course 1 lesson 3 - philippine real estate

TRANSCRIPT

WHY INVEST IN PHILIPPINE

REAL ESTATE

“The Philippine real estate sector is back, the best since the Ramos administration. Due to strong demand, developers continue to churn out new office, retail, hotel and residential projects. The Philippines is benefiting from the Aquino administration’s good infrastructure, good governance leadership stance.”

Rick M. Santos CBRE Philippines

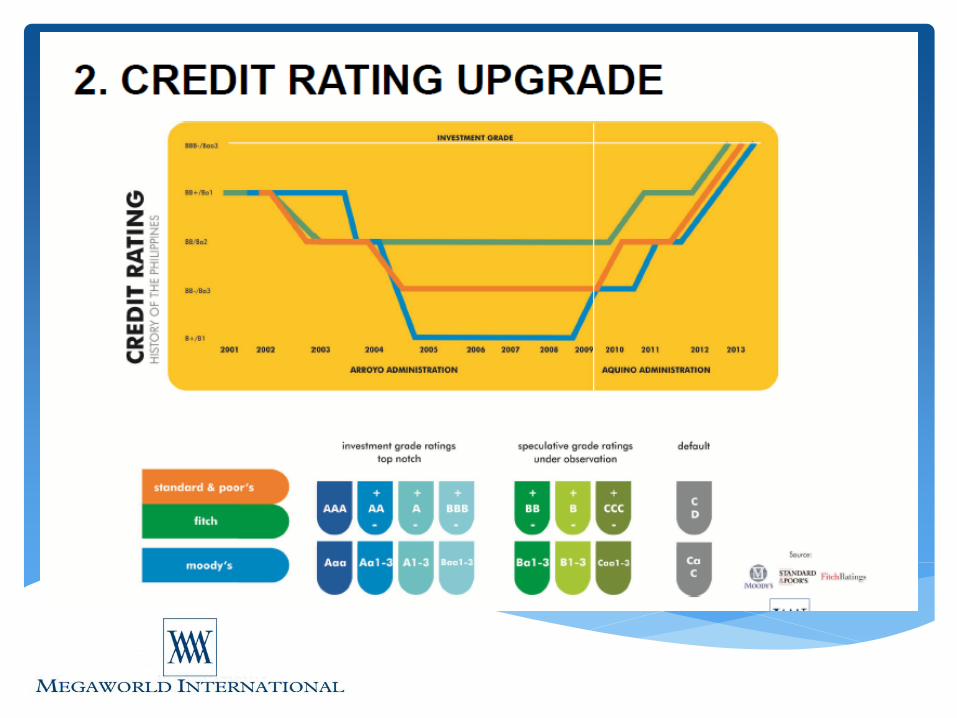

“The investment grade rating is a great news particularly for the property market and especially since there have been a lot of foreign investors looking into the market. This tells foreign investors it’s about time to invest in the Philippines.“

Colliers International

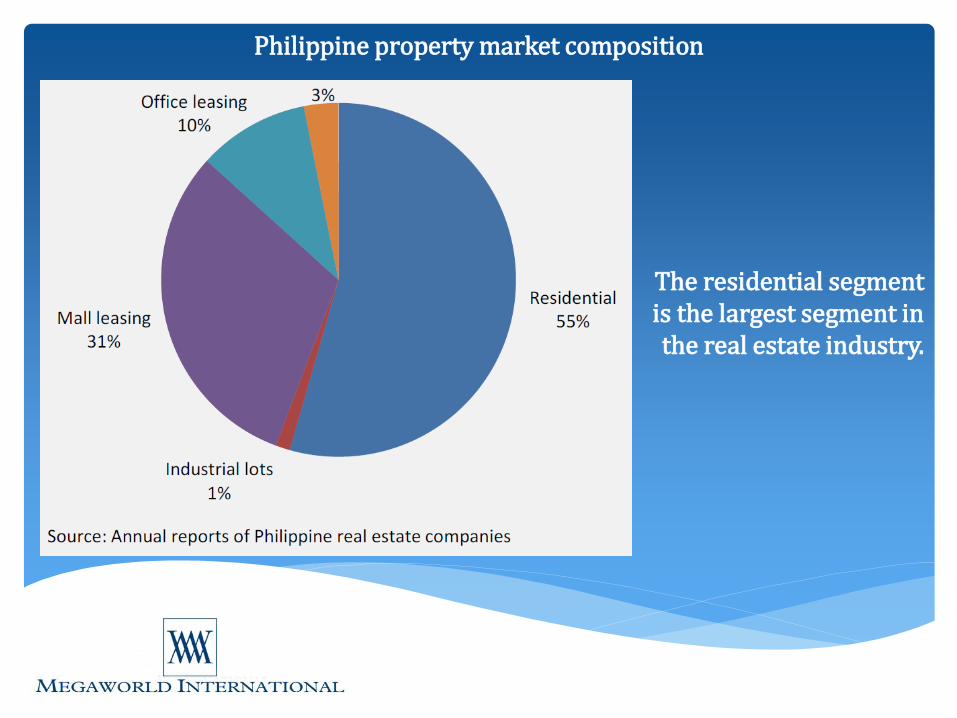

The Philippine real estate market comprises five main segments: 1. residential (e.g., condominium units, and house and lots), 2. office spaces, 3. shopping malls, 4. hotels, and 5. industrial lots. The residential segment accounts for the biggest share of total revenues at around 55 percent (equivalent to 6.4 percent of GDP).

