creating a footprint in underserved...

TRANSCRIPT

Creating a footprint in underserved niches

Swedbank Healthcare Seminar, December 1, 2016 Peter Wolpert, CEO & Founder

1 D-2495919-v1

The purpose of this presentation (the "Presentation") is to provide an overview of Moberg Pharma AB (publ) (the "Company"). For the purposes of this notice, "Presentation" means this document, its contents or any part of it, any oral presentation, any question or answer session and any written or oral material discussed or distributed during the Presentation meeting.

This Presentation is not a prospectus or similar offer document. This Presentation does not purport to contain comprehensive or complete information about the Company and is qualified in its entirety by the business, financial and other information the Company is required to publish in accordance with the rules, regulations and practices applicable to companies listed on Nasdaq Stockholm (the "Exchange Information"). Any decision to invest in any securities of the Company should only be made on the basis of a thorough examination of the Exchange Information and an independent investigation of the Company itself and not on the basis of this Presentation. This Presentation has not been independently verified by any other person unless expressly stated therein. No representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy or completeness of the information or opinions contained in this Presentation.

Except where otherwise indicated in this Presentation, the information provided herein is based on matters as they exist at the date of preparation of this Presentation and not as of any future date. All information presented or contained and any opinions expressed in this Presentation are subject to change without notice. The Company does not undertake to update, complete, revise or keep current the information contained in this Presentation. This Presentation does not constitute an audit or due diligence review and should not be construed as such. This Presentation has not been approved by any regulatory or supervisory authority.

This Presentation does not constitute or form part of, and should not be construed as (i) an offer, solicitation or invitation to subscribe for, sell or issue, underwrite or otherwise acquire any securities or financial instruments, nor shall it, or the fact of its communication, form the basis of, or be relied upon in connection with, or act as any inducement to enter into any contract or commitment whatsoever with respect to such securities or financial instruments or (ii) any form of financial opinion, recommendation or investment advice with respect to any securities or financial instruments. The recipient must make its own independent assessment and such investigations as it deems necessary.

This Presentation contains "forward-looking" statements. These forward-looking statements can be identified by the fact that they do not relate only to historical or current facts. In particular, forward-looking statements include all statements that express forecasts, expectations, plans, outlook and projections with respect to future matters, including trends in results of operations, margins, growth rates, overall market trends, the impact of interest or exchange rates, the availability or cost of financing, anticipated cost savings or synergies, the completion of strategic transactions and restructuring programmes, anticipated tax rates, expected cash payments, and general economic conditions. By their nature, forward-looking statements involve risk and uncertainty because they relate to events and depend on circumstances that will occur in the future and they are subject to change at any time. There are a number of factors that could cause actual results and developments to differ materially from those expressed or implied by these forward-looking statements, including risks associated with the inherent uncertainty of pharmaceutical research and product development, manufacturing and commercialization, the impact of competitive products, patents, legal challenges, government regulation and approval, the Company’s ability to secure new products for commercialization and/or development and other risks and uncertainties detailed from time to time in the Company’s interim or annual reports, prospectuses or press releases and other factors that are outside the Company's control. Any forward-looking statements made by or on behalf of the Company speak only as of the date they are made. The Company does not undertake to update forward-looking statements to reflect any changes in the Company's expectations with regard thereto or any changes in events, conditions or circumstances on which any such statement is based.

2

Disclaimer

CONFIDENTIAL

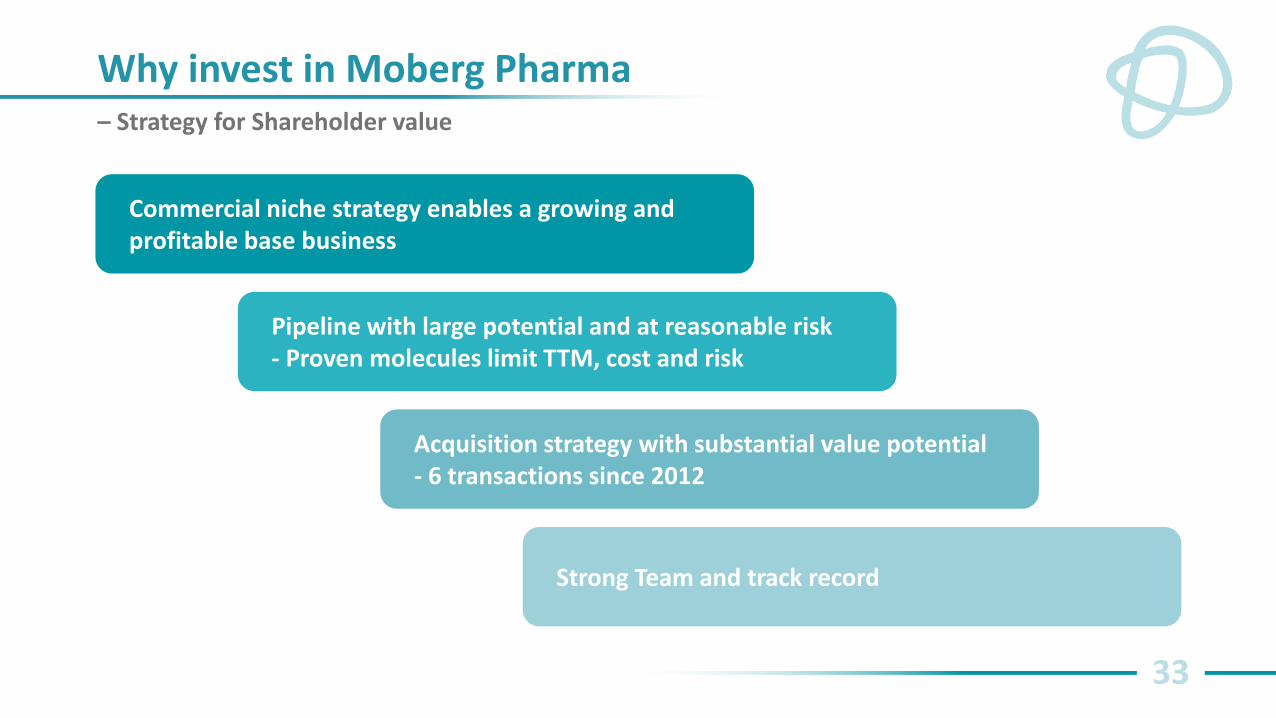

Why invest in Moberg Pharma – Strategy for Shareholder value

3

Commercial niche strategy enables a growing and profitable base business

Pipeline with large potential and at reasonable risk - Proven molecules limit TTM, cost and risk

