country report - markables · country report . february 17th, 2016 . ... castrol, doc martens,...

TRANSCRIPT

BRAND BRITAIN – British brands in M&A

1 7

Trademark Comparables AG Bahnhofstrasse 48 CH-6430 Schwyz Switzerland

+41 (41) 810 28 83 [email protected]

The Leading Source for Trademark

Values

Country Report

February 17th, 2016

BRAND BRITAIN – WHERE WILL THE JOURNEY LEAD? An analysis of British brands in M&A from 2005-2014

When it comes to brands and branding, the United Kingdom has always been one of

the most influential countries in the world. Modern advertising based on targeted slogans and images was invented in London. London has always been an inspiring place for new ideas, creations and trends. The prosperity of the British facilitated the diffusion of innovations, delicacies, luxury things and gadgets. A perfect hotbed for branding and brands. Many British companies successfully spread their brands over the British Empire, the Commonwealth and the whole world. Many British brands have become global icons, such as Burberry, Johnnie Walker, Jaguar, Virgin, After Eight, Church’s, Schweppes, Marks & Spencer, Castrol, Doc Martens, Benson & Hedges, Harry Potter, the Spice Girls (and the Beatles and the Rolling Stones), James Bond, Mister Bean, and many many more. In addition, London has always been one of the leading financial centers, attracting investors from all over the globe. In the late 80ies, the financial valuation of brands was developed in London. It is no surprise that many of the heavyweights on London Stock Exchange are strongly branded global businesses, including GSK, Unilever, Vodafone, BAT, SABMiller, Diageo, Reckitt Benckiser, Imperial Tobacco, Carnival, and WPP, not to mention banks and financial services. In contrast, hi-tech or materials businesses play a less important role in the British economy.

Is it therefore right to characterize the United Kingdom as a brand minded nation and

a brand driven economy? In this report we will have a look at brands and branding in the United Kingdom from a new perspective: that of investors who acquire branded businesses. The analysis is based on the MARKABLES database which lists over 8,200 M&A transactions worldwide and the values attributed to their various assets, including – among others – their brands. MARKABLES lists 617 acquired businesses and their brands located in the UK, and 467 businesses acquired by British compa-

BRAND BRITAIN – British brands in M&A

2 7

Trademark Comparables AG Bahnhofstrasse 48 CH-6430 Schwyz Switzerland

+41 (41) 810 28 83 [email protected]

nies abroad.1

An in-depth analysis of these cases provides evidence for a decreasing significance of British brands and may etch some worry lines about their future.

How important are brands to M&A investors in the UK? To understand that, we have

a look at the proportion attributed to brands in acquisitions in the UK, and how this proportion developed during the last ten years (exhibit 1). Ten years ago, brands were the single most important asset class in takeovers in the UK, which confirms our above opinion. However, some dark clouds are gathering. The trend line during the last ten years indicates a significant decrease for brands. While the proportion at-tributed to brands was 25% of enterprise value in 2005, this figure decreased to only 13% in 2014. The downside trend is the same for both British and foreign acquirers, albeit at different levels. It is worth to note that the interest of foreign investors in Brit-ish brands is only half of the interest of domestic investors.

What are the reasons for this decline? One of the root causes is that during the same

period the value of customer relations increased from 12% to 24%, thus taking over the role of brands in acquisitions (exhibit 2).2

Well, one might say that customer rela-tions and brands are interrelated and both belong to marketing, thus paying into the same account. But this would be oversimplified and only half true.

Bolstered by the digital age and CRM, businesses shifted their marketing strategies

much more towards direct relations and interactions with their customers, away from traditional mass media. In B2B marketing, knowing the names and purchase histories

1 MARKABLES is the largest and most comprehensive database for purchase price allocations report-

ed in financial statements of listed companies according to IFRS 3/IAS 38. However, the records listed in MARKABLES represent only a certain part of all PPAs. Acquisitions made by unlisted com-panies remain undisclosed. For some M&A done by listed companies are reported, the PPAs are re-ported but not in sufficient detail. And MARKABLES may have missed out a few of the reported PPAs.

2 As a result of the financial crisis, abnormal distortions are visible in the year 2009. Brands play literally no role in 2009 acquisitions.

