credit scoring basics

TRANSCRIPT

Credit Scoring BasicsFICO World PreviewFICO World Preview

Julie WoodingJulie WoodingPrincipal Consultant, ScoresFICO

1

This presentation is provided for the recipient only and cannot be reproduced or shared without Fair Isaac Corporation's express consent.© 2010 Fair Isaac Corporation.

FICO World Preview Workshop SessionFICO World Preview – Workshop Session

» Special, Pre-Conference Session

» Full Day of Practical Workshops

» Six Industry Experts on Hand

» Best Practices, Advice and Examples

» Free with Conference Registration

2 © 2010 Fair Isaac Corporation. © 2010 Fair Isaac Corporation. 2

g

» 30% off Conference Fee

Agenda» Credit Scoring Basics

» FICO® Score Content

» Preview of Full FICO World Session

3 © 2010 Fair Isaac Corporation. © 2010 Fair Isaac Corporation. 3

Credit Risk Scoring

A statistical process whereby information about aA statistical process whereby information about a credit applicant or an existing accountholder is converted into a numerical score.converted into a numerical score.

This score is then regarded as a measure of thedit i k f th i di id l d (i thcredit risk of the individual concerned (i.e., the

probability of repayment).

4 © 2010 Fair Isaac Corporation.

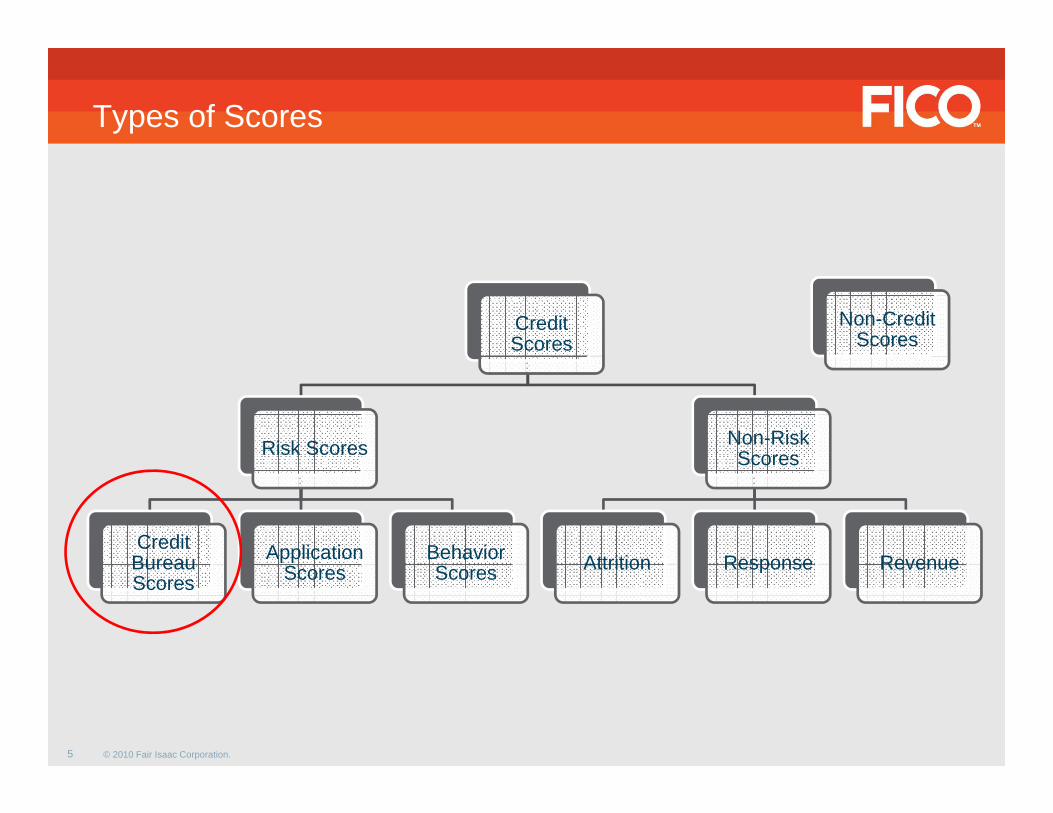

Types of Scores

Credit Scores

Non-Credit Scores

Risk Scores Non-Risk Scores

Credit Bureau Application Behavior

Scores

Attrition Response RevenueBureau Scores

ppScores Scores Attrition Response Revenue

5 © 2010 Fair Isaac Corporation.

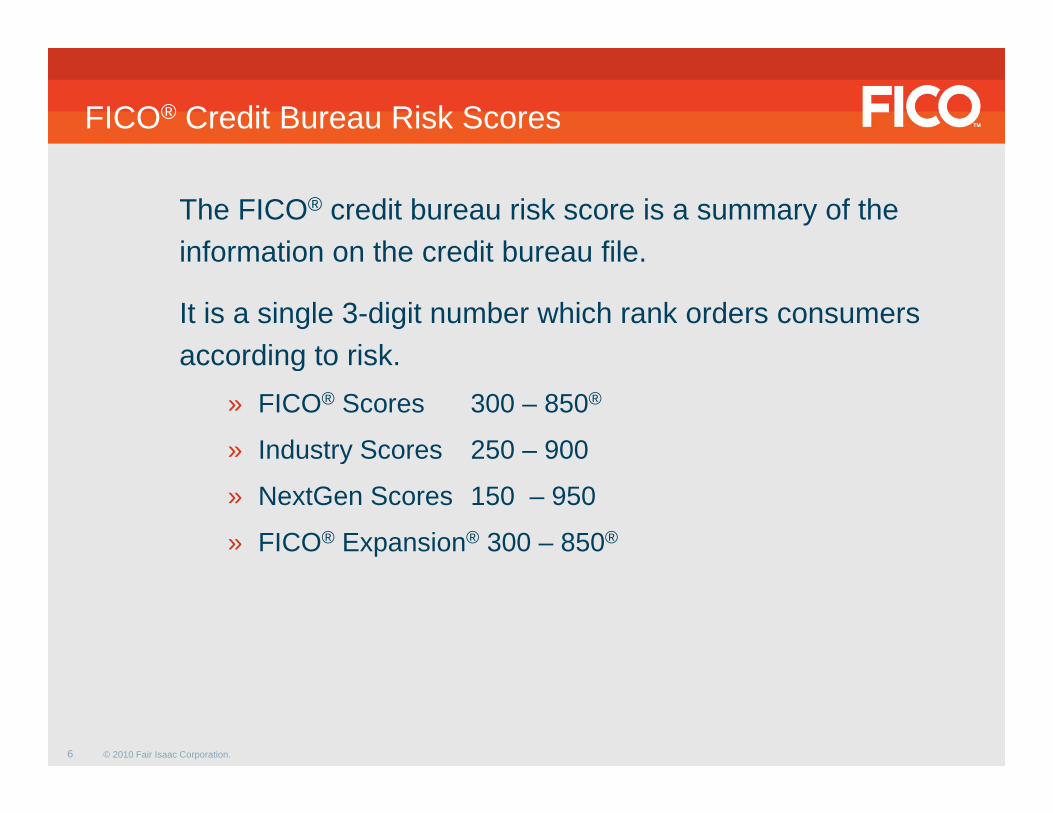

FICO® Credit Bureau Risk Scores

The FICO® credit bureau risk score is a summary of the information on the credit bureau fileinformation on the credit bureau file.

It is a single 3-digit number which rank orders consumers according to riskaccording to risk.

» FICO® Scores 300 – 850®

» Industry Scores 250 – 900Industry Scores 250 900

» NextGen Scores 150 – 950

» FICO® Expansion® 300 – 850®

6 © 2010 Fair Isaac Corporation.

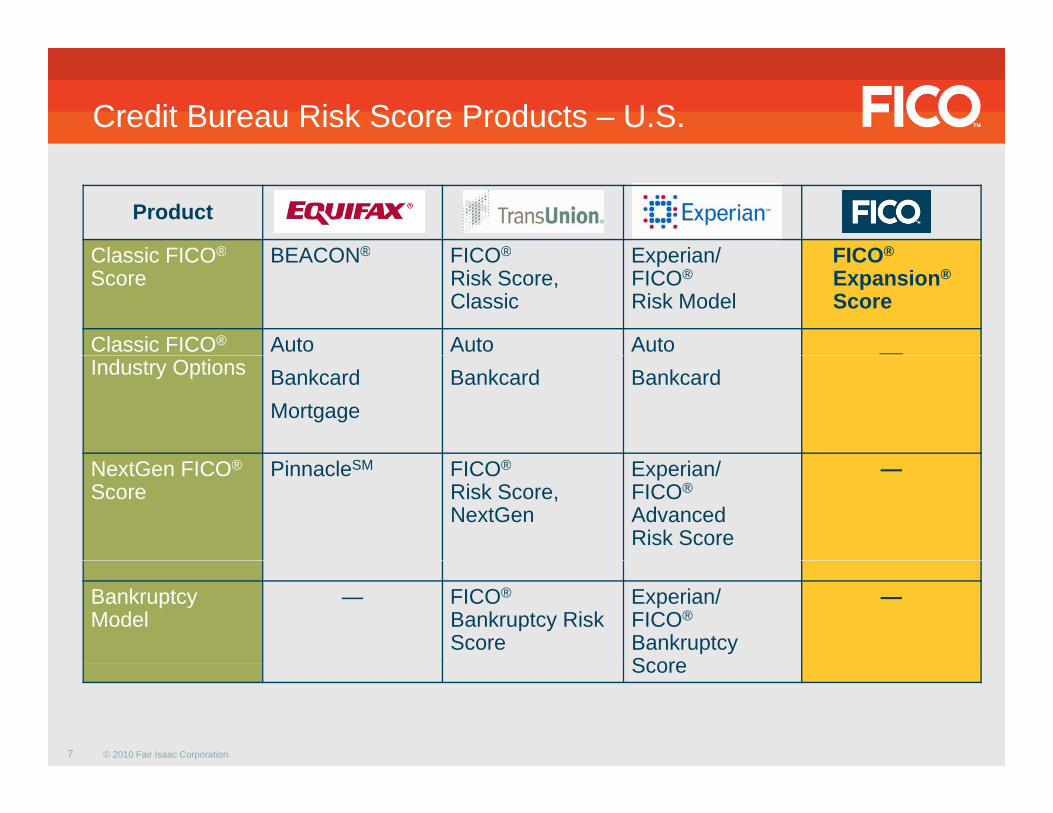

Credit Bureau Risk Score Products – U.S.

