covers february 2014 - bizsolindia.com · bizsol update february - 2014 ... bit of communicating...

TRANSCRIPT

1

Bizsol UPDATE February - 2014

Close on the heels of Manmohan Singh holding a

Press Conference, Rahul Gandhi also did his two-

bit of communicating with the masses through a

Television interview recently. It is obvious that the GOP

has suddenly discovered that in the process of

governance there is an entity called the people who

happen to be voters in an election. The party is now

on an overdrive to reach out to them. Rahul's interview

was part of this plan. The interview turned out to be

an unmitigated disaster is another matter. Rahul had

always been an enigma - a permanent bachelor and

a reluctant politician. Both are very "un-Indian" indeed.

For all those who wanted to know what our possible

future Prime Minister stood for, the interview only

helped to deepen that mystery. Possibly, as part of a

deal, Arnab Goswami who interviewed Rahul chose

to be civil, for a change. No person with an iota of

self-respect would want to be on his show normally,

for he, with his opinionated and judgmental stance

on all issues, becomes a panellist himself forgetting

his fundamental role as a neutral anchor of a talk show.

Be that as it may, Rahul the boy came prepared for

an examination selectively learning the subjects he

knew something about only to be asked questions on

topics on which he knew nothing about, which were

many. Rahul Gandhi's interview was remarkable for

its consistency.

For every question put to him he had only one

standard answer - the one he had come prepared

with. It was almost like a child reciting poetry. If it

forgets a line it starts from the beginning. By the time

the interview ended the boy had separated himself

from the men in the adult world of politics. If you cut

out the clichés and platitudes which he mouthed

repeatedly throughout the interview, the ninety -

minute interview would have been over in just under

twenty minutes! Thank God Arnab Goswami did not

ask him questions on subjects like global warming

and family planning. Had he done that you could

almost predict Rahul's responses - a lecture on RTI

FROM THE DESK OF THE CHAIRMAN

and the systemic problems of Indian polity! The best

part of the interview was after the interview. The spin

doctors of the Congress Party were working overtime

to project Rahul through the interview as a savant (in

simple English a learned person). Ask the same

question to a BJP spokesman prompt would come

the reply - Rahul suffers from 'savant syndrome' (again

in plain language, a condition in which an intellectually

challenged person shows streaks of brilliance normally

not associated with him). For all those looking to

decipher Rahul, he turned out to be 'a riddle wrapped

in a mystery inside an enigma' to quote Winston

Churchill, the wartime Prime Minister of Britain.

A recent nationwide survey projected that the BJP is

set to do well; perhaps even better than their own

expectation. So be it. That is not the point of

discussion here. The Survey has come out with an

interesting observation. Wherever there is a strong

Chief Minister in a State the party in power (Congress,

BJP or any other) appears to have done well even

fighting anti-incumbency. In the good old days when

the Congress had such a galaxy of powerful leaders

in the States across the country the overall

performance of the Central government run by

Congress also had improved. A charismatic leader

like Jawaharlal Nehru could carry such regional

satraps in his own party as a team. Once Indira

Gandhi took over the reins and brought about her

own brand of politics there was no room for

disagreements in the party apparatus at any level.

Dissent of any kind was branded as insubordination

and sycophancy became the order of the day. For

Indira Gandhi's Congress the State Chief Ministers

were like Branch Managers of a corporate set-up run

by circulars issued from the Head Office (read High

Command). While dismissing even genuine

differences of opinions as rebellious behaviour, the

party got rid of their tall leaders and insulated

themselves from the masses so much so that today it

is so difficult to find able leaders in the Grand Old

2

Bizsol UPDATE February - 2014

Party at any level. No surprise that people like Sushil

Kumar Shinde are so much in demand. Imagine that

he is now sitting in the same chair which was once

occupied by a leader called Sardar Vallabhbhai Patel!

When Rahul Gandhi laments about his party's

disconnect with the people and a small coterie running

the affairs of the nation he has to be reminded that

this is the handiwork of his own ancestors and he

himself is the beneficiary of this unholy arrangement.

Satyapal Singh the erstwhile Commissioner of Mumbai

sprang a surprise by opting for voluntary retirement

from his post and joined politics the next day raising

certain disturbing questions. Congress is crying foul

as Singh chose to join BJP. Recently R K Singh the

former Home Secretary after retirement joined BJP

and raised a stink against his former political boss

Sushil Kumar Shinde. The former Army Chief who

had a score to settle with the Government joined the

Anna movement and is now inching closer to BJP. It

is an open secret that the bureaucrats start planning

their second innings even before they demit office.

By currying favour with the ruling establishment they

make sure that once you join the government service

you never really retire. So is the case with the

appointments post retirement for judicial officers. The

service rules only provide that an officer after

retirement cannot take up a private sector job before

completing a mandatory cooling off period of two

years which is also observed more in breach as there

is no bar in engaging their services as consultants.

Appointment as Governor of a state is another window

of opportunity to the retired bureaucrats. The recent

incident of Satyapal Singh has brought this sordid state

of affairs more into focus. This practice has to stop.

One hopes that out of sheer pique that most of these

retirees are joining the Opposition the Central

government may enact some legislation which would

bar such patently unethical practices. This could very

well be an AAP Agenda to cleanse the system.

Corruption takes many forms and this is definitely one

of them.

On a day when the whole of Andhra Pradesh should

be celebrating the achievement of one of their own

who goes by the name of Satya Nadella on being

chosen to head Microsoft as its CEO, his folks back

home are engaged in a bitter dispute over the creation

of Telengana. Manmohan Singh and his government

have gone to seed is an accepted fact and the people

of the country have also resigned to that inevitable

fact. It is, however, dangerous that even in the dying

moments the government is still trying to spawn

anarchy and lawlessness. What the congress

government is doing is to preside over a dangerous

game of permanently damaging the social fabric in

every part of the nation pitting one against the other

all in the name of politics and for electoral gains. Even

if there is merit in the creation of a new state, the

present lame duck government should not be allowed

go ahead with its plan of bifurcating Andhra Pradesh,

for the present dispensation has no credibility left to

take such an important decision involving the future

of so many people in that region. As we go to press

the government is trying to hustle the Telengana Bill

through the Parliament by hook or by crook. One hope

it doesn't succeed. By the way when we celebrate

the achievement of Satya Nadella we are also passing

an indictment on our system which forces the potential

achievers to migrate out of the country if they have to

do what they have done - be it Nobel laureates,

business tycoons or whatever. By the way again, none

of these icons who have achieved something big are

Indian citizens; they may be of Indian origin.

The flavour of the season is undoubtedly what has

now come to be known as Dharna politics. No one is

interested in the old fashioned practice of raising

people's issues in Parliament (that is, if the Parliament

were to function, in the first place). There is much

better visibility and freedom at Jantar Mantar. Kejriwal

and his Aam Aadmi Party have made it fashionable

to sit on Dharna notwithstanding the cause and effect.

In the process Dharna Dharma is being reinvented

and rewritten. As of writing this piece there is this Chief

Minister of Andhra Pradesh sitting on Dharna against

his own government in Delhi; the Telengana

protagonists on a Dharna next to him demanding

creation of a separate state; Kejriwal & Co. back again

on the ground to announce to the world that their

earlier Dharna about wanting to bust the prostitution

and drug racket have been proved right and justified,

after all. At this rate it may be advisable for the Delhi

government consider building a Dharna Complex at

Jantar Mantar on the lines of a huge Exhibition Centre.

This would generate some much needed revenue for

the state government. Proper arrangements can be

made for the Ministers and Bureaucrats to visit the

concerned stalls where causes associated with their

ministries are being agitated upon. They will save

precious time and can plan their days better. This

3

Bizsol UPDATE February - 2014

could result in better traffic management, availability

of water for water-cannons, better employment

opportunities for catering services, event

management outfits and the like. Delhi would look

better organised. Moreover, Dharna as a concept

stands self authenticated as it has been invented by

none other than the original Gandhi (may his soul

rest in peace). On a serious note one sincerely hopes

that street democracy does not lead to meting out

street justice. Amen.

From Dharna politics let us now move to Statue

politics. News has just come in that the tallest statue

in the country would be that of Shivaji Maharaj off the

coast of Mumbai. In this highly competitive atmosphere

with elections round the corner every extra inch on

the statue could mean extra votes. Never mind the

cost. Whose money is it any way? Mayawati and her

handbag were criticised equally when she built her

own statue with her handbag during her tenure as

the Chief Minister of Uttar Pradesh. When Sardar

Patel, the real 'iron man' was to be resurrected through

a statue made of iron by Narendra Modi the congress

party was quick to criticise BJP. Now a Congress Chief

Minister himself has joined the bandwagon of

competitive statue politics. Prithviraj Chavan may have

won the battle but not the war yet. Remember there

are another 27 states left who are yet to announce

their decision to join the statue politics and their

budgets. Watch this space.

The chatterati in a society consisting largely of the

middle class serves a useful purpose. They serve

themselves very well even at the expense of others.

