creating value through knowledge sharing -...

TRANSCRIPT

Creating value through knowledge sharingReal estate accounting

Subdivision and Housing Developers Association, Inc.

11 May 2016

www.pwc.com

Isla Lipana & Co., PwC member firm

Notice

The information presented herein is the property of Isla Lipana & Co., member firm of PricewaterhouseCoopers. Such information is provided for general guidance and not to be used as a substitute for reading the respective Philippine Financial Reporting Standards, Philippine Accounting Standards or Philippine Interpretations and do not constitute any type of professional advice. Unauthorized use of the information may violate copyright, trademark and other laws. Should this information be used for presentation purposes, the user must retain all copyright, trademark, or other similar notices contained in the original materials on any copies of the material.

Slide 2

11 May 2016SHDA Real Estate Accounting

Isla Lipana & Co., PwC member firm

Topic outline

Accounting for real estate sales

Current: Philippine Interpretations Committee (PIC) Q&A 2006-01, PAS 18

Future: Philippine Financial Reporting Standard (PFRS) 15

Slide 3

11 May 2016SHDA Real Estate Accounting

Isla Lipana & Co., PwC member firm

Current accounting for real estate sales

Slide 4

11 May 2016SHDA Real Estate Accounting

Isla Lipana & Co., PwC member firm

Current accounting for real estate sales

Standards and interpretations

PIC Q&A No. 2006–01: Revenue Recognition for Sale of Property Units under Pre-completion Contracts

Philippine Accounting Standard (PAS) 18: Revenue

Slide 5

11 May 2016SHDA Real Estate Accounting

Isla Lipana & Co., PwC member firm

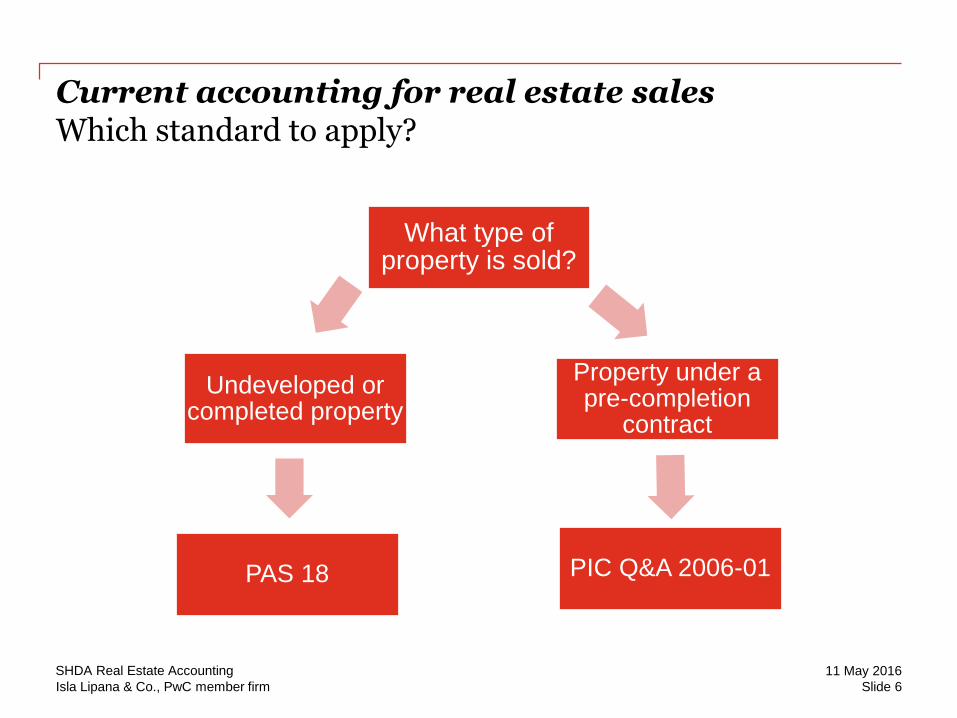

Current accounting for real estate salesWhich standard to apply?