Product

Classic FICO® BEACON® FICO® Experian/ FICO®Classic FICO®

ScoreBEACON® FICO®

Risk Score, Classic

Experian/FICO®

Risk Model

FICO®

Expansion®

Score

Classic FICO® Auto Auto Auto __Industry Options Bankcard

MortgageBankcard Bankcard

__

NextGen FICO®

ScorePinnacleSM FICO®

Risk Score, NextGen

Experian/FICO®

AdvancedRisk Score

—

Bankruptcy Model

— FICO®

Bankruptcy Risk Score

Experian/FICO®

Bankruptcy Score

—

7 © 2010 Fair Isaac Corporation.

Score

The Relationship “Web”

Consumers CreditGrantors

8 © 2010 Fair Isaac Corporation.

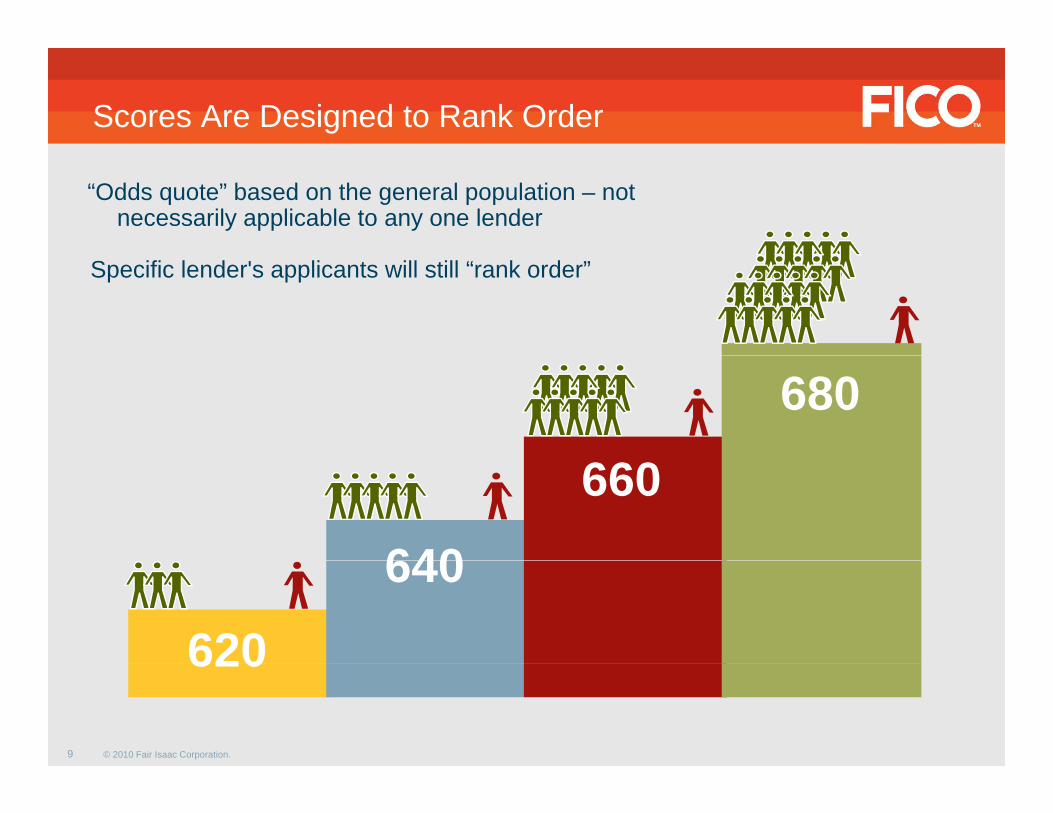

Scores Are Designed to Rank Order

“Odds quote” based on the general population – notnecessarily applicable to any one lender

Specific lender's applicants will still “rank order”

680

640

660

620

640

9 © 2010 Fair Isaac Corporation.

620

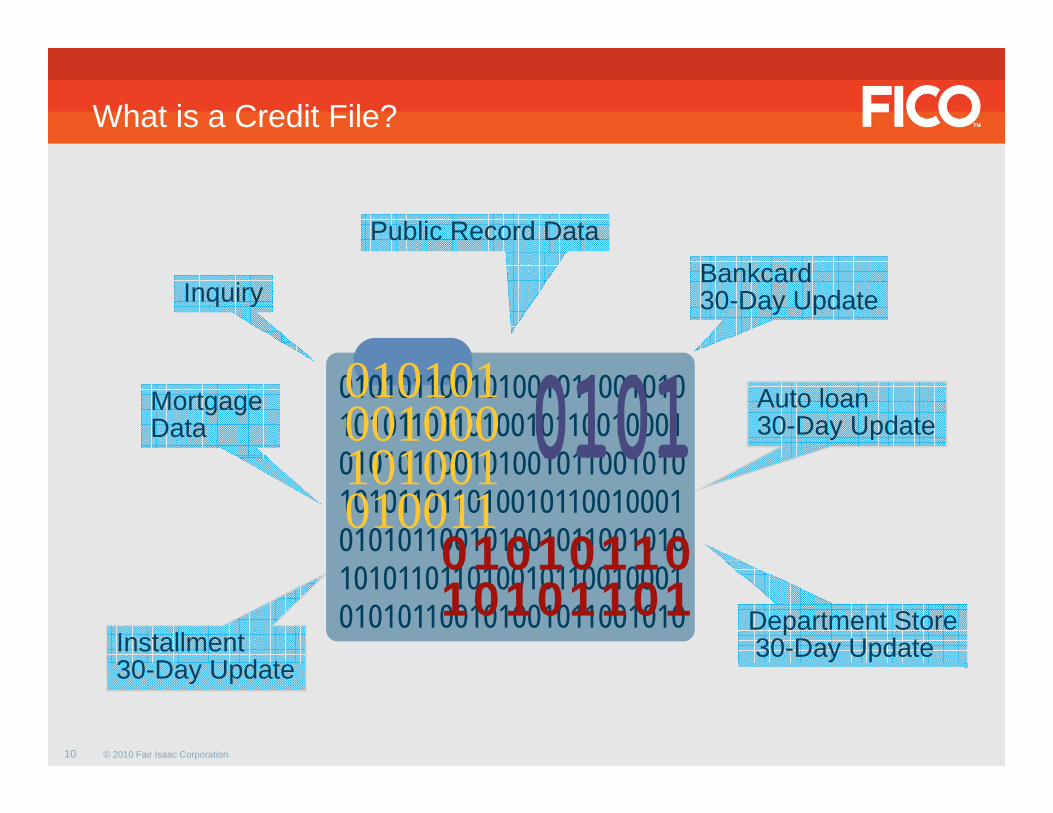

What is a Credit File?

Public Record DataBankcard30-Day UpdateInquiry

Mortgage Data

Auto loan30-Day Update

010101100101001011001010101011011010010110010001010101100101001011001010

010101001000101001 010101010110010100101100101010101101101001011001000101010110010100101100101001010110

101001010011

0 0

Installment30 D U d t

Department Store30-Day Update

101011011010010110010001010101100101001011001010

0101011010101101

10 © 2010 Fair Isaac Corporation.

30-Day Update

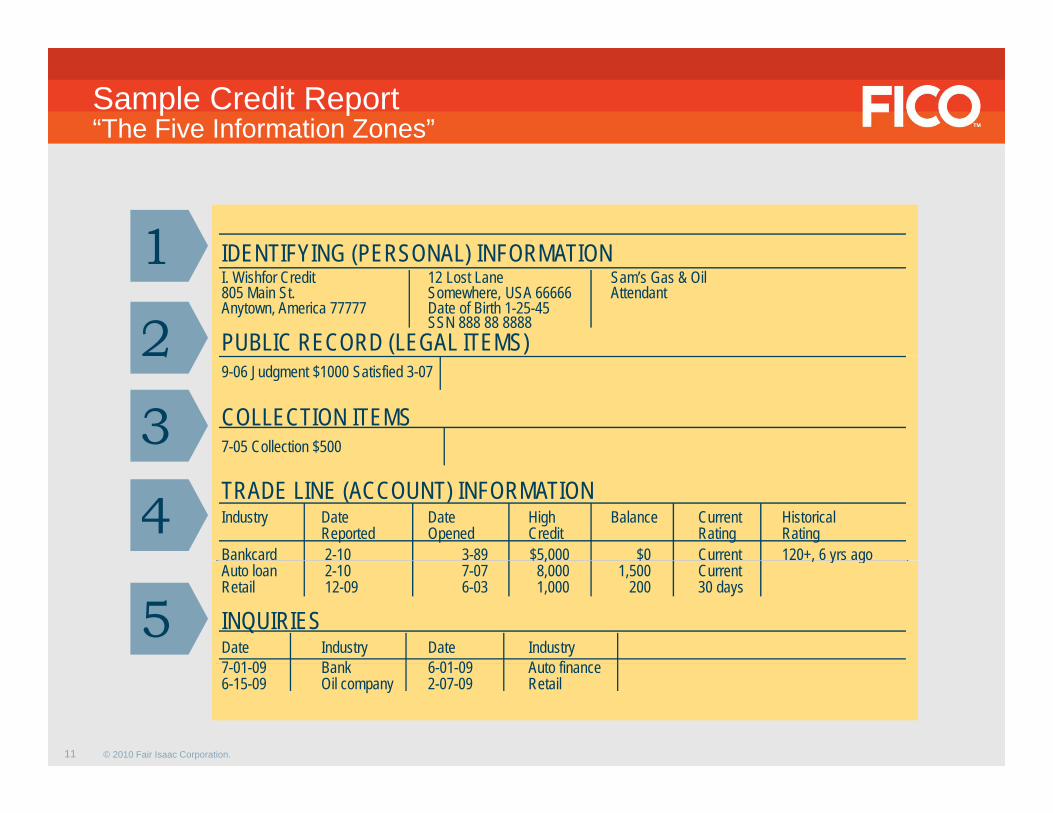

Sample Credit Report“The Five Information Zones”

