creating & delivering sustainable value : sam 2015 plenary session day3

TRANSCRIPT

CREATING & DELIVERING SUSTAINABLE VALUE

Ms. ROSE MWANIKI

CONSULTANT: MF/SPM NAIROBI – KENYA

9th September 2015

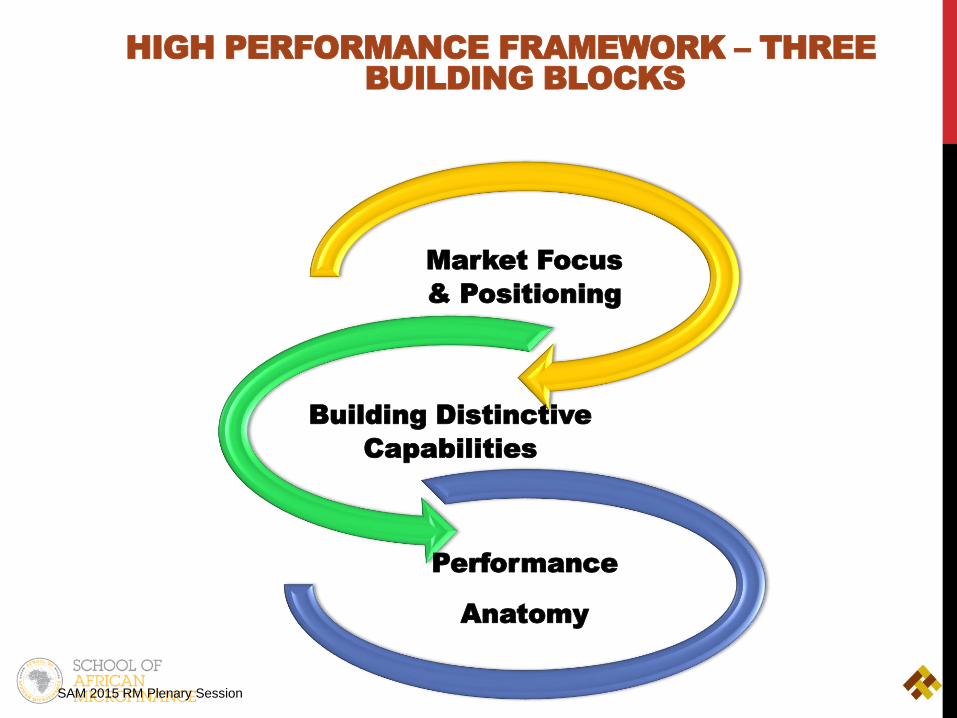

HIGH PERFORMANCE FRAMEWORK – THREE

BUILDING BLOCKS

SAM 2015 RM Plenary Session

Market Focus

& Positioning

Building Distinctive

Capabilities

Performance

Anatomy

HIGH PERFORMANCE FRAMEWORK – THREE BUILDING

BLOCKS

USING SKS CASE STUDY WE SAW THAT:

A CLEAR STRATEGY – WILL RESULT IN BETTER DECISIONS

BUILDING OF DISTINCTIVE CAPABILITIES – WILL RESULT IN BETTER PRACTICES THAT ENABLE US SERVE OUR CLIENTS BETTER

BUILDING PERFORMANCE ANATOMY – WITH STRONG CULTURE/LEADERSHIP AND TALENT – WILL RESULT IN BETTER MINDSETS.

SAM 2015 RM Plenary Session

GOOD ENOUGH BUT THE BIG QUESTION

REMAINS?

HIGH PERFORMANCE TO BENEFIT WHO?

THE MICROFINANCE INSTITUTION ITSELF –DIRECTORS, SHAREHOLDERS?

OR

THE CLIENT – POOR WOMEN, YOUTH, DISABLED, VULNERABLE?

OR BOTH?

SAM 2015 RM Plenary Session

GOOD ENOUGH BUT THE BIG QUESTION

REMAINS? SUSTAINABILITY FOR WHO??/

??

SAM 2015 RM Plenary Session

GOOD ENOUGH BUT THE BIG QUESTION

REMAINS?

One of the biggest bank that is targeting low incomegroups in my country reports huge financial results - inthe billions

But the question ringers – who is becomingsustainable? The bank owners? Directors or thecustomer?

Something to think about?

SAM 2015 RM Plenary Session

GOOD ENOUGH BUT THE BIG QUESTION

REMAINS?

