crash insurance · 2019-01-03 · 1 dentresearch.com crash insurance: keep your dark window gains...

TRANSCRIPT

CRASH INSURANCEKeep Your Dark Window Gains

Intact and Make 20X Your Money as the Market Crashes

DENTRESEARCH.COM 1

Crash Insurance: Keep Your Dark Window Gains

Intact and Make 20X Your Money as the Market Crashes

By: Harry Dent & Rodney Johnson

As I explained in your report entitled The Dark Window Profit Blueprint: Make 10 Years' Worth of Stock Gains in the Next 12 Months, the opportunity before us is rare and powerfully profitable. But it is also extremely dangerous, because if you’re not prepared, when it slams shut it could crush you.

So, with this report, I’m going to help you prepare for the end of this Dark Window so that you can rest assured you’re making hey while the sun shines, AND that you’re ready to not only protect yourself when the inevitable storm hits, but also set up to profit from it too.

First though, it’s important that I impress on you why – and how hard – this Dark Window will slam shut.

You see, in the final part of the bull market, as stocks soar way higher, most people begin to stop fearing a crash as much as they do now. In fact, at the top of the market, everyday folks will be more likely to panic into the market, fearing they’ll miss out.

During the last Dark Window, Joe Kennedy said he knew it was time to sell when he received stock tips from a shoe shine boy. It will be the same again this time.

Right at the point where main street investors become extremely bullish again – the bottom will fall out of the market. And most people will get totally wiped out.

After the last Dark Window slammed shut in 1929, stocks declined 89%!

And they didn’t bottom until three years later, in 1932.

Even worse, the Dow Jones didn’t return to its 1929 highs until 1954 – 25 years later!

DENTRESEARCH.COM 2

If the same thing happens at the end of this Dark Window – and I’m about to show you why I expect this is virtually inevitable – that would put the Dow at just 3,500 in 2023. I see 5,500 as the minimum target.

That means stocks would slide for three straight years, and wouldn’t return to their previous highs until 2045.

My demographic research suggests stocks may not even get quite back up there because the next generation doesn’t have the growth trends the Boomers had.

If you did nothing – if you hadn’t joined us here at Boom & Bust – what would your portfolio look like then? My guess is that if your balance is down nearly 90%, your lifestyle in retirement could be best described in two words: “Scraping by.”

No more luxuries or vacations. You couldn’t contribute to your kids’ or grandkids’ lives. And a “nice” dinner might consist of baked beans and hot dogs.

Thankfully, you won’t have that experience thanks to this Dark Window and your preparations for when it slams shut.

Following the Specific Patterns and Cycles

The advantage we have here is that I follow the markets very specific patterns, based on cycles and demographic trends. The one that drives the Dark Window is a 90-year cycle that goes all the way back to the 1700s, when the democracy and free market capitalism collided, igniting the Industrial Revolution.