IDENTIFYING (PERSONAL) INFORMATION1 IDENTIFYING (PERSONAL) INFORMATIONI. Wishfor Credit 12 Lost Lane Sam’s Gas & Oil805 Main St. Somewhere, USA 66666 AttendantAnytown, America 77777 Date of Birth 1-25-45

SSN 888 88 8888PUBLIC RECORD (LEGAL ITEMS)

1

2 ( )9-06 Judgment $1000 Satisfied 3-07

COLLECTION ITEMS7-05 Collection $500

2

3TRADE LINE (ACCOUNT) INFORMATIONIndustry Date Date High Balance Current Historical

Reported Opened Credit Rating RatingBankcard 2-10 3-89 $5,000 $0 Current 120+, 6 yrs ago

4$ , $ , y g

Auto loan 2-10 7-07 8,000 1,500 CurrentRetail 12-09 6-03 1,000 200 30 days

INQUIRIESDate Industry Date Industry7 01 09 B k 6 01 09 A t fi

5

11 © 2010 Fair Isaac Corporation.

7-01-09 Bank 6-01-09 Auto finance6-15-09 Oil company 2-07-09 Retail

FICO® Score Predictive Information

CONSIDERED NOT CONSIDERED

Tradelines

CONSIDERED NOT CONSIDERED

Age

Inquiries

Collections

Address

Employment

Public Records

p y

Income

GenderGender

12 © 2010 Fair Isaac Corporation.

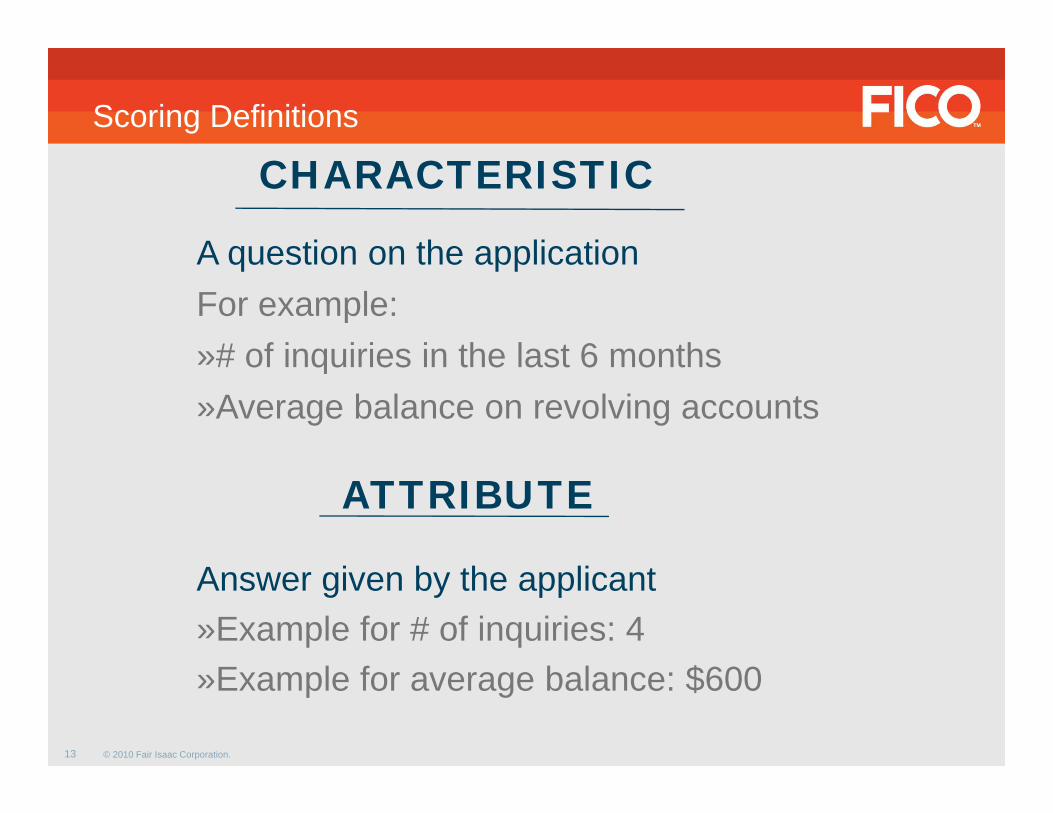

Scoring Definitions

CHARACTERISTIC

A question on the applicationA question on the applicationFor example:»# of inquiries in the last 6 months»# of inquiries in the last 6 months»Average balance on revolving accounts

ATTRIBUTE

Answer given by the applicant»Example for # of inquiries: 4

13 © 2010 Fair Isaac Corporation.

»Example for average balance: $600

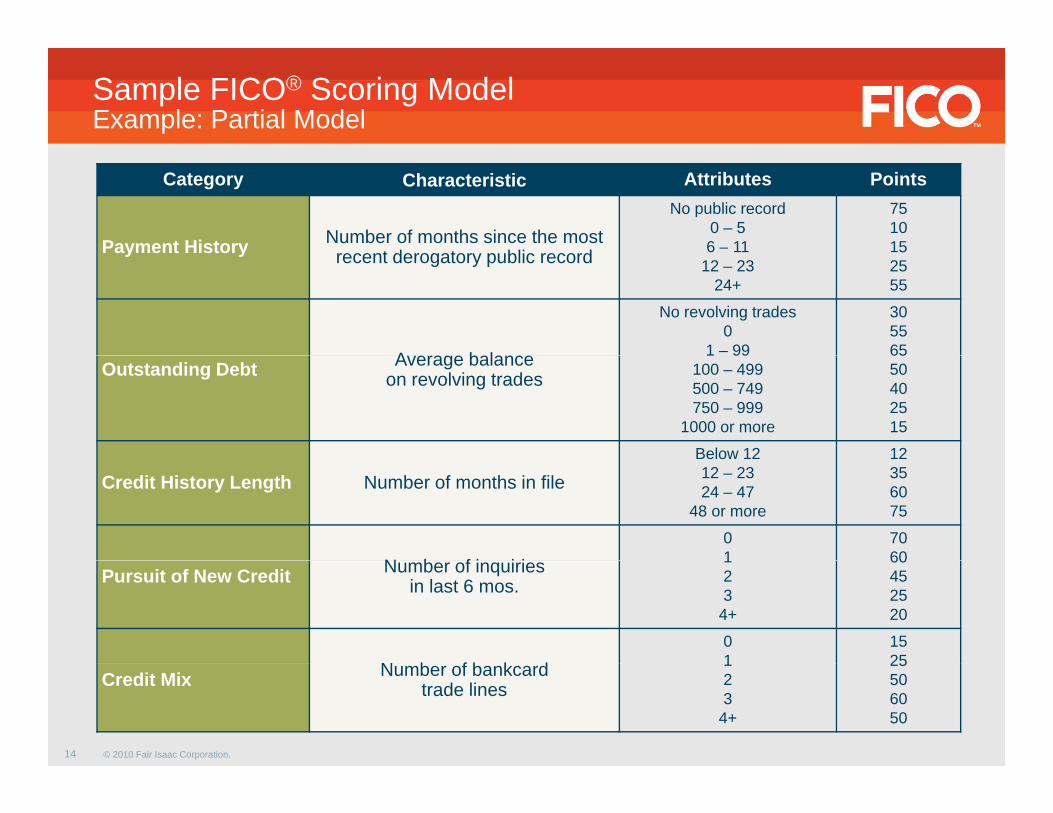

Sample FICO® Scoring ModelExample: Partial Model

Category Characteristic Attributes Points

Payment History Number of months since the mostt d t bli d

No public record0 – 56 – 11

751015Payment History recent derogatory public record 12 – 23

24+2555

A b l

No revolving trades0

1 – 99

305565

Outstanding Debt Average balance on revolving trades

1 99100 – 499500 – 749750 – 999

1000 or more

6550402515

Below 12 12

Credit History Length Number of months in fileBelow 1212 – 2324 – 47

48 or more

12356075

N b f i i i01

7060

Pursuit of New Credit Number of inquiries in last 6 mos.

123

4+

60452520

N b f b k d01

1525

14 © 2010 Fair Isaac Corporation.

