csc_txt vol 01_2010_12_en

TRANSCRIPT

Prepared and published by

CSI

200 Wellington Street West, 15th Floor Toronto, Ontario M5V 3C7

Telephone: 416.364.9130Toll-free: 1.866.866.2601

Fax: 416.359.0486 Toll-free fax: 1.866.866.2660

www.csi.ca

Canadian Securities CourseVolume 1

Where leaders learn fi nancial services.

Copies of this publication are for the personal use of

properly registered students whose names are entered

on the course records of CSI Global Education Inc.

(CSI)®. This publication may not be lent, borrowed

or resold. Names of individual securities mentioned

in this publication are for the purposes of comparison

and illustration only and prices for those securities were

approximate fi gures for the period when this publication

was being prepared.

Every attempt has been made to update securities industry

practices and regulations to refl ect conditions at the time

of publication. While information in this publication has

been obtained from sources we believe to be reliable, such

information cannot be guaranteed nor does it purport

to treat each subject exhaustively and should not be

interpreted as a recommendation for any specifi c product,

service, use or course of action. CSI assumes no obligation

to update the content in this publication.

A Note About References to Third Party Materials: There may be references in this publication to third party

materials. Those third party materials are not under the

control of CSI and CSI is not responsible for the contents

of any third party materials or for any changes or updates

to such third party materials. CSI is providing these

references to you only as a convenience and the inclusion

of any reference does not imply endorsement of the third

party materials.

ISBN: 978-1-926694-56-6

First printing: 1997Revised and reprinted: 2000, 2001, 2002, 2003, 2004, 2005, 2006, 2007, 2008, 2010

Copyright © 2010 by CSI Global Education Inc.

Notices Regarding This Publication: This publication is strictly intended for information and

educational use. Although this publication is designed to

provide accurate and authoritative information, it is to be

used with the understanding that CSI is not engaged in

the rendering of fi nancial, accounting or other professional

advice. If fi nancial advice or other expert assistance is

required, the services of a competent professional should

be sought.

In no event shall CSI and/or its respective suppliers be

liable for any special, indirect, or consequential damages or

any damages whatsoever resulting from the loss of use, data

or profi ts, whether in an action of contract negligence, or

other tortious action, arising out of or in connection with

information available in this publication.

© 2010 CSI Global Education Inc. All rights reserved. No part of this publication may be

reproduced, stored in a retrieval system, or transmitted

in any form by any means, electronic, mechanical,

photocopying, recording, or otherwise, without the prior

written permission of CSI Global Education Inc.

© CSI GLOBAL EDUCATION INC. (2010) i

Preface

This course covers the three central elements of the Canadian securities industry: investment products, fi nancial markets, and the role of fi nancial intermediaries. Its goal is to help you understand the Canadian fi nancial services marketplace and introduce you to industry terminology and practices.

We begin in Volume 1 with an overview of the industry. Your focus should be on gaining an understanding of the different fi nancial markets and the securities that trade on those markets. In Volume 2, the focus shifts to analyzing the various fi nancial products so that you better understand how they are used as part of a well-planned portfolio of investments.

Our goal for you is that you gain the knowledge necessary to apply towards an exciting career in fi nancial services or to your own personal fi nancial circumstances.

This edition of the Canadian Securities Course (CSC) textbook was prepared in the Fall of 2009 and updated in the Fall of 2010. This edition retains all of the enhancements included in its predecessor edition, the 40th anniversary of the Canadian Securities Course released in 2004. The CSC textbook is updated and revised on a regular basis to better refl ect the rapidly changing fi nancial services industry.

PREFACE iii

© CSI GLOBAL EDUCATION INC. (2010)

Key Chapter FeaturesLearning features included as part of each chapter include:

Chapter Outlines: The chapter outline lets you know what content will be covered in the chapter and will prepare you for the material you are about to read.

Learning Objectives: The learning objectives help to focus your studies on important topic areas. Be sure to read each objective before you begin a chapter; the objectives specify precisely what you are expected to know after reading the chapter and studying the material. To highlight their importance, we have linked each objective directly to the chapter’s major headings.

Chapter Openers: Each chapter begins with a short overview of the importance and relevance of the material to be covered. The openers set the stage by linking the chapter content to the real world and should help increase your motivation.

Key Terms: A list of key terms is provided at the start of each chapter. Understanding the terminology and jargon of the securities industry is an important part of your success in this course. Each key term is boldfaced in the chapter and appears in the glossary included at the end of the textbook.

Chapter Summaries: Each chapter closes with a concise summary of the material organized by learning objective. The summaries will help to reinforce the relationship between the material and the chapter learning objectives and may suggest areas of weakness that require further study.

Thanks are due to those students and industry representatives who provided input into the revision process, either through their suggestions or by providing or verifying information for the book.

Canadian Securities Course Online ModulesYour registration as a student in the Canadian Securities Course includes access to online modules that guide your progress through the course materials. The modules are designed as study guides that help reinforce the textbook content and assess your knowledge. We suggest you log on to the online course and use the modules along with your text.

Enhancements to the CSC textbook include providing you with better links between the textbook and the CSC online modules. You will see icons throughout the text that correspond to the various learning resources included in the online modules. Each icon has a matching learning resource for the particular topic discussed in the text.

A description for each of the icons in the CSC online modules follows.

GETTING STARTED

Getting Started is provided to set up your expectations for each online module. It provides an introduction to the module’s purpose and content. There may also be a review activity or additional reading as preparation for the study of the module’s content.

LEARNING ACTIVITIES

The Learning Activities provide you with a variety of online exercises to test your knowledge of the material. The activities may be case- or scenario-based and allow you to practice calculations or comprehension of key concepts discussed in the text.

CANADIAN SECURITIES COURSE • VOLUME 1iv

© CSI GLOBAL EDUCATION INC. (2010)

POST-LESSON ASSESSMENT

Post-lesson tests are designed to test the key concepts in each chapter and module. You can complete a post-lesson test after studying the material in the chapter. Your results may suggest areas of weakness that require further study.

CSI Global Education Inc. CSI has been setting the standard for world-class, life-long education for financial professionals for more than 30 years. Having trained over 700,000 global professionals, makes us the preferred partner for individual and corporate financial services education internationally. Our expertise extends from securities to mutual funds, from banking and trust to insurance, from portfolio management to financial planning and wealth management.

CSI is a thought leader whose real world training sets professionals apart in their field, by developing them into leaders who are able to excel in their chosen careers. Our focus on leading educational and ethical standards means that our graduates have met the highest level of proficiency and certification. We develop course content based on industry trends and continuous involvement from our worldwide partners to ensure our graduates are the most current in every financial sector.

CSI is a partner – Working collaboratively with practitioners and industry regulators leads to a higher educational standard in an evolving financial services marketplace. Anticipating industry requirements allows us to develop relevant curriculum and testing for real world application.

CSI grants designations that have become a true measure of expertise. We focus on state of the art industry knowledge that is the recognized standard for regulatory authorities, financial organizations and associations in Canada and around the globe. Our graduates come with highly endorsed credentials respected throughout the financial services industry.

CSI is valued for its expertise in both course content and program delivery. CSI has established professional designations in growing specialties like financial derivatives and wealth management, adding to our respected and established courses and seminars. We’ve also pioneered the use of the Internet as a powerful tool for teaching and professional development, launching online courses and study aids.

CSI – leaders in innovative, lifelong education for career-minded financial professionals. CSI courses are available on demand in a variety of formats anywhere and anytime to suit the needs of learners and their organizations.

© CSI GLOBAL EDUCATION INC. (2010) v

Contents

SECTION I

THE CANADIAN INVESTMENT MARKETPLACE

1 The Capital Market ....................................................................1•1What is Investment Capital? ........................................................................... 1•5

Characteristics of Capital ............................................................................................ 1•5Why Capital Is Needed ............................................................................................... 1•6

Who are the Sources and Users of Capital? .................................................. 1•6Sources of Capital ....................................................................................................... 1•7Users of Capital .......................................................................................................... 1•8

What are the Financial Instruments? ............................................................. 1•9Debt Instruments ....................................................................................................... 1•9Equity Instruments ................................................................................................... 1•10Investment Funds ..................................................................................................... 1•10Derivatives and Other Financial Instruments ............................................................ 1•10

What are the Financial Markets? ...................................................................1•11Auction Markets in Canada ...................................................................................... 1•11Stock Exchanges Around the World .......................................................................... 1•14Dealer Markets ......................................................................................................... 1•17Private Equity ........................................................................................................... 1•19Trends in Financial Markets ...................................................................................... 1•21

Summary ...........................................................................................................1•22

VOLUME I

© CSI GLOBAL EDUCATION INC. (2010)

CANADIAN SECURITIES COURSE • VOLUME 1vi

2 The Canadian Securities Industry ...............................................2•1Overview of the Canadian Securities Industry .............................................. 2•5