A year ago, one of the pioneer microfinance banks in Kenya was bought by a billionaire and one cannot help but wonder:

Is the billionaire getting into the MF business space to help the poor or make more money for himself?

Do you think this billionaire will somewhere along the way work to reduce poverty among his clients?

SAM 2015 RM Plenary Session

STATUS OF MICROFINANCE – GLOBAL LEVEL

AN INDUSTRY STRUGGLING TO GROW

SAM 2015 RM Plenary Session

STATUS OF MICROFINANCE

HIGH PERFORMANCE STILL A DREAM…….

CASE STUDY – KENYA

SAM 2015 RM Plenary Session

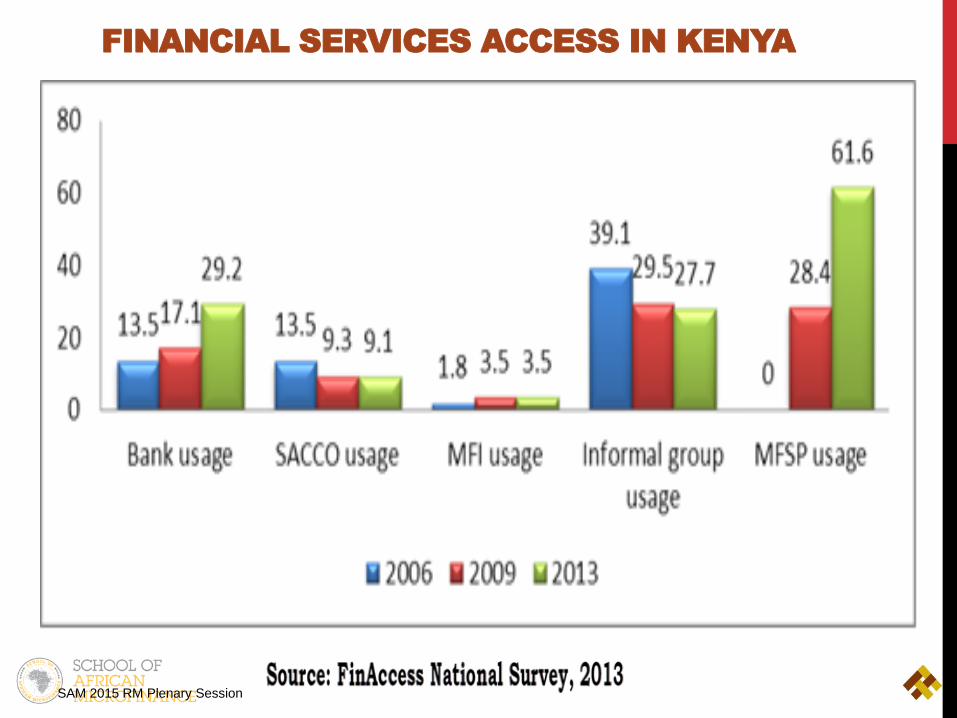

FINANCIAL SERVICES ACCESS IN KENYA

SAM 2015 RM Plenary Session

FINANCIAL SERVICES USERS IN KENYA

SAM 2015 RM Plenary Session

OVERALL ACCESS TO FINANCIAL SERVICES IN

KENYA – IMPROVED EXCEPT IN THE MF

INDUSTRY

SAM 2015 RM Plenary Session

MICROFINANCE FINANCIAL SERVICES

ACCESS IN KENYA

SAM 2015 RM Plenary Session

Overall the microfinance institutions use

remains at less than 4% aggregate.

The penetration of microfinance services

in the rural areas ranges between 2.5% to

5.3%.

The implications of these findings are that

the products and services of these

institutions seem to appeal to only a small

segment of the population.

MICROFINANCE FINANCIAL SERVICES ACCESS IN

KENYA

SAM 2015 RM Plenary Session

Overall, a large proposition of the Kenyan adult

population use informal financial services.

Over 25% of the population is completely excluded

from financial service access - indicating that the

market though ‘competitive’ has

potential/opportunities for growth.

WHAT IS AILING THE KENYAN MFIS?....

SAM 2015 RM Plenary Session

MFIs

Stagnated Growth

Limited & Expensive

Capital

Capacity Talent &

Processes

Mistrust

Very High Client Exit

Costly product

Offerings/slow service delivery

New Legislation &

Laws

New Entrants Leadership

Culture

STAGNATED GROWTH – CHALLENGES FOR

KENYA MF INDUSTRY

SAM 2015 RM Plenary Session

The funding base for most of the credit only microfinance

institutions is made up of mix of commercial/social

investors’ debt.