Credit Mix Number of bankcard trade lines

123

4+

25506050

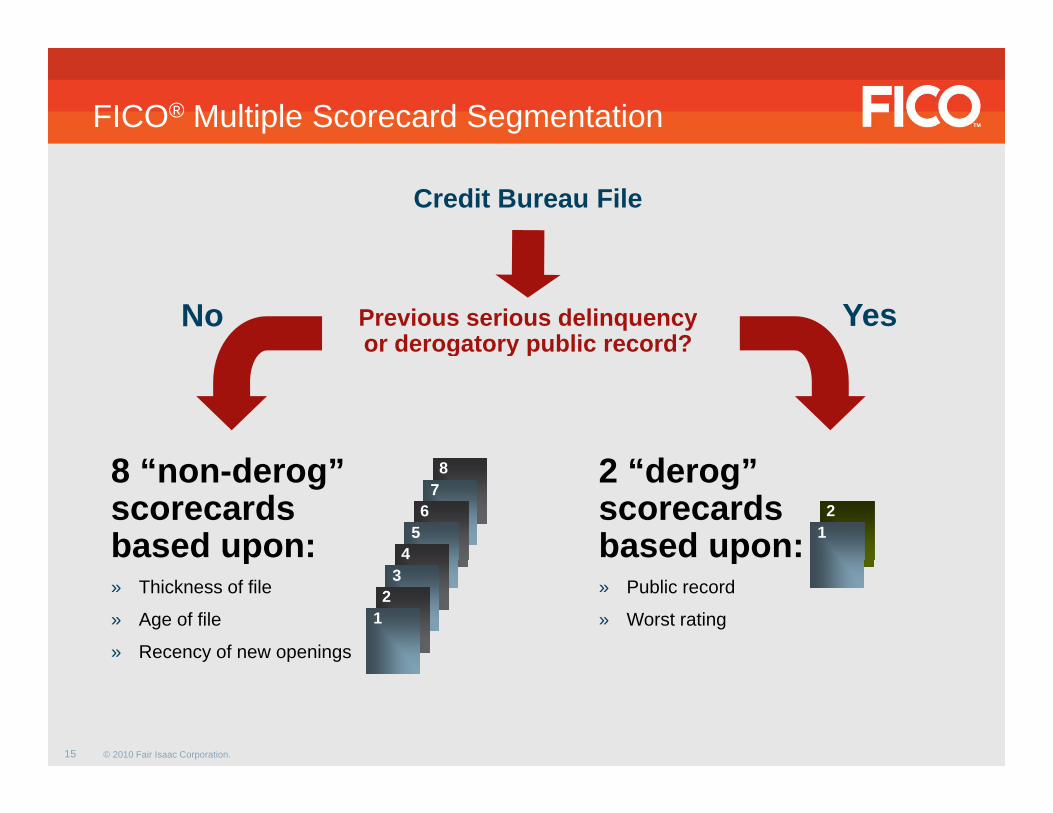

FICO® Multiple Scorecard Segmentation

Credit Bureau File

Previous serious delinquencyor derogatory public record?

YesNog y p

2 “d ”8 “ d ” 2 “derog” scorecards based upon:

8 “non-derog” scorecards based upon:

87

65

4

21p

» Public record

» Worst rating

p» Thickness of file

» Age of file

» Recency of new openings

32

1

15 © 2010 Fair Isaac Corporation.

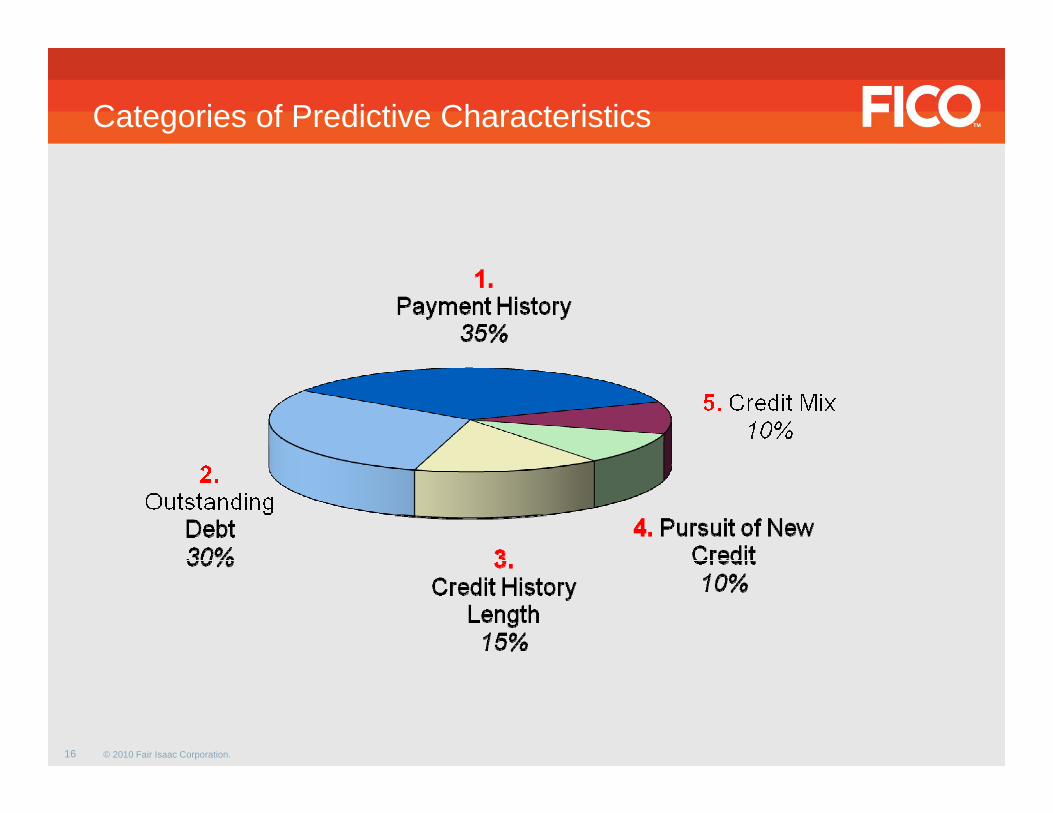

Categories of Predictive Characteristics

16 © 2010 Fair Isaac Corporation.