The Role of Financial Intermediaries .............................................................. 2•8Types of Firms ............................................................................................................ 2•9Organization within Firms ........................................................................................ 2•10How Securities Firms are Financed ........................................................................... 2•12Dealer, Principal and Agency Functions .................................................................... 2•12The Clearing System ................................................................................................. 2•14Trends in the Securities Industry ............................................................................... 2•14

Banks as Financial Intermediaries ..................................................................2•15Schedule I Chartered Banks ...................................................................................... 2•15Schedule II and Schedule III Banks .......................................................................... 2•16Trends in the Role of Banks ...................................................................................... 2•17

Trust Companies, Credit Unions and Life Insurance Companies ..............2•18Trust and Loan Companies ....................................................................................... 2•18Credit Unions and Caisses Populaires ....................................................................... 2•18Insurance Companies ............................................................................................... 2•19Trends in Insurance .................................................................................................. 2•20

Investment Funds, Savings Banks, Pension Plans, Sales Finance and Consumer Loan Companies ....................................................................2•21

Investment Funds ..................................................................................................... 2•21Savings Banks ........................................................................................................... 2•21Pension Plans ............................................................................................................ 2•22Sales Finance and Consumer Loan Companies ......................................................... 2•22

Summary .......................................................................................................... 2•23

© CSI GLOBAL EDUCATION INC. (2010)

CONTENTS vii

3 The Canadian Regulatory Environment ......................................3•1Who are the Regulators? .................................................................................. 3•5

The Offi ce of the Superintendent of Financial Institutions ......................................... 3•5Canada Deposit Insurance Corporation ...................................................................... 3•5Credit Union Deposit Insurance Corporation ............................................................. 3•6The Provincial Regulators ........................................................................................... 3•6The Self-Regulatory Organizations ............................................................................. 3•7Canadian Investor Protection Fund ............................................................................ 3•9Mutual Fund Dealers Association Investor Protection Corporation .......................... 3•11Role of Arbitration.................................................................................................... 3•12Ombudsman for Banking Services and Investments .................................................. 3•12

What are the Principles of Securities Legislation? ......................................3•13Full,True and Plain Disclosure .................................................................................. 3•13Registration .............................................................................................................. 3•14The National Registration Database (NRD) ............................................................. 3•15Know Your Client Rule ............................................................................................. 3•15Fiduciary Duty ......................................................................................................... 3•16

What are the Ethics of Trading? .....................................................................3•16Examples of Unethical Practices ................................................................................ 3•17Prohibited Sales Practices .......................................................................................... 3•18

What are Public Company Disclosures and Investor Rights? .....................3•18Continuous Disclosure ............................................................................................. 3•18Statutory Rights for Investors ................................................................................... 3•20Proxies and Proxy Solicitation ................................................................................... 3•21

Takeover Bids and Insider Trading .................................................................3•21Takeover Bids ........................................................................................................... 3•22Insider Trading ......................................................................................................... 3•23

Summary .......................................................................................................... 3•25

© CSI GLOBAL EDUCATION INC. (2010)

CANADIAN SECURITIES COURSE • VOLUME 1viii

SECTION II

THE ECONOMY

4 Economic Principles ...................................................................4•1Foundations of Economics................................................................................ 4•6

Microeconomics and Macroeconomics ....................................................................... 4•6The Decision Makers .................................................................................................. 4•7Demand and Supply ................................................................................................... 4•7

Economic Growth ............................................................................................. 4•9Measuring Gross Domestic Product .......................................................................... 4•10Productivity and Determinants of Economic Growth ............................................... 4•13

The Business Cycle ...........................................................................................4•15Phases of the Business Cycle ..................................................................................... 4•16Using Economic Indicators ....................................................................................... 4•18Identifying Recessions ............................................................................................... 4•20

The Canadian Labour Market .........................................................................4•21Labour Market Indicators ......................................................................................... 4•22Types of Unemployment ........................................................................................... 4•23

Interest Rates ................................................................................................... 4•25Determinants of Interest Rates .................................................................................. 4•25How Interest Rates Affect the Economy ................................................................... 4•26Expectations and Interest Rates ................................................................................. 4•26

Money and Infl ation ......................................................................................... 4•28The Nature of Money ............................................................................................... 4•28Infl ation .................................................................................................................... 4•29Disinfl ation .............................................................................................................. 4•32Defl ation .................................................................................................................. 4•33

© CSI GLOBAL EDUCATION INC. (2010)

CONTENTS ix

International Economics ................................................................................ 4•34The Balance of Payments .......................................................................................... 4•34The Exchange Rate ................................................................................................... 4•37

Summary .......................................................................................................... 4•40

5 Economic Policy .........................................................................5•1Economic Theories ........................................................................................... 5•5

Rational Expectations Theory ..................................................................................... 5•5Keynesian Theory ....................................................................................................... 5•5Monetarist Theory ...................................................................................................... 5•6Supply-Side Economics .............................................................................................. 5•6

Fiscal Policy ........................................................................................................ 5•6The Federal Budget .................................................................................................... 5•7How Fiscal Policy Affects the Economy ...................................................................... 5•9

The Bank of Canada .........................................................................................5•11Role of the Bank of Canada ...................................................................................... 5•11Functions of the Bank of Canada .............................................................................. 5•11

Monetary Policy ................................................................................................5•13Implementing Monetary Policy ................................................................................ 5•13Open Market Operations .......................................................................................... 5•14Cash Management Operations .................................................................................. 5•16

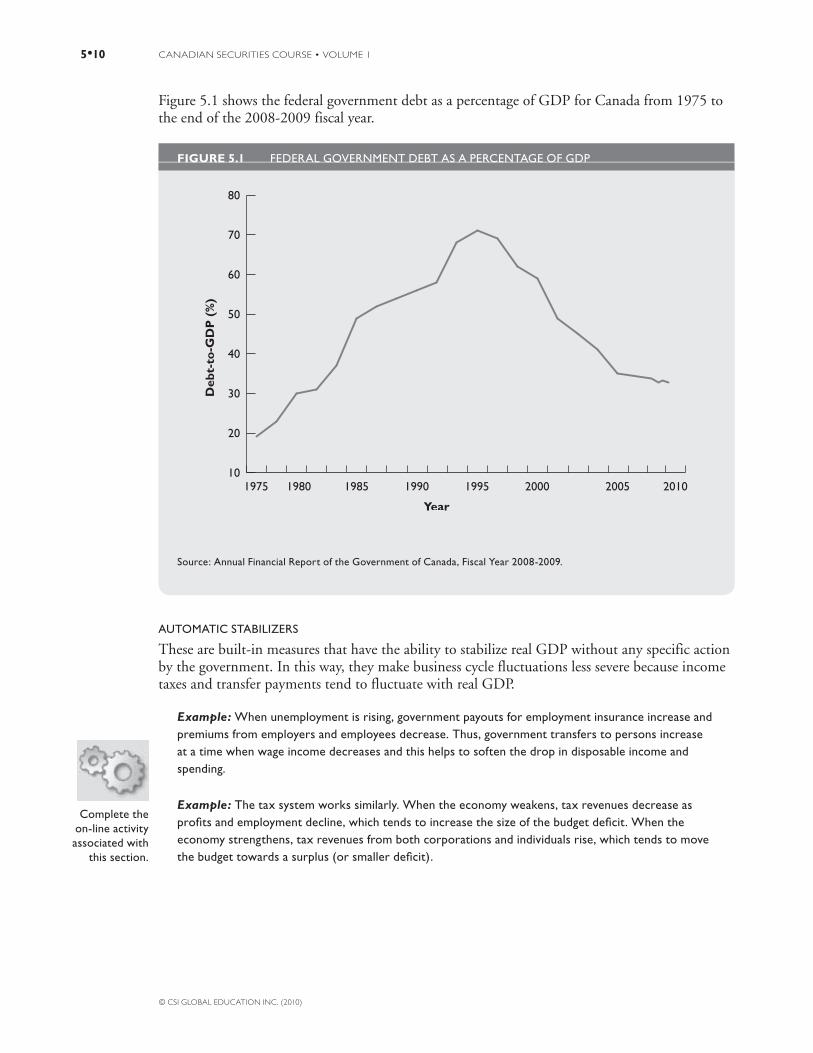

Government Policy Challenges.......................................................................5•17The Consequences of Failed Fiscal Policy .................................................................. 5•18

Summary ...........................................................................................................5•19

© CSI GLOBAL EDUCATION INC. (2010)

CANADIAN SECURITIES COURSE • VOLUME 1x

SECTION III

INVESTMENT PRODUCTS

6 Fixed-Income Securities: Features and Types ...............................6•1The Fixed-Income Marketplace....................................................................... 6•6

The Rationale for Issuing Fixed-Income Securities ...................................................... 6•6Size of the Fixed-Income Market ................................................................................ 6•7