Overview of the Philippine Real Estate Market

Philippine property market composition

The residential segment is the largest segment in the real estate industry.

• Real estate development has expanded geographically. Private building construction has become more dispersed with the development of new projects outside Metro Manila such as the provinces of Cavite and Laguna, and Metro Cebu and Metro Davao.

• The concentration of construction activity in Metro Manila has gone down to 40% from almost 80% in pre-1997 and 60% prior to 2009.

• The surge in construction and real estate activities reflects higher demand for office spaces, residential condominiums, and house and lots.

• Moreover, 2012 growth benefited from low base effect, because between 2009 and 2011, real estate companies put on hold major development projects in light of the volatile growth outlook brought about by the European fiscal crisis and slowdown in other advanced economies.

Why is Philippines so compelling?

Highly Attractive Investment

Property Comparison of Southeast Asian Market

(Singapore, Malaysia, Philippines, Vietnam, Thailand & Indonesia)

• Heightened exposure • Affordability • Accessibility • Liberal to foreign ownership • Easy access to financing • Easy to buy (Low quantum) • Freehold lease • Sales Contract in English • No Capital gain tax before turnover • Good Gov’t administrative • Government transparency and re- inventing • Growing population • Communication (Language, English) • Rental (Daily, Monthly or Service Apt) • Casino’s (Solaire, Belle Grande, Melco Crown, Resorts

World) • Tourism ( Leisure and Medical) • No Aging Issues • Exit strategy (can sub-sale anytime), Investment grade

economy

Philippines

• Exposure to strong commodity price • Macroeconomic stability • Relatively open investment • Generally low cost structure • Underspending on capital investment • Investment incentives • High mortgage interest rates • Foreign ownership restrictions • High costs of building materials • High tax rates • Red tape in government

Indonesia

Thailand

• Constitutional Monarchy • Well developed infrastructure • Efficient modern telecommunications and

internet system • Corporate income tax reduction • Gears up Infrastructure spending • Manufacturing and export hub • Low unemployment • Income Taxes are high • Subsale • Complicated buying process

• Political stability • High inflation • Tight liquidity • Tough regulation requirement • State- owned enterprising • Poor infrastructure • Dynamic market- based economic • Tourist destination • Tax, duty and rental incentives to investment • Economic technical zone • Restrictions on non-resident foreigners buying property • High flat rental income tax • Economic Mismanagement • Condominium market outlook remains bleak

Vietnam

• Affordability • Accessibility • Liberal to foreign ownership • Tighten financing • Easy to buy (Low quantum) • Government re- inventing • Sales Contract in English • Rebate scheme (Inflate sales price) • Foreign ownership • Foreigners can not buy low and medium cost

properties determined by the State Authority • Rental market practice is pro-tenant • Subsale • Upgrading infrastructure

Malaysia

Singapore

• High Property prices • Cooling Measures (ABSD, SSD, LTV, TDxx) • Growing population • High Cost living (retirement) • Rental yields continue low • Rental Income Tax is high

More then 1 billion people are within a 4-hour radius, which include the countries like: • China • Macau • Taiwan • Hong Kong • Brunei • Thailand • Singapore • Japan • Malaysia • South Korea

Location in Asia

REASONS TO CONSIDER ON INVESTING IN PHILIPPINE REAL ESTATE:

1. Positive Economic Growth 2. Credit Rating Upgrade 3. Consistent Increase of Capital Values 4. Attractive Rental Yields 5. Affordable and less expensive compared to other countries;

and greater yields compared to other investments 6. BEST climate for LIVE-WORK-PLAY 7. Cash flow and income generating investment. Real estate

investment: a pride of ownership 8. Growing BPO employment and expanding expatriate

community as your rental market

3. Consistent increase in capital values • It is almost automatic that real estate properties tend to

appreciate over time.

• The price of the property today will be different from the price next year.

• Many people choose to invest in pre-selling properties as they are aware that the price will have doubled at the time the project is completed.

