#cpaf15 ws2: value chain integration (monika sopov, joost guijt, centre for development...

Upload: technical-centre-for-agricultural-and-rural-cooperation-acp-eu-cta

Post on 09-Apr-2017

340 views

TRANSCRIPT

Value chain integration

2015, Monika Sopov, Joost Guijt

Objectives

By the end of the session you can

Define what vertical and horizontal integrations are

Identify forces that stimulate and hinder integrations in general

Identify forces that stimulate and hinder integrations in agriculture

Guiding questions

What is the difference between “comparative advantage” and “competitive advantage”?

What is the difference between a supply chain and a value chain or value net?

What differences are there between the efficiency of an individual enterprise and the efficiency of a market chain as a system?

Value Chain

The value chain describes the full range of activities which are required to bring a product or service from conception, through the different phases of production (involving a combination of physical transformation and the input of various producer services), delivery to final consumers, and final disposal after use. (Kaplinsky)

Value chain

According to Hobbs et al. (2000) 5, a value chain is differentiated from a production / supply chain because:

● Participants in the value chain have a long-term strategic vision.

● Participants recognize their interdependence and are disposed to work together to define common object, share risks and benefits, and make the relation work.

● It is oriented by demand and not by supply, and thus responds to consumer needs.

● Participants have a shared commitment to control product quality and consistency.

● Participants have a high level of confidence in one another that allows greater security in business and facilitates the development of common goals and objectives

Enterprise relations

Factors

Supply chain Value chain

Information flow Little or none Extensive

Principal focus Cost / price Value / quality

Strategy

Basic product (commodity) Differentiated product

Orientation Led by supply Led by demand

Organizational

structure

Independent actors Interdependent actors

Philosophy Competitiveness of the

enterprise

Competitiveness of the

market chain

Adapted from Hobbs et al. (2000)

Supply chain structure and flows within the

chain

Seed suppliers Wholesale purchasers

Exporting companies

End Customer

(the source

of funds) Growers

Distributors

Produce

Funds, information, know-how

Supply networks

Distributors Mother

Earth

Converters Customers

Capital

Know-how

Information

Produce

Tools used for market chain analysis

include

Value chain mapping

(Market chain history)

Market research

Quantifying performance (value added, production costs, cost drivers, transaction costs, benchmarking)

Economic and financial analysis

Assignment 1

Analyzing supply chains (1)

Draw a supply chain

● Map the core processes in the value chain

● Map the actors involved at the various stages in the

chain

● Map the activities as the product moves along the chain

● Map the support service providers to the chain. Who are

the main actors in the chain?

● Who is the most important in the chain?

● Where is the most value created in the chain?

● Who has the most power in the chain?

Assignment 1

Analyzing supply chains (2)

Draw a supply chain

● Map information flow

● Map constraints

Coordination vs. Integration

Horizontal Integration

● Growth via acquisition of one or more similar firms operating at the same stage of the production-marketing chain

Vertical Coordination

● Organization of economic activity including all the ways of harmonizing the various stages of production-processing-distribution chain

Vertical Integration

● Partial or full ownership of the various stages of production-processing-distribution chain

Vertical and Horizontal Integration

Farmer Farmer

Processor Processor

Wholesaler Wholesaler

Acquisitions or mergers of suppliers or customer businesses are vertical

integration

Acquisitions or mergers of competing businesses are horizontal integrations

Examples

Intermediate Forms of Organization:

A Continuum of Governance

Arrangements

SPOT MARKET

INTERNAL HIERARCHY (full integration)

RANGE OF INTERMEDIATE FORMS

LONG-TERM CONTRACTS

STRATEGIC ALLIANCES

QUASI-VERTICAL INTEGRATION (PARTIAL OWNERSHIP)

both parties invest resources into the relationship eg. joint venture, franchises, licenses

Strategy categories along the vertical

coordination continuum (1)

Strategy Definition Example

Spot Market Coordination intensity is low.