DENTRESEARCH.COM 3

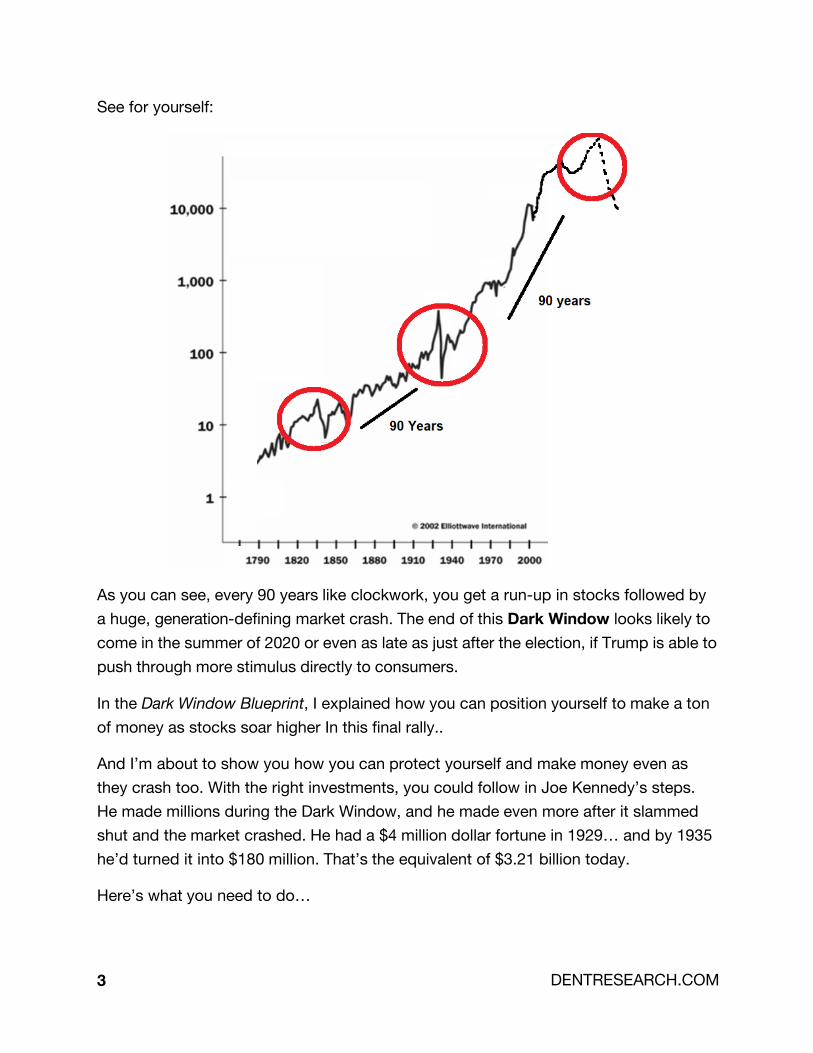

See for yourself:

As you can see, every 90 years like clockwork, you get a run-up in stocks followed by a huge, generation-defining market crash. The end of this Dark Window looks likely to come in the summer of 2020 or even as late as just after the election, if Trump is able to push through more stimulus directly to consumers.

In the Dark Window Blueprint, I explained how you can position yourself to make a ton of money as stocks soar higher In this final rally..

And I’m about to show you how you can protect yourself and make money even as they crash too. With the right investments, you could follow in Joe Kennedy’s steps. He made millions during the Dark Window, and he made even more after it slammed shut and the market crashed. He had a $4 million dollar fortune in 1929… and by 1935 he’d turned it into $180 million. That’s the equivalent of $3.21 billion today.

Here’s what you need to do…

DENTRESEARCH.COM 4

The Crash Insurance Plan First, we’ll employ options as a “hedge” against the crash. Don’t worry. Options are much easier to buy than you might think. We’re not trying to use some complicated strategy, we’re simply buying some portfolio “insurance” against the possibility of a dramatic crash.

I don’t want you to buy these options now because I’m forecasting the markets to move higher before they tank. If you bought put options and the markets went higher, you’d lose money. Instead, wait until the middle of July, and then buy put options that expire in March of 2020.

We want to buy at-the-money call options on the proxy stocks for the S&P500 (NYSE: SPY), the Invesco QQQ Trust (NYSE: QQQ), which tracks the top 100 non-financial stocks in the Nasdaq, and the Russell 2000 (NYSE: IWN), depending on what types of stock you own.

If your portfolio holds a broad mix of stocks, then the SPY is appropriate. If you hold mostly tech stocks, then choose the QQQs. And if you buy a lot of small cap stocks, then the IWN would be best. It might be that you buy a few options from each.

Select the strike price of the March 2020 puts that is closest to the price at which each of these securities are trading in mid-July. Remember that each contract controls 100 shares of stock, so if the SPY is trading at $250, then each option controls 100 shares at $250, or $25,000.

If you want to hedge a $100,000 portfolio that moves like the S&P500, you’d buy four put options on SPY.

I anticipate that you’ll hold these through the end of 2019 as the markets fall apart.

Next, dump these assets out of your portfolio… or at the very least, don’t add more of them to your portfolio. If you don’t, they’ll drag your portfolio down like a stone during the crash…

Stay away from junk bonds! Yields on junk bonds skyrocket when the economy collapses, which it will when this Dark Window slams shut, because of the sharply rising default risks.

DENTRESEARCH.COM 5

A quick glance at BAA bond yields during the 1930s reveals the danger here. Back then, yields spiked from 5.7% to 11% from mid-1930 into late 1932, when the economy was at its worst. Those bonds fell out of favor to the tune of 45% (remember, when yield goes up, value goes down in the bond market).

Stay away from utility stocks. Many people think they’ll be OK in utility stocks line SCANA (South Carolina Electric and Gas) during a crash because such companies don’t see demand go down all that much, they pay high dividends, and they benefit from lower interest rates down the road.