• Philippine capital values (secondary market) on Metro Manila posted an average annual growth rate of 13%. (2005-2010)

• Capital values of Pre selling Megaworld projects exceeded the average annual growth rate of 13%. (2005- 2010)

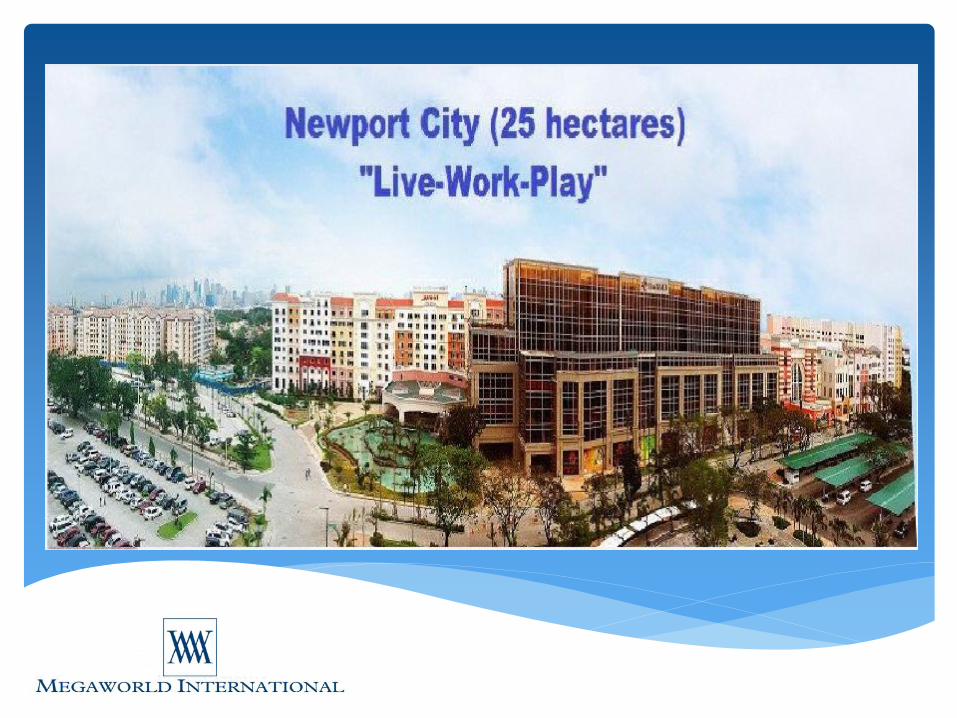

• Newport City – The tourist oriented, township community across the NAIA terminal 3 Airport in Pasay posted an annual average growth of 18% from its pre launched price in 2005.

Source: company information

MARKET VALUE: • Bonifacio Global City recorded the highest maximum capital value

appreciation since 2009 at 111%. While average capital value appreciation was at 38%.

• Makati followed with a maximum capital value appreciation of 109%. The average was at 33%.

• Slowest gain was seen in Quezon City with capital value gaining 36% at maximum, against the average of capital value appreciation of 9%.

Location Averagecondo

pricepersquare

meter in PHP

Annual

Average

growthrate

(2005-2010)

Makati 125,000-145,000 14%

OrtigasCBD 55,000-105,000 9%

Taguig/Global

City

115,000-130,000 18%

QuezonCity/

Eastwood

110,000-130,000 10%

AVERAGE CONDOMINIUM PRICES IN METRO MANILA

4. Attractive Rental Yields

Despite the continuous developments around the traditional CBDs, primarily Makati and BGC, will continue to have the highest rents and capital values due to the maturity of their developments and the availability of top quality real estate facilities.

GREATER YIELDS OF MEGAWORLD PROJECTS

Rates based on fully furnished Studio unit

Source: Company information

Square

Meters

Average

Rental

rateinUS

Dollars

Average

Rental

Ratein

Pesos

Average

cost

to buy

In US

Dollars

Average

cost

in Phil. Peso

Yield

PA as

unit

bought

in cash

30sqm 539 P23,400 73,410 P3,183,289 8.82%

50sqm 810 P35,100 116,150 P5,036,630 8.36%

70sqm 1,308 P56,700 159,880 P6,932,900. 9.81%

120sqm 1,836 P79,600 288,840 P12,525,012 7.63%

250sqm 3,820 P165,647 500,000 P21,681,576 9.17%

5. Affordable and less expensive compared to other countries and greater yields compared to other investments

Business confidence improved in the Philippines, as more investors are attracted to invest on real estate because:

(a) Properties are more affordable compared to other countries;

(b) A strong demand in the residential market can work for every investor; and

(c) these investments can earn through capital appreciation and rental income.

6. Best climate for

“LIVE-WORK-PLAY”

The Philippines continues to enjoy a warm sunny climate that is perfect for any type of activity: LEISURE, RECREATION, TRAVELLING, and even RETIRING.