Parties engage in price

discovery and make either a

yes or no decision to enter

the transaction. It is easy to

walk away from the

transaction.

A corn farmer who calls up

local grain elevators to find

out the current cash price for

corn. The corn farmer

decides to sell his corn to the

highest bidder.

Specification

contract

Coordination intensity is

moderately low. Contracts

are based on the legally

enforceable establishment of

specific and detailed

conditions of exchange.

A potato farmer that signs a

production contract with a

potato processor for a

specific quality and quantity

of potatoes at a specified

delivery time.

Relation-based

alliance

Coordination intensity is

moderate. Relationship

based on shared risk and

benefits emanating from

mutually identified

objectives.

Wal-Mart and Procter &

Gamble,where Wal-Mart

agrees to share propriety

sales and inventory

information and P&G

physically locate their

employees at Wal-Mart’s

headquarters.

Equity-based

alliance

Coordination intensity is

moderately high.

Agricultural cooperative,

private firms who form a

joint venture.

Vertical

integration

Coordination intensity is

high.

Tyson coordinates the entire

poultry process from

genetics to the retail shelf

Dutch exporters in Ethiopia,

Kenya

Strategy categories along the vertical

coordination continuum (2)

Vertical integration can occur in 2 directions:

● Backward Integration (producing own inputs)

● Forward Integration (disposing of own outputs)

Source: Robert M. Grant, Contemporary Strategy Analysis, Basil Blackwell, 1995

Directions of Vertical Integration

Discussion

Why vertical integration?

Dependency

• Suppliers

• Customers

Dependency

• Suppliers

• Customers

Why Vertical Integration?

Factors

● Reduce transaction

costs

● Secure access to

resources (raw

material, distribution)

● Internalize an

externality

(technology)

● Increase monopoly

power

● Better quality control

and coordination

Dependency

Business 1

Business 2

Analyzing Vertical Integration: The Transaction

Cost Perspective

Market

transaction

Monitoring

costs

Monitoring

costs

Enforcement

costs

Enforcement

costs

Costs of

written

contract

Costs of

written

contract

Search costs Search costs Negotiating

costs

Negotiating

costs

Risks of Vertical Integration

Risks ● Costs and expenses

associated with increased overhead and capital expenditures

● Differences between

stages in optimal scale

of operation

● Managing strategically

different businesses

● Loss of flexibility resulting from inability to respond quickly to changes in the external environment

Business 1

Business 2

Dependency

The number of companies

The requirements for specific investment

The difficulty of specifying and managing contracts

Uncertainty of market demand

Scale of operations (difference)

Discussion

Will it hinder or motivate vertical

integration?

What is governance?

Characteristics of governance

Interactions between firms along a value chain are somewhat organized.

Value chains are governed when parameters requiring product, process, and logistic qualification are set which have consequences up or down the value chain

Power asymmetry

Functions of Governance

Three functions of governance (the “separation of powers”)

● the legislature (making the laws)

● the executive (implementing the laws)

● judiciary (monitoring the conformance to laws)

Consequences of (not) complying

Sanction

● Negative

● exclusion

● limiting the role which particular producers play in the chain

● imposing cost penalties for non-conformance

● Rewards

● Different level of auditing

Governance in Value Chains

Discussion

More tightly aligned supply chains are increasingly becoming common-place in the food production and distribution industries.

1. What drives the formation of more tightly aligned supply chains?

2. What are the core competencies in chain formation?

3. What are the key barriers to chain formation?

What drives the formation of more tightly

aligned supply chains?

