d random variables.

iq are i.i.d random variables.

For i kπ , the pairs ( ),ij iX q and ( ),km kX q are i.i.d random

variables.

There exist functions ( )m and ( )2s such that:

( ) ( )2( ) | ( ) var |i ij i ijm E X s Xq q q q= = .

Estimators: Unbiased estimators for ( )E m qÈ ˘Î ˚ , ( )2E s qÈ ˘Î ˚ and ( )var m qÈ ˘Î ˚ are

given on Page 29 of the Tables.

Credibility factor:

[ ]2( )

var ( )

nZ

E sn

m

=Ê ˆÈ ˘

Î ˚Á ˜+Á ˜Ë ¯

Credibility premium: We are trying to estimate ( )im q given X . The estimator, or

credibility premium is ( )1iZ X Z X+ - .

Page 42 CT6-06: Empirical Bayes Credibility theory

© IFE: 2014 Examinations The Actuarial Education Company

Empirical Bayes Credibility Theory Model 2

Definitions: ijY represents the number of claims (or aggregate claim amount)

for risk ( 1... )i i n= in year ( 1... )j j N= .

ijP represents the corresponding risk volume (eg number of

policies or premium income). The ijP ’s are assumed to be known.

/ij ij ijX Y P=

Assumptions: For each risk i , the distribution of ijX depends on a parameter iq

whose value is the same for each j but is unknown.

|ij iX q are independent random variables.

iq are i.i.d random variables.

For i kπ , the pairs ( ),ij iX q and ( ),km kX q are independent

random variables.

There exist functions ( )m and ( )2s such that:

( ) ( )2( ) | ( ) var |i ij i ij ijm E X s P Xq q q q= =

Estimators: Unbiased estimators for ( )E m qÈ ˘Î ˚ , ( )2E s qÈ ˘Î ˚ and ( )var m qÈ ˘Î ˚ are

given on Page 30 of the Tables.

Credibility factor:

[ ]

1

2

1

( )

var ( )

n

ijj

in

ijj

P

ZE s

Pm

=

=

=Ê ˆÈ ˘

Î ˚Á ˜+Á ˜Ë ¯

Â

Â

Credibility premium: We are trying to estimate ( )im q given X . The estimator, or

credibility premium is ( )1i i iZ X Z X+ - .

CT6-07: Risk models (1) Page 19

The Actuarial Education Company IFE: 2014 Examinations

The next three sections consider compound distributions using various models for the number of claims, N. Of the three types of compound distribution described, the compound Poisson is the one that has been asked about most often in past examination questions. However, they are all important. Note that the compound geometric distribution mentioned in the syllabus item is just a specific example of a compound negative binomial distribution.

3.4 The compound Poisson distribution

First consider aggregate claims when N has a Poisson distribution with mean

denoted ( )N Poi l . S then has a compound Poisson distribution with

parameter , and F x( ) is the CDF of the individual claim amount random

variable. F x( ) here represents a general distribution for the individual claim amounts.

The results required for this distribution for N are:

= =[ ] var[ ]E N N l

M t eNt( ) exp ( ) 1

Note that these results are given in the Tables. Check that you can derive them. These results can be combined with those of Section 3.1 as follows: from (3.3), E S m[ ] 1 (3.8)

from (3.4), = 2var[ ]S ml (3.9)

ie ( )m m m2 12

12

Page 20 CT6-07: Risk models (1)

IFE: 2014 Examinations The Actuarial Education Company

and from (3.7), M t M tS X( ) exp ( ( ) ) 1 (3.10)

The results for the mean and variance have a very simple form. Note that the variance of S is expressed in terms of the second moment of X i about zero (and

not in terms of the variance of X i ).