What type of property is sold?

Property under a pre-completion

contract

PIC Q&A 2006-01PAS 18

Undeveloped or completed property

Slide 6

11 May 2016SHDA Real Estate Accounting

Isla Lipana & Co., PwC member firm

Current accounting for real estate salesUndeveloped or completed property

PAS 18, Revenue

Revenue is recognized when the following are met:

a) Risks and rewards of ownership of the goods transferred to the buyer

b) Seller retains no continuing managerial involvement

c) Revenue can be measured reliably

d) Probable that economic benefits will flow to the entity

e) Costs can be measured reliably

Slide 7

11 May 2016SHDA Real Estate Accounting

Isla Lipana & Co., PwC member firm

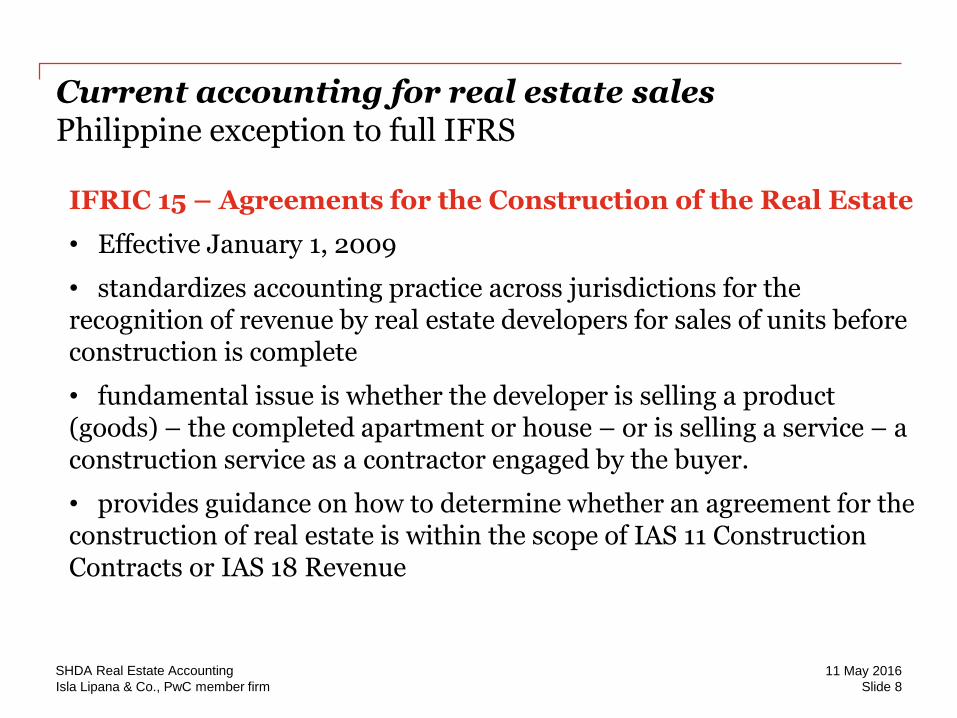

Current accounting for real estate salesPhilippine exception to full IFRS

IFRIC 15 – Agreements for the Construction of the Real Estate

• Effective January 1, 2009

• standardizes accounting practice across jurisdictions for the recognition of revenue by real estate developers for sales of units before construction is complete

• fundamental issue is whether the developer is selling a product (goods) – the completed apartment or house – or is selling a service – a construction service as a contractor engaged by the buyer.