At one point in time recently it looked as though they

had lost their voice when the government at the Centre

decided that subsidised LPG cylinders would be

limited to 6 despite their vociferous protest. They had

their day when it was revised upwards to 9 a short

while later. They scored a decisive victory when Rahul

Gandhi in his newly acquired aggressive avatar at

the recent AICC session demanded this quota be

increased to 12 and the government obliged post-

haste. In the process what was rolled back was one

of the very few sensible reform measures introduced

by this government. Subsidy on LPG is a classic case

of misdirected subsidies even according to the

Governor of the Reserve Bank of India. The economist

Prime Minister then defended the earlier decision to

limit the quota to 6 by saying that "money doesn't

grow on trees". As it is still not growing on trees, at

least in India, will the government explain the rationale

for the recent decision? "Rob Paul to pay Peter" - so

goes the saying. In this instance it is robbing the poor

to pay the not-so-poor. The story of a puppet

becoming a pied piper is complete. Will the real

Manmohan Singh please stand up?

Mani Shankar Aiyar, the Congress Party's self

appointed ideologue wants the world to see him as

an erudite and scholarly politician belonging to a

different class. He kicked up a controversy recently

by contemptuously calling Narendra Modi an ordinary

chai-walla and not worthy of his attention even. In

one stroke he gave BJP a stick to beat the congress

with and also showed himself up as an intellectually

arrogant bigot. He belongs to that class which equates

command over the English language to uncommon

common sense and even some form of extreme

wisdom. His comment was not only in bad taste but

also obnoxious. With people like him the ruling party

is increasingly looking like a zoo where all kinds

inmates are allowed thrive with total protection.

Revolutionaries across the globe justify their actions

with the rationale that end justifies the means. In a

well entrenched system running on its own inertia

looking for volunteers to make change happen is

difficult, nay, impossible. Kejriwal the Chief Minister

of Delhi was pilloried by all the arms of the established

society like the government, the media, the judiciary,

the police and what have you when he took the unusual

step of sitting on a Dharna to demand action against

the Delhi Police for dereliction of duty. In doing so

Kejriwal did not endear himself to the puritans in the

society. But these tactics suited him politically and

helped him to highlight the rot in the police system

quite effectively though perhaps not so conventionally.

No police reform has come about through

conventional means all these years till date. It is

perhaps time that someone thinks out of the box to

force the hands of those who are well entrenched in

the establishment and use the police to do their

bidding. The jury is still out on whether the means

adopted by Kejriwal would indeed be condoned if it

results in cleansing the rotten system in which we all

live.

Thank you.

Venkat R. Venkitachalam

4

Bizsol UPDATE February - 2014

CUSTOMS

NOTIFICATIONS

Tariff

• Import of specified goods from the Republic of

Korea shall attract lesser duties on most of the

products since there is further reduction in rate

of customs leviable on specified goods w.e.f 1st

January 2014. [Notification No. 54/2013-Cus

dated 31-12-2013]

• Import of Tanks and other armoured fighting

vehicle (8710) and Hydraulic Turbines, Water

Wheels and regulators, Turbo Jets, other engines

(falling under 8410 to 8412) from Japan will

attract higher duties w.e.f 1st January 2014.

[Notification No. 55/2013-Cus dated

31-12-2013]

• Import of goods from Malaysia shall attract lesser

duties on most of the products since there is

further reduction in rate of customs leviable on

goods as described in the notification w.e.f 1st

January 2014. [Notification No. 56/2013-Cus

dated 31-12-2013]

• Import of specified goods from Member States

of the Association of Southeast Asian Nations

(ASEAN) shall attract lesser duties on most of

the products since there is further reduction in

rate of customs leviable on goods as described

in the notification w.e.f 1st January 2014.

[Notification No. 57/2013-Cus dated

31-12-2013]

• Exemption from payment of whole of customs

duty, additional duty, safeguard duty and anti-

dumping duty on material imported into India

against Advance Authorization meant for export

of prohibited item, subject to certain conditions

as specified in the notification. [Notification 01/

2014-Cus Dated 17-01-2014]

• Standard rate of customs duty has been

increased from 7.5% to 10% in case of following

chapter heading nos. pertaining to edible oils:

Sr.No. Chapter Heading Description of goods

56 15079010 All goods

58 1508, 1509, 1510, 1512, All goods, refined and

1513, 1514 or 1515 edible grade

59 1511 90 All goods

63 15121910 All goods

66 1514 19 or 15 14 99 All goods, edible grade

69 1516 20 All goods, edible grade

71 1517 10 21, 1517 90 10, All goods, edible grade

1517 90 20, 1518 00 11,

1518 00 21 or 1518 00 31

[Notification No. 02/2014-Cus dated

20-01-2014]

• Standard rate of custom duty on import of "Iron

ore pellets" under chapter heading 26011210 has

been increased to 5% from nil rate of duty as

provided in Notification No. 27/2011-Cus dated

01-03-2011. [Notification No. 03/2014-Cus

Dated 27-01-2014]

• Exemption for Tunnel Boring Machine has been

revised to read as under,

Table Chapter or AddiSr.No. Heading or Description of Stand- tional Condi-

sub-heading goods ard duty tionor tariff item rate rate No.

397 84 or any The followingother Chapter goods, namely :-

(A) Tunnel boring Nil - -machines(B) Parts and Nil - -

components of(A) for using theassembly of Tunnelboring machines

[Notification No. 04/2014-Cus Dated 03-02-2014]

5

Bizsol UPDATE February - 2014

• Rate of All Industry duty drawback has been amended for goods falling under chapter headings - 3, 42,

48, 57, 60, 61, 62, 63, 73, 84, 87 & 95 with effect from 25th January 2014. Details are given separately as

below.

1. In CHAPTER - 3, for Tariff item 030602 and the entries relating thereto, the following Tariff items

and entries shall be substituted, namely :-

030602 In frozen form other than Accelerated Kg 3.3% 14.6 2.3% 10.2

030603 Accelerated Freeze Dried Kg 1.8% 38 1% 21.1

2. In CHAPTER - 42, -

a) against Tariff item 420207, for the entry in column 5, the entry "70" shall be substituted;

b) against Tariff item 420207, for the entry in column 7, the entry "15.4" shall be substituted;

c) against Tariff item 420210, for the entry in column 5, the entry "70" shall be substituted;

d) against Tariff item 420210, for the entry in column 7, the entry "15.4" shall be substituted;

e) against Tariff item 420307, for the entry in column 5, the entry "42" shall be substituted;

f) against Tariff item 420307, for the entry in column 7, the entry "14.3" shall be substituted;

3. In CHAPTER - 48,-

a) against Tariff item 4820200001, in column 2, the words "or without", shall be omitted;

b) against Tariff item 4820200001, for the entry in column 4, the entry "6.7%" shall be substituted

c) against Tariff item 4820200001, for the entry in column 5, the entry "7.2" shall be substituted;

d) against Tariff item 4820200001, for the entry in column 7, the entry "3.5" shall be substituted;

e) against Tariff item 4820200009, for the entry in column 4, the entry "6.7%" shall be substituted;

f) against Tariff item 4820200009, for the entry in column 5, the entry "7.2" shall be substituted;

g) against Tariff item 4820200009, for the entry in column 7, the entry "1.8" shall be substituted;

4. In CHAPTER - 57,-

a) against Tariff item 570206, for the entry in column 5, the entry "53.5" shall be substituted;

b) against Tariff item 570206, for the entry in column 7, the entry "28.4" shall be substituted;

c) against Tariff item 570305, for the entry in column 5, the entry "53.5" shall be substituted;

d) against Tariff item 570305, for the entry in column 7, the entry "28.4" shall be substituted;

e) against Tariff item 570505, for the entry in column 5, the entry "53.5" shall be substituted;

f) against Tariff item 570505, for the entry in column 7, the entry "28.4" shall be substituted;

5. In CHAPTER - 60,-

a) after the Tariff item 600209 and the entries relating thereto, the following Tariff items and entries

shall be inserted, namely:-

Tariff

ItemDescription of goods Unit

Drawback when

Cenvat facility has

not been availed

Drawback when

Cenvat facility has

been availed

DrawbackRate

Drawbackcap per

unit in Rs.

DrawbackRate

Drawbackcap per

unit in Rs.

6

Bizsol UPDATE February - 2014

Tariff

ItemDescription of goods Unit

Drawback when

Cenvat facility has

not been availed

Drawback when

Cenvat facility has

been availed

DrawbackRate

Drawbackcap per

unit in Rs.

DrawbackRate

Drawbackcap per

unit in Rs.