Anchored by the robust tourist arrivals, it really proves that the Philippines is still one of the best tourist destinations. Among the top destinations are Manila, Cebu, and Boracay.

Entertainment City- Philippines’ Grandest Tourism,

Entertainment, Shopping and Business Center Development

4 Hotel Casino Resort Complexes 6 IT Center Buildings and more in the pipeline SM Mall of Asia- 10th Largest Mall in the world More than 10 luxury and business hotels

Developments in Entertainment City will create more than 1.8 million jobs when fully developed- estimated

250,000 are expats.

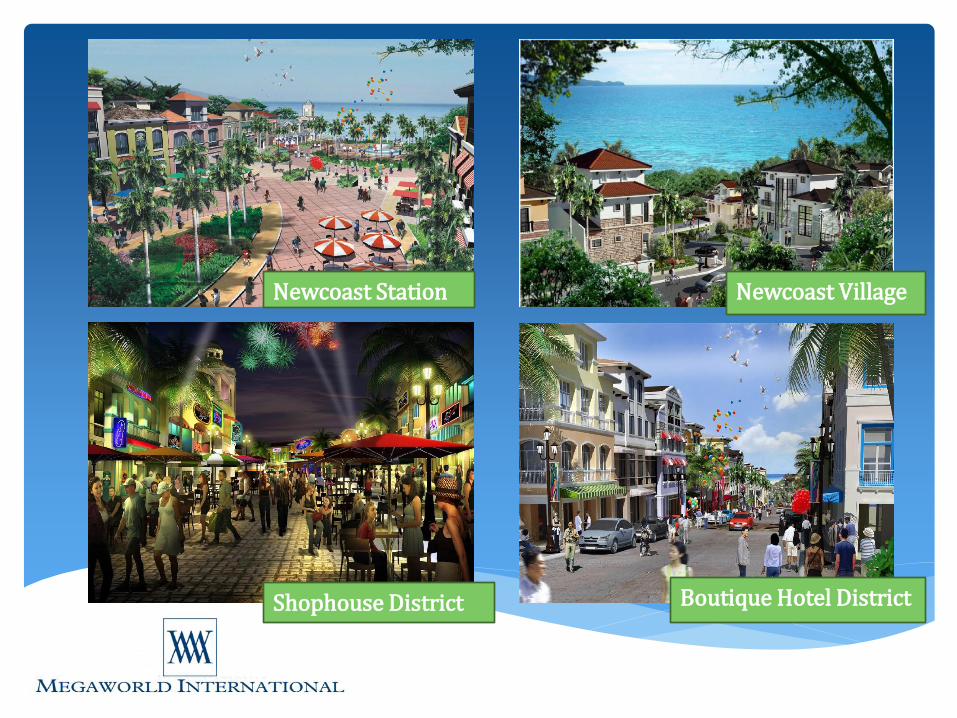

BORACAY NEWCOAST

The first and only master planned, tourism oriented community spanning 14% of the island, the single biggest development of its kind in Boracay offers over 1,000 international grade rooms managed by distinct and reputable world class hotel operators

Features a fresh and vibrant leisure atmosphere complete with boutique, hotels, ocean, villas, health and wellness centers and dining and shopping districts

Boasts an 18-hole Graham Marsh par71, 6,600 yard championship golf course complete with golf club, spa center and nature farm

Newcoast Station

Shophouse District

Newcoast Village

Boutique Hotel District

TWIN LAKES

• Located in Tagaytay and Laurel, encompasses 1,149 hectares designed to be the premiere medical and educational tourism estate

• Provides refreshing views of famous Taal lake & Volcano

• Offers a cool mountain breeze amid rugged terrain and a man made lake

TWIN LAKES

• Features a chateau and vineyard surrounded by palm trees and botanical gardens

• Initial phase – Twin lakes hotel and spa, shopping and dining areas, residential condominium and modern sports amenities

• Succeeding phases – plantation estate, golf course community, lake view manor, mountain inspired lodging and facilities, health & wellness centers, and a vibrant retirement village

TWIN LAKES : AN INTEGRATED TOURISM ESTATE

COMPLETE URBAN LIVING WITH MEGAWORLD‘S TOWNSHIP PROJECTS

7. Cash flow and income generating investment

REAL ESTATE: A BASIC NEED THAT NEVER ENDS

• Rental income

• Property selling

• Capital appreciation

• Control

REAL ESTATE: A Rewarding investment

Legacy: Passed on to generations

Testament of hardwork

and success

Sense of pride and

ownership

8. Growing BPO employment and expanding expatriate community as your rental market

The Demand for Residential Condominium in the Philippines

• Business Process Outsourcing revenue in 2012 reached $13.6 billion expected to increase by $2.6 billion by 2013

Became the first IT Park to be designated PEZA special economic zone in 1999, and built more than 200,000 sqm of BPO office space.