• provides guidance on how to determine whether an agreement for the construction of real estate is within the scope of IAS 11 Construction Contracts or IAS 18 Revenue

Slide 8

11 May 2016SHDA Real Estate Accounting

Isla Lipana & Co., PwC member firm

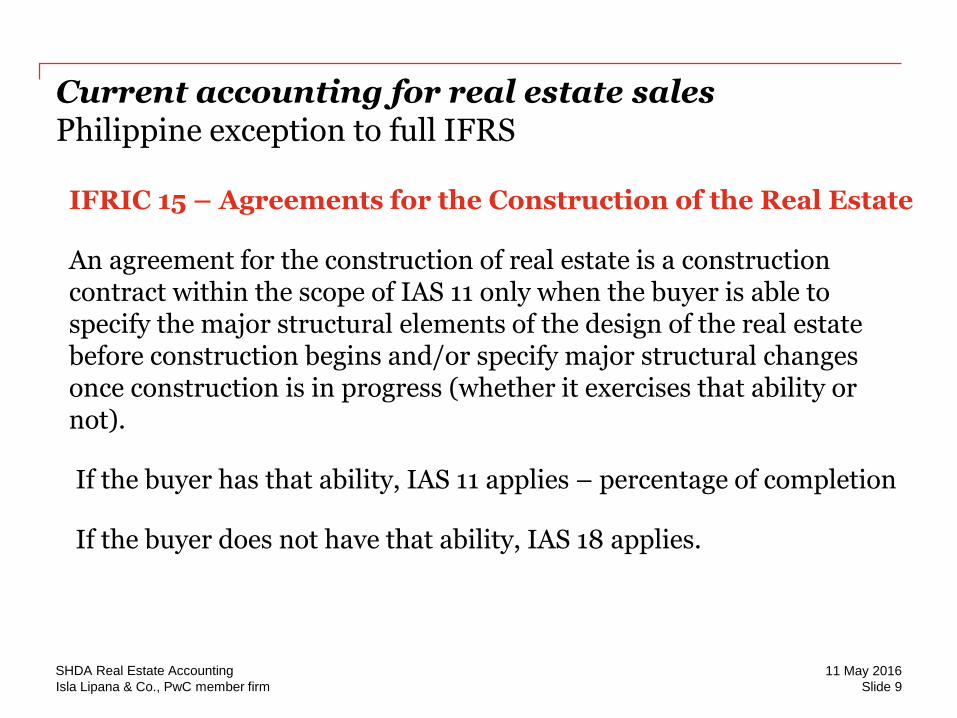

Current accounting for real estate salesPhilippine exception to full IFRS

IFRIC 15 – Agreements for the Construction of the Real Estate

An agreement for the construction of real estate is a construction contract within the scope of IAS 11 only when the buyer is able to specify the major structural elements of the design of the real estate before construction begins and/or specify major structural changes once construction is in progress (whether it exercises that ability or not).

If the buyer has that ability, IAS 11 applies – percentage of completion

If the buyer does not have that ability, IAS 18 applies.

Slide 9

11 May 2016SHDA Real Estate Accounting

Isla Lipana & Co., PwC member firm

Current accounting for real estate salesPhilippine exception to full IFRS

IFRIC 15 – Agreements for the Construction of the Real Estate

If IAS 18 applies,

Is it only construction service ? - percentage of completion.

But if the entity is required to provide services together with construction materials in order to perform its contractual obligation to deliver real estate to the buyer, the agreement is accounted for as the sale of goods under IAS 18.