Fixed-Income Terminology and Features ...................................................... 6•7Interest on Bonds........................................................................................................ 6•7Face Value and Denomination .................................................................................... 6•8Price and Yield ............................................................................................................ 6•8Term to Maturity ........................................................................................................ 6•9Liquid Bonds, Negotiable Bonds and Marketable Bonds ............................................ 6•9Callable Bonds .......................................................................................................... 6•10Sinking Funds and Purchase Funds ........................................................................... 6•11Extendible and Retractable Bonds ............................................................................. 6•12Convertible Bonds and Debentures .......................................................................... 6•13Protective Provisions of Corporate Bonds ................................................................. 6•15

Government of Canada Securities .................................................................6•16Marketable Bonds ..................................................................................................... 6•16Treasury Bills ............................................................................................................ 6•16Canada Savings Bonds .............................................................................................. 6•17

Provincial and Municipal Government Securities ........................................6•18Guaranteed Bonds .................................................................................................... 6•19Provincial Securities .................................................................................................. 6•20Municipal Securities ................................................................................................. 6•20

Corporate Bonds ..............................................................................................6•21Mortgage Bonds ....................................................................................................... 6•21Collateral Trust Bonds .............................................................................................. 6•22Equipment Trust Certifi cates .................................................................................... 6•22Subordinated Debentures ......................................................................................... 6•22

© CSI GLOBAL EDUCATION INC. (2010)

CONTENTS xi

Floating-Rate Securities ............................................................................................ 6•22Corporate Notes ....................................................................................................... 6•23Strip Bonds ............................................................................................................... 6•23Domestic, Foreign and Eurobonds ............................................................................ 6•23Preferred Securities ................................................................................................... 6•24

Other Fixed-Income Securities ..................................................................... 6•25Bankers’ Acceptances ................................................................................................ 6•25Commercial Paper .................................................................................................... 6•25Term Deposits .......................................................................................................... 6•25Guaranteed Investment Certifi cates .......................................................................... 6•25

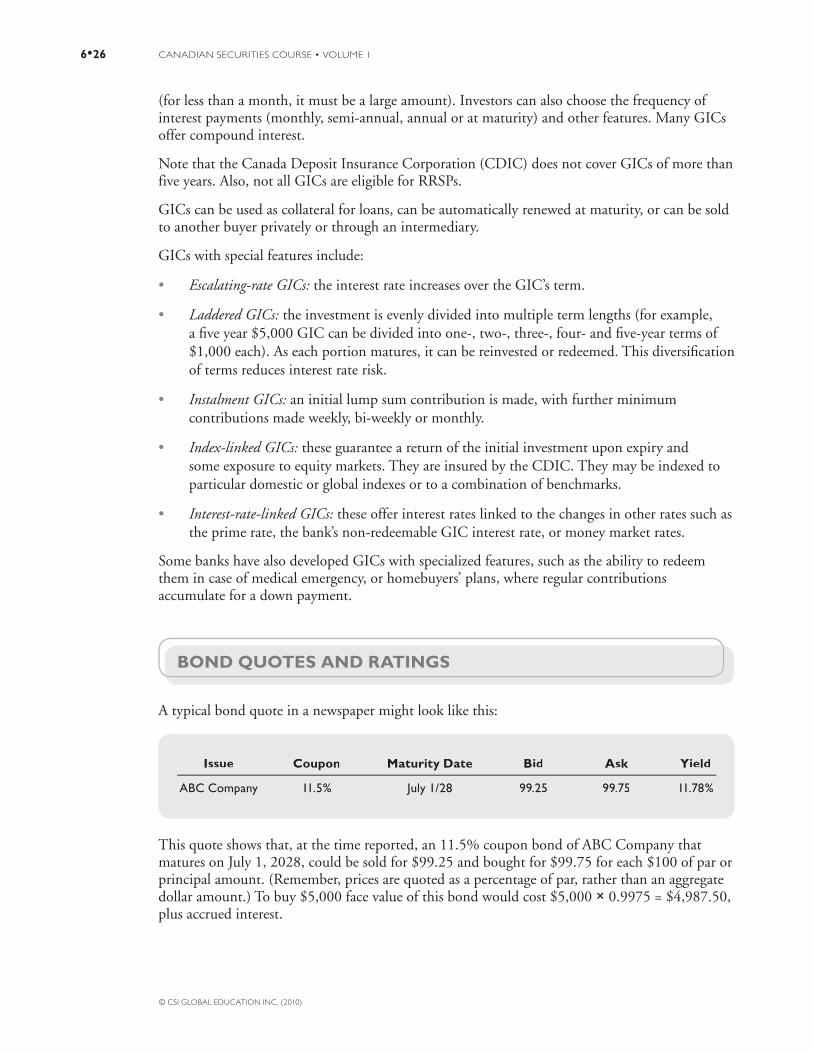

Bond Quotes and Ratings ............................................................................... 6•26

Summary .......................................................................................................... 6•30

7 Fixed Income Securities: Pricing and Trading ..............................7•1Bond Pricing Principles ..................................................................................... 7•5

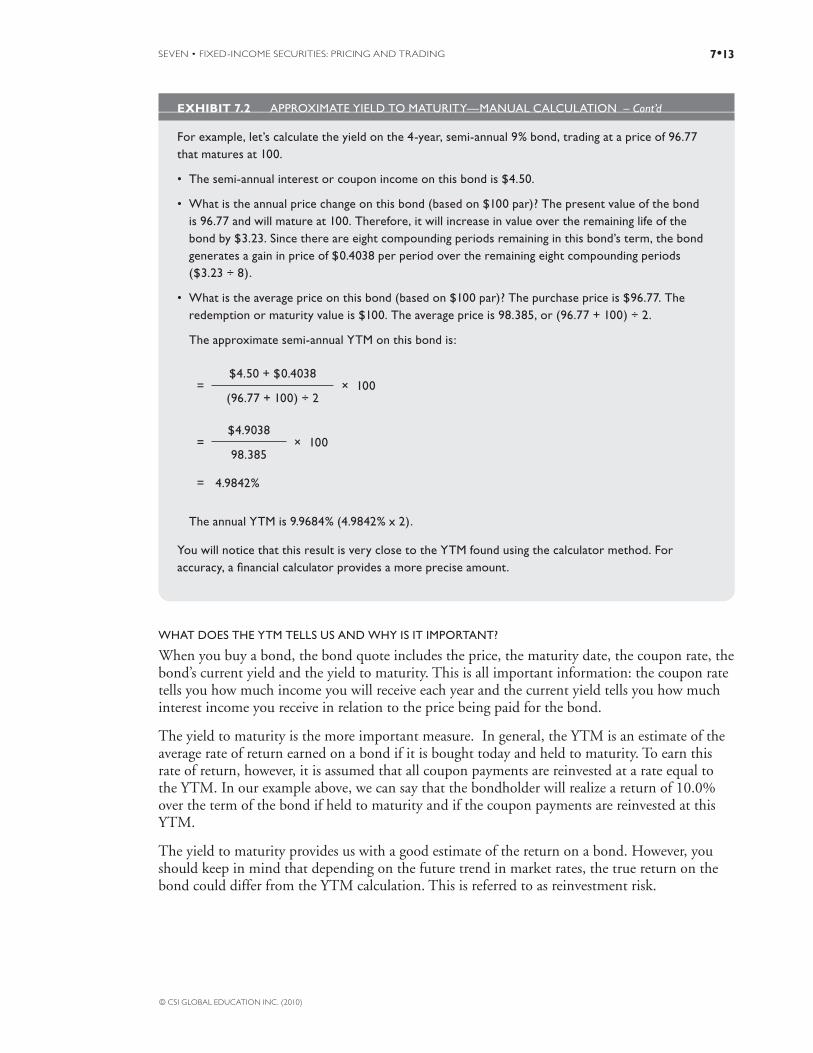

Calculating the Fair Price of a Bond ............................................................................ 7•7Calculating the Yield on a Treasury Bill .................................................................... 7•11Calculating the Current Yield on a Bond .................................................................. 7•11Calculating the Yield to Maturity on a Bond ............................................................ 7•11

Term Structure of Interest Rates ...................................................................7•14The Real Rate of Return ........................................................................................... 7•14The Yield Curve ....................................................................................................... 7•15

Bond Pricing Properties ..................................................................................7•17The Relationship Between Bond Prices and Interest Rates ........................................ 7•17The Impact of Maturity ............................................................................................ 7•18The Impact of the Coupon ....................................................................................... 7•19The Impact of Yield Changes .................................................................................... 7•20Duration as a Measure of Bond Price Volatility ......................................................... 7•20

Bond-Switching Strategies ............................................................................. 7•22

© CSI GLOBAL EDUCATION INC. (2010)