Acquisition strategy with substantial value potential - 6 transactions since 2012

Strong Team and track record

Overview

Q3 2016 - Highlights

Commercial Operations and Innovation Engine

M&A Opportunities

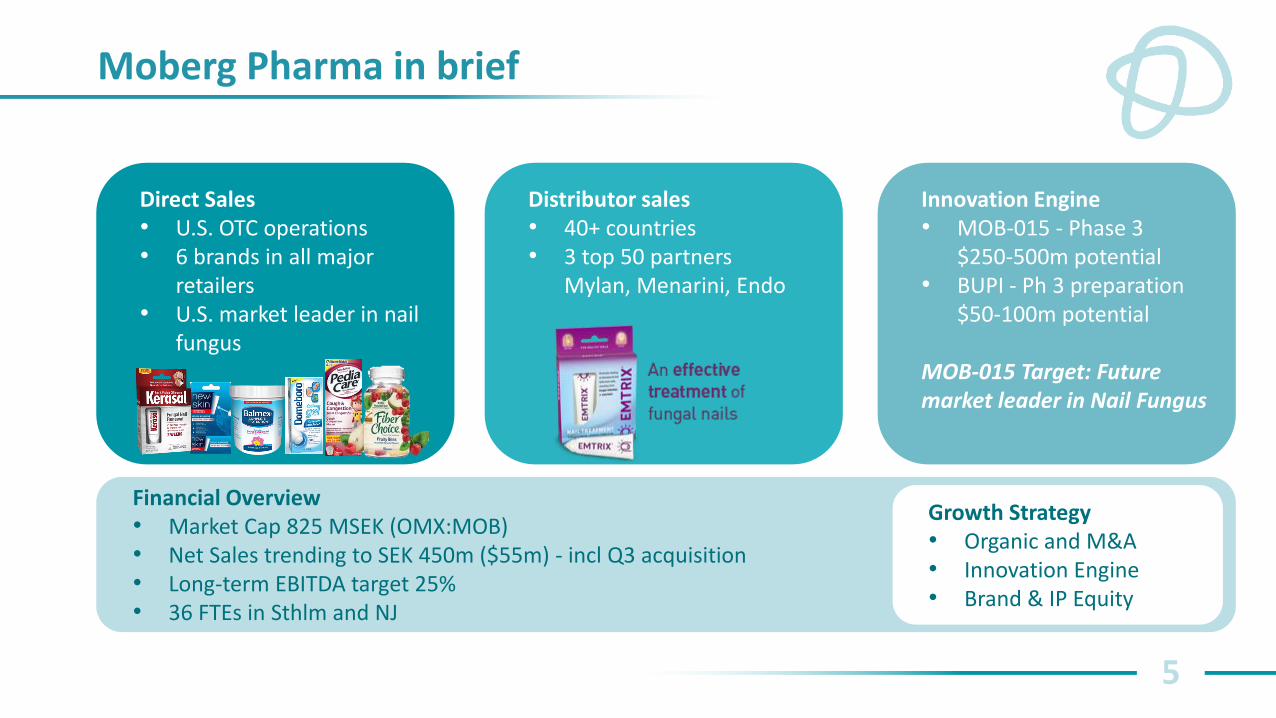

Moberg Pharma in brief

5

Innovation Engine • MOB-015 - Phase 3

$250-500m potential • BUPI - Ph 3 preparation

$50-100m potential MOB-015 Target: Future market leader in Nail Fungus

Financial Overview • Market Cap 825 MSEK (OMX:MOB) • Net Sales trending to SEK 450m ($55m) - incl Q3 acquisition • Long-term EBITDA target 25% • 36 FTEs in Sthlm and NJ

Direct Sales • U.S. OTC operations • 6 brands in all major

retailers • U.S. market leader in nail

fungus

Distributor sales • 40+ countries • 3 top 50 partners

Mylan, Menarini, Endo

Growth Strategy • Organic and M&A • Innovation Engine • Brand & IP Equity

The rapid growth continues

Product Sales, MSEK

- fueled by a major brand acquisition in July and strong Q3 results

2010 2011 2012 2013 2014 2015 2016

8

56

112

157

200

276

6

Positive momentum in 2016

Targets set for 2016 have been delivered

• Acquire additional brands

• Initiate phase 3 studies for MOB-015

• Strengthen lead brand – Kerasal Nail - in U.S.

• Broaden international distribution

7

- 2016 was an investment year

Overview

Q3 2016 - Highlights

Commercial Operations and Innovation Engine

M&A Opportunities

9

Q3 2016 – Significant growth in Sales & Profitability

42%

61% 56% GROWTH

DIRECT SALES

DISTRIBUTOR SALES

104.1MSEK NET SALES

110% GROWTH

29MSEK EBITDA

28% EBITDA MARGIN

Q3 - Q4 2016 – Excellent Progress

10

Commercial

• Growth in all distribution channels

– 29% market share for Kerasal Nail in the U.S (L26W*) - All-Time High

– Acquired brands contributed significantly to sales and profitability Integration progressing according to plan Non-core brand PediaCare under divestment

Innovation engine

• Phase 3 ongoing for MOB-015 in North America & Europe

• EU patent for BUPI (patent term 2031)

Financial

• Increased flexibility in debt financing of acquisitions

Source: Symphony IRI, U.S. retail sales of nail fungus products excluding private label in Multi Outlet Stores

*L26W/E 10/2/16 vs YAGO

All-Time High share in 2016

• New packaging, commercial and website launched in March

• Very positive reception from consumers and trade, ATH market share

• Note: there is a lag of at least one month between growth in consumer sales and effects on net sales

– U.S. market share for Kerasal Nail following successful relaunch

Source: Symphony IRI, U.S. retail sales of nail fungus products excluding private label in Multi Outlet Stores *L26W/E 10/2/16 vs YAGO

11

29% +2% 29% 24%

MARKET SHARE* CATEGORY GROWTH* VALUE GROWTH*

Three brands acquired for $40 million

• Expected EBITDA contribution ca $5 million (12m post-closing)

• Expected to double sales of our U.S. franchise

• Non-dilutive financing. Financed by available cash resources and bond loan

• Sold through our established sales channels in the U.S, primarily through chain drugstores and mass retailers, such as:

– Closed on July 7

12

Acquisition of brands from Prestige

• New Skin is the #1 OTC liquid bandage brand in the U.S. An antiseptic which kills germs and dries rapidly to form a clear protective cover

• Fiber Choice is a line of fiber supplements

PediaCare (children’s cough cold) - signed Nov 24 to be divested for $5 million

Under divestment

Additional acquisition opportunities - Several attractive acquisition opportunities are under evaluation

13

Option to acquire Dermoplast from Prestige Brands

• Moberg has secured an exclusive option, to the end of 2017, to acquire Dermoplast, an attractive dermatology brand from Prestige Brands

– Currently no 1. pharmacist recommended brand, and no 2 brand in the $33.7 million U.S. retail pain relief sprays market.