While this argument seems sound, don’t be fooled. Utility stocks fell 89% into early 1935! In fact, they crashed even before the broader stock market in early 1929, and lost 56% in a matter of months.

More than a decade ago, I looked at a number of 1930s stock sectors to see if utilities, alcohol, casinos, movies, cigarettes… anything… did well during the bad times. And I discovered that not a single one did. The risk premiums on these stocks all went up and the stocks all tanked, losing between 50% and 90%... some even more than that.

Stay away from real estate. This is another one of those “safe havens” that people are told to turn to, but real estate will be anything but safe during the meltdown at the end of this Dark Window. During the Great Depression, real estate didn’t bubble up the way it did into 2006 or even recently. Speculation in the property market wasn’t as rife back then. Despite this, real estate prices dropped 26% into 1933!

There are two troubling characteristics of real estate. The first is that it becomes illiquid (and so immovable) with lightning speed… and the value of your home is only what the buyer is ultimately willing to pay for it.

Now that Baby Boomers are quickly becoming die-ers rather than buyers in this sector, real estate faces a terrible decade (if not more).

Stay away from gold. Finally, gold is NOT the safe haven you’ve been led to believe all your life. Gold may be a temporary crisis hedge, but when deflation comes home to roost – which it will during the collapse ahead – gold will become a weight around your neck rather than a life jacket. I expect gold to melt down to below $1,000 before all is said and done.

DENTRESEARCH.COM 6

Then, once you’ve got the options hedge in place, and you’re removed the deadweight from your portfolio, look to add the following:

• Cash, T-bills, and high-quality CDs; • High-quality, long-term government bonds (Treasurys); and • AAA corporate bonds.

During the Great Depression (and I compare what we face ahead to that awful time in history because it will be similar, if not worse!), total gains, with interest payments on high-quality, long-term government bonds, rose by 78% from 1929 to 1941!

And lastly, here are five opportunities to look out for to grow your portfolio during a time when everyone else is running scared…

• Bet on the dollar via the PowerShares DB US Dollar Bullish ETF (NYSEArca: UUP).

• Invest in the Fixed Income Trade of the Decade by buying 30-Year Treasury bonds when the yield hits 4%.

• Buy put options on gold or buy an inverse fund like DB Gold Short ETN (NYSE: DGZ) with a target of around $750 an ounce in gold.

• Short sell oil or frackers. Oil could drop to as low as $10 a barrel before “normalcy” returns to the markets.

• Invest in India. It’s demographic and urbanization trends have positioned it to become the world’s next China.

We face a once-in-a-lifetime opportunity with this Dark Window AND the epic crash that will follow.

Prepare now. You’ll be glad you did.

Have a question or comment? Contact a member of our customer service team toll free at 888-211-2215, Monday through Friday between 9 a.m. and 8 p.m. EST, or write to us at [email protected].

Legal Notice: This work is based on what we’ve learned as financial journalists. It may contain errors and you should not base investment decisions solely on what you read here. It’s your money and your responsibility. Nothing herein should be considered personalized investment advice. Although our employees may answer general customer service questions, they are not licensed to address your particular investment situation. Our track record is based on hypothetical results and may not reflect the same results as actual trades. Likewise, past performance is no guarantee of future returns. Certain investments such as futures, options, and currency trading carry large potential rewards but also large potential risk. Don’t trade in these markets with money you can’t afford to lose. Charles Street Publishing expressly forbids its writers from having a financial interest in their own securities or commodities recommendations to readers. Such recommendations may be traded, however, by other editors, Charles Street Publishing, its affiliated entities, employees, and agents, but only after waiting 24 hours after an internet broadcast or 72 hours after a publication only circulated through the mail. Also, please note that due to our commercial relationship with EverBank, we may receive compensation if you choose to invest in any of their offerings.

(c) 2019 Charles Street Publishing. All Rights Reserved. Protected by copyright laws of the United States and international treaties. This Newsletter may only be used pursuant to the subscription agreement. Any reproduction, copying, or redistribution, (electronic or otherwise) in whole or in part, is strictly prohibited without the express written permission of Charles Street Publishing, 819 N. Charles St., Baltimore, MD 21201 USA.

Publisher..............................Shannon Sands Senior Editors.....................Harry Dent and Rodney Johnson

Boom & Bust 819 N. Charles St. Baltimore, MD 21201 USA USA Toll Free Tel.: (800) 538-0428 Contact: [email protected] Website: www.dentresearch.com