600210 Of Man Made Fibres containing 5% or more

by weight of spandex/lycra/elastane (Grey) Kg 8.30% 60 3.10% 22.4

600211 Of Man Made Fibres containing 5% or more

by weight of spandex/lycra/elastane (Grey) Kg 8.80% 72 3.10% 25.4

600212 Of Cotton containing 5% or more by weight

of spandex/lycra/elastane (Grey) Kg 5.90% 34 1.60% 9.2

600213 Of Cotton containing 5% or more by weight

of spandex/lycra/elastane (Dyed) Kg 6.40% 40 1.60% 10

600214 Of Blend containing Cotton and Man Made

Fibre where MMF predominates by weight

and containing 5% or more by weight of

spandex / lycra / elastane (Grey) Kg 7.50% 57.3 3.10% 23.7

600215 Of Blend containing Cotton and Man Made

Fibre where MMF predominates by weight

and containing 5% or more by weight of

spandex / lycra / elastane (Dyed) Kg 8% 63.9 3.10% 24.8

600216 Of Blend containing Cotton and Man Made

Fibre where Cotton predominates by weight

and containing 5% or more by weight of

spandex / lycra / elastane (Grey) Kg 5.90% 37.9 1.30% 8.3

600217 Of Blend containing Cotton and Man Made

Fibre where Cotton predominates by weight

and containing 5% or more by weight of

spandex / lycra / elastane (Dyed) Kg 6.40% 50.1 1.30% 10.2

b) after the Tariff item 600409 and the entries relating thereto, the following Tariff items and entries shall be

inserted, namely:-

Tariff

ItemDescription of goods Unit

Drawback when

Cenvat facility has

not been availed

Drawback when

Cenvat facility has

been availed

DrawbackRate

Drawbackcap per

unit in Rs.

DrawbackRate

Drawbackcap per

unit in Rs.

600410 Of Man Made Fibres containing 5% ormore by

weight ofspandex/lycra/elastane (Grey) Kg 8.3% 60 3.1% 22.4

600411 Of Man Made Fibres containing 5% or more by

weight ofspandex/lycra/elastane (Dyed) Kg 8.8% 72 3.1% 25.4

600412 Of Cotton containing 5% or more by weight of

spandex/lycra/elastane (Grey) Kg 5.9% 34 1.6% 9.2

7

Bizsol UPDATE February - 2014

Tariff

ItemDescription of goods Unit

Drawback when Cenvatfacility has

not been availed

Drawback whenCenvat facility has

been availed

DrawbackRate

Drawbackcap per

unit in Rs.

DrawbackRate

Drawbackcap per

unit in Rs.

600413 Of Cotton containing 5% or more by weight of

spandex/lycra/ elastane (Dyed) Kg 6.4% 40 1.6% 10.0

600414 Of Blend containing Cotton and ManMade

Fibre where MMF predominates by weight and

containing 5% or more by weight of spandex/

lycra/elastane (Grey) Kg 7.5% 57.3 3.1% 23.7

600415 Of Blend containing Cotton and ManMade

Fibre where MMF predominates by weight and

containing 5% or more by weight of spandex/

lycra/elastane (Dyed) Kg 8% 63.9 3.1% 24.8

600416 Of Blend containing Cotton and Man Made

Fibre where Cotton predominates by weight

and containing5% or more by weight of

spandex/lycra/elastane (Grey) Kg 5.9% 37.9 1.3% 8.3

600417 Of Blend containing Cotton and ManMade

Fibre where Cotton predominates by weight

and containing5% or more by weightofpandex/

lycra/elastane (Dyed) Kg 6.4% 50.1 1.3% 10.2";

6. In CHAPTER - 61, after the Tariff item 611608 and the entries relating thereto, the following

611609 Gloves, specially designed for use in sports Per

namely Golf Gloves made of synthetic materials piece 7.6% 35.2 1.7% 7.9

7. In CHAPTER - 62, after the Tariff item 621607 and the entries relating thereto, the following

TariffItem

Description of goods Unit

Drawback when Cenvatfacility has

not been availed

Drawback when Cenvatfacility has been

availed

DrawbackRate

Drawbackcap per

unit in Rs.

DrawbackRate

Drawbackcap per

unit in Rs.

TariffItem

Description of goods Unit

Drawback when Cenvatfacility has

not been availed

Drawback when Cenvatfacility has been

availed

DrawbackRate

Drawbackcap per

unit in Rs.

DrawbackRate

Drawbackcap per

unit in Rs.

621608 Gloves, specially designed for use insports Per

namely Golf Gloves made of synthetic Piece 7.6% 35.2 1.7% 7.9

materials

8

Bizsol UPDATE February - 2014

8. In CHAPTER - 63, for Tariff items falling under heading 6307 and the entries relating thereto, the following

Tariff items and entries shall be substituted, namely :

Tariff Description of goods Unit

Drawback when Cenvatfacility has

Drawback when Cenvatfacility has been

Drawback Drawbackcap per

Drawback Drawbackcap per

630701 Fabric Swatches Kg 7.2% 69.2 1.8% 17.3

630702 Others (excluding fabricswatches)

63070201 Of Cotton Kg 7.2% 75 1.8% 18.7

63070202 Of Blend containing Cotton and

Man Made Fibre Kg 8.2% 84 1.5% 15.4

63070203 Of Man Made Fibres Kg 9.2% 94 1.1% 11.2

63070204 Of Silk (other than containing noil silk) Kg 7.8% 414.5 4% 212.6

63070205 Of Noil Silk Kg 7.8% 129 4% 66.2

63070206 Of Wool Kg 7.2% 108 1.8% 27

63070207 Of Others Kg 7.2% 69.2 1.8% 17.3

9. In CHAPTER - 73, after Tariff item 732643 and the entries relating thereto, the following Tariff item and

the entries shall be inserted, namely:-

TariffItem

Description of goods Unit

Drawback when Cenvatfacility has

not been availed

Drawback when Cenvatfacility has been

availed

DrawbackRate

Drawbackcap per

unit in Rs.

DrawbackRate

Drawbackcap per

unit in Rs.

732644 Steel Cops/Pirn/Bobbins 1.9% 1.9%

TariffItem

Description of goods Unit

Drawback when Cenvatfacility has

not been availed

Drawback when Cenvatfacility has been

availed

DrawbackRate

Drawbackcap per

unit in Rs.

DrawbackRate

Drawbackcap per

unit in Rs.

8436 Other agricultural, horti-cultural, forestry,

poultry-keeping or bee- keeping machinery,

including germi-nation plant fitted with

echanical or thermal equipment; poultry

incubators and brooders

843601 Poultry equipment and parts thereof Kg 7.2% 10 1.7% 2.3

843699 Others 1.7% 1.7%

10. In CHAPTER - 84, for Tariff item 8436 and the entries relating thereto, the following Tariff items and

entries shall be substituted, namely :-

9

Bizsol UPDATE February - 2014

11. In CHAPTER - 87, for all the Tariff items and the entries relating thereto, the following Tariff items and

entries shall be substituted, namely :-

TariffItem

Description of goods Unit

Drawback when Cenvatfacility has

not been availed

Drawback when Cenvatfacility has been

availed

DrawbackRate

Drawbackcap per

unit in Rs.

DrawbackRate

Drawbackcap per

unit in Rs.

8701 Tractors (otherthantractors of heading 8709) 1 No. 6.5% 26000 2% 8000

8702 Motorvehiclesforthetransport

Oftenormorepersons,including the driver

870201 CommercialVehicleofGVWupto

7.5 MT in CBU/SKD/CKD Condition 2% 2%

870202 Commercial Vehicles of GVW

above7.5MTinCBU/SKD/CKD condition 2% 2%

870299 Others 2% 2%

8703 Motor cars and other motor vehicles principally

designed for the transport ofpersons (other

thanthoseofheading 8702), including station

wagons and racing cars

870301 Rear Engine Auto Rickshaw in

CKD/ SKD/ CBU condition 2% 2%

870302 Motor cars having Manual Transmission 1 No. 2.85% 25000 2.85% 25000

870303 Motor cars having Automatic Transmission 1 No. 3.67% 34000 3.67% 34000

870399 Others 2% 2%

8704 Motorvehiclesforthetransport ofgoods

870401 CommercialVehicleofGVWupto

7.5 MT in CBU/SKD/CKD Condition 2% 2%

870402 Commercial Vehicles of GVW

above7.5MTinCBU/SKD/CKD condition 2% 2%

870499 Others 2% 2%

8705 Special purpose motor vehicles, other than

those principally designed for the transport of

persons or goods (for example, break down

lorries, crane lorries, firefighting vehicles,

concrete- mixers lorries, spraying lorries,

mobile workshops, mobile radiological units)

870501 CommercialVehicleofGVWupto

7.5 MT in CBU/SKD/CKD Condition 2% 2%

870502 Commercial Vehicles of GVW

above7.5MTinCBU/SKD/CKD condition 2% 2%

1 0

Bizsol UPDATE February - 2014

TariffItem

Description of goods Unit

Drawback when Cenvatfacility has

not been availed

Drawback when Cenvatfacility has been

availed

DrawbackRate

Drawbackcap per

unit in Rs.

DrawbackRate

Drawbackcap per

unit in Rs.