The average interest rate on borrowed funds has resulted in

lower margins, profitability and growth of the loan asset.

The scaling up of microfinance operations has also been

negated by very high client exit for some MFIs as much as

50% of its clientele annually.

STAGNATED GROWTH – CHALLENGES FOR

KENYA MF INDUSTRY

SAM 2015 RM Plenary Session

The high clients exit is largely a factor of high staff turnover

especially at the operational level leading to rising PAR.

Costly products offerings and relatively slower service

delivery compared to those of the other market players.

MFIs are therefore unable to grow the size of their loan asset

to generate incomes to allow for expansion of the outreach

leading to stagnation and lower demand for their products/

services.

WHAT IS GOING ON HERE??

SAM 2015 RM Plenary Session

PLUGGING THE HOLES: TO REDUCE RUN-OFF

SAM 2015 RM Plenary Session

THERE COULD BE A NUMBER OF ROUTES BUT FIRST….

GOING BACK TO THE FUNDAMENTALS OF

MICROFINANCE – THE DOUBLE BOTTOM LINE

REFOCUSING ON SOCIAL AND FINANCIAL

GOALS COULD HELP.

PUTTING THE CLIENT FIRST – AS THE MFI GROWS ITS BUSINESS

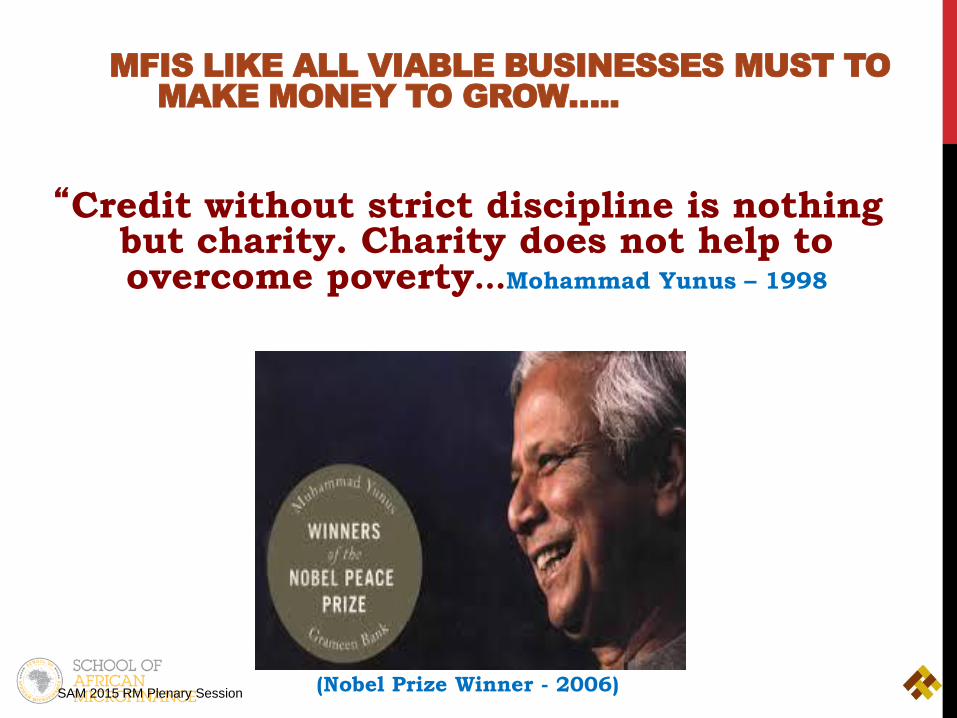

MFIS LIKE ALL VIABLE BUSINESSES MUST TO

MAKE MONEY TO GROW…..