CANADIAN SECURITIES COURSE • VOLUME 1xii

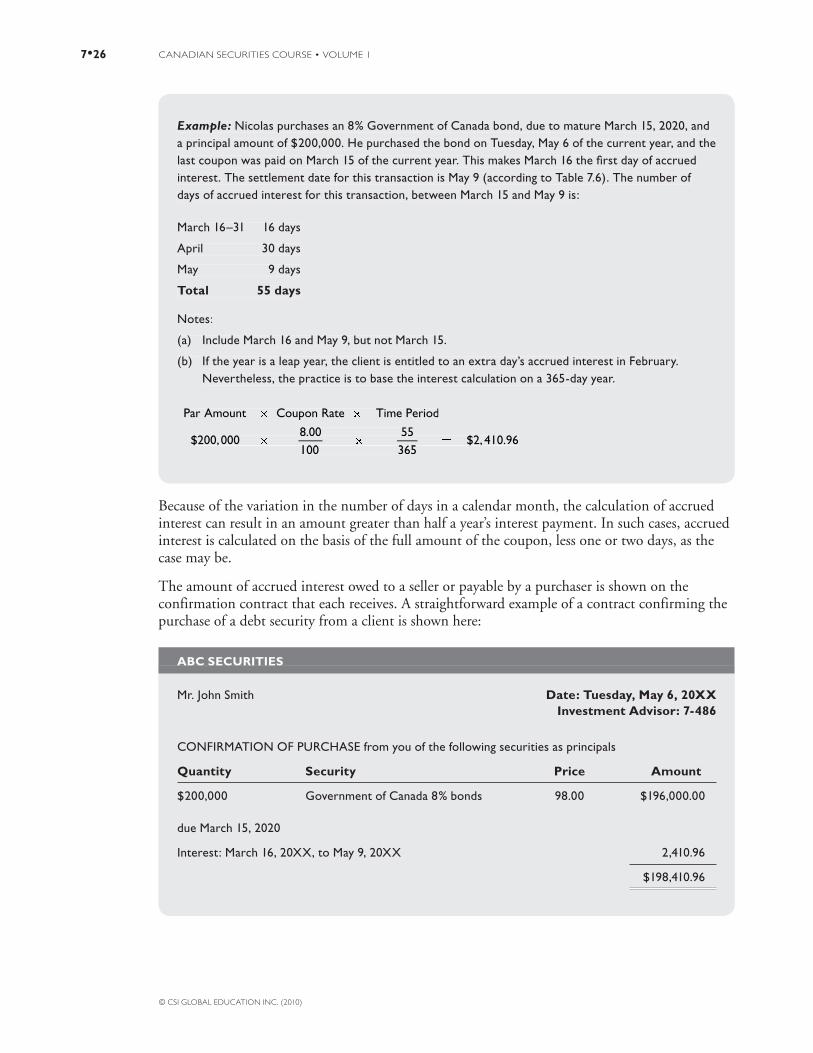

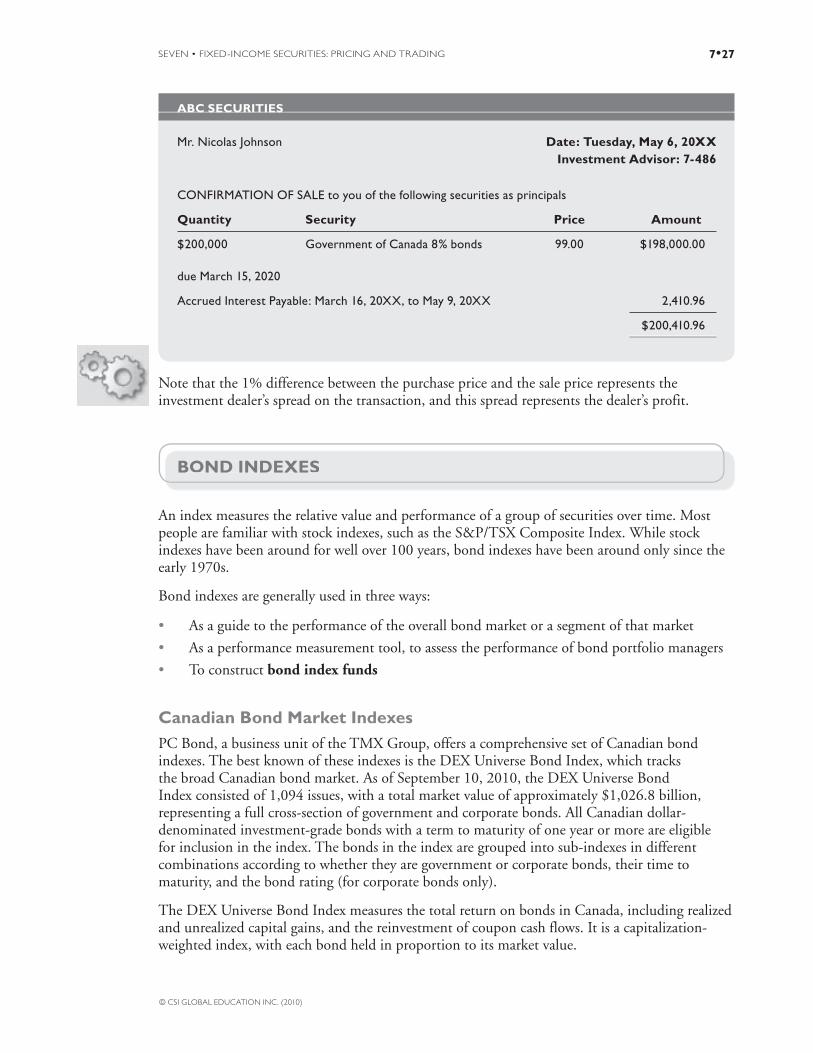

Bond Market Trading ...................................................................................... 7•24Clearing and Settlement ........................................................................................... 7•25Calculating Accrued Interest ..................................................................................... 7•25

Bond Indexes .....................................................................................................7•27Canadian Bond Market Indexes ................................................................................ 7•27Global Indexes .......................................................................................................... 7•28

Summary ...........................................................................................................7•29

8 Equity Securities: Common and Preferred Shares ........................8•1Common Shares ................................................................................................ 8•5

Benefi ts of Common Share Ownership ....................................................................... 8•5Capital Appreciation ................................................................................................... 8•6Dividends ................................................................................................................... 8•6Voting Privileges ....................................................................................................... 8•10Tax Treatment ........................................................................................................... 8•11Stock Splits and Consolidations ................................................................................ 8•12Reading Stock Quotations ........................................................................................ 8•14

Preferred Shares ..............................................................................................8•15The Preferred’s Position ............................................................................................ 8•15Why Companies Issue Preferred Shares ..................................................................... 8•16Why Investors Buy Preferred Shares .......................................................................... 8•17Preferred Share Features ............................................................................................ 8•17Straight Preferreds ..................................................................................................... 8•19Convertible Preferreds .............................................................................................. 8•19Retractable Preferreds ............................................................................................... 8•21Floating-Rate Preferreds ............................................................................................ 8•22Foreign-Pay Preferreds .............................................................................................. 8•23Other Types of Preferreds .......................................................................................... 8•23

© CSI GLOBAL EDUCATION INC. (2010)

