crdb bank plc...2015/12/31 · steady balance sheet growth 13 financial position • customer...

TRANSCRIPT

CRDB BANK PLC

The Bank that Listens

2

About Us CRDB Bank Plc is a leading, wholly-owned private commercial bank in Tanzania

offering a comprehensive range of Corporate, Retail, Treasury, Premier and

Microfinance Services.

The Bank was established in 1996 and has grown and prospered over the years to

become the most innovative, first choice, and trusted bank in the country.

CRDB Bank was listed on the Dar es Salaam Stock Exchange on 17th June, 2009.

Vision and Mission

Vision:

To be the leading Bank, which is customer need driven with competitive returns to

shareholders.

Mission

To provide competitive and innovative financial products and services leveraging

technology to achieve distinctive customer experience. We strive to create value for

stakeholders and the society.

Economic outlook

3

Global Economy

• Global economic activity for 2015 is projected at 3.1 percent, 0.3 percentage point lower than

2014 and 0.2 percent point below the forecast in July 2015 WEO.

• Global economic activity is projected to gather some pace in 2016 with a growth of 3.4

percent.

• Growth in sub-Saharan Africa slowed in 2015 this year to 3.8 percent (from 5.0 percent in

2014)

Tanzania economy

• Real GDP expanded at 7.4 percent in 2015 and is projected at 7.2 percent in 2016.

• The Annual Headline Inflation rate for the month of December 2015 increased to 6.8% from

4.8% recorded in December 2014.

• The Shilling continued to stabilize at levels of 2100/2200 following inflows from export of

commodities.

– The overall lending rate in December remained at 16.00 % same as of December 2014.