– Total net sales ca $12m, 21% market share in retail and growing L52W. Significant Hospital business in addition to retail

Moberg received approval at bondholders’ meeting (written procedure) and received additional flexibility in debt-financing of acquisitions

• Waiver to, at one occasion in conjunction with an acquisition, increase the Company’s ratio of net debt to EBITDA to 4.5. Valid up to the end of 2017.

• Upon a utilization of the Waiver, Moberg Pharma will pay a consent fee of 0.50 percent.

• >99% of votes supported the decision

Source: Symphony IRI, Brand ranking according to Pharmacy Times Prestige Brands Earnings call, Nov 3, 2016

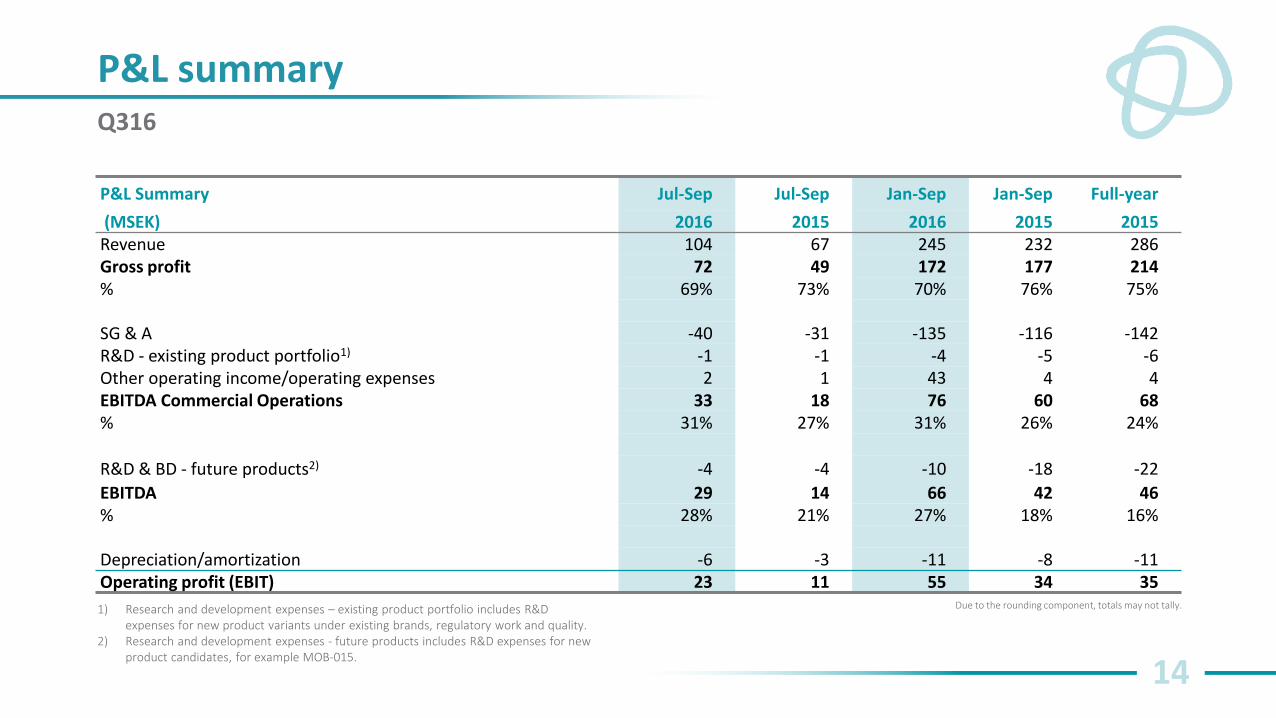

P&L summary Q316

14

1) Research and development expenses – existing product portfolio includes R&D expenses for new product variants under existing brands, regulatory work and quality.

2) Research and development expenses - future products includes R&D expenses for new product candidates, for example MOB-015.

Due to the rounding component, totals may not tally.