1.1 Responding to demand and consumption

1.2 Managing /allocating risks

1.3 Productivity and technology

1.4 Government regulations and policies

1.5 Resources – efficiency and lowering cost

2. Core competencies for chain formation

1. capacity to trust and to be trust-worthy

2. improved ability to respond and customize products to end-user needs,

3. increased focus on product and process development,

4. continued focus on cost control and efficiency,

5. more emphasis on risk management,

6. optimization of the logistics and transportation/distribution system,

7. a focus on holistic systems that integrate the entire supply chain,

8. increased emphasis on quality and quality assurance along the chain,

9. more emphasis on information and information sharing,

10. increased skill in negotiation and joint decision-making,

11. development of cooperative/collaborative attitudes and perspectives,

3. Barriers to chain formation

Lack of

1. mutual trust by chain participants (A)

2. communication and information flow across chain participants (K, A)

3. commitment and willingness to invest in chain infrastructure (D)

4. awareness of the benefits and costs of more tightly aligned supply chains (A)

5. equitable sharing of the risk and rewards in a supply chain (D, K, A)

6. an acceptable governance system with equitable sharing of power and control (D, K, A)

7. a policy environment that does not constrain or limit chain (A, K, D)

8. willingness to adopt a collaborative vs. competitive business approach (A, D, K, A)

Soy case study

1.Please analyze industry from the view of the joint venture (Porter’s

five forces)

2.What are the options for sourcing soy now, and how will it change in

the future? What will happen when soy will be traded on ECX? How

can Seba Foods still ensure inclusiveness?

3.In light of the risks the company is facing, was vertical integration a

good idea? Provide your reasons. What are the risks in contract

farming?

4.How to prepare for the launch of the Tasty Soy? What should be the

marketing strategy of the company?

5.What is HACCP? What are the benefits of using HACCP?

6.Tasty Soy Pieces

1. Inclusiveness (Rabobank / IFC - adapted

from Vermeulen and Cotula, 2010):

How values are shared between producers (smallholders) and

buyers (agribusiness companies).

1. Ownership: of the business (equity shares) and of key

project assets such as land and processing facilities.

2. Voice: the ability to influence key business decisions,

including weight in decision-making arrangements for review

and grievance and mechanisms for dealing with information

access.

3. Risk: including commercial risk, but also wider risk such as

political and reputational risk.

4. Reward: the sharing of economic costs and benefits,

including price-setting and finance arrangements

1. Inclusiveness - CDI

1.Create opportunities that enable small-scale farmers and their

cooperatives to become economically viable business partners

in supply chains.

2.Support small- and medium-scale enterprises to enable them

to flourish as processors and service providers along the

supply chain.

3.Provide employment opportunities in processing and service

enterprises under fair labour conditions.

4.Establish agri-hubs and clusters that help to drive overall

rural economic prosperity.

5.Deliver healthy, affordable, accessible food products and ser-

vices for low-income consumers in rural and urban areas.

2. Sourcing options for Seba

a.Source from small holders

i.Spot market

ii.Contract farming

1.Outgrower model

2.Nucleus estate model

b.Source from large scale, commercial) farms, however, this

option does not fit the business model of the involved

parties.

c.Source from farm owned by Seba Foods, which is not yet

in existence at the time of writing the case. However, this

option does not fit the model of the involved parties.

3. Risks in contract farming

Quantity

Quality

Contracts / agreements

Collection of produce

Extension support

Side selling

Access to credit

Pricing methods and payments

Risk sharing

Contract enforcement

4. Risks Seba food will face

1.Climate risks: not enough soybeans will be produced locally

2.Price volatility as already described in the case

3.Market risks: Ethiopian consumers aren’t interested in buying

TSP

4.Political risk

5.ECX

ECX

ECX consists of 55 warehouses in 17 regional locations.

It has grown from trading 138,000 ton in its first year to 508,000 tons in its third year, with nearly equal shares of coffee and oilseeds and pulses.

The value of the ECX rose 368% between 2010 and 2011 to reach US$1.1 billion.

In July 2011, its total membership equalled 243 with total clients, who trade through members, numbered about 7,800. Farmer Cooperatives represented 2.4 million smallholder farmers, which make up 12% of the membership.

Next day payment

Provides market data

Improvement points ECX, 1

Due to the fact that the minimum parcels to be traded on ECX floor are 5 tons, most (small) farmers are obliged to sell the product through middle man. That results in lower prices to the farmer. The expectations were that farmer would get higher income!