Slide 10

11 May 2016SHDA Real Estate Accounting

Isla Lipana & Co., PwC member firm

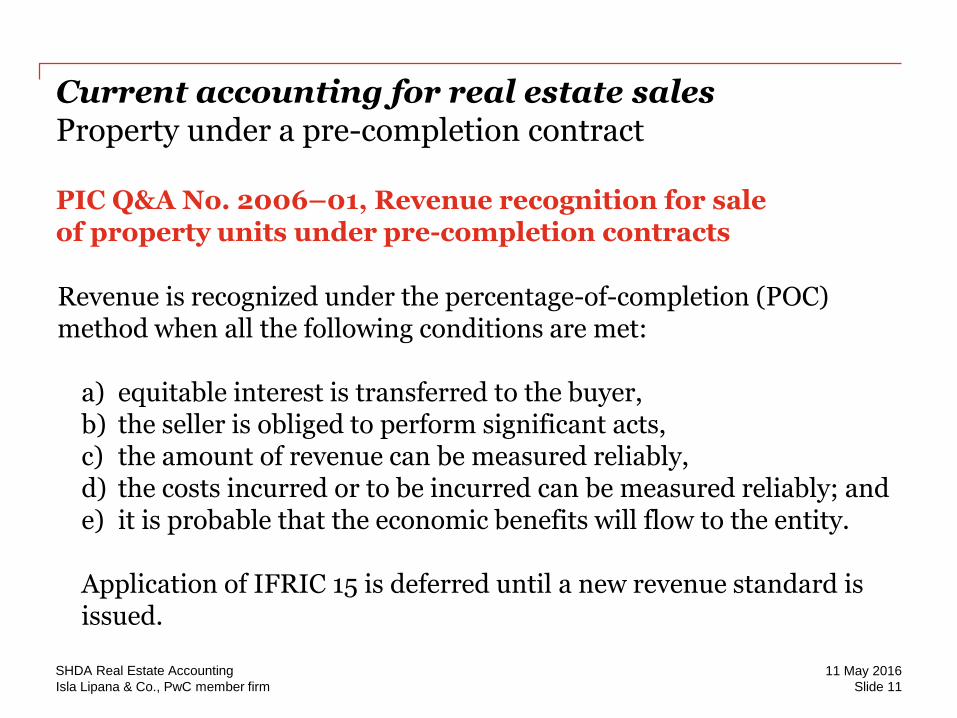

Current accounting for real estate salesProperty under a pre-completion contract

PIC Q&A No. 2006–01, Revenue recognition for saleof property units under pre-completion contracts

Revenue is recognized under the percentage-of-completion (POC) method when all the following conditions are met:

a) equitable interest is transferred to the buyer,b) the seller is obliged to perform significant acts, c) the amount of revenue can be measured reliably,d) the costs incurred or to be incurred can be measured reliably; ande) it is probable that the economic benefits will flow to the entity.

Application of IFRIC 15 is deferred until a new revenue standard is issued.

Slide 11

11 May 2016SHDA Real Estate Accounting

Isla Lipana & Co., PwC member firm

Current accounting for real estate sales

Accounting method under PIC Q&A 2006-01

Percentage-of-completion method

Cost-to-cost

Milestone (engineer’s estimate)

Slide 12

11 May 2016SHDA Real Estate Accounting

Isla Lipana & Co., PwC member firm

PFRS 15 - the future accounting for real estate sales

Slide 13

11 May 2016SHDA Real Estate Accounting

Isla Lipana & Co., PwC member firm

Future accounting for real estate sales

PFRS 15, Revenue from Contracts with Customers

Effective 1 January 2018

PFRS 15 establishes the principles for revenue recognition.

Revenue is recognized upon satisfaction of a performance obligation by transferring a good or service to a customer.

Generally, a good is considered to be delivered or a service is considered performed when the customer obtains control.

“Point in time” vs. “Over time”