P&L Summary Jul-Sep Jul-Sep Jan-Sep Jan-Sep Full-year

(MSEK) 2016 2015 2016 2015 2015

Revenue 104 67 245 232 286

Gross profit 72 49 172 177 214

% 69% 73% 70% 76% 75%

SG & A -40 -31 -135 -116 -142

R&D - existing product portfolio1) -1 -1 -4 -5 -6

Other operating income/operating expenses 2 1 43 4 4

EBITDA Commercial Operations 33 18 76 60 68

% 31% 27% 31% 26% 24%

R&D & BD - future products2) -4 -4 -10 -18 -22

EBITDA 29 14 66 42 46

% 28% 21% 27% 18% 16%

Depreciation/amortization -6 -3 -11 -8 -11

Operating profit (EBIT) 23 11 55 34 35

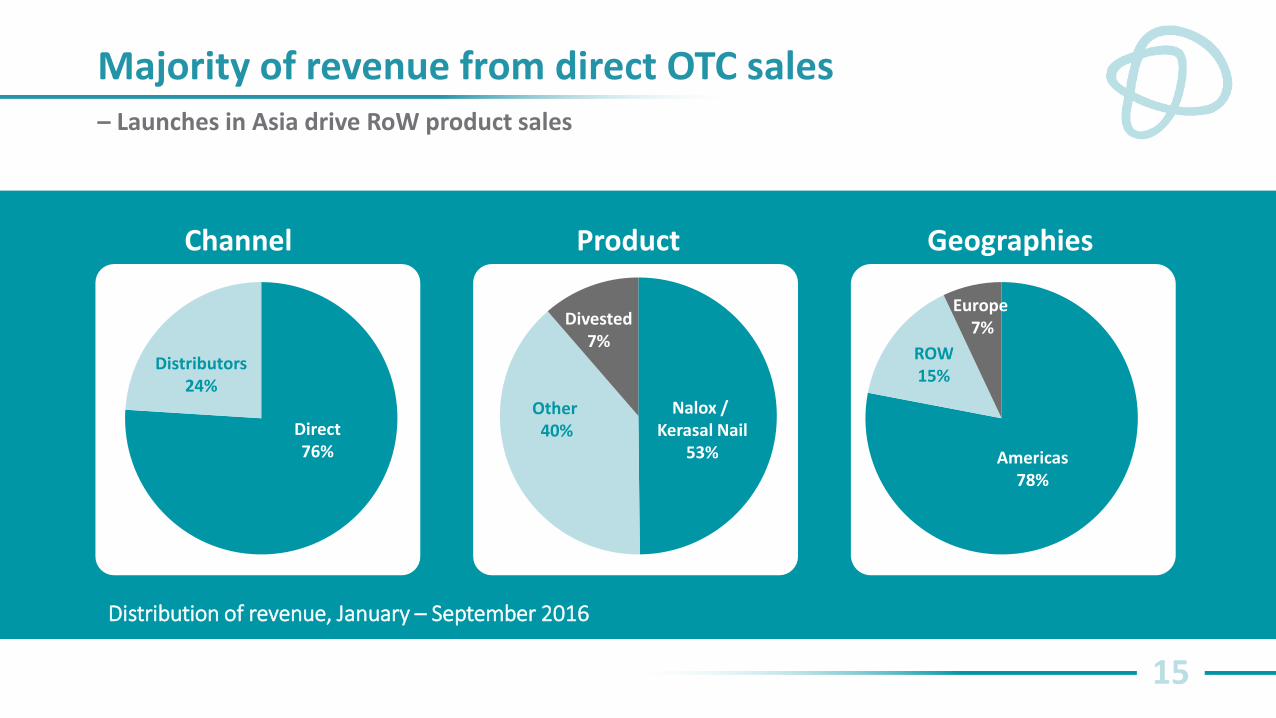

– Launches in Asia drive RoW product sales

15

Majority of revenue from direct OTC sales

Channel Product Geographies

Distributors 24%

Direct 76%

Other 40%

Nalox / Kerasal Nail

53%

Divested 7%

ROW 15%

Europe 7%

Americas 78%

Distribution of revenue, January – September 2016

Revenue segmentation

16

Revenue by channel Jul-Sep Jul-Sep Jan-Sep Jan-Sep Full-year

(MSEK) 2016 2015 2016 2015 2015

Direct sales 83 52 186 165 207

Sales of products to distributors 21 15 59 64 76

Milestone payments - 0 - 3 3

TOTAL 104 67 245 232 286

Revenue by product category Jul-Sep Jul-Sep Jan-Sep Jan-Sep Full-year

(MSEK) 2016 2015 2016 2015 2015

Nalox/Kerasal Nail®, sales of products 48 30 129 132 155

Nalox/Kerasal Nail®, milestone payments - 0 - 3 3

JointFlex®, Fergon®, Vanquish® (divested April 1 2016) - 13 16 40 52

Other products 56 23 100 58 77

TOTAL 104 67 245 232 286

• Growth in all distribution channels Q3

– Direct sales increased by 61% (12% excluding acquisitions and divestments)

– Distributor sales increased by 42% (88% excluding divested brands)

Due to the rounding component, totals may not tally.

17

Balance Sheet

(MSEK) June 30, 2016 Sep 30, 2016 Assets Intangible fixed assets 242 592 Property, plant and equipment 1 1 Financial assets 0 11 Deferred tax asset 10 6 Total non-current assets 253 609 Inventories 17 39 Trade receivables and other receivables 60 77 Current financial assets 200 - Cash and bank balances 196 111 Total current assets 474 227 TOTAL ASSETS 726 836 Equity and liabilities Equity 380 397 Long-term interest-bearing liabilities 294 378 Long-term non-interest-bearing liabilities - 19 Current non-interest-bearing liabilities 51 41 TOTAL EQUITY AND LIABILITIES 726 836

Newskin, PediaCare and Fiber Choice acquired for $40 million + inventory → reduces cash, bond tap issue added cash

Increased by ca 3 month inventory of acquired products, GM ca 60%

Acc receivable increased, ca 3 months payment terms for acquired products

Bond tap issue, ca 85 MSEK

Product rights bought for $40 million

Significant changes during Q3:

Dermoplast option

Holdback

Overview

Q3 2016 - Highlights

Commercial Operations and Innovation Engine

M&A Opportunities

Focus on strategic brands in the U.S.

Strategic brands

• Kerasal® and Emtrix® - Foot care

• New Skin - Antiseptic liquid

• Balmex® - Diaper rash

• Domeboro® - Derma/Skin irritation

19

Mature brands

• Fiber Choice® - Prebiotic fiber supplements

• PediaCare® - Pediatric cough cold (under divestment)