BRAND BRITAIN – British brands in M&A

3 7

Trademark Comparables AG Bahnhofstrasse 48 CH-6430 Schwyz Switzerland

+41 (41) 810 28 83 [email protected]

of individual customers and directing individual, personalized marketing messages to them has been normal since long. It is however rather new in B2C and goes far be-yond traditional direct marketing. Digitalization changed the lives of both marketers and consumers. Digital has changed the media landscape, allocation of marketing budgets, campaign creation and content, media planning, performance monitoring and the way how marketing and brand management functions are organized. Market-ing will soon overtake IT in IT-related spending. Today, most businesses have a much larger customer database than ten years ago – both in numbers and in quality. On the consumer’s side, people suffer message overflow, spend more time online, read much less printed media, and are less attentive to TV advertising. Consumers became used to decide themselves when and how to take information on brands. With a multitude of different information about brands available, they also became more selective in what they accept as a brand message. And more critical. Com-pared to ten years ago, only few stones in marketing and brand management are left unturned.

The individualization of marketing has also changed the appreciation of branding and

brands. As a reminder – branding once was not only an effective, but also the only way to reach out to anonymous customers. It was vital for recognition that the brand identity remained stable over time. Today, many more customers are known in per-son and can be reached directly, with higher impact and at lower cost. Brand images and messages alter flexibly and fast. Of course, traditional branding is still needed to attract new customers and to communicate new products, but it lost its dominance. Today, there are two major market-related intangible assets: brands (with the proper-ty rights to use the registered brand exclusively) and customer relations (with the customer database and the related access to clients and their purchase pattern). The important thing to understand for marketers is that both assets have a stand-alone value, need to be protected separately, and are appreciated by investors separately.

Similarly for M&A investors, the focus has shifted from brands to customer relations during the last ten years. They now pay more for customer relations than they pay for brands, for a simple reason - their superior potential to create additional value from the combination of two businesses. Once the customer is known in person, it is easy to sell additional products to him (up selling or cross selling). In contrast, the creation of additional value from brands is far more difficult. Price increases (at lower vol-umes), market share gains (at lower prices), or internationalization (particularly diffi-cult for most consumer brands to launch in new territories) are all hard to achieve. Moreover, it is easier to realize cost savings from the integration of a customer ori-ented organization than from the integration of a strong brand. As a result, corporate investors effectively spend significantly less to acquire brands than they did ten years ago. It has become a reality that they no longer acquire businesses for their brands but for their true direct customer relations.

Simply put, brand value is the result of two major elements. One is the extra profit

margin that can be attributed to the brand (brand-related price premium minus brand expenses). The other is the length of time into the future during which the brand is expected to generate such extra margins. Not surprisingly, both elements show a decline during the last ten years (exhibit 3). Average brand margins (expressed as implied royalty rates) decline from 5% to 3.5%. The average length of time (ex-pressed as remaining useful life) declines from 34 to 20 years.3

3 Where remaining useful lives were in(de)finite, we have set a period of 50 years. Due to the discount-

ing effect in DCF calculations, contributions from years beyond 50 to present value become negligible.

BRAND BRITAIN – British brands in M&A

4 7

Trademark Comparables AG Bahnhofstrasse 48 CH-6430 Schwyz Switzerland

+41 (41) 810 28 83 [email protected]

However, it would be simplistic to assume a general decline of brand value. There

are still many British brands out there that succeed in preserving or even increasing their value even in adverse times. But one thing remains an incontestable fact. M&A investors turned away from acquiring brand-centric businesses (exhibit 4). Brand-centric businesses are businesses where brand is the single most important asset. Generally, businesses can be dominated by physical assets (capacity or infrastruc-ture), synergy assets (cost savings or growth potential), brands, customer relations, or technology. Approximately one third of all businesses are hybrid types. Brand cen-tric businesses typically include food & beverage brands, retailers, OTC drugs, fash-ion brands, restaurants, among others. Although oscillating over time, the trend line is very visibly declining for brand-centric businesses and at the same time increasing for customer-centric businesses.4

Ap-parently is has become more difficult for British brand-centric businesses to attract acquirers – in particular if they have no digitalized, direct access to their customers. Instead, M&A investors now largely prefer to acquire customer-centric businesses. Overall, the future seems to look less rosy for British brands.