870599 Others 2% 2%

8706 Chassis fitted with engines, for the motor

vehicles of headings 8701 to 8705

870601 Front EngineThree Wheeler Drive away

Chassis in CKD/ SKD/CBU condition 2% 2%

870602 Chassis,with or without cabin, for Commercial

Vehicle of GVW upto 7.5 MT in CBU/SKD/CKD

Condition 2% 2%

870603 Chassis,with or withoutcabin, for Commercial

Vehiclesof GVW above 7.5MTinCBU/SKD/CKD

condition 2% 2%

870699 Others 2% 2%

8707 Bodies (including cabs), for the motor vehicles

of headings 8701 to 8705 2% 2%

8708 Parts and accessories of the motor vehicles of

headings 8701 to 8705

870801 Nozzles Kg 7.2% 17.0 2% 4.7

870802 Piston Pin/ GudgeonPin Kg 7.2% 17.0 2% 4.7

870803 Steel Anchor Pin Kg 7.2% 17.0 2% 4.7

870804 BB Axle Kg 7.2% 17.0 2% 4.7

870805 Brake shoe plate Kg 7.2% 17.0 2% 4.7

870806 Chain Cover Hinges Shakle Plates

Made of CRCA Sheet Kg 7.2% 17.0 2% 4.7

870807 ConnectingRods Kg 7.2% 17.0 2% 4.7

870808 Crank for chain wheel Kg 7.2% 17.0 2% 4.7

870809 FrontAxlebeam/I-Beam, made of Alloysteel Kg 7.2% 17.0 3% 7.1

870810 Front Axle beam/I-Beam, made of

non-alloy steel Kg 7.2% 17.0 2% 4.7

8708011 FullTensionSleeve Kg 7.2% 17.0 2% 4.7

8708012 Spokes (Galvanised) Kg 7.2% 17.0 2% 4.7

8708013 Machined trailor ball/ hitch pin/Linkage pin Kg 7.2% 17.0 2% 4.7

8708014 Push rod Kg 7.2% 17.0 2% 4.7

1 1

Bizsol UPDATE February - 2014

8708015 RadiatorCap Kg 7.2% 17.0 2% 4.7

8708016 SleeveShaftandBallJoint Kg 7.2% 17.0 2% 4.7

8708017 Slip StubShaft Kg 7.2% 17.0 2% 4.7

8708018 Spindles Kg 7.2% 17.0 2% 4.7

8708019 Sprocket with central axle Kg 7.2% 17.0 2% 4.7

8708020 V-BeltCoverBcP Kg 7.2% 17.0 2% 4.7

8708021 Valve Tappets Kg 7.2% 17.0 2% 4.7

8708022 Automotive Radiator Core of Copper/Brass

construction Kg 7.2% 49.5 2% 13.7

8708023 Automotive Radiator assembly with radiator

core of Copper/ Brassconstruction Kg 7.2% 49.5 2% 13.7

8708024 Automotive Radiator assembly with radiator

core of Steel/Brass construction Kg 7.2% 34.0 2% 9.4

8708025 Roller for auto break shoe Kg 7.2% 17.0 2% 4.7

8708026 SplineHubforClutchPlates Kg 7.2% 17.0 2% 4.7

8708027 Front/rear axle shaft Kg 7.2% 17.0 2% 4.7

8708028 Auto Parts Double Brake Chamber

Type 24 L/S Kg 7.2% 17.0 2% 4.7

8708029 Auto Parts Brake Chamber Type 16L/S Kg 7.2% 17.0 2% 4.7

8708030 Auto Parts Brake Chamber Type 20L/S Kg 7.2% 17.0 2% 4.7

8708031 Auto Parts Brake Chamber Type 24L/S Kg 7.2% 17.0 2% 4.7

8708032 Auto Parts Brake Chamber Type 30L/S Kg 7.2% 17.0 2% 4.7

8708033 Auto Parts Brake Chamber Type 30 S/S Kg 7.2% 17.0 2% 4.7

8708034 Steering Knuckle Kg 7.2% 17.0 2% 4.7

8708035 TractorParts-Top Link Assembly and

Parts thereof Kg 7.2% 17.0 2% 4.7

8708036 Tractor Parts-Stabilizer Assembly/Chain

Assembly and Parts thereof Kg 7.2% 17.0 2% 4.7

8708037 Tractor Parts- Lift Arm/Lower

Link and Parts thereof Kg 7.2% 17.0 2% 4.7

8708038 Tractor Parts-Draw Bar Kg 7.2% 17.0 2% 4.7

TariffItem

Description of goods Unit

Drawback when Cenvatfacility has

not been availed

Drawback when Cenvatfacility has been

availed

DrawbackRate

Drawbackcap per

unit in Rs.

DrawbackRate

Drawbackcap per

unit in Rs.

1 2

Bizsol UPDATE February - 2014

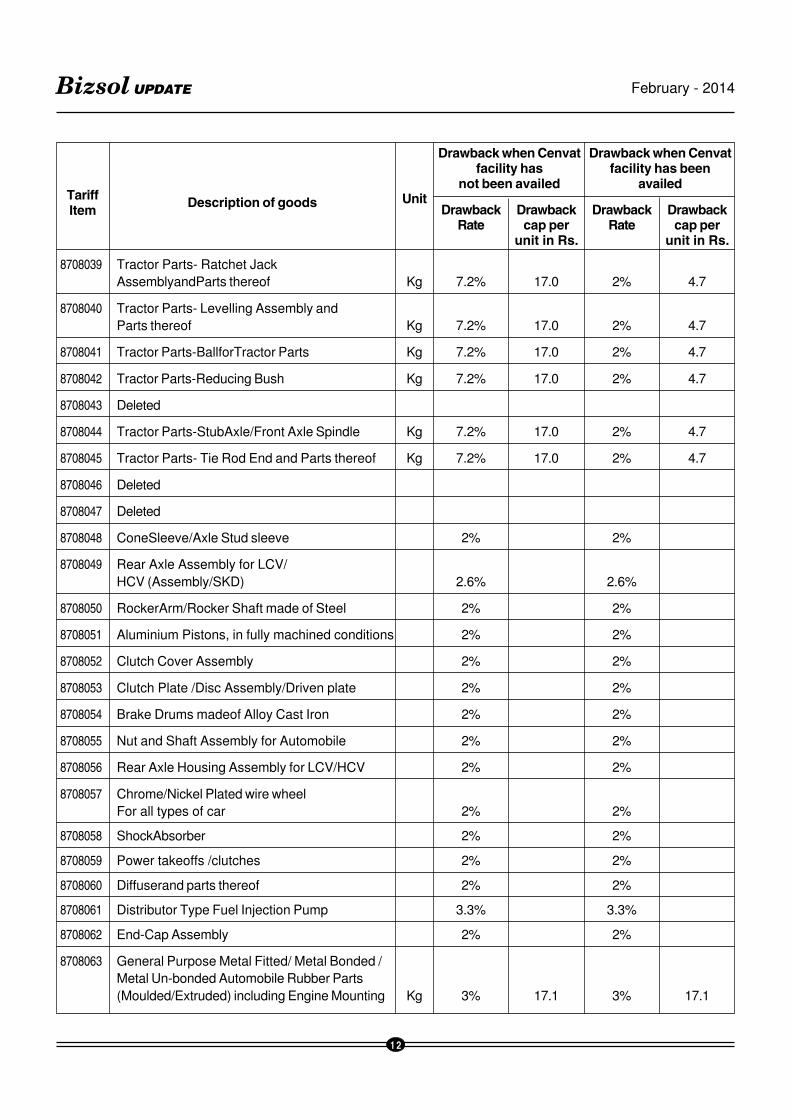

8708039 Tractor Parts- Ratchet Jack

AssemblyandParts thereof Kg 7.2% 17.0 2% 4.7

8708040 Tractor Parts- Levelling Assembly and

Parts thereof Kg 7.2% 17.0 2% 4.7

8708041 Tractor Parts-BallforTractor Parts Kg 7.2% 17.0 2% 4.7

8708042 Tractor Parts-Reducing Bush Kg 7.2% 17.0 2% 4.7

8708043 Deleted

8708044 Tractor Parts-StubAxle/Front Axle Spindle Kg 7.2% 17.0 2% 4.7

8708045 Tractor Parts- Tie Rod End and Parts thereof Kg 7.2% 17.0 2% 4.7

8708046 Deleted

8708047 Deleted

8708048 ConeSleeve/Axle Stud sleeve 2% 2%

8708049 Rear Axle Assembly for LCV/

HCV (Assembly/SKD) 2.6% 2.6%

8708050 RockerArm/Rocker Shaft made of Steel 2% 2%

8708051 Aluminium Pistons, in fully machined conditions 2% 2%

8708052 Clutch Cover Assembly 2% 2%

8708053 Clutch Plate /Disc Assembly/Driven plate 2% 2%

8708054 Brake Drums madeof Alloy Cast Iron 2% 2%

8708055 Nut and Shaft Assembly for Automobile 2% 2%

8708056 Rear Axle Housing Assembly for LCV/HCV 2% 2%

8708057 Chrome/Nickel Plated wire wheel

For all types of car 2% 2%

8708058 ShockAbsorber 2% 2%

8708059 Power takeoffs /clutches 2% 2%

8708060 Diffuserand parts thereof 2% 2%

8708061 Distributor Type Fuel Injection Pump 3.3% 3.3%

8708062 End-Cap Assembly 2% 2%

8708063 General Purpose Metal Fitted/ Metal Bonded /

Metal Un-bonded Automobile Rubber Parts

(Moulded/Extruded) including Engine Mounting Kg 3% 17.1 3% 17.1

TariffItem

Description of goods Unit

Drawback when Cenvatfacility has

not been availed

Drawback when Cenvatfacility has been

availed

DrawbackRate

Drawbackcap per

unit in Rs.

DrawbackRate

Drawbackcap per

unit in Rs.