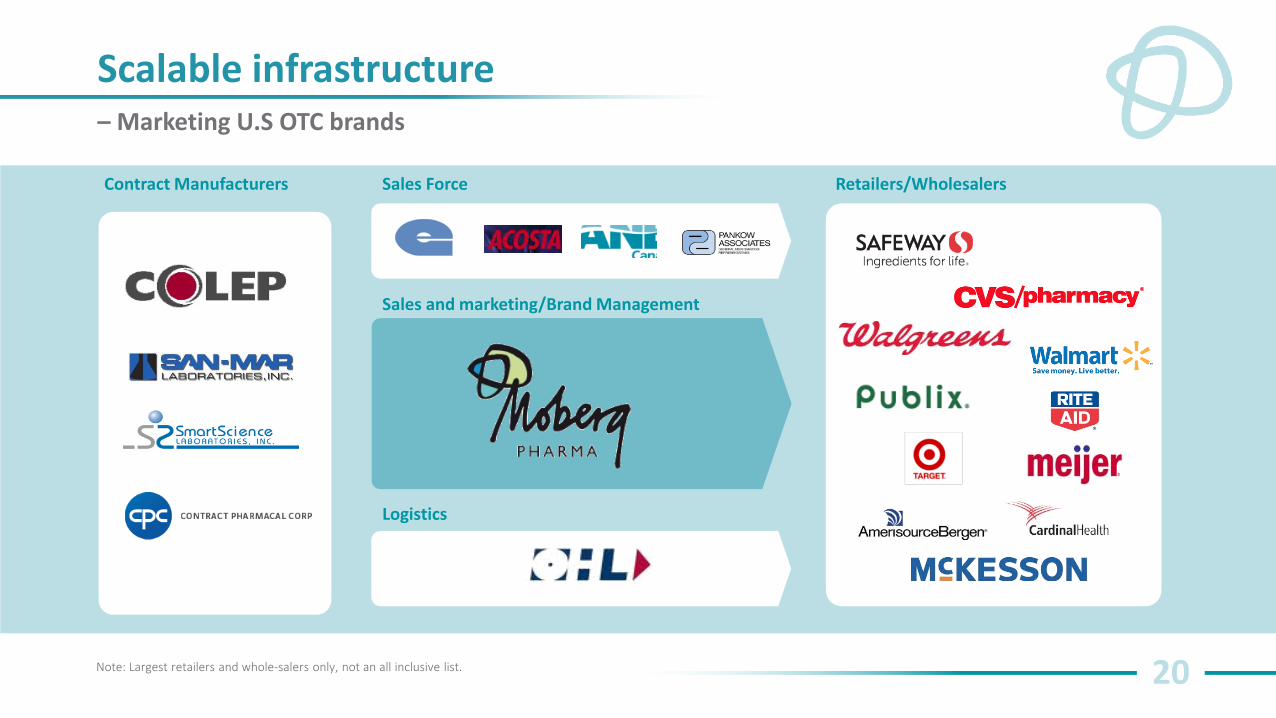

Scalable infrastructure – Marketing U.S OTC brands

20

Retailers/Wholesalers Contract Manufacturers Sales Force

Logistics

Sales and marketing/Brand Management

Note: Largest retailers and whole-salers only, not an all inclusive list.

Growth potential in Asia

• Sales in ca 40 markets

• Market leader or top 3 position in Nordics, several EU and Asian countries

• Growth in all markets Q3 2016:

– RoW growth 88%

– Europe growth 158%

• Asian launches progress well

• Launches initiated in Japan and Taiwan

• Direct sales launch initiated in the UK

– for Distributor Sales

21 Note: Three largest distributors only, not an all inclusive list.

Pipeline assets – target leadership in two niches – Building on Topical drug delivery know how

22

Pipeline Asset

Indication

Status

Peak sales potential, m$

USP

MOB-015 Onychomycosis Phase 3 started Q316

250-500 Topical terbinafine with fast visible improvement and superior cure rates (Patent term 2032, granted in major territories)

BUPI Oral Mucositis and oral pain

Phase 3 preparation

50-100 Lozenge formulation with effective pain relief for 2-3 hrs(vs 0,5 hrs for competition) (Patent term 2031, granted in EU, pending US/CAN)

Source: Moberg Pharma analysis and estimate

MOB-015 target: Market leadership in Nail Fungus

23

• MOB-015 builds on Emtrix/Kerasal nail, adds terbinafine

• Phase 2 demonstrated efficacy and safety

• Phase 3:

– Managed by leading Derm CROs ProInnovera (EU) and TKL (US/CA)

– Manufacturing partner Colep co-invests in MOB-015

– Primary endpoint: Complete Cure after 52w

– Timeline: Aiming at completing enrollment mid 2017 Data H2 2018

Source: An open, single center pilot study of efficacy and safety of topical MOBO15B in the treatment of distal subungual onychomycosis, Faergemann et al, poster presentation at American Academy of Dermatology, March 2016; 54% of the patients completing the study were mycologically cured. Mycological cure for FAS was 52% and for PPAS 60%

1000X 40X 54% MYCOLOGICAL CURE MORE TERB IN NAIL BED VS ORAL MORE TERB IN NAIL VS ORAL

MOB-015

24

Phase 2 results demonstrates efficacy and safety

Source: Moberg Pharma data on file, MOB-015 phase II study

* 54% of patients completing the treatment (13 of 24), 52% of FAS (13 of 25) and 60% of PPAS ** Means 10% or less clinical involvement *** Post-hoc analysis

MYCOLOGICAL CURE AT 60 WEEKS* MYC CURE AT 24 WEEKS NEGATIVE CULTURE AT 60 WEEKS MYC CURE AND ALMOST CURED OR CURED** CLEAR NAIL GROWTH***