Quality grading has shown great mishaps. Many exporters and producers complain about the lack of consistency in quality. In fact many parcels in the highest category should not have been classified as such.

Due to the grading, many exporters and producers lose money as they need to adjust before use/export.

Prices on ECX are still higher than world market levels. As result, export potential is not tapped in full.

Due to introduction ECX the tracking and tracing system has gone ‘out of the window’. The Identity Preserved mechanism (as in tracking and tracing) are increasing demanded by importers in Japan/Europe and USA.

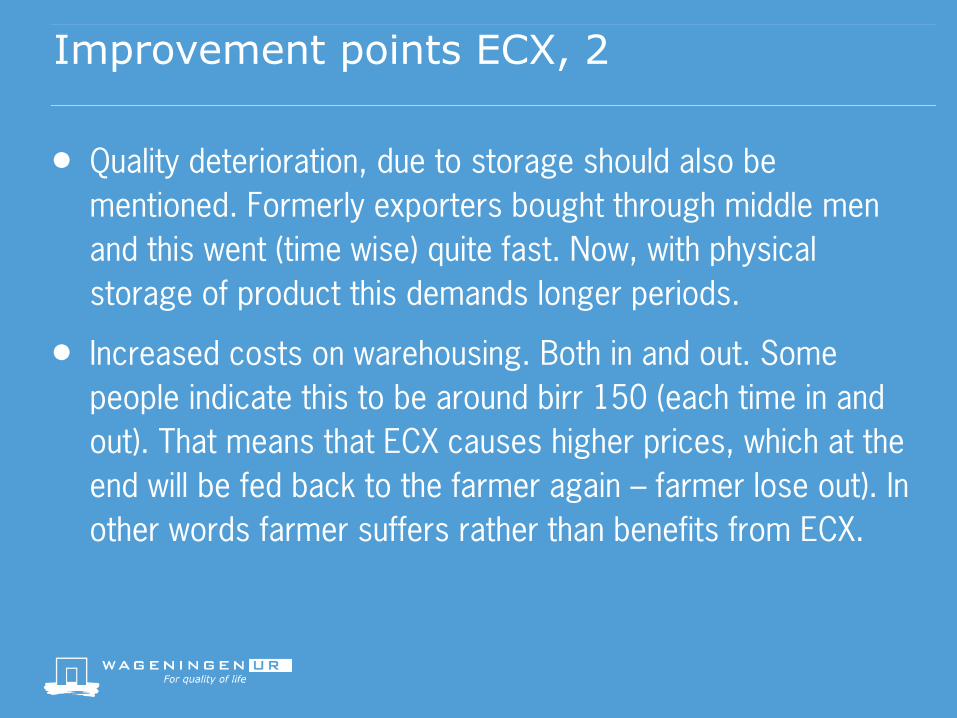

Improvement points ECX, 2

Quality deterioration, due to storage should also be

mentioned. Formerly exporters bought through middle men

and this went (time wise) quite fast. Now, with physical

storage of product this demands longer periods.

Increased costs on warehousing. Both in and out. Some

people indicate this to be around birr 150 (each time in and

out). That means that ECX causes higher prices, which at the

end will be fed back to the farmer again – farmer lose out). In

other words farmer suffers rather than benefits from ECX.

5. Competitive edge of Ethiopia

6. HACCP

Principle 1: Conduct a hazard analysis. –biological, chemical,

or physical

Principle 2: Identify critical control points. – A critical control

point (CCP) is a point, step, or procedure in a food

manufacturing process at which control can be applied and, as

a result, a food safety hazard can be prevented, eliminated, or

reduced to an acceptable level.

Principle 3: Establish critical limits for each critical control

point.

Principle 4: Establish critical control point monitoring

requirements.

Principle 5: Establish corrective actions.

6. HACCP

Principle 6: Establish procedures for ensuring the HACCP

system is working as intended.