Slide 14

11 May 2016SHDA Real Estate Accounting

Isla Lipana & Co., PwC member firm

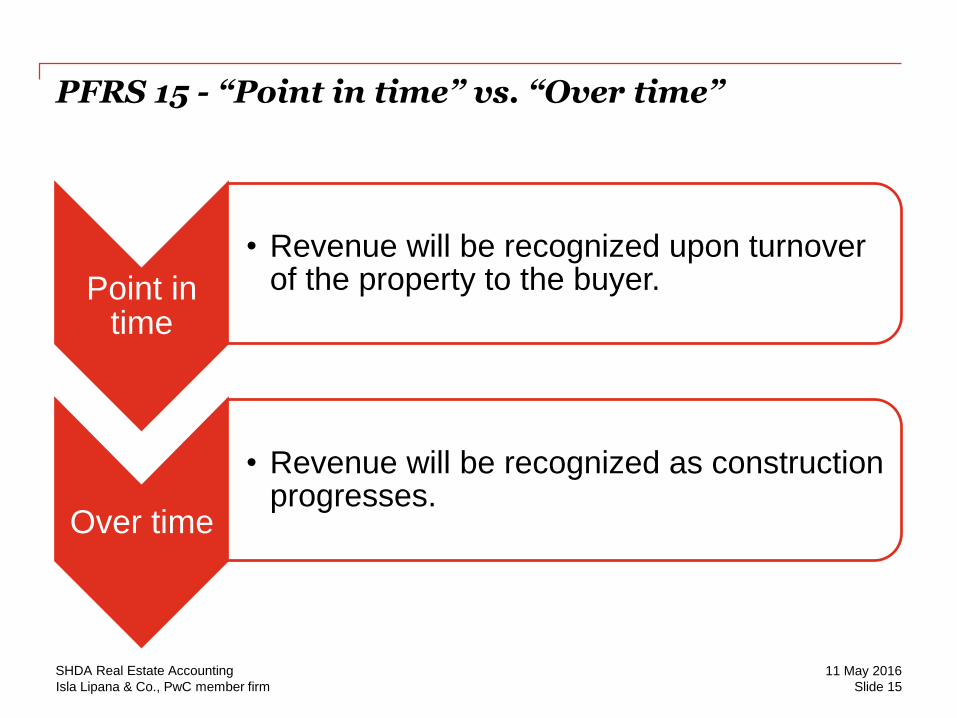

PFRS 15 - “Point in time” vs. “Over time”

Point in time

• Revenue will be recognized upon turnover of the property to the buyer.

Over time

• Revenue will be recognized as construction progresses.

Slide 15

11 May 2016SHDA Real Estate Accounting

Isla Lipana & Co., PwC member firm

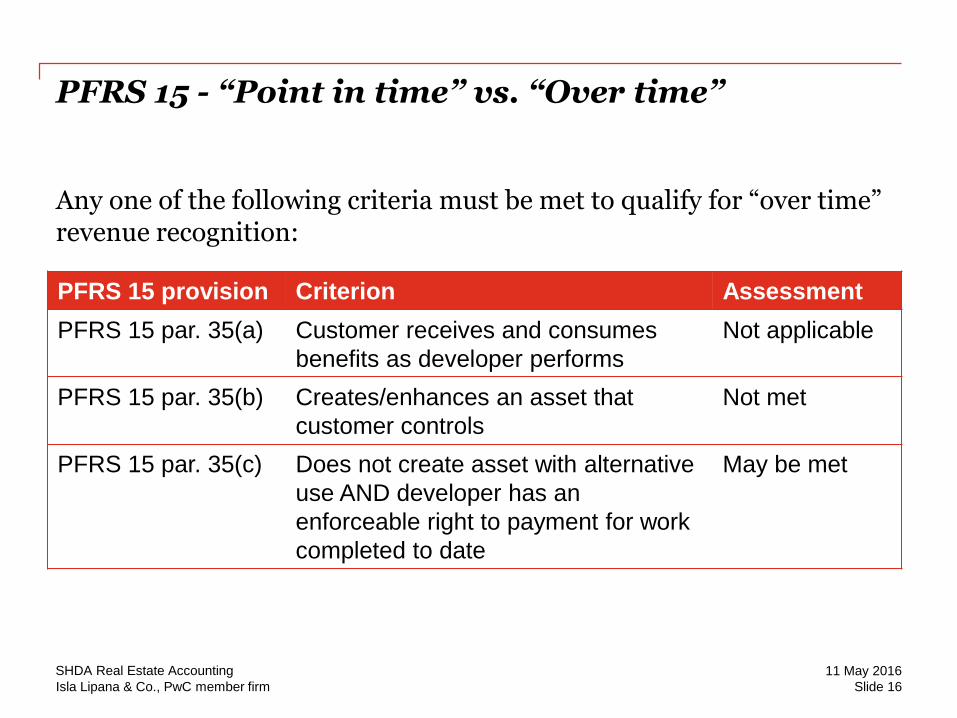

PFRS 15 - “Point in time” vs. “Over time”