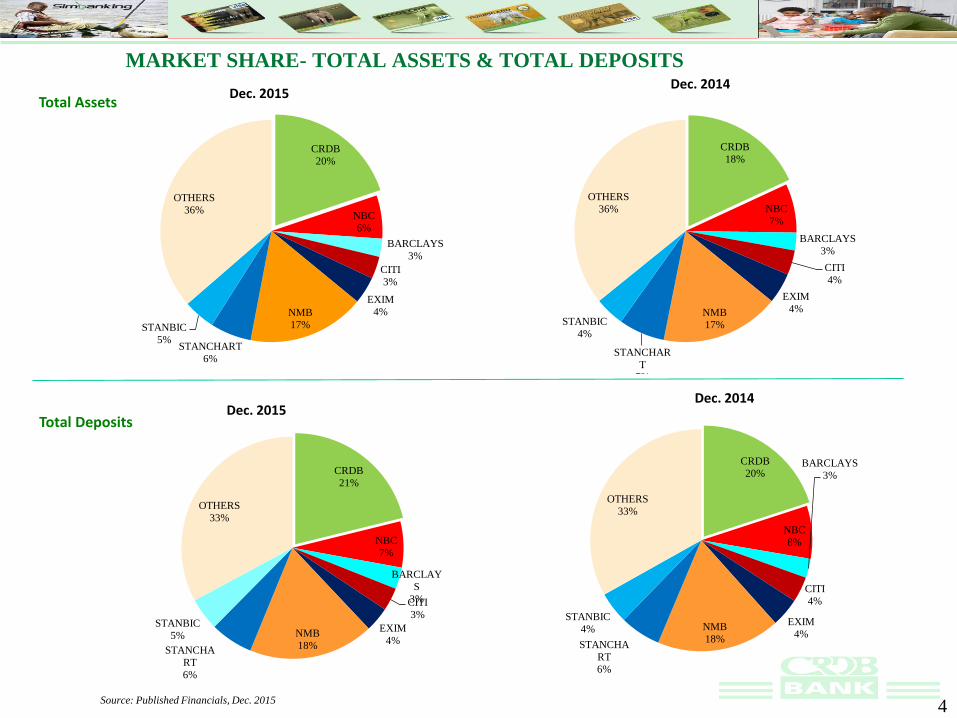

MARKET SHARE- TOTAL ASSETS & TOTAL DEPOSITS

Source: Published Financials, Dec. 2015

Total Assets

Total Deposits

Dec. 2015Dec. 2014

Dec. 2015Dec. 2014

4

CRDB

20%

NBC

6%

BARCLAYS

3%

CITI

3%

EXIM

4%NMB

17%

STANCHART

6%

STANBIC

5%

OTHERS

36%

CRDB

18%

NBC

7%

BARCLAYS

3%

CITI

4%

EXIM

4%NMB

17%

STANCHAR

T

7%

STANBIC

4%

OTHERS

36%

CRDB

21%

NBC

7%

BARCLAY

S

3%CITI

3%

EXIM

4%NMB

18%STANCHA

RT

6%

STANBIC

5%

OTHERS

33%

CRDB

20%

NBC

8%

BARCLAYS

3%

CITI

4%

EXIM

4%NMB

18%STANCHA

RT

6%

STANBIC

4%

OTHERS

33%

MARKET SHARE - SHAREHOLDERS’FUNDS AND LOANS & ADVANCES

Source: Published Financials, Dec. 2015

Capital

Loans & Advances

Dec. 2015 Dec. 2014

Dec. 2015 Dec. 2014

5

CRDB

18%

NBC

6%

BARCLAYS

2%

CITI

4%

EXIM

3%

NMB

17%

STANCHAR

T

6%

STANBIC

4%

OTHERS

40%

CRDB

15%

NBC

6%BARCLAYS

2%CITI

5%

EXIM

4%

NMB

19%

STANCHART

7%

STANBIC

5%

OTHERS

37%

CRDB

22%

NBC

6%

BARCLAYS

3%CITI

1%

EXIM

4%NMB

17%

STANCHART

5%

STANBIC

3%

OTHERS

39%

CRDB

21%

NBC

6%

BARCLAYS

3%CITI

1%

EXIM

4%NMB

17%

STANCHAR

T

6%

STANBIC

3%

OTHERS

39%

The Banking Industry continued to be competitive with 56 banks operating in the

market, but the market is controlled by 5 Banks led by CRDB.

Banks continue to introduce innovative products and services such as Internet

banking, Mobile banking and cards

– Expanding with additional physical and e-banking outlets – ATM’s, mobile

banking, internet banking.

– Competition for payment system – Debit Cards, prepaid cards, Money transfer

and payment system by telecoms i.e. M-Pesa

5 banks including CRDB Bank PLC licensed to started Agency banking

– Agent Banking is expected to enhance accessibility and convenience of banking

services to customers.

Increasing competition for qualified staff.

Potential for growth expected in – Mortgage finance, Islamic banking, Investment

Banking, Agent Banking and micro-finance and insurance.

Market

6

Bank Financial Performance

as at 31st December 2015

7

CRDB Bank PLC offers a

comprehensive range of

Corporate, Retail, Treasury,

Premier, Agent banking and

microfinance services

Network footprint of;

– 199 branches including

mobile branches and service

centers.

– 432 ATMs including 18

Depository ATMs,

– 778 Merchants Network

– 1,747 Agents (Fahari

Huduma)

– 441 Microfinance partner

institutions.

– 222 E-commerce merchants

CRDB Profile end of December, 2015

851997

1,153 1,239

1,311 1,437

1,658

1,898

2,158

2,387

2,651

34 38 44 56 6072 82

93 103120

199

30 50 71

100

132

164

190

245

311

374

432

0

50

100

150

200

250

300

350

400

450

500

0

500

1000

1500

2000

2500

3000

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Number of Staffs Number of Branches Number of ATMs

8

9

Shareholding Structure before and after Rights Issue 31.12.2015

(After rights issue)

30.06.2015

(Before rights

issue)