CONTENTS xiii

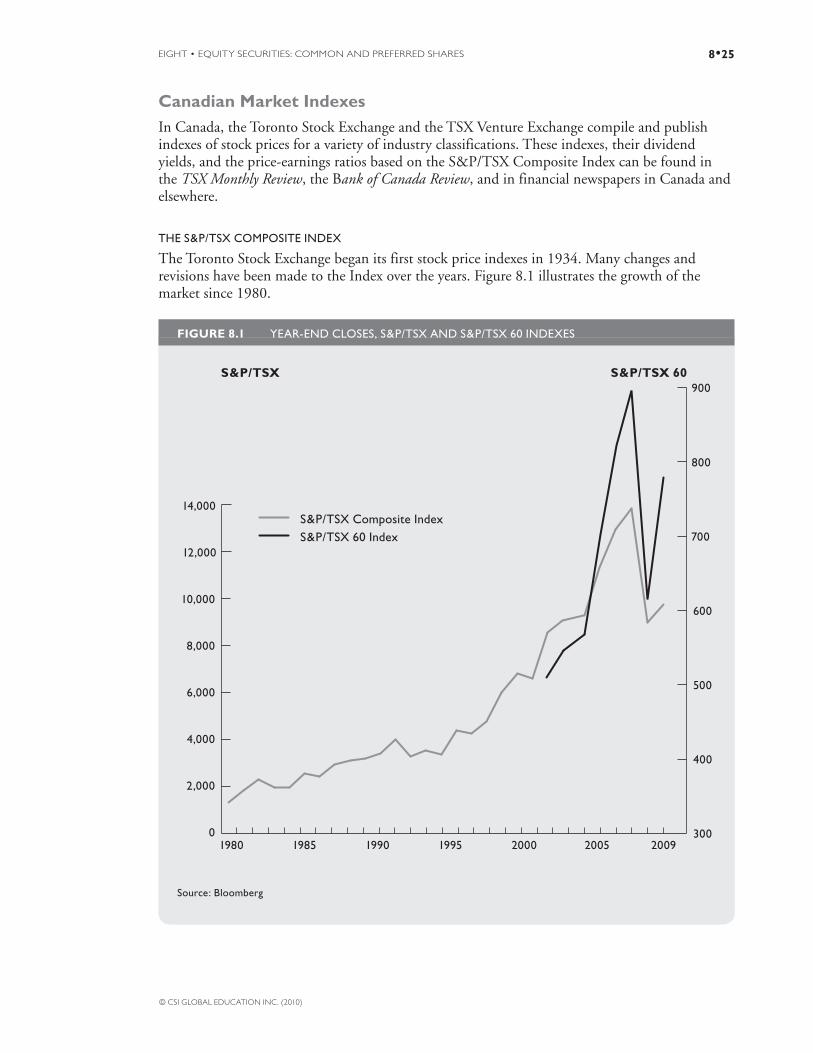

Stock Indexes and Averages........................................................................... 8•24Canadian Market Indexes ......................................................................................... 8•25U.S. Stock Market Indexes ........................................................................................ 8•28International Market Indexes and Averages ............................................................... 8•30

Summary .......................................................................................................... 8•32

9 Equity Securities: Equity Transactions .........................................9•1Cash Accounts ................................................................................................... 9•5

Cash Account Rules .................................................................................................... 9•5Free Credit Balances .................................................................................................. 9•5