The gradual loss of importance of British brands can be seen from other observations

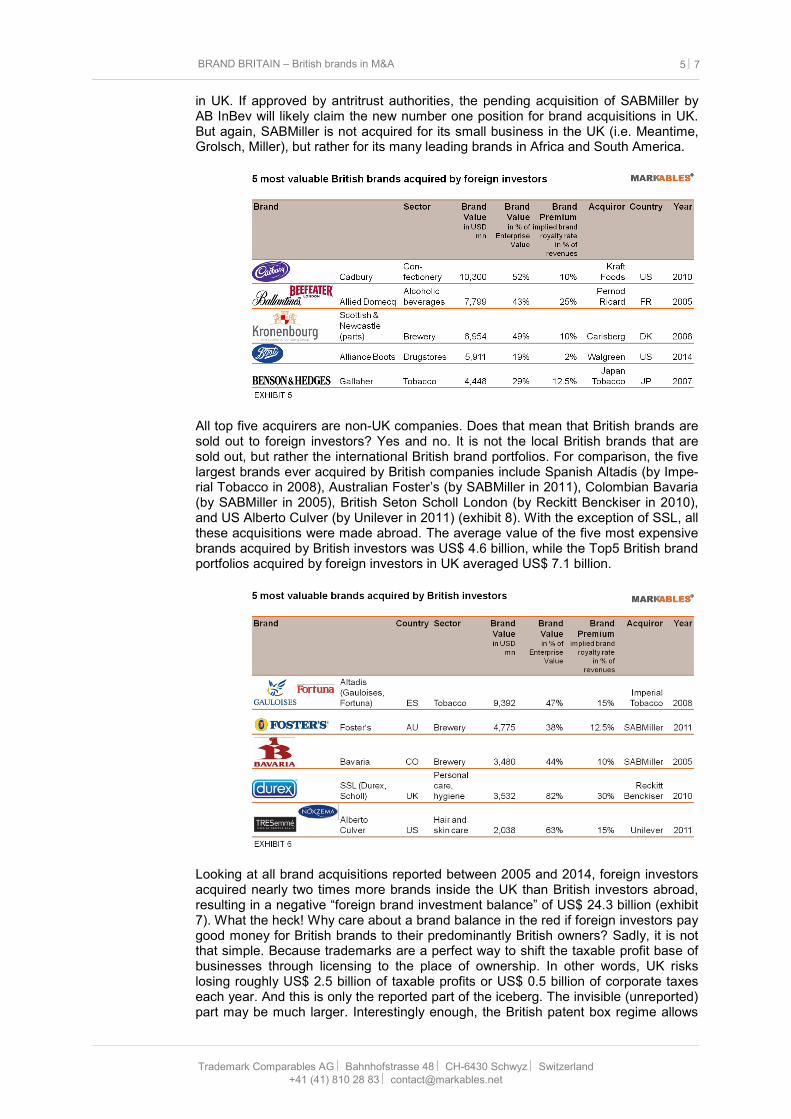

as well, for example from the foreign brand investment balance. The five most ex-pensive brands (or brand portfolios) ever acquired in the UK are Cadbury (in 2010 by Kraft), Allied Domecq (by Pernod Ricard in 2005), large parts of Scottish & Newcastle (by Carlsberg in 2008), Alliance Boots (by Walgreen in 2014), and Gallaher (by Ja-pan Tobacco in 2007) (exhibit 5). The rationale behind all of these acquisitions was a) their strong brands and b) their important international or global revenue base. One of these five acquisitions ranks among the global Top10 brands ever acquired, and four among the Top20, illustrating once more the strong significance of branding

4 Again, we observe abnormal distortions in 2008 and 2009, as a result of the financial crisis.

BRAND BRITAIN – British brands in M&A

5 7

Trademark Comparables AG Bahnhofstrasse 48 CH-6430 Schwyz Switzerland

+41 (41) 810 28 83 [email protected]

in UK. If approved by antritrust authorities, the pending acquisition of SABMiller by AB InBev will likely claim the new number one position for brand acquisitions in UK. But again, SABMiller is not acquired for its small business in the UK (i.e. Meantime, Grolsch, Miller), but rather for its many leading brands in Africa and South America.

All top five acquirers are non-UK companies. Does that mean that British brands are

sold out to foreign investors? Yes and no. It is not the local British brands that are sold out, but rather the international British brand portfolios. For comparison, the five largest brands ever acquired by British companies include Spanish Altadis (by Impe-rial Tobacco in 2008), Australian Foster’s (by SABMiller in 2011), Colombian Bavaria (by SABMiller in 2005), British Seton Scholl London (by Reckitt Benckiser in 2010), and US Alberto Culver (by Unilever in 2011) (exhibit 8). With the exception of SSL, all these acquisitions were made abroad. The average value of the five most expensive brands acquired by British investors was US$ 4.6 billion, while the Top5 British brand portfolios acquired by foreign investors in UK averaged US$ 7.1 billion.