Principle 7: Establish record keeping procedures. – The HACCP

regulation requires that all plants maintain certain documents,

including its hazard analysis and written HACCP plan, and

records documenting the monitoring of critical control points,

critical limits, verification activities, and the handling of

processing deviations

Example of a value market chain: “Las

Brisas,” Santa Cruz de Turrialba

Las Brisas, began activities over 10 years ago,

It functioned like all the other plants in the cheese-making cluster of Santa Cruz de Turrialba in Costa Rica: unstable relations with suppliers and buyers.

Change: establishment of trust-based relationships with both suppliers and buyers.

Example of a value market chain: “Las

Brisas,” Santa Cruz de Turrialba

On the milk production input market side, La Brisas made its biggest milk provider a new partner in the business, and thus guaranteed 70% of its daily consumption

On the output market side, Las Brisas pursued two market strategies.

● Biscuit factory – to produce a special cheese for manufacturing biscuits. The two businesses jointly obtained support from the University of Costa Rica for specific research on the best type of cheese for the biscuits. Through this product development process Las Brisas was able to enter a new market, in which no competition existed, as well as assisting the biscuit factory to expand production and sales.

● Important chain of supermarkets in San José, the country’s capital - application of a methodical quality control process for its own brand. This relationship has resulted in joint promotion and marketing strategies as well as the development and testing of new products based on consumer demands detected by the supermarket

What are the results has Las Brisas achieved

through its value chain strategy?

The quality of its products is recognized as being the best in the zone and, therefore, has high acceptance in the market.

Las Brisas is the only business from the cheese cluster in Santa Cruz that sells consistently directly to supermarkets in San José. In 2001, a promotion of cream was so successful that it contracted additional production with other plants of Santa Cruz, but under its supervision and brand.

Las Brisas suffers less than other businesses during times of milk shortage.

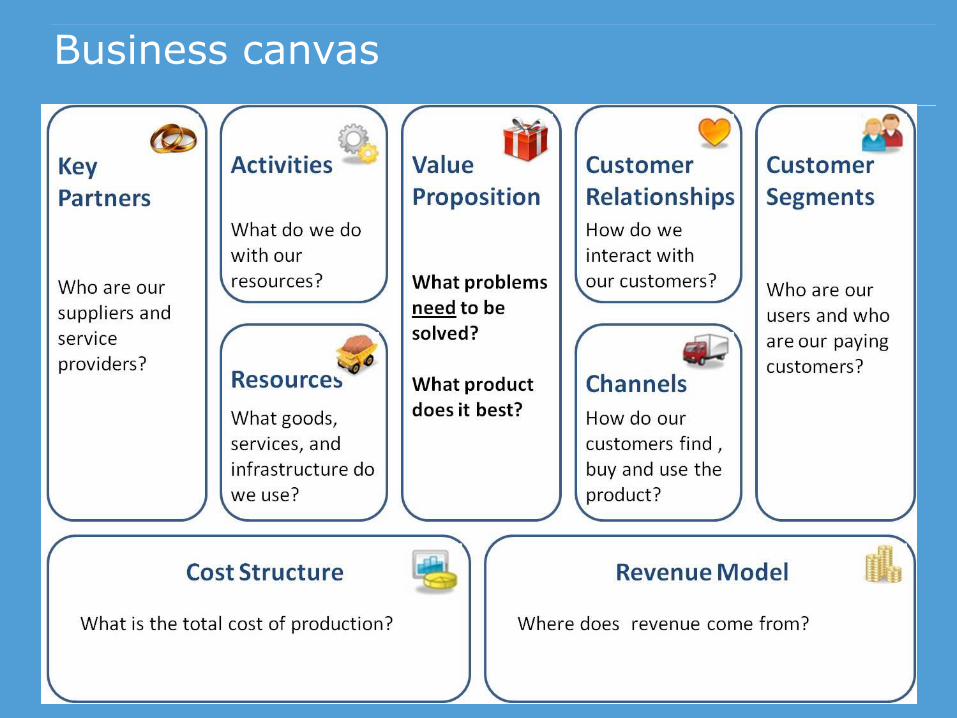

Business canvas