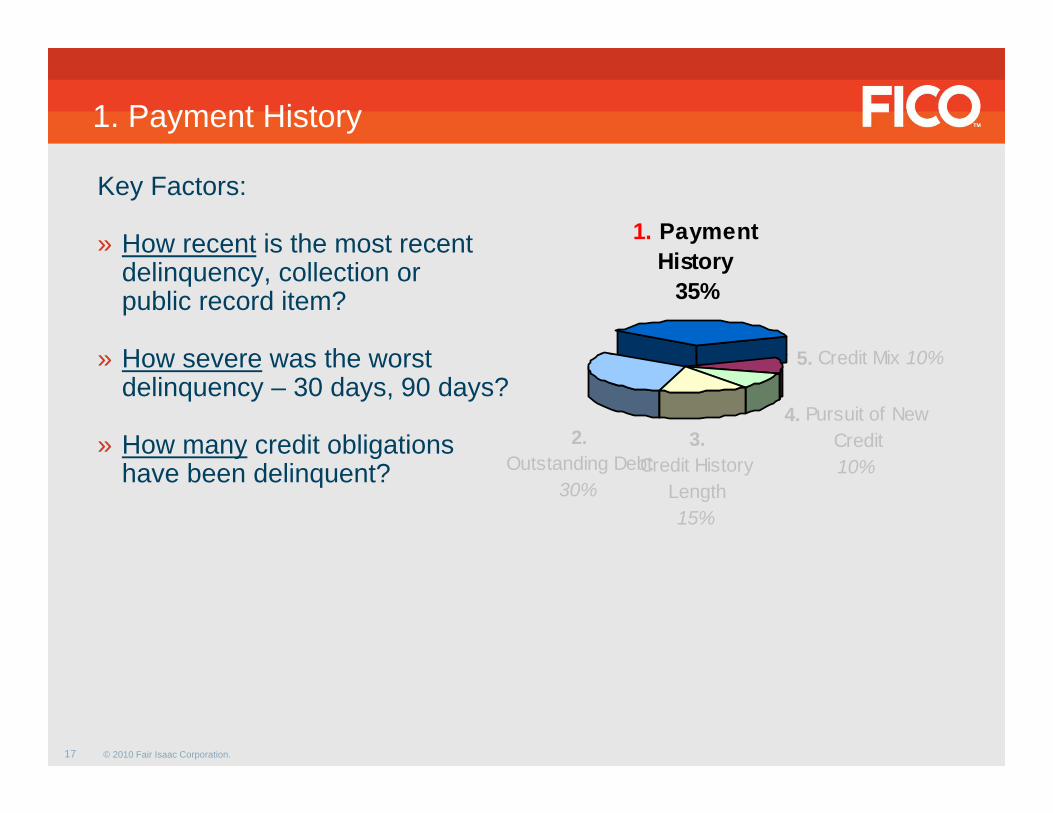

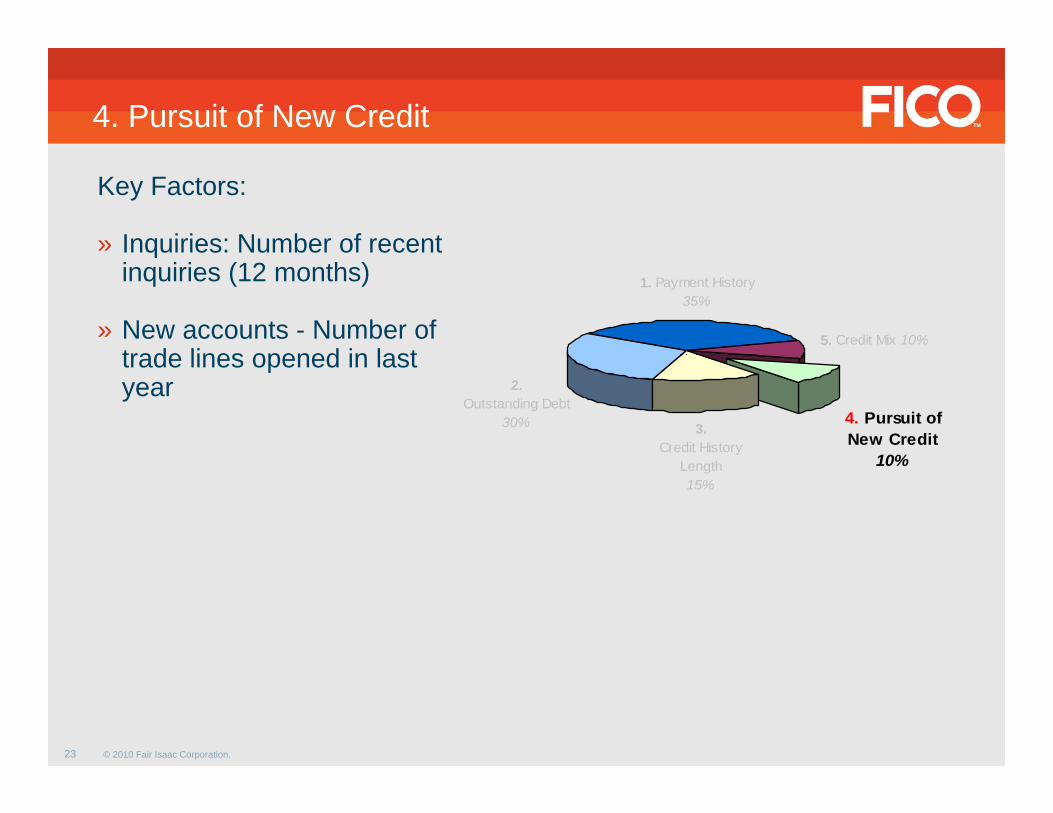

1. Payment History

Key Factors:

» How recent is the most recent 1. Payment Hi tdelinquency, collection or

public record item?

» How severe was the worst

History35%

5 Credit Mix 10%» How severe was the worst delinquency – 30 days, 90 days?

» How many credit obligations 4. Pursuit of New

Credit3. C di Hi

2. O t t di D bt

5. Credit Mix 10%

y ghave been delinquent? 10%Credit History

Length15%

Outstanding Debt30%

17 © 2010 Fair Isaac Corporation.

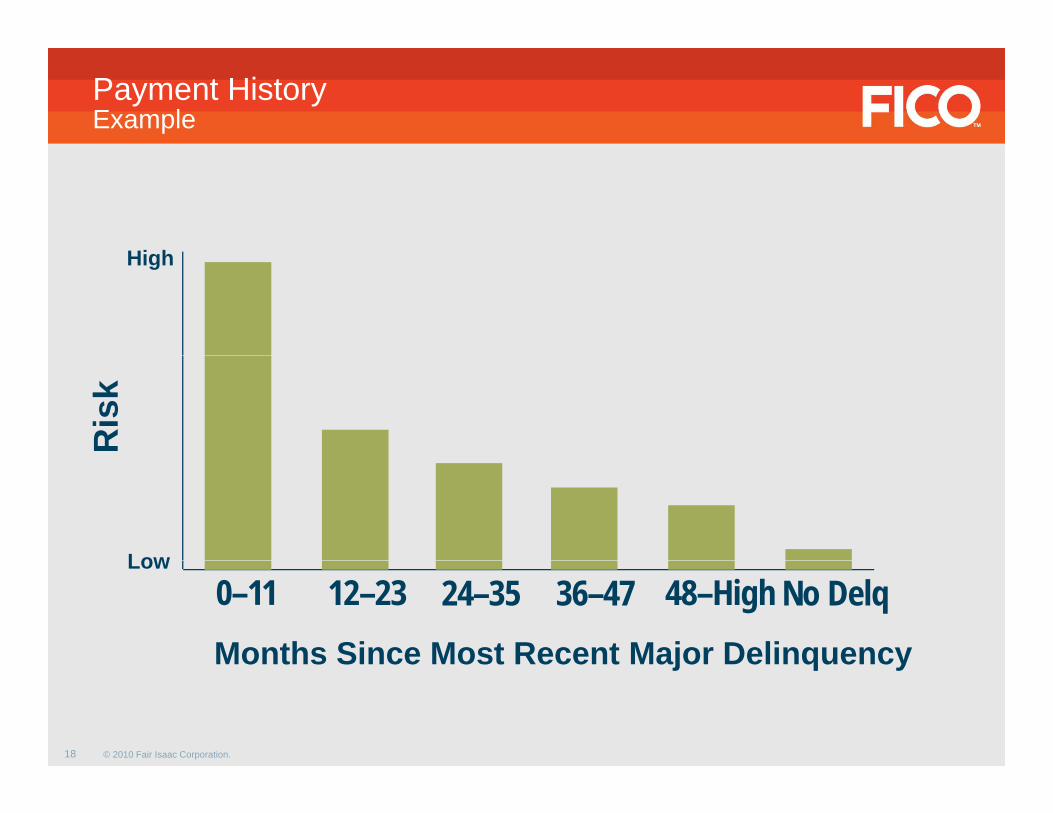

Payment HistoryExample

Hi hHigh

Ris

k

Low

Months Since Most Recent Major Delinquency

Low0–11 24–35 36–47 48–High No Delq12–23

18 © 2010 Fair Isaac Corporation.

Months Since Most Recent Major Delinquency

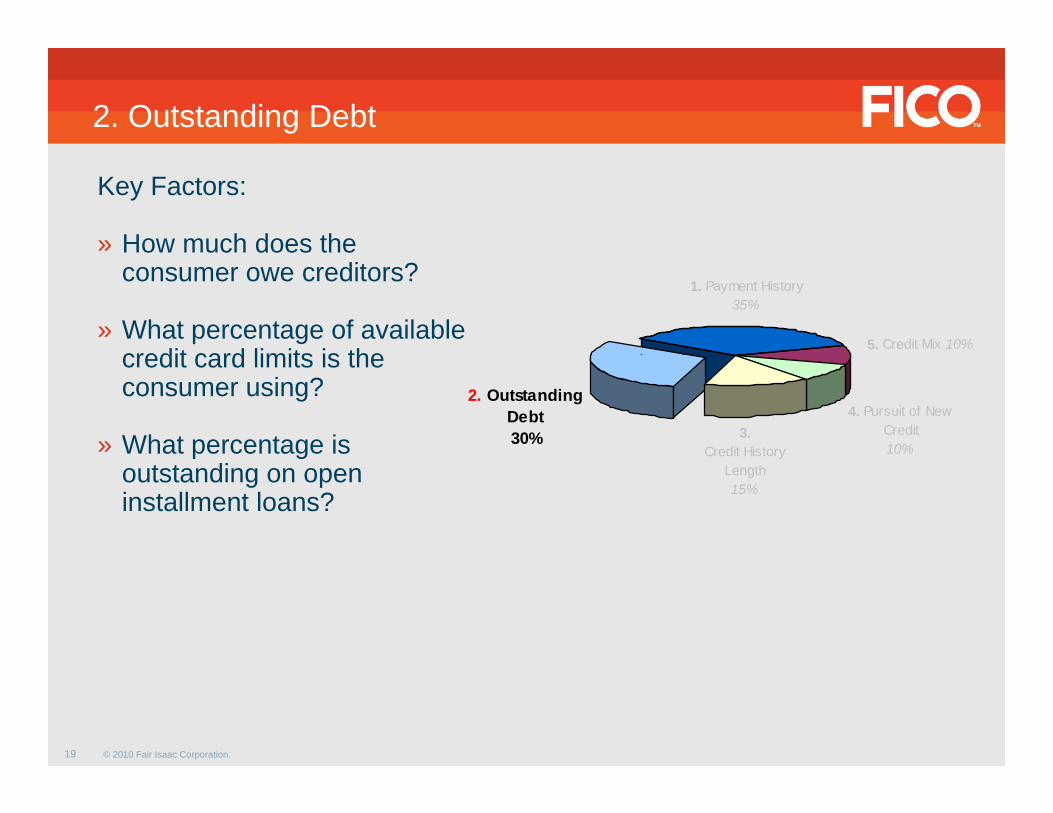

2. Outstanding Debt

Key Factors:

» How much does the consumer owe creditors?

» What percentage of available credit card limits is the

1. Payment History35%

5. Credit Mix 10%credit card limits is the consumer using?

» What percentage is 4. Pursuit of New

Credit10%

3. Credit History

2. Outstanding Debt30%p g

outstanding on open installment loans?

yLength15%

19 © 2010 Fair Isaac Corporation.