SAM 2015 RM Plenary Session

“Credit without strict discipline is nothing but charity. Charity does not help to overcome poverty…Mohammad Yunus – 1998

(Nobel Prize Winner - 2006)

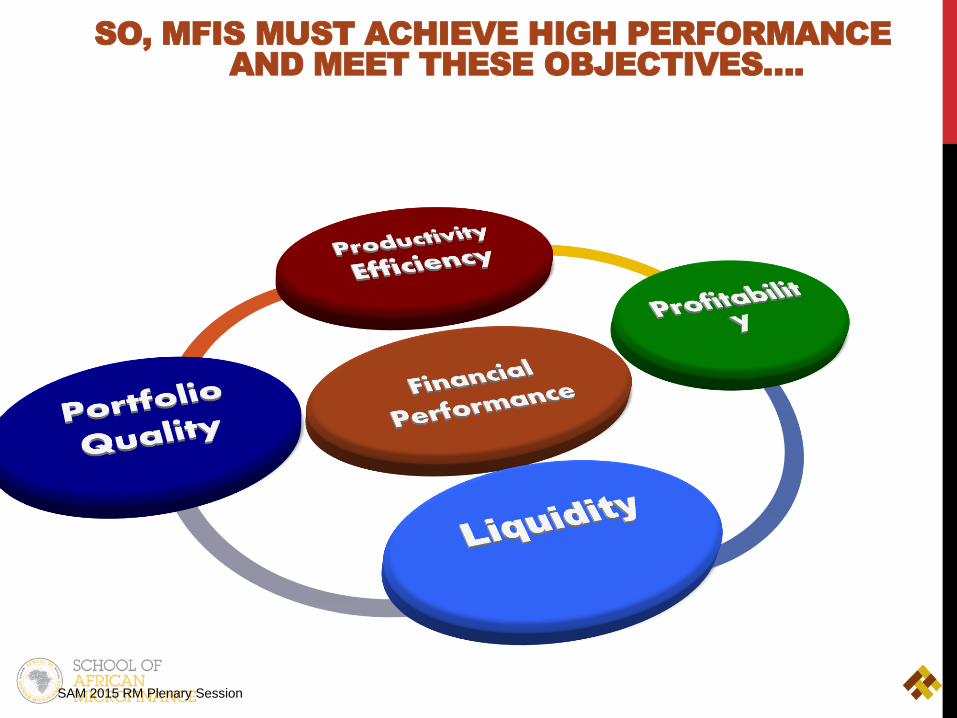

SO, MFIS MUST ACHIEVE HIGH PERFORMANCE

AND MEET THESE OBJECTIVES….

SAM 2015 RM Plenary Session

BUT MF BUSINESS IS UNIQUE – IT HAS A

SOCIAL ANGLE !

SAM 2015 RM Plenary Session

TRUE MICROFINANCE IS MORE THAN A BUSINESS

IT HAS A PHILOSOPHY BEHIND IT

MFIS ARE NOT ONLY CONCERNED WITH THEIR OWN

INSTITUTIONAL PROFITABILITY – THEY ALSO WANT

TO CREATE VALUE/AND IMPACT THEIR CLIENTS.

CHANGING THE LIVES OF ITS CLIENTS AND THEIR

FAMILIES IS A CRITICAL CONSIDERATION.

THE SOCIAL ANGLE OF MICROFINANCE BUSINESS

SAM 2015 RM Plenary Session

THE SOCIAL ANGLE OF MICROFINANCE

BUSINESS – WHAT DOES THIS MEAN?

SAM 2015 RM Plenary Session

TREAT YOUR CLIENTS RESPONSIBLY

PUTTING YOUR CLIENT INTERESTS FIRST

TAKING CARE OF YOUR CLIENTS’ SO THAT THEY

TAKE CARE OF YOUR BUSINESS

treat clients responsibly – IN A NUTSHELL

Client Protection

Product Design & Delivery

Prevent over-indebtedness

Transparency

Responsible Pricing

Fair Treatment of clients

Privacy of client data

Mechanism of client complaint

Resolution

SAM 2015 RM Plenary Session

CLIENT PROTECTION – WHAT IS ITS FOCUS?

Client protection is focused on several dimensions of product

and delivery quality;

Transparent;

Respectful and;

Prudent treatment of clients

Client Protection Principle is a simple matter of fair treatment

and harm avoidance - of clients by financial providers.

Client protection practices should especially be beneficial for

the more vulnerable populations that MF serves – women, youth,

rural dwellers, disabled, etc.