Note also that the formula for the skewness of S has a simple form when S is a compound Poisson random variable: = 3[ ]skew S ml (3.11)

In order to find the skewness of a compound Poisson distribution, we need to use cumulant generating functions (CGFs). These were covered in Subject CT3, but we provide the theory required again here. The cumulant generating function ( )XC t is defined by:

( ) log ( )X XC t M t=

Mean, variance and skewness in terms of ( )C tX

CGF Results If the cumulant generating function of a random variable X is ( )XC t , then:

( ) (0)XE X C= ¢ var( ) (0)XX C= ¢¢ skew( ) (0)XX C= ¢¢¢

The CGF of X is: ( ) log ( )X XC t M t=

Differentiating this using the chain rule (or function-of-a-function rule):

1 ( )( ) ( )

( ) ( )X

X XX X

M tC t M t

M t M t

¢= ¥ =¢ ¢

Putting t 0 :

(0) ( )(0) ( )

(0) 1X

XX

M E XC E X

M

¢= = =¢

CT6-07: Risk models (1) Page 21

The Actuarial Education Company IFE: 2014 Examinations

Differentiating again, using the product rule and the chain rule:

2

2 2

1 ( ) ( ) [ ( )]( ) ( ) ( )

( ) ( )[ ( )] [ ( )]X X X

X X XX XX X

M t M t M tC t M t M t

M t M tM t M t

- ¢ ¢¢ ¢= ¥ + ¥ = -¢¢ ¢¢ ¢

Putting t 0 :

22 2

2

(0) [ (0)](0) ( ) [ ( )] var( )

(0) [ (0)]X X

XX X

M MC E X E X X

M M

¢¢ ¢= - = - =¢¢

Differentiating again, and simplifying, gives:

3

2 3

( ) ( ) ( ) [ ( )]( ) 3 2

( ) [ ( )] [ ( )]X X X X

XX X X

M t M t M t M tC t

M t M t M t

¢¢¢ ¢¢ ¢ ¢= - +¢¢¢

Putting t 0 :

3

2 3

3 2 3

(0) (0) (0) [ (0)](0) 3 2

(0) [ (0)] [ (0)]

( ) 3 ( ) ( ) 2[ ( )] skew( )

X X X XX

X X X

M M M MC

M M M

E X E X E X E X X

¢¢¢ ¢¢ ¢ ¢= - +¢¢¢

= - + =

Using these results, we can show that the skewness of the compound Poisson distribution is m3 .

An alternative approach would be to expand log ( )t XE e as a power series and look at the

coefficients of individual terms. The easiest way to show that the third central moment of S is m3 is to use the cumulant generating function: =( ) log ( )S SC t M t

To determine the skewness, we differentiate it three times with respect to t and set = 0t , ie:

E S md

dtM tS t[( ) ] log ( )| 1

33

3 0

Page 22 CT6-07: Risk models (1)

IFE: 2014 Examinations The Actuarial Education Company

Now ( )log ( ) ( ) 1S XM t M tl= - , so:

0

3 3

33 3log ( ) ( ) 1

t

S Xd d

M t M t mdt dt

l l=

È ˘= - =Í ˙

Í ˙Î ˚

This is because 3(0) ( )XM E X=¢¢¢ for any random variable.

ie E S m m[( ) ] 13

3

and the coefficient of skewness = m m3 23 2/ ( ) / .

For the compound Poisson it is worth remembering the formulae m1 , m2 and m3

for the mean, variance and skewness. However, they are given in the Tables. This result shows that the distribution of S is positively skewed, since m3 is the

third moment about zero of Xi and hence is greater than zero because Xi is a

non-negative valued random variable. Note that the distribution of S is positively skewed even if the distribution of Xi is negatively skewed. The coefficient of

skewness of S is m m3 23 2/ ( ) / , and hence goes to 0 as . Thus for large

values of , the distribution of S is almost symmetric.

Sums of compound Poisson distributions A very useful property of the compound Poisson distribution is that the sum of independent compound Poisson random variables is itself a compound Poisson random variable. A formal statement of this property is as follows. Let S1, S2, ..., Sn be independent random variables. Suppose that each Si has a

compound Poisson distribution with parameter i , and that the CDF of the

individual claim amount random variable for each iS is F xi ( ) .

Define A = S1 + S2 + + Sn. Then A has a compound Poisson distribution with

parameter , and F x( ) is the CDF of the individual claim amount random

variable for A , where:

ii

n

1

and F x F xi ii

n

( ) ( )1

1

is just the capital form of the Greek letter .