PFRS 15 provision Criterion Assessment

PFRS 15 par. 35(a) Customer receives and consumes

benefits as developer performs

Not applicable

PFRS 15 par. 35(b) Creates/enhances an asset that

customer controls

Not met

PFRS 15 par. 35(c) Does not create asset with alternative

use AND developer has an

enforceable right to payment for work

completed to date

May be met

Any one of the following criteria must be met to qualify for “over time” revenue recognition:

Slide 16

11 May 2016SHDA Real Estate Accounting

Isla Lipana & Co., PwC member firm

Is “over time” revenue recognition supportable?Considerations for the Philippine scenario

• Due to the contractual terms of the CTS and the unique nature of the industry, it is unclear whether the buyer is able to control the work-in-progress in accordance with paragraph 35(b) of PFRS 15. Hence, the more relevant criterion is PFRS 15 par. 35(c). (PFRS 15.BC149-152)

Slide 17

11 May 2016SHDA Real Estate Accounting

Isla Lipana & Co., PwC member firm

Is “over time” revenue recognition supportable?Considerations for the Philippine scenario

The developer’s performance does not create an asset with an alternative use to the developer.

• The Contract to Sell (CTS) provides the specifications of the property unit bought by the customer.

• The contractual provisions restricts the developer’s ability to direct the property for another use, e.g., selling it to a different customer. Hence, a property covered by a CTS does not have an alternative use to the developer.

• This criterion is met.

Slide 18

11 May 2016SHDA Real Estate Accounting

Isla Lipana & Co., PwC member firm

Is “over time” revenue recognition supportable?Considerations for the Philippine scenario

The developer has an enforceable right to payment for performance completed to date.

Paragraph 37 of PFRS 15:

• Consider the terms of the contract

• Payments do not need to be fixed amounts

• Developer should be able to enforce payment based on performance completed to date

• Right to payment must be enforceable even if contract is terminated for reasons other than the entity's failure to perform

Slide 19

11 May 2016SHDA Real Estate Accounting

Isla Lipana & Co., PwC member firm

Is “over time” revenue recognition supportable?Considerations for the Philippine scenario

The developer has an enforceable right to payment for performance completed to date. (cont’d)

Paragraph B11 of PFRS 15:

• Scenario:

o Customer fails to perform its obligations as promised (including paying the contract price)

o CTS (or other laws) entitles the developer to continue to transfer to the customer the goods or services promised in the contract AND require the customer to pay the consideration.

• Conclusion: Developer has a right to payment for performance completed to date.

Slide 20

11 May 2016SHDA Real Estate Accounting

Isla Lipana & Co., PwC member firm

Is “over time” revenue recognition supportable?Considerations for the Philippine scenario