SAM 2015 RM Plenary Session

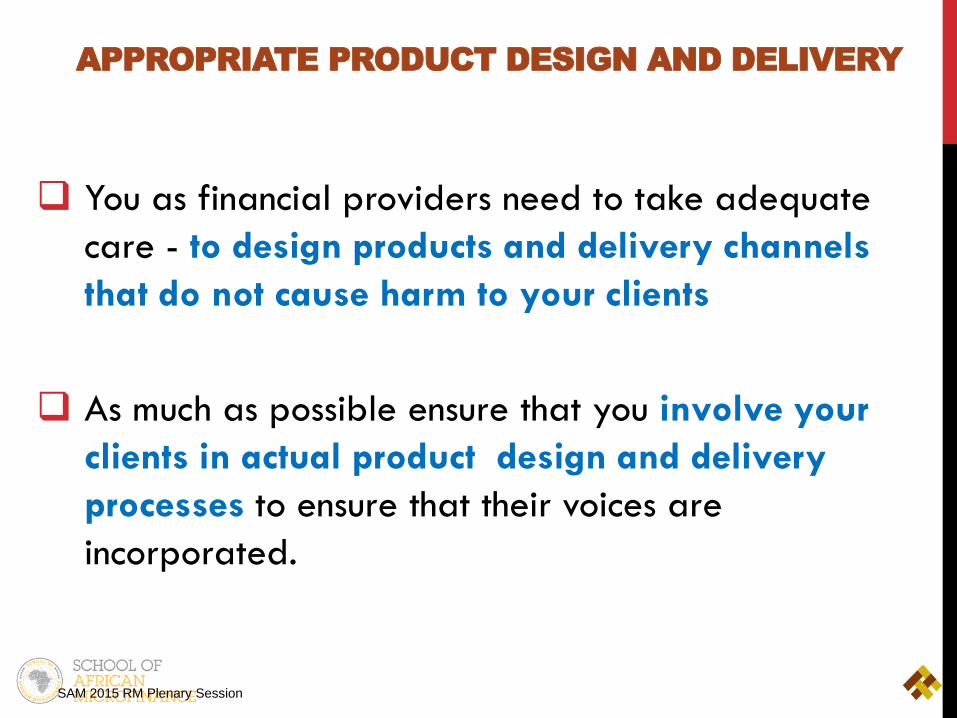

APPROPRIATE PRODUCT DESIGN AND DELIVERY

You as financial providers need to take adequate

care - to design products and delivery channels

that do not cause harm to your clients

As much as possible ensure that you involve your

clients in actual product design and delivery

processes to ensure that their voices are

incorporated.

SAM 2015 RM Plenary Session

APPROPRIATE PRODUCT DESIGN AND

DELIVERY – HOW?

Conduct regular market studies and client surveys to collect information on client needs

Design products & services: loans/savings/insurance/payments based on clients' needs.

For all products, ensure that delivery is reliable and convenient for the client - keep transaction costs at a minimal for clients.

In short products and services should not cause harm to the clients SAM 2015 RM Plenary Session

PREVENTION OF OVER-INDEBTEDNESS

Over indebtedness is the inability for your client to

handle loan repayments without sacrificing basic

quality of life.

It is different from credit risk

A client may still be able to make loan repayments

by selling assets or making other sacrifices that

reduces their quality of life or even make them

more poorer.

SAM 2015 RM Plenary Session

PREVENTION OF OVER-INDEBTEDNESS - HOW?

Identify causes of indebtedness – multiple loans;

inadequate capacity analysis or unpredictable events.

Establish the borrower’s ability to afford the loan and

repay it. Train loan officers and provide incentives for

thorough client screening.

Monitor over-indebtedness – use of client & finance

education to create awareness.

Verify credit history – where credit bureau is available

especially in competitive markets.

SAM 2015 RM Plenary Session

TRANSPARENCY

Meeting your commitment to transparency

requires that you communicate clear, sufficient,

and timely information in a manner and language

clients can understand so that they make informed

decisions?