TBF IN NAIL BED (MEDIAN) 40X ORAL TBF IN NAIL (MEDIAN) 1000x ORAL

54%

40%

100%

29%

>4.5 mm

45 µg/g

1610 µg/g

25

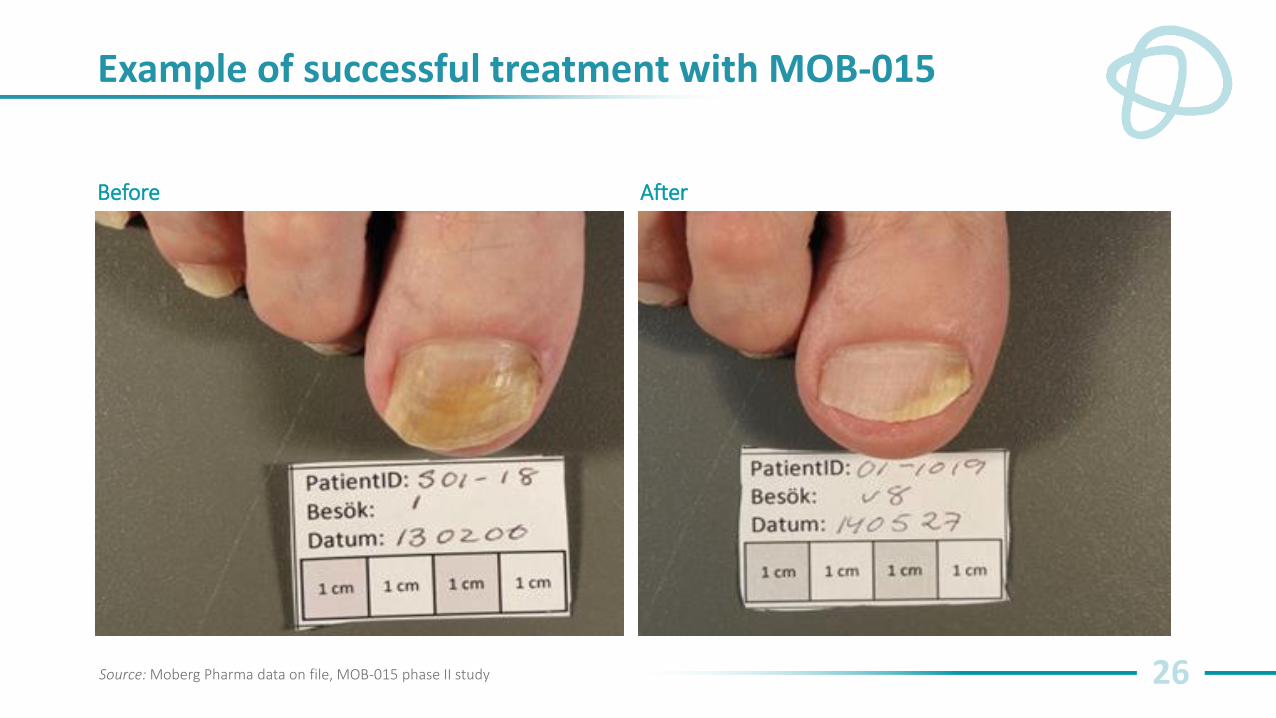

Example of successful treatment with MOB-015

Before After

Source: Moberg Pharma data on file, MOB-015 phase II study

26

Example of successful treatment with MOB-015

Before After

Source: Moberg Pharma data on file, MOB-015 phase II study

27

Example of successful treatment with MOB-015

Before After

Source: Moberg Pharma data on file, MOB-015 phase II study

28

Example of successful treatment with MOB-015

Before After

Source: Moberg Pharma data on file, MOB-015 phase II study

Pat nr 1011

29

Example of too severe nail included in Phase 2

Source: Moberg Pharma data on file, MOB-015 phase II study

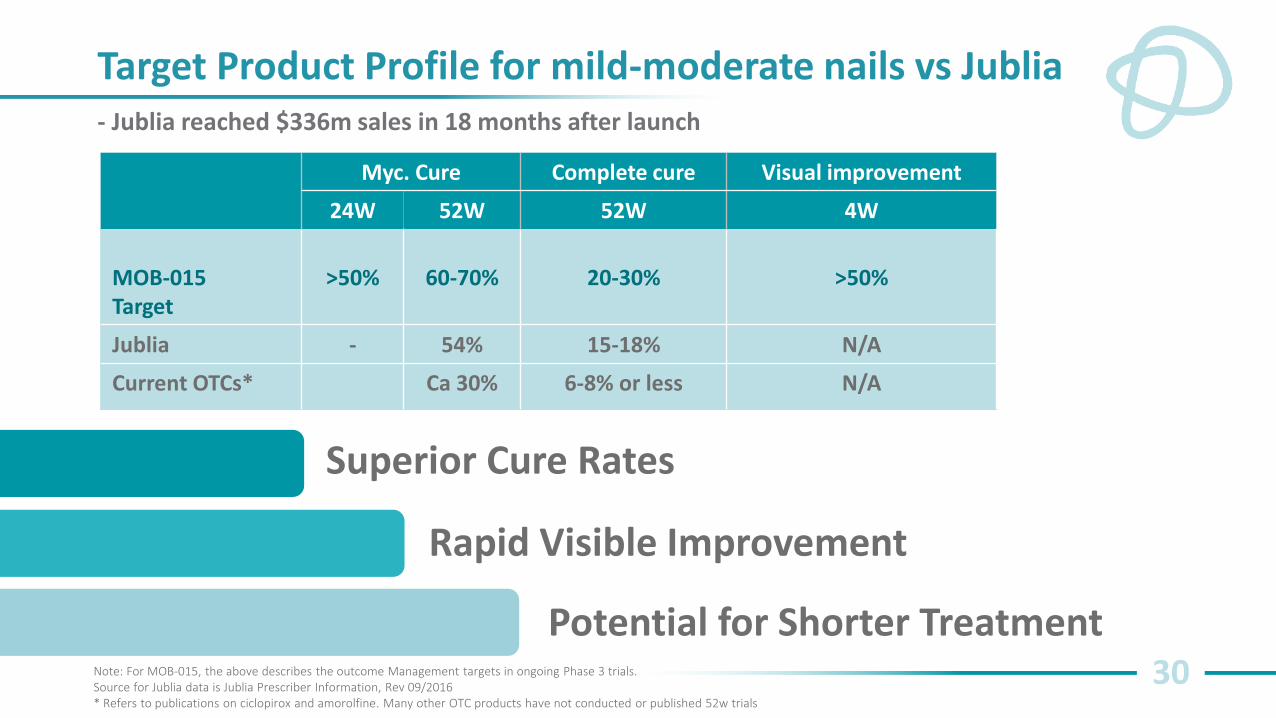

Target Product Profile for mild-moderate nails vs Jublia - Jublia reached $336m sales in 18 months after launch

30

Myc. Cure Complete cure Visual improvement

24W 52W 52W 4W

MOB-015 Target

>50%

60-70%

20-30%

>50%

Jublia - 54% 15-18% N/A

Current OTCs* Ca 30% 6-8% or less N/A

Superior Cure Rates

Rapid Visible Improvement

Potential for Shorter Treatment Note: For MOB-015, the above describes the outcome Management targets in ongoing Phase 3 trials. Source for Jublia data is Jublia Prescriber Information, Rev 09/2016 * Refers to publications on ciclopirox and amorolfine. Many other OTC products have not conducted or published 52w trials