CT6-07: Risk models (1) Page 23

The Actuarial Education Company IFE: 2014 Examinations

This is a very important result. To prove the result, first note that F(x) is a weighted average of distribution functions and that these weights are all positive and sum to one. This means that F(x) is a distribution function and this distribution has MGF:

•

== ÂÚ0

1

1( ) exp( ) ( )

n

i ii

M t tx f x dxlL

where fi(x) is the density of Fi(x). Hence:

•

= == =Â ÂÚ0

1 1

1 1( ) exp ( ) ( )

n n

i i i ii i

M t tx f x dx M tl lL L

(3.12)

where Mi(t) is the MGF for the distribution with CDF Fi(x).

Let MA(t) denote the MGF of A. Then:

MA(t) = E[exptA] = E[exptS1 + tS2 + + tSn]

By independence of Si in1:

=

=’1

( ) (exp )n

A ii

M t E tS

As Si is a compound Poisson random variable, its MGF is of the form given by

formula (3.10), so:

E tS M ti i i[exp ] exp ( ( ) ) 1

Thus:

1 1

( ) exp ( ( ) 1) exp ( ( ) 1)nn

A i i i ii i

M t M t M tl l= =

Ï ¸Ô Ô= - = -Ì ˝Ô ÔÓ ˛Â’

ie M t M tA( ) exp ( ( ) ) 1 (3.13)

where ii

n

1

and M t M ti ii

n

( ) ( )1

1

.

Page 24 CT6-07: Risk models (1)

IFE: 2014 Examinations The Actuarial Education Company

By the one-to-one relationship between distributions and MGFs, formula (3.13) shows that A has a compound Poisson distribution with Poisson parameter . By (3.12), the individual claim amount distribution has CDF F(x).

Question 7.8

The distributions of aggregate claims from two risks, denoted by S1 and S2 , are as

follows: S1 has a compound Poisson distribution with parameter 100 and distribution

function F x x1 1( ) exp( / ) , x 0 and S2 has a compound Poisson distribution

with parameter 200 and distribution function F x x x2 1 0( ) exp( / ), . If S1 and

S2 are independent, what is the distribution of S S1 2 ?

3.5 The compound binomial distribution

Under certain circumstances, the binomial distribution is a natural choice for N. For example, under a group life insurance policy covering n lives, the distribution of the number of deaths in a year is binomial if it is assumed that each insured life is subject to the same mortality rate, and that lives are independent with respect to mortality. The notation N ~ bin(n, p) is used to denote the binomial distribution for N. The key results for this distribution are:

E[N] = np

var[N] = np(1 p)

MN (t) = (pet + 1 p)n

Note that these results are given in the Tables. However, the notation for the MGF is slightly different. Again, check that you can derive the results for yourself. When N has a binomial distribution, S has a compound binomial distribution. One important point about choosing the binomial distribution for N is that there is an upper limit, n, to the number of claims. Expressions for the mean, variance and MGF of S are now found in terms of n, p, m1, m2 and MX (t) when N ~ bin(n, p).

CT6-07: Risk models (1) Page 25

The Actuarial Education Company IFE: 2014 Examinations

We wouldn’t recommend you to learn the formulae in this section. But make sure you know how to derive them. Formulae (3.3) and (3.4) give the mean and variance: = 1[ ]E S npm (3.14)

= - + -

= -

2 22 1 1

2 22 1

var[ ] ( ) (1 )S np m m np p m

npm np m (3.15)

Lastly, formula (3.7) gives the MGF:

= + -( ) ( ( ) 1 )nS XM t pM t p

We can also find expressions for the skewness and the coefficient of skewness. The third central moment is found from the cumulant generating function. To do

the next few steps, liberal use is made of the function-of-a-function rule ( )d d dudx du dx= ¥

and the product rule for differentiation ( )ddx uv u v uv= +¢ ¢ . Please refer to FAC or an A-

level textbook for more detail if necessary here.