1 3

Bizsol UPDATE February - 2014

8708064 Identifiable ready touse machined Parts/

components made whollyor predominantly of

iron / carbon steel /Non Alloy Steel/Alloy steel

(other than StainlessSteel) (not less than 90%

by weight) manufactured through casting

process, not else where specified. 2% 2%

8708065 Identifiable ready touse machined Parts/

components madewhollyor predominantly of

Stainless Steel (not less than 90% by weight)

manufactured through casting process, not else

where specified. Kg 2.6% 6.2 2.6% 6.2

8708066 Identifiable ready touse machined parts/

components made whollyor predominantly of

carbon steel / Non Alloy Steel/ (not less than

90% by weight) manufactured through forging

process, not else where specified. 2% 2%

8708067 Identifiable ready touse machined parts/

components made wholly or predominantly of

Alloy Steel (not less than 90% by weight)

manufactured through Forging process, not else

where specified Kg 3% 6.5 3% 6.5

8708068 Identifiable ready touse machined parts /

components made wholly or predominantly of

Stainless Steel (not less than 90% by weight)

manufactured through Forging process, not

else wheres pecified Kg 3% 14.4 3% 14.4

8708069 Cast articles including parts/components of

Aluminium, not else where specified 2% 2%

8708070 Alloy Steel Forgings (Machined) Kg 3% 6.5 3% 6.5

8708099 Others 2% 2%

8709 Works trucks, self-propelled, not fitted with

lifting or handling equipment, of the type used

infactories, warehouses, dockareas or airports

for short distance transport of goods; tractors

of the type usedon railway station platforms;

parts of the foregoing vehicles 2% 2%

87100000 Tanks and other armoured fighting vehicles,

motorized, whether or notfitted with weapons,

and parts of such vehicles Nil Nil

TariffItem

Description of goods Unit

Drawback when Cenvatfacility has

not been availed

Drawback when Cenvatfacility has been

availed

DrawbackRate

Drawbackcap per

unit in Rs.

DrawbackRate

Drawbackcap per

unit in Rs.

1 4

Bizsol UPDATE February - 2014

871102 Automotive Steel Wheel Rims14"- 16"

(Excluding Wire Wheels) Kg 7.2% 14.2 2% 3.9

871103 Scooter (in CKD/SKD/CBU condition) 2% 2%

871104 Motor Cycle (inCKD/SKD/CBU condition) 2% 2%

871105 Moped (in CKD/SKD/CBU condition) 2% 2%

871199 Others 2% 2%

8712 Bicycles and other cycles (including delivery

tricycles), not motorized

871201 Complete Bicycle singlespeed 1 No. 11.7% 439.5 2% 75.1

871202 Complete Bicycle having multi- Speed

chain wheel and crank with multi-speed

freewheel 1 No. 13.3% 608 4.3% 196.6

871203 Multi-speed complete bicycle with geared hubs 1 No. 13.3% 608 4.3% 196.6

871299 Others 2% 2%

8713 Carriages for disabled persons, whether or not

motorised or otherwise mechanically propelled 2% 2%

8714 Partsandaccessoriesofvehicles of headings

8711 to 8713

871401 BB axle 100 11.4% 351 2% 61.6

Pcs

871402 BBCup set of 3 1 Set 11% 2.7 2% 0.5

871403 Deleted

871404 Brakeset 1 Set 11.4% 10.9 2% 1.9

871405 Chain 100 11% 661 2% 120.2

Pcs

871406 Chain Adjuster Per 11% 0.5 2% 0.1

pair

871407 Single speed Chain wheel and Crank

(Crank madeof steel) 1 Set 11% 17.3 2% 3.1

871408 Cotter pin-Set of 2 1 Set 11% 0.6 2% 0.1

871409 FramemadeofsteelwithoutB.B. cup and axle Per 8% 53 2% 13.2

piece

871410 Fork 100 11.4% 1658.7 2% 291

Pcs.

TariffItem

Description of goods Unit

Drawback when Cenvatfacility has

not been availed

Drawback when Cenvatfacility has been

availed

DrawbackRate

Drawbackcap per

unit in Rs.

DrawbackRate

Drawbackcap per

unit in Rs.

1 5

Bizsol UPDATE February - 2014

871411 ForkFitting 1 Set 10.5% 3.8 2% 0.7

871412 Freewheel single speed 100 10.5% 472.5 2% 90

Pcs.

871413 Handle bar madeof steel 1 Set 10.5% 23.7 2% 4.5

871414 Handle stem madeof steel 100 11.4% 345 2% 60.5

Pcs.

871415 Hub (front orrear)madeofsteel 100 10.5% 672 2% 128

Pcs.

871416 Lamp bracket 100 11.4% 135.7 2% 23.8

Pcs.

871417 Mudguard (pair) Per 11.4% 22.4 2% 3.9

Pcs.

871418 Pedal (pair) Per 11.4% 8.2 2% 1.4

Pcs.

871419 Rim(pair)madeof steel Per 11.4% 37.2 2% 6.5

Pcs.

871420 Saddle 100 11.4% 2297 2% 403

Pcs

871421 Seat Pillar 100 11.4% 169.8 2% 29.8

Pcs

871422 Spokes set of144 pieces 1 Set 11.4% 13.7 2% 2.4

871423 Single speed Chain wheel and Crank

(Crank made of aluminium) Kg 10% 25.8 2% 5.1

871424 Cranks madeout of aluminium Kg 10% 45 2% 9

871425 Triplechainwheelandcrank set 1 Set 10% 29.1 2% 5.8

871426 Handle Bar Switch Per 10% 29.1 3% 8.7

piece

871427 Half Collets for engine valves Per 10% 6.8 2% 1.3

piece

871428 Industrial Roller Chain/Motor cycles including

Moped Chain/Automotive Timing Chains

(all types includings pares) Kg 10% 25.8 2% 5.1

871429 Chain wheel Per

piece 10% 51.6 2% 10.3

TariffItem

Description of goods Unit

Drawback when Cenvatfacility has

not been availed

Drawback when Cenvatfacility has been

availed

DrawbackRate

Drawbackcap per

unit in Rs.

DrawbackRate

Drawbackcap per

unit in Rs.

1 6

Bizsol UPDATE February - 2014

871430 Multispeed freewheel Per

piece 10% 34.3 2% 6.8

871499 Others Kg 10% 17.1 2% 3.4

8715 Baby carriages and parts thereof Kg 7.2% 14.2 2% 3.9

8716 Trailers and semi-trailers; other vehicles,

not mechanically propelled; parts thereof

871601 Truck and Trailer Wheels Kg 7.2% 14.2 2% 3.9

871602 Earth Moving Wheel Components, namely,

Bead Seat Ring, Gutter Band Fixed Flange

and Lock Ring Kg 7.2% 14.2 2% 3.9

871603 Others 2% 2%

TariffItem

Description of goods Unit

Drawback when Cenvatfacility has

not been availed

Drawback when Cenvatfacility has been

availed

DrawbackRate

Drawbackcap per

unit in Rs.

DrawbackRate

Drawbackcap per

unit in Rs.

12. In CHAPTER - 95,-

a) against Tariff item 950304, in column 3, the

entry "Kg" shall be inserted;

b) against Tariff item 950304, for the entry in

column 4, the entry "4.7%" shall be

substituted;

c) against Tariff item 950304, in column 5, the

entry "26.9" shall be inserted;

d) against Tariff item 950304, in column 7, the

entry "9.7" shall be inserted;

e) against Tariff item 950305, in column 3, the

entry "Kg" shall be inserted;

f) against Tariff item 950305, for the entry in

column 4, the entry "4.7%" shall be

substituted;

g) against Tariff item 950305, in column 5, the

entry "26.9" shall be inserted;

h) against Tariff item 950305, in column 7, the

entry "9.7" shall be inserted;

i) against Tariff item 95069962, for the entry

in column 3, the entry "set" shall be

substituted;

j) against Tariff item 95069962, for the entry

in column 4, the entry "7.2%" shall

besubstituted;

k) against Tariff item 95069962, for the entry

in column 5, the entry "470" shall be

substituted;

l) against Tariff item 95069962, for the entry

in column 7, the entry "111" shall be

substituted;

[Notification No. 05/2014-Cus (N.T) Dated 21-

01-2014]

• Prohibition for import of goods from Bhutan will

not be applicable in case of import of machinery

and equipment, which were exported to Bhutan

from countries other than India through an Indian

place of entry subject to condition notified.

[Notification No. 07/2014-Cus (N.T) Dated 28-

01-2014]

• Tariff value of following items has been revised:

Sr. Chapter / heading / Description Tariff value US $No. sub-heading / of goods (Per Metric

tariff item Tonne)

1 1511 10 00 Crude Palm Oil 857

2 1511 90 10 RBD Palm Oil 880

3 1511 90 90 Others - Palm Oil 869

4 1511 10 00 Crude Palmolein 896

5 1511 90 20 RBD Palmolein 899

6 1511 90 90 Others - Palmolein 898

1 7

Bizsol UPDATE February - 2014

7 1507 10 00 Crude Soyabean Oil 917

8 7404 00 22 Brass Scrap 3959

(all grades)

9 1207 91 00 Poppy seeds 3195

10 71 or 98 Gold, in any form, in 404 per 10respect of which the gramsbenefit of entries atserial number 321and 323 of the Notifi-cation No. 12/2012-Customs dated17.03.2012 is availed

11 71 or 98 Silver, in any form, in 635 perrespect of which the kilogrambenefit of entries atserial number 322and 324 of the Notifi-cation No. 12/2012-Customs dated

17.03.2012 is availed

12 080280 Areca nuts 1816"

[Notification No. 08/2014-Cus (N.T) Dated

31-01-2014]

Safeguards

No new notifications!!