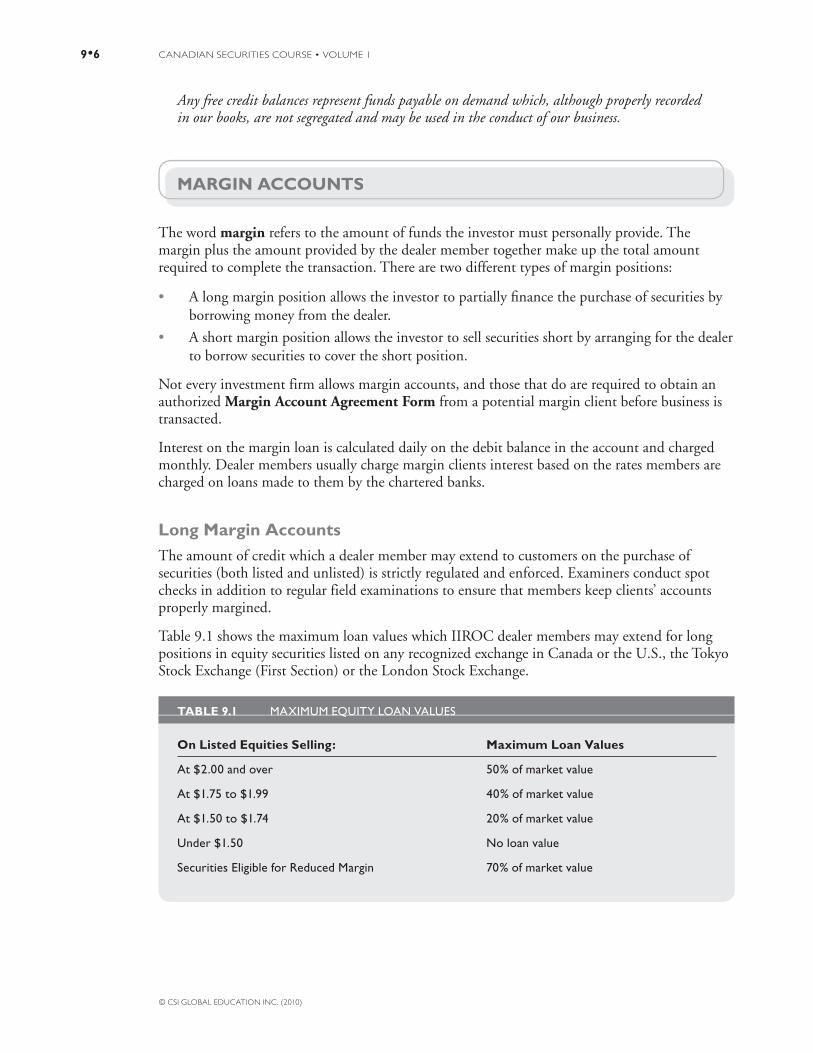

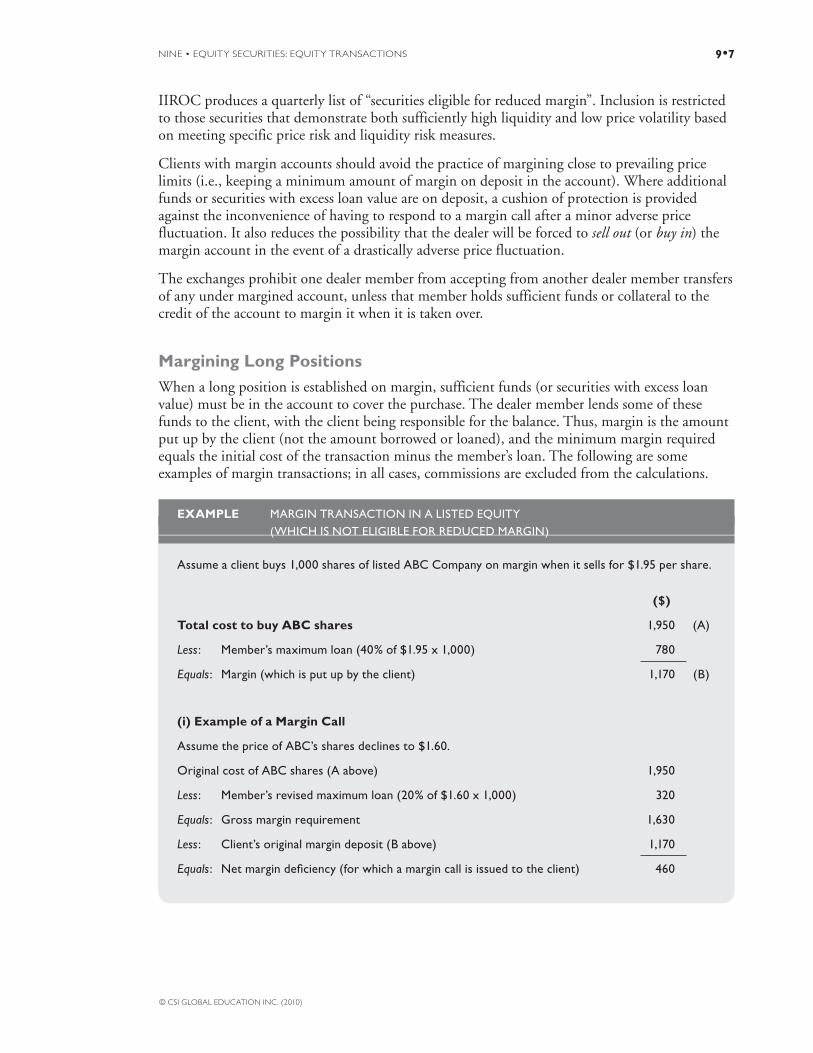

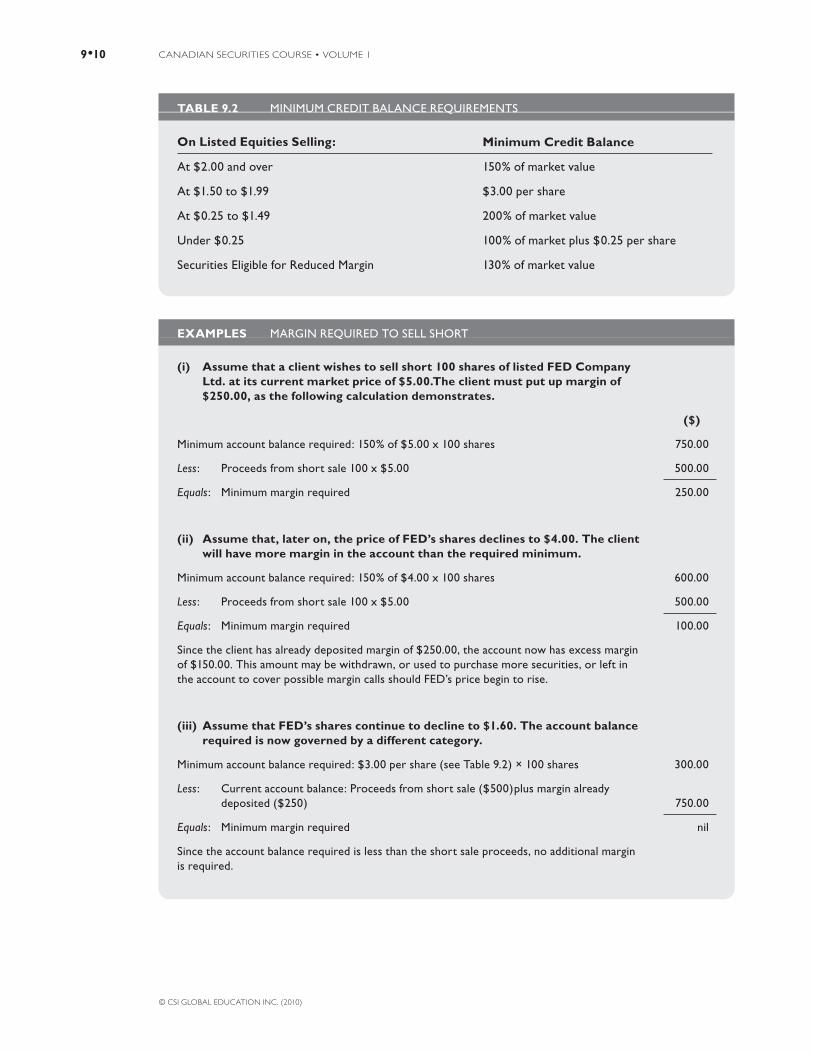

Margin Accounts ................................................................................................ 9•6Long Margin Accounts ............................................................................................... 9•6Margining Long Positions ........................................................................................... 9•7

Short Selling ....................................................................................................... 9•9How Short Selling is Done ......................................................................................... 9•9Dangers of Short Selling ........................................................................................... 9•12

Trading and Settlement Procedures ..............................................................9•13Trading Procedures ................................................................................................... 9•13

Buying and Selling Securities ..........................................................................9•16

Summary ...........................................................................................................9•19

10 Derivatives ................................................................................10•1What is a Derivative? ...................................................................................... 10•5

Features Common to All Derivatives ........................................................................ 10•5Derivative Markets.................................................................................................... 10•6Exchange-Traded versus OTC Derivatives ................................................................ 10•6

Types of Underlying Assets ............................................................................ 10•9Commodities ............................................................................................................ 10•9Financials .................................................................................................................. 10•9

© CSI GLOBAL EDUCATION INC. (2010)

CANADIAN SECURITIES COURSE • VOLUME 1xiv

Why Investors Use Derivatives ....................................................................10•10Individual Investors ................................................................................................ 10•10Institutional Investors ............................................................................................. 10•11Corporations and Businesses ................................................................................... 10•12Derivative Dealers ................................................................................................... 10•14

Options ............................................................................................................10•14Option Exchanges .................................................................................................. 10•17Option Strategies for Individual and Institutional Investors .................................... 10•18Option Strategies for Corporations ......................................................................... 10•25

Forwards and Futures ................................................................................... 10•26Key Terms and Defi nitions ..................................................................................... 10•27Futures Exchanges .................................................................................................. 10•28Futures Strategies for Investors ................................................................................ 10•30

Rights and Warrants ..................................................................................... 10•33Rights ..................................................................................................................... 10•33Warrants ................................................................................................................. 10•36

Summary ........................................................................................................ 10•38

SECTION IV

THE CORPORATION

11 Financing and Listing Securities ................................................11•1Types of Business Structures ..........................................................................11•6

Incorporated Businesses ..................................................................................11•6Public and Private Corporations ............................................................................... 11•9The Structure of the Organization .......................................................................... 11•12

Government Financings ................................................................................. 11•13Canadian Government Issues .................................................................................. 11•14Provincial and Municipal Issues .............................................................................. 11•16

© CSI GLOBAL EDUCATION INC. (2010)

CONTENTS xv

Corporate Financings..................................................................................... 11•16Equity Financing .................................................................................................... 11•17Debt Financing and Other Alternatives .................................................................. 11•19

The Corporate Financing Process ................................................................ 11•19The Dealer’s Advisory Relationship with Corporations ........................................... 11•20The Method of Offering ......................................................................................... 11•22The Prospectus ....................................................................................................... 11•23Other Documents and Sale of the Issue .................................................................. 11•26After-Market Stabilization ...................................................................................... 11•29

Other Methods of Distributing Securities to the Public ...........................11•30Junior Company Distributions ............................................................................... 11•30Options of Treasury Shares and Escrowed Shares .................................................... 11•31Capital Pool Company Program ............................................................................. 11•31NEX ....................................................................................................................... 11•32

The Listing Process ........................................................................................11•32Advantages and Disadvantages of Listing ................................................................ 11•32Listing Procedure for a Company ........................................................................... 11•34Withdrawing Trading Privileges .............................................................................. 11•34

Summary .........................................................................................................11•36

12 Corporations and their Financial Statements .............................12•1The Balance Sheet ...........................................................................................12•5

Classifi cation of Assets .............................................................................................. 12•6Classifi cation of Liabilities ...................................................................................... 12•11Shareholders’ Equity ............................................................................................... 12•13

The Earnings Statement................................................................................12•14Structure of the Earnings Statement ........................................................................ 12•14The Operating Section (items 28 to 34) ................................................................. 12•15The Non-Operating Section (items 35 and 36)....................................................... 12•16The Creditors’ Section (items 37 and 38) ............................................................... 12•17The Owners’ Section (items 40 to 45) .................................................................... 12•17

© CSI GLOBAL EDUCATION INC. (2010)

CANADIAN SECURITIES COURSE • VOLUME 1xvi

The Retained Earnings Statement ...............................................................12•19

The Cash Flow Statement .............................................................................12•19Operating Activities ................................................................................................ 12•20Financing Activities (items 51 to 54) ...................................................................... 12•21Investing Activities (items 55 to 57) ........................................................................ 12•21The Change in Cash Flow (items 58 to 60) ............................................................ 12•21Supplemental Information (items 61 to 62) ............................................................ 12•21

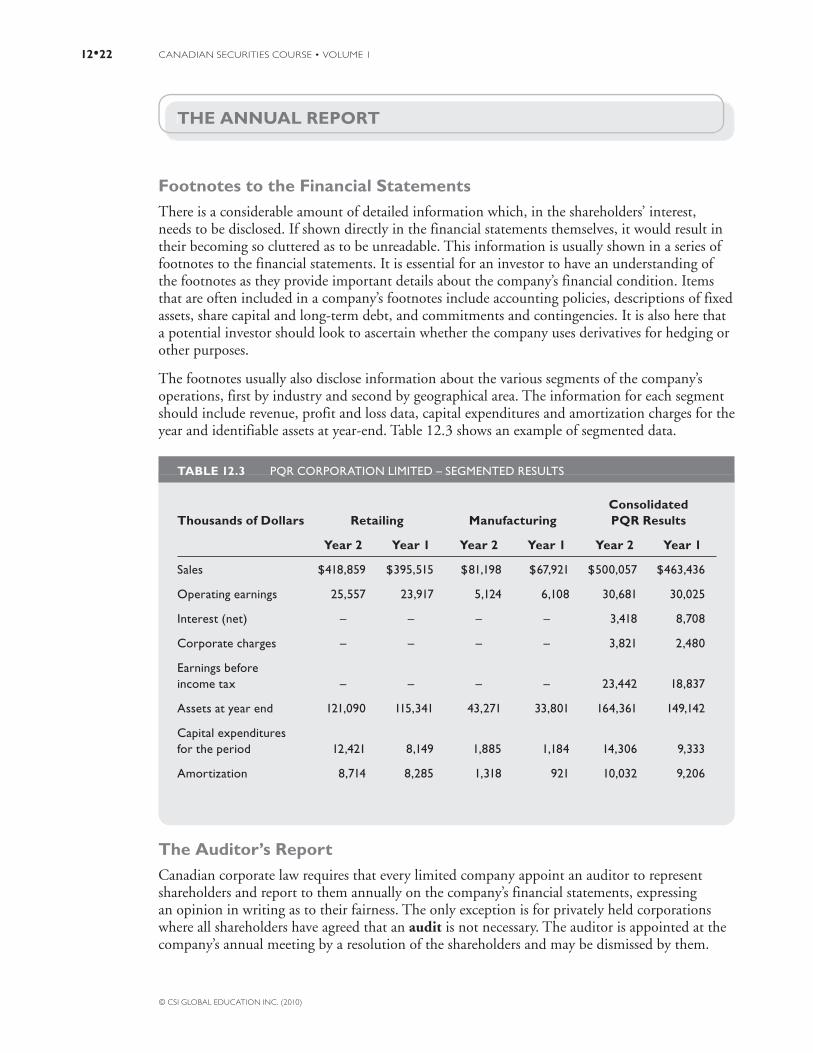

The Annual Report.........................................................................................12•22Footnotes to the Financial Statements ..................................................................... 12•22The Auditor’s Report .............................................................................................. 12•22Trends in accounting standards ............................................................................... 12•23