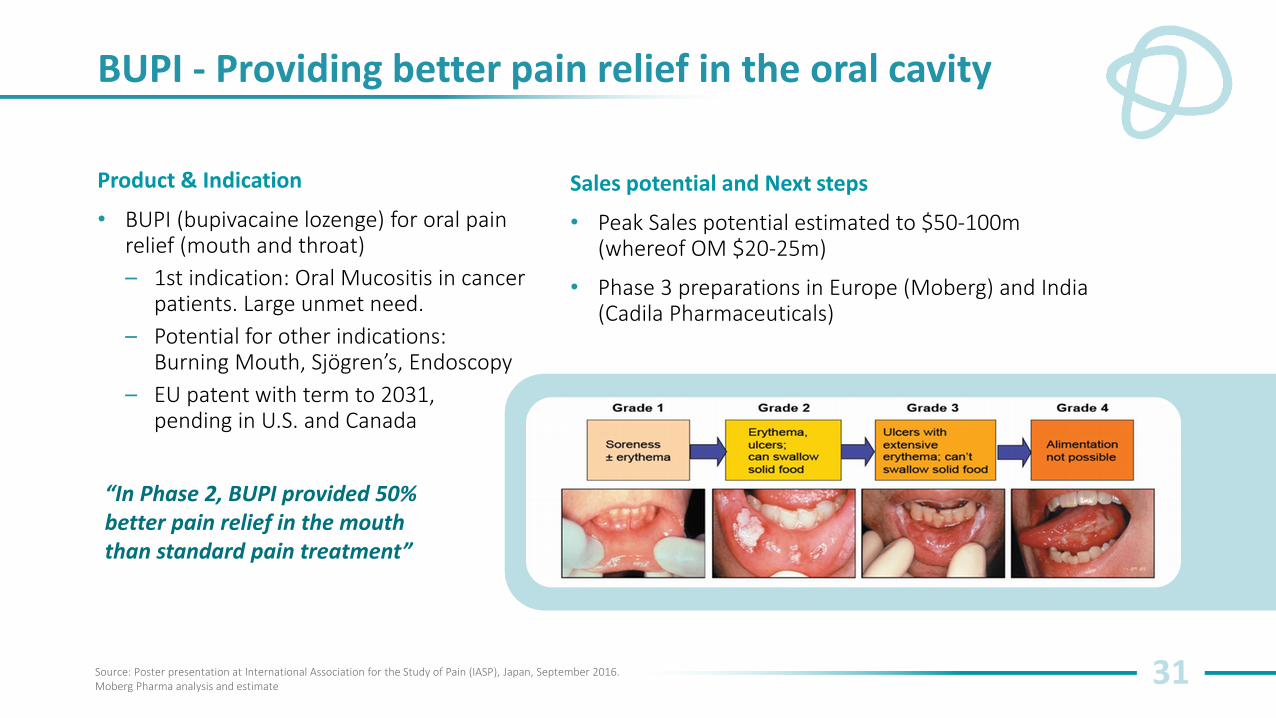

BUPI - Providing better pain relief in the oral cavity

Product & Indication

• BUPI (bupivacaine lozenge) for oral pain relief (mouth and throat)

– 1st indication: Oral Mucositis in cancer patients. Large unmet need.

– Potential for other indications: Burning Mouth, Sjögren’s, Endoscopy

– EU patent with term to 2031, pending in U.S. and Canada

31

Sales potential and Next steps

• Peak Sales potential estimated to $50-100m (whereof OM $20-25m)

• Phase 3 preparations in Europe (Moberg) and India (Cadila Pharmaceuticals)

“In Phase 2, BUPI provided 50% better pain relief in the mouth than standard pain treatment”

Source: Poster presentation at International Association for the Study of Pain (IASP), Japan, September 2016. Moberg Pharma analysis and estimate

- Control group had access too oral painkillers, morphine and lidocain mouthwash

32

Phase 2 – Significantly lower pain levels in BUPI group

0

10

20

30

40

50

60

70

BUPI Control

baseline average max VAS

• Primary endpoint: 31% less pain in BUPI group (Highest VAS score in mouth/pharynx, p=0,0032) • In Mouth only: 50% less pain in BUPI group (p=0,0002)

0

5

10

15

20

25

30

35

40

BUPI Control

baseline average max VAS

VAS Score (Highest of Mouth/Pharynx) VAS Score in Mouth only

-40% -49%

Why invest in Moberg Pharma – Strategy for Shareholder value

33

Commercial niche strategy enables a growing and profitable base business

Pipeline with large potential and at reasonable risk - Proven molecules limit TTM, cost and risk

Acquisition strategy with substantial value potential - 6 transactions since 2012

