credit cards the good, the bad, and the ugly judith walker

TRANSCRIPT

Credit Cards

The Good, The Bad, and the Ugly

Judith Walker

History

• In the US first used in the 1920s to sell fuel to the growing number of car owners

• In 1938 companies started accepting each other’s cards

History

• Concept of paying merchants using a card developed by Ralph Schneider and Frank X. McNamara in 1950 to consolidate individual cards

• Diners Club produced the first charge card

• The BankAmericard was developed in 1958 and evolved into Visa

• MasterCard was introduced in 1966

Different Card Types

• Debit Card– Card directly connected to an account where

money is removed directly from that account

• Credit Card– Card issuer lends consumer money not in an

account, can revolve balance

• Charge Card (≠ Credit Card)– Similar to credit charge except in must be paid

in full each month

Merchants

• Second most secure form of payment – Most secure is cash in hand– Issuing bank commits to payment at the

moment of verification

• Merchant charged commission for the privilege of the service

• It is a privilege to be able to accept credit cards and it can be removed due to violations by the merchant

Number System

• The first digit in your credit-card number signifies the system: – 3 - travel/entertainment cards (Amer. Express & Diners Club) – 4 - Visa – 5 - MasterCard – 6 - Discover Card – Phone companies, gas companies and department stores have

their own numbering systems

How They Work – Consumer

• Consumer is approved for a certain level of credit based on income and credit history

• Electronic verification system (magnetic strip) verifies card validity and if there is sufficient credit to cover purchase

• Statement sent each month to consumer with total balance and payment requirements

Magstripe

• Magstripe – the magnetic strip on the back of the card– made up of tiny iron-based magnetic particles in a plastic-like film. Each

particle is really a tiny bar magnet about 20-millionths of an inch long

– The magstripe can be "written" because the tiny bar magnets can be magnetized in either a north or south pole direction. The magstripe is very similar to a piece of cassette tape

Credit Card – Pin

• PIN – personal identification number– The PIN is not on the card – it’s encrypted

(hidden in code) in a database– The PIN can be either in the bank's computers in

an encrypted form or encrypted on the card itself – The transformation used in this type of

cryptography is called one-way– This feature was designed to protect the

cardholder from being impersonated by someone who has access to the bank's computer files

Interest

• Pay in full each month, no interest accrued

• Not paid in full– Typically full interest on the entire outstanding

balance each month from the date of purchase if the balance is not paid

– Interest rates will jump drastically if late with just ONE payment

• In some cases rates will double• Often delinquency will result in rates of 25-30%

Interest

• 4 common methods of charging interest– Detailed in Regulation Z of the Truth in

Lending Act• Average Daily Balance

• Two-Cycle Average Daily Balance

• Adjusted Balance

• Previous Balance

• The UK uses the Daily Accrual method

Incentives

• Frequent Flyer Miles

• Gift certificates

• Cash back (usually

one 1%)

• Donation to charity or

cause

– Environmental

– National Geographic

Credit Score

• Three-digit rating that

estimates how

‘trustworthy’

concerning

repayment

• Affects loan

qualification, credit

limits, interest rates

FICO Score

• Best known US credit score– Developed by Fair Isaac Corporation

• Use a statistical model to generate a score and compare with other individuals with similar history

• Models subject to federal regulation– Regulation B

• Specific reasons must be given for denial

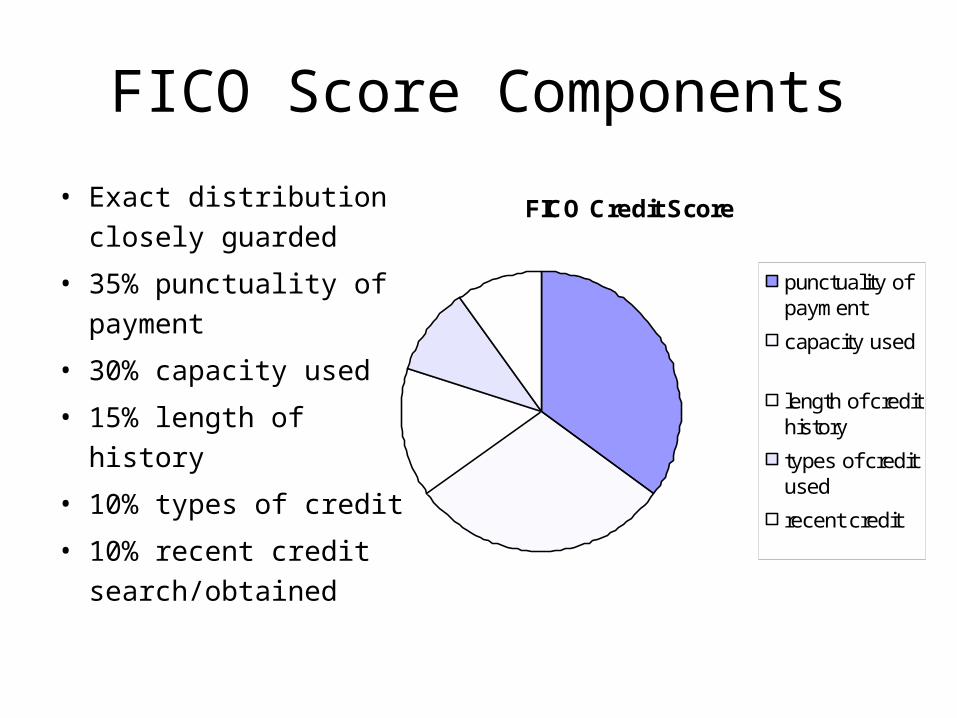

FICO Credit Score

punctuality ofpayment

capacity used

length of credithistory

types of creditused

recent credit

FICO Score Components

• Exact distribution

closely guarded

• 35% punctuality of

payment

• 30% capacity used

• 15% length of history

• 10% types of credit

• 10% recent credit

search/obtained

FICO Score

• Current income and

employment history do

not factor into the score

but are weighed when

applying for credit

• Range from 300 to 850– US median around 725

– Score >720 good

– Score <600 poor

How to Improve Credit Score

• Check report for accuracy

• Pay on time

• Clean up derogatory statements

• Decrease capacity used

• Establish a credit history

• Minimize damage in difficult times

• Limit credit inquiries

Secured Credit Cards

• Credit card secured by a deposit account owned by the cardholder– Generally 100% to 200% of the desired credit– Still make payments as if it was a regular

credit card– Default on payment, lose security and can

accrue additional debt due to interest

• Sometimes the only option to rebuild credit

Fair Credit Reporting Act

• American Federal Law– 15 U.S.C. § 1681

• Regulates the collection, dissemination, and use of consumer credit information

• Regulates credit reporting agencies

• In 2003 the act was amended to guard against identity theft

Credit Card Fraud

• The type of fraud where a merchant is accepts a card under the assumption the account will provide payment

• Later the merchant does not receive payment or it is reclaimed by the issuing bank

• Today half of all credit card fraud is conducted online

Types of Fraud

• Mail Non-Receipt– Theft of mail containing a replacement card

• Chargeback Fraud– Bank notified that illegal purchases were

made and they charge payment is taken back from the merchant

• Skimming– Merchant copies the magnetic strip illegally

Fraud Prevention

• Card-Present

– Signed receipt that

matches signature on

back of the credit card

– Show photo

identification

– Checking the last 4

digits on the card

Fraud Prevention

• Card Not Present

– Telephone or on-line

purchases

– Fax copies of the

credit card along with

photo identification

– Card Security Code on

the back of the credit

card