NAME SHARES % SHARES %

Above 10%

DANIDA Investment Fund 548,067,648 21.0 467,781,934 21.5

PPF Pension Fund 260,882,095 10.0 217,401,746 10.0

Sub Total 808,949,743 31.0 685,183,680 31.5

Above 1% and less than 10%

CDC Group Plc / International Finance Corporation / Africa Capitalization Fund Ltd 130,692,741 5.0 0 0

Mr. Aunali F Rajabali and Sajjad F Rajabali 105,506,395 4.0 60,100,945 2.8

Pinebridge 78,878,880 3.0 65,732,400 3.0

General Partners IV Ltd-TZ 64,704,702 2.5 55,082,392 2.5

LAPF Pension Fund 58,077,549 2.2 48,397,958 2.2

Blakeney General Partners III Ltd 52,953,203 2.0 47,805,578 2.2

PSPF Pension Fund 37,837,620 1.4 31,531,350 1.4

Hans Macha 32,764,200 1.3 27,303,500 1.3

National Health Insurance Fund 32,040,040 1.2 26,700,034 1.2

Western Zone Tobacco Growers Cooperative Union Ltd 30,000,000 1.1 25,000,000 1.1

CMG Investment Ltd 29,330,971 1.1 24,742,476 1.1

Kimberlite Frontier Master Africa Fund LP RCKM 28,720,830 1.1 - -

Blakeney Investors - - 21,120,714 1.0

Altree Custody Services Ltd – 008 -Tanzania - - 27,013,409 1.2

Lind Development Fund - - 21,660,000 1.0

Patrick Schegg - - 21,230,300 1.0

Sub Total 681,507,131 25.9 503,421,056 23.1

Less than 1%

More than 28,000 shareholders 1,121,381,710 43.1 987,927,424 45.4

Grand Total 2,611,838,584 100.0 2,176,532,160 100.0

The Bank successfully raised Tzs. 150 bn. as additional capital from the rights issue which closed in mid

July 2015.

Investment Ratio as at 31st December, 2015

10

Share Performance As at 31st Dec. 2015 As at 31st Dec. 2014

Market Price Closing TZS 405 TZS 430

Earning per share (EPS) 53.3 43.9

Price Earning Ratio (P/E) 7.6 9.8

Book Value (BV) 267.5 203.0

Price book value ratio (P/B) 1.5 2.0

Market Capitalisation (TZS billions) 1,057.8 935.9

Foreign Holding (%) 22.0 19.6

CRDB Bank Plc. – Performance Summary

(TZS Billion)

Interest Income 499.8 371.7 34% 16%

Interest Expenses 108.8 95.5 14% 18%

Net Interest Income 390.9 276.2 42% 15%

Net Fees and commissions 143.9 121.4 19% 13%

Net Foreign Exchange Income 35.7 29.3 22% 39%

Operating Expenses 315.6 258.1 22% 18%

Profit Before Tax 198.9 132.2 50% 15%

Loans & Advances to Customers 3,309.6 2,545.2 30% 24%

Customer Deposits 4,236.4 3,390.2 25% 17%

Shareholder Equity 701.5 441.1 59% 27%

Total Assets 5,436.7 4,210.1 29% 20%

Return on Avg. Assets 4.1% 3.6%

Return on Avg. Equity 24.4% 25.2%

NPL/Total Loans 6.6% 5.0%

Dec. 2015 Dec. 2014%

Change

Note: Total Assets for the Group closed at 5 trillion for the first time

Industry

11

Operating Profit Grew 50% YoY

12

Profitability

NII and other income coupled with operating efficiencies supported the overall profit growth

114,820

22,464 6,341 427 19,864 57,445

198,978

Operating

profit 2014NII Fee and

CommisionsFx Trading &

RevaluationOthers Impairment Operating

ExpensesOperating

profit 2015

50%

48,9

97

51,0

13

119,

282

130,

008

132,

244

198,

978

47,2

46

37,7

10

80,5

43

84,3

78

95,6

45

139,

285

21.4%

15.5%

28.2%24.4%

22.0%20.0%

0. 0%

5. 0%

10. 0%

15. 0%

20. 0%

25. 0%

30. 0%

-

50, 000

100, 000

150, 000

200, 000

250, 000

2010 2011 2012 2013 2014 Q4 2015 Q4

PBT PAT ROE

Profitability Trend

• YoY growth of 50%

• Mainly contributed by increase in NII

and fees and commissions.