SAM 2015 RM Plenary Session

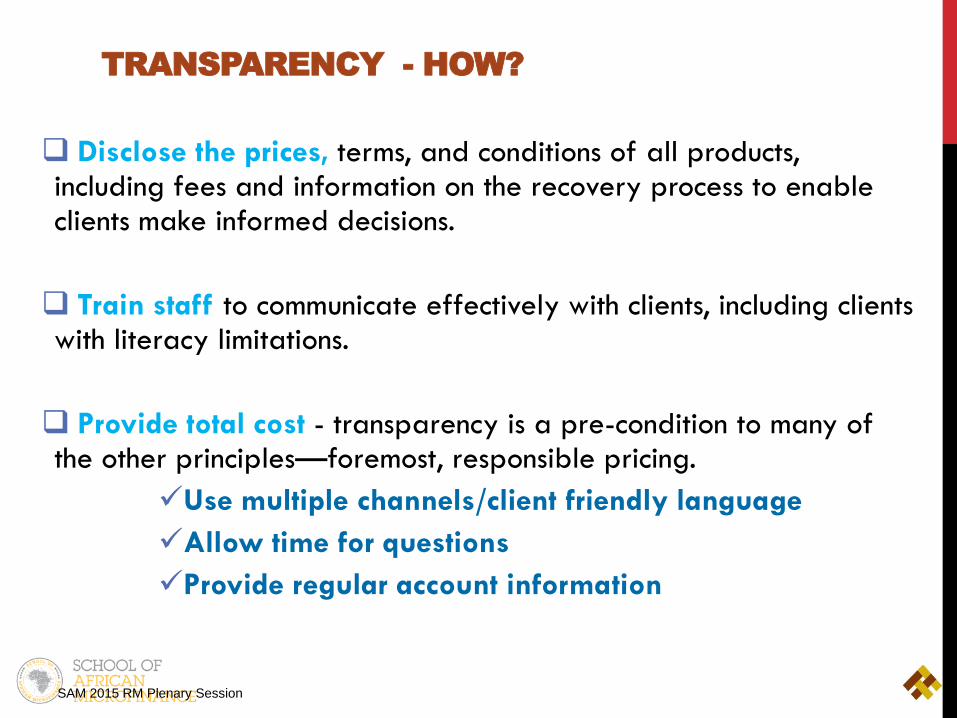

TRANSPARENCY - HOW?

Disclose the prices, terms, and conditions of all products, including fees and information on the recovery process to enable clients make informed decisions.

Train staff to communicate effectively with clients, including clients with literacy limitations.

Provide total cost - transparency is a pre-condition to many of the other principles—foremost, responsible pricing.

Use multiple channels/client friendly language

Allow time for questions

Provide regular account information

SAM 2015 RM Plenary Session

RESPONSIBLE PRICING

This principle requires that your institution set prices,

terms, and conditions that are affordable to clients while

ensuring that you also attain your institutional

sustainability?

How do you achieve these two seemingly conflicting

goals?

SAM 2015 RM Plenary Session

RESPONSIBLE PRICING

Pricing, terms, and conditions are set in a way that is both

affordable to clients and sustainable for the financial

institution.

Financial sustainability is required to continue serving

clients:

Price competitively – fees & interest

Earn reasonable return

Use profits to benefit clients

Do not pass inefficiencies to the client

SAM 2015 RM Plenary Session

FAIR AND RESPECTFUL TREATMENT OF CLIENTS

How well or fairly or respectfully do you treat your

clients?

SAM 2015 RM Plenary Session

FAIR AND RESPECTFUL TREATMENT OF CLIENTS

Set ethical standards – behaviors that are acceptable or not – offensive language and threats; unethical seizure of collaterals; careless debt extension.

Set appropriate debt collection practices – clear steps should be well detailed

Train staff on ethics – for example on appropriate and inappropriate practices on loan recovery.

Offensive language and threats

SAM 2015 RM Plenary Session

PRIVACY OF CLIENT DATA

Do you know that client data belongs to the client not

you as the institution?

Are you also aware that misuse of the data has the

potential to harm your own clients?

So What is required of your as a financial provider?