Anti Dumping Duty

• Name of producer/exporter "Grodno

Khimvolokno" has been substituted by "JSC

Grodno Azot" for anti-dumping duties on import

of Nylon Tyre Cord Fabric Notification No. 121/

2009-Cus dated 30-10-2009, against serial no.

1 & 2. [Notification No. 01/2014-Cus (ADD)

Dated 03-01-2014]

• Anti-dumping duty on imports of Compact

Fluorescent Lamps originating in or exported

from China PR was imposed vide Notification No.

55/2009-Cus dated 26-05-2009 without any time

limit. Explanation has been added to the above

said notification as - anti-dumping duty imposed

against serial nos. 1 to 28 shall remain in force

up to and inclusive of the 20-11-2014.

[Notification No. 02/2014-Cus (ADD) Dated

03-01-2014]

• Anti-dumping duty on Caustic Soda, falling under

Chapter 28, originating in, or exported from

People's Republic of China, imposed vide

Notification No. 137/2008-Cus dated 26-12-2008

valid till date 25-12-2013 has been further

extended by 1 year to date 25-12-2014.

[Notification No. 03/2014-Cus (ADD) Dated

16-01-2014]

• Anti-dumping duty on Caustic Soda, falling under

Chapter 28, originating in, or exported from

Korea RP, imposed vide Notification No. 95/

2011-Cus dated 03-11-2011 valid till date 25-

12-2013 has been further extended by 1 year to

date 25-12-2014. [Notification No. 04/2014-

Cus (ADD) Dated 16-01-2014]

• Anti-dumping duty on imports of Nonyl Phenol

(falling 29071300) originating in or exported from

Chinese Taipei, imposed vide Notification No. 94/

2007-Cus dated 22-08-2007 valid till date 21-

08-2013 has been imposed further for another

5 years from the date of publication of this

notification in the Official Gazette. [Notification

No. 05/2014-Cus (ADD) Dated 16-01-2014]

• Anti-dumping duty on Acrylonitrile Butadiene

Rubber, originating in, or exported from Korea

RP, imposed vide Notification No. 01/2009-Cus

dated 02-01-2009 valid till date 01-01-2014 has

been further extended by 1 year to date 01-01-

2015. [Notification No. 06/2014-Cus (ADD)

Dated 23-01-2014]

• Anti-dumping duty on imports of Float Glass of

thickness 2 mm to 12 mm (both inclusive) of clear

as well as tinted variety (other than green glass)

but not including reflective glass, processed glass

meant for decorative, industrial or automotive

purposes falling under heading 7005, originating

in, or exported from, China PR and Indonesia

imposed vide Notification No. 04/2009-Cus dated

06-01-2009 valid till date 05-01-2014 has been

further extended by 1 year till date 05-01-2015.

[Notification No. 07/2014-Cus (ADD) Dated

23-01-2014]

• Anti-dumping duty on imports of Hexamine falling

under tariff item 2921/2910, originating in or

exported from the Saudi Arabia and Russia,

imposedvide Notification No. 89/2007-Cus dated

25-07-2007 valid till date 24-07-2013 has been

imposed further for another 5 years from the date

1 8

Bizsol UPDATE February - 2014

of publication of this notification in the Official

Gazette. [Notification No. 08/2014-Cus (ADD)

Dated 23-01-2014]

• Anti-dumping duty has been imposed on imports

of Diamino Stilbene , Disulphonic Acid (DASDA)

falling under Chapter 29, originating in, or

exported from the People's Republic of Chinafor

a period of 5 Years from the date of publication

of this notification in the Official Gazette.

[Notification No. 09/2014-Cus (ADD) Dated

23-01-2014]

• Anti-dumping duty on imports of Phosphoric Acid

- Technical Grade and Food Grade(including

Industrial Grade), falling under Sub-heading

280920 originating in, or exported from People's

Republic of China, imposed vide Notification No.

17/2008-Cus dated 19-02-2008 has been

imposed further for another 5 years from the date

of publication of this notification in the Official

Gazette. [Notification No. 33/2013-Cus (ADD)

Dated 31-12-2013]

• Anti-dumping duty on imports of Recordable

Digital Versatile Disc (DVD) of all kinds originating

in or exported from Vietnam, imposed vide

Notification No. 98/2010-Cus dated 28-09-2010

has been amended to modify the quantum of

anti-dumping duty. [Notification No. 34/2013-

Cus (ADD) Dated 31-12-2013]

CENTRAL EXCISE

Notifications

Tariff

• The excise duties on Pan Masala and Pan

Masala containing tobacco classified under 2106

90 20 and 2403 99 90 has been increased in the

range of 5% to 8% in case of Pan Masala and

around 28% in case of Pan Masala containing

tobacco. Accordingly apportionment of total

excise duties into Central Excise duties, National

Calamity Contingent duties, ED Cess and SHE

cess has also been changed. [Notification no.

01/2014-CE dated the 24/01/2014]

• The excise duties on Chewing tobacco classified

under tariff item 2403 99 10, unmanufactured

tobacco classified under Heading 2401 and

Jarda scented tobacco classified under 2403 99

30, notified under section 3A is being enhanced.

[Notification No.02/2014-CE dated the 24/01/

2014]

Non-Tariff

• Cenvat Credit Rules has been amended w.r.t.

remission of duties on finished goods. Now

Cenvat Credit availed on input and input services

also will be required to be reversed. However

the procedure to identify the input services is not

been specified in the rules, this will lead to

confusion. Moreover, there will be a conflict of

Cenvat Credit reversal required under sub rule

3(A) of Rule 6 of Cenvat Credit Rules 2004 vis-

à-vis reversal of cenvat on input service required

for remission. The formula of how to arrive

reversal of input services has not been defined

and therefore there will be always disputes and

permission of remission may be denied.

[Notification No. 01/2014 - Central Excise

(N.T.) dated 08/01/2014]

• Confusion created by audit team w.r.t. date of

payment of duty for removal of input as such and

capital goods after use has been clarified and

the same has been aligned with payment of duty

on finished goods i.e. on or before 5th of the

following month except for the month of March

which is on 31st March [Notification No. 01/

2014 - Central Excise (N.T.) dated 08/01/2014]

• Recovery provision of Cenvat Credit in

accordance with Rule 14 of Cenvat Credit Rules

2004 has been extended to recovery / reversal

of duties in case of remission of the duties under

Rule 21 of Central Excise Rules, 2004.

[Notification No. 01/2014 - Central Excise

(N.T.) dated 08/01/2014]

• Omission of inclusion of notification 1/2010 has

been corrected so as to include the said

notification in the Rule 12 of CCR Rules 2004,

which grants special dispersion to inputs

manufactured in factories located in specified

areas like north east region, Kutch district of

Gujarat, J&K & Sikkim. Now Cenvat credit of

duties paid input and capital goods will be allowed

even in case such goods are manufactured by a

Unit located in Jammu & Kashmir and claiming

1 9

Bizsol UPDATE February - 2014

exemption under notification 1/2010-CE.

[Notification No. 02/2014 - Central Excise

(N.T.) dated

20/01/2014]

• Deemed number of pouches per operating

packing machine per month has also been

revised to higher side under Pan Masala packing

machine (capacity determination and collection

of duty) Rules 2008. The form for submission of

return has been revised in line with

apportionment of excise duties as mentioned in

tariff notification. [Notification No. 03/2014 -

Central Excise (N.T.) dated 24/01/2014]

• Deemed Capacity of production per packing

machine per month for chewing tobacco

(including Filter Khaini) ,unmanufactured tobacco

and Jarda scented tobacco (number of pouches)

has been revised on higher side under Chewing

Tobacco & Unmanufactured tobacco packing

machine (capacity determination and collection

of duty) Rules 2010. [Notification No. 04/2014

- Central Excise (N.T.) dated 24/01/2014]

Circular

• Education Cess and the Secondary and Higher

Education Cess are not to be calculated on

cesses which are levied under Acts administered

by Department/Ministries other than Ministry of

Finance (Department of Revenue) but are only

collected by the Department of Revenue in terms

of those Acts. Necessary instruction has been

issued to departmental officer to clear all pending

assessment may be finalized accordingly.

[Circular No. 978/02/2014-CX dated

07/01/2014]

• Guidelines have been issued to Departmental

Officer while applying the Supreme Court

Judgement in case of Fiat India. Some of the

guidelines are as under,

a) No general inference should be taken from

the judgement that duties will arise in case

the manufacturer has sold goods at a price

lower than manufacturing cost. Hon'ble

Supreme Court has cited two instances

where a manufacturer may sell goods at a

price lower than the cost of manufacture and

profit when the company wants to switch

over its business or where a manufacturer

has goods which could not be sold within a

reasonable time. The Hon'ble Court has

further held that these examples are not

exhaustive. Therefore, mere sale of goods

below the manufacturing cost and profit

cannot be taken as the sole basis for

rejecting the transaction value.

b) Calculations of manufacturing cost may be

carried out using CAS-4 standards.