• ROE recorded decrease due to

additional capital of about TZS

150bn.

• Cost to income ratio as at Dec. 2015

was 54%.

Tzs

Mil

lions

Tzs

Mil

lions

12

Steady Balance Sheet Growth

13

Financial Position

• Customer Deposits Accounts for 80% of

total funding in the Balance Sheet.

• Borrowing includes subordinated debt

87.3bn,other borrowings 206.9 bn.

29%

Key sources of funding – Tzs billions

Tzs

bil

lions

13

2,30

5

2,71

4

3,07

5 3,55

9

4,21

0 5,43

4

24%

18%

13%

16%18%

29%

25%

17% 16% 15%18%

20%

2010 2011 2012 2013 2014 Q4 2015 Q4

0%

5%

10%

15%

20%

25%

30%

35%

Total assets Crdb growth Industry growth

Loans and Advances

14

Steady Growth in Loan and Advances.

Loans and advances growth and contribution by key segments as at December 2015

Portfolio diversification among sectors and segments

• YoY Loan growth 30% above industry

24%.

• 29% of the total Loan is held in Foreign

Currency.

• FX Loans grew by 27% mainly due to

TZS depreciation against USD by 29%.

• Remarkable growth in retail segment

accounting for 41% of total loan portfolio

(2014 – Q3 was 36%)

821 979 1,177 1,393 1,795 2,357

302 450

630 600

750

953

17%

24%26%

10%

28%

30%

19%

30%

18%

17%

21%

24%

0%

5%

10%

15%

20%

25%

30%

35%

-

500

1,000

1,500

2,000

2,500

3,000

3,500

2010 2011 2012 2013 2014 Q4 2015 Q4

LCY FCY Bank Growth Industry GrowthTzs

bil

lions

62%

11%

17%

4%

6%

1%

55%

11%

23%

4%

7%

1%

0% 10% 20% 30% 40% 50% 60% 70%

Corporate

SME

Personal

Staff

MFSC

Mortgage

2015

2014

21%

18%

15%

8%

8%

5%

5%

19%

27%

19%

14%

4%

7%

3%

4%

21%

0% 5% 10% 15% 20% 25% 30%

Individual

Agriculture

Trading

Manufacturing

Transport and comm

Building & constru

Hospitality

Others

2015

2014

Customer Deposits

15

Funding Growth Through Deposit Mobilization

Deposit Growth

1,494 1,692 1,712 2,512 2,617

3,490 525 717 879

850 773

746

2010 2011 2012 2013 2014 Q4 2015 Q4

CASA Time Deposits

• Low cost CASA base grew

to 82% of total deposits with

YoY growth of 34%.

• YoY Deposit growth 25%

• Mainly from growth in

Bank network, Agency and

Government business and

customer convenience.

• 25% of the total deposits

are held in Foreign

Currency.