SAM 2015 RM Plenary Session

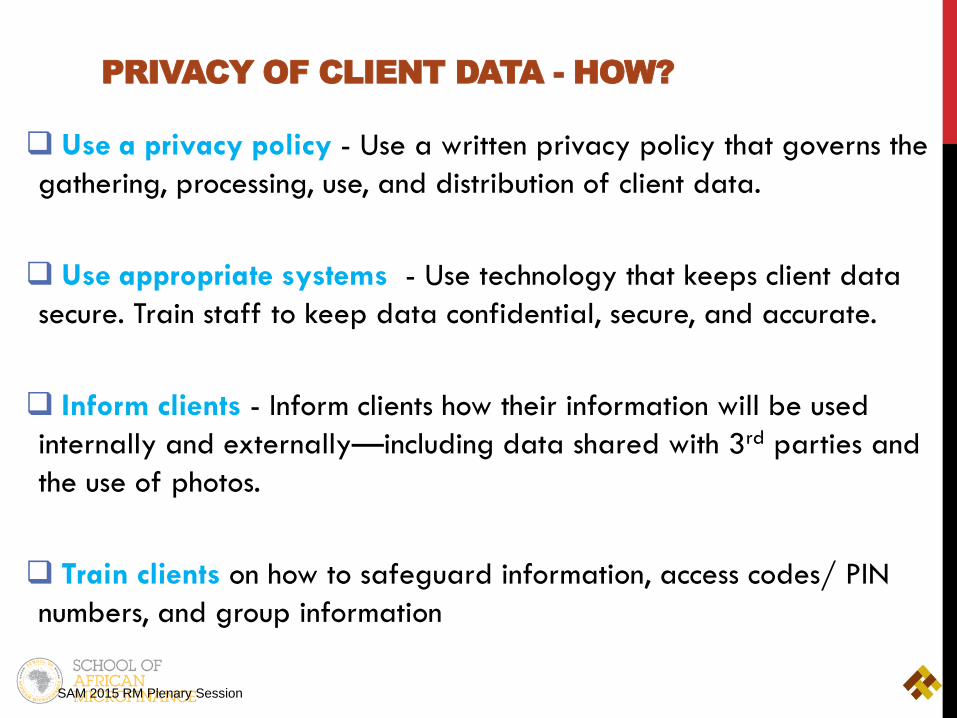

PRIVACY OF CLIENT DATA - HOW?

Use a privacy policy - Use a written privacy policy that governs the

gathering, processing, use, and distribution of client data.

Use appropriate systems - Use technology that keeps client data

secure. Train staff to keep data confidential, secure, and accurate.

Inform clients - Inform clients how their information will be used

internally and externally—including data shared with 3rd parties and

the use of photos.

Train clients on how to safeguard information, access codes/ PIN

numbers, and group information

SAM 2015 RM Plenary Session

MECHANISMS FOR COMPLAINT RESOLUTION

Clients Protection also means that your institution has put

in place a mechanism for handling client complaints.

Clients should be free to air their concerns; express

specific problems; and provide any complement.

A complaints resolution mechanism is much more than a

suggestion box!

SAM 2015 RM Plenary Session

MECHANISMS FOR COMPLAINT RESOLUTION – HOW?

Set a complaints policy – for customer complaints to be fully investigated and resolved in a timely manner without bias.

Actively use a mechanism - to handle customer complaints, dedicate staff resources to it, and ensure that it is actively used.

Train staff - Train staff to handle complaints and refer them to the appropriate person for investigation and resolution.

Monitor the system – to check how complaints are handled.

Use the information – to improve products, processes, etc.

SAM 2015 RM Plenary Session

IMPLICATIONS FOR NOT PROTECTING CLIENTS?

Mission Drift

High client Exit

High staff turnover (operational team)

High loan delinquency rates

Poor client loyalty – inhibiting business growth

Financial Sustainability can never be achieved!

The list only gets longer

SAM 2015 RM Plenary Session

WHAT DOES ALL THIS MEAN FOR LEGITIMATE MF

PROVIDERS

In the past, MFIs may have taken client protection for

granted but with the growing highly competitive

markets, there is need for more explicit attention.

Over indebtedness in several countries due to multiple

providers competing for the same clients today requires

respectful face-to-face treatments of clients.

SAM 2015 RM Plenary Session

HIGH PERFORMANCE MFIS

WILL HAVE CLIENTS AS THEIR KEY FOCUS

Client

protection

Profitability

Growth

Positioning

for the futureLongevity

Consistency

SAM 2015 RM Plenary Session

RESPONSIBILITY TO CLIENTS - A PREREQUISITE

FOR SUSTAINABLE MF BUSINESS

o Response from a similar presentation - SAM

2013

o An encounter with a CEO of an international

microfinance Institution

o Is there a business case for client protection

or do we join my CEO in breaking clients legs

and arms?

SAM 2015 RM Plenary Session

responsibility to clients - a prerequisite for

sustainable mf business

MICROFINANCE HAS A HUMAN FACE

HIGH PERFORMANCE MFIS WILL NEED TO

ADOPT DOUBLE OR EVEN TRIPPLE

BOTTOM LINE TO CREATE VALUE THAT

LASTS

MICROFINANCE IS AN INDUSTRY THAT

PROMOTES FINANCE +++++

SAM 2015 RM Plenary Session

KEY REFERENCE FOR CPPS

www.smartcampaign.org

“Select Tools and Resources” at the top of the home page.

Rose Mwaniki

Consultant – MF/RURAL FINANCE/SPM

Nairobi Kenya

SAM 2015 RM Plenary Session