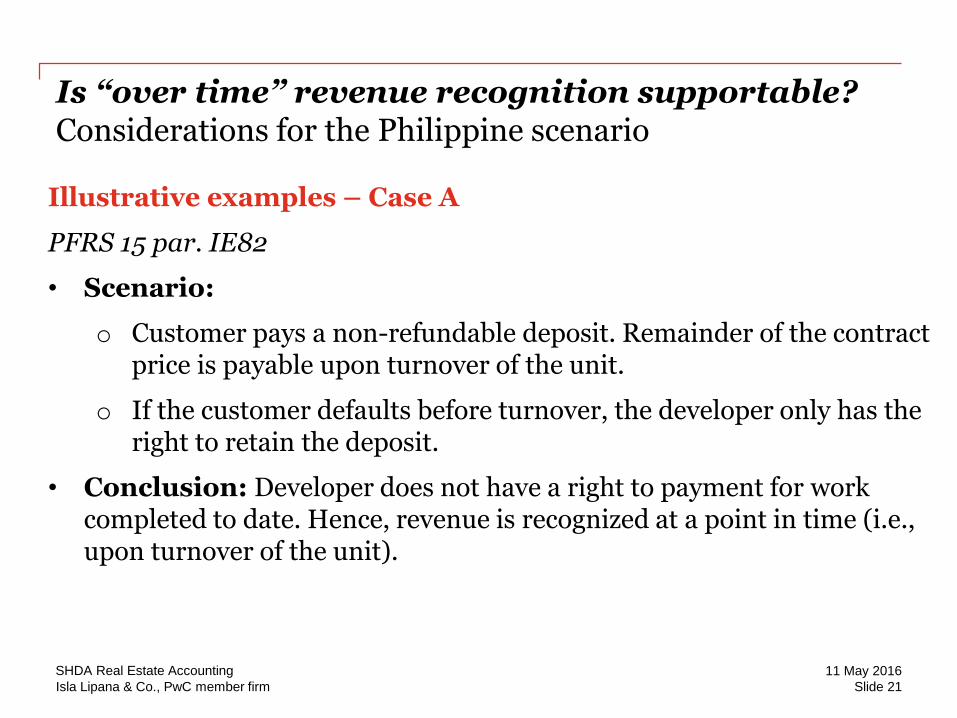

Illustrative examples – Case A

PFRS 15 par. IE82

• Scenario:

o Customer pays a non-refundable deposit. Remainder of the contract price is payable upon turnover of the unit.

o If the customer defaults before turnover, the developer only has the right to retain the deposit.

• Conclusion: Developer does not have a right to payment for work completed to date. Hence, revenue is recognized at a point in time (i.e., upon turnover of the unit).

Slide 21

11 May 2016SHDA Real Estate Accounting

Isla Lipana & Co., PwC member firm

Is “over time” revenue recognition supportable?Considerations for the Philippine scenario

Illustrative examples – Case B

PFRS 15 par. IE84

• Scenario:

o Customer pays a non-refundable deposit and will make progress payments during construction.

o If the customer defaults, the developer would have a right to all of the consideration promised in the contract if it completes the construction of the unit.

o The courts have previously upheld similar rights of the developer.

• Conclusion: Developer has a right to payment for work completed to date. Hence, revenue is recognized over time (i.e., based on stage of completion of project).

Slide 22

11 May 2016SHDA Real Estate Accounting

Isla Lipana & Co., PwC member firm

Is “over time” revenue recognition supportable?Considerations for the Philippine scenario

Illustrative examples – Case C

PFRS 15 par. IE89

• Scenario:

o Customer pays a non-refundable deposit and will make progress payments during construction.

o If the customer defaults, the developer has an option: (a) enforce the contract; or (b) cancel the contract.

o The courts have previously upheld similar rights of the developer.

• Conclusion: Developer has a right to payment for work completed to date. The fact that the developer may choose to cancel the contract does not affect such assessment, provided that the right to payment is enforceable.

Slide 23

11 May 2016SHDA Real Estate Accounting

Isla Lipana & Co., PwC member firm

PFRS 15 - Output method vs. Input method

Measures of progress over time

Management should select the method that best depicts the transfer of goods or services to the customer (not an accounting policy choice)

Methods for measuring progress:

o Output methods – based on direct measurements of the value transferred to the customer. Examples: surveys of work performed, units produced, units delivered, contract milestones

o Input methods – based on resources consumed or efforts expended relative to total resources or total efforts. Examples: costs incurred, labor hours expended, machine hours used, time elapsed, quantities of materials

Slide 24

11 May 2016SHDA Real Estate Accounting

Isla Lipana & Co., PwC member firm

PFRS 15 - Other considerations

Timing of sale of completed property may change under the new revenue recognition model

Generally, revenue will be recognized at a particular point in time.