Strong Team and track record

Appendix

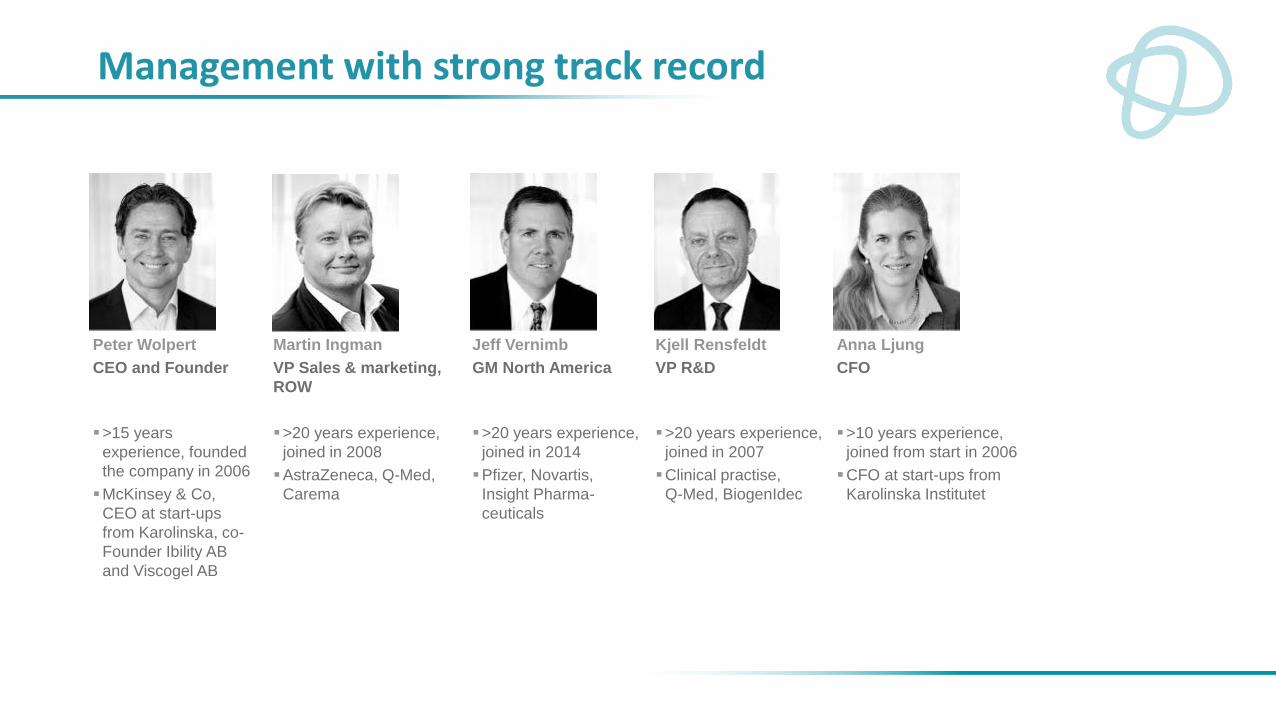

Management with strong track record

Anna Ljung

CFO

>10 years experience,

joined from start in 2006

CFO at start-ups from

Karolinska Institutet

Peter Wolpert

CEO and Founder

>15 years

experience, founded

the company in 2006

McKinsey & Co,

CEO at start-ups

from Karolinska, co-

Founder Ibility AB

and Viscogel AB

Kjell Rensfeldt

VP R&D

>20 years experience,

joined in 2007

Clinical practise,

Q-Med, BiogenIdec

Martin Ingman

VP Sales & marketing,

ROW

>20 years experience,

joined in 2008

AstraZeneca, Q-Med,

Carema

Jeff Vernimb

GM North America

>20 years experience,

joined in 2014

Pfizer, Novartis,

Insight Pharma-

ceuticals

Experienced Board

36

Thomas Thomsen

Ex. Johnson &

Johnson Consumer,

Reckitt Benckiser

and Novartis

Chairman of

Walmark a.s.(Czech

Republic) and Non-

Executive Director

of Symprove (UK),

NoA (Norway) and

Alkalon (Denmark).

Torbjörn Koivisto

Ex. Mannheimer

Swartling, Lindahl and

Bird & Bird.

Bard member of

Hemcheck Sweden AB,

Forslid & Co AB and

KIBACQ AB.

Thomas Eklund

(Chair)

Ex. Investor Growth

Capital AB, Alfred

Berg ABN AMRO

Capital Investment

AB, Handelsbanken

Markets.

Chairman of Swevet

AB and Itrim AB, and

board member of

Boule Diagnostics

AB, Biotage AB,

Neoventa Medical

AB, Memira AB,

Rodebjer Form AB.

Wenche Rolfsen

Ex. Pharmacia and

Quintiles Scandinavia

AB.

Chairman of Index

Pharmaceutical and

Sarsia Seed, Norway.

Board member of

Swedish Match AB

and Smartfish,

Norway.

Geert Cauwenbergh

Ex. Barrier Therapeutics

(U.S.) and Johnson &

Johnson in the U.S.

Managing Partner of

Phases123 LLC (U.S.),

and Board member of

Cutanea Life Sciences

(USA), Phosphagenics

(ASX-Australia) and RXi

Pharmaceuticals Corp

(U.S)

Mattias Klintemar

Östersjöstiftelsen.

Ex. Morphic Technologies

AB, Hexaformer, ABG

Sundal Collier and Arthur

Andersen.

Chairman of the board at

Dilafor and board

member of Ceba/Oatly

and Phoniro.

Share price development last 3 years

37

Source: Bloomberg

0,00

10,00

20,00

30,00

40,00

50,00

60,00

70,00

80,00

11

-28

-13

1-2

8-1

4

3-2

8-1

4

5-2

8-1

4

7-2

8-1

4

9-2

8-1

4

11

-28

-14

1-2

8-1

5

3-2

8-1

5

5-2

8-1

5

7-2

8-1

5

9-2

8-1

5

11

-28

-15

1-2

8-1

6

3-2

8-1

6

5-2

8-1

6

7-2

8-1

6

9-2

8-1

6

11

-28

-16

SEK

Shareholders - By Sep 30, 2016

38

Largest Shareholders 30 Sep 2016 Number of shares Share capital and

voting rights

ÖSTERSJÖSTIFTELSEN 2 238 074 15.7

FÖRSÄKRINGSAKTIEBOLAGET, AVANZA PENSION 1 246 817 8.7

GRANDEUR PEAKS INERNATIONAL (FUNDS) 1 016 280 7.1

BANQUE CARNEGIE LUXEMBOURG S.A, (FUNDS) 619 394 4.3

WOLCO INVEST AB(1) 600 000 4.2

NORDNET PENSIONSFÖRSÄKRING AB 381 284 2.7

HANDELSBANKEN SVENSKA SMABOLAG, SFOND 300 000 2.1

SOCIETE GENERALE 279 532 2

MERRIL LYNCH PROF CLEAR CORP 269 446 1.9

UBS SEC. LLC HFS CUST. SEGR. ACC. 258 000 1.8

STATE STREET BANK & TRUST COM., BOSTON 200 000 1.4

SUM, 11 LARGEST SHAREHOLDERS 6 868 827 51.9

Other Shareholders 7 420 361 48.1

TOTAL 14 289 188 100

(1) Owned by CEO Peter Wolpert

39

Equity Analysts

Klas Palin, Redeye Phone: +46 8 545 013 44 E-mail: [email protected]

Christian Lee, Remium Nordic AB Phone: +46 8 454 32 21 E-mail: [email protected]

Sten Gustafsson, ABG Sundal Collier Phone: +46 8 566 28 693 E-mail: [email protected]

Jerry Isaacson, LifeSci Capital Phone: +1 (646) 597-6991 E-mail: [email protected]

Peter Östling, Pareto Securities Phone: +46 84 02 52 65 Email: [email protected]

Analyst coverage

CONFIDENTIAL

Bond Analysts

Ingvar Mattson, Swedbank Phone: +46 8 700 93 49 E-mail: [email protected]

Jacob Zachrison, Carnegie Phone: +46 8 5886 87 05 E-mail: [email protected]

Moberg Pharma AB (Publ) Gustavslundsvägen 42, 5 tr.

167 51 Bromma mobergpharma.se