Summary .........................................................................................................12•25

Appendix A - Sample Financial Statements ...............................................12•26

Glossary . ........................................................................................G•1

Selected Web Sites .......................................................................Web•1

Index............................................................................................ Ind•1

© CSI GLOBAL EDUCATION INC. (2010)

CONTENTS xvii

SECTION V

INVESTMENT ANALYSIS

13 Fundamental and Technical Analysis .........................................13•1Overview of Analysis Methods ....................................................................... 13•5

Fundamental Analysis ............................................................................................... 13•5Quantitative Analysis ................................................................................................ 13•5Technical Analysis ..................................................................................................... 13•5Market Theories ....................................................................................................... 13•6

Fundamental Macroeconomic Analysis .........................................................13•7The Fiscal Policy Impact ........................................................................................... 13•7The Monetary Policy Impact .................................................................................... 13•8The Flow of Funds Impact...................................................................................... 13•10The Infl ation Impact .............................................................................................. 13•11

Fundamental Industry Analysis ....................................................................13•12Classifying Industries by Product or Service ............................................................ 13•12Classifying Industries by Stage of Growth ............................................................... 13•14Classifying Industries by Competitive Forces .......................................................... 13•15Classifying Industries by Stock Characteristics ........................................................ 13•16

Fundamental Valuation Models ...................................................................13•18Dividend Discount Model ...................................................................................... 13•18Using the Price-Earnings Ratio ............................................................................... 13•19

Technical Analysis ..........................................................................................13•20Comparing Technical Analysis to Fundamental Analysis ......................................... 13•21Commonly Used Tools in Technical Analysis .......................................................... 13•21

Summary .........................................................................................................13•29

VOLUME 2

© CSI GLOBAL EDUCATION INC. (2010)

CANADIAN SECURITIES COURSE • VOLUME 1xviii

14 Company Analysis ....................................................................14•1Overview of Company Analysis ..................................................................... 14•5

Earnings Statement Analysis ..................................................................................... 14•5Balance Sheet Analysis .............................................................................................. 14•6Other Features of Company Analysis ........................................................................ 14•8

Interpreting Financial Statements ............................................................... 14•9Trend Analysis ........................................................................................................ 14•10External Comparisons ............................................................................................. 14•11

Financial Ratio Analysis .................................................................................14•12Liquidity Ratios ...................................................................................................... 14•13Risk Analysis Ratios ................................................................................................ 14•15Operating Performance Ratios ................................................................................ 14•22Value Ratios ............................................................................................................ 14•27

Assessing Preferred Share Investment Quality ..........................................14•34Dividend Payments ................................................................................................. 14•35 Credit Assessment ................................................................................................... 14•35Selecting Preferreds ................................................................................................. 14•36How Preferreds Fit Into Individual Portfolios ......................................................... 14•37

Summary .........................................................................................................14•39

Appendix A: Company Financial Statements ............................................ 14•40

Appendix B: Sample Company Analysis .................................................... 14•44

© CSI GLOBAL EDUCATION INC. (2010)

CONTENTS xix

SECTION VI

PORTFOLIO ANALYSIS

15 Introduction to the Portfolio Approach .....................................15•1Risk and Return ............................................................................................... 15•5

Rate of Return ......................................................................................................... 15•6Risk ........................................................................................................................ 15•10

Portfolio Risk and Return ..............................................................................15•12Calculating the Rate of Return on a Portfolio ......................................................... 15•14Measuring Risk in a Portfolio ................................................................................. 15•14Combining Securities in a Portfolio ........................................................................ 15•15

Overview of the Portfolio Management Process .......................................15•19

Objectives and Constraints ...........................................................................15•20Return and Risk Objectives .................................................................................... 15•20Investment Objectives............................................................................................. 15•21Investment Constraints ........................................................................................... 15•24Managing Investment Objectives ............................................................................ 15•27

The Investment Policy Statement ...............................................................15•27

Summary .........................................................................................................15•31

16 The Portfolio Management Process ...........................................16•1Developing an Asset Mix ................................................................................ 16•5

The Asset Mix .......................................................................................................... 16•5Setting the Asset Mix ................................................................................................ 16•6

Portfolio Manager Styles ...............................................................................16•13Equity Manager Styles ............................................................................................ 16•13Fixed-Income Manager Styles ................................................................................. 16•16

© CSI GLOBAL EDUCATION INC. (2010)

CANADIAN SECURITIES COURSE • VOLUME 1xx

Asset Allocation .............................................................................................16•17Balancing the Asset Classes ..................................................................................... 16•20Strategic Asset Allocation ........................................................................................ 16•20Ongoing Asset Allocation ....................................................................................... 16•22Passive Management ............................................................................................... 16•23

Portfolio Monitoring ......................................................................................16•24Monitoring the Markets and the Client .................................................................. 16•24Monitoring the Economy ....................................................................................... 16•25A Portfolio Manager’s Checklist .............................................................................. 16•30

Evaluating Portfolio Performance ................................................................16•32Measuring Portfolio Returns ................................................................................... 16•32Calculating the Risk-Adjusted Rate of Return ......................................................... 16•33Other Factors in Performance Measurement ........................................................... 16•34

Summary .........................................................................................................16•35

SECTION VII

ANALYSIS OF MANAGED PRODUCTS

17 Evolution of Managed and Structured Products ........................17•1Managed and Structured Products ................................................................17•4

What Is a Managed Product? .................................................................................... 17•4What Is a Structured Product? .................................................................................. 17•5

A Comparison of Managed and Structured Products .................................17•6Advantages of Managed Products .............................................................................. 17•6Advantages of Structured Products ............................................................................ 17•7Disadvantages of Managed Products ......................................................................... 17•7Disadvantages of Structured Products ....................................................................... 17•8

Risks Involved With Managed and Structured Products .............................17•9Types of Risk ............................................................................................................ 17•9

Types of Managed and Structured Products ...............................................17•10

© CSI GLOBAL EDUCATION INC. (2010)

CONTENTS xxi

The Evolving Market for Managed and Structured Products ................... 17•11Market Growth Factors for Managed and Structured Products ............................... 17•11

Changing Compensation Models ..................................................................17•12

Summary .........................................................................................................17•13

18 Mutual Funds: Structure and Regulation ..................................18•1What Is a Mutual Fund? .................................................................................. 18•5

Advantages of Mutual Funds..................................................................................... 18•5Disadvantages of Mutual Funds ................................................................................ 18•7

The Structure of Mutual Funds ..................................................................... 18•8Organization of a Mutual Fund ................................................................................ 18•9Pricing Mutual Fund Units or Shares ...................................................................... 18•10Charges Associated with Mutual Funds .................................................................. 18•11

Labour-Sponsored Venture Capital Corporations ....................................18•15Advantages of Labour-Sponsored Funds ................................................................. 18•15Disadvantages of Labour-Sponsored Funds ............................................................. 18•16

Regulating Mutual Funds ...............................................................................18•16Mutual Fund Regulatory Organizations .................................................................. 18•17National Instrument 81-101 and 81-102 ................................................................ 18•17General Mutual Fund Requirements ....................................................................... 18•18The Simplifi ed Prospectus ...................................................................................... 18•18

Other Forms and Requirements ................................................................. 18•20Registration Requirements for the Mutual Fund Industry ....................................... 18•21Mutual Fund Restrictions ....................................................................................... 18•22Distribution of Mutual Funds by Financial Institutions .......................................... 18•26

Summary ........................................................................................................ 18•28

© CSI GLOBAL EDUCATION INC. (2010)

CANADIAN SECURITIES COURSE • VOLUME 1xxii

19 Mutual Funds: Types and Features ............................................19•1Types of Mutual Funds .................................................................................... 19•5

Cash and Equivalents Funds ..................................................................................... 19•5Fixed-Income Funds ................................................................................................. 19•6Balanced Funds......................................................................................................... 19•6Equity Funds ............................................................................................................ 19•7Specialty and Sector Funds ....................................................................................... 19•9Index Funds .............................................................................................................. 19•9Comparing Fund Types .......................................................................................... 19•10

Fund Management Styles ..............................................................................19•10Indexing and Closet Indexing ................................................................................. 19•11Multi-Manager ....................................................................................................... 19•11

Redeeming Mutual Fund Units or Shares ...................................................19•12Tax Consequences................................................................................................... 19•12Reinvesting Distributions ....................................................................................... 19•14Types of Withdrawal Plans ...................................................................................... 19•15Suspension of Redemptions .................................................................................... 19•18

Comparing Mutual Fund Performance ........................................................19•19Reading Mutual Fund Quotes ................................................................................ 19•19Measuring Mutual Fund Performance ..................................................................... 19•20Issues that Complicate Mutual Fund Performance .................................................. 19•22