Looking at all brand acquisitions reported between 2005 and 2014, foreign investors

acquired nearly two times more brands inside the UK than British investors abroad, resulting in a negative “foreign brand investment balance” of US$ 24.3 billion (exhibit 7). What the heck! Why care about a brand balance in the red if foreign investors pay good money for British brands to their predominantly British owners? Sadly, it is not that simple. Because trademarks are a perfect way to shift the taxable profit base of businesses through licensing to the place of ownership. In other words, UK risks losing roughly US$ 2.5 billion of taxable profits or US$ 0.5 billion of corporate taxes each year. And this is only the reported part of the iceberg. The invisible (unreported) part may be much larger. Interestingly enough, the British patent box regime allows

BRAND BRITAIN – British brands in M&A

6 7

Trademark Comparables AG Bahnhofstrasse 48 CH-6430 Schwyz Switzerland

+41 (41) 810 28 83 [email protected]

for reduced tax rates on income from technology (patents), but not from brands. For tax oriented brand investors, UK is not an attractive domicile.

The US$ 25 billion shortfall in brand value is fully attributable to the balance from the

ten largest inbound and outbound acquisitions. Going further down to smaller brand acquisitions, the account is balanced. Obviously, British branding heavyweights have reduced their corporate acquisitions, while foreign heavyweights acquire large British brands. But this interest of foreign investors is directed mostly to international brand portfolios rather than to national British brands.

The decreasing share of brand value in M&A as shown above is however not specific

to the UK. The harmful effects of digitalization on the long-term value of brands are similar all over the world.5

Another effect is however UK-specific: it has the strongest and most powerful retail sector worldwide. Nowhere in the world have big retailers been so aggressive and successful in establishing private or own labels than in the UK. This move of Tesco, Waitrose, Sainsbury, Marks & Spencer, Boots and the likes did not only increase their profitability through own brands, but also weakened the position and power of traditional wholesale brands. Instead of pursuing offensive marketing strategies, most of them stuck in a mature market between powerful retail-ers and the digitalization of consumer behavior.

Brand Britain needs to stand up, invest and – most importantly - innovate. Brand value alone does no longer create superior business value. Brand managers must therefore find new approaches to grow the value of their businesses. One approach is digital. Brand owners must intensify direct communication and sales with their end consumers, and reduce their dependence from sales intermediaries. Another ap-proach is technology and uniqueness. By incorporating (patentable or exclusive) technology into their products or services, brand owners create not only uniqueness and higher margins, but also valuable technological assets which a corporate inves-tor can potentially integrate into his own offering. Or alternatively go international with the Britishness factor. Britishness is an attribute which is attractive to consumers all over the world, in many different categories. The world loves Britishness in all of its different aspects – its conservatism, its style, and its craziness - provided that it is authentic. Brand Britain should adhere to and capitalize on Britishness, instead of divesting it to foreigners.

5 See here https://hbr.org/2015/04/why-strong-customer-relationships-trump-powerful-brands

BRAND BRITAIN – British brands in M&A

7 7

Trademark Comparables AG Bahnhofstrasse 48 CH-6430 Schwyz Switzerland

+41 (41) 810 28 83 [email protected]

Another country report on brand transactions in Australia is downloadable here

www.markables.net/files/CountryReport_Australia_20151112.pdf

Detailed data and background information about the most expensive brands acquired and other issues related to the valuation of brands is available here: https://www.markables.net/brand_valuation_savviness

About Trademark Comparables AG / MARKABLES

Trademark Comparables AG is a privately held, Swiss based company engaged in the valu-ation and capitalization of IP, notably brands and customer relations. Trademark Comparables AG develops valuation methods and provides input data for valuation algorithms to appraisers, accountants, auditors, tax advisers, brand owners, banks and investors all over the world. Trademark Comparables AG operates MARKABLES®, the leading and unique source for trademark values worldwide. MARKABLES® contains the results of over 8,200 reported and audited trademark valuations resulting from acquisitions and transactions. For more infor-mation regarding MARKABLES®, please visit www.markables.net