Information submitted by the manufacturer,

duly certified by a Chartered or Cost

Accountant should normally be accepted.

Only where a decision to investigate a case

has been taken at the level of the

Commissioner and it is considered

necessary in the interest of investigation,

steps such as ordering Cost Audit of the Unit

or summoning of the Costing data should

be undertaken.

c) Aspects such as the percentage of loss at

which sale has taken place , the period for

which such loss making price has prevailed,

reasons for sale at such loss making price,

whether such sales are contrary to the

standard and accepted business practices,

and whether such sale is leading to erosion

of capital of the company, may be looked

into. In addition, due care may be taken at

the level of the Commissioner to see

whether the case at hand is similar to the

facts and circumstances of the FIAT case.

d) For the period prior to the date of the

judgment, in cases where a show cause

notice has been issued on the grounds of

the FIAT judgment alone, there may not be

a case for invoking the extended period of

limitation. In such cases, only the normal

period of limitation will apply.

e) For the period after the date of the

judgment, i.e. from 29- 8-2012 onwards, if

there is a sale in the circumstances similar

to the case of M/s FIAT and yet transaction

value of goods is declared as the correct

assessable value, then such declaration

would amount to wilful misstatement of the

2 0

Bizsol UPDATE February - 2014

assessable value and accordingly extended

period will be applicable.

[Circular No. 979/03/2014-CX dated 15/1/2014]

• It has been clarified that the duties on Pan

Masala is determined based on deemed

production with respect to the number of

operating packing machines in the factory during

the month and the Retail Sale Price printed on

the pouches and not on the basis of actual

production by a unit. Therefore duty cannot be

re-determined on the basis of the speed of the

packing machine and actual production thereof,

which may be higher / lower than the deemed

production [Circular No. 980/04/2014-CX dated

24/01/2014]

Instructions

• No new instructions

SERVICE TAX

Notifications• Service tax exemption has been granted to

services by way of sponsorship of sporting events

organised by a national sports federation, or its

affiliated federations, where the participating

teams or individuals represent country. Earlier

this exemption was restricted to "district, State

or zone". [Notification No. 1/2014-ST Dated

10-01-2014]

• The definition of Government Authority has been

redrafted. Earlier in order to be fit into the

government authority, the authority needs to

satisfy both the conditions i.e. set-up by act of

the Parliament or a State Legislature and to be

established by Government. Now the new

definition states that the authority can be either

set-up by act of the Parliament / State Legislature

or established by Government. [Notification No.

2/2014-ST Dated 30-01-2014]

• Service providers providing services to the

member of a recognized association or a

registered association, in relation to a forward

contract will not be required to pay service tax

for the services rendered for the period 10-Sep.

2004 to 30-Jun. 2012. This is in accordance with

the practice prevalent during the said period and

power of the Government under Sec 11C Central

Excise Act, 1934. [Notification No. 3/2014-ST

Dated 3-02-2014]

Circulars:

• Following clarification have been issued in

case services provided by a Resident Welfare

Sr.No.

Doubt Clarification

1 (i) In a residential complex,

monthly contribution collected

from members is used by the

RWA for the purpose of mak-

ing payments to the third par-

ties, in respect of commonly

used services or goods [Ex-

ample: for providing security

service for the residential com-

plex, maintenance or upkeep

of common area and common

facilities like lift, water sump,

health and fitness centre, swim-

ming pool, payment of electric-

ity Bill for the common area

and lift, etc.]. Is service tax levi-

able?

(ii) If the contribution of a mem-

ber/s of a RWA exceeds five

thousand rupees per month,

how should the service tax li-

ability be calculated?

Exemption at Sl. No. 28 (c) in

notification No. 25/2012-ST is

provided specifically with ref-

erence to service provided by

an unincorporated body or a

non-profit entity registered

under any law for the time be-

ing in force such as RWAs, to

its own members.

However, a monetary ceiling

has been prescribed for this

exemption, calculated in the

form of five thousand rupees

per month per member con-

tribution to the RWA, for sourc-

ing of goods or services from

third person for the common

use of its members.

If per month per member con-

tribution of any or some mem-

bers of a RWA exceeds five

thousand rupees, the entire

contribution of such members

whose per month contribution

exceeds five thousand rupees

would be ineligible for the ex-

emption under the said notifi-

cation. Service tax would then

be leviable on the aggregate

amount of monthly contribution

of such members.

2 (i) Is threshold exemption un-

der notification No. 33/2012-

ST available to RWA?

(ii) Does 'aggregate value' for

the purpose of threshold ex-

emption, include the value of

exempt service?

Threshold exemption available

under notification No. 33/2012-

ST is applicable to a RWA,

subject to conditions prescribed

in the notification. Under this

notification, taxable services of

aggregate value not exceed

2 1

Bizsol UPDATE February - 2014

Association (RWA) to its own members:

• Clarification regarding issue of Discharge

Certificate under VCES and availment of

CENVAT credit thereof:As per Section 108 (2)

of the Finance Act, 2013, a declaration made

under Section 107 (1) shall become conclusive

only upon issuance of acknowledgement of

discharge under Section 107 (7). Thus Cenvat

credit can be availed only after payment of tax

dues in full and receipt of Acknowledgement of

Discharge in form VCES-3. [Circular 176/02/

2014-ST Dated 20-01-2014]

FOREIGN TRADE POLICY

Notifications• Export of commodities like cotton, jute, cotton

yarn and other commodities subject to obtaining

of registration certificate from respective Export

Promotion Council. The procedure of obtaining

Registration Certificate has been relaxed and

submission of hard copies has been dispensed

with and only online application needs to be done.

[Notification No. 63 (RE - 2013)/2009-2014

dated 03/01/2014]

• SHIS, SFIS and AIIS scrip's cannot be used for

payment of Custom duty for shortfall in EO in

Advance Authorisation or DFIA (i.e. default in EO

for authorisation issued under Chapter 4 of

Foreign Trade Policy. This is in line with policy

for utilisation of this scrip's which allows only

import of capital goods against these scrip's. In

other words scrip's cannot be utilised for payment

of duties in case of defaults / shortfall in export

obligation, except for EPCG. However scrip's can

be utilised for payment of composition fees.

[Notification No. 64 (RE - 2013)/2009-2014

dated 06/01/2014]

• An earlier condition has been relaxed for import

of customised cars and motor cars and parts

thereof required for race events. [Notification

No. 65 (RE - 2013) / 2009-2014 dated 8/1/2014]

• Export of Cotton Yarn is made eligible for benefits

under Incremental Export Incentivisation

Scheme for the entire financial year 2013-14.

[Notification No. 66 (RE - 2013)/2009-2014

dated 23/01/2014]

Sr.No.

Doubt Clarification

ing ten lakh rupees in any fi-nancial year is exempted fromservice tax. As per the defini-tion of 'aggregate value' pro-vided in Explanation B of thenotification, aggregate valuedoes not include the value ofservices which are exemptfrom service tax.

3 In Rule 5(2) of the Service Tax(Determination of Value) Rules,2006, it is provided that expen-diture or costs incurred by aservice provider as a pureagent of the recipient of ser-vice shall be excluded from thevalue of taxable service, sub-ject to the conditions specifiedin the Rule.

For illustration, where the pay-ment for an electricity bill raisedby an electricity transmissionor distribution utility in the nameof the owner of an apartmentin respect of electricity con-sumed thereon, is collectedand paid by the RWA to theutility, without charging anycommission or a considerationby any other name, the RWAis acting as a pure agent andhence exclusion from the valueof taxable service would beavailable. However, in the caseof electricity bills issued in thename of RWA, in respect ofelectricity consumed for com-mon use of lifts, motor pumpsfor water supply, lights in com-mon area, etc., since there isno agent involved in thesetransactions, the exclusionfrom the value of taxable ser-vice would not be available.

If a RWA provides certain ser-

vices such as payment of elec-

tricity or water bill issued by

third person, in the name of its

members, acting as a 'pure

agent' of its members, is ex-

clusion from value of taxable

service available for the pur-

poses of exemptions provided

in Notification 33/2012-ST or

25/2012-ST ?

4 Is CENVAT credit available to

RWA for payment of service

tax?

RWA may avail cenvat credit

and use the same for payment

of service tax, in accordance

with the Cenvat Credit Rules.

[Circular No. 175/01/2014-ST Dated 10-01-2014]

2 2

Bizsol UPDATE February - 2014

Public Notices

• The Standard Input Output Norms (SION) for

export product under Sr.No. A-1730, has been

modified as under:

Export Qty. Sr. Import Qty.

Product No. Product Allowed

Ambre- 1 kg 1 Trimethyl Orthoformate 0.1.724 kg

ttolide

2 Britol 1.020 kg

(Paraffinic Mineral Oil)

3 Glycerine 3.053 Kg

4 Seedlac 12.757 Kg

[Public Notice No. 45 (RE: 2013)/2009-2014

dated 06/01/2014]

• Now manufacturer exporter or other exports

exporting through third party may be also able

to claim the benefits under EDI systems provided

third party exporter do not claim such benefits.