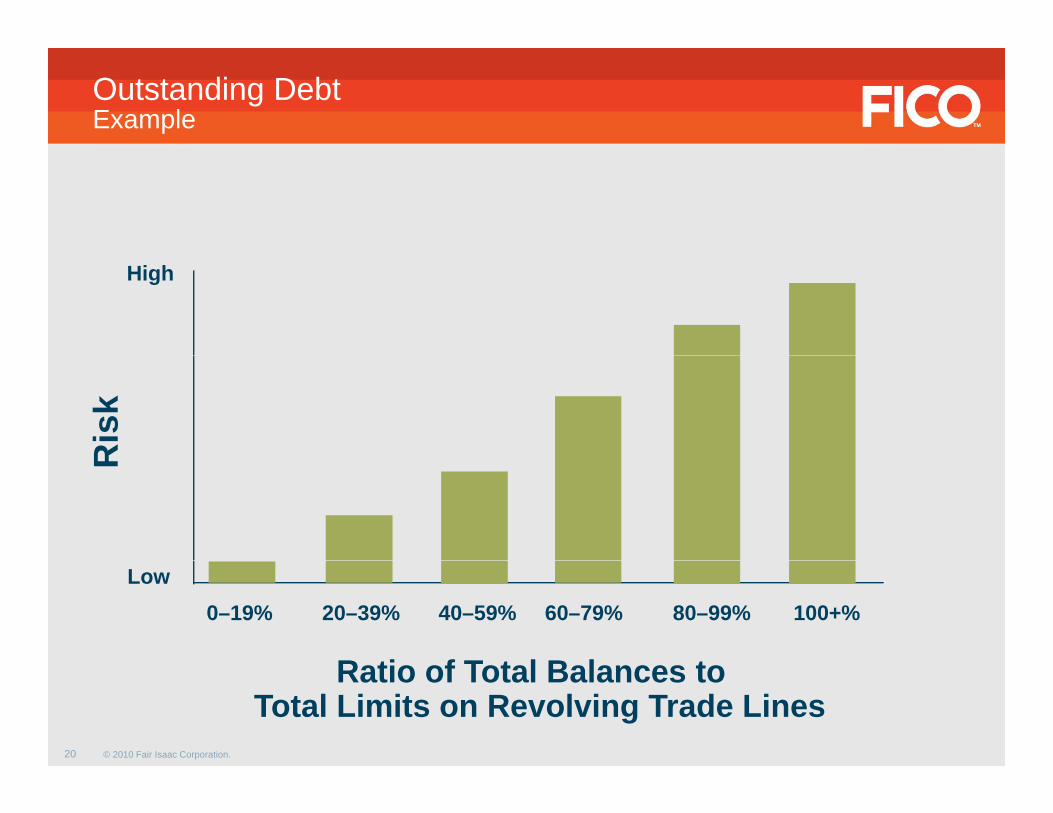

Outstanding DebtExample

High

Ris

kR

R ti f T t l B l t

0–19% 40–59% 60–79% 80–99% 100+%20–39%Low

20 © 2010 Fair Isaac Corporation.

Ratio of Total Balances to Total Limits on Revolving Trade Lines

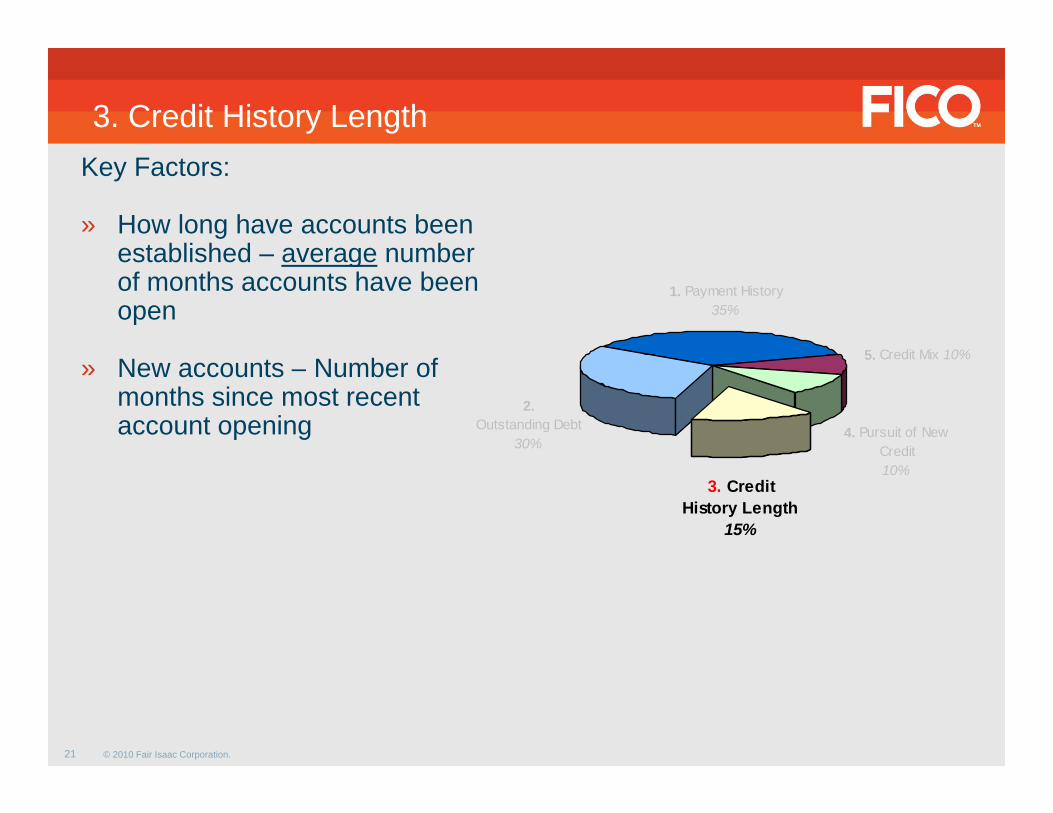

3. Credit History LengthKey Factors:

» How long have accounts been established average numberestablished – average number of months accounts have been open

1. Payment History35%

5 Credit Mix 10%» New accounts – Number of

months since most recent account opening 4. Pursuit of New

Credit

2. Outstanding Debt

30%

5. Credit Mix 10%

10%3. Credit

History Length15%

21 © 2010 Fair Isaac Corporation.

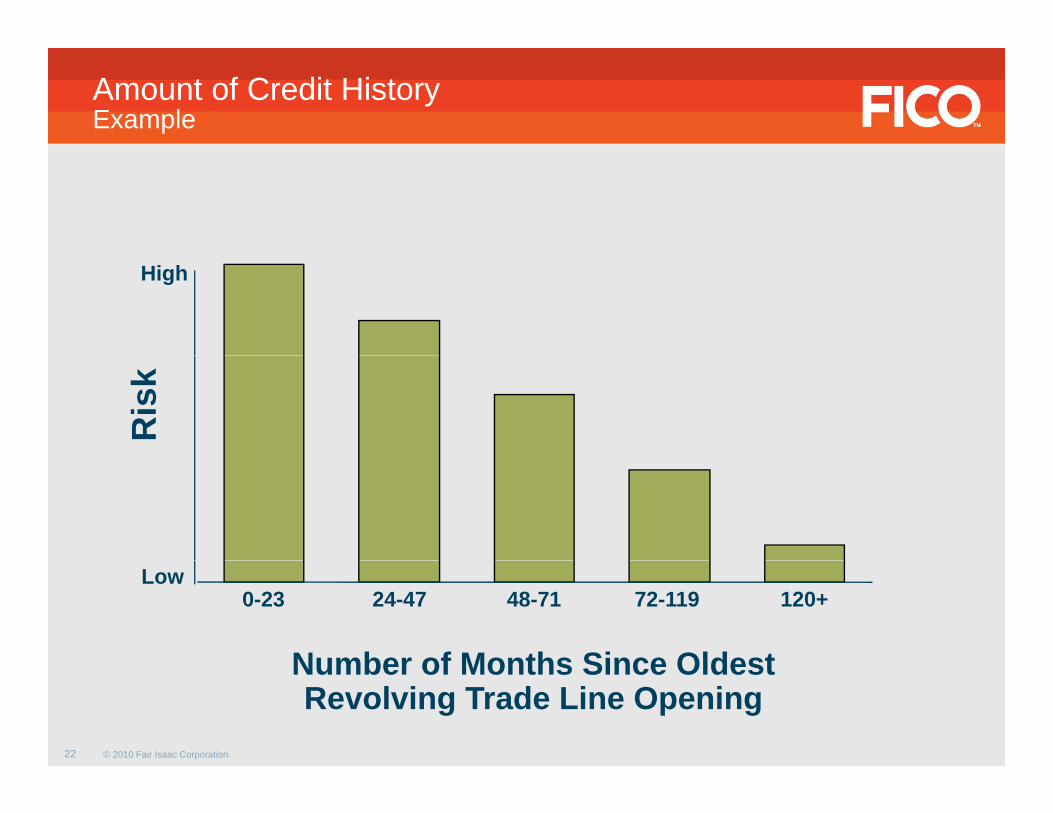

Amount of Credit HistoryExample

High

Ris

k

0-23 24-47 48-71 72-119 120+

Number of Months Since Oldest

Low

22 © 2010 Fair Isaac Corporation.

Number of Months Since Oldest Revolving Trade Line Opening

4. Pursuit of New Credit

Key Factors:

» Inquiries: Number of recent qinquiries (12 months)

» New accounts - Number of trade lines opened in last

1. Payment History35%

5. Credit Mix 10%

trade lines opened in last year

4. Pursuit of New Credit

10%

3. Credit History

2. Outstanding Debt

30%

10%Length15%

23 © 2010 Fair Isaac Corporation.