Shift in focus: FROM significant risks and rewards of ownership TO transfer of control.

Slide 25

11 May 2016SHDA Real Estate Accounting

Isla Lipana & Co., PwC member firm

PFRS 15 - Other considerations

Accounting for work to be completed after delivery of the property unit to the customer; identification of different goods and services within a contract

Slide 26

11 May 2016SHDA Real Estate Accounting

Accounting for contract modifications

Significant financing component under different payment methods may require different accounting; revenue adjusted for the effects of time value of money

Isla Lipana & Co., PwC member firm

PFRS 15 - Other considerations

Variable consideration

Slide 27

11 May 2016SHDA Real Estate Accounting

Accounting for uninstalled materials

Isla Lipana & Co., PwC member firm

PFRS 15 - Other considerations

Accounting for contract costs

Slide 28

11 May 2016SHDA Real Estate Accounting

Collaboration arrangement (e.g., “joint venture”)

Isla Lipana & Co., PwC member firm

PFRS 15 - Other considerations

More disclosures

The disclosure requirements are significantly greater than existing disclosure requirements.

Slide 29

11 May 2016SHDA Real Estate Accounting

Isla Lipana & Co., PwC member firm

Other matters with impact on real estate industry

• Contracts – existing contracts may have to be revisited to maintain the original intent

• Tax implications• Investors relations – stakeholders would want to know how your

revenue recognition will change and how the new standard will affect the Company’s financial picture

• Controls and processes – more estimates and disclosures that will call for new processes and controls

• Technology – may need to update the current system to capture new information that might not have been necessary before

• Compensation and bonus plans – revenue recognition can trigger payments like bonuses. Consider how timing changes for revenue recognition affect these and other internal arrangements

Slide 30

11 May 2016SHDA Real Estate Accounting

Isla Lipana & Co., PwC member firm

Recap

Current accounting for real estate sales: PIC Q&A 2006-01

o Percentage-of-completion method

Future accounting for real estate sales: PFRS 15

o Point in time vs. over time

o Is “over time” revenue recognition supportable?

o Output method vs. Input method

o Other considerations

Slide 31

11 May 2016SHDA Real Estate Accounting

Isla Lipana & Co., PwC member firm

Lorem ipsum dolor sit amet, consectetuer adipiscingelit. Proin mi. Sed Questions? risus, nonummy iaculis, volutpat eu, tincidunt non, purus. Pellentesque at ante a ipsum imperdiet ornare. Curabitur nonummy velit a sapien. Praesent a orci. Nunc eget mi non semconsequat auctor. Proin felis. Integer rutrum. Nullaaliquet. Questions? in arcu. Aenean lectus. Duisornare. Donec dui. Aenean eu eros. Aliquam eratvolutpat. Ut euismod, diam vel tincidunt fringilla, estodio accumsan orci, sed rutrum lacus sem sit amet mi. Pellentesque habitant Questions? tristique senectus et netus et malesuada fames ac turpis egestas.

Questions?

Questions?

Questions?

Slide 32

11 May 2016SHDA Real Estate Accounting

Thank you!

This publication has been prepared for general guidance on matters of interest only, and does

not constitute professional advice. You should not act upon the information contained in this

publication without obtaining specific professional advice. No representation or warranty

(express or implied) is given as to the accuracy or completeness of the information contained

in this publication, and, to the extent permitted by law, Isla Lipana & Co., its members,

employees and agents do not accept or assume any liability, responsibility or duty of care for

any consequences of you or anyone else acting, or refraining to act, in reliance on the

information contained in this publication or for any decision based on it.

© 2016 Isla Lipana & Co. All rights reserved. In this document, “PwC” refers to Isla Lipana &

Co. which is a member firm of PricewaterhouseCoopers International Limited, each member

firm of which is a separate legal entity.