9.14 For claiming benefits under EDI system in

respect of Third Party exports the process will

be initiated by the First party who will link shipping

bills and BRCs to repository. If the First Party

chooses not to claim benefit for a particular

shipping bill item/s, it may authorize Third Party

to claim benefit for such shipping bill item/s. After

such authorization by First party, Third Party will

be able to utilize the shipping bill item/s in its

application".

Guidelines for adopting currencies for claiming

such benefits have been notified.

9.15 (a) Currencies, where Exchange rates are

notified by CBEC

The foreign exchange realized (as mentioned by

bank in the EBRC) is converted to Indian Rupee

(INR) using the monthly exchange rates

published by CBEC.

(b) Currencies, where Exchange rates are not

notified by CBEC

In such cases, total realized value in INR (as

mentioned by bank in the EBRC), will be

converted into US$ by using the US$ /INR

exchange rate prevailing on the date of

realization as published by CBEC."

[Public Notice No. 46 (RE: 2013)/2009-2014

dated 08/01/2014]

• Procedure for processing of claims in respect of

realization of export proceeds through insurance

agency is being introduced. After para 2.25.2 of

HBP (Vol. I) two new sub para 2.25.2 (a) & (b)

are being added.

"2.25.2 (a) An applicant realizing export proceeds

through Insurance Agency will approach the

concerned RA with the proof of payment issued

by the concerned Insurance Agency. RA after

satisfying itself of the bona fide of the claim will

obtain approval of Additional DGFT (EDI) and

then will upload the value (in lieu of EBRC value)

in EDI system of DGFT for processing of the case.

"2.25.2 (b) If the proof of payment issued by the

Insurance Agency mentions claim value both in

foreign exchange and INR, RA will use the foreign

exchange value for processing. If the claim value

is mentioned only in equivalent INR, RA will

convert this INR value in equivalent US$ using

the exchange rate (published by CBEC)

applicable on the date of settlement of insurance

claim"

[Public Notice No. 47 (RE: 2013)/2009-2014

dated 08/01/2014]

• Installation of capital goods under EPCG scheme

is required in six months however it can be

extended maximum upto 18 months from the

date of completion of imports by regional

authorities. This clarification will avoid lot of

difficulties faced by the exporters and importers

.[Public Notice No. 48 (RE: 2013)/2009-2014

dated 10/01/2014]

• Nine new Pre Shipment Inspection Agencies

(PSIA) have been notified in following Areas:

Malaysia, UAE, Singapore, Tanzania, Mexico,

Namibia, Thailand, Gabon, Congo, Latvija,

Australia, Lebanon, Saudi Arabia, Jordan,

Bahrain, Angola, Vietnam & Thailand as one

territory, Russia, South America with Brazil as

head office. [Public Notice No. 49 (RE: 2013)/

2009-2014 dated 31/01/2014]

Policy Circulars

• The list of the countries from which the list of

International accredited agencies for issuance

of type Approval Certificate / COP as notified by

2 3

Bizsol UPDATE February - 2014

United Nations Economic and Social Council has

been notified. [Policy Circular No. 12 (RE-

2013)/2009-14 dated 15/01/2014]

INCOME TAX

Notification• Central Government has specified the officer of

the rank of Secretary who is responsible for

implementation of National Food Security Act,

2013 on behalf of respective government.

[Notification 1/2014 dated 6th Jan 2014]

• Government of Republic of India & the Council

of Ministers of Republic Albenia has entered into

Avoidance of Double Taxation and respective

Articles for DTAA have been issued.

[Notification 2/2014 dated 7th Jan 2014]

• The Government of the Republic of India and

the Government of Belize has entered into

agreement to facilitate the exchange of

information with respect to taxes. [Notification

3/2014 dated 7th Jan 2014]

• Central government has notified Orissa State

AIDS Control Society, a body constituted by the

Government of Orissa for the income arising to

that society namely "amount received in the form

of grants-in-aid from the Central Government"

for claiming exemption u/s 10(46) of Income Tax

act, 1961. [Notification 4/2014 dated 10th Jan

2014]

• Government has notified Contributory Health

Service Scheme of the Department of Space for

the purposes of claiming deduction under section

80D of Income Tax Act, 1962. [Notification 6/

2014 dated 15th Jan 2014]

• For the purpose of taxation of FII from securities

or CG arising from their transfer (Sec 155 AD),

government has specified Foreign Portfolio

Investors registered under SEBI Regulations,

2014 as FII. [Notification 9/2014 dated 22nd

Jan 2014]

Circular

• Clarification has been issued for non deduction

of TDS on the service tax component in case

the service tax has been separately charged.

[Circular 1/2014 dated 13th Jan 2014]

• Now Department has realised the need to issue

explanatory notes to the provision of the Finance

Act, 2013 subsequent to enactment of the Act.

[Circular 3/2014 dated 24th Jan 2014]

Maharashtra VAT

Notification1. Determination of sales price and purchase price

in respect of sale of transfer of property in India

involved in the execution of works contract under

Rule 58 of MVAT Rules 2005 has been modified

to the extent of note inserted with effect from

20.06.2006 when separate accounts are not

maintained. Now cost of the land also to be

deducted from the total quantum of contract value

so as to arrive amount to be deducted as

specified in the table. However onus of proving

the value of land so deducted will be on assessee

subject to providing that value of land is higher

as per authorities including Town Planning, Ready

Reckoner rate adopted for payment of stamp

duty. And if land cost so deducted is lower than

that of such rates refund application can be

made.

2. If such value cannot be determined or assessee

choses the option not to determine than while

determination of value of works contract for the

purpose of VAT valuation should be done in

accordance with the following table and

accordingly rule 1(B)(a) has been inserted.

S No. Stage during which the developer enters Amount to be

into a contract with purchaser deducted as

value of goods

involved in WC

1 Before issue of commencement certificate 100%

2 From commencement certificate to

completion of plinth level 95%

3 After completion of plinth level to

completion of 100% RCC framework 85%

4 After completion of 100% RCC frame

work to Occupancy Certificate 55%

5 After the Occupancy Certificate NIL

[Vat Notification 1513/CR-147/Taxation dated

29th Jan 2014]

2 4

Bizsol UPDATE February - 2014

Trade Circulars

• Date of submission of VAT audit report in form

704 has been extended with respect to

imposition of penalty for dealers opting for

composition scheme if filed within one month from

the due date i.e. on or before 15th Feb 2014.

[Trade Circular 2T dated 7th Jan 2014]

• Special Amnesty Scheme 2013 declared by the

Department of Industries. Amnesty scheme is

made applicable for the units not in operation

and not able to rehabilitation only. Such units

should fulfil the conditions under earlier state

government package scheme and now obtains

such certificate for their eligibility under the

scheme from Ministry of Industry. The scheme

will be valid up to 31.03.2014. Amnesty Scheme

exempts interest and penalty provided pending

dues is paid in one instalment only. Such units

needs to make in application in prescribed form

to Assistant Commissioner VAT or Jt

Commissioner (Recovery) Mazgaon as the case

may be along with following documents

1. Eligibility Certificate as mentioned above

2. Challan of payment of such type of dues

3. Withdrawal of appeal if any from competent

authority

4. Declaration by the transferor if any

5. Acceptance of transferee for the dues of

future along with interest and penalty

No application can be processed of which

payment has not been made on or before

31.03.2014. And after submission of application

and verification of same no due certificate to be

obtained. [Trade Circular 3T dated 24-01-2014]

• Registered Dealers will be relieved from the pains

of obtaining C forms since online procedure has

been introduced. The new procedure prescribed

will substantially reduce human interference and

eligible cases shall receive electronic forms on

email, detailed trade circular is as follows.

1. Procedure to be followed by the applicants:

a. Digital CST declarations in non-editable

PDF Format shall be issued in case of all

the applications made on or after 01 Feb

2014, The procedure for filling on-line

application i.e. Statement of Requirement,

has been revised and shall come in to force

from 1 February 2014.

b. The requisite utility for the said purpose has

been made available on the sales tax

Department's website www.mahavat.gov.in

c. The new proposed SOR is slightly changed

over the existing SOR so as to contain the

invoice vise purchase annexure. Three

separate Annexure(s) have been prescribed

for each of the forms / Declarations viz,

i. Declarations/certificates in both Form

C and F,

ii. Certificates in Form H.

iii. Declarations/certificates in Form E-I

and E-II

d. Before making an application for the CST

declarations the applicant shall ensure that

the turnover of interstate transactions for

which the application is being made is within

the limits of the turnover of interstate

transactions shown by him in the return

covering the period of transactions. If the

turnover of interstate transactions shown in

the return is less than the turnover of

interstate transactions mentioned in the

SORs filed by the dealer then the applicant

shall file the revised return, admit the

additional turnover and then apply for the

CST declarations.

e. The applicant dealer shall neither be

required to upload any document as an

attachment nor submit any physical

documents in respect of the SOR.

f. The applicants with six monthly periodicity

are presently unable to make quarterly

applications for the CST declarations. Such

applicants, at the beginning of the year, have

an option of changing their periodicity to the

quarterly and apply for the CST declarations