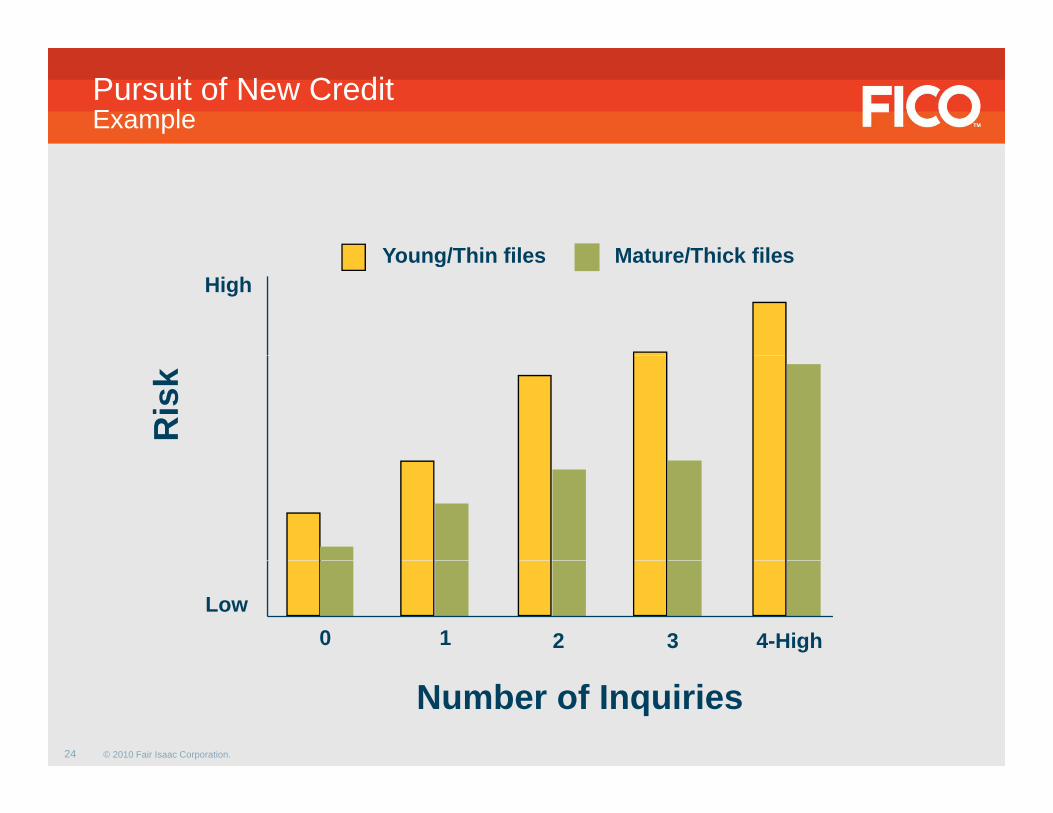

Pursuit of New CreditExample

Young/Thin files Mature/Thick filesYoung/Thin files Mature/Thick filesHigh

Ris

k

2 3 4-High0 1Low

24 © 2010 Fair Isaac Corporation.

Number of Inquiries

Types of Inquiries

» FICO® scores only consider consumer-initiated inquiries posted in the last 12 months

» FICO® scores do not consider the following inquiries:» Promotional inquiries» Account review inquiriesq» Consumer disclosure inquiries» Insurance inquiries» Employment inquiries» Employment inquiries

25 © 2010 Fair Isaac Corporation.

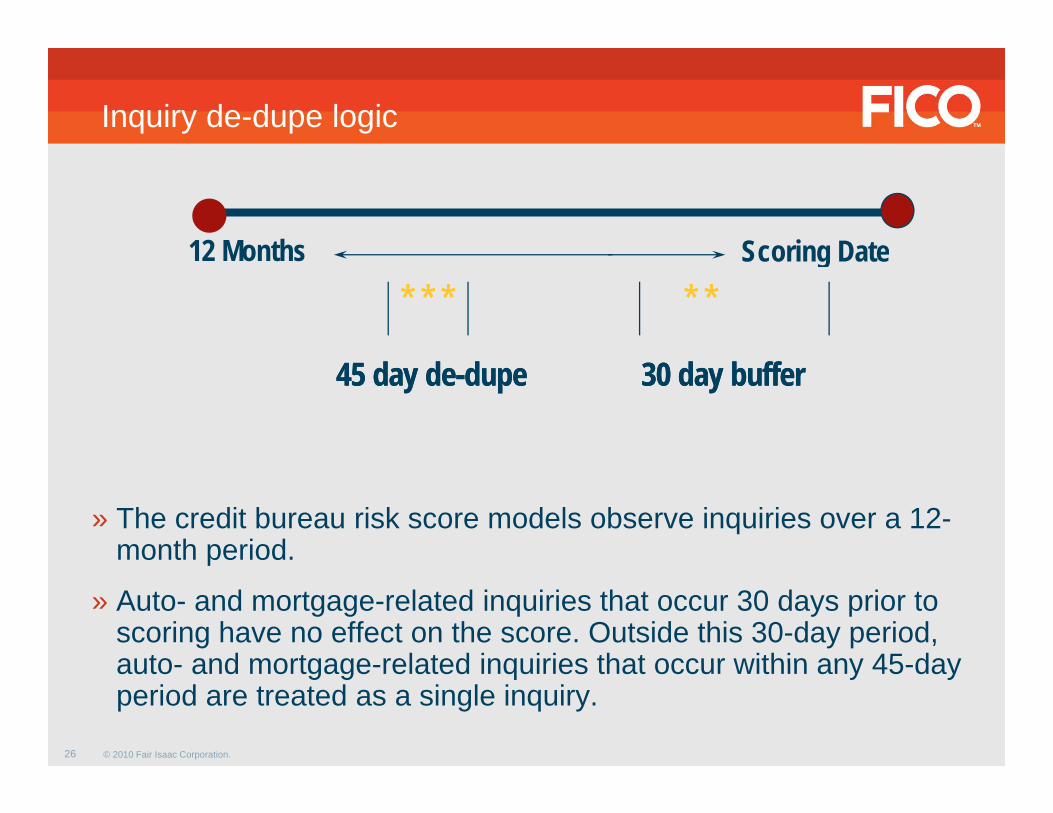

Inquiry de-dupe logic

12 Months Scoring Date* * ** * * * * * *

12 Months Scoring Date

45 day de45 day de--dupedupe 30 day buffer30 day buffer

» The credit bureau risk score models observe inquiries over a 12-month period. p

» Auto- and mortgage-related inquiries that occur 30 days prior to scoring have no effect on the score. Outside this 30-day period, auto and mortgage related inquiries that occur within any 45 day

26 © 2010 Fair Isaac Corporation.

auto- and mortgage-related inquiries that occur within any 45-day period are treated as a single inquiry.

5. Credit MixKey Factors:

» What is the mix of credit product types?product types?

» Revolving credit – number of bankcard trade lines

1. Payment History35%

5. Credit Mix 10%

» Installment credit – percent of trade lines that are installment loans

4. Pursuit of New Credit10%

3. C dit Hi t

2. Outstanding Debt

30%

10%

installment loans 10%Credit History Length15%

27 © 2010 Fair Isaac Corporation.

f CO SPreview of Full FICO World SessionPresented by multiple FICO experts

» FICO Score Basics» Use of Scores Across the Account Lifecycle» Tracking and Monitoring» Risk Management – Customer Management» Risk Management – Originationsg g

28 © 2010 Fair Isaac Corporation. © 2010 Fair Isaac Corporation. 28

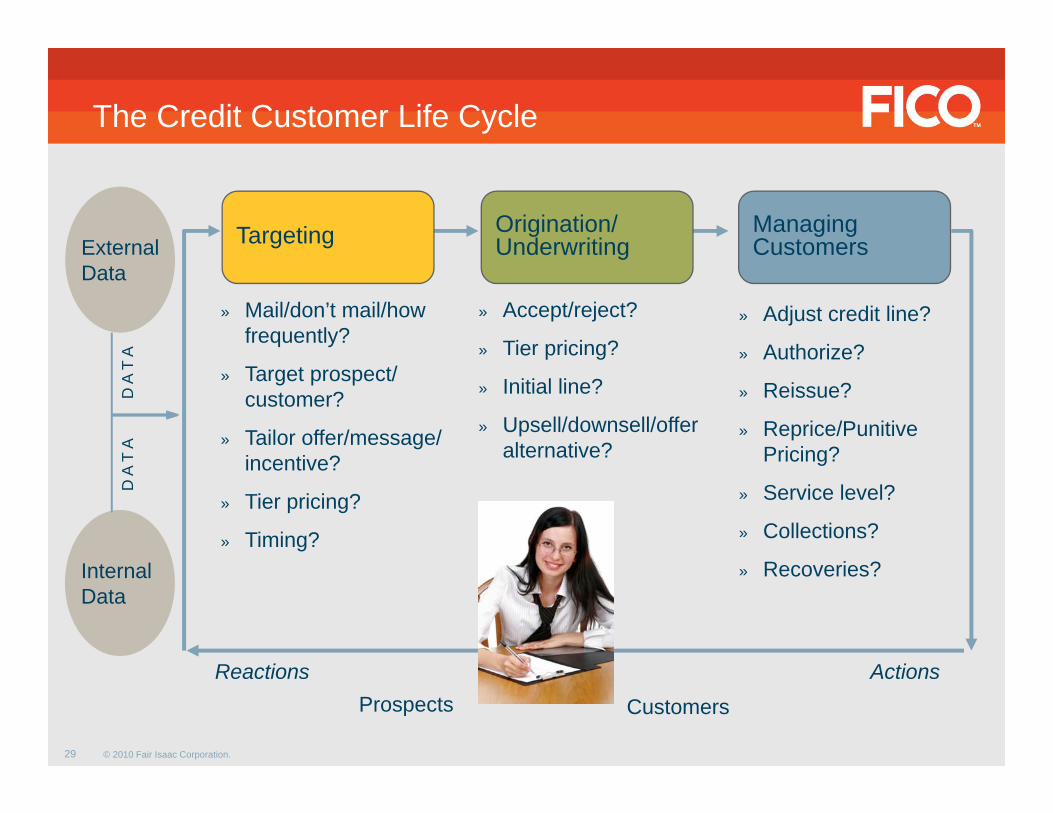

The Credit Customer Life Cycle

Targeting Origination/Underwriting

ManagingCustomersExternal

» Mail/don’t mail/how frequently?