• Foreign Currency deposits

grow by 23% mainly

resulting from TZS

deprecation against USD.34%

25%

1,498 1,734

1,950

2,619 2,499

3,136 521

675 641

405 891

1,007 25%

19%

8%

17%

12%

22%

25%

16%

13%12%

13%

17%

0%

5%

10%

15%

20%

25%

30%

-

500

1, 000

1, 500

2, 000

2, 500

3, 000

3, 500

4, 000

4, 500

2010 2011 2012 2013 2014 Q4 2015 Q4

LCY FCY CRDB- Growth Industry Growth

Tzs

bil

lions

Tzs

bil

lions

16

18.0%

14.0%16.0%

14.5%13.1%

14.2%

18.0%

15.0%16.0%

15.1% 14.3%

18.3%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

18.0%

20.0%

2010 2011 2012 2013 2014 Q4 2015 Q4

Tier I Total

1,285 1,605 1,849 2,334 2,882

3,652 21

8 8

3 14

9 57% 59% 60%66% 69% 67%

0 %

1 0 %

2 0 %

3 0 %

4 0 %

5 0 %

6 0 %

7 0 %

8 0 %

-

500

1, 000

1, 500

2, 000

2, 500

3, 000

3, 500

4, 000

2010 2011 2012 2013 2014 Q4 2015 Q4

Market Risk

Credit Risk

Risk weighted Assets/Total Assets

Capital adequacy ratio

Risk weighted assets

Tzs

bil

lions

17

Non performing Loans and Provisions

Diversification of the loan book - Dec. 2015

11.5%

9.4%

6.8%6.2%

5.0%

6.6%

9.3%

6.8% 7.3%6.5%

6.7%

6.8%

2010 2011 2012 2013 2014 Dec-15CRDB NPL Ratio Industry Average

133 135 125 126 129 218

23%

34%

26% 28% 24%

49%

0 %

1 0 %

2 0 %

3 0 %

4 0 %

5 0 %

6 0 %

-

50

100

150

200

250

2010 2011 2012 2013 2014 Dec-15

Total NPL

27%

20%

14%6%

7%

3%4%

20%

Individual

Agriculture

Trading

Manufacturing

Transport and communication

Building & construction

Hospitality

Others 7%

14%

8%

2%

11%

3%

14%

2%

6%

10%

4%

2%

3%

3%

7%

2%

Others

Hospitality

Building & construction

Transport and …

Manufacturing

Trading

Agriculture

Individual

Provission NPL

Sector NPL and Provision as at Dec. 2015

TZ

S b

illi

ons

Sector NPL as a %age of Total NPL as at Dec. 2015

19.8%

4.5%

14.2%

6.7%

3.0%

27.4%

4.2%

20.2%

42.9%

7.4%

6.7%

1.9%

3.4%

7.5%

8.9%

21.2%

Agriculture

Manufacturing and processing

Trade and Commerce

Transport and Communication

Building and Construction

Individuals /Personal Loans

Hospitality

Others

NPL % Outstanding Loan %

18

1. CRDB Microfinance Services Company Limited

The Bank offers Microfinance products through its subsidiary by partnering with

Microfinance institutions (MFIs) mostly savings and credit cooperative societies (SACCOS).

The Bank provides financial products - microfinance loans, mobilise deposits from partner

MFIs on behalf of the parent company, insurance products and services, information and

communication technology solutions and support.

The number of partner MFIs were 441 in Dec. 2015.

Total loans extended by the Bank to these institutions at the end of December 2015 stood at

TZS 221 billion.

The subsidiary made a profit of TZS 5.8 billion compared to TZS 4.9 billion in 2014, which is

a growth of 16%.

CRDB Bank Plc Subsidiaries

2. CRDB Bank Burundi S.A.

The Bank has also a subsidiary in Bujumbura, capital city of Burundi and opened four branches.

The subsidiary recorded a profit of TZS 1,064 million compared to TZS 3,578 million loss

recorded in 2014 despite security instability in the country. The subsidiary was able to breakeven.

The subsidiary total assets as at 31st December 2015 grew to TZS 154 billion from TZS104 billion

in 2014.

Total deposits was TZS 60,363 million compared to TZS 28,894 million in 2014.

19

20

STRATEGIC FOCUS FOR 2016

For the past years, the Bank has been focusing on expanding its distribution channels

through opening of new outlets (mainly Government centres and Microfinance service

centres) and in alternative channels. Such investments needed to bring returns and

contribute to the profitability of the Bank. In addition to this, the Bank conducted business

process improvement with the aim of improving its customer service while also achieving

operational excellence.

Focus will therefore be on optimization of investments made and attain operation

excellence.

Thank You

21