Summary ........................................................................................................ 19•25

20 Segregated Funds and Other Insurance Products .......................20•1Features of Segregated Funds ....................................................................... 20•5

Owners and Annuitants ............................................................................................ 20•5Benefi ciaries .............................................................................................................. 20•6Maturity Guarantees ................................................................................................. 20•6Death Benefi ts .......................................................................................................... 20•8Creditor Protection ................................................................................................... 20•9Bypassing Probate ................................................................................................... 20•10

© CSI GLOBAL EDUCATION INC. (2010)

CONTENTS xxiii

Cost of the Guarantees ........................................................................................... 20•10Bankruptcy and Family Law ................................................................................... 20•10Disclosure Documents ............................................................................................ 20•11Comparison to Mutual Funds ................................................................................. 20•11

Taxation of Segregated Funds ..................................................................... 20•12Impact of Allocations on Net Asset Values .............................................................. 20•13Tax Treatment of Guarantees .................................................................................. 20•15Tax Treatment of Death Benefi ts ............................................................................. 20•16

Regulation of Segregated Funds .................................................................. 20•17Monitoring Solvency .............................................................................................. 20•17The Role Played by Assuris ..................................................................................... 20•17

Other Insurance Products ............................................................................ 20•18Guaranteed Minimum Withdrawal Benefi t Plans ................................................... 20•18Portfolio Funds ....................................................................................................... 20•19Protected Funds ...................................................................................................... 20•19

Summary ....................................................................................................... 20•21

21 Hedge Funds.............................................................................21•1Overview of Hedge Funds ...............................................................................21•5

Comparisons to Mutual Funds ................................................................................. 21•5Who Can Invest in Hedge Funds? ............................................................................ 21•6History of Hedge Funds ........................................................................................... 21•7Size of the Hedge Fund Market ................................................................................ 21•8Tracking Hedge Fund Performance ........................................................................... 21•8

Benefi ts and Risks of Hedge Funds ................................................................21•9Benefi ts ..................................................................................................................... 21•9Risks ....................................................................................................................... 21•10Due Diligence......................................................................................................... 21•13

© CSI GLOBAL EDUCATION INC. (2010)

CANADIAN SECURITIES COURSE • VOLUME 1xxiv

Hedge Fund Strategies ..................................................................................21•14Relative Value Strategies .......................................................................................... 21•15Event-Driven Strategies........................................................................................... 21•17Directional Funds ................................................................................................... 21•18

Funds of Hedge Funds ....................................................................................21•21Advantages .............................................................................................................. 21•21Disadvantages ......................................................................................................... 21•22

Summary .........................................................................................................21•23

22 Exchange-Listed Managed Products ..........................................22•1Closed-End Funds ............................................................................................ 22•4

Advantages of Closed-End Funds .............................................................................. 22•4Disadvantages of Closed-End Funds ......................................................................... 22•5

Income Trusts .................................................................................................. 22•6Real Estate Investment Trusts (REITs) ...................................................................... 22•7Royalty or Resource Trusts ........................................................................................ 22•7Business Trusts .......................................................................................................... 22•8

Exchange-Traded Funds .................................................................................. 22•9Trading ETFs ............................................................................................................ 22•9The Market for ETFs .............................................................................................. 22•10Recent Trends in ETFs ............................................................................................ 22•11Regulatory Issues .................................................................................................... 22•12

Listed Private Equity ......................................................................................22•12Structure of Listed Private Equity Companies ......................................................... 22•13Advantages and Disadvantages of Listed Private Equity .......................................... 22•14

Summary .........................................................................................................22•16

© CSI GLOBAL EDUCATION INC. (2010)

CONTENTS xxv

23 Fee-Based Accounts ...................................................................23•1Overview of Fee-Based Accounts ................................................................. 23•4

Managed Accounts ................................................................................................... 23•5Fee-Based Non-Managed Accounts ........................................................................... 23•6Advantages and Disadvantages of Fee-Based Accounts .............................................. 23•6Discretionary Accounts ............................................................................................. 23•7

Types of Managed Accounts ........................................................................... 23•8Single-Manager Accounts ......................................................................................... 23•8Multi-Manager Accounts ........................................................................................ 23•10Private Family Offi ce .............................................................................................. 23•13

Summary .........................................................................................................23•14

24 Structured Products ..................................................................24•1Principal-Protected Notes ............................................................................. 24•5

PPN Guarantors, Manufacturers and Distributors .................................................... 24•5The Structure of PPNs.............................................................................................. 24•6Risks Associated with PPNs ...................................................................................... 24•8Tax Implications of PPNs ....................................................................................... 24•10

Index-Lined Guaranteed Investment Certifi cates .....................................24•11Structure of Index-Linked GICs ............................................................................. 24•12How Returns are Determined ................................................................................. 24•12Risks Associated with Index-Linked GICs .............................................................. 24•13Tax Implications ..................................................................................................... 24•13

Split Shares .....................................................................................................24•14What are Split Shares? ............................................................................................. 24•14Risks Associated with Split Shares ........................................................................... 24•15Tax Implications ..................................................................................................... 24•16

Canadian Originated Preferred Securities (COPrS) .................................24•17

© CSI GLOBAL EDUCATION INC. (2010)

CANADIAN SECURITIES COURSE • VOLUME 1xxvi

Asset-Backed Securities ................................................................................24•17The Securitization Process ...................................................................................... 24•17Asset-Backed Commercial Paper ............................................................................. 24•19

Mortgage-Backed Securities ........................................................................ 24•20Structure and Benefi ts of MBS ................................................................................ 24•21

Summary ........................................................................................................ 22•24

SECTION VIII

WORKING WITH THE CLIENT

25 Canadian Taxation ....................................................................25•1Taxation ............................................................................................................ 25•5

The Income Tax System in Canada ........................................................................... 25•5Types of Income ....................................................................................................... 25•6Calculating Income Tax Payable ................................................................................ 25•7Taxation of Investment Income ................................................................................ 25•7Tax-Deductible Items Related to Investment Income .............................................. 25•10

Calculating Investment Gains and Losses ...................................................25•11Disposition of Shares .............................................................................................. 25•12Disposition of Debt Securities ................................................................................ 25•13Capital Losses ......................................................................................................... 25•14Tax Loss Selling ...................................................................................................... 25•16Minimum Tax......................................................................................................... 25•16

Tax Deferral Plans ..........................................................................................25•17Registered Pension Plans (RPPs) ............................................................................. 25•17Registered Retirement Savings Plans (RRSPs) ......................................................... 25•18Registered Retirement Income Funds (RRIFs) ........................................................ 25•22Deferred Annuities ................................................................................................. 25•22Tax Free Savings Accounts (TFSA) ......................................................................... 25•23Registered Educations Savings Plans (RESPs) ......................................................... 25•24

© CSI GLOBAL EDUCATION INC. (2010)

CONTENTS xxvii

Tax Planning Strategies ................................................................................ 25•26

Summary ........................................................................................................ 25•28

26 Working with the Retail Client .................................................26•1Financial Planning ............................................................................................ 26•5

The Financial Planning Process ..................................................................... 26•6Interview the Client: Establish the Client Advisor Engagement ................................ 26•6Data Gathering and Determining Goals and Objectives ........................................... 26•6Identify Financial Problems and Constraints ............................................................. 26•8Develop a Written Financial Plan and Implement the Recommendations ................. 26•9Periodically Review and Revise the Plan and Make New Recommendations ............. 26•9

Financial Planning Aids ..................................................................................26•10Life Cycle Analysis .................................................................................................. 26•10The Financial Planning Pyramid ............................................................................. 26•11

Ethics and the Advisor ...................................................................................26•12The Code of Ethics ................................................................................................. 26•12Standards of Conduct ............................................................................................. 26•13Standard A – Duty of Care ..................................................................................... 26•14Standard B – Trustworthiness, Honesty, Fairness .................................................... 26•15Standard C – Professionalism .................................................................................. 26•17Standard D – Conduct in Accordance with Securities Acts ..................................... 26•19Standard E – Confi dentiality .................................................................................. 26•20

Summary ........................................................................................................ 26•21

Appendix A .................................................................................................... 26•23

Appendix B – Client Scenarios .................................................................... 26•27

© CSI GLOBAL EDUCATION INC. (2010)

CANADIAN SECURITIES COURSE • VOLUME 1xxviii

27 Working With the Institutional Client ......................................27•1Who Are Institutional Clients? ...................................................................... 27•4

The Institutional Marketplace .................................................................................. 27•4

Suitability Requirements: Institutional vs. Retail Clients ...........................27•7Suitability Standards for Institutional Clients ............................................................ 27•7

Roles and Responsibilities in the Institutional Market ................................ 27•8The Role of the Institutional Salesperson .................................................................. 27•9The Role of the Institutional Trader ........................................................................ 27•12

Summary .........................................................................................................27•14