» Accept/reject?

» Tier pricing? » Adjust credit line?

» Authorize?

Underwriting CustomersExternalData

A

» Target prospect/ customer?

» Tailor offer/message/ i ti ?

e p c g

» Initial line?

» Upsell/downsell/offer alternative?

» Authorize?

» Reissue?

» Reprice/Punitive Pricing?

D A

T A

T A

incentive?

» Tier pricing?

» Timing?

Pricing?

» Service level?

» Collections?

D A

T

» Recoveries?InternalData

29 © 2010 Fair Isaac Corporation.

Prospects CustomersActionsReactions

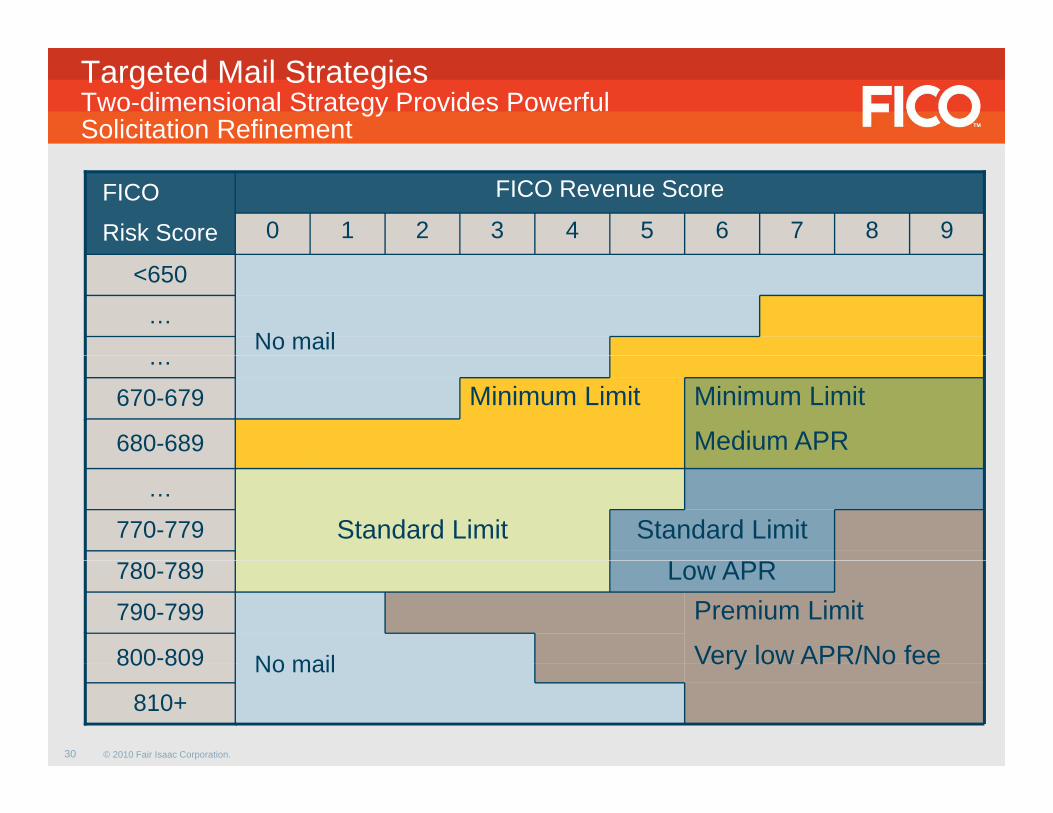

Targeted Mail StrategiesTwo-dimensional Strategy Provides PowerfulSolicitation Refinement

9876543210

FICO Revenue ScoreFICO

Risk Score

…

<650

No mail

680-689

Minimum Limit

Medium APR

Minimum Limit670-679

…

Standard LimitStandard Limit770-779

…

Low APR

800-809

Premium Limit

Very low APR/No fee790-799

780-789

No mail

30 © 2010 Fair Isaac Corporation.

810+

800 809 Very low APR/No feeNo mail

f CO SPreview of Full FICO World SessionPresented by multiple FICO experts

» FICO Score Basics» Use of Scores Across the Account Lifecycle» Tracking and Monitoring» Risk Management – Customer Management» Risk Management – Originationsg g

31 © 2010 Fair Isaac Corporation. © 2010 Fair Isaac Corporation. 31

Acceptance Rates Declining

100%

75%

50%%

25%25%

0%

32 © 2010 Fair Isaac Corporation.

J0%

F M A M J J A S O N D J F M A M J J

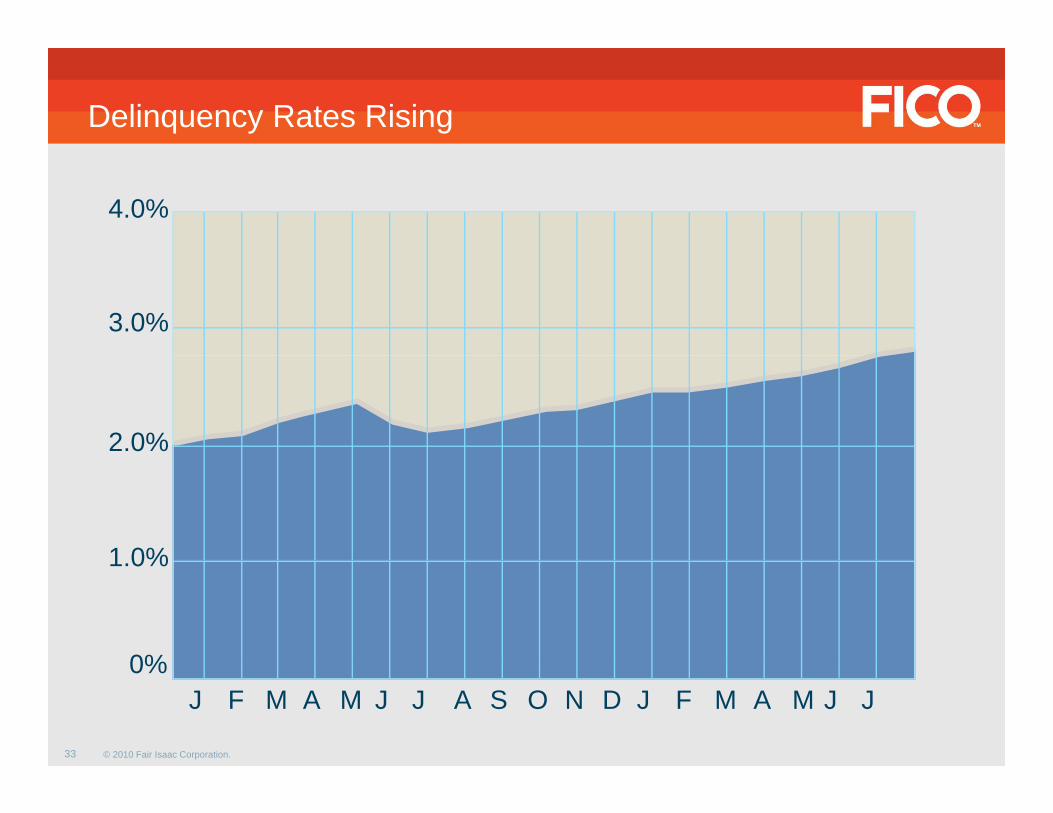

Delinquency Rates Rising

4.0%

3.0%

2.0%

1 0%1.0%

0%

33 © 2010 Fair Isaac Corporation.

J0%

F M A M J J A S O N D J F M A M J J

Summary

» FICO Score Basics

» In April please join us for this practical set of sessions included in p p j pyour registration price!

» The Full FICO World session include these additional sections» Use of Scores Across the Account Lifecycle» Use of Scores Across the Account Lifecycle» Tracking and Monitoring» Risk Management – Customer Fundamentals» Risk Management - Originations

» Learn with the experts, ask questions about your portfolio and take away sensible tips that you can use to be successful in your y p y yjob.

34 © 2010 Fair Isaac Corporation.

This webinar is a preview of a presentation at:presentation at:FICO World 2010April 13-16 Intercontinental MiamiApril 13 16 Intercontinental Miami

www.fico.com/ficoworld

K t P t Mi h l P tKeynote Presenter Michael PorterAuthor, On Competition, Competitive Strategy

90+ Presentations, Case Studies and WorkshopsF C lt ti ith FICO E t

35

This presentation is provided for the recipient only and cannot be reproduced or shared without Fair Isaac Corporation's express consent.© 2010 Fair Isaac Corporation.

Free Consultations with FICO Experts

Q&A

Julie [email protected]@

Get your 30% discount on FICO World registration!» Register at www.fico.com/ficoworld

Get your 30% discount on FICO World registration!» Register at www.fico.com/ficoworld» Register at www.fico.com/ficoworld» Use code WEB70

Join us at these upcoming FICO World Previews

» Register at www.fico.com/ficoworld» Use code WEB70

Join us at these upcoming FICO World Previewsp g» March 3 - Solving the Top Issues in Collections & Recovery» March 17 - Improve Your Customers' Experience with Fraud

Management - Success Story

p g» March 3 - Solving the Top Issues in Collections & Recovery» March 17 - Improve Your Customers' Experience with Fraud

Management - Success StoryManagement Success StoryManagement Success Story

36

This presentation is provided for the recipient only and cannot be reproduced or shared without Fair Isaac Corporation's express consent.© 2010 